Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.28 Billion |

| Market Size (2031) | USD 5.72 Billion |

| Growth Rate (2026 - 2031) | 20.15% CAGR |

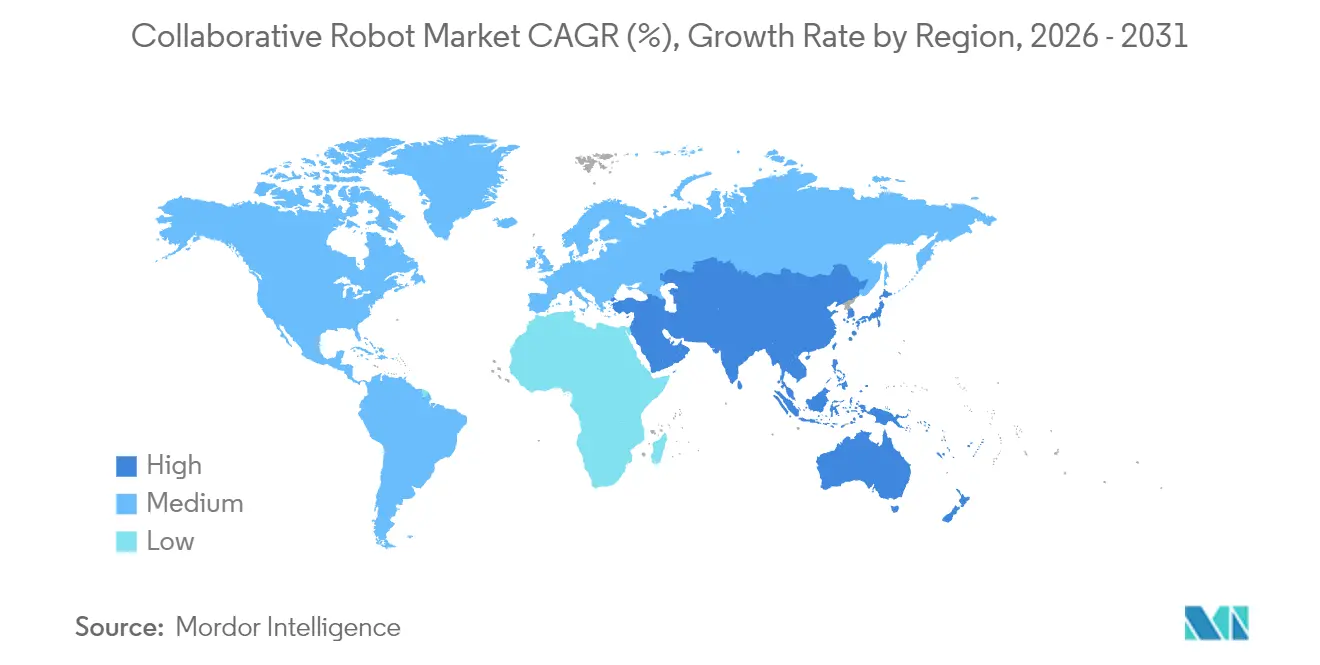

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

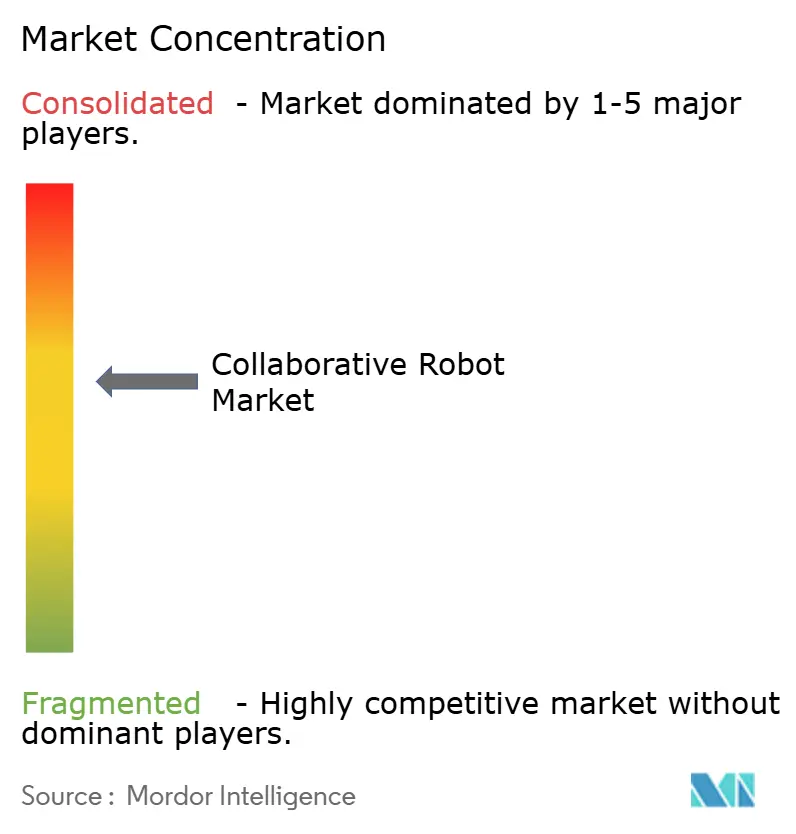

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Collaborative Robots Market Analysis by Mordor Intelligence

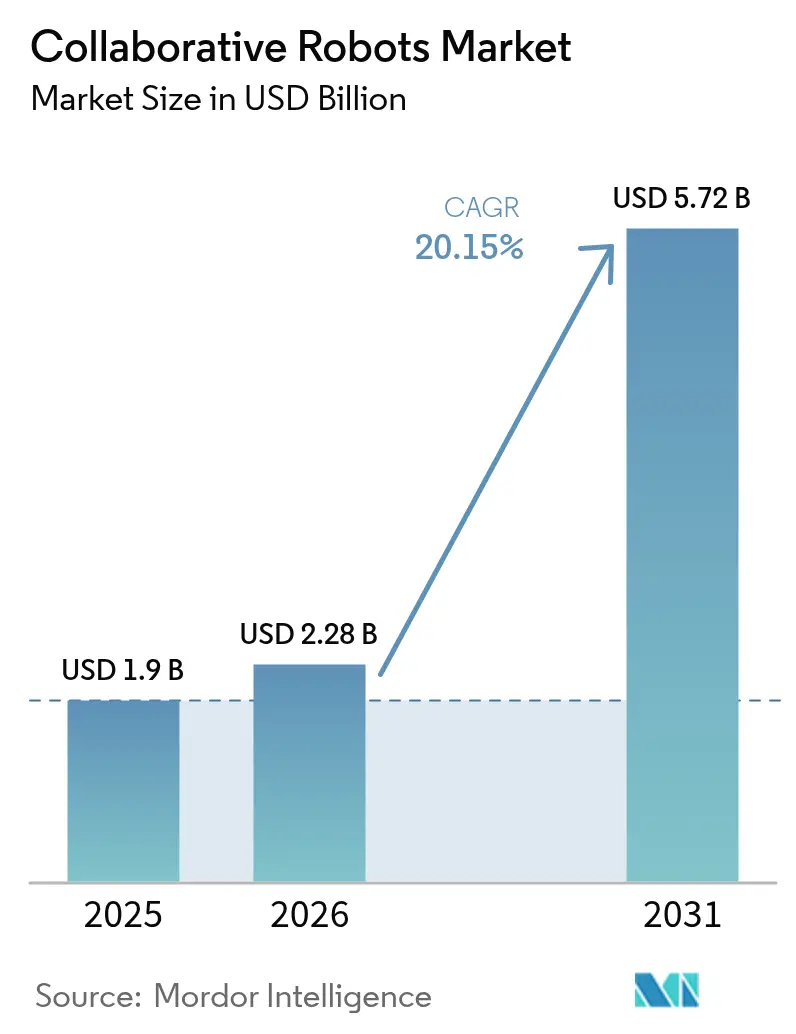

The Collaborative Robots Market size is projected to expand from USD 1.9 billion in 2025 and USD 2.28 billion in 2026 to USD 5.72 billion by 2031, registering a CAGR of 20.15% between 2026 to 2031. Demand accelerates as updated ISO/TS 15066 standards clarify safety requirements, tax incentives lower payback periods, and labor shortages raise the urgency of flexible automation. Manufacturers increasingly deploy cobots to lift productivity rather than replace workers, while maturing software and simplified programming shorten deployment cycles. Growing payload capacities, warehouse automation needs, and widening service-sector use cases strengthen adoption momentum across global value chains. [1]Source: U.S. Department of Commerce, “South Korea Robotics Industry,” trade.gov

Key Report Takeaways

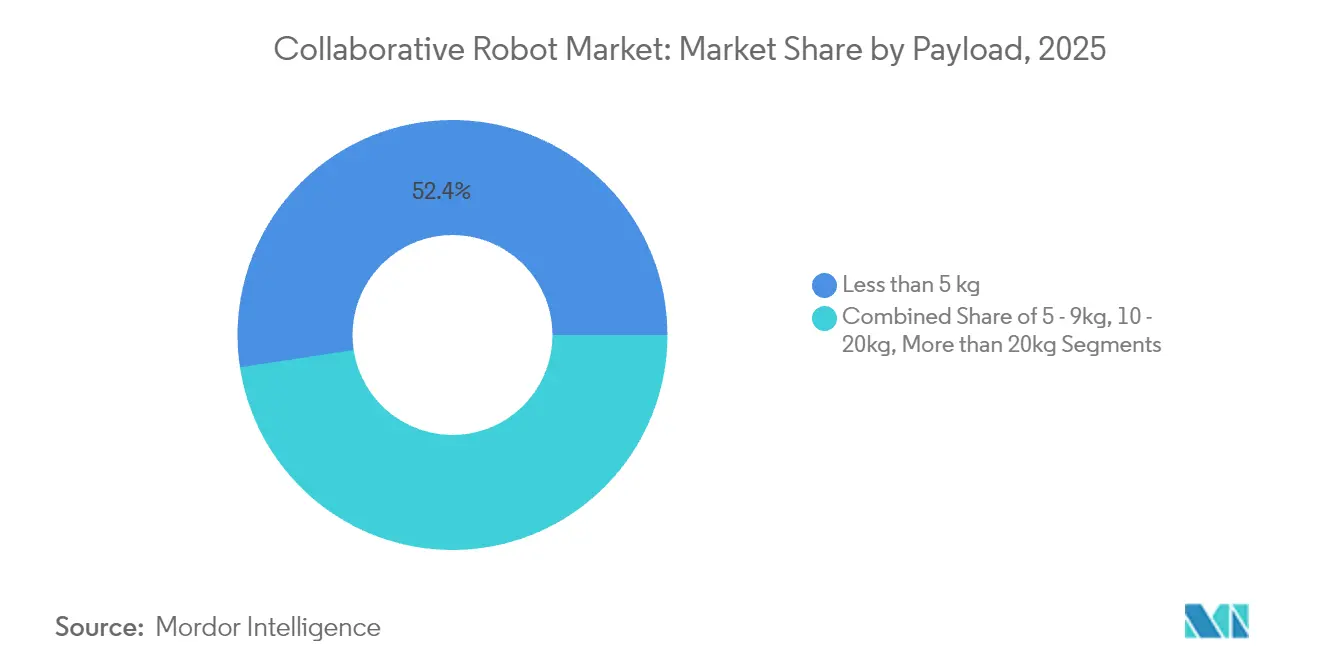

- By payload, sub-5 kg models held 52.40% of the collaborative robot market share in 2025; 10-20 kg units are expanding at a 22.95% CAGR through 2031.

- By component, hardware accounted for 71.35% of the collaborative robots market size in 2025, though software revenue is growing at 27.15% CAGR.

- By application, assembly retained 25.60% revenue share in 2025, while palletizing and de-palletizing are advancing at a 24.55% CAGR to 2031.

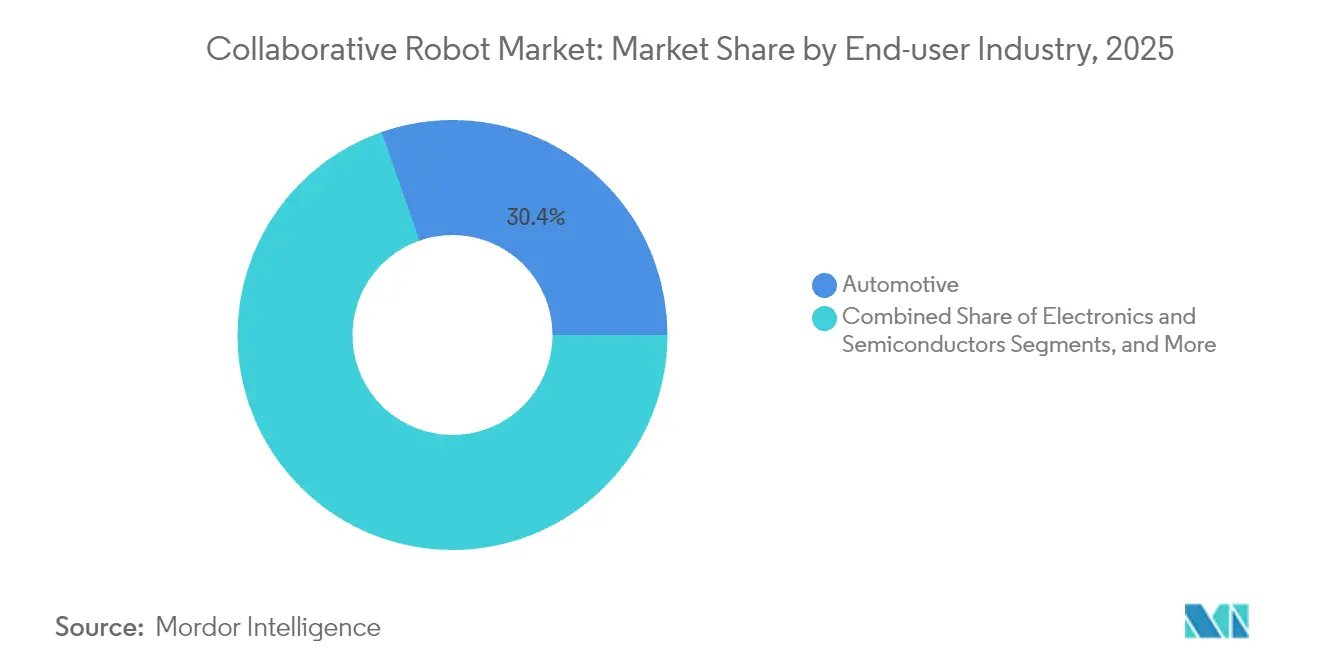

- By end-user, automotive captured 30.35% market share in 2025; logistics and e-commerce record the fastest 30.40% CAGR.

- By Geography, Asia-Pacific commanded 40.55% revenue in 2025, are expanding at a 21.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Collaborative Robots Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost-effective Re-deployment in High-mix Manufacturing | + 3.20% | Europe, North America | Medium term (2-4 years) |

| OEM Push Toward Plug-and-Play Cobots for SMEs | + 4.10% | Global, concentrated in North America | Short term (≤ 2 years) |

| Rapid E-Commerce Fulfilment Drives Warehouse Cobots | + 5.80% | Global, led by Asia-Pacific | Short term (≤ 2 years) |

| ISO/TS 15066 Updates Easing Liability Concerns | + 2.90% | Global | Medium term (2-4 years) |

| Tax Incentives for Reshoring Automation | + 3.40% | United States, selective EU markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cost-effective Redeployment in High-mix Manufacturing

European and North American factories now rotate cobots across assembly cells within a single shift, cutting changeover from weeks to hours This agility lets automotive suppliers accept smaller, high-margin orders while retaining automation gains.[2]Yaskawa Electric Corporation, “Yaskawa Report 2024,” yaskawa-global.com

OEM Push Toward Plug-and-Play Cobots for SMEs

New controllers, capped wiring, and pre-loaded task libraries allow small manufacturers to install cobots without specialist integrators. Universal Robots’ UR-series refresh shows how cycle-time gains and intuitive hand-guiding shrink total cost of ownership, opening the collaborative robot market to thousands of first-time users

Rapid E-commerce Fulfilment Drives Warehouse Cobots

Logistics firms combine autonomous mobile robots with stationary cobots for goods-to-person picking, enabling same-day shipping even during seasonal surges. DHL Supply Chain’s global rollout of 5,000 units underscores cobots’ ability to flex capacity without over-capitalizing facilities

ISO/TS 15066 Updates Easing Liability Concerns

The 2024 revision clarifies contact-force thresholds and risk-assessment procedures, letting integrators certify workcells faster and insurers price policies more accurately. Manufacturers now view cobots as compliant assets rather than legal hazards.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration Bottlenecks with Brownfield PLC Architectures | -2.80% | Global, concentrated in established manufacturing regions | Short term (≤ 2 years) |

| Payload-Speed Trade-offs Limiting Heavy-duty Tasks | -1.90% | Global, particularly in automotive and metals industries | Long term (≥ 4 years) |

| Fragmented Component Ecosystem Inflates TCO for SMEs | -2.10% | Global, most acute in emerging markets | Medium term (2-4 years) |

| Insurance underwriting gaps for human-robot workcells | −1.5% | Global, early-stage adopters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Integration Bottlenecks with Brownfield PLC Architectures

Legacy PLCs often lack real-time Ethernet or safe-motion channels, forcing costly controller upgrades when cobots are added to decades-old lines . The expense pushes some automotive plants to defer adoption until full line overhauls.

Payload-Speed Trade-offs Limiting Heavy-duty Tasks

Force-limiting designs cap joint velocities, so even new 30 kg units run slower than traditional arms. In high-volume stamping or welding, throughput penalties outweigh safety gains, limiting addressable demand in heavy industries

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Payload: Lightweight Dominance Shifts Toward Mid-Range

Sub-5 kg models controlled 52.40% of the collaborative robot market in 2025, largely in electronics and medical device assembly where precision is paramount. The 10-20 kg band, however, is pacing a 22.95% CAGR, signaling rising interest in palletizing, machine tending, and automotive sub-assembly. Mid-range units also integrate longer reaches, enabling line-side work without moving humans to new safety zones. Heavy-duty (>20 kg) cobots remain niche but prove valuable in paint and chemical environments where explosion-proof certification is essential. As robot makers refine dynamic torque sensing, the collaborative robots market size for mid-payloads is projected to outgrow light units after 2028.

Within 5-9 kg, vendors package vision and AI for pick-and-place cycles under one second, catering to semiconductor back-end operations. The shift reflects buyers’ search for units that bridge dexterity and strength, reducing fleet complexity. Manufacturers leveraging the collaborative robot market gain the option to standardize grippers and controllers across payload classes, simplifying spare-parts management and operator training.

By Component: Hardware Foundation Enables Software Innovation

Hardware generated 71.35% of revenue in 2025, yet software is advancing 27.15% annually as users emphasize intelligence over mechanics. Vision-guided path planning, fleet orchestration, and predictive maintenance modules convert one-time hardware sales into recurring licenses, moving vendor profit pools toward digital services. Cobots now ship with ROS-compatible APIs and cloud connectors, allowing quick app integrations.

Growth in consulting and lifecycle services reflects SME reliance on external expertise. Vendors bundle safety assessment, programming, and operator up-skilling into subscription models, further enlarging the cobot market. Over time, software-defined payload upgrades may lower replacement cycles, letting plant managers keep frames in service longer while lifting performance through firmware enhancements.

By Application: Assembly Leadership Challenged by Logistics Growth

Assembly accounted for 25.60% of 2025 revenue as cobots solder PCBs and fasten interior trim alongside workers. Warehouse palletizing is rising fastest at 24.55% CAGR because e-commerce skews toward high-mix, low-volume flows that fixed conveyors cannot handle. Operators appreciate cobots’ quick redeployment between SKUs and minimal guarding needs. Machine tending and quality inspection also gain share as cameras and AI enable inline defect detection without tooling swaps.

Beyond manufacturing, hospitals pilot cobots for laboratory sample handling and pharmacy fulfillment, broadening the collaborative robot market. Food processors adopt hygienic-design arms for portioning and packaging, leveraging IP69K-rated enclosures to withstand wash-down routines.

By End-user Industry: Automotive Maturity Meets E-commerce Dynamism

Automotive held 30.35% collaborative robots market share in 2025 but shows slowing incremental growth. OEMs concentrate on final-trim stations where lightweight doors and dashboards require human guidance. Conversely, logistics and e-commerce exhibit a 30.40% CAGR as fulfillment centers scale robot fleets to meet next-day delivery benchmarks. Electronics assembly, general industry, and healthcare add resilience by diversifying revenue beyond cyclical vehicle production.

Pharmaceutical packagers apply cobots in sterile filling, exploiting clean-room certification levels unattainable by legacy industrial arms. Metals processing remains cautious due to payload-speed constraints, but weld-assist cobots still carve out sub-tasks such as tacking and cosmetic seam finishing.

By Programming Method: Intuitive Interfaces Drive Adoption

Hand-guiding dominates as operators teach paths by physically moving the arm, eliminating code. Lead-through teaching layers simple drag-and-drop waypoints for more precise jobs. Offline simulation appeals to automotive and aerospace users seeking cycle-time optimization before line-side deployment. The intuitive trend opens the collaborative robot industry to labor pools with limited coding exposure.

Advances in augmented-reality overlays let technicians visualize reach studies and collision envelopes on a tablet, cutting commissioning days. Voice-guided instruction is in early pilots, promising further democratization and reinforcing the collaborative robot market’s customer base among SMEs.

Geography Analysis

Asia generated 40.55% of 2025 revenue, propelled by China’s 1-trillion-yuan robotics push under the 14th Five-Year Plan and Japan’s Society 5.0 roadmap that blends AI, IoT, and next-generation automation . Chinese electronics and battery plants install cobots for precision gluing and cell stacking, while Japanese hospitals test service robots for elder care. South Korea’s Fourth Intelligent Robot Basic Plan funds local SMEs to adopt collaborative solutions, reinforcing domestic supply chains.

North America ranks second. U.S. reshoring incentives combined with record labor scarcity elevate the market. Semiconductor fabs subsidized by the CHIPS Act integrate dual-arm cobots for wafer loading, shrinking transport contamination risk. Canadian auto parts suppliers adopt mid-payload units for die-casting part finishing, while Mexican maquiladoras deploy cobots to balance wage inflation with export competitiveness. Cross-border standardization allows integrators to reuse cell designs, accelerating rollout.

Europe shows robust uptake led by Germany’s Industrie 4.0 lighthouse projects linking MES data to cobot fleets. Horizon Europe grants finance human-machine interface research, spurring startups in Denmark and Italy that build AI motion-planning stacks. French aerospace plants choose cobots for carbon-fiber trimming, citing weight reduction and ergonomic gains. Rising energy costs push factories toward leaner layouts where cobots save floor space relative to fenced robots. Environmental regulations also favor cobots’ lower idle power draw compared with hydraulic presses, aiding the collaborative robots market size in sustainability-conscious regions.

Competitive Landscape

Universal Robots, FANUC, ABB, and KUKA anchor the market through broad portfolios and global service networks. Together they form a durable core, yet Doosan Robotics, Techman Robot, and AUBO Robotics erode share by specializing in palletizing, vision-guided inspection, and cost-sensitive emerging markets. Product roadmaps center on higher payloads, IP ratings, and software ecosystems rather than raw reach.

Strategic partnerships are multiplying. FANUC collaborates with paint-booth OEMs for explosion-proof packages, while ABB and Microsoft co-develop AI platforms that process vision data on the edge. Universal Robots hosts a growing UR+ marketplace where third-party grippers and cameras gain plug-and-play certification, reducing integration friction and expanding the collaborative robot market. Component suppliers such as Harmonic Drive and Schaeffler invest in torque-dense actuators that lift performance without sacrificing compliance.

Pricing remains stable despite rising volumes because vendors bundle software licenses and support services. Integrators differentiate through vertical templates; a warehouse integrator may guarantee pick accuracy, whereas a medical integrator focuses on sterilization workflows. Industry consolidation is likely as smaller players seek capital to fund global support footprints, yet open interfaces preserve a multi-vendor environment for now.

Collaborative Robots Industry Leaders

Universal Robots AS

Fanuc Corp.

TechMan Robot Inc.

AUBO Robotics USA

ABB Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Foxconn announced humanoid robot deployment at its new Houston plant for Nvidia server production, targeting Q1 2026 go-live.

- May 2025: DHL Group signed a memorandum of understanding with Boston Dynamics for an additional 1,000 robots, extending a 7,500-unit fleet.

- April 2025: Collaborative Robotics raised USD 100 million in Series B funding, bringing total to USD 140 million within two years.

- January 2025: Yaskawa Electric reported 12% lower FY 2024 operating profit at JPY 58 billion amid semiconductor softness.

Global Collaborative Robots Market Report Scope

Collaborative robots are designed to work with humans and are built with safety features such as integrated sensors, passive compliance, and overcurrent detection. The integrated sensors feel external forces, and if the force is too high, they halt the robot's movement.

The Collaborative Robots Market is segmented by payload (less than 5 kg, 5-9 kg, 10-20 kg, and more than 20 kg), end-user industry (electronics, automotive, manufacturing, food and beverage, chemicals and pharmaceutical), application (material handling, pick and place, assembly, palletizing & de-palletizing), and geography (North America (United States, Canada), Europe (United Kingdom, Germany, France, Rest of Europe ), Asia Pacific (China, India, Japan, Rest of Asia Pacific) Latin America (Brazil, Mexico, Rest of Latin America), and Middle East and Africa (United Arab Emirates, Saudi Arabia, Rest of Middle East and Africa)). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

By Payload

| Less than 5 kg |

| 5 - 9 kg |

| 10 - 20 kg |

| More than 20 kg |

By Component

| Hardware | |

| Software | |

| Services | Consulting and Integration |

| Maintenance and Training |

By Application

| Material Handling |

| Pick and Place |

| Assembly |

| Palletizing and De-palletizing |

| Welding and Soldering |

| Quality Testing and Inspection |

| Packaging |

| Other Applications |

By End-user Industry

| Automotive |

| Electronics and Semiconductors |

| General Manufacturing |

| Food and Beverage |

| Chemicals and Pharmaceuticals |

| Logistics and E-commerce |

| Healthcare and Life Sciences |

| Metals and Machining |

| Other Industries |

By Programming Method (qualitative only)

| Hand-Guiding / Direct Teaching |

| Lead-through Teaching |

| Offline Programming and Simulation |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Nordics | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| South America | Brazil |

| Argentina | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Africa | South Africa |

| Rest of Africa |

| By Payload | Less than 5 kg | |

| 5 - 9 kg | ||

| 10 - 20 kg | ||

| More than 20 kg | ||

| By Component | Hardware | |

| Software | ||

| Services | Consulting and Integration | |

| Maintenance and Training | ||

| By Application | Material Handling | |

| Pick and Place | ||

| Assembly | ||

| Palletizing and De-palletizing | ||

| Welding and Soldering | ||

| Quality Testing and Inspection | ||

| Packaging | ||

| Other Applications | ||

| By End-user Industry | Automotive | |

| Electronics and Semiconductors | ||

| General Manufacturing | ||

| Food and Beverage | ||

| Chemicals and Pharmaceuticals | ||

| Logistics and E-commerce | ||

| Healthcare and Life Sciences | ||

| Metals and Machining | ||

| Other Industries | ||

| By Programming Method (qualitative only) | Hand-Guiding / Direct Teaching | |

| Lead-through Teaching | ||

| Offline Programming and Simulation | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Nordics | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| South America | Brazil | |

| Argentina | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current collaborative robot market size in 2026?

The collaborative robot market size stands at USD 2.28 billion in 2026 and is on track to reach USD 5.72 billion by 2031.

Which payload segment is growing fastest?

Cobots with 10-20 kg payloads are expanding at a 22.95% CAGR as manufacturers automate heavier assembly and palletizing tasks.

Why are cobots gaining traction in warehouses?

Flexible deployment, safe human interaction, and rapid scalability make cobots ideal for e-commerce fulfillment peaks, evidenced by DHL’s multi-site roll-out of 5,000 units.

How do updated ISO/TS 15066 standards affect adoption?

Clarified safety thresholds reduce liability and shorten certification timelines, encouraging insurers and regulators to support new installations.

Page last updated on: