Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

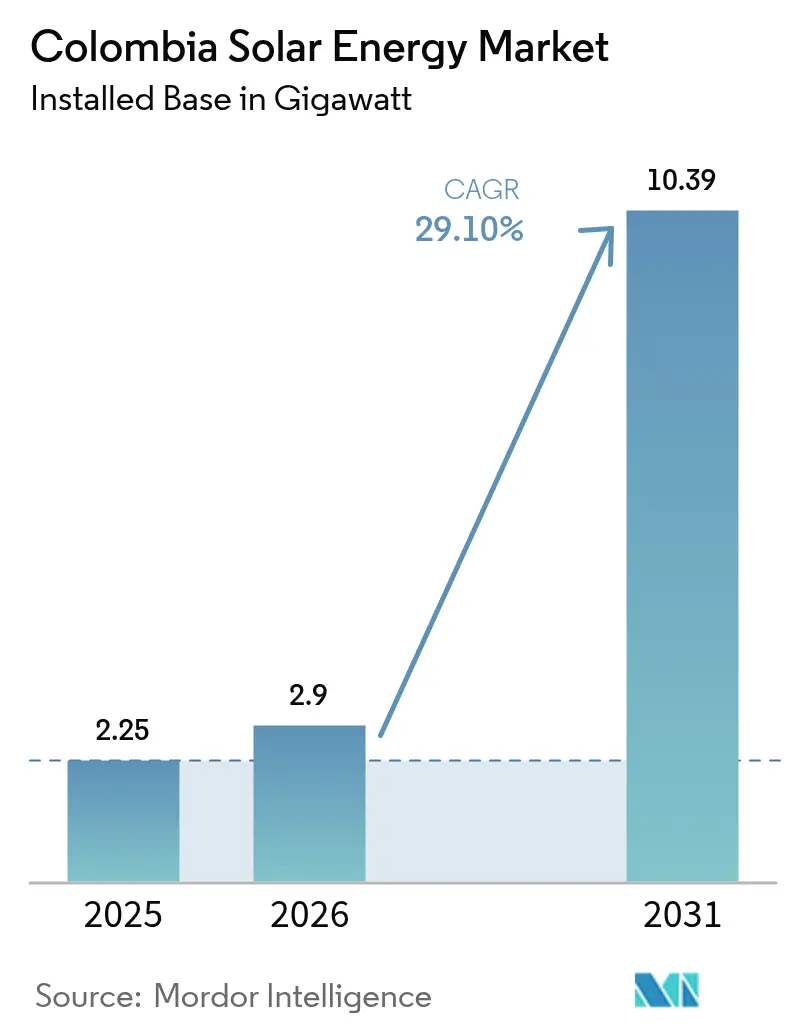

| Base Year Market Size (2025) | 2.25 gigawatt |

| Market Volume (2026) | 2.9 gigawatt |

| Market Volume (2031) | 10.39 gigawatt |

| Growth Rate (2026 - 2031) | 29.10% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Colombia Solar Energy Market Analysis by Mordor Intelligence

The Colombia Solar Energy Market size was valued at 2.25 gigawatt in 2025 and estimated to grow from 2.9 gigawatt in 2026 to reach 10.39 gigawatt by 2031, at a CAGR of 29.10% during the forecast period (2026-2031).

This forecast highlights the Colombia solar energy market size trajectory and underscores the country’s growing role within Latin American renewables. Growth reflects a deliberate pivot away from hydropower following a 23% price spike in April 2024, driven by El Niño, which exposed hydro variability risks and accelerated demand for new generation sources.[1]Daniela Morales Soler, “Alza de precios eléctricos tras El Niño,” portafolio.co Rapid deployment is evident, as installed solar capacity surpassed the 1 GW mark in 2024, with an additional 952 MW added since early 2023 across both grid-connected and off-grid systems. Declining levelised costs, VAT exemptions under Law 1715, and streamlined auctions continue to draw international developers to the Colombia solar energy market. Government support for green-hydrogen projects, which rely on abundant low-cost solar electricity, further widens long-term demand for the Colombia solar energy market.

Key Report Takeaways

- By grid type, on-grid installations held 71.80% of the Colombia solar energy market share in 2025, while off-grid capacity is forecast to expand at a 34.20% CAGR through 2031.

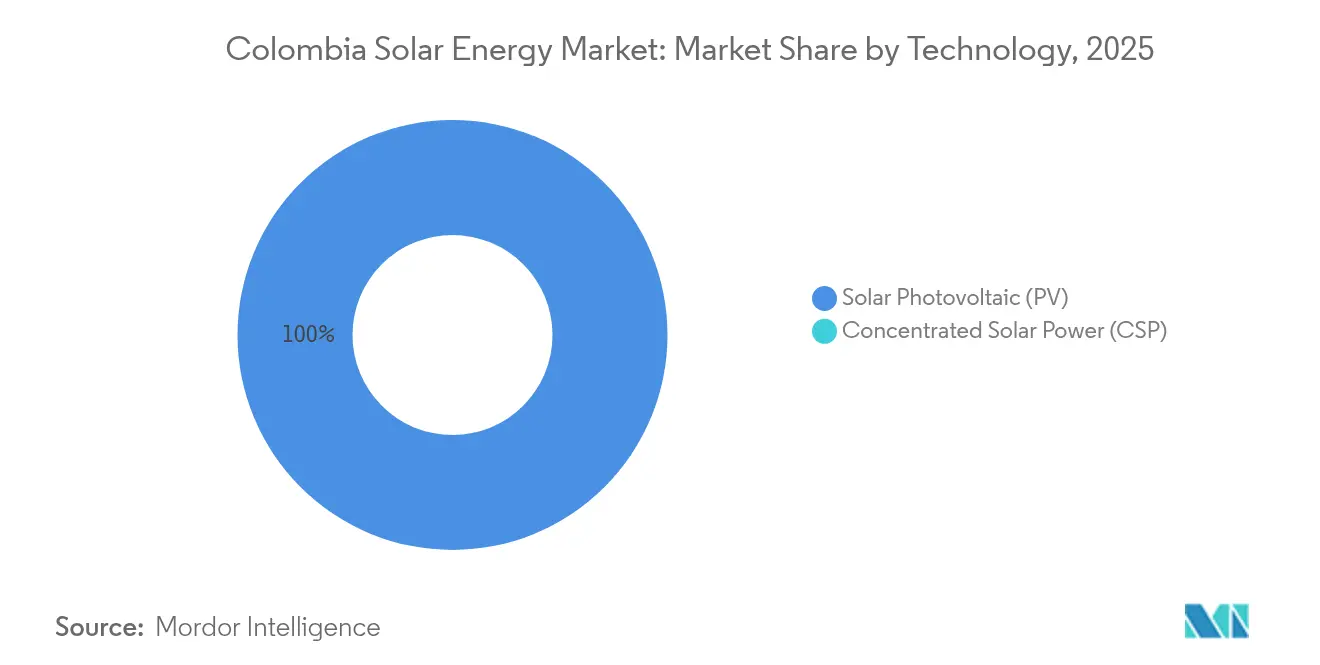

- By technology, Solar PV captured 100.00% of installed capacity in 2025 and is expected to maintain its lead with a 29.60% CAGR through 2031.

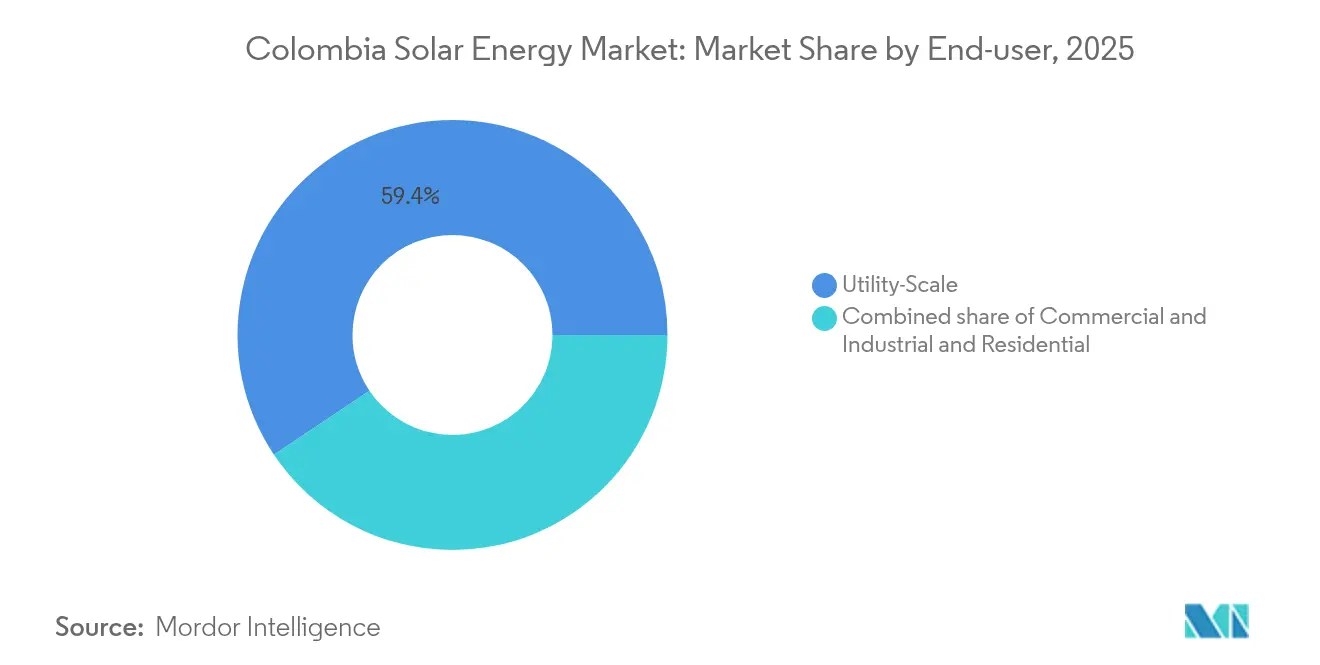

- By end user, utility-scale plants accounted for 59.40% of the Colombia solar energy market size in 2025, whereas residential capacity is projected to grow at a 32.10% CAGR to 2031.

- Atlántico, Cesar, and Córdoba contributed 54% of the 2024 additions, while Tolima and Cundinamarca, together, hold 73% of the capacity planned for 2025.

- Enel Colombia, Celsia, and Atlas Renewable Energy together controlled 35% of national solar output in 2024.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Colombia Solar Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Falling levelised cost of PV electricity | 8.2% | National, with early gains in Caribbean coast | Medium term (2-4 years) |

| Net-metering incentives for small self-generators | 5.8% | Urban centers, particularly Bogotá, Medellín, Cali | Short term (≤ 2 years) |

| Corporate PPAs from mining & data-centre sectors | 6.4% | Mining regions (Cesar, La Guajira), urban data centers | Medium term (2-4 years) |

| Green-hydrogen linkage raising solar demand | 4.9% | La Guajira, Caribbean coast industrial zones | Long term (≥ 4 years) |

| Digitised O&M lowering operating risk | 2.7% | Large-scale utility projects nationwide | Medium term (2-4 years) |

| Accelerated grid-connection process for <5 MW | 3.5% | Distributed generation markets nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Falling Levelised Cost of PV Electricity

Utility projects now post LCOE below USD 0.10/kWh, undercutting diesel generation that dominates non-interconnected zones. Local distribution hubs established by global module vendors reduce logistics premiums, while the European Investment Bank's financing of Enel Colombia's 486 MW portfolio demonstrates investor confidence in continued cost declines.[2]European Investment Bank, “Loan to Enel Colombia,” eib.org Bifacial panels in La Loma raise annual yield and reinforce the cost advantage of the Colombia solar energy market.

Net-Metering Incentives for Small Self-Generators

Decree 348 streamlines interconnection and guarantees credit for exported surplus, shrinking rooftop payback periods to 11.3-13.8 years. Banco de Bogotá offers low-cost financing for residential arrays, and distribution utilities deploy smart meters to support bidirectional flows.[3]Comisión de Regulación de Energía y Gas, “Decreto 348,” creg.gov.co

Corporate PPAs from Mining & Data-Centre Sectors

After the 2024 price spike, mining operators have secured long-term solar PPAs to hedge against volatility, exemplified by PazdelRío’s 9.9 MW deal, which cuts 2,268 t of CO₂ annually. Hyperscale data centre operators demand renewable certificates, spurring the development of tailored contract structures permitted by Colombia’s open-access regulations.

Green-Hydrogen Linkage Raising Solar Demand

The national roadmap, targeting 1.9 million tonnes of annual hydrogen demand by 2050, requires gigawatts of new solar capacity. Ecopetrol pilots confirm technical viability at La Guajira, where high irradiation supports round-the-clock electrolyser operations. Export-oriented offtake agreements underpin large solar clusters dedicated to hydrogen production.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Land-use conflicts in La Guajira | -4.2% | La Guajira department, indigenous territories | Medium term (2-4 years) |

| Transmission bottlenecks on Caribbean coast | -2.8% | Caribbean coastal departments | Short term (≤ 2 years) |

| Peso depreciation raising module import costs | -2.4% | National, affecting all import-dependent projects | Short term (≤ 2 years) |

| Community opposition driven by indigenous consultation gaps | -3.3% | Indigenous territories, primarily La Guajira | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Land-Use Conflicts in La Guajira

Wayuu communities have halted major wind projects and are extending scrutiny to large solar arrays that overlap grazing lands and sacred sites, causing Celsia and Enel to suspend developments and negotiate higher royalty frameworks. Cultural consultation gaps raise reputational risk and complicate timelines despite a new 6% royalty proposal designed to share economic benefits.[4]Alexander Iñigo, “Indigenous resistance in La Guajira,” theguardian.com

Transmission Bottlenecks on Caribbean Coast

The delayed Colectora line limits the evacuation of 6 GW of renewables slated for La Guajira, forcing developers to stagger commissioning schedules or fund costly grid upgrades. Concentrated build-out stress-tests legacy networks originally designed for dispersed thermal plants, pressing authorities to accelerate new 500 kV corridors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Solar PV Sustains Total Market Leadership

Solar PV accounted for 100.00% of installed capacity in 2025. Crystalline-silicon modules dominate due to their high efficiency and extensive global supply chain. The Colombia solar energy market continues to adopt bifacial panels, single-axis trackers, and digital O&M systems that reduce downtime. Concentrated Solar Power remains absent due to higher costs and water requirements, despite irradiation levels exceeding 4.5 kWh/m² per day.

Utility developers integrate storage to improve capacity factors, while distributed systems incorporate smart inverters that manage bidirectional flows under net metering. Continuous cost compression supports a 29.60% CAGR for Solar PV through 2031 within the Colombia solar energy market.

By Grid Type: Off-Grid Growth Accelerates Rural Access

On-grid capacity commanded 71.80% of installations in 2025. Off-grid momentum rises with a 34.20% CAGR outlook, propelled by the Light for the Amazon program targeting 228,000 homes where diesel costs top USD 0.30/kWh. Hybrid mini-grid configurations combine solar, batteries, and backup generators to ensure reliability in remote areas such as Putumayo and Vichada.

International donors and government subsidies improve affordability, and new business models attract private capital to the Colombia solar energy market’s off-grid segment.

By End User: Residential Installations Lead Future Growth

Utility-scale assets held 59.40% of the Colombia solar energy market share in 2025, anchored by 4.4 GW of auction-backed PPAs. Commercial and industrial buyers sign bespoke PPAs to secure stable pricing. Residential capacity is expected to show the highest growth outlook at a 32.10% CAGR through 2031, driven by net-metering and the USD 10 billion Colombia Solar program, which subsidizes low-income households.

Solar-as-a-service models further lower barriers by spreading upfront costs over multi-year service contracts. Attractive payback periods of 11-14 years motivate middle-income adoption, adding depth to the Colombia solar energy market.

Geography Analysis

Solar build-out concentrates along the Caribbean coast, where Atlántico, Cesar, and Córdoba delivered 54% of added capacity in 2024, benefiting from irradiation above 4.5 kWh/m² day and proximity to existing 500 kV lines. La Guajira hosts marquee projects such as Enel’s 370 MW Guayepo complex, though indigenous land conflicts and grid bottlenecks have delayed 82% of regional pipelines.

Interior departments are gaining traction as developers diversify to mitigate coastal congestion. Tolima anchors Atlas Renewable Energy’s 201 MW Shangri-La plant, while Cundinamarca and Tolima, together, represent 73% of the capacity scheduled for 2025 commissioning, reflecting streamlined permitting and lower social conflict risk. The Colombia solar energy market size for interior regions is projected to rise at double-digit rates, underscoring the geographic broadening of investment flows.

Remote Amazonian and Orinoquia departments present high-margin opportunities for distributed solar, replacing diesel generation that costs above USD 0.30/kWh in non-interconnected zones. Bogotá, Medellín, and Cali continue to lead rooftop installations under net metering, confirming the critical mass of urban markets. Geographic diversification buffers systemic risk and aligns Colombia’s decarbonisation goals with inclusive regional development.

Competitive Landscape

Enel Colombia leads the Colombia solar energy market with a significant share of national output through its flagship projects, Guayepo (370 MW) and La Loma (187 MW). Celsia follows with 350 MW across 18 plants, leveraging existing customer relationships to lock in industrial PPAs. International module giants such as Trina Solar, Canadian Solar, and First Solar have established supply partnerships that guarantee bankable equipment pipelines.

Competition intensifies as Atlas Renewable Energy, Statkraft, and Verano Energy pursue buy-and-build strategies, drawn by a transparent auction regime and robust demand outlook. Traditional thermal players AES Colombia and Grupo Energía Bogotá are pivoting toward renewables to preserve relevance, creating a crowded field where operational expertise and local stakeholder management become decisive advantages. Developers are increasingly integrating storage, digital operations and maintenance (O&M), and community programs to differentiate their bids.

Capital allocation remains aggressive: Enel Américas earmarks USD 1.7 billion for Colombia between 2025 and 2027, while Ecopetrol’s acquisition of Enerfín Colombia signals state-backed scale-up ambitions. Vertical integration across development, EPC, and asset management enables margin capture along the value chain, suggesting that supply-chain control will shape future competitive hierarchies within the Colombia solar energy market.

Colombia Solar Energy Industry Leaders

-

Enel Green Power Colombia

-

Celsia S.A.

-

Grenergy Renovables S.A.

-

Canadian Solar Inc.

-

Ventus Ingeniería SRL

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: In a strategic move to bolster its renewable energy portfolio, Ecopetrol has signed a deal to acquire a 49% stake in the 1,087 MW Jemeiwaa Ka'I wind cluster from AES Colombia.

- December 2024: Enel Colombia has launched commercial operations at its Guayepo solar project, boasting a capacity of 370 MW. Located in the departments of Ponedera and Sabanalarga in Atlántico, Colombia, the expansive project spans 1,110 hectares and features over 820,000 solar panels.

- October 2024: Enel Colombia secures a USD 300 million loan from EIB Global, aimed at bolstering renewable energy generation and enhancing the power grid. The funding is directed towards solar photovoltaic (PV) plants with a combined capacity of around 486 MW, alongside upgrades and expansions to Enel Colombia's distribution network.

- September 2024: IDB Invest, a multilateral development bank, along with Bancolombia, a Colombian private bank, and Atlas Renewable Energy, a renewable energy firm, have sealed a long-term financial deal amounting to COP 474 billion (USD 113 million). This funding is earmarked for the development, construction, and operation of the 201 MW Shangri-La solar PV power plant located in Colombia's Tolima department.

Colombia Solar Energy Market Report Scope

Solar energy refers to the radiant light and heat emitted by the Sun, which can be harnessed and converted into usable forms of energy. It is a renewable and sustainable source of power that does not produce greenhouse gas emissions or contribute to air pollution. Solar energy is primarily captured and utilized through solar panels or photovoltaic (PV) cells. These devices consist of semiconductor materials, typically silicon, which can generate electricity when exposed to sunlight. When photons (particles of light) strike the surface of the solar panel, they excite the electrons within the semiconductor material, creating an electric current.

The Colombian solar energy market is segmented by technology and end user. By technology, the market is segmented into solar photovoltaic (PV) and concentrated solar power. By end user, the market is segmented into residential, commercial and industrial, and utility. For each segment, the market size and forecast are provided based on installed capacity in gigawatts (GW).

By Technology

| Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) |

By Grid Type

| On-Grid |

| Off-Grid |

By End-User

| Utility-Scale |

| Commercial and Industrial (C&I) |

| Residential |

By Component (Qualitative Analysis)

| Solar Modules/Panels |

| Inverters (String, Central, Micro) |

| Mounting and Tracking Systems |

| Balance-of-System and Electricals |

| Energy Storage and Hybrid Integration |

| By Technology | Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) | |

| By Grid Type | On-Grid |

| Off-Grid | |

| By End-User | Utility-Scale |

| Commercial and Industrial (C&I) | |

| Residential | |

| By Component (Qualitative Analysis) | Solar Modules/Panels |

| Inverters (String, Central, Micro) | |

| Mounting and Tracking Systems | |

| Balance-of-System and Electricals | |

| Energy Storage and Hybrid Integration |

Key Questions Answered in the Report

What is the current installed capacity of the Colombia solar energy market?

Capacity will reach 2.9 GW in 2026.

How fast will Colombia add new solar capacity by 2031?

The Colombia solar energy market is forecast to expand at a 29.10% CAGR, reaching 10.39 GW by 2031.

Which technology leads Colombia’s solar sector?

Solar PV holds 100% of installations, driven by crystalline-silicon modules and falling equipment prices.

What drives off-grid solar growth in Colombia?

Rural electrification programs targeting 228,000 households and high diesel costs propel off-grid capacity at a 34.20% CAGR.

Who are the leading companies in the Colombia solar energy market?

Enel Colombia, Celsia, and Atlas Renewable Energy are the largest players, jointly controlling about 35% of output.

Why is residential solar adoption accelerating?

Net-metering, improved financing, and the USD 10 billion Colombia Solar initiative reduce costs and shorten payback periods for households.

Page last updated on: