Cold Chain Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

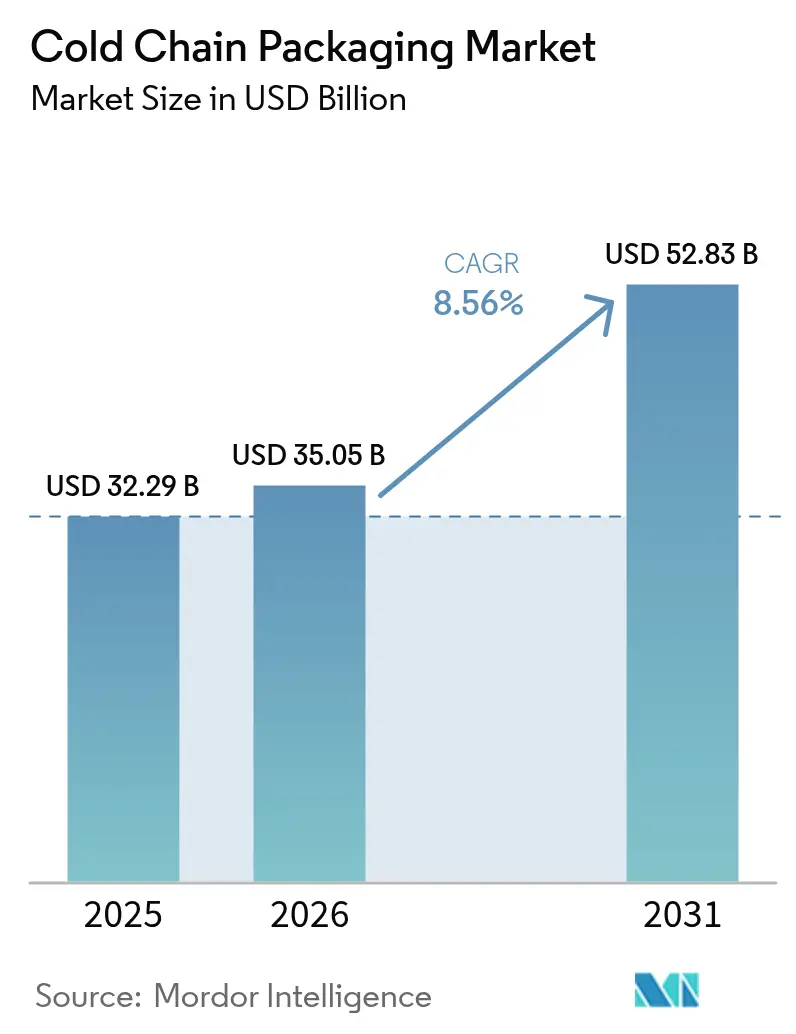

| Market Size (2026) | USD 35.05 Billion |

| Market Size (2031) | USD 52.83 Billion |

| Growth Rate (2026 - 2031) | 8.56% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cold Chain Packaging Market Analysis by Mordor Intelligence

The cold chain packaging market size was valued at USD 32.29 billion in 2025 and estimated to grow from USD 35.05 billion in 2026 to reach USD 52.83 billion by 2031, at a CAGR of 8.56% during the forecast period (2026-2031). Growth is underpinned by rising biologics volumes, expanding e-commerce grocery fulfilment, and global vaccine initiatives that standardize temperature-controlled distribution. Regulatory frameworks such as the United States Food and Drug Administration’s 21 CFR 600.15 and the European Union’s new Packaging and Packaging Waste Regulation compel validated solutions, while real-time IoT monitoring elevates performance expectations. Consolidation among logistics majors amplifies technology diffusion, and corporate ESG targets accelerate the pivot toward reusable and bio-based formats, reshaping supplier strategies across the cold chain packaging market.

Key Report Takeaways

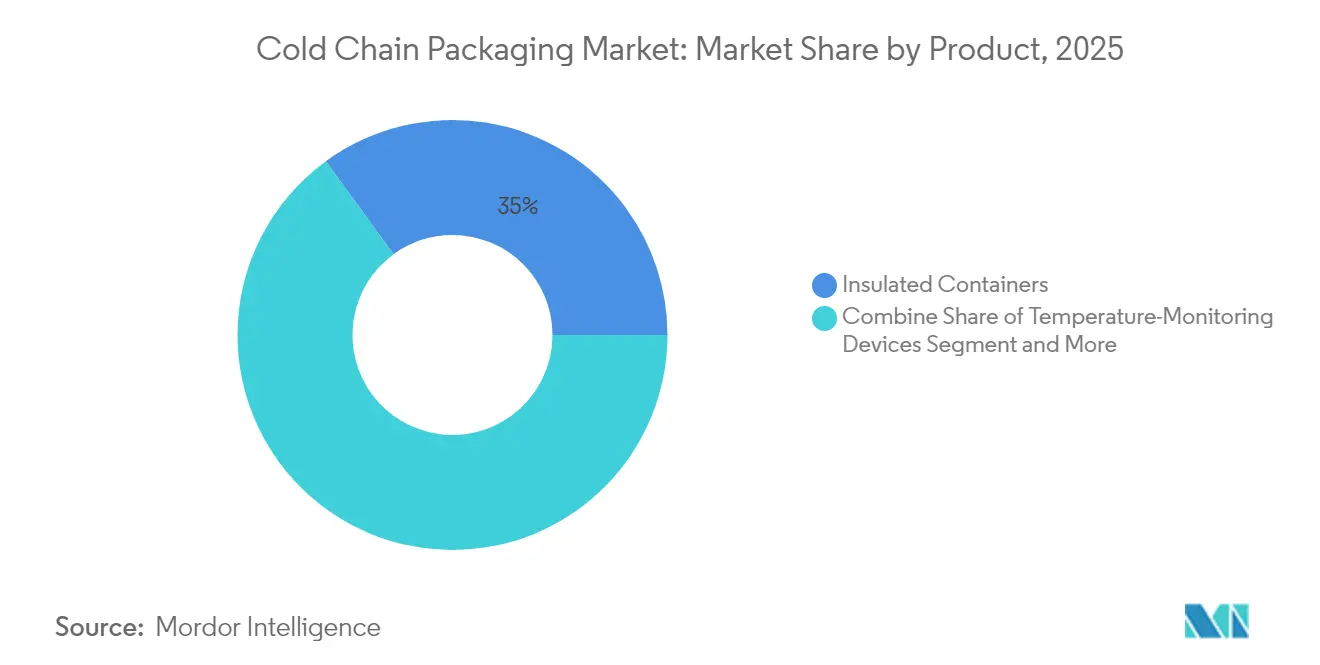

- By product, insulated containers led with 35.02% revenue share in 2025; temperature-monitoring devices are forecast to grow at a 12.44% CAGR to 2031.

- By packaging system, passive solutions held 54.88% of the cold chain packaging market share in 2025, while hybrid systems record the highest projected CAGR at 10.05% through 2031.

- By material, expanded polystyrene accounted for 39.87% share of the cold chain packaging market size in 2025; bio-based phase change materials are advancing at an 10.84% CAGR through 2031

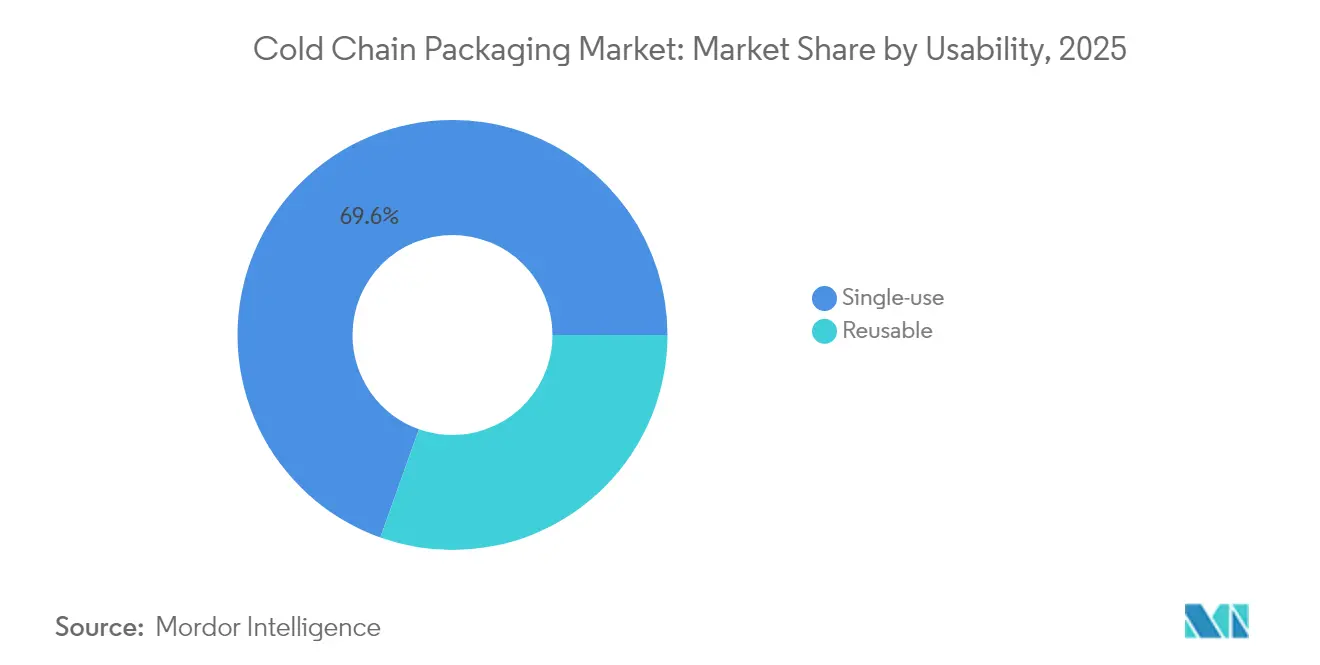

- By usability, single-use formats commanded 69.55% share in 2025, whereas reusable solutions are projected to expand at 9.29% CAGR to 2031.

- By application, pharmaceuticals and biotechnology captured 44.76% of the cold chain packaging market in 2025; clinical trials and diagnostics are expected to grow at 10.98% CAGR by 2031.

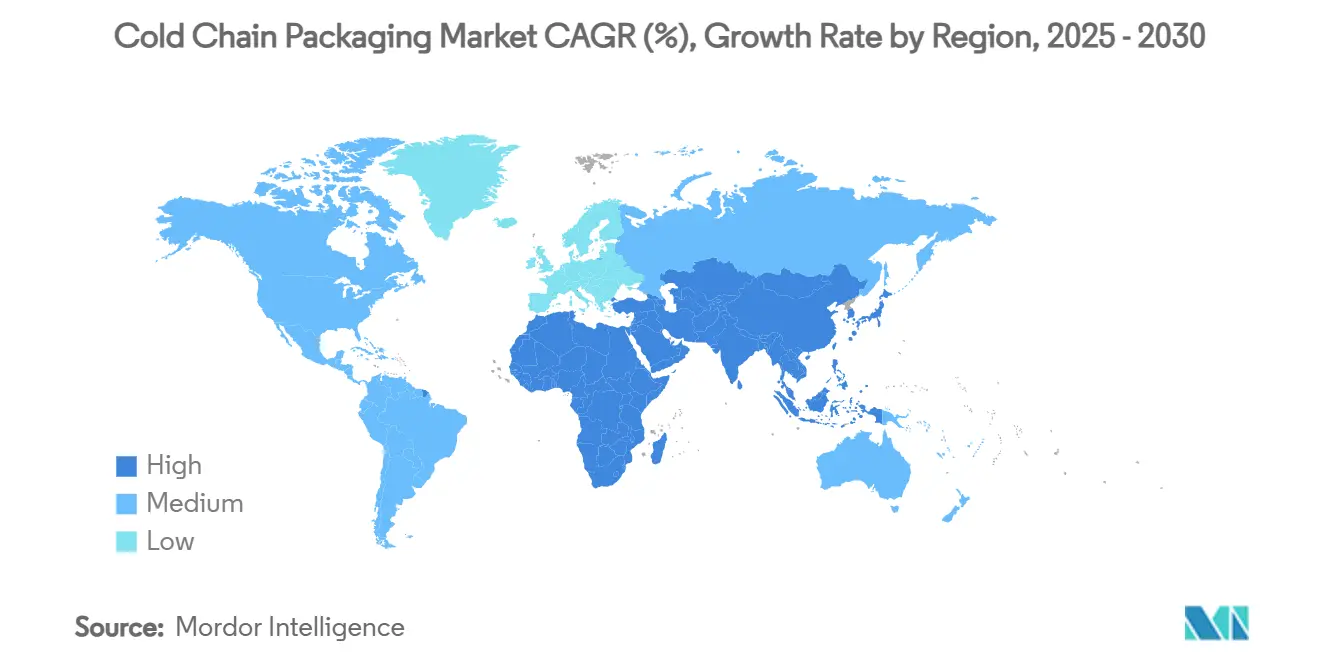

- By geography, Europe led with 38.52% share in 2025, while Asia-Pacific is set to expand at 11.63% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cold Chain Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Biologics and cell-/gene-therapy logistics | +1.8% | North America & Europe | Medium term (2-4 years) |

| E-commerce grocery and meal-kit expansion | +1.5% | Asia-Pacific and North America | Short term (≤ 2 years) |

| Global vaccine programmes | +1.2% | Asia-Pacific, Middle East & Africa, Latin America | Medium term (2-4 years) |

| Decentralized clinical-trial parcels | +0.9% | North America, Europe, expanding Asia-Pacific | Long term (≥ 4 years) |

| Reusable passive shippers for ESG compliance | +0.7% | Europe and North America | Long term (≥ 4 years) |

| Insurer-driven smart indicator uptake | +0.6% | Developed markets worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Boom in Biologics and Cell-/Gene-Therapy Logistics

Nearly half of new pharmaceuticals require temperature control, and many advanced therapies need cryogenic conditions below -150 °C. In January 2025 Cryoport introduced the HV3 shipper that maintains such ultra-low levels for prolonged periods, illustrating the sector’s shift toward specialised designs. [1]Cryoport, “Cryoport Unveils HV3 Cryogenic Shipping System for Advanced Therapies,” gasworld.com The FDA’s biologics licensing requirements demand validated evidence of stability throughout transit, making packaging qualification integral to product approval.[2]U.S. Food and Drug Administration, “Biologics License Applications and Master Files,” federalregister.gov Personalised medicine trends intensify shipment frequency and value, driving premium demand across the cold chain packaging market.

Expansion of E-commerce Grocery and Meal-Kit Delivery

Online grocery volumes for chilled and frozen foods increase the need for lightweight, space-efficient insulation that withstands last-mile variability. HelloFresh employs AI to adjust pack configuration to weather and route specifics, demonstrating how data drives material selection. Ranpak’s curbside-recyclable climaliner Plus, launched April 2024, offers 72 hours of thermal protection and responds to consumers’ sustainability expectations. These innovations expand the cold chain packaging market beyond traditional pharmaceutical lanes.

Global Vaccine Initiatives in Emerging Nations

Gavi, UNICEF and WHO establish procurement frameworks that set global performance baselines. Ethiopia’s 2024 solar electrification of 300 clinics underscores infrastructure constraints that packaging must overcome. Freeze-preventive cold boxes endorsed by WHO eliminate ice-pack conditioning and reduce wastage in rural deployments. Such programmes push suppliers toward rugged, rapidly deployable designs, sustaining demand across the cold chain packaging market.

Decentralized Clinical-Trial Parcel Demand

Regulatory support for direct-to-patient models increases shipment counts while shrinking payloads. Digital display labelling, recognised by ISPE in 2025, allows real-time multilingual updates without relabelling. [3]ISPE, “Digital Display Labelling in Clinical Supplies,” ispe.org Packaging must protect sensitive samples under varied domestic storage conditions, favouring extended-duration passive systems equipped with smart sensors. Drone-compatible formats are also gaining traction, enhancing service reach for remote participants.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Polymer feedstock price volatility | -1.4% | Global, pronounced Asia-Pacific | Short term (≤ 2 years) |

| EU circular-economy limits on EPS | -0.8% | European Union | Medium term (2-4 years) |

| Air-freight capacity squeeze for bulky shippers | -0.6% | Global air-cargo hubs | Short term (≤ 2 years) |

| Lithium battery limits on active systems | -0.4% | Worldwide air transport routes | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Polymer Feedstock Price Volatility

Upward swings in polyethylene and polypropylene costs compress converter margins and can delay switching to reusable packaging that carries higher upfront spend. Smaller producers often lack hedging mechanisms, prompting them to rationalise portfolios and prioritise high-value pharmaceutical accounts.

EU Circular-Economy Limits on EPS

The Packaging and Packaging Waste Regulation effective February 2025 obliges full recyclability by 2030. Makers accelerate alternative developments; DS Smith’s TailorTemp fibre solution, launched January 2025, keeps goods cool for 36 hours while fitting curbside recycling streams DS Smith. Mandatory extended-producer responsibility fees raise compliance costs, nudging the cold chain packaging market toward bio-based materials.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Smart Monitoring Drives Innovation

Insulated containers provided the backbone of shipments and accounted for 35.02% of the cold chain packaging market in 2025. Despite this dominance, temperature-monitoring devices post a 12.44% CAGR as supply chains demand continuous visibility. Smart labels such as Timestrip’s semaglutide indicator extend compliance to high-value biologics, capturing adoption across healthcare providers.

The convergence of IoT chips and low-power networks upgrades passive boxes into connected assets. SkyCell’s 1500X hybrid container runs for 270 hours and transmits live data, illustrating how monitoring devices integrate with insulation substrates to limit excursions. These advances attract insurers that now reward proven risk reduction, expanding addressable volumes for device makers within the cold chain packaging market.

By Packaging System: Hybrid Solutions Gain Momentum

Passive shippers retained 54.88% share of the cold chain packaging market size in 2025, valued for simplicity and regulatory familiarity. Hybrid formats, however, post the fastest 10.05% CAGR by embedding sensors and limited power assistance inside traditional shells, thereby balancing cost and control. Va-Q-Tec’s Thermal Coat adds an intelligent layer to legacy boxes and reduces reliance on fully powered units.

Global airlines tighten lithium-battery carriage rules, capping state-of-charge at 30%, which constrains active container usage. Solar harvesting and supercapacitor integration mitigate this hurdle and push manufacturers toward passive-active hybrids. As compliance audits intensify, shippers with built-in traceability gain procurement preference, strengthening hybrid growth across the cold chain packaging market.

By Material: Bio-Based PCMs Lead Sustainability Shift

Expanded polystyrene dominated 39.87% of the cold chain packaging market share in 2025 owing to cost efficiency. Regulatory scrutiny, however, elevates demand for bio-based phase change materials, which grow at 10.84% CAGR. MDPI research in 2025 showed microencapsulated PCMs delivering 144.3 kJ/kg latent heat, meeting 2 °C to 8 °C pharma requirements while enabling recycling.

Vacuum panels and phenolic foams serve premium niches seeking thinner walls and extended duration. Cellulose sponge cooling media, documented by peer-reviewed studies, add antimicrobial benefits and biodegradability, aligning with EU circular goals. Material diversification therefore accelerates, migrating the cold chain packaging market toward circularity without compromising performance.

By Usability: Reusable Systems Gain ESG Traction

Single-use designs still occupied 69.55% of shipments in 2025 due to contamination control and logistical ease. Corporate sustainability pledges now favour loops: Cold Chain Technologies targets elimination of 100 million lb of landfill waste by 2025 through reusable fleets, reporting 60% fossil-fuel savings on mature lanes.

Asset-tracking via IoT reduces loss rates and maximises turns, shortening payback to fewer than eight trips for high-frequency routes. Rental models such as Sonoco’s Orion r® service shift capex to opex, widening adoption among mid-sized pharma exporters. These incentives underpin the 9.29% CAGR for reusable formats across the cold chain packaging market.

By Application: Clinical Trials Propel Specialized Demand

Pharmaceuticals and biotechnology represented 44.76% of revenue in 2025, driven by strict 2 °C to 8 °C and -20 °C protocols. Decentralized clinical trials lift demand for small, patient-direct cartons and drive an 10.98% CAGR in the segment. ISPE-recognised digital labelling eliminates manual over-stickering, cutting errors and meeting multilingual rules.

Food applications remain volume heavy, especially dairy and frozen desserts that require moderate hold times. Cross-pollination of pharma-grade indicators into premium seafood shipping raises quality benchmarks. Chemical and industrial flows use cryo-friendly drums for specialty resins, adding incremental demand to the cold chain packaging market.

Segment Analysis: By End-User Application

Geography Analysis

Europe’s 38.96% share in 2024 reflects mature pharmaceutical clusters, advanced infrastructure, and regulatory emphasis on carbon reduction. The European Medicines Agency updated guidance in 2025, prompting wider validation of reusable systems. Va-Q-Tec’s German facilities anchor regional innovation, while new Dutch production from Cold Chain Technologies shortens lead times for life-science clients.

Asia-Pacific records the highest 12.02% CAGR to 2030, fuelled by pharmaceutical capacity expansions in India and rising biologics output in South Korea. Government vaccine programmes mobilise refrigerated logistics, and local suppliers partner with Cryoport’s new United Kingdom hub to replicate best practice regionwide. As infrastructure scales, regional players increasingly specify hybrid containers to navigate variable power networks, strengthening the cold chain packaging market in the region.

North America continues to invest in serialisation and traceability under the Drug Supply Chain Security Act, reinforcing demand for smart shippers. Cross-border trade with Mexico sustains temperature-controlled produce flows, while Canada’s biologics firms pilot bio-based PCMs. Middle East and Africa benefit from Gavi-backed solar-powered storage that lifts vaccine coverage, and Latin America improves seafood exports through insulated pallet covers. This diverse landscape ensures the cold chain packaging market remains geographically balanced with Asia-Pacific supplying the lion’s share of incremental growth.

Regulatory Landscape

Regulatory compliance in cold chain packaging is anchored in GDP-aligned validated distribution controls, which drive packaging qualification, temperature mapping, and documentation requirements across lanes. In Europe, GDP guidance remains grounded in the 5 November 2013 guideline (2013/343/01), and the EMA signaled a shift back to normal enforcement cadence when it confirmed that, as of 24 February 2025, blanket extensions of GDP certificates are no longer granted and national authorities resumed regular on-site inspections. This increases the bar for shippers, data loggers, and validation service providers that support audited distribution networks.

Sustainability and circular-economy policy also affects material choices and end-of-life design. The EU Packaging and Packaging Waste Regulation effective February 2025 tightens recyclability and extended producer responsibility expectations, which accelerates substitution away from expanded polystyrene toward fiber-based and other circular-ready insulation formats already being commercialized for temperature-controlled applications. At the global health-system level, WHO guidance for storage and distribution of time- and temperature-sensitive pharmaceutical products continues to set widely referenced benchmarks for handling and packaging performance in emerging-market vaccine and medicine programs.

Competitive Landscape

The cold chain packaging market is moderately fragmented yet consolidating. Global integrators pursue scale and technology depth; DHL’s March 2025 acquisition of CRYOPDP added 600,000 annual life-science shipments and widened reach in Asia-Pacific and EMEA. TOPPAN’s USD 1.8 billion purchase of Sonoco’s Thermoformed and Flexible Packaging unit broadened its sustainable material suite.

Incumbents such as Sonoco ThermoSafe, Pelican BioThermal, and Va-Q-Tec defend share through patent portfolios in vacuum insulation and hybrid monitoring. Emerging tech suppliers like Wiliot embed postage-stamp-sized sensors that broadcast via Bluetooth, turning every box into a data node. Strategic alliances flourish; Envirotainer’s 2024 pact with a leading airline promotes sustainable aviation fuel usage within temperature-controlled lanes.

Competition now hinges on aligning performance with recyclability. DS Smith’s fibre-based TailorTemp, Ranpak’s paper-based thermal liners, and SkyCell’s long-run hybrid containers differentiate on verified carbon savings. Suppliers failing to invest in circular-ready platforms risk exclusion from pharmaceutical vendor lists, sharpening innovation cycles across the cold chain packaging market.

Cold Chain Packaging Industry Leaders

Cold chain Technologies

Cryopak

Sonoco Thermosafe

Sofrigam Company

Softbox Systems Ltd

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

An opportunity is emerging where tighter compliance requirements intersect with the need to reduce friction in qualification for shippers moving temperature-sensitive pharmaceuticals and clinical supplies. Pre-qualified, standards-aligned packaging platforms can reduce validation burden across decentralized parcel flows, supporting uptake of modular, pre-certified shipper families and integrated monitoring. The April 2026 launch of Altor Solutions Odyssey pre-certified thermal shippers aligned to ISTA 7E ambient profiles illustrates how qualification needs are translating into configurable insulation options, giving users more repeatable performance across lanes and seasons.

Infrastructure build-outs and gateway-centric cold chain networks also create space for packaging suppliers that combine physical protection with operational services such as reverse logistics, refurbishment, and asset tracking in high-throughput corridors. Americold and EQT announced a USD 1.3 billion North American cold storage joint venture in May 2026, and Americold opened an integrated import-export cold chain facility at Port Saint John in June 2026 with DP World and CPKC, highlighting investment into hubs where packaging turnover, preconditioning, and reuse loops can be industrialized. In emerging markets, Ethiopia inaugurated a USD 30 million cold storage facility in Addis Ababa in May 2026 to reduce post-harvest losses, which supports demand for durable insulation and last-mile temperature assurance as refrigerated capacity extends beyond major urban centers.

Recent Industry Developments

- June 2026: Cold Chain Technologies expanded its EcoFlex reusable parcel shipper service into Europe, supported by operational hubs in the UK, Netherlands, and Ireland. The expansion broadens access to managed reuse loops and reverse logistics for pharma parcel lanes, helping customers cut single-use waste while maintaining validated performance.

- May 2026: Cold Chain Technologies partnered with Gobi Technologies to support cell and gene therapy distribution using the Altai self-cooling thermal shipper. The addition of a self-cooling option targets high-value therapy workflows where excursion risk and operational complexity are elevated, strengthening premium shipper portfolios in advanced-therapy logistics.

- June 2024: Cold Chain Technologies opened a manufacturing and distribution center in Breda, Netherlands, expanding regional supply capacity. The facility improves lead times and service coverage for European customers and supports scaling of both single-use and reusable packaging programs closer to demand centers.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers packaging products and systems designed to keep goods within a required temperature band during storage and transport, mainly for chilled and frozen foods and for temperature-sensitive healthcare shipments. It includes both passive and active cold chain packaging used from the shipper to the destination.

Scope exclusions: We exclude the value of refrigerated transport and cold storage services, as well as temperature-monitoring devices sold as standalone hardware.

Segmentation Overview

- By Product

- Insulated Containers

- Insulated Shippers

- Refrigerants Gel Packs and PCMs

- Temperature-Monitoring Devices

- Vacuum-Insulated Panels

- Dry-Ice Systems

- By Packaging System

- Active Systems

- Passive Systems

- Hybrid Systems

- By Material

- Expanded Polystyrene (EPS)

- Polyurethane (PUR)

- Vacuum Insulation Panels (VIP)

- Expanded Polypropylene (EPP)

- Bio-based PCMs

- Corrugated Cardboard with Barrier Liners

- High-performance Foams (Phenolic, PIR)

- By Usability

- Single-use

- Reusable

- By Application

- Pharmaceuticals and Biotechnology

- Clinical Trials and Diagnostics

- Dairy and Frozen Desserts

- Meat and Seafood

- Other Application

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the starting structure of the market and to anchor demand assumptions with real-world shipment and production signals. We leaned on public sources such as USDA and FDA releases, CDC cold chain guidance, UN Comtrade trade statistics for packaging materials, and USITC tariff and import data. For air cargo handling context, we also reviewed publications from groups such as the International Air Transport Association.

To keep the packaging scope clean, we also reviewed company annual reports, investor presentations, and product catalogs to separate packaging revenue from logistics services. Where needed, we checked a paid import and export shipment-level database and a paid patent database to confirm adoption patterns (for example, insulation formats and phase-change material activity) without overstating what can be proven from public information alone. The sources listed here are illustrative, and many other public and paid references were used for data collection, validation, and clarification during the study.

Primary Interviews and Surveys

Primary interviews and short surveys were used to pressure-test what desk research could not answer cleanly, including typical shipper configurations, reuse rates, and how buyers decide between active versus passive solutions by lane length and risk level. We spoke with packaging manufacturers, distributors, cold chain users, and logistics stakeholders across APAC, EMEA, and the Americas, so regional handling practices and compliance expectations could be reflected in the final assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 20% | APAC: 43% |

| Mid tier: 45% | Functional/Unit leaders: 37% | EMEA: 34% |

| Smaller Players: 22% | Managers: 43% | Americas: 23% |

Market-Sizing & Forecasting

The sizing model starts from a top-down build where temperature-sensitive shipping activity is reconstructed by application, and then packaging intensity is applied to that demand pool. For example, we map cold chain volumes to typical shipper units, payload protection requirements, and average pack-out mixes, which are then converted into value using observed price bands.

Key inputs used to keep the math realistic include the split of chilled versus frozen shipments, the share of active versus passive systems, average shipper lifecycles and reuse rates, insulation material mix (such as EPS, PUR, and VIP), and the adoption of parcel-friendly formats driven by direct-to-consumer delivery. We adjust these variables by region using signals such as cold storage expansion, pharma shipment growth, and trade flows for insulated packaging components.

Forecasts were developed using scenario analysis supported by short trend lines on a few leading indicators, including biopharma pipeline activity, vaccine and specialty drug distribution needs, and food export growth. Bottom-up approximations were used as a check, such as sampled supplier capacity, channel checks on average selling prices, and a limited roll-up of well-tracked packaging formats. Where gaps remained, we handled them by applying conservative penetration ranges that were validated in interviews.

Data Validation & Update Cycle

Outputs are checked in layers so a single assumption does not drive the result unnoticed. We compare country and regional totals against independent signals, including cold chain trade flows, insulated material demand indicators, and known adoption trends for reusable shippers, then investigate any large variance before sign-off.

A second analyst reviews the model logic, units, and conversions. After that, follow-up questions are sent back to selected interviewees when a data point falls outside the expected range. Reports are refreshed annually, and interim updates are made when material events occur, such as regulation changes, major capacity additions, or supply disruptions that can move pricing. Before delivery, one last review pass is completed so clients receive the most current view available.

Mordor Intelligence's Cold Chain Packaging Market Size Measured Against Other Published Estimates

Different published market sizes for cold chain packaging can look far apart even when they cite similar demand drivers, because each study makes its own calls on what to include, the base year used, and how prices and mix shift over time. We explain these choices clearly so buyers understand what the number does and does not represent.

The biggest gap drivers in this market are usually whether cold storage and refrigerated transport services are blended into the packaging value, how reusable systems are counted across multiple trips, and how active solutions are priced across regions. Some estimates also apply aggressive price escalation assumptions or extend the forecast horizon, which can inflate near-term comparisons when mapped back to the same year and currency timing.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 35.05 B (2026) | |

| Industry Publisher A | USD 30.88 B (2025) | This figure is anchored to a 2025 base and uses a longer forecast window, and it also appears to blend adjacent cold chain activities like warehousing and transportation into the packaging view in some cuts, which shifts the comparable 2026 packaging-only value. |

| Global Publisher B | USD 35.56 B (2025) | This estimate is presented on a factory-gate revenue basis and can treat packaging and related services as a bundled offering, and it uses faster historic-to-forecast step-ups that can move the 2025 to 2026 bridge more sharply than a packaging-unit-driven approach. |

The spread in the table mainly comes down to scope boundaries and how reuse, pricing, and service bundling are treated from one year to the next. By keeping refrigerated logistics services out of the value total and by tying pack-out and reuse assumptions back to observed shipment patterns and interview checks, the number stays easier to reconcile across regions and applications, which is the modeling choice applied by Mordor Intelligence.

Key Questions Answered in the Report

What is the current cold chain packaging market size and expected growth?

The market stands at USD 35.05 billion in 2026 and is projected to reach USD 52.83 billion by 2031, reflecting an 8.56% CAGR.

Which segment is growing fastest within the cold chain packaging market?

Temperature-monitoring devices lead with a 12.44% CAGR as supply chains prioritise real-time visibility.

How do sustainability regulations influence material choices?

The EU requirement for full recyclability by 2030 accelerates shifts from EPS to bio-based PCMs and fibre-based insulation solutions.

Why are hybrid packaging systems gaining traction?

Hybrid shippers merge passive insulation with smart sensors, balancing cost with regulatory compliance, and are expanding at 10.05% CAGR.

What drives Asia-Pacific’s rapid cold chain packaging market growth?

Pharmaceutical manufacturing expansion, vaccine logistics, and modernising refrigeration infrastructure push the region to a 11.63% CAGR.

How are reusable packaging formats affecting total cost of ownership?

IoT-enabled tracking and rental models reduce loss and capital expenditure, cutting payback periods to fewer than eight shipping cycles for high-frequency lanes.

Page last updated on: