Cryogenic Valves Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.41 Billion |

| Market Size (2031) | USD 4.19 Billion |

| Growth Rate (2026 - 2031) | 4.24% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

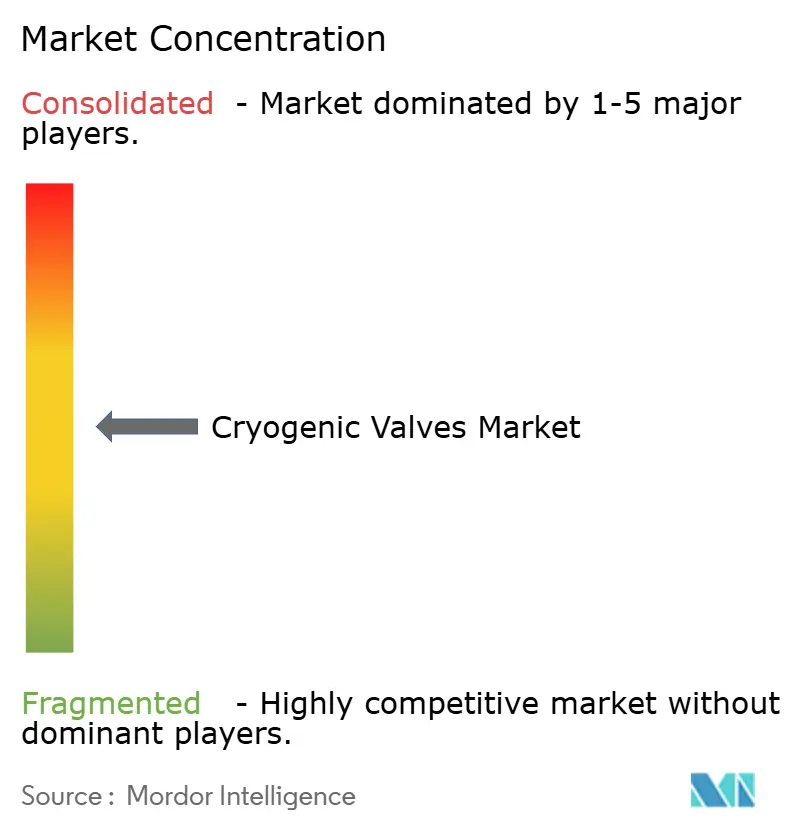

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cryogenic Valves Market Analysis by Mordor Intelligence

The Cryogenic Valves Market size was valued at USD 3.27 billion in 2025 and estimated to grow from USD 3.41 billion in 2026 to reach USD 4.19 billion by 2031, at a CAGR of 4.24% during the forecast period (2026-2031). Rising investment in liquefied natural gas (LNG) terminals, green-hydrogen projects, and petro-chemical expansions underpins this steady trajectory. Large‐scale facilities each require hundreds of valves capable of sealing at temperatures below –150 °C, and owners favour suppliers able to certify products quickly for multiple codes. Asia-Pacific remains the largest regional buyer of equipment, while North America delivers high-value opportunities tied to hydrogen pilot plants. Producers able to combine cryogenic engineering depth with aftermarket services are attracting premium contract awards, as end-users seek long-term reliability and fast turn-round maintenance.

Key Report Takeaways

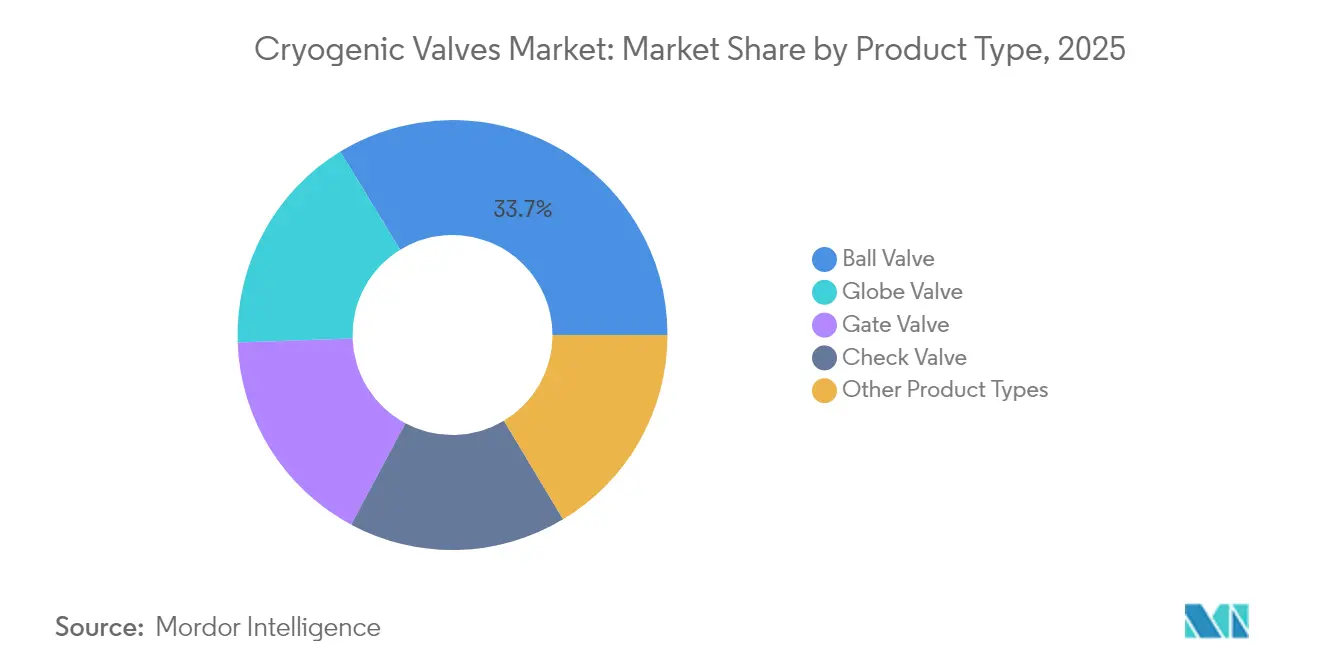

- By product type, ball valves led with 33.74% of cryogenic valves market share in 2025; globe valves are projected to post the fastest 5.18% CAGR through 2031.

- By actuation, manual systems commanded 59.10% share of the cryogenic valves market size in 2025, whereas pneumatic actuation is forecast to expand at 5.33% CAGR between 2026-2031.

- By gas handled, LNG accounted for 44.92% share of the cryogenic valves market size in 2025, while hydrogen applications are set to grow at a 5.62% CAGR to 2031.

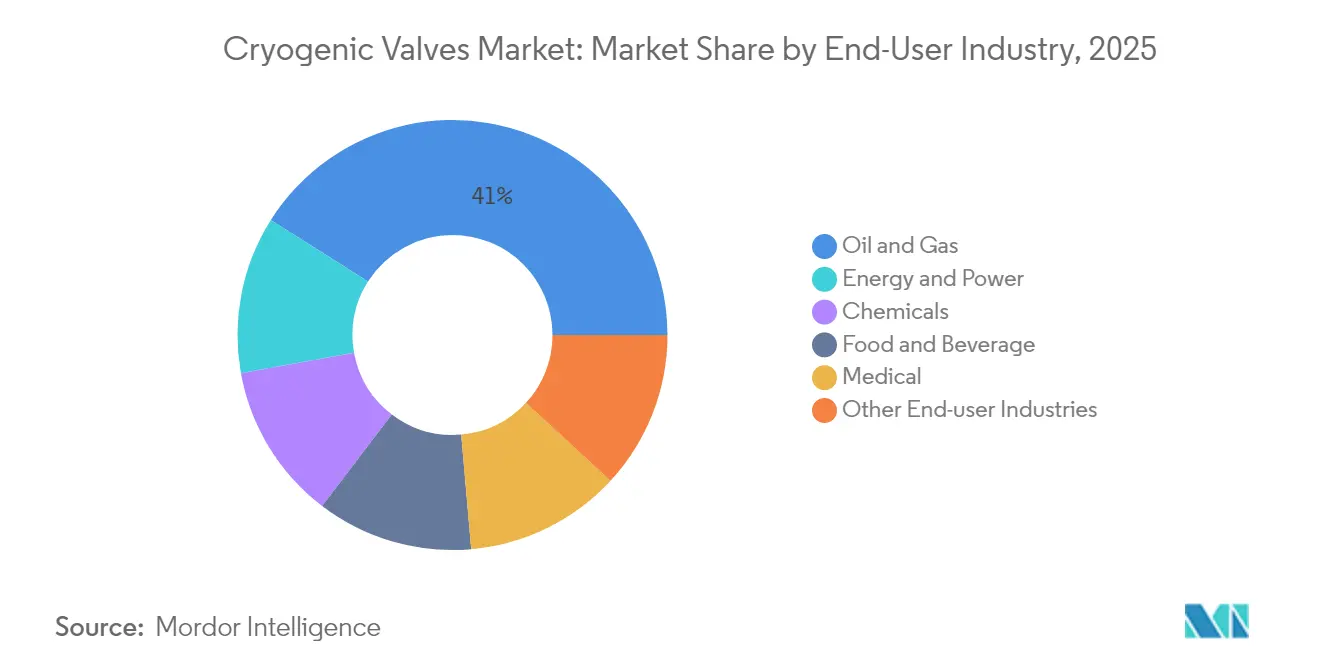

- By end-user, the oil & gas sector held 41.02% share of the cryogenic valves market size in 2025; energy & power installations record the top 5.12% CAGR outlook.

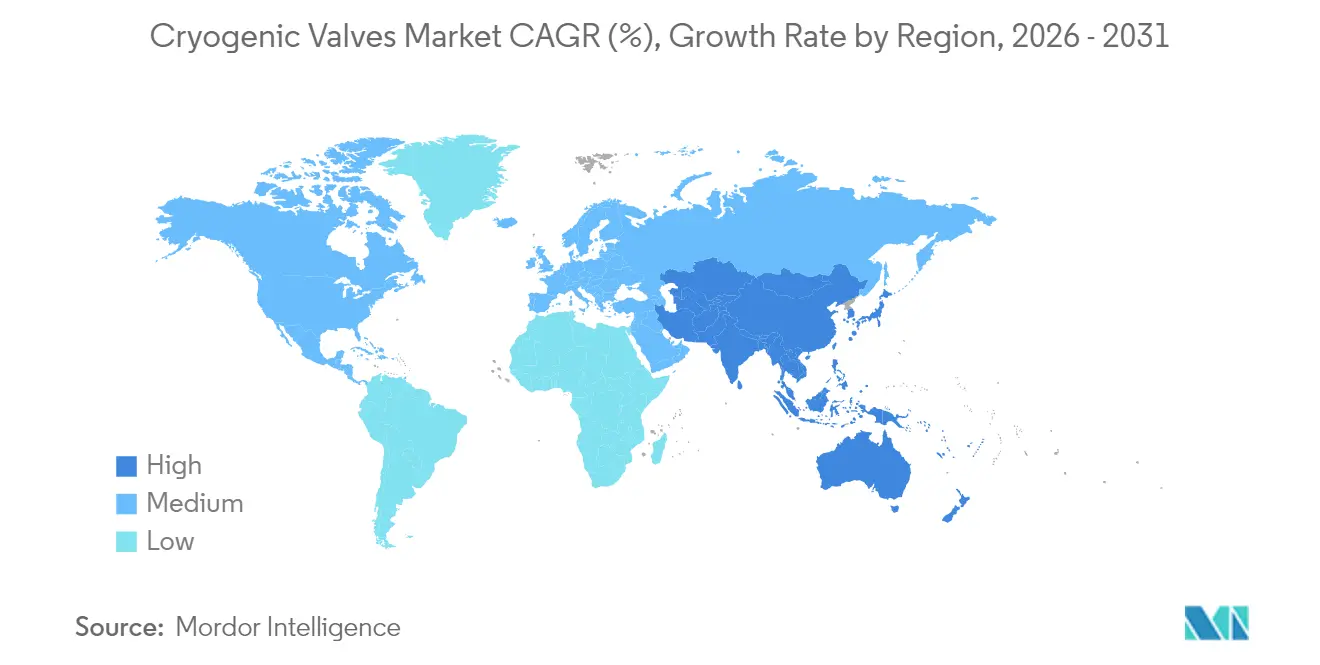

- By geography, Asia-Pacific retained 26.10% share of the cryogenic valves market in 2025 and is the fastest-growing region at a 5.48% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cryogenic Valves Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising LNG infrastructure investments | +1.8% | Global; focus on Asia-Pacific & North America | Medium term (2-4 years) |

| Growth in industrial gas demand | +1.2% | Global; strong in Asia-Pacific & North America | Long term (≥ 4 years) |

| Hydrogen-economy project pipeline acceleration | +0.9% | North America & EU, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Capacity additions in petro-chem & specialty gas plants | +0.7% | Global; Middle East & Asia-Pacific focus | Medium term (2-4 years) |

| Small-scale LNG bunkering at global ports | +0.5% | Worldwide along major shipping routes | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising LNG Infrastructure Investments

Expansions slated between 2024-2028 will lift global LNG liquefaction capacity by 40%, with the United States overtaking Qatar as lead exporter while Asia-Pacific purchases the bulk of incremental cargoes. Baker Hughes secured USD 5.6 billion of LNG equipment awards for two Louisiana trains, illustrating contractor appetite for field-proven valve partners able to guarantee ultra-low-leak performance[1]Baker Hughes, “Q4 2024 Investor Presentation,” bakerhughes.com. Marine bunkering demand is forecast to exceed 16 million t annually by 2030, prompting ports to specify automated cryogenic transfer assemblies that integrate emergency shut-off valves. Enterprise Products Partners is expanding Houston Ship Channel refrigeration capacity by 300,000 bbl/d, creating new orders for triple-offset stop-valves rated down to –162 °C. Saudi Aramco’s USD 7.7 billion Fadhili upgrade will add 1.3 Bcf/d of sweet-gas processing, each train fitted with redundant cryogenic flow-paths to handle mixed refrigerants.

Growth in Industrial Gas Demand

Air Liquide’s four modular air-separation units in Texas will deliver 9,000 t/d of oxygen to ExxonMobil’s low-carbon hydrogen complex and generate the continent’s largest argon stream, placing long-cycle demand on valve makers able to certify for oxygen service[2]Air Liquide, “Large ASU Investment in Texas,” airliquide.com. Healthcare expansion keeps liquid-oxygen consumption rising, and hospitals mandate valve designs that prevent particle shedding in patient circuits. Food processors favour liquid nitrogen tunnels for flash-freezing, with valves that tolerate rapid thermal cycling down to –196 °C while maintaining hygienic finishes. Renewable-powered air-separation plants require fast-response control trim so operators can throttle output to match fluctuating grid tariffs.

Hydrogen-Economy Project Pipeline Acceleration

The U.S. Department of Energy’s H-Mat Consortium reports cryogenic hydrogen storage achieving 73.46 kg/m³ at –223 °C, nearly doubling gaseous density and intensifying demand for zero-leak HP valves. NASA plans a dedicated hydrogen test facility at the Glenn Research Center to support aviation propulsion, drawing on five decades of cryo expertise that suppliers must replicate in commercial hardware. Horizon Europe is funding liquefiers targeting 8–10 kWh/kg energy use, a step change that will employ hundreds of precision globe valves for sub-cooled flow control. Developers of 700 bar cryo-compressed tanks are specifying high-pressure stainless alloys with low-emission packings. University research into pump-free hydrogen feed systems illustrates future instrument-style valve opportunities across the transport sector.

Capacity Additions in Petro-chem & Specialty Gas Plants

Air Liquide’s USD 850 million Baytown complex will provide 9,000 t/d O₂ and 6,500 t/d N₂, plus argon, xenon and krypton, each stream segregated by low-temperature fractionation that relies on tight-shutoff valve arrays. Saudi Aramco’s Fadhili project will lift sulfur output by 2,300 t/d, necessitating alloys capable of resisting both cold shock and sour-gas corrosion. Enterprise Products Partners is adding separate flash-gas, propane and butane services, widening the mix of valve metallurgy needed for multi-grade operations. Building-in carbon-capture loops pushes operators to select valves qualified for sub-zero CO₂ phase-change cycling, further broadening specifications.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Safety & compliance complexities | –0.8% | Global; stringent in North America & Europe | Medium term (2-4 years) |

| Stainless-steel & nickel price volatility | –0.6% | Global manufacturing hubs, notably Asia-Pacific | Short term (≤ 2 years) |

| Supply-chain gaps in vacuum-brazed components | –0.4% | Global; specialised applications most affected | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Safety & Compliance Complexities

ASME B31.3 mandates impact-tested materials below –425 °F; complying valves use austenitic stainless or aluminium alloys proven by Charpy testing. The 2025 ASME VIII update introduces fresh cryogenic case studies, prompting designers to add thicker bonnets or bellows seals to satisfy the new rules. MSS SP-158-2021 requires high-pressure gas tests that inflate development costs, yet utilities increasingly insist on the certification to reduce outage risk. U.S. Code 49 CFR obliges valves to hold tank test pressure without seepage and to include robust guards against mechanical damage, shaping layout choices on trailers. Five-year recertification cycles for safety valves generate recurring service revenue but raise ownership costs for small operators. Smaller fabricators struggle to keep pace with multi-jurisdiction code work, giving established brands a competitive edge.

Stainless-Steel & Nickel Price Volatility

Nickel prices swinging by more than 40% during 2024 created budgeting headaches for valve projects locked into fixed-price EPC contracts. Austenitic grades 304L and 316L remain dominant due to ductility and toughness retention at –196 °C, yet their cost volatility is accelerating research into duplex stainless and aluminium-bronze options that could shave 15% off raw-material spend. Leading OEMs now sign multi-year supply agreements to guarantee tonnage and hedge cost spikes, while some invest in in-house precision foundries to de-risk cast component availability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Ball Valves Maintain Lead While Globe Valves Accelerate

Ball valves held a dominant 33.74% cryogenic valves market share in 2025, owing to proven tight shut-off and straightforward maintenance. Manufacturers supply extended-stem designs that isolate the seat from boiling liquefied gases, cutting ice buildup and seat damage. Emerson’s Fisher HP series uses spring-energised PTFE rings to hold Class VI shut-off at –198 °C. Globe valves, though smaller in installed base, are expected to grow at 5.18% CAGR as hydrogen liquefaction projects favour their throttling precision. The cryogenic valves market size for globe valves is anticipated to widen notably in pilot plants producing 8–10 t/h of liquid hydrogen, each calling for variable-flow control to manage ortho-para conversion heat.

Technical enhancements continue across both lines. Ball-valve makers are adding graphite bonnet seals certified to ISO 15848-1 Class A for ultra-low fugitive emissions, an important factor for operators seeking ESG credits. Globe-valve OEMs are deploying contoured plugs that deliver equal-percentage characteristics, enhancing process stability in multi-stage expanders. Gate and check valves retain niche uses: gate valves accommodate full-bore LNG loading lines up to 42 in, while dual-plate cryogenic check valves prevent reverse surge in boil-off gas recirculation loops. Specialty butterfly and plug valves fill gaps such as helium service at ultra-low density where very low torque is essential.

By Actuation: Manual Systems Dominate Yet Pneumatic Momentum Builds

Manual gear and hand-wheel operators represented 59.10% of the cryogenic valves market in 2025, prized for simplicity and intrinsic fail-safe capability during power loss. LNG export terminals rely on manual isolation valves to secure cargo lines during berth-side emergencies. The segment, however, grows slowly as facility owners look to remote operation to cut staffing. Pneumatic actuation will expand at 5.33% CAGR to 2031, leveraging plant air or nitrogen to deliver quick stroke times under fail-closed logic. Hydrogen sites favour pneumatic drives to avoid ignition risks linked to electric motors.

Electric actuators achieve niche uptake where data-rich position feedback is essential, such as in digitally managed nitrogen freezing tunnels that fine-tune flow to maintain product texture. Hybrid solutions that bolt a declutchable gearbox onto a pneumatic drive combine manual override with automated speed, capturing demand in dual-use installations. OEMs increasingly embed smart positioners measuring stem friction and cycle count, feeding plant historians that trigger service work orders before leakage occurs. This predictive-maintenance model strengthens aftermarket ties and lifts lifetime revenue per installed valve.

By Gas: LNG Retains Leadership While Hydrogen Sets the Growth Pace

LNG applications generated 44.92% of the cryogenic valves market size in 2025. Each liquefaction train integrates more than 800 process, isolation and safety valves rated for –162 °C, ensuring a substantial baseline for replacements as older Gulf Coast and Australian facilities reach overhaul cycles. Hydrogen, currently smaller, is poised for the swiftest 5.62% CAGR to 2031. The cryogenic valves market is responding with new alloys that curb hydrogen embrittlement while retaining low-temperature toughness, coupled with bellows seal technology that limits fugitive mass loss to under 1 × 10-⁶ sccs.

Liquid nitrogen and oxygen remain vital although slower growth sectors. Food, electronics and healthcare end-users demand ultra-clean internal finishes, driving valve suppliers to polish wetted parts to Ra ≤ 0.4 µm. Specialty gases such as helium, xenon and neon, though small in volume, command premium pricing; valves here must guard against micro-leakage that would waste product costing USD 20–100 per m³. Overall, portfolio breadth across multiple cryogenic gases improves supplier resilience against cyclical spending in any single commodity group.

By End-User Industry: Oil & Gas Still Largest, Energy Transition Boosts Power Sector

Oil & gas companies owned 41.02% of the cryogenic valves market in 2025. LNG liquefaction, regasification and LPG export terminals deliver repetitive, high-ticket orders for 8-12-in ball and gate valves designed for 900-class duty. Yet the fastest 5.12% CAGR resides in energy & power, fuelled by utility-scale hydrogen demonstration plants and renewable-linked air-separation units. These projects favour globe valves paired with digital actuators to modulate flow in response to wind and solar output swings.

Chemical producers apply cryogenic separation to extract argon, krypton and CO₂ streams, utilising multi-port manifolds packed with small-bore needle valves. Food and beverage processors adopt liquid nitrogen tunnels for quality preservation, selecting hygienic ball valves with FDA-compliant seals for clean-in-place procedures. Hospitals and drug manufacturers require oxygen and nitrogen valves certified for non-lubricated service, expanding specialty revenue niches. Aerospace test facilities use helium down to –270 °C, an extreme demanding bespoke stem materials. Diversification across such sectors cushions suppliers against volatility in LNG mega-projects.

Geography Analysis

Asia-Pacific controlled 26.10% of the cryogenic valves market in 2025 and is projected to expand by a 5.48% CAGR through 2031. China’s gas-to-power policy reversal and India’s heat-wave-driven demand are reviving import growth, while Japan and South Korea invest in re-loading hubs that reposition cargoes from the United States. Australia’s ageing liquefaction trains enter refurbishment cycles, pushing aftermarket valve services. Government hydrogen roadmaps in China, South Korea and Australia create incremental bids for high-pressure globe valves at pilot liquefier sites.

North America benefits from the United States becoming the world’s largest LNG exporter and from aggressive federal funding for hydrogen hubs. Gulf Coast brownfield liquefaction projects stipulate North American Valve Manufacturers Association membership, favouring domestic suppliers with local inventories. Air Liquide’s Baytown investment plus multiple mid-scale liquid-oxygen build-owns maintain steady industrial-gas valve uptake. Canada’s first LNG shipment slated for 2027 from British Columbia will add western-hemisphere demand.

Europe, despite softer LNG imports in 2024, commits heavily to hydrogen. Germany’s planned 10 GW of electrolyser capacity links to liquefaction and underground storage schemes, each specifying ultra-low-leak isolation valves. Horizon Europe funds mobile LH₂ tank trials between Spain and the Netherlands, generating specialty cargo-handling valve orders. Nordic ports accelerate LNG bunkering roll-outs supporting green-corridor shipping alliances.

The Middle East and Africa witness sizeable greenfield gas processing. Saudi Aramco’s Fadhili expansion, Qatar’s North Field South and multiple Omani petro-chem complexes need durable cryogenic metallurgy that resists sour-gas compounds. Abu Dhabi is exploring blue-ammonia, which will import design philosophies from LNG trains to valve packages. In Africa, Mozambique’s postponed onshore LNG plant, once security stabilises, promises a fresh cycle of valve procurement.

South America remains nascent yet promising. Brazil eyes floating storage and regasification units to manage seasonal gas deficits, requiring compact cryogenic valve skids. Argentina’s Vaca Muerta shale may eventually feed LNG export barge projects, though timetable uncertainty tempers near-term demand. Chile’s mining sector investigates liquid oxygen for process efficiency, presenting small but high-margin valve prospects.

Competitive Landscape

Consolidation is reshaping the cryogenic valves market. The all-stock merger of Chart Industries and Flowserve, valued at USD 19 billion, creates a vertically integrated entity spanning process pumps, valves, and aftermarket services expected to yield USD 300 million annual cost synergies within three years. Flowserve’s earlier USD 290 million acquisition of MOGAS Industries bolsters severe-service isolation capability, positioning the group for hydrogen duties. Dover-owned PSG purchased Cryogenic Machinery Corp, and OPW bought Marshall Excelsior, broadening their clean-energy portfolios.

Technology differentiation remains vital. Emerson’s Fisher HP balanced plug design sustains tight control under 300-bar differentials, while Samson AG’s top-entry globe valves allow in-situ trim swaps that cut downtime 40%. Emerging firms such as HeLIUM Cryogenics commercialise miniature Stirling coolers that integrate proprietary micro-valves, signalling a future of decentralised refrigeration. Baker Hughes leverages compressors plus valve packages in turnkey bids, winning multi-train LNG awards worth USD 5.6 billion.

Service remains a revenue cornerstone. The combined Chart-Flowserve group expects 42% of sales from aftermarket contracts, reflecting operator preference for bundled spares and annual inspection programmes. OEMs increasingly deploy digital twins that log valve cycles and predict seat wear, strengthening client stickiness. Regionally, Japanese manufacturers retain best-in-class reputations for cleanroom-built oxygen valves; European houses lead in vacuum-jacketed assemblies; and U.S. brands dominate large-bore LNG isolation.

Competitive intensity is moderate: top five suppliers together control roughly 55% of installed liquefaction capacity, while hundreds of local specialists serve niche segments such as dewars and laboratory freezers. Price pressure persists in commodity ball valves, but high-spec hydrogen and aerospace projects command premium margins. Suppliers able to support rapid certification for ASME, CE-PED and KGS simultaneously capture multi-continental opportunities.

Cryogenic Valves Industry Leaders

Emerson Electric Co.

Baker Hughes

Flowserve Corporation

Velan

Samson AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Chart Industries and Flowserve Corporation announced an all-stock merger of equals valued at USD 19 billion, forming a differentiated player in industrial process technologies with USD 300 million expected cost synergies.

- February 2025: Baker Hughes won a contract from Bechtel to supply gas-technology equipment, including eight main refrigeration compressors, for two liquefaction trains totaling 11 MTPA in Louisiana.

Global Cryogenic Valves Market Report Scope

A cryogenic valve is generally designed to react to high pressure, which pushes the valve into an open position to allow the gas or other media to flow readily through. The market is segmented by product type, gas, end-user industry, and geography. By product type, the market is segmented into ball valve, check valve, gate valve, globe valve, and other product types. By gas, the market is segmented into liquid nitrogen, liquid helium, hydrogen, oxygen, and other gases. By end-user industry, the market is segmented int chemicals, oil and gas, energy and power, food and beverage, medical, and other end-user industries. The report also covers the size and forecasts for the cryogenic valves market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of revenue (USD million).

| Ball Valve |

| Gate Valve |

| Globe Valve |

| Check Valve |

| Other Product Types |

| Manual |

| Pneumatic |

| Electric |

| Liquid Nitrogen |

| Liquid Natural Gas |

| Hydrogen |

| Oxygen |

| Other Gases |

| Oil and Gas |

| Energy and Power |

| Chemicals |

| Food and Beverage |

| Medical |

| Other End-user Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Ball Valve | |

| Gate Valve | ||

| Globe Valve | ||

| Check Valve | ||

| Other Product Types | ||

| By Actuation | Manual | |

| Pneumatic | ||

| Electric | ||

| By Gas | Liquid Nitrogen | |

| Liquid Natural Gas | ||

| Hydrogen | ||

| Oxygen | ||

| Other Gases | ||

| By End-user Industry | Oil and Gas | |

| Energy and Power | ||

| Chemicals | ||

| Food and Beverage | ||

| Medical | ||

| Other End-user Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current Cryogenic Valves Market size?

The market is valued at USD 3.41 billion in 2026 and is forecast to grow to USD 4.19 billion by 2031.

Which region leads demand for cryogenic valves?

Asia-Pacific holds the top regional position with 26.10% of revenue in 2025, driven by LNG import growth and expanding gas infrastructure.

Which product type has the largest cryogenic valves market share?

Ball valves lead with 33.74% share owing to tight shut-off performance in LNG and petro-chemical applications.

What gas segment is expected to grow fastest?

Hydrogen-handling valves are projected to register the highest 5.62% CAGR to 2031 as green-hydrogen investments accelerate.

What standards govern cryogenic valve safety in North America?

Key regulations include ASME B31.3 process piping, ASME VIII pressure vessel code updates, MSS SP-158 testing protocols, and 49 CFR transport rules.

Page last updated on: