Aerospace Bearings Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 12 Billion |

| Market Size (2031) | USD 13.99 Billion |

| Growth Rate (2026 - 2031) | 3.12% CAGR |

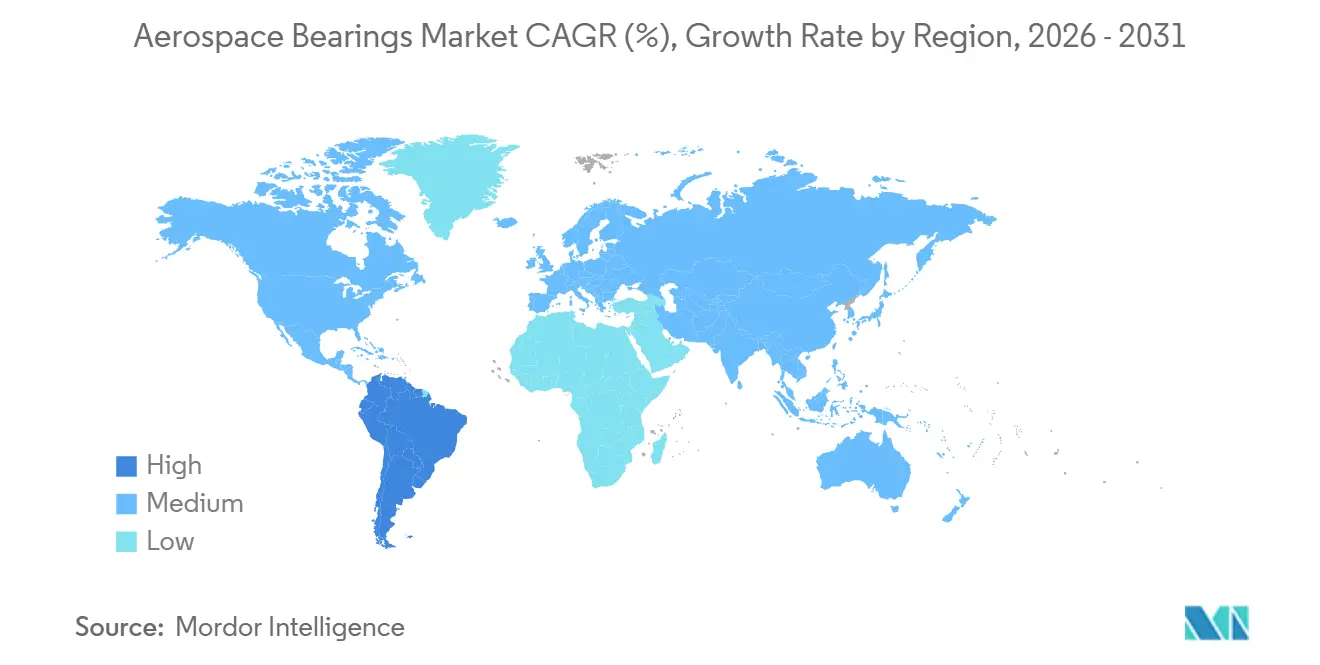

| Fastest Growing Market | South America |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aerospace Bearings Market Analysis by Mordor Intelligence

The aerospace bearings market is expected to grow from USD 11.66 billion in 2025 to USD 12.00 billion in 2026 and to reach USD 13.99 billion by 2031, at a 3.12% CAGR over 2026-2031. Fleet expansion programs, the adoption of advanced materials, and the shift toward electric actuation strengthen demand across commercial, defense, and space platforms. Boeing anticipates 43,975 new commercial aircraft deliveries by 2043, and this backlog is pushing bearing suppliers to raise output while maintaining strict aerospace quality standards. Lightweight composite and ceramic bearings are gaining share because they help cut fuel burn and extend maintenance intervals. Meanwhile, consolidation among key vendors and an intensified focus on supply-chain resilience shape competitive strategies.

Key Report Takeaways

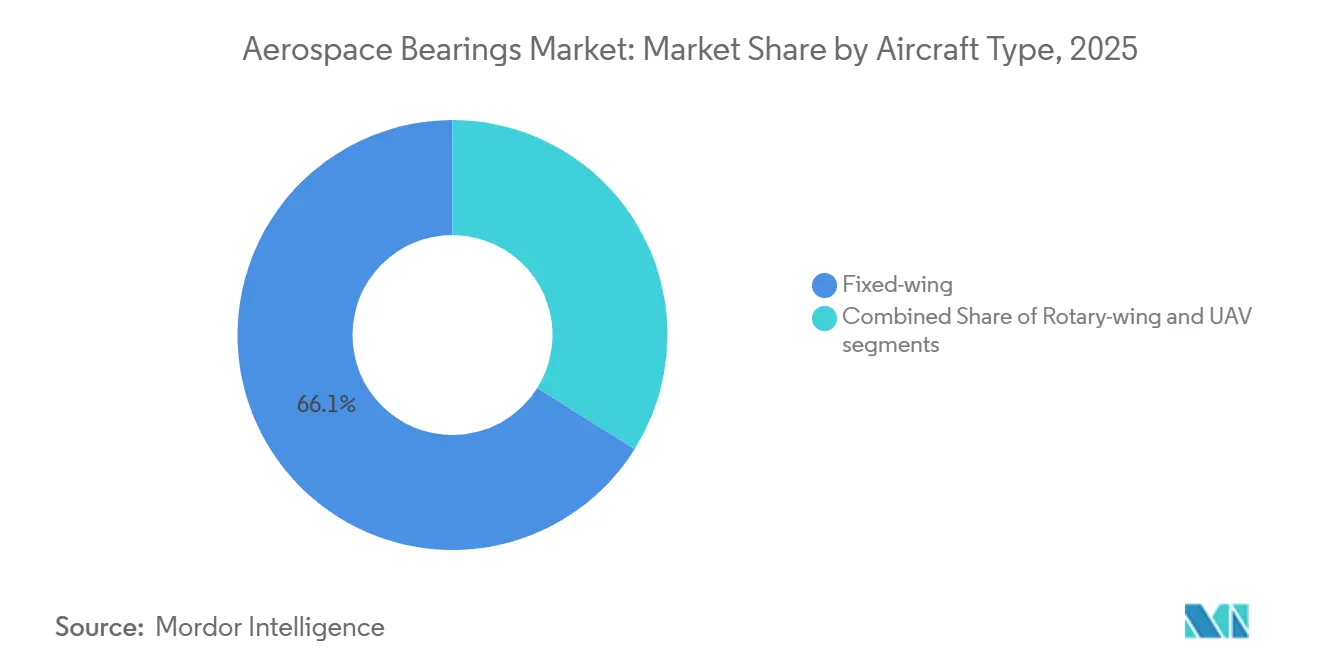

- By aircraft type, fixed-wing aircraft accounted for 66.10% of revenue in 2025, and unmanned aerial vehicles are forecast to expand at a 9.62% CAGR through 2031.

- By product type, ball bearings led with a 41.17% share in 2025, while roller bearings are projected to grow at a 3.38% CAGR through 2031.

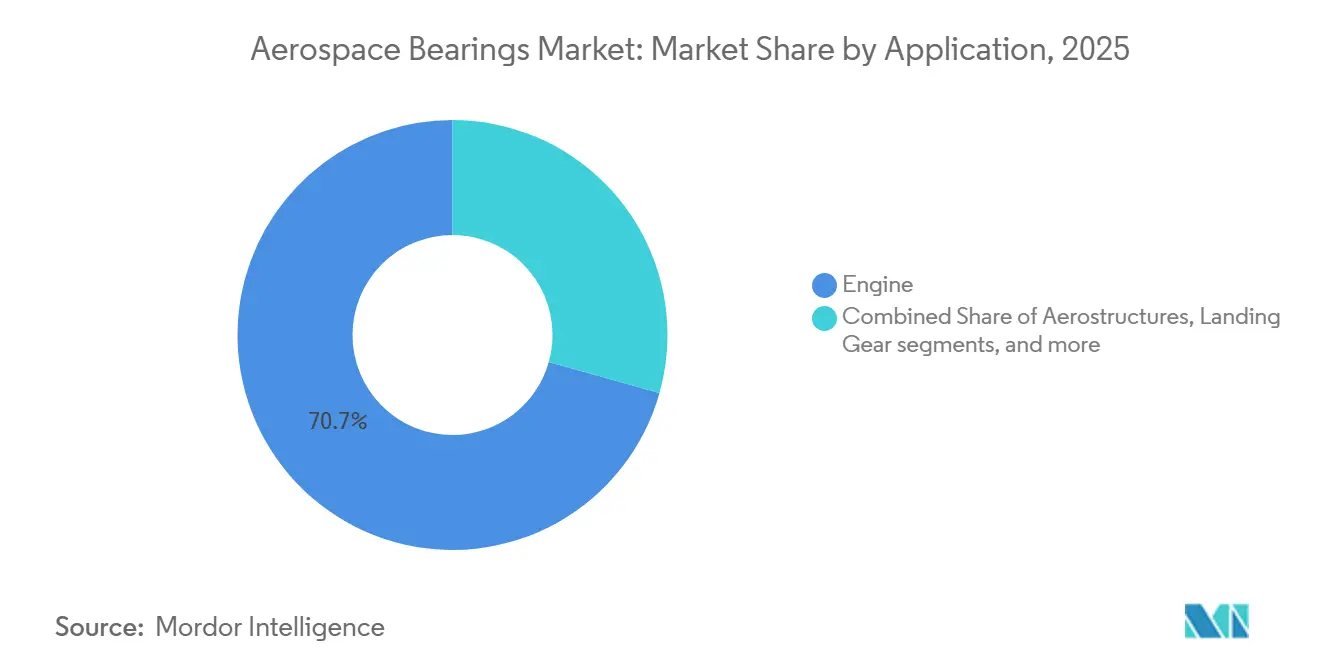

- By application, engine systems accounted for 70.65% of the aerospace bearings market in 2025, and aerostructures are projected to advance at a 3.45% CAGR through 2031.

- By material, metal bearings captured a 65.76% share in 2025; metal-polymer and engineered plastics are forecast to grow at a 3.83% CAGR to 2031.

- By sales channel, the aftermarket accounted for 64.93% of the aerospace bearings market share in 2025, whereas the OEM segment is forecast to grow at a 5.57% CAGR.

- By region, North America dominated with a 33.15% share in 2025; South America is forecast to grow at a 3.40% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aerospace Bearings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging global commercial aircraft fleet | +1.8% | Global, led by Asia-Pacific and Middle East | Medium term (2-4 years) |

| Light-weighting imperatives in next-gen programs | +1.2% | North America and Europe, expanding worldwide | Long term (≥4 years) |

| Defense rotorcraft life-extension budgets | +0.9% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Boom in small-sat and launch vehicles | +0.7% | United States, Europe, China | Short term (≤2 years) |

| Electrified flight-control actuation demand | +0.6% | Global, headed by North America and Europe | Long term (≥4 years) |

| Advanced air-mobility (eVTOL) proliferation | +0.4% | North America, Europe, selected Asia-Pacific markets | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Surging Global Commercial Aircraft Fleet

Boeing projects that single-aisle jets will form 76% of future deliveries, creating large-volume, standardized bearing requirements that support economies of scale. Order backlogs exceed 17,000 units, giving OEMs with local plants in Asia-Pacific a scheduling advantage.[1]The Boeing Company, “Commercial Market Outlook 2024,” boeing.com SKF is investing SEK 400 million (USD 42.22 million) in China to boost ball-bearing output to capitalize on this opportunity. Suppliers that offer rapid certification support gain preferred status because OEMs cannot risk production delays. Capacity expansions must also align with government mandates on domestic content, which shape sourcing decisions.

Light-weighting Imperatives in Next-gen Programs

Silicon-nitride rolling elements weigh 40% less than steel and deliver longer fatigue life, a critical benefit for high-bypass engines operating near thermal limits. NASA demonstrated nickel-titanium-hafnium bearings that meet grade 10 ABEC tolerances while cutting weight, targeting corrosion-prone locations. GE Aerospace is scaling ceramic-matrix composites after injecting more than USD 100 million into US pilot lines in 2025.[2]GE Aerospace, “Composite Materials Expansion,” geaerospace.com Composite cages resist high temperatures yet require multi-year qualification programs, slowing time-to-market. Despite longer certification cycles, airlines prioritize fuel burn savings, reinforcing demand.

Defense Rotorcraft Life-extension Budgets Rising

The US Army’s T901 engine integrates advanced bearings produced via additive manufacturing to extend the service life of the Black Hawk and Apache. NATO partners evaluate Sikorsky’s X2 coaxial designs, channeling over USD 1 billion into rotorcraft upgrades.[3]Lockheed Martin, “Next Generation Rotorcraft Capability,” lockheedmartin.com Rotor gearboxes endure oscillatory loads, so suppliers develop self-lubricating coatings and real-time wear sensors. Condition-based maintenance systems from New Hampshire Ball Bearings help fleets avoid unscheduled downtime by detecting spall growth early.

Boom in Small-sat and Launch Vehicles

Low-Earth-orbit (LEO) constellations demand bearings that operate in a vacuum and withstand radiation without lubrication. NASA validated 60NiTi spherical sliders for zero-lubricant operation during extended orbital periods. SpaceX’s reusable boosters push bearings through rapid cycles of cryogenic chill, extreme acceleration, and sea-salt exposure upon recovery. Manufacturers counter vibration with duplex pair configurations and precision preload control. Cost-driven launch markets spur modular bearing platforms that fit multiple vehicle classes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile specialty alloy and rare-earth prices | –0.8% | Global, acute in North America and Europe | Short term (≤2 years) |

| Lengthy FAA/EASA certification cycles | –0.6% | Global, most restrictive in North America and Europe | Medium term (2-4 years) |

| Emergence of magnetic and air-foil bearing tech | –0.4% | North America and Europe initially, expanding worldwide | Long term (≥4 years) |

| Aerospace-grade powder supply-chain bottlenecks | –0.5% | Global, concentrated in advanced manufacturing regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Specialty Alloy and Rare-earth Prices

Titanium prices swing sharply as geopolitics disrupt Russian supply routes, squeezing margins for forged rings and races. Rhenium trades near USD 1,200-1,800 per kg and remains critical for high-temperature superalloys that power widebody engines. The Pentagon now mandates dual sourcing of critical minerals to cut reliance on adversarial nations, compelling suppliers to diversify procurement. Bearing firms explore recycling loops that could meet 30% of rhenium demand by 2025.

Lengthy FAA/EASA Certification Cycles

New designs undergo TSO testing that may last 7 years, especially as additive manufacturing enters safety-critical zones.[4]FAA, “Additive Manufacturing Guidance,” faa.gov Dual approvals from the FAA and EASA add document redundancy and drive costs. Smaller firms often lack dedicated regulatory teams, which delays commercialization. The market answers with early joint reviews in pre-design phases, yet the fundamental timeline still reduces ROI for breakthrough materials.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Aircraft Type: UAVs Drive Next-generation Demand

Fixed-wing aircraft contributed 66.10% of the aerospace bearings market revenue in 2025, anchored by high-volume single-aisle programs that standardize bearing part numbers for engines, landing gear, and control surfaces. Multi-sourcing agreements improve resilience, but each supplier must pass stringent PPAP and AS9100 audits before line fitment. The aerospace bearings market benefits from synchronized production schedules across North American and Asian final-assembly lines, which lowers logistics risk.

Unmanned aerial vehicles (UAVs) are projected to post the strongest 9.62% CAGR to 2031 as militaries and commercial operators adopt long-endurance drones for ISR and cargo roles. These platforms need bearings that resist electromagnetic interference around high-power electronics. The aerospace bearings market size for UAV actuation systems is projected to expand steadily as fleets migrate from prototype to mass production.

By Product Type: Roller Bearings Gain Traction

Ball bearings held a 41.17% share in 2025, remaining the baseline solution for radial and axial loads across most rotating groups. OEMs approve design families once, enabling long production runs that protect volume. Roller bearings are forecast to grow at a 3.38% CAGR, driven by the demand for precise linear motion from electrified flight-control actuators. Hybrid ceramic-steel designs cut weight while maintaining stiffness, strengthening the outlook for roller screws in the aerospace bearings market.

Plain bearings persist in high-temperature zones of turbomachinery, whereas tapered roller sets handle extreme landing-gear shocks. Additive manufacturing will lift complex one-piece bearing-cage geometries that optimize lubrication paths. The aerospace bearings market is seeing greater differentiation between commodity ball bearings and application-specific roller screw assemblies.

By Application: Aerostructures Showcase Significant Growth

Engines accounted for 70.65% of 2025 revenues because each turbofan contains hundreds of precision bearings that must withstand temperatures above 400°C. Predictive analytics shorten time-on-wing by flagging spall initiation via vibration signatures. The aerospace bearings market size remains anchored to engine build rates, which climb as airlines favor fuel-efficient variants.

The aerostructures segment will grow at a 3.45% CAGR through 2031. These bearings play a crucial role in ensuring safety, facilitating flight control maneuverability, and maintaining structural stability. The growing emphasis on aircraft safety and maintenance is a primary driver of demand for bearings in doors and access panels. Foil-magnetic hybrids could eliminate oil and set new reliability benchmarks. Ancillary applications such as APU starter generators and environmental-control blowers maintain stable demand.

By Material: Composites Lead Innovation

Metallic solutions secured a 65.76% share in 2025 because steel and titanium continue to deliver proven life at an economical cost. Powder-bed fusion permits optimized grain structures that raise contact fatigue strength. In parallel, metal-polymer and engineered plastics are forecast to grow at a 3.83% CAGR through 2031. Weight reduction and maintenance-free solutions are critical drivers in aerospace applications, as they directly impact efficiency and cost-effectiveness. For instance, TriStar's Ultracomp UC 200 polymer bearings address this demand with a compressive strength of 54,000 psi, tailored for high-load pivot points, fuselage joining fixtures, landing gears, and gear doors. Their advanced polymer composite construction reduces weight compared to traditional metal bearings, provides corrosion resistance, and eliminates the need for lubrication. Similarly, these innovations align with the industry's focus on enhancing operational efficiency and reducing long-term costs, making them indispensable for modern aerospace systems.

By Sales Channel: Aftermarket Dominated the Market

Aftermarket accounted for 64.93% of the aerospace bearings market share in 2025 because fleets age and operators stretch service life amid supply-chain constraints. DER-approved repairs from Barden Corporation cut replacement costs by up to 35%, making overhauled units attractive. Predictive maintenance platforms mine flight data to forecast bearing replacement windows. That visibility helps MROs plan inventory and lowers unscheduled removals. As digital twins mature, the size of the aerospace bearings market for analytics-enabled spares could exceed earlier forecasts.

The OEM segment delivers the faster 5.57% CAGR because every new aircraft integrates a large bill of materials of certified bearings. Production ramp-ups at Airbus and COMAC will uphold OEM demand through 2031.

Geography Analysis

North America accounted for 33.15% of revenue in 2025, driven by increased aircraft production, engine manufacturing, and a growing aftermarket fueled by extended fleet usage. It is home to the largest pool of certified bearing plants. GE Aerospace plans to invest nearly USD 1 billion in US facilities in 2025, boosting ceramic-matrix composite throughput.

South America will be the fastest-growing region, with a CAGR of 3.40% during 2026-2031. Brazil is the most developed aerospace manufacturing hub in Latin America, supported by a robust domestic OEM and an expanding supplier network. The industry is dominated by Embraer, a leading global producer of regional jets and a significant player in business aviation. Unlike many other emerging markets, Brazil possesses comprehensive aircraft manufacturing capabilities, including design, assembly, and integration.

Rapid growth in air traffic and domestic manufacturing policies are fueling the Asia-Pacific's expansion. In China, local procurement of bearings is spearheaded by COMAC, whereas in India, the private sector is bolstering its capabilities through global asset acquisitions. Japanese firms supply ultra-precision races used in regional jet programs. South Korea and Australia expand maintenance hubs that attract regional overhaul work. Europe advances sustainable aviation programs that integrate hybrid-electric propulsion, pushing bearing suppliers to refine high-speed ceramic designs.

The Middle East is expected to record moderate growth as sovereign funds allocate capital to defense procurement and industrial offsets. Tawazun Precision Industries partners with Boeing to operate a surface-treatment plant that anchors bearing-finishing activities in Abu Dhabi. Moreover, Saudi Arabia's Vision 2030 earmarks aerospace as a pillar of economic diversification, boosting regional demand.

Competitive Landscape

The aerospace bearings market is moderately consolidated. SKF, Timken, and Schaeffler each sustain global networks of AS9100 facilities and deepen vertical integration through acquisitions. SKF divested a non-core US plant for USD 220 million and purchased John Sample Group’s lubrication assets to bundle bearings with flow-management systems. Timken expands into high-speed spindle bearings for composite machining centers. Schaeffler integrates Vitesco Technologies to co-develop electromobility solutions that cross-pollinate into the aerospace industry.

Disruptive entrants focus on magnetic and air-foil bearings that remove oil circuits. Spin-outs from university laboratories secure defense research grants to mature hybrid designs with triple load capacity. Barriers to entry remain high because certification tests cost tens of millions of dollars. Partnerships with eVTOL integrators offer new routes to revenue. Competitive differentiation now rests on weight saving, predictive maintenance readiness, and supply chain localization.

Aerospace Bearings Industry Leaders

AB SKF

The Timken Company

NSK Ltd.

RBC Bearings Incorporated

Schaeffler AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: South African Airways announced its plans to expand its fleet to 25 aircraft by the end of 2026, up from its significantly reduced fleet following restructuring. This expansion aims to restore regional and international connectivity, enhance aircraft utilization, and drive demand for maintenance-intensive components, including bearings.

- November 2025: AB SKF introduced ARCTIC15, a bearing steel that enables compact solutions with higher load capacity, supporting next-generation aircraft engines designed to reduce emissions by up to 25% and aligning with advancements in aerospace engineering requirements.

- June 2025: The Timken Company announced advancements in aerospace bearings for electric and next-generation aircraft. The company emphasized hybrid ceramic bearings designed to enhance electric flight and improve traditional aviation. These ceramic hybrid roller bearings, engineered for reduced weight and extended lifespan, are integral to next-generation aircraft designs and align with evolving aerospace requirements.

- March 2025: The Boeing Company and AB SKF Aerospace announced the expansion of their partnership, with Boeing’s distribution business becoming an authorized distributor for AB SKF Aerospace bearings. Under this agreement, Boeing Distribution Services will be listed in D1-4426 as an approved distributor of AB SKF’s bearings.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study counts the value of every new, flight-qualified bearing fitted to fixed-wing aircraft, helicopters, and UAVs, covering engines, landing gear, flight-control actuation, cabin, and door mechanisms.

Scope exclusion: bearings sold only as aftermarket repair kits or used on space vehicles or ground test benches sit outside the boundary.

Segmentation Overview

- By Aircraft Type

- Fixed-wing

- Rotary-wing

- Unmanned Aerial Vehicles (UAVs)

- By Product Type

- Plain Bearings

- Roller Bearings

- Ball Bearings

- Roller Screws

- Ball Screws

- By Application

- Engine

- Aerostructures

- Landing Gear

- Flight Control and Actuation

- Others

- By Material

- Metal

- Ceramic

- Metal-Polymer and Engineered Plastics

- Fiber-Reinforced Composites

- By Sales Channel

- Original Equipment Manufacturer (OEM)

- Aftermarket

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- France

- Germany

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Rest of the Middle East

- Africa

- Egypt

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Our analysts interviewed procurement heads at OEMs, aftermarket distributors in Asia, and design engineers in Europe and North America. Their guidance confirmed unit counts, regional ASPs, and the pace at which ceramic hybrids replace metal races.

Desk Research

We start with open datasets. Airframe production totals come from FAA, EASA, and Boeing and Airbus delivery files, while UN Comtrade codes reveal shipment values. Peer-reviewed tribology journals flag service-life trends, and company 10-Ks show bearing revenue splits. Paid resources, notably D&B Hoovers and Factiva, verify supplier margins. The list is illustrative, and many additional public records reinforce each datapoint.

Market-Sizing and Forecasting

Mordor's model begins with a top-down build: annual aircraft deliveries multiplied by standard bearing counts and regional ASPs. Select bottom-up checks, supplier revenue slices, and sampled invoices validate totals. Key variables include build rates, fleet hours, composite penetration, overhaul cycles, and defense budgets. Multivariate regression with ARIMA overlays projects the series to 2030. Where disclosures are partial, historical ASP dispersion fills gaps.

Data Validation and Update Cycle

Our outputs pass a two-level peer review. Variances above five percent against external metrics trigger re-checks. The model refreshes yearly, with interim updates after material program shifts.

Why Mordor's Aerospace Bearing Baseline Commands Reliability

Estimates differ because publishers stretch or shrink scope, apply assorted exchange rates, and refresh at uneven intervals. Our disciplined variable selection and annual audit keep the baseline steady yet responsive.

Key Gap Drivers: external figures often fold in cabin spares, omit UAVs, or carry forward pre-pandemic exchange rates. Others extrapolate straight lines, while Mordor Intelligence folds live build-rate guidance and material-mix shifts into every update.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 12.28 B (2025) | Mordor Intelligence | - |

| USD 13.01 B (2024) | Global Consultancy A | Includes MRO software and interior spares |

| USD 18.20 B (2024) | Global Consultancy B | Uses wider aerospace parts basket |

| USD 1.80 B (2024) | Industry Journal C | Counts only OE bearings for large jets |

The comparison shows Mordor's balanced scope yields a transparent, repeatable baseline rooted in measurable aircraft build data.

Key Questions Answered in the Report

What is the value of the aerospace bearings market in 2026 and how fast is it growing?

The market stands at USD 12.00 billion in 2026 and is forecasted to expand at a 3.12% CAGR to reach USD 13.99 billion by 2031.

Which region leads the aerospace bearings market today?

North America accounted for 33.15% of global revenue, driven by large-scale aircraft production and fleet expansion in the US and Canada.

Which platform type is expected to grow the fastest through 2031?

Unmanned aerial vehicles (UAVs) show the highest growth outlook, advancing at an 9.62% CAGR as defense and commercial operators scale drone fleets.

How is aircraft electrification influencing bearing demand?

Electric flight-control actuation is pushing adoption of high-precision roller screws and hybrid foil-magnetic bearings that lower weight and remove oil circuits.

What key challenges could restrain market growth?

Volatile prices for titanium and rare-earth elements and lengthy FAA/EASA certification cycles together shave roughly 1.4 percentage points off the market’s forecast CAGR.

Page last updated on: