Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

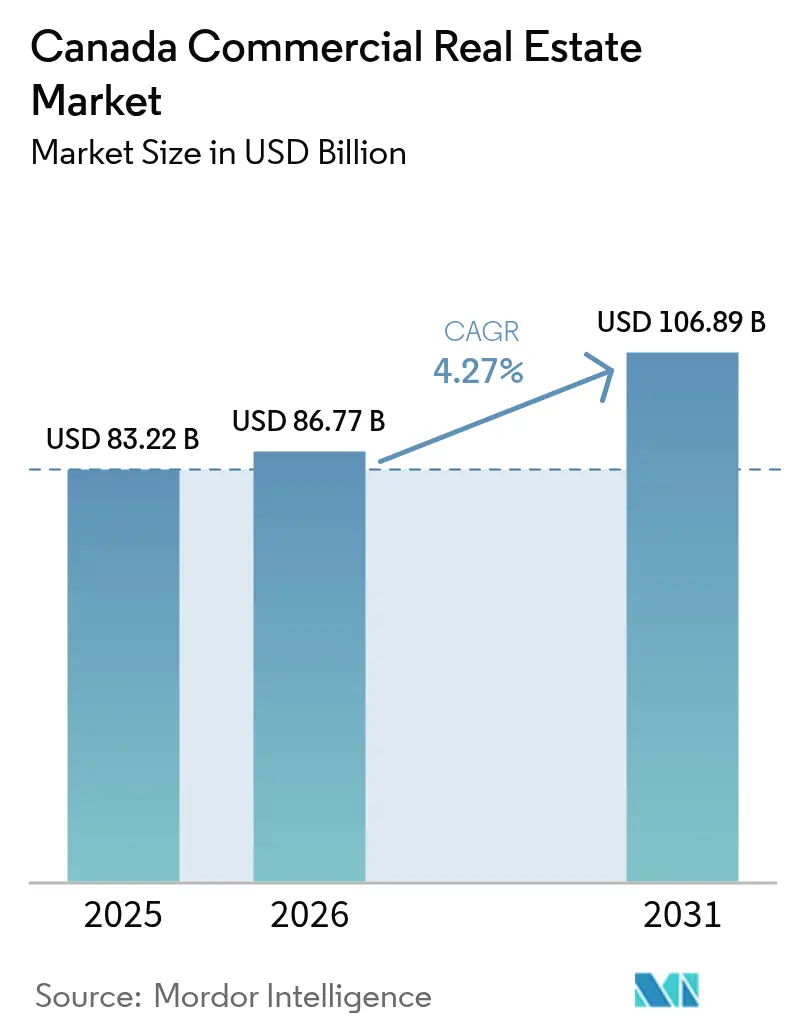

| Base Year Market Size (2025) | USD 83.22 Billion |

| Market Size (2026) | USD 86.77 Billion |

| Market Size (2031) | USD 106.89 Billion |

| Growth Rate (2026 - 2031) | 4.27% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Commercial Real Estate Market Analysis by Mordor Intelligence

The Canada commercial real estate market size was valued at USD 83.22 billion in 2025 and estimated to grow from USD 86.77 billion in 2026 to reach USD 106.89 billion by 2031, at a CAGR of 4.27% during the forecast period (2026-2031). Investor sentiment has improved as lower policy rates narrow financing spreads, prompting pension funds and REITs to recycle capital into core assets while off-loading non-strategic properties. Immigration-led population growth, an uptick in near-shoring manufacturing, and persistent e-commerce adoption are widening demand for offices, logistics facilities, and mixed-use developments. Infrastructure spending, such as the USD 356 million CN rail upgrade in Quebec, is reinforcing trade corridors and boosting industrial site absorption. Meanwhile, Quebec’s low-cost hydro power is luring data-center operators, deepening the province’s appeal as a technology services hub.

Key Report Takeaways

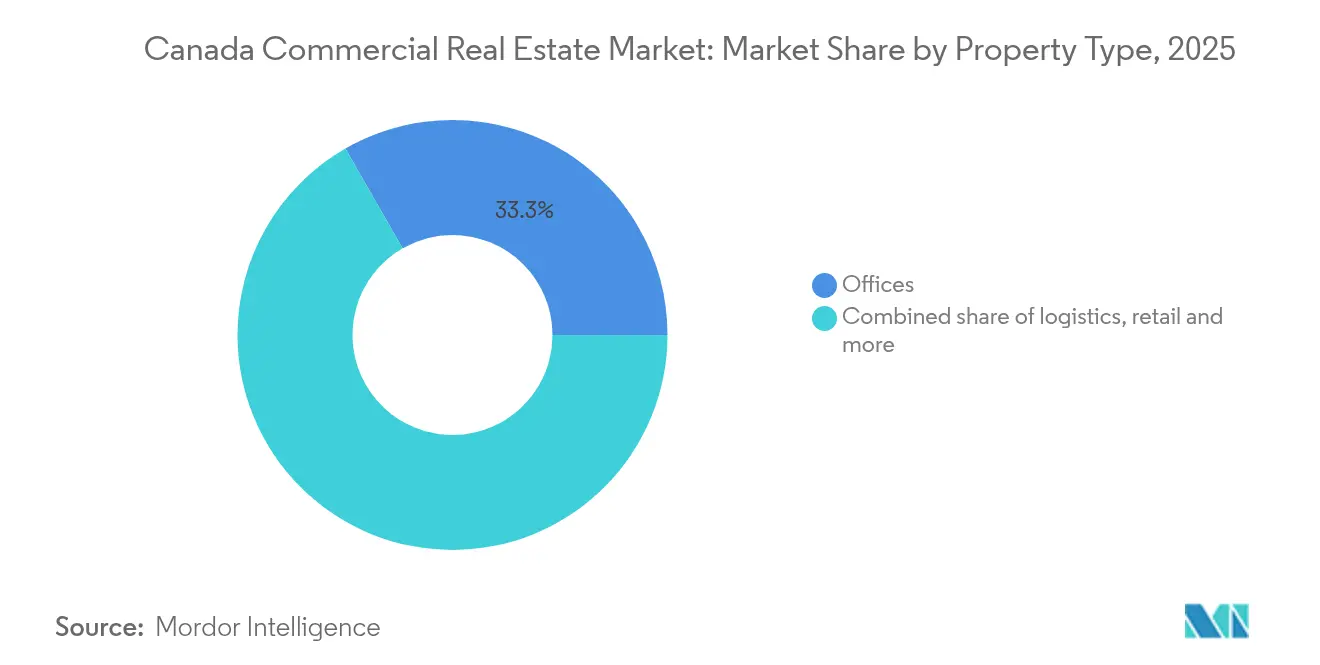

- By property type, offices led with a 33.30% share of the Canada commercial real estate market in 2025; logistics assets are projected to grow at a 4.96% CAGR to 2031.

- By business model, the sales segment held 62.30% of the Canada commercial real estate market share in 2025, while the rental segment records the quickest expansion at 4.85% CAGR through 2031.

- By end-user, corporates and SMEs accounted for 72.45% of the Canada commercial real estate market size in 2025 and are advancing at a 4.72% CAGR.

- By region, Ontario captured 28.90% of the Canada commercial real estate market in 2025; Quebec is the fastest-growing geography with a 4.95% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Commercial Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Federal immigration target of 500 k new residents yearly | +1.2% | National; concentrated in Toronto, Vancouver, Montreal | Long term (≥ 4 years) |

| Near-shoring industrial demand along Ontario–Quebec corridor | +0.8% | Ontario & Quebec, spillover to Atlantic Canada | Medium term (2–4 years) |

| E-commerce surpassing 8% of retail sales | +0.6% | National urban centers | Medium term (2–4 years) |

| REIT capital recycling and pension-fund dry powder | +0.5% | Core markets of Toronto, Vancouver, Montreal | Short term (≤ 2 years) |

| Toronto tech-tenant expansion in Class-A offices | +0.4% | Greater Toronto Area, Ottawa, Waterloo | Short term (≤ 2 years) |

| Data-center migration to Quebec hydro power | +0.3% | Quebec; extension to Manitoba, British Columbia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in near-shoring-fueled industrial demand along the Ontario–Quebec corridor

Manufacturers moving production closer to North American consumers are absorbing warehouse and flex assets across the Windsor-Quebec City stretch, encouraged by Quebec’s USD 4.05 billion competitiveness plan that counters U.S. trade barriers.[1]“Discours sur le budget 2025-2026,” finances.gouv.qc.cammigration,” canada.ca Industrial leasing remains brisk in automotive and advanced-manufacturing clusters, even though national exports fell 2.8% in Q3 2024. Enhanced CN rail capacity, underpinned by a USD 356 million upgrade, lifts throughput and reduces transit times, strengthening the corridor’s logistics profile. Developers are adding modern, high-clear-height facilities, yet construction pipelines stay disciplined amid cost inflation, preventing oversupply. Medium-term absorption is set to dominate new completions as distribution operators prioritize speed-to-market advantages.

Federal immigration targets adding 500 k residents annually boosting multi-family construction

Policy makers aim to admit 395 000 permanent residents in 2025, tapering to 365 000 by 2027, with 29% of arrivals holding construction trades skills.[2]Statistics Canada, “Building Construction Price Indexes, Q1 2025,” statcan.gc.ca The influx intensifies demand for neighborhood retail, life-cycle office services, and urban logistics nodes in Toronto, Vancouver, and Montreal. Stable household formation supports mixed-use projects near transit, narrowing the housing supply gap by an expected 670 000 units by 2027. Secondary cities such as Halifax and Saskatoon are also attracting newcomers, broadening the geographic footprint of commercial developments. Developers are leveraging modular designs that can pivot between residential and ground-floor commercial use to future-proof projects.

Toronto tech-tenant expansion sustaining Class-A office pre-leasing despite hybrid work

Technology employers continue to prioritise collaborative hubs, evidenced by Kainos tripling Toronto headcount to 300 by 2025. Large pre-lease deals are queued for delivery through 2026 even as the citywide vacancy sits at 19.2%. Tenants prefer amenity-rich towers that support employee wellness and ESG credentials, leading to a bifurcated market in which Grade-A space outperforms commodity offices. Co-working operators are also scaling footprints, absorbing backfill space from occupiers rightsizing portfolios. Short-term incentives, such as turnkey build-outs and rent abatements, remain prevalent but are expected to taper once vacancy plateaus.

E-commerce penetration crossing 8% of retail sales driving last-mile urban logistics

Retailers upgrading omnichannel capabilities are leasing micro-fulfillment centers within 10 km of dense consumer clusters, decreasing delivery times and lowering emissions. The International Transport Forum highlights sidewalk delivery robots as a promising solution for congestion alleviation, nudging zoning authorities to permit smaller logistics footprints in mixed-use areas. Adaptive reuse of older retail boxes into cross-docks is common, especially around Toronto and Vancouver. Developers are factoring in higher power loads and data connectivity to accommodate automation. Medium-term demand for sub-150 k sq ft facilities is forecast to outstrip supply, keeping rents on an upward trajectory.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Elevated Bank of Canada policy rate keeping cap rates sticky and valuations volatile | -0.9% | National; most acute in Toronto & Vancouver | Short term (≤ 2 years) |

| Construction-cost inflation averaging 11% CAGR pressuring development margins | -0.7% | Major urban centers nationwide | Medium term (2–4 years) |

| Tightening ESG disclosure requirements raising retrofit capex for legacy assets | -0.6% | National; older Class-B/C assets in Toronto, Montreal, Calgary | Medium term (2–4 years) |

| Suburban office vacancy spikes post-pandemic dampening rental growth outside CBDs | -0.4% | Suburban sub-markets of Toronto, Vancouver, Ottawa | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Elevated Bank of Canada policy rate keeping cap rates sticky and valuations volatile

Although the policy rate eased to 3% in 2025, mortgage spreads continue to shadow bond yields, sustaining a bid-ask gap that muffles transaction velocity. Cap-rate decompression is most visible in secondary office and retail, while prime industrial remains tighter. Smaller sponsors relying on bank credit are retreating, allowing well-capitalized REITs to consolidate positions. Forward hedging costs keep development starts subdued until financing markets stabilise further. Short-term, price discovery hinges on additional rate cuts and clarity around U.S. tariff policies.

Construction-cost inflation averaging 11% CAGR pressuring development margins

Statistics Canada recorded a 3.5% year-over-year cost rise for non-residential builds in Q1 2025, with local spikes in London and Regina. [3]Government of Canada, “Government of Canada Reduces IMinistère des Finances du Québec, Material volatility, notably for steel and aluminum, complicates tender pricing and squeezes fixed-price contracts. Developers of affordable housing and mixed-use projects struggle to pass costs to tenants, forcing redesigns or phased delivery. Prefabrication and bulk-buy procurement are mitigating some pressures but require scale that smaller builders lack. Supply-chain hiccups in mechanical equipment elongate project timelines, adding carry costs and contingency premiums.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Type: Offices anchor activity while logistics accelerates

Offices accounted for 33.30% of the Canada commercial real estate market in 2025, reinforcing their role as the sector’s primary revenue driver. Vacancy peaked at 18.4% nationwide yet stabilized as tenants traded up to modern space, compressing obsolescence risk in newer towers. Investment flowed into experiential upgrades—wellness centers, flexible collaboration zones, and renewable-powered HVAC—to retain knowledge-sector occupiers. The flight-to-quality dynamic, coupled with limited new-build starts, underpins rental resilience in Class-A assets across Toronto, Vancouver, and Montreal. Meanwhile, provincial incentives for office-to-residential conversion removed 870 000 sq ft from stock in Q1 2024, tightening prime supply and supporting rent growth in downtown nodes.

Logistics is the fastest-growing category, expanding at a 4.96% CAGR through 2031 as retailers target same-day fulfilment standards. Multi-level urban warehouses and cold-chain facilities attract institutional capital keen to capture steady cash flows. Developers emphasize power redundancy, dock-door ratios, and turnaround lanes compatible with electric delivery fleets. Despite elevated land prices near Toronto’s Pearson Airport, demand consistently outruns supply, maintaining rent premiums and low structural vacancy. Investors employing cross-docking retrofits and mezzanine build-outs are boosting returns without large green-field risk. Collectively, offices and logistics together represent more than half of the Canada commercial real estate market size, signalling balanced exposure between legacy and growth-oriented assets.

By Business Model: Sales turnover dominates, but rentals lead growth

Sales transactions constituted 62.30% of the Canada commercial real estate market in 2025, reflecting capital-recycling strategies among REITs and pension funds. Mega-deals, such as Artis REIT’s USD 729.7 million divestment program, illustrate active portfolio rebalancing that supports liquidity in core markets. Foreign investors, notably from Singapore and Germany, are net buyers of stabilized retail and industrial assets, leveraging favorable currency differentials. Title transfers have clustered around Toronto and Vancouver, where data transparency accelerates underwriting. Nonetheless, bid-ask alignment remains fragile when debt pricing is volatile.

The rental model, growing at 4.85% CAGR, is becoming central to institutional strategies prioritizing income durability during economic uncertainty. CAPREIT’s 98.1% occupancy and USD 117.3 million same-property NOI in 2024 spotlight rental resilience s25.q4cdn.com. Asset managers are deploying smart-building systems to optimize landlord-controlled utilities, lifting net operating income without elevating face rents. ESG compliance frameworks also unlock green financing advantages, lowering interest costs on refinances. As debt markets stabilise, analysts expect rental portfolios to command valuation premiums relative to trading-oriented platforms, cementing their share of the Canada commercial real estate market size over the forecast horizon.

By End-User: Corporates and SMEs shape demand patterns

Corporates and SMEs commanded 72.45% of the Canada commercial real estate market in 2025 and are forecast to expand at a 4.72% CAGR, buoyed by technology-sector hiring and on-shoring manufacturing. Employers seek high-density, transit-rich office precincts to access talent and foster collaboration. The segment’s growth also fuels requirements for regional distribution hubs that support omnichannel retail strategies. SMEs in life sciences, fintech, and creative industries gravitate toward flexible leases within innovation districts, creating opportunities for landlords offering plug-and-play space.

Demand from individuals and households centers on neighborhood-scale retail and mixed-use assets that integrate grocery anchors with community services. Government and institutional users, while smaller, supply steady revenue streams through long-duration leases, particularly in defense, education, and healthcare facilities. Corporates’ shift toward hybrid work has increased interest in adaptable floor plates and wellness-certified air filtration systems, pushing landlords to retrofit stock quickly. Immigration-driven labor growth adds further depth to occupier pipelines, ensuring that corporates and SMEs remain the dominant influencers of Canada commercial real estate market share over the medium term.

Geography Analysis

Ontario held 28.90% of the Canada commercial real estate market in 2025, anchored by the Greater Toronto Area’s dense agglomeration of financial, technology, and life-science tenants. Electricity demand in the province is projected to climb 60% by 2050, underpinning infrastructure investment that boosts commercial construction. The Ministry of Economic Development earmarked USD 1.85 billion for 2025-2026 to court advanced-manufacturing projects, while the Transit-Oriented Communities initiative incentivizes mixed-use nodes around new subway stations. Vulnerability to U.S. trade policy persists, as three-quarters of provincial exports cross the American border, but near-shoring trends partly offset that risk by encouraging local production.

Quebec, the fastest-growing province at a 4.95% CAGR, leverages USD 4.05 billion in economic programs and abundant hydro power to court data-center and aerospace investors. Investissement Québec logged USD 6.5 billion in foreign direct investment across 82 projects in 2024-2025, signalling diversified demand beyond traditional manufacturing. CN’s USD 356 million rail upgrade and the REM light-rail project propel logistics capabilities and catalyze USD 9 billion in contiguous real estate development. Broader export strategies targeting Europe and Asia reduce dependence on U.S. markets, softening cyclical shocks.

British Columbia and Alberta offer counter-cyclical positioning, with Calgary’s recovery anchored by energy diversification and professional-services growth. The Canada Infrastructure Bank pipeline exceeding USD 25 billion in public-private projects across Western provinces enlarges the industrial and office footprints of second-tier cities. Atlantic Canada benefits from spillover logistics demand and a growing near-shoring footprint in food processing and clean-tech components. Across regions, specialization—whether in clean energy, AI infrastructure, or advanced manufacturing—dictates capital allocation strategies, widening the canvas for investors pursuing balanced exposure within the Canada commercial real estate market.

Regulatory Landscape

Canada commercial real estate development and transactions operate within a layered framework covering federal taxation and procurement, national model codes, and provincial and municipal land-use and permitting. The Canada Revenue Agency oversees GST/HST treatment for commercial real property sales and rentals, while federal real property held or acquired by the Crown is governed under the Federal Real Property and Federal Immovables Act and related Treasury Board policy instruments, with Public Services and Procurement Canada using CanadaBuys for real property-related procurement.

In 2025-2026, policy emphasis has focused on accelerating construction and standardizing technical compliance. The National Research Council published the National Building Code of Canada 2025, and the Canadian Board for Harmonized Construction Codes made the 2025 National Model Codes available, reinforcing updated baseline requirements that shape structural and life-safety design across jurisdictions as provinces adopt or adapt the model codes. On the enabling-policy side, the Government of Canada introduced the Build Canada Homes Act in February 2026 to establish a dedicated Crown corporation for affordable housing construction, alongside March 2026 federal measures aimed at boosting supply and addressing municipal cost structures that can spill over into mixed-use and neighborhood commercial formats.

Value Chain Analysis

The Canadian commercial real estate value chain starts with land assembly and planning approvals, then moves through design (architects and engineers), construction delivery (general contractors and specialty trades), materials and equipment supply (including steel, aluminum, and MEP systems), and finally leasing, brokerage, property management, and capital markets (REITs, pension funds, lenders, plus valuation and advisory). Federal and provincial infrastructure programs and trade-corridor upgrades support the upstream stages by improving site viability and tenant access, while lenders, appraisers, and insurance providers shape underwriting standards and transaction velocity.

In 2025-2026, execution risk has been influenced by labor availability and input-cost volatility, with construction-industry reporting pointing to a 3% to 4% cost inflation range and continued shortages in MEP trades. Contractor feedback suggests supply chain disruptions are easing but remain present, with 34% reporting disruptions in 2026 (down from 38% in 2025 and 58% in 2024), which is supporting procurement shifts toward longer-lead ordering and design-build contracting. On the demand and operations side, modern logistics facilities are incorporating higher-density automation, exemplified by lululemon completing a one-million-square-foot distribution center in Brampton with an AutoStore robotics installation, which drives higher power, floor-loading, and fit-out specifications and feeds back into development and retrofit decisions.

Competitive Landscape

Market competition is moderate, with nationally diversified REITs and pension-backed managers holding substantial portfolios while specialist developers carve out high-growth niches. RioCan, Brookfield Properties, and Oxford Properties rely on scale to access low-cost debt and seize core urban redevelopment plots. Colliers’ pending purchase of Triovest forms a services powerhouse overseeing more than 95 million sq ft, adding integrated asset-management capacity and expanding brokerage presence in secondary markets. The consolidation wave enhances bargaining power with lenders and contractors, but it narrows supplier diversity for smaller landlords.

Strategic activity centers on capital recycling: Artis REIT cut leverage to 40.2% after unloading USD 729.7 million of assets, redeploying funds into high-growth Vancouver industrial projects. PROREIT’s USD 72.4 million Winnipeg acquisition lifts its industrial weighting to 88% of gross leasable area, demonstrating a pivot toward defensive cash-flow assets. Pension funds such as CDPQ pursue data-center and life-science platforms that align with long-duration liabilities and ESG mandates. Each move underscores a trend toward sharpening portfolio focus, reducing exposure to vulnerable suburban offices.

Technology adoption further differentiates leading landlords. ESG reporting suites, tenant-engagement apps, and predictive maintenance platforms are now standard across top portfolios. Brookfield leverages AI-based energy analytics to trim operating costs, while Oxford deploys smart-building sensors to optimize air quality and occupant comfort. Smaller entrants mitigate scale disadvantages by targeting underserved niches—cold storage near Atlantic ports or mass-timber office buildings appealing to green-economy tenants. The resulting competitive dynamic rewards both capital muscle and specialized operating expertise within the Canada commercial real estate market.

Canada Commercial Real Estate Industry Leaders

Brookfield Property Partners L.P.

Cadillac Fairview Corporation Ltd.

Oxford Properties Group

Allied Properties REIT

Dream Office REIT

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term opportunity set is emerging around policy-led acceleration of housing and infrastructure, which is also expanding demand for complementary commercial formats such as mixed-use nodes, neighborhood retail, and urban logistics tied to population growth and densification. In March 2026, the federal government introduced Bill C-26 proposing CAD 1.7 billion in payments to provinces and territories to increase housing supply, including measures to reduce development fees and levies, and the Canada-Ontario Partnership to Build announced CAD 8.8 billion over 10 years for housing-enabling infrastructure, contingent on municipalities reducing development charges by up to 50% for three years. In Ontario, Bill 98 (Building Homes and Improving Transportation Infrastructure Act, 2026) targets faster planning and approvals, which supports whitespace for developers and investors in transit-oriented and services-heavy submarkets.

Another opportunity is operational modernization and retrofit activity across existing stock, driven by tightening disclosure and performance expectations and by landlords prioritizing net operating income resilience. BOMA Canada reported that 62% of building decision-makers surveyed plan to invest in AI within two years, focusing on building automation, advanced analytics, predictive maintenance, and sustainability reporting, which aligns with owner priorities to manage energy and maintenance costs. In parallel, federal regulatory streamlining for large projects is creating a macro catalyst: in May 2026, the Government of Canada noted 21 nation-building projects referred to the Major Projects Office, representing over CAD 126 billion in investment, with cooperation agreements in place across multiple provinces. These arrangements support more predictable timelines for major employment and industrial nodes, which typically translates into incremental demand for offices, logistics facilities, and supporting retail.

Recent Industry Developments

- July 2026: LiUNA and Fengate, with The Hi-Rise Group, broke ground on the West Orchard Urban Rentals project in Ottawa, a 37-storey mixed-use rental development positioned as transit-oriented city building. The project adds momentum to infill, mixed-use delivery models that blend rental housing with complementary commercial uses, supporting footfall and services demand in growing urban nodes.

- June 2026: Fengate announced the Toronto Rail Yards mixed-use project in downtown Toronto, planned to include 85,000 square metres of office space and 4,700 square metres of retail. The scale and transit-connected positioning reinforce developer and investor focus on mixed-use intensification strategies that combine office utilization with curated retail and placemaking.

- April 2026: Immostar and Primaris REIT completed a CAD 62.3 million acquisition of the North and South complexes of Les Galeries de la Capitale in Quebec City, adding 307,900 square feet of retail space. The transaction highlights continued portfolio activity in established regional retail nodes and signals selective capital deployment into stabilized, cash-flowing commercial assets outside the largest gateway markets.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers income-producing commercial properties in Canada where pricing is driven by leasing demand and investment activity across major property classes.

Scope exclusions: We exclude purely residential housing, raw land banking, public infrastructure, and standalone property management service fees.

Segmentation Overview

- By Property Type

- Offices

- Retail

- Logistics

- Others (industrial real estate, hospitality real estate, etc.)

- By Business Model

- Sales

- Rental

- By End-user

- Individuals / Households

- Corporates & SMEs

- Others

- By Region (Province)

- Ontario

- Quebec

- British Columbia

- Alberta

- Rest of Canada

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to anchor the model with public signals that can be checked year after year, especially for transactions, supply, and demand. We leaned on sources such as Statistics Canada (construction, investment, and price series), the Bank of Canada (policy rates and financing conditions), and Canada Mortgage and Housing Corporation for pipeline context that can spill into mixed-use activity.

To keep the market context grounded, we also reviewed the Canada Revenue Agency and customs trade statistics where they help explain capital goods and fit-out activity, plus municipal and provincial planning portals for development approvals and zoning changes. Industry association websites, public REIT filings, investor presentations, and reputable business press were used to cross-check leasing sentiment and cap-rate direction. Where public disclosures were thin, a paid subscription for company financials and intelligence supported ownership and portfolio checks, and a paid news and financials product helped track deal announcements. The desk sources listed above are illustrative only, and many additional public documents were referenced for data collection, cross-checks, and clarification.

Primary Interviews and Surveys

Primary interviews and surveys were done to pressure-test the demand and pricing assumptions behind leasing and transactions, since headline market activity can swing with interest rates. We spoke with a mix of owners, developers, brokers, lenders, and large occupiers across major provinces so that leasing conditions, vacancy shifts, and cap-rate moves were validated against what is happening on the ground.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 14% | |

| Mid tier: 48% | Functional/Unit leaders: 29% | |

| Smaller Players: 19% | Managers: 57% |

Market-Sizing & Forecasting

The sizing work starts from a top-down build where national transaction value and development completion signals are reconstructed into a Canada-wide demand pool, and then split by commercial asset class based on observed activity and typical deal mix. To make sure the totals do not drift, the outputs are then corroborated with selective bottom-up checks such as sampled deal sizes by asset type, indicative cap-rate bands, and volume-by-ticket-size patterns shared by market participants.

A few practical inputs were treated as core drivers, since they show up consistently in interviews and public data. These included policy interest rates and lending spreads, office and industrial vacancy direction, construction cost inflation, immigration and population growth pressure on mixed-use intensity, and e-commerce penetration as a proxy for logistics space demand. When certain sub-markets had thin disclosure, gaps were handled by using province-level proxies and then adjusting them with interview-based weights so the roll-up stayed consistent.

For forecasting, we relied on scenario analysis tied to rate paths and leasing conditions, followed by a simple regression check that relates transaction value to financing costs and vacancy trends. The forward assumptions were kept conservative and were re-validated with experts so the forecast stays explainable and repeatable.

Data Validation & Update Cycle

Outputs were validated by comparing the model totals with independent signals such as deal flow commentary, shifts in cap-rate expectations, and public construction and investment series, and then reviewing any large variances by asset type. When results did not line up with the market narrative for a given year, we re-checked inputs, revisited the source series timing, and re-contacted a small set of respondents to confirm what had changed.

Before sign-off, the work is reviewed in steps so that calculation logic, assumptions, and currency treatment are consistent across historical years and the forecast period. The report is refreshed annually, and interim updates are made when material events occur, after which a final pre-delivery review is completed so clients receive the latest view.

Mordor Intelligence's Canada Commercial Real Estate Market Sizing Compared With Other Published Estimates

Published estimates for Canada commercial real estate can differ a lot because some sources are sizing annual investment volume, while others size the broader value of completed, income-producing assets and activity tied to them. Differences also come from how mixed-use assets are counted, how currency and constant-dollar assumptions are treated, and whether the year is a realized close or a forward-looking outlook.

By checking deal close values, practical completion timing, and lease-driven pricing signals, Mordor Intelligence keeps the Canada commercial real estate total aligned to income-producing built assets instead of only annual capital deployed, which shifts the measured market size.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 83.22 B (2025) | |

| Industry Data Provider A | USD 38.00 B (2025) | This estimate reflects annual investment volume, so it captures the year's transaction flow rather than the broader market value tied to income-producing commercial assets. It can also be more sensitive to deal count swings in a single quarter. |

| Global Brokerage Outlook B | USD 34.50 B (2025) | This number is a forward-looking investment total for the year and may embed a different rate-path assumption and partial-year run-rate logic. It is not designed to represent the full commercial property market beyond investment turnover. |

The spread in the table is mainly explained by what is being measured, where flow-based investment totals naturally come in below an asset-focused market size. When buyers compare sources, it helps to match the decision need, since tracking yearly deal activity answers a different question than sizing the value of income-producing commercial assets.

Key Questions Answered in the Report

What is the current size of the Canada commercial real estate market and how fast is it growing?

The market is valued at USD 86.77 billion in 2026 and is forecast to expand at a 4.27% CAGR to reach USD 106.89 billion by 2031.

Which property type holds the largest market share today?

Offices lead the landscape with a 33.30% share of the 2025 Canada commercial real estate market, underpinned by a flight-to-quality toward amenity-rich, Class-A buildings.

What segment is expected to grow the quickest through 2031?

Logistics properties are projected to post the fastest growth, advancing at a 4.96% CAGR as e-commerce and near-shoring boost demand for urban distribution space.

Which province is the biggest contributor, and which is expanding the fastest?

Ontario tops the chart with 28.90% of market revenue in 2025, while Quebec is the pace-setter with a 4.95% CAGR driven by clean-energy advantages and near-shoring investments.

How are rising immigration targets influencing commercial real estate demand?

Annual inflows of nearly 500 000 new residents reinforce demand for mixed-use developments, neighborhood retail, and supporting logistics hubs, especially in Toronto, Vancouver, and Montreal.

What are the primary risks clouding near-term investment decisions?

Elevated debt costs and construction-price inflation—running at 3.5% year-over-year in Q1 2025—are squeezing development margins and delaying transactions until financing markets stabilize.

Page last updated on: