Market Overview

| Study Period | 2020 - 2031 |

|---|---|

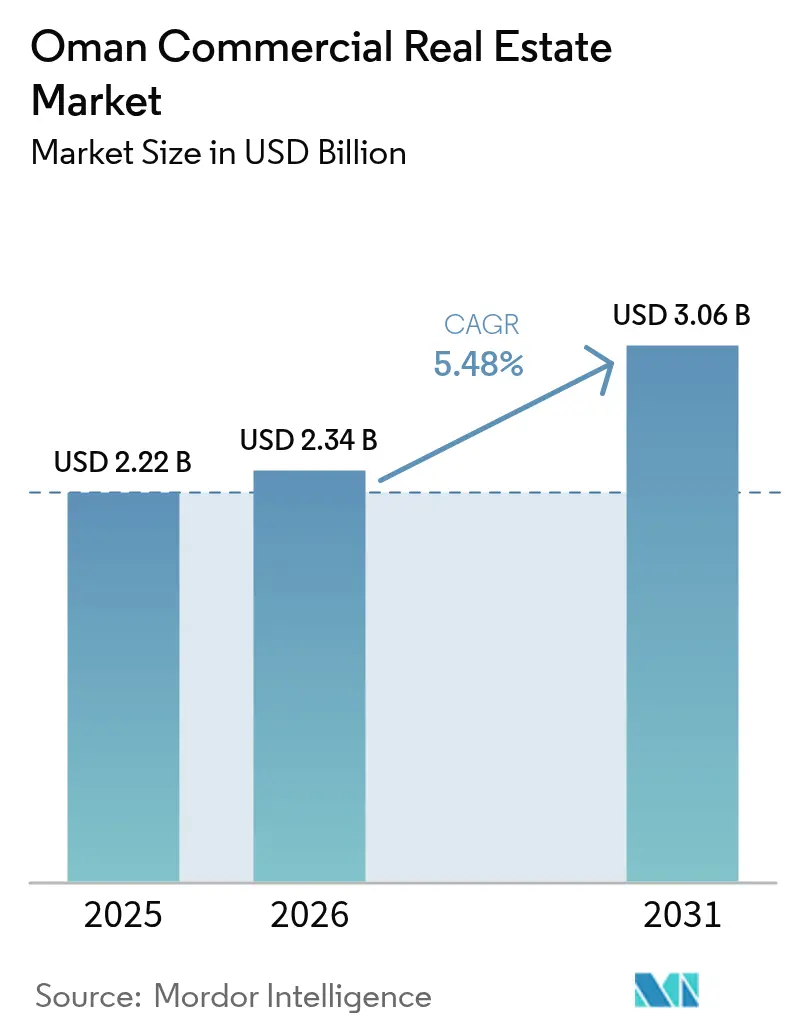

| Base Year Market Size (2025) | USD 2.22 Billion |

| Market Size (2026) | USD 2.34 Billion |

| Market Size (2031) | USD 3.06 Billion |

| Growth Rate (2026 - 2031) | 5.48% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oman Commercial Real Estate Market Analysis by Mordor Intelligence

The Oman Commercial Real Estate Market size was valued at USD 2.22 billion in 2025 and estimated to grow from USD 2.34 billion in 2026 to reach USD 3.06 billion by 2031, at a CAGR of 5.48% during the forecast period (2026-2031). Vision 2040’s diversification agenda, the USD 5.2 billion Future Fund, and the USD 15 billion National Railway network are positioning the Oman commercial real estate market as a pivotal enabler of logistics and tourism-led growth. Foreign direct investment (FDI) stock reached USD 69.3 billion by Q3 2024, a 17.6% increase over five years, with real estate listed among the top 20 opportunities on the Invest in Oman platform. Royal Decree 38/2025 now allows non-Omanis investors to acquire freehold property in designated zones, broadening the international investor pool. While office assets retained a 33.73% share in 2024, sustained port expansion and free-trade-zone incentives are propelling logistics assets, which are forecast to grow at a 7.80% CAGR through 2030.

Key Report Takeaways

- By property type, offices held 33.21% of the Oman commercial real estate market share in 2025, whereas logistics assets are advancing at a 7.45% CAGR through 2031.

- By business model, rentals commanded a 70.02% share of the Oman commercial real estate market size in 2025, while sales are projected to expand at a 6.47% CAGR to 2031.

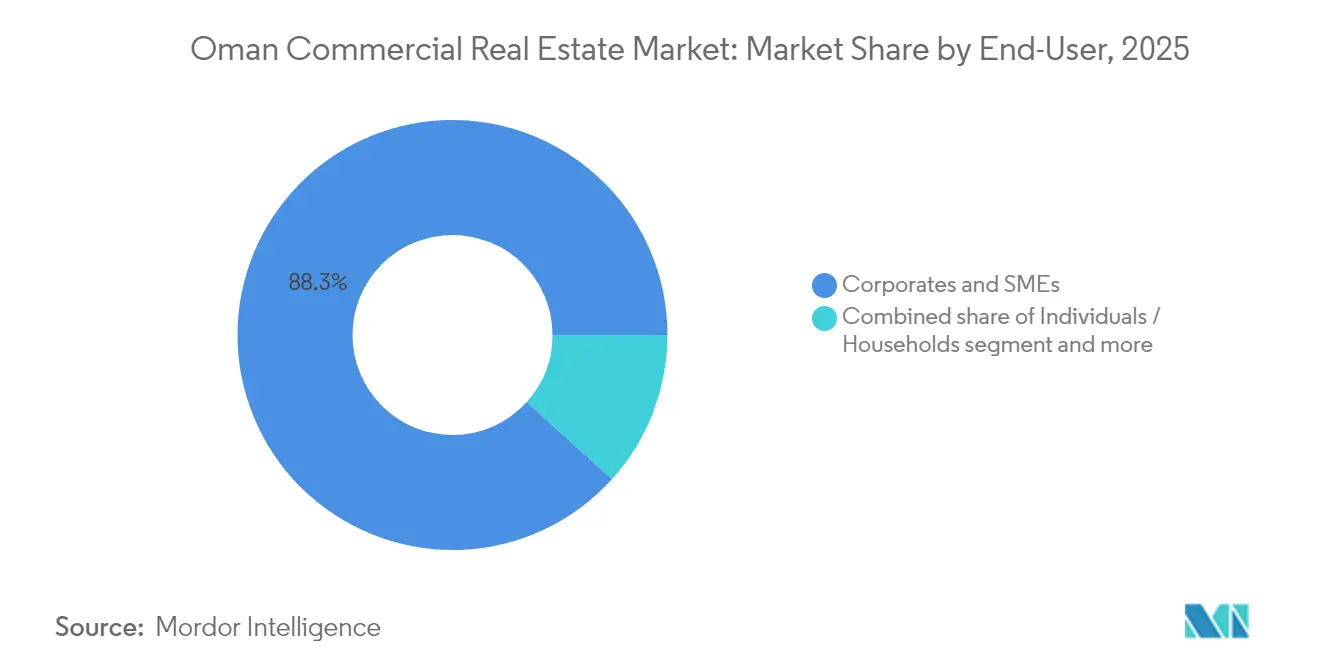

- By end-user, corporate and SME occupiers accounted for 88.31% of the Oman commercial real estate market size in 2025, whereas household participation is rising at a 7.12% CAGR through 2031.

- By geography, Muscat captured 69.25% of the Oman commercial real estate market share in 2025; regions outside Muscat are expected to grow at a 6.94% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Oman Commercial Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2040 infrastructure pipeline | +2.1% | Muscat, Duqm, Salalah, nationwide | Long term (≥ 4 years) |

| GCC & Asian FDI inflows into real assets | +1.8% | Duqm, Sohar SEZs, national coverage | Long term (≥ 4 years) |

| Rising working-age population and urbanization | +1.2% | Muscat, Sohar, national spillovers | Medium term (2-4 years) |

| Free-trade-zone logistics demand | +0.9% | Sohar, Duqm, Salalah port areas | Medium term (2-4 years) |

| Corporate ESG mandates and green offices | +0.6% | Primarily Muscat; expanding to regional centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Oman Vision-2040 Infrastructure Pipeline

Mega-projects such as Madinat Al Irfan (624 ha, target 280,000 residents and 90,000 jobs) and Yiti (11 million m² of integrated tourism space) demonstrate how the Vision 2040 pipeline is reshaping asset demand in every commercial segment. The USD 15 billion National Railway will connect Sohar to Muscat and the UAE border, catalyzing corridor-based warehouse clusters. Duqm SEZ, covering 2,000 km² with USD 14 billion commitments, is birthing entirely new sub-markets for hotels, offices, and industrial parks. These projects generate ripple effects, retail, healthcare, and education facilities follow workforce migration, and reinforce the Oman commercial real estate market as an essential diversification lever[1]Suhail Al Maawali, “National Railway Project Factsheet,” Ministry of Transport, motc.gov.om.

Steady Inflow of GCC & Asian FDI into Real Assets

Capital from Gulf and Asian investors is cascading into large-scale industrial, tourism, and logistics schemes, amplifying liquidity across the Oman commercial real estate market. Investcorp’s USD 500 million commitment to Duqm port and industrial infrastructure exemplifies this momentum. Sohar Port and Freezone has attracted USD 30 billion in cumulative investment with 85% land occupancy, including a USD 1.35 billion polysilicon plant, stimulating demand for adjacent warehouses and worker accommodation. Oman’s sustainable finance framework, the first in the GCC, offers labeled green bonds across 14 categories, pulling ESG-focused Asian capital toward LEED and BREEAM-certified assets. This financial diversification underpins stronger take-up of premium offices, hospitality, and logistics space that meets global investor benchmarks[2]Haitham Al Said, “OIA Launches USD 5.2 Billion Future Fund,” Oman Investment Authority Press Release, oia.gov.om.

Rising Working-Age Population and Urbanization

Oman’s expanding labor force is accelerating internal migration toward mixed-use corridors in Muscat, Sohar, and Salalah. The OMR 1 billion Sultan Haitham City scheme will accommodate 39,000 residents across 7,000 units by 2030, underpinning demand for office, retail, and community facilities. Parallel initiatives such as New City Salalah’s waterfront project for 60,000 residents and 200,000 m² of retail-hospitality space create secondary demand for logistics and service assets. Al Khuwair Downtown in Muscat, backed by USD 1.3 billion, targets population expansion from 1.5 million to 2.7 million by 2040, spurring Grade-A office absorption. Ministerial Decree 501/2024 is accelerating Omanization, driving corporate spending on training centers and compliant workspace. Collectively, these demographic shifts provide foundational support for the Oman commercial real estate market through 2030.

Corporate ESG Mandates Spurring Green-Certified Offices

Multinational tenants increasingly require LEED Silver or higher ratings, prompting developers to retrofit or build to global environmental standards. Omran Group’s Office Park in Madinat Al Irfan achieved LEED Gold pre-certification in 2024, inducing similar moves by private peers. International lenders offer interest rate discounts of up to 50 basis points for certified green stock under Oman’s sustainable finance program, lowering the weighted average cost of capital for compliant developers. Early adopters report rental premiums of 7%–10% for green buildings, improving asset value retention despite rising construction costs. Demand is expanding from Muscat CBD to emerging hubs like Sohar and Duqm, embedding sustainability as a competitive requirement across the Oman commercial real estate market[3]Aisha Al Rawahi et al., “Green Building Adoption in GCC Commercial Real Estate,” Journal of Sustainable Construction, jsusc.org.

Restraints Impact Analysis*

| Restraint | ( ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating construction material & labor costs | -0.8% | Muscat, Sohar, nationwide | Short term (≤ 2 years) |

| Threat of Grade-B office and retail oversupply | -0.6% | Muscat, emerging in Sohar | Medium term (2-4 years) |

| Restrictive bank lending to developers | -0.4% | Nationwide, hits smaller players | Short term (≤ 2 years) |

| Fragmented permitting & title registration | -0.3% | National, regional variations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Construction Material and Labor Costs

Global steel and cement price volatility is squeezing developer margins just as Omanization drives wage inflation. The Bandar Al Khairan resort’s OMR 36 million (USD 93 million) budget underscores cost pressures filtering into hospitality assets. Ministry of Labor restrictions on expatriate technical roles compel additional training and recruitment outlays, further elevating input costs. The AECOM Property & Construction Handbook 2025 cites Oman among GCC countries facing above-regional average escalation for rebar and ready-mix concrete. Project delays and scope revisions have become common, particularly for SMEs lacking balance-sheet resilience. Although green finance incentives provide marginal relief, short-term cost inflation remains a meaningful drag on the Oman commercial real estate market.

Growing Threat of Oversupply in Grade-B Offices/Retail

New stock continues to flow at a faster rate than tenant absorption, especially in secondary corridors where demand drivers are weaker. The Capital Market Incentives Program has sparked a surge of listings on the Muscat Stock Exchange, yet many newly listed entities maintain lean headcounts, limiting net office take-up. Retail vacancy risks have risen following the opening of City Centre Sohar (35,301 m², 120 stores), adding supply in a market already contending with e-commerce substitution. Oman Chamber of Commerce data reveal that one large retail franchise recorded a fivefold jump in operating losses during 2024 as footfall shifted online. Grade-B landlords face rising incentives and shorter lease terms, challenging income stability within the Oman commercial real estate market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Type: Logistics Leads Expansion

Logistics assets contributed the fastest incremental growth to the Oman commercial real estate market size, outpacing all other categories with a 7.45% CAGR outlook to 2031. Sohar Port’s 85% land occupancy, USD 30 billion cumulative investments, and new agro-bulk terminal illustrate robust warehouse absorption along the Batinah coastline. The Oman commercial real estate market share for offices remained highest at 33.21% in 2025, buoyed by government relocation programs to Madinat Al Irfan and the launch of corporate campuses in Duqm. Retail assets face a structural shift as mobile commerce scales; nonetheless, flagship centers like City Centre Muscat sustained annual footfall above 10.2 million, retaining prime-location appeal.

Tenant demand patterns are evolving toward sustainable specifications. Port-centric developers are integrating solar-ready roofs and LED lighting to meet shipping clients’ carbon mandates. Industrial assets in Duqm SEZ benefit from USD 14 billion in manufacturing commitments focused on energy-intensive sectors such as green hydrogen and petrochemicals. Hospitality pipelines remain active, evidenced by the USD 731.6 million Duqm tourism complex and the USD 100 million Club Med Musandam resort targeting BREEAM certification. Emerging sub-sectors include data centers, Oman Data Park’s USD 450 million initiative showcases rising demand for resilient power and fiber connectivity. Together, these forces are reshuffling capital toward future-proofed asset classes within the Oman commercial real estate market.

By Business Model: Rentals Retain Primacy, Sales Accelerate

Rentals controlled 70.02% of the Oman commercial real estate market share in 2025, reflecting corporate preference for operational flexibility in a diversifying economy. Lease volume surged following a 28.1% year-on-year rise in transaction values as of November 2024, propelled by new company formations under Vision 2040. Simultaneously, sales transactions are charting a 6.47% CAGR through 2031, energized by freehold permissions in SEZs and 10-year tax holidays introduced by Royal Decree 38/2025. The Oman commercial real estate market size tied to expatriate buyers continues to expand, with Indians, British, and Emiratis collectively accounting for more than 57% of Integrated Tourism Complex purchases.

Luxury leasing in enclaves such as Shatti Al Qurum and Muscat Hills maintains yields above 7%, supported by zero property tax and the new mortgage-friendly Banking Law that enhances consumer protection. Capital Market Incentives streamline conversion to joint-stock status, unlocking preferential financing for corporates seeking to own operational premises. Robust banking sector profits, totaling OMR 522.6 million in 2024, signal sustained credit support for owner-occupied developments. These factors collectively underpin a dual-track trajectory where rentals dominate cash flow stability while sales unlock capital appreciation in the Oman commercial real estate market.

By End-User: Corporate Mainstay, Household Upswing

Corporate and SME tenants generated 88.31% of the Oman commercial real estate market size in 2025, underwritten by the USD 5.2 billion Future Fund and escalating private-sector job creation mandates. Blue-chip occupiers gravitate toward Grade-A stock; Omran Group reported a 94% Omanization rate and OMR 25.2 million net profit in 2024, signaling robust demand for premium premises. The Oman commercial real estate market is witnessing a fresh wave of corporate expansion into green buildings, targeting utility cost savings and ESG compliance.

Household participation, although smaller, is expanding at a 7.12% CAGR through 2031, catalyzed by expatriate population growth surpassing 43% of residents. Integrated Tourism Complexes allow foreign freehold ownership, drawing upscale buyers to mixed-use schemes blending residential, retail, and workspace. SME demand benefits from dedicated incubation zones within Sultan Haitham City and other Vision 2040 projects, offering subsidized rents and access to business support services. Household investors increasingly favor properties with energy-efficient designs and community amenities, aligning with the broader sustainability trajectory of the Oman commercial real estate market.

Geography Analysis

Muscat commanded 69.25% of the Oman commercial real estate market share in 2025, anchored by governmental functions and mega-projects such as the USD 1.3 billion Al Khuwair Downtown regeneration, which targets a city-center population of 2.7 million by 2040. Madinat Al Irfan’s 624-hectare master plan foresees 90,000 jobs and 280,000 residents by 2044, driving sustained take-up of offices, retail, and hotels. Premium coastal developments, including Al Mouj and AIDA, capture high-net-worth demand while pushing land prices upward in Shatti Al Qurum and Muscat Hills. Nevertheless, Grade-B office oversupply and escalating costs are spurring capital migration toward secondary cities.

Sohar stands out as the fastest-growing node, leveraging USD 30 billion of port-based investments and 85% land occupancy to attract logistics-led projects. Upcoming assets such as the USD 1.6 billion LNG bunkering facility and a new railway link to Muscat and the UAE border reinforce connectivity advantages. Retail expansion continues, highlighted by City Centre Sohar’s 35,301 m² opening, though vacancy risks demand cautious tenant curation. Sohar’s geostrategic location outside the Strait of Hormuz appeals to global investors seeking supply-chain resilience, supporting further growth within the Oman commercial real estate market.

Salalah and the broader “Rest of Oman” corridor are growing at a 6.94% CAGR through 2031, propelled by tourism and industrial diversification initiatives. New City Salalah promises 60,000 residents and 200,000 m² of hospitality-retail space, broadening the demand base for mixed-use assets. Duqm SEZ’s 2,000 km² footprint with USD 14 billion commitments fosters green-field hotel, office, and industrial clusters. A USD 731.6 million Duqm tourism complex exemplifies rising hospitality capital deployment. Strategic fuel reserves in Dhofar and generous free-zone tax incentives enhance developer attractiveness by offsetting Muscat’s premium cost structure. Together, these regional centers diversify the geographic footprint of the Oman commercial real estate market.

Regulatory Landscape

Oman has been tightening and modernizing commercial real estate governance through royal decrees and technical standards, with the Ministry of Housing and Urban Planning (MHUP) positioned as the central regulator. The Law Regulating Real Estate (Royal Decree 79/2025) entered into force in March 2026, consolidating oversight that had been spread across multiple mandates and tightening licensing and compliance expectations across developers, brokers, and project activity.

On the transaction and asset-quality side, Royal Decree 56/2026 promulgated a new Real Estate Registry Law in May 2026, replacing the legacy registration system and reinforcing formal title registration processes. MHUP introduced Urban Compliance Certification in June 2026 to confirm adherence to the Oman Building Code, which includes 2025 technical codes spanning design, building services, and energy efficiency/sustainability. Permitting and approvals continue to rely on digital submission pathways (for example, Muscat Municipality e-services and Ministry of Interior technical services), with environmental and civil defense clearances embedded into the process for new development and major alterations.

Value Chain Analysis

Oman's commercial real estate value chain runs from land allocation and master planning, often linked to government and special-zone programs, through development finance, design, contracting, materials supply, sales and leasing, and ongoing operations. MHUP anchors the upstream regulatory and permitting interface, while special-zone ecosystems around Duqm, Sohar, and Salalah connect developers and investors to port and free-zone demand drivers that translate into requirements for logistics parks, office campuses, hospitality assets, and mixed-use schemes.

Execution relies on contractors and materials suppliers meeting national building standards, with the 2025 Oman Building Code and newer compliance mechanisms raising the bar for safety and sustainability specifications. The construction inputs layer reflects local capacity and import exposure, supported by domestic iron and steel capacity referenced at around 3 million tonnes annually, alongside a sizable construction materials market where architectural and decorative segments represent a large share. Downstream, the market depends on brokers, digital transaction channels, and property or facilities management to stabilize occupancy and performance, with tourism-led and master-planned projects (for example, Al Bustan and Duqm waterfront planning) expanding the role of branded operators and professional managers in hospitality and mixed-use assets.

Competitive Landscape

Oman’s commercial real estate arena is moderately fragmented, with government-linked entities, global investors, and agile local developers coexisting. Omran Group’s OMR 25.2 million net profit and OMR 156 million FDI attraction in 2024 underscore its role as a bellwether state-backed player. Strategic alliances are multiplying: Club Med partnered with Royal Court Affairs and Omran for a USD 100 million Musandam eco-resort aiming for BREEAM certification and 1,200 new jobs. Technology adoption differentiates landlords; smart building platforms and digital twin solutions increasingly appear in RFPs for Grade-A offices and logistics parks.

White-space opportunities are forming in data centers, cold storage, and green buildings. Oman Data Park’s USD 450 million collaboration with INTRO Technology signals a pivot toward cloud infrastructure demand. Sohar Port’s agro-bulk terminal validates niche logistics potential beyond container handling. International advisory firms such as CBRE are scaling their local footprint to supply valuation, facilities management, and ESG consulting services, pointing to the professionalization of the Oman commercial real estate market.

Regulatory evolution is shaping competitive dynamics. The Banking Law (Royal Decree 2/2025) tightens oversight yet enhances consumer protection, favoring well-capitalized sponsors able to comply. Royal Decree 38/2025 liberalizes foreign ownership in SEZs, enabling cross-border developers to compete on an equal footing with domestic incumbents. Disruptors focusing on sustainable tourism, last-mile logistics, and modular construction methods are emerging, challenging traditional players to modernize. Overall, the market rewards firms combining capitalization, sustainability credentials, and agile execution capabilities.

Oman Commercial Real Estate Industry Leaders

Omran Group

Al-Taher Group

Shanfari Group

BBH Group

Malik Developments

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory and transaction-system upgrades create room for institutional-grade product and services that reduce friction for both domestic and cross-border capital. The Real Estate Registry Law (Royal Decree 56/2026) and MHUPs expanding compliance frameworks, including Urban Compliance Certification tied to the Oman Building Code, add practical value to digital conveyancing, escrow and off-plan enablement, valuation advisory, and audit-ready property management, particularly for portfolios targeting international investors and lenders.

Multiple 2026 programs and financings also point to near-term development and funding pathways that can support absorption across mixed-use, retail, and hospitality clusters. In Sultan Haitham City, Al Adrak Group signed a USD 480 million development contract in January 2026 that includes a shopping arcade alongside residential delivery, supporting demand for retail and surrounding service real estate. Capital formation mechanisms are widening, highlighted by the July 2026 launch of a RO 96 million real estate investment fund by Tanmia and FIM Partners Muscat that targets property development via structured financing. With OPAZ unveiling the Al Duqm waterfront master plan in June 2026, including thousands of planned hotel and residential units by 2040, developers, contractors, and operators have a clearer pipeline for hospitality-adjacent commercial assets. Royal Oman Police Decision 87/2026 also links sponsor-free residency to property ownership, supporting the addressable buyer and tenant pool for integrated developments.

Recent Industry Developments

- July 2026: Tanmia and FIM Partners Muscat launched a RO 96 million real estate investment fund to back property development through preferred equity and structured financing. The vehicle adds a dedicated, programmatic capital channel for developers beyond traditional bank lending, supporting deal execution for commercial and mixed-use pipelines.

- April 2025: Royal Decree 38/2025 introduced 10-year tax exemptions and enshrined freehold ownership rights for non-Omanis in designated special economic zones. The change broadened the eligible investor base for income-producing commercial assets and strengthened the sell-down and exit options for developers operating in SEZ-linked submarkets.

- January 2024: Oman Investment Authority unveiled a USD 5.2 billion Future Fund to support foreign investment and SME growth across strategic sectors. The funding program underpins demand creation for offices, logistics, and supporting commercial space tied to new company formation and project activity.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the market refers to the value generated from commercial property activity in Oman across office, retail, industrial and logistics assets, plus hospitality and other income oriented commercial formats, tracked in USD for a consistent time series.

Scope exclusions: It excludes pure residential housing activity and one off construction contracting revenues that do not translate into commercial property value or ongoing asset operation.

Segmentation Overview

- By Property Type

- Offices

- Retail

- Logistics

- Others (industrial real estate, hospitality real estate, etc.)

- By Business Model

- Sales

- Rental

- By End-user

- Individuals / Households

- Corporates & SMEs

- Others

- By Geography

- Muscat

- Sohar

- Salalah (Dhofar)

- Rest Of Oman

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the basic demand context for Oman and to anchor inputs that can be checked against public records. We relied on official and non paywalled sources such as Oman National Centre for Statistics and Information releases, Central Bank of Oman publications, the Ministry of Housing and Urban Planning announcements, and the Public Authority for Special Economic Zones and Free Zones updates.

To make the real estate picture more practical, we also reviewed public project and planning updates, company filings, and investor presentations, along with reputable press coverage of leasing trends and new supply additions. Where needed, paid subscriptions focused on company financials and another focused on news and financials were used to cross-check timelines, ownership structures, and reported revenue exposure that helps sanity check the model. This list is illustrative, and many other public sources were also referred to for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was run to test what desk signals do not clearly show, especially on pricing, occupancy movement, and how quickly new supply is being absorbed. We spoke with a balanced mix of developers, asset managers, brokers, corporate occupiers, and logistics users, and then used follow ups to confirm the direction of assumptions across Muscat and other active hubs in Oman.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 13% | |

| Mid tier: 51% | Functional/Unit leaders: 27% | |

| Smaller Players: 17% | Managers: 60% |

Market-Sizing & Forecasting

Sizing was built using a top-down and bottom-up approach, with the main totals reconstructed from Oman level property activity signals and then checked using selective roll ups. In practice, the top-down path tied market value to the active stock and new additions, and then applied observed rent or sale price ranges by asset type and location, followed by occupancy and utilization adjustments.

Key inputs that shaped the model included new completions and the planned pipeline by city, lease rate movement for prime and secondary stock, vacancy and absorption direction, and demand from logistics and industrial users linked to free zones and port corridors. The model also tracked the pace of tourism driven hospitality supply entering operations. Where a clean public series was missing, the gaps were handled through interview led ranges that were then kept consistent with visible indicators like project launches, leasing chatter, and macro credit conditions.

For forecasting, scenario analysis was used so the model could reflect different speeds of supply delivery and tenant demand recovery, while keeping the base case aligned with what most interviewees described as realistic. The final numbers were cross checked with a lightweight bottom-up approximation using sampled rent per square foot times estimated occupied area for representative submarkets, which helped adjust any totals that drifted away from on ground pricing.

Data Validation & Update Cycle

Validation was done in steps so the final market values stay explainable and repeatable. We compared outputs against independent signals like announced project timelines, macro investment direction, and the observed trend in rents and vacancy, then reviewed outliers that looked too high or too low for a given year.

Before sign off, the model assumptions and calculations are reviewed by another analyst, and follow up calls are triggered when a key variable shifts beyond a set tolerance, such as a sudden change in delivered supply or a sharp rent reset in a major node. Reports are refreshed annually, and interim updates are made when material events occur, followed by a final pre delivery check so clients receive the latest updated view.

Mordor Intelligence's Oman Commercial Real Estate Market Size Compared With Other Published Estimates

It is normal to see different market size numbers for Oman commercial real estate because sources do not always count the same asset types, and they also treat sales versus rentals in different ways. Differences can also come from the year chosen as the base, how currency conversion is timed, and whether the estimate is tied to active operating stock or to broader investment style totals.

In this case, the biggest gap drivers are usually whether hospitality and multi family are counted inside the commercial bucket, whether the scope is limited to income generating property operations versus including wider investment channels, and how fast new supply is assumed to stabilize after delivery. When the calculation is anchored to occupied stock, rent ranges, and realistic absorption checks, and then refreshed when major policy or project news changes the outlook, the result stays more traceable, which is the approach applied here by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.34 B (2026) | |

| Industry Publisher A | USD 3.80 B (2026) | Often broadens the scope to include additional investment structures and mixed use treatment that can pull in value not directly tied to operating occupancy and rent based sizing for Oman. |

| Industry Publisher B | USD 2.22 B (2025) | Uses an earlier base year value and can understate near term growth if new supply delivery timing and rent reset effects are not rechecked with current leasing and absorption signals. |

The spread in the table is mainly explained by scope and timing choices, not by arithmetic. By keeping the model linked to asset level demand signals (occupied stock, rent ranges, vacancy direction, and pipeline timing) and then stress testing the assumptions through field feedback, the final market size stays balanced and easier to defend year to year.

Key Questions Answered in the Report

What is the current value of the Oman commercial real estate market?

The Oman commercial real estate market size is valued at USD 2.34 billion in 2026 and expected to reach USD 3.06 billion by 2031.

Which property type is growing fastest in Oman’s commercial segment?

Logistics assets lead growth with a projected 7.45% CAGR through 2031, underpinned by port expansion and free-trade-zone incentives.

How have recent royal decrees affected foreign ownership?

Royal Decree 38/2025 permits non-Omani investors to acquire freehold property in designated zones and grants 10-year tax exemptions in SEZs.

Why do rentals dominate over sales in Oman’s commercial market?

Corporates favor lease flexibility, resulting in rentals accounting for 70.02% of 2025 activity, though sales are gaining momentum as regulations liberalize.

Page last updated on: