Coffee Capsules And Pods Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

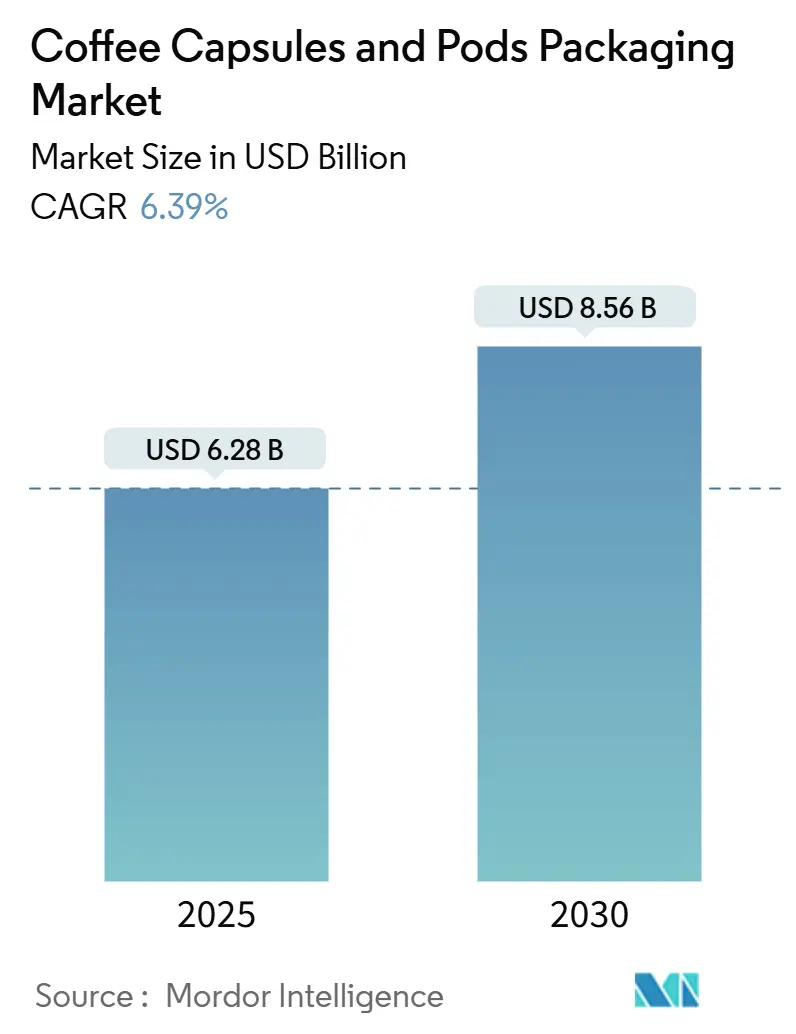

| Market Size (2025) | USD 6.28 Billion |

| Market Size (2030) | USD 8.56 Billion |

| Growth Rate (2025 - 2030) | 6.39% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Coffee Capsules And Pods Packaging Market Analysis by Mordor Intelligence

The coffee capsules and pods packaging market was valued at USD 6.28 billion in 2025 and is projected to reach USD 8.56 billion by 2030, growing at a 6.39% CAGR. This growth trajectory stems from rising demand for convenient single-serve beverage solutions, premiumization of at-home coffee rituals, and sustained innovation in biodegradable materials that address tightening sustainability regulations. Brand owners continue to expand their proprietary capsule ecosystems, encouraging packaging suppliers to invest in oxygen-barrier biopolymers, smart labeling, and vertically integrated foil lines that mitigate raw material volatility. Meanwhile, patent expirations on early Nespresso-compatible designs amplify price competition, sharpening the focus on cost-efficient sustainable formats. Supply chain disruptions for aluminum and EVOH resins further accelerate the search for multi-layer compostable films that preserve freshness without compromising circularity mandates.

Key Report Takeaways

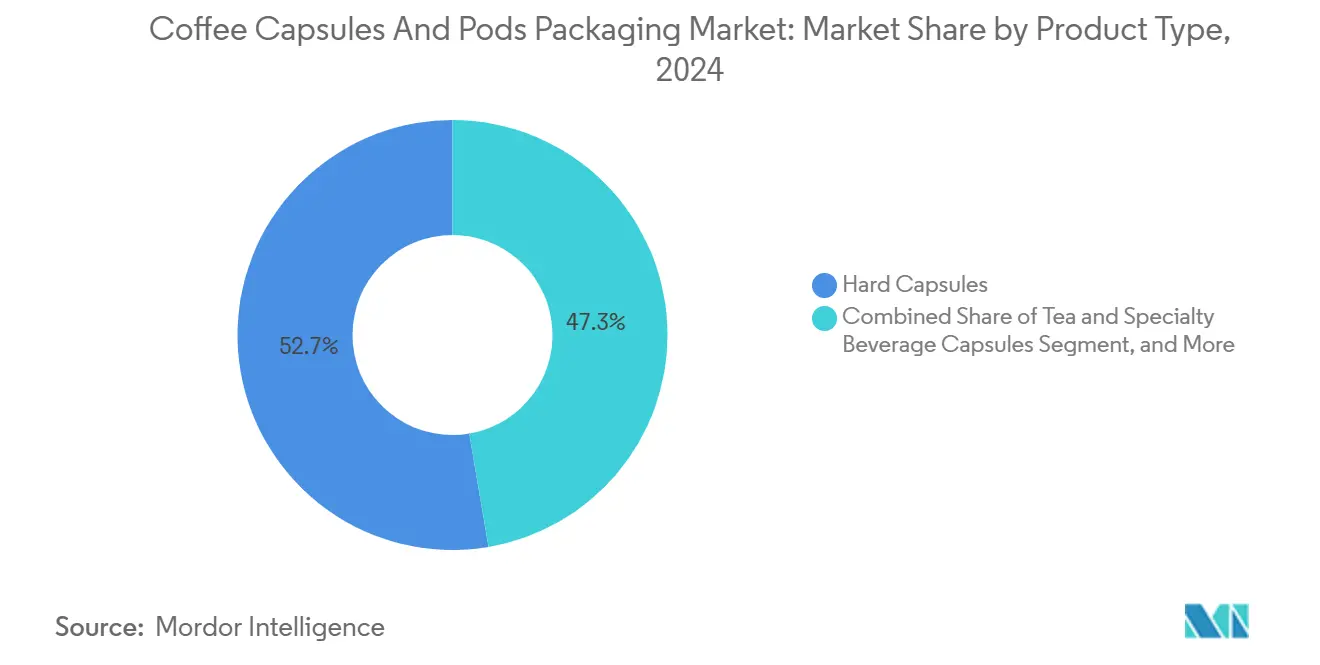

- By product type, hard capsules captured 52.67% of the coffee capsules and pods packaging market share in 2024.

- By material type, the coffee capsules and pods packaging market size for biodegradable solutions is projected to grow at a 7.74% CAGR between 2025–2030.

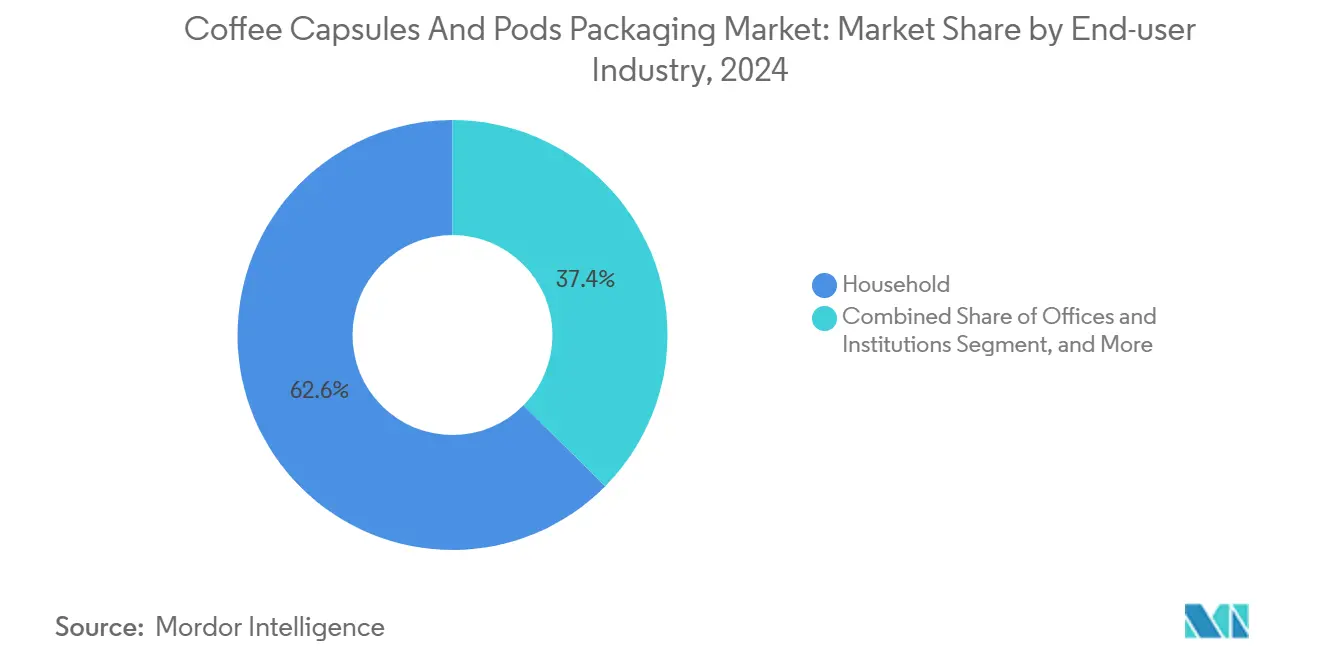

- By end user, household consumption captured 62.58% of the coffee capsules and pods packaging market share in 2024.

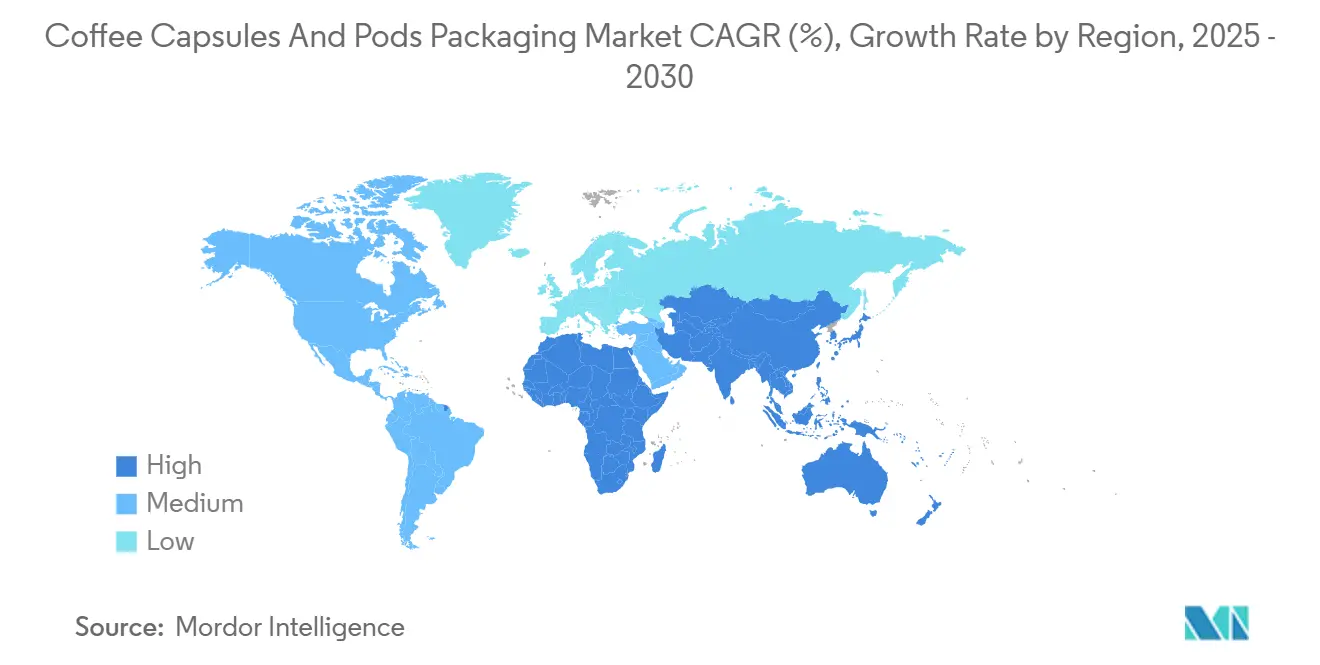

- By geography, the coffee capsules and pods packaging market size for Asia-Pacific is projected to grow at a 9.18% CAGR between 2025–2030.

Global Coffee Capsules And Pods Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Consumer Demand for Convenient Single-Serve Coffee Formats | +1.40% | Global, with strongest growth in APAC emerging markets | Medium term (2-4 years) |

| Premiumization of At-Home Coffee Consumption | +1.20% | North America and Europe, expanding to urban APAC | Long term (≥ 4 years) |

| Expansion of Capsule Machine Installed Base in Emerging Markets | +0.8% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Surge In Private-Label Capsule Packaging Outsourcing by Supermarket Chains | +0.6% | Europe and North America retail consolidation | Short term (≤ 2 years) |

| Development of Oxygen-Barrier Multi-Layer Biopolymer Films for Compostable Capsules | +0.9% | Europe leading, North America following | Long term (≥ 4 years) |

| Smart Packaging (QR/NFC) Enabling Personalized Brewing Recommendations | +0.7% | North America and Europe premium segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Consumer Demand for Convenient Single-Serve Coffee Formats

Remote work habits increase in-home consumption, driving multi-portion households to seek freshness-preserving packs that extend shelf life across longer replenishment cycles. Disposable income growth in the Asia-Pacific region transforms instant-coffee users into capsule adopters, prompting machine vendors to harmonize brew-pressure profiles and packaging tolerances across brands. The trend pressures suppliers to standardize capsule dimensions while still enabling proprietary lock-in mechanisms, a balance shaped by EU extended producer responsibility rules that already influence material choices. Growing scrutiny of end-of-life impacts motivates converters to pair convenience with compostability, encouraging rapid scale-up of industrial composting infrastructure in metropolitan regions. Packaging formats that achieve this dual target secure shelf prominence at global grocery chains, accelerating the overall trajectory of the coffee capsules and pods packaging market.

Premiumization of At-Home Coffee Consumption

Retailers report that consumers equate thicker walls, metallic finishes, and aroma-retentive linings with café-quality performance, legitimizing small price premiums in a crowded aisle. Leading roasters, therefore, specify crystalline PLA lids and laser-etched branding to communicate value, a design shift that is echoed by rising demand for adaptogen-infused or single-origin beverages, whose volatile flavor compounds require high-barrier, compostable solutions.[1]Source: Matthew Naitove, “PHA/PLA Blends for Coffee Pods Meet EU Compostability Specs,” Plastics Technology, ptonline.com Private-label challengers follow suit by outsourcing to contract packers that guarantee equivalent shelf-life metrics, forcing incumbents to refresh packaging every two to three years. As top brands pledge net-zero scopes, premium imagery now intertwines with lifecycle transparency, linking static QR codes to blockchain-secured farm data that reassures discerning buyers.

Development of Oxygen-Barrier Multi-Layer Biopolymer Films for Compostable Capsules

Collaborative work between Danimer Scientific and TotalEnergies Corbion demonstrated PHA/PLA structures that exceed 0.1 cc·m-2·day-1 oxygen transmission, matching the performance of incumbent aluminum foil lids while decomposing within 180 days under home compost conditions. TÜV certification unlocks European distribution, as Brussels considers mandatory compostability for select single-serve packs, positioning early adopters for regulatory head starts. Commercial viability now hinges on upscaling extrusion and thermoforming lines that handle lower melt strengths without yield loss. Equipment retrofits remain minimal, allowing brown-field factories to convert gradually, a factor that speeds acceptance in family-owned Italian roasting clusters.

Smart Packaging (QR/NFC) Enabling Personalized Brewing Recommendations

Digitally enhanced lids extend on-pack storytelling into post-purchase interaction, enabling apps to auto-adjust brew time, temperature, and water dose based on varietal metadata. Pilot runs at specialty roasters in the United States have recorded scan rates above 32%, demonstrating consumer willingness to engage when perks include loyalty points or recipe tips. IoT-linked refill reminders feed subscription platforms, stabilizing demand forecasts for capsule manufacturers. Implementation costs decline as NFC inlays fall below USD 0.045 per unit in 2025, making the feature economical for mid-tier brands. The collected telemetry guides the development of next-generation capsules, engineered around actual consumer extraction profiles rather than lab presets, thereby closing the loop between packaging design and beverage experience.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustainability concerns over plastic and aluminum waste | -0.8% | Global with strongest regulatory pressure in Europe | Short term (≤2 years) |

| Volatile raw-material prices (aluminum, PLA, EVOH) | -0.5% | Global supply chain impacts, acute in manufacturing hubs | Short term (≤2 years) |

| Limited composting infrastructure in key consuming regions | -0.3% | North America suburban areas, emerging markets | Medium term (2–4 years) |

| Equipment compatibility constraints for novel materials | -0.2% | Global legacy machine installed base | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Sustainability Concerns Over Plastic and Aluminum Waste

Annual discard volumes exceeded 576,000 metric tons in 2024, prompting NGOs and lawmakers to intensify their spotlight on single-use beverage systems. Europe leads with deposit-return pilots and tax disincentives on virgin plastics, forcing retailers to reprioritize end-of-life claims in assortment reviews. Consumer sentiment data show willingness to switch brands if disposal clarity remains ambiguous beyond two clicks on product pages. In the United States, only 27% of households have access to municipal composting, which dilutes the environmental benefits of biodegradable formats and delays full conversion. Brands respond by funding take-back schemes that consolidate used capsules for centralized recycling or industrial composting; however, this approach raises logistical costs that weigh on short-term profitability.

Volatile Raw-Material Prices (Aluminum, PLA, EVOH)

Aluminum premiums spiked to USD 390 per metric ton in early 2025 amid energy-driven smelting cutbacks in Europe, inflating lid costs for hard capsules that rely on foil overwraps. EVOH copolymer shortages, tied to cracker outages in Northeast Asia, extend lead times beyond 90 days, compelling formulators to qualify alternative gas-barrier additives. Meanwhile, PLA trades at multiples of traditional PP resin, challenging the financial case for mass-market compostable pods. Some converters hedge through vertical integration, acquiring stakeholdings in regional recycling plants or bio-resin ventures to stabilize input costs. Others negotiate cost-pass-through clauses with roasters, but intense retail competition caps the acceptable price increases, squeezing margins and tempering the investment pace in the coffee capsules and pods packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Tea Capsules Drive Format Diversification

The segment reached notable scale as brands leveraged capsule familiarity to court health-conscious consumers seeking portion-controlled antioxidants. Tea and specialty beverage capsules are projected to widen their footprint at an 8.75% CAGR, supported by matcha, rooibos, and chai recipes that demand precise temperature profiles to prevent polyphenol degradation. Hard capsules retain primacy through 2030, owing to 52.67% baseline dominance and superior pressure resistance during long supply-chain voyages. Soft pods, typically paper-based, secure artisan niches where lighter extraction suits delicate loose-leaf blends.

Diverse beverage expansion compels packagers to refine multi-pierce lids and micro-perforated filters that modulate flow rate, ensuring fine powders neither bypass nor clog outlets. Premium labels introduce dual-chamber capsules that stage heat exposure, preserving volatile aromas until the final seconds of brewing. The coffee capsules and pods packaging market size for tea derivatives, although smaller today, is set to accelerate as urban Asian consumers migrate from sachet teas to appliance-based convenience. Meanwhile, cross-category cannibalization remains limited because capsule machine owners frequently alternate between coffee and non-coffee drinks on the same day, thereby broadening net unit demand.

By Material Type: Biodegradable Solutions Gain Momentum

Biodegradable formats are projected to chart a 7.74% CAGR through 2030, driven by European supermarket commitments to list only compostable or fully recyclable single-use packs by 2028. Plastic, however, is expected to continue anchoring a 47.29% revenue share in 2024, driven by ingrained converting ecosystems and robust supply availability. Aluminum remains relevant in premium niches targeting oxygen sensitivity below 0.05 cc·m-2·day-1, but faces image challenges tied to its high carbon intensity.

Steady migration toward polylactide blends showcases how circularity targets can coexist with high-barrier expectations when supplemented by thin EVOH co-extrusions. The coffee capsules and pods packaging market size for biodegradable lines is projected to exceed USD 1.4 billion by 2030; however, the actual rollout pace will depend on resin capacity expansions announced in Thailand and the United States. Paper-based hybrid capsules, incorporating bio-based coatings, are gradually gaining favor among boutique roasters seeking a visible fiber look that conveys naturalness. Collectively, these shifts diversify supplier revenue streams and reduce exposure to fluctuations in aluminum prices.

By End-user Industry: Workplace Solutions Accelerate Growth

Household channels captured a 62.58% share in 2024, but large employers are now installing compact brewers to elevate employee experience, driving a 7.94% CAGR for office and institutional demand. Post-pandemic sanitation concerns have spotlighted single-serve formats over communal drip pots, reinforcing product safety messaging and sustaining growth. In canteen and hospital settings, packagers optimize line speeds to satisfy peak-time surges without compromising seal integrity.

Capsule suppliers collaborate with vending-machine OEMs to develop near-frictionless feed mechanisms that accept both branded and white-label pods, thereby expanding menu flexibility. Price sensitivities in education and government accounts spark interest in private-label outsourcing, channeling volume to contract packers adept at thin-wall molding. The convergence of workplace and household taste profiles is steering the coffee capsules and pods packaging market toward modular designs and harmonized materials that serve both channels with minimal specification drift.

Geography Analysis

Europe maintained a 34.73% revenue contribution in 2024, backed by decades of single-serve familiarity and established curbside recycling. The region serves as the proving ground for home-compostable certification, with Germany and France actively piloting expansions of bio-waste collection that could accelerate the adoption of PHA-lined capsules. Regulatory clarity under the Packaging and Packaging Waste Regulation sets ambitious recycling and composting targets, compelling converters to invest early in mono-material laminate lines that facilitate sorting. Northern European consumers exhibit the highest willingness to pay for packaging bearing validated carbon footprints, sustaining premium price tiers.

Asia-Pacific represents the engine of volume growth, climbing at a 9.18% CAGR as rising urban incomes in China, India, and Indonesia unlock affordable coffee appliance purchases. The coffee capsules and pods packaging market size in China alone is forecast to more than double between 2025 and 2030 as local roasters partner with international packagers to integrate bilingual smart labels that educate first-time buyers on machine maintenance routines.[2]Source: China Coffee Association, “China Consumer Coffee Report 2025,” cca.cn Singapore and South Korea set regional benchmarks for QR-enabled traceability, influencing broader acceptance of digital engagement. Production footprints follow demand shifts, with several European converters announcing joint ventures in Vietnam and Thailand to shorten lead times and insulate against ocean-freight volatility.

North America delivers steady mid-single-digit expansion anchored in premiumization and corporate sustainability goals. Retailers allocate more shelf space to certified compostable SKUs, leveraging state-level extended producer responsibility laws in California and Washington that incentivize low-impact designs. Latin America supplies raw coffee yet shows rising domestic consumption, especially in Brazil and Mexico where younger consumers experiment with flavored capsule launches. The Middle East and Africa still trail in machine penetration but reveal high per-capita consumption in United Arab Emirates and Israel, signaling future pockets of rapid growth once local distribution networks mature.

Competitive Landscape

The competitive structure exhibits moderate concentration, with the top five suppliers collectively accounting for roughly 48% of global revenues, positioning the market at a balanced point between scale and innovation from smaller specialists. Amcor, Huhtamaki, and Sonoco leverage multi-continent converting plants and in-house barrier-film research to secure long-term contracts with Nestlé and JDE Peet’s. Vertical integration emerges as a hedge against price swings in aluminum and PLA, as evidenced by Huhtamaki’s investment in a Finnish biopolymer facility that secures feedstock for its proprietary compostable lids.

Niche challengers differentiate themselves through intellectual property related to low-gauge PLA foams or fiber-based valve structures, filing patents that extend beyond capsule walls into entire brew-chamber assemblies. The lapse of Nespresso-related patents accelerates commoditization, motivating incumbents to bundle services such as machine maintenance, analytics, and SKU-level demand forecasting powered by AI. Strategic alliances proliferate: Flo Group and NatureWorks co-develop Keygea pods that weigh just 2.6 grams yet pass industrial compostability audits, demonstrating how joint R&D can close performance gaps with conventional plastics.

Emerging opportunities lie in regionalization. Suppliers who embed finishing assets near high-growth Asia-Pacific markets gain freight savings and currency-hedge benefits while satisfying government localization incentives. Conversely, lack of vertical expertise in specialized foil embossing renders some small players vulnerable to supply chain disruptions, prompting consolidation as evidenced by Alupak’s acquisition of ALUCAPS assets in 2024.[3]Source: Comunicaffe Staff, “Swiss Coffee Capsule Pioneer Alupak to Acquire Global ALUCAPS Business,” Comunicaffe, comunicaffe.com

Coffee Capsules And Pods Packaging Industry Leaders

Amcor plc

Constantia Flexibles International GmbH

Huhtamäki Oyj

Sonoco Products Company

Graphic Packaging International, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: OxBarrier launched its first technology licensing program for patented compostable single-serve capsule designs, following validation by the European Patent Office across 30 countries.

- April 2025: Flo Group and NatureWorks introduced Keygea, a 2.6-gram thermoformed Ingeo PLA pod certified for industrial composting and engineered for high-speed filling lines.

- January 2025: Nestlé acquired Seattle’s Best Coffee from Starbucks, integrating roast-and-ground and K-Cup portfolios while retaining the Global Coffee Alliance distribution agreement.

- January 2025: Nestlé and Starbucks executed their global coffee alliance for USD 7.15 billion, granting Nestlé perpetual rights to commercialize Starbucks-branded packaged coffee in 80+ markets.

Global Coffee Capsules And Pods Packaging Market Report Scope

| Hard Capsules |

| Soft Pods |

| Tea and Specialty Beverage Capsules |

| Other Products |

| Plastic |

| Aluminum |

| Biodegradable |

| Paper |

| Household |

| Hotels, Restaurants, and Catering/Cafés (HoReCa) |

| Offices and Institutions |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Product | Hard Capsules | ||

| Soft Pods | |||

| Tea and Specialty Beverage Capsules | |||

| Other Products | |||

| By Material | Plastic | ||

| Aluminum | |||

| Biodegradable | |||

| Paper | |||

| By End-user Industry | Household | ||

| Hotels, Restaurants, and Catering/Cafés (HoReCa) | |||

| Offices and Institutions | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How big is the coffee capsule and pod packaging market in 2025?

The market is valued at USD 6.28 billion in 2025 and is projected to hit USD 8.56 billion by 2030.

Which region will grow the fastest by 2030?

Asia-Pacific is forecast to post a 9.18% CAGR, outpacing all other regions as capsule machine ownership expands rapidly.

What material segment is advancing the quickest?

Biodegradable and compostable materials are leading with a 7.74% CAGR, driven by regulatory incentives and brand sustainability targets.

What share do hard capsules hold today?

Hard capsules accounted for 52.67% of the global revenue in 2024, owing to their superior barrier properties and broad machine compatibility.

Why are raw material prices a restraint?

Fluctuating costs for aluminum, PLA, and EVOH squeeze converter margins and complicate long-term supply contracts, dampening near-term investment appetite.

How are brands addressing sustainability concerns?

Companies are investing in home-compostable PHA/PLA blends, launching capsule take-back schemes, and adopting mono-material structures to improve recyclability.

Page last updated on: