Commercial Genset Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 14.38 Billion |

| Market Size (2031) | USD 21.20 Billion |

| Growth Rate (2026 - 2031) | 8.07% CAGR |

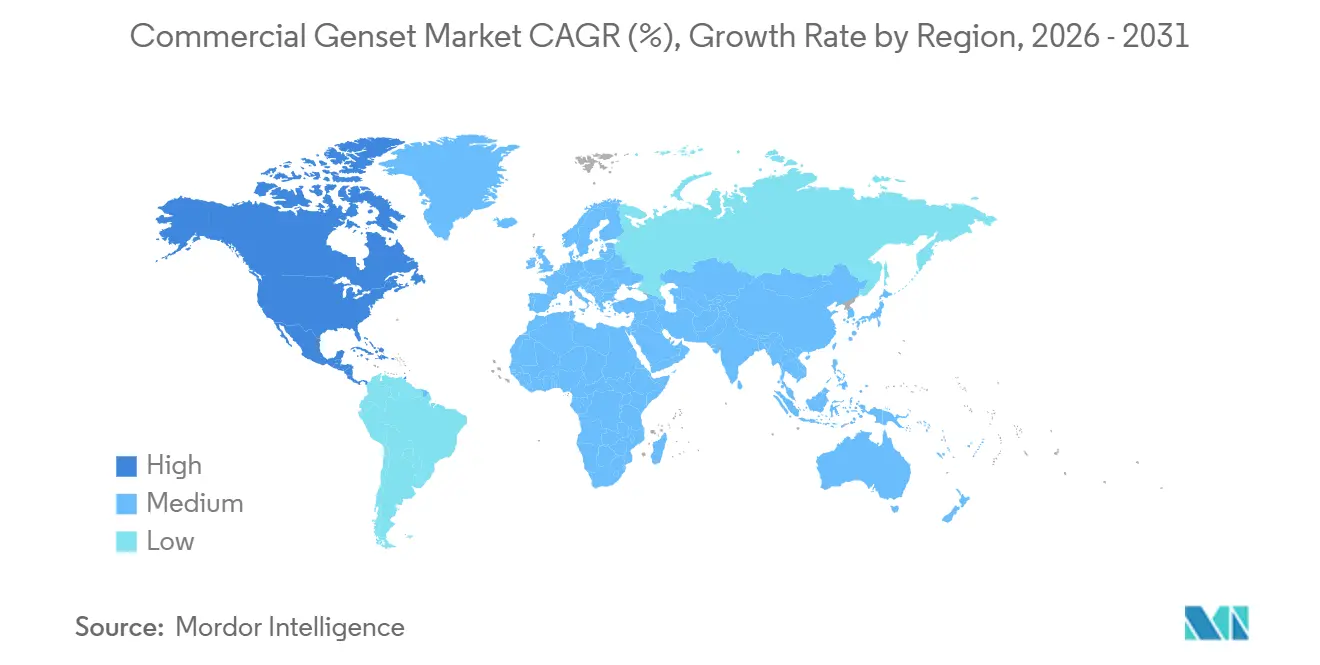

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Commercial Genset Market Analysis by Mordor Intelligence

The Commercial Genset Market is expected to grow from USD 13.26 billion in 2025 and USD 14.38 billion in 2026 to USD 21.20 billion by 2031, with a CAGR of 8.07% during the period from 2026 to 2031. Onsite generation has evolved from a mere contingency to a pivotal element in capacity planning, driven by factors like the expansion of data-center footprints, intensified 5G tower densification, and extended grid interconnection queues lasting four to eight years. By 2030, hyperscalers are set to invest over USD 40 billion in server-farm developments across India. Concurrently, the International Energy Agency forecasts a surge in global data-center electricity demand, estimating it will approach 945 TWh by 2030. Stricter regulations, namely the EPA Tier 4-Final and Euro Stage V, are inflating diesel genset costs by 15-30%. This uptick in costs is steering the industry towards natural-gas and hybrid configurations. Furthermore, as battery prices decline, the once-significant cost advantage of gensets for prolonged runtimes diminishes. In response, suppliers are bolstering their offerings, introducing features like acoustic enclosures, hydrogen-ready engines, and AI-driven maintenance solutions.

Key Report Takeaways

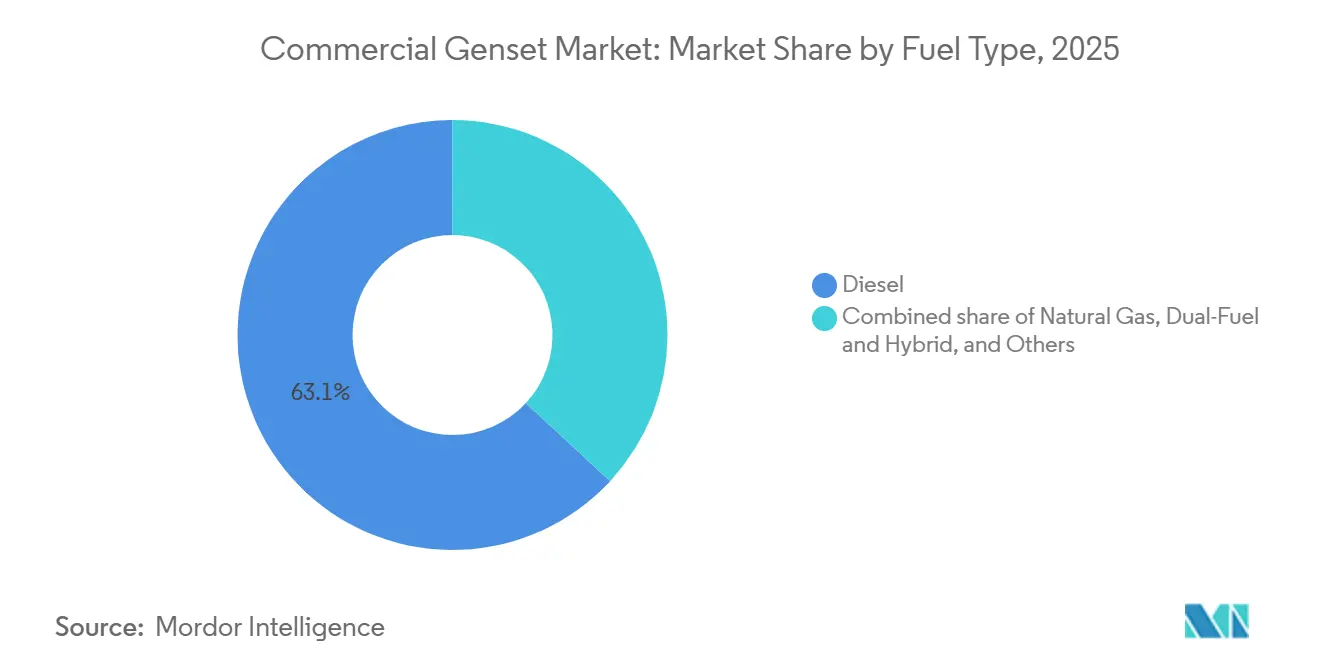

- By fuel type, diesel retained 63.1% share of the commercial genset market size in 2025, while natural gas is forecast to expand at an 11.4% CAGR through 2031.

- By power rating, the >750 kVA class is expected to capture 10.1% CAGR growth, eclipsing the 75-750 kVA segment, which retained 49.7% of the commercial genset market size in 2025.

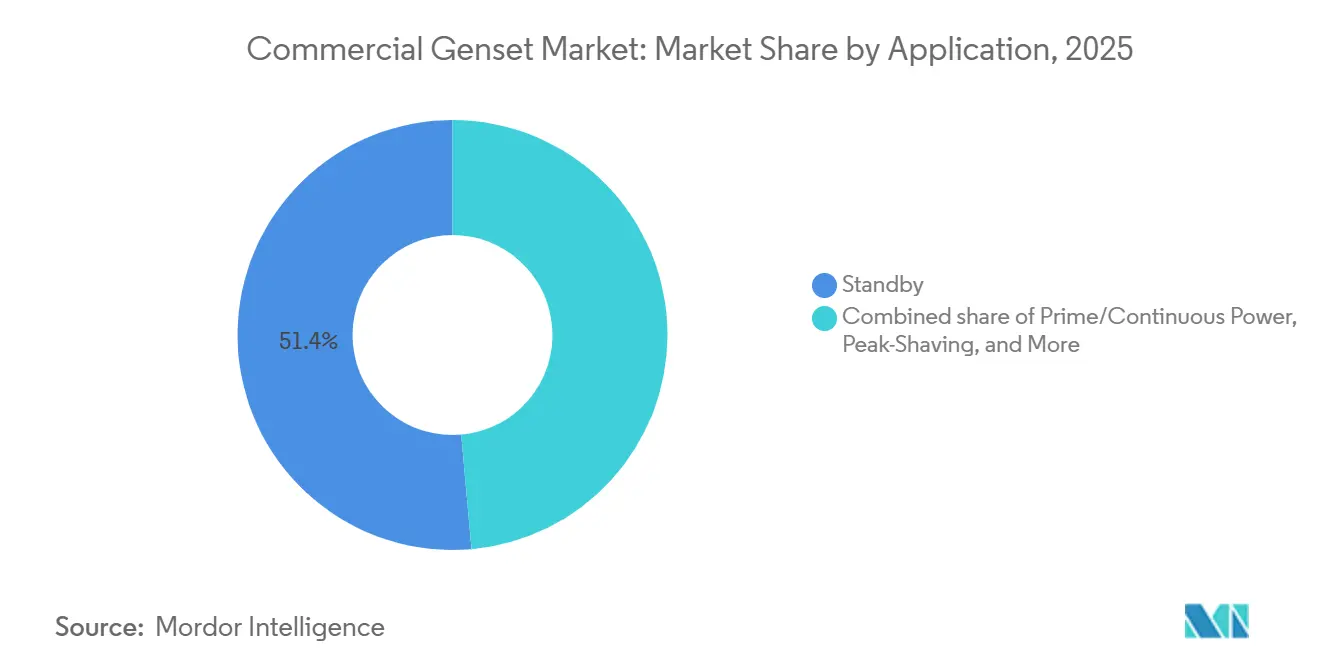

- By application, prime/continuous power is expected to rise at a 9.6% CAGR, overtaking standby deployments that formed 51.4% of shipments in 2025.

- By end-user industry, data centers led with 35.3% of the commercial genset market share in 2025 and are expected to advance at an 8.5% CAGR to 2031.

- By geography, Asia-Pacific held a 45.2% revenue share in 2025, while North America records the fastest projected CAGR at 9.1% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Commercial Genset Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in hyperscale & edge data-centers | +2.10% | Global, focus on North America & India | Medium term (2-4 years) |

| Fast-rising grid-constrained commercial real estate | +1.50% | Texas, Arizona, EU core economies | Short term (≤ 2 years) |

| Diesel-to-gas switch from Tier 4-Final & Stage V norms | +1.30% | North America & EU | Medium term (2-4 years) |

| Telecom 5G densification | +1.00% | APAC & Africa | Long term (≥ 4 years) |

| Adoption of hydrogen-ready and hybrid gensets | +0.80% | EU & North America | Long term (≥ 4 years) |

| AI-enabled predictive maintenance | +0.60% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Hyperscale & Edge Data-Centers

Queue delays at PJM and ERCOT average around eight years, leading operators to secure an estimated 10-12 GW of onsite generation rather than waiting for new transmission infrastructure. In India, the installed data center power capacity increased from 1.4 GW in Q2 2025, with a target of reaching 4-10 GW by 2030, supported by USD 40 billion in new hyperscaler investments. Atlas Energy’s USD 840 million order for 1.4 GW of Caterpillar CG260-16 and G3520 natural gas units underscores substantial multi-megawatt behind-the-meter procurement aimed at addressing grid constraints.

Fast-Rising Grid-Constrained Commercial Real-Estate in the US Sun Belt & EU

ERCOT's interconnection queue is projected to reach 226 GW by 2025, with data centers accounting for approximately three-quarters of the backlog. Transmission upgrades are expected to take seven to ten years to complete. Developers in cities such as Austin, Dallas, Phoenix, and Tampa are incorporating prime-power gensets into new constructions, while German offices are installing continuous-duty machines to manage periods of reduced solar and wind energy generation, referred to as Dunkelflaute. (1)ERCOT, “Generator Interconnection Status Report 2025,” ercot.com

Diesel-to-Gas Switch Driven by Tier 4-Final & Euro Stage V Norms

The addition of particulate filters and SCR hardware has increased diesel genset prices by up to 30%, driving demand for natural gas models, which reduce CO₂ emissions by approximately 25% per kWh and eliminate the need for DEF logistics. Henry Hub natural gas prices are projected to reach USD 3.76 per MMBtu by 2026, further strengthening the cost-of-ownership advantage as pipeline expansions progress.

Telecom 5G Densification in APAC & Africa

Tower power constitutes approximately 30-34% of the operating costs for Indian tower companies. Hybrid solutions combining solar energy, lithium iron phosphate (LFP) batteries, and appropriately sized generators can decrease diesel consumption by up to 70%, with payback periods of less than three years. In Zambia, Nigeria, and Kenya, 20-50 kW generator sets remain widely used to maintain baseline resilience, as grid uptime in these regions averages between 60% and 70%.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid fall in commercial-scale battery prices | -1.20% | Global, led by China | Short term (≤ 2 years) |

| Stricter urban noise ordinances | -0.50% | North America & EU cities | Medium term (2-4 years) |

| LNG & pipeline-gas price volatility | -0.40% | North America, EU, APAC | Short term (≤ 2 years) |

| Expanding green-lease clauses | -0.30% | EU & North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Fall in Commercial-Scale Battery Prices

Average lithium-iron-phosphate pack pricing decreased by 31% year-over-year to USD 98 per kWh in 2025 and is projected to decline further to USD 72 per kWh by 2028.(2)Volta Foundation, “Battery Price Survey 2025,” volta-foundation.org Data centers now utilize batteries for the initial 30 minutes of outages, reserving gensets for prolonged events and reducing diesel consumption by 15-25%.

Stricter Urban Noise Ordinances on Standby Units

Chicago enforces a nighttime mechanical noise limit of 55 dB(A) at a distance of 100 feet. This regulation has led vendors to offer acoustic packages that lower noise levels by 10-25 dB, resulting in a 10-20% increase in installed costs. Additionally, the Better Buildings Partnership's "dark green" leases require quiet, low-emission backup power systems in densely populated urban areas.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fuel Type: Natural Gas Gains Despite Diesel Dominance

Natural gas is expected to grow at a compound annual growth rate (CAGR) of 11.4% by 2025, in contrast to diesel's 63.1% share of the commercial genset market. This shift is driven by operators aiming to avoid the expenses associated with Tier 4-Final after-treatment systems. Caterpillar’s 1.4 GW Atlas Energy agreement underscores this transition, while hydrogen-blending engines offer a potential route for long-term decarbonization. However, fluctuating LNG indices and the anticipated price tightening in 2027 complicate fuel-hedging strategies for buyers.

Diesel continues to play a critical role in rapid-start standby applications, particularly in hospitals and other life-safety facilities where gas pipeline access is limited. Vendors are addressing compliance costs by offering modular selective catalytic reduction (SCR) kits and ensuring compatibility with bio-diesel. Additionally, hybrid diesel-battery systems, tailored for telecom sites in regions such as Indonesia and Nigeria, incorporate automated load-tracking to enhance engine efficiency, minimize idle emissions, and extend maintenance intervals.

By Power Rating: Hyperscale Drives High-Capacity Growth

Generator sets above 750 kVA are projected to grow at a CAGR of 10.1%, driven by the demand from multimegawatt data center facilities requiring N+1 redundancy. Atlas Energy's record order for 4.5 MW modules highlights the increasing preference for containerized blocks that can scale up to 100 MW farms.

The mid-range segment of 75-750 kVA is expected to maintain its position as the volume leader, accounting for 49.7% of the market share by 2025. This segment primarily caters to office parks, hotels, and clinics, which are increasingly required to comply with stricter efficiency mandates similar to MEES. Meanwhile, portable units below 75 kVA face competition from battery alternatives. However, rural African 5G network expansions continue to specify 20-50 kW gensets due to grid uptime remaining at approximately 65%.

By Application: Prime Power Outpaces Standby Growth

Prime-power units experienced an annual growth rate of 9.6%, surpassing standby deployments, which accounted for 51.4% of shipments in 2025. This shift is driven by Sun Belt developers incorporating onsite generation during the design phase to avoid seven-year transmission delays. While standby power remains a requirement under healthcare and high-rise building codes, its share is gradually declining as batteries increasingly address short-duration interruptions.

Peak-shaving has emerged as an additional revenue source, with facilities in California and Texas incurring demand charges exceeding USD 18 per kW-month. These facilities utilize gas generators to reduce peak loads for 100-200 hours annually, achieving capital expenditure recovery within four years. Similarly, hybrid microgrids combine photovoltaic systems, lithium iron phosphate (LFP) batteries, and gas engines, managed by AI-based dispatch systems, to comply with green-lease requirements while maintaining system resilience.

By End-User Industry: Data Centers Sustain Leadership

Data centers accounted for 35.3% of 2025 shipments and are projected to grow at a CAGR of 8.5% through 2031. Approximately 73% of operators are incorporating onsite generation into campus designs. Commercial buildings and retail sectors follow, frequently opting for 500 kVA diesel generators equipped with hospital-grade mufflers to meet urban noise regulations.

The healthcare sector is upgrading aging fleets to gas-plus-battery hybrid systems, offering 96-hour autonomy in line with Joint Commission recommendations. In the telecom sector, power solutions for towers remain a localized growth area, particularly as Africa's mast installations increase. Hybrid solar-battery-generator systems in this segment provide payback periods of less than three years while reducing diesel consumption by over 60%.

Geography Analysis

Asia-Pacific is projected to hold the largest share of the commercial genset market, accounting for 45.2% in 2025. The growth is driven by India's server-farm expansion, influenced by AWS outages in the Gulf and a USD 40 billion hyperscaler capital expenditure, which is increasing demand in Tier-II cities such as Nagpur and Jaipur. Additionally, Chinese OEMs are gaining traction in mid-tier segments. In Southeast Asia, 5G network expansions, where grid extension costs can reach USD 50,000 per kilometer, are sustaining orders for gensets in the 30 kW-250 kW range.

North America is expected to record the fastest compound annual growth rate (CAGR) at 9.1% through 2031. Grid constraints in the Sun Belt region are driving high demand for prime-duty gensets. For instance, ERCOT's 226 GW project queue and Phoenix's 12% annual load growth highlight structural undersupply, fueling the deployment of multi-megawatt natural gas stations for AI fabs and chip manufacturing plants. In Canada, federal incentives are promoting hydrogen-ready retrofits, while Mexico's USD 20 billion nearshoring initiatives are channeling demand for 1,000 kVA gensets in Monterrey's industrial parks.

Europe is managing its high renewable energy adoption alongside Dunkelflaute risks. In Germany, office buildings are incorporating gas engines into building-scale microgrids. In the United Kingdom, landlords are addressing Minimum Energy Efficiency Standards (MEES) upgrades, which often include backup gensets to support HVAC electrification without requiring grid reinforcement. Nordic mines pilot 100% hydrogen units, and acoustic rules in Paris and Milan make low-noise canopies standard accessories.(3)Government of the United Kingdom, “Minimum Energy Efficiency Standards Consultation 2026,” gov.uk

Competitive Landscape

The commercial genset market demonstrates moderate concentration. Hybrid microgrid integrators, including Generac and Wärtsilä, are reducing the market share of pure diesel systems by incorporating Battery Energy Storage Systems (BESS) and Energy Management System (EMS) platforms. Caterpillar's USD 840 million acquisition of Atlas Energy, which includes 1.4 GW of gas engines, highlights the shift by original equipment manufacturers (OEMs) toward lower-carbon fuel solutions.

Suppliers are strategically diversifying into hydrogen-ready kits and artificial intelligence (AI)-based diagnostics. Wärtsilä’s GEMS 7 EMS manages multi-gigawatt-hour (GWh) storage systems, while Cummins’ acquisition of First Mode enhances its hybrid mining equipment portfolio. Cost-competitive Asian brands, such as Mahindra Powerol, Kirloskar, and Himoinsa, capitalize on price advantages in the sub-250 kVA segment, particularly in regions like Africa and Latin America.

Emerging players, such as Mainspring Energy and Jubaili Bros, are introducing flexible linear generators and diesel-battery hybrid systems that claim fuel savings of 30-70%. Rental companies like Aggreko and United Rentals are integrating IoT sensors to reduce truck rolls, with each avoided service call saving an average of USD 800. Overall, competition in the market is increasingly driven by fuel flexibility, digital service offerings, and adherence to urban acoustic and emission regulations.

Commercial Genset Industry Leaders

Caterpillar Inc.

Cummins Inc.

Generac Holdings Inc.

Kohler Co.

Rolls-Royce Power Systems

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Cummins in India introduced its CPCBIV+ compliant 82.5 kVA genset at the CII EXCON 2025. The genset features a compact design, improved fuel efficiency, and optimized performance, providing a reliable and cleaner power solution tailored to the growing demands of India’s quick-commerce, construction, and infrastructure markets.

- April 2025: Generac acquired Deep Sea Electronics, expanding advanced control capabilities for natural-gas sets and microgrids.

- March 2025: Cummins completed Project Brunel, unveiling a 6.7-liter hydrogen engine with 99% tailpipe carbon reduction.

- March 2025: Caterpillar debuted the C13D engine at Bauma Munich, offering 340–515 kW with renewable-fuel support.

Global Commercial Genset Market Report Scope

A commercial genset (generator set) is a robust power unit designed to supply backup or primary electricity to commercial facilities, including offices, retail spaces, restaurants, and smaller industrial sites. These units typically combine a diesel or natural gas engine with an alternator, serving as an intermediate solution between small residential generators and large industrial generators.

The Global Commercial Genset Market is segmented into fuel type, power rating, application, end-user industry, and geography. By fuel type, the market is segmented into diesel, natural gas, dual-fuel and hybrid, and others. By power rating, the market is segmented into below 75 kVA, 75 to 750 kVA, and above 750 kVA. By application, the market is segmented into standby power, prime/continuous power, peak-shaving, rental/temporary power, and micro-grid and hybrid support. By end-user industry, the market is segmented into commercial buildings, data centers, healthcare, hospitality, education, telecom, airports, and others. The report also covers the market size and forecasts for the commercial genset market in 18 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Diesel |

| Natural Gas |

| Dual-Fuel and Hybrid |

| Others (Renewable/Bio-fuel, LPG, Hydrogen-ready, etc.) |

| Below 75 kVA |

| 75 to 750 kVA |

| Above 750 kVA |

| Standby Power |

| Prime/Continuous Power |

| Peak-Shaving |

| Rental/Temporary Power |

| Micro-grid and Hybrid Support |

| Commercial Buildings (Offices, Retail, Malls) |

| Data Centers |

| Healthcare Facilities |

| Hospitality (Hotels & Resorts) |

| Education Institutions |

| Telecom (Towers, Edge POPs) |

| Airports & Transportation Hubs |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Fuel Type | Diesel | |

| Natural Gas | ||

| Dual-Fuel and Hybrid | ||

| Others (Renewable/Bio-fuel, LPG, Hydrogen-ready, etc.) | ||

| By Power Rating | Below 75 kVA | |

| 75 to 750 kVA | ||

| Above 750 kVA | ||

| By Application | Standby Power | |

| Prime/Continuous Power | ||

| Peak-Shaving | ||

| Rental/Temporary Power | ||

| Micro-grid and Hybrid Support | ||

| By End-user Industry | Commercial Buildings (Offices, Retail, Malls) | |

| Data Centers | ||

| Healthcare Facilities | ||

| Hospitality (Hotels & Resorts) | ||

| Education Institutions | ||

| Telecom (Towers, Edge POPs) | ||

| Airports & Transportation Hubs | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2026 value of the commercial genset market?

The commercial genset market size stands at USD 14.38 billion in 2026.

Which end-user vertical buys the most commercial gensets?

Data centers lead demand, holding 35.3% share in 2025 and expanding at an 8.5% CAGR through 2031.

Why are natural-gas gensets gaining traction over diesel?

Tier 4-Final and Stage V rules raise diesel ownership costs by up to 30%, while gas units avoid particulate filters and emit 25% less CO₂.

How fast are battery prices falling compared with genset costs?

Lithium-iron-phosphate pack prices dropped 31% in 2025 to USD 98 per kWh and could hit USD 72 by 2028, compressing gensets’ cost advantage for short-duration backup.

Which region posts the quickest growth?

North America, driven by Sun Belt grid bottlenecks, is projected to record a 9.1% CAGR through 2031.

What fuels are emerging beyond diesel and natural gas?

Hydrogen-ready engines that run on or blend H₂ are entering commercial service, alongside LPG and biofuel units for niche applications.

Page last updated on: