Nickel Alloys Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

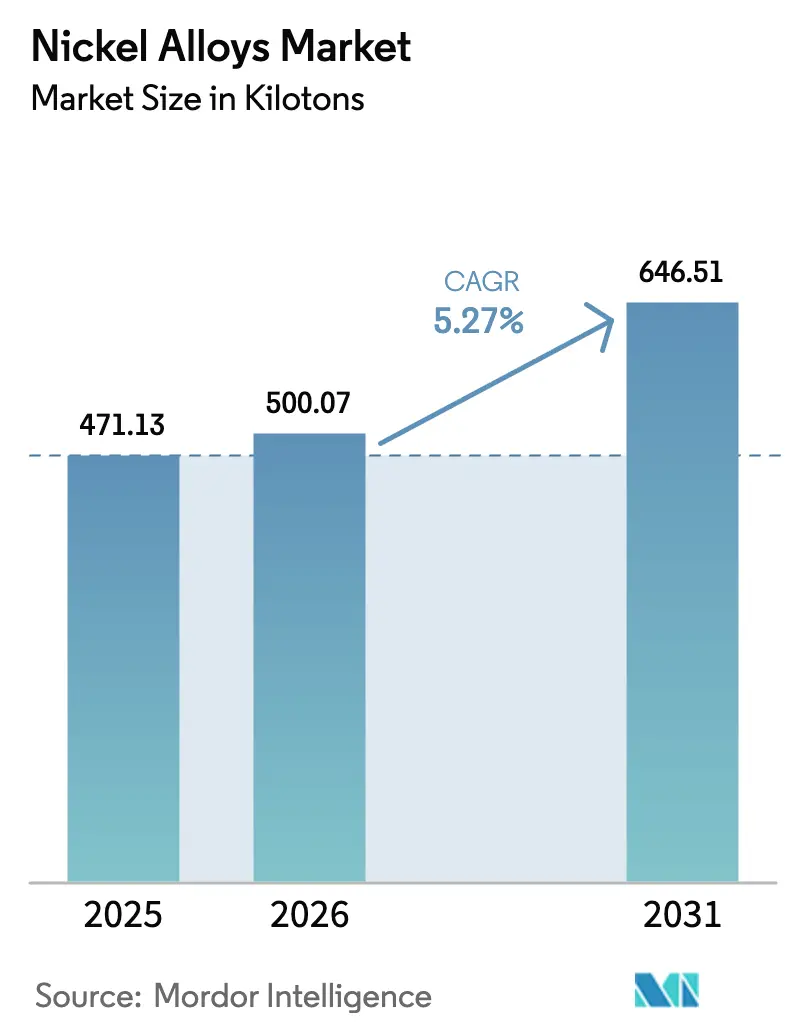

| Market Volume (2026) | 500.07 kilotons |

| Market Volume (2031) | 646.51 kilotons |

| Growth Rate (2026 - 2031) | 5.27% CAGR |

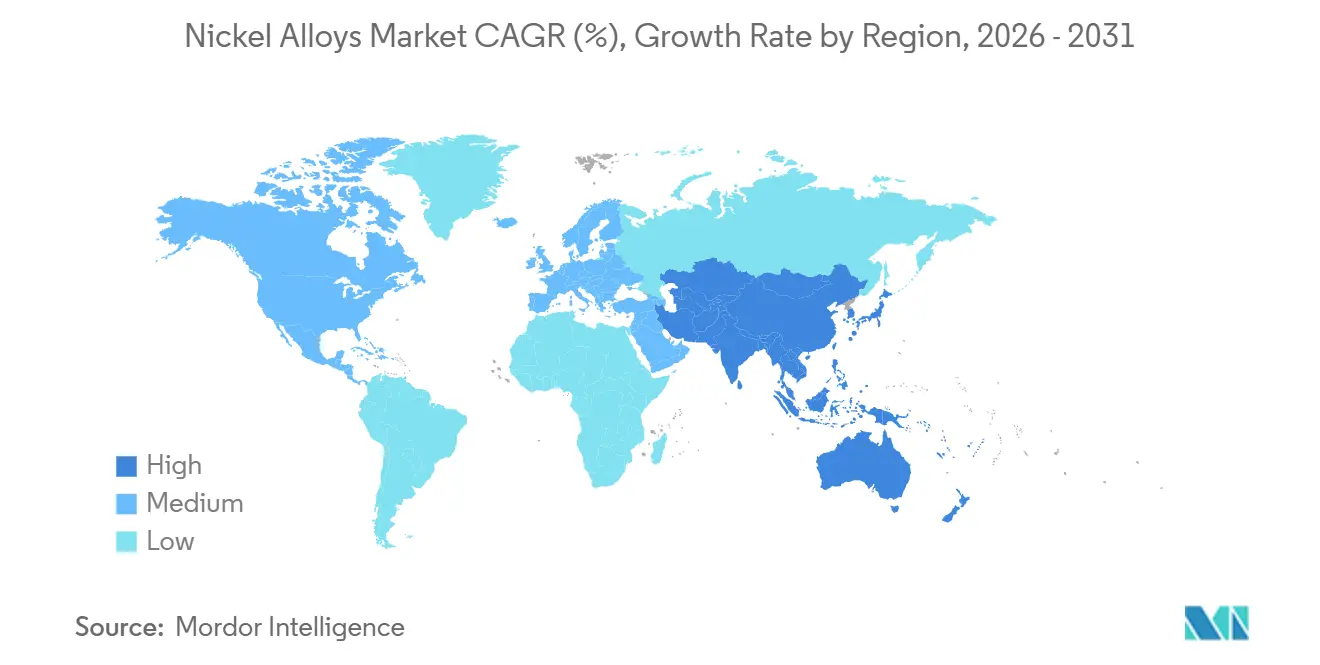

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nickel Alloys Market Analysis by Mordor Intelligence

The Nickel Alloys Market size is expected to increase from 471.13 kilotons in 2025 to 500.07 kilotons in 2026 and reach 646.51 kilotons by 2031, growing at a CAGR of 5.27% over 2026-2031. Growth is being propelled by super-alloy consumption in next-generation aircraft engines, rising volumes of battery-grade Class 1 nickel for high-nickel EV cathodes, and expanding orders for corrosion-resistant alloys in small-modular nuclear reactors and hydrogen turbines. Defense hypersonics programs and space-launch systems add another structural demand layer, while additive manufacturing is shortening prototype cycles and amplifying alloy uptake across multiple end-use sectors. Volatility in London Metal Exchange pricing remains a constraint, yet producers with low-carbon footprints and certified aerospace pedigrees continue to secure premium contracts.

Key Report Takeaways

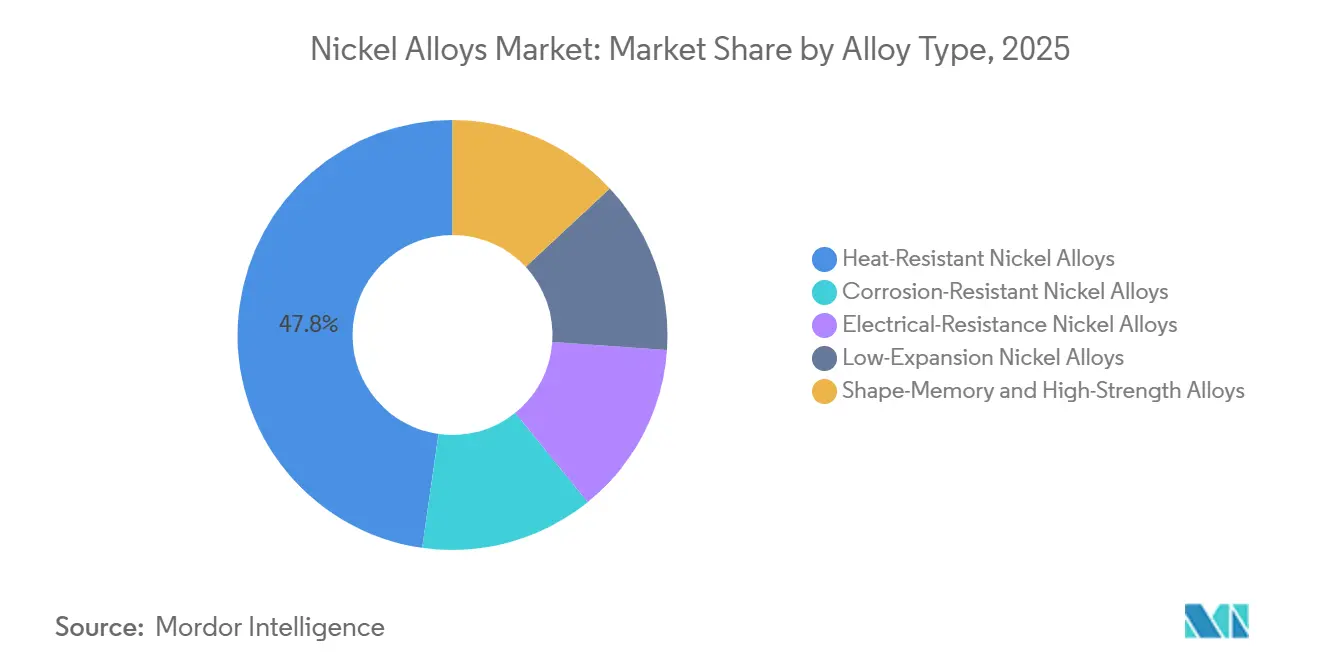

- By alloy type, Heat-Resistant Nickel Alloys (includes superalloys) led with 47.76% nickel alloys market share in 2025, and are forecast to grow at an 6.26% CAGR through 2031.

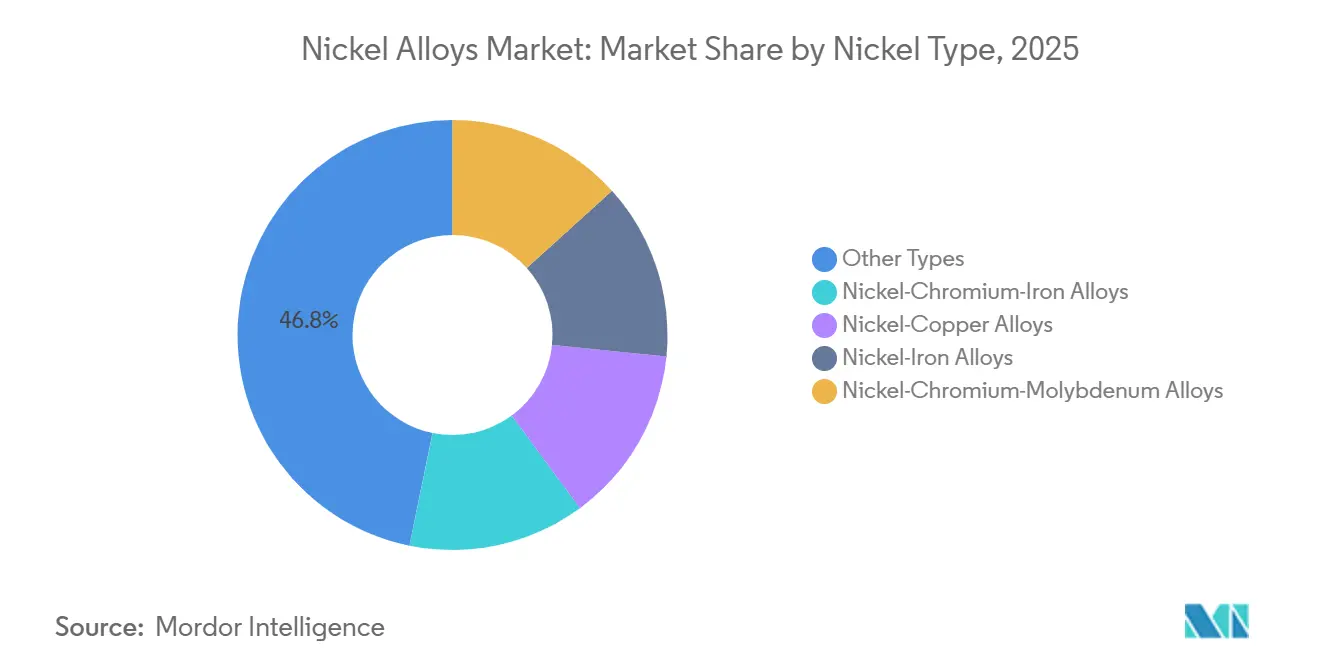

- By nickel chemistry, Other Types held 46.80% of 2025 nickel alloys market size revenue; Nickel-Chromium-Iron Alloys are projected to expand 6.52% annually to 2031.

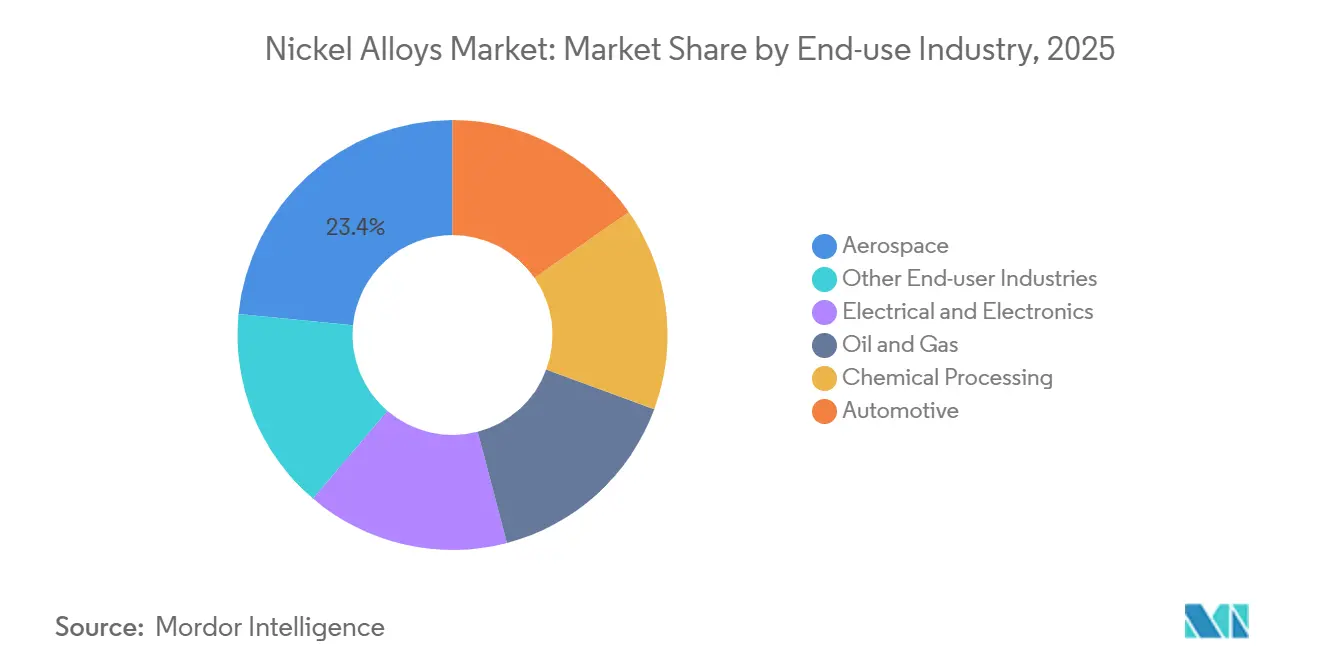

- By end-use, aerospace captured 23.44% revenue in 2025, and is expected to grow at a 7.23% CAGR through 2031.

- By geography, Asia-Pacific accounted for 49.62% of 2025 revenue and is forecast to advance 7.56% annually to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Nickel Alloys Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aerospace super-alloys demand surge | +2.1% | North America, Europe | Long term (≥ 4 years) |

| Battery-grade nickel shift in EV cathodes | +1.8% | Asia-Pacific, North America, EU | Medium term (2-4 years) |

| Small-modular nuclear reactors build-out | +1.3% | North America, Europe, Middle East | Long term (≥ 4 years) |

| Hydrogen turbine retrofits | +1.0% | Europe, Asia-Pacific, Middle East | Medium term (2-4 years) |

| Defense hypersonics and space vehicles | +1.5% | United States, China, India | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aerospace Super-Alloys Demand Surge

Commercial backlogs exceeded 14,000 aircraft in 2024, translating to an estimated 280,000 metric tons of nickel-based super-alloy demand over the next decade. Engine makers are adopting higher-pressure-ratio architectures that operate beyond 1,650 °C, a regime that mandates single-crystal René and Inconel castings with exceptionally tight chemistry windows. Defense programs such as the U.S. Air Force Next Generation Air Dominance fighter require alloys that cycle between −55 °C and 1,200 °C within milliseconds. Additive manufacturing is reducing weight by up to 25% on turbine components although powder feedstock remains three to four times costlier than wrought bar. These aerospace dynamics ensure sustained, high-value pull on the nickel alloys market for at least another decade.

Battery-Grade Nickel Shift in EV Cathodes

High-nickel NMC 811 and NMC 9-5-5 chemistries now deliver energy densities above 250 Wh kg-1, displacing earlier 532 formulations. Automakers outside China are signing multi-year offtake contracts to secure low-carbon Class 1 supply; General Motors committed to 75,000 metric tons from 2026-2030, subject to carbon thresholds below 10 tons CO₂ per ton nickel. The European Union Battery Regulation will impose mandatory carbon-footprint ceilings from 2030, reinforcing demand for responsibly sourced feedstock. While China’s LFP surge diluted nickel intensity in 2025, global battery-grade nickel tonnage still rose on aggregate, locking in a pivotal growth vector for the nickel alloys market.

Small-Modular Nuclear Reactors Build-Out

Factory-fabricated SMRs reduce site construction cycles from ten to under three years and incorporate 150 metric tons of nickel alloys per 300 MWe module[1]United States Department of Energy, “Battery Materials Supply Chain Review 2026,” energy.gov. NuScale received final NRC design approval and is partnering with Romania to deploy six modules by 2030. TerraPower’s Natrium demonstrator specifies Hastelloy X heat exchangers capable of 560 °C service for 60 years. ASME Section III traceability requirements limit eligible suppliers, cementing an attractive, high-barrier avenue for established producers within the nickel alloys market.

Hydrogen Turbine Retrofits

Siemens Energy validated 100% hydrogen combustion on an SGT-400 turbine using Hastelloy X combustor liners in 2024[2]Siemens Energy AG, “Hydrogen-Capable Turbine Validation,” siemens-energy.com . Mitsubishi Power’s JAC class employs single-crystal nickel super-alloys with ≥3 % rhenium to prevent creep rupture at 1,650 °C firing temperatures. Saudi Arabia’s 4 GW NEOM electrolyzer project will need hydrogen-ready turbines for backup power. Higher mass flow raises mechanical stress by 15%, pushing alloy tonnage per megawatt upward and supporting incremental nickel alloys market growth into the 2030s.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nickel supply-chain geopolitical risk | −1.2% | North America, Europe | Short term (≤ 2 years) |

| Volatile LME pricing and hedging costs | −0.9% | Global | Short term (≤ 2 years) |

| High lifecycle CO₂ footprint vs. green-steel options | −1.0% | Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Nickel Supply-Chain Geopolitical Risk

Indonesia’s ore-export ban and downstream mandates have routed 68% of incoming FDI to Chinese-controlled joint ventures, centralizing supply but elevating Western security concerns. The United States invoked the Defense Production Act to fast-track the Tamarack project, yet permitting challenges persist. Jakarta’s WTO appeal against an unfavorable November 2024 ruling prolongs uncertainty, compelling aerospace primes to requalify alternative feedstocks, a process costing up to USD 5 million per grade. This uncertainty tempers near-term volume expansion in the nickel alloys market.

Volatile LME Pricing and Hedging Costs

Post-2022 volatility lifted implied options premiums above 35%, adding USD 800–1,200 t-1 to hedged procurement costs, according to LME settlement data. Smaller alloy mills lack the balance-sheet capacity for multi-year hedges, exposing them to margin erosion when long-term aerospace contracts collide with spot-price weakness. The absence of a deep forward curve beyond 27 months further complicates capital allocation for smelter projects that require five-plus years from study to production. These financial headwinds shave roughly 0.9 percentage points from the projected nickel alloys market CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Alloy Type: Heat-Resistant Nickel Alloys Dominate the Market

In 2025, Heat-Resistant Nickel Alloys, including superalloys, dominated the nickel alloys market with a 47.76% share. Their leadership stems from their indispensable role in high-temperature, high-stress environments. Advanced precipitation-hardened superalloys and directionally solidified variants are preferred for critical applications such as aero-engine hot sections, industrial gas turbines, and hydrogen-fueled power plants operating above 1,000 °C. The expansion of commercial aviation fleets, increasing maintenance cycles, and the development of LNG and hydrogen infrastructures drive consistent demand for forged disks, turbine blades, and combustors. Additionally, retrofitting power generation systems for improved thermal efficiency is boosting the use of higher-creep-strength alloys, supporting long-term consumption.

Heat-Resistant Nickel Alloys (including superalloys) is also the fastest-growing segment, with a projected 6.26% CAGR from 2026 to 2031, driven by additive manufacturing and next-generation propulsion programs. Laser and electron-beam powder-bed fusion enable intricate cooling channels and lighter components, increasing superalloy powder demand and improving material utilization across aerospace supply chains. Thermal-barrier-coated superalloys are gaining traction in small modular reactors and concentrated solar power receivers, while advanced coatings extend service intervals in heavy-duty turbines. Although design optimizations are improving material efficiency per engine, rising engine production, overhaul cycles, and demand for high-temperature industrial equipment offset these gains. As electrification shifts metal demand from traditional alloys, heat-resistant nickel superalloys remain structurally essential, ensuring stable, performance-driven growth in the nickel alloys market.

By Nickel Type: Ni-Cr-Fe is the Fastest Growing Segment

Nickel-Chromium-Iron (Ni-Cr-Fe) Alloys are projected to grow at a 6.52% CAGR from 2026 to 2031, driven by their ability to withstand carburizing and oxidizing atmospheres. The Inconel 600/601/690 family is preferred for ultra-supercritical boilers, hydrogen reformers, and waste-to-energy plants, where higher firing temperatures challenge stainless steels. Coal-to-chemicals projects in Asia-Pacific and refinery heater retrofits in the Middle East are boosting demand for superheater tubing and furnace hardware. Electrification and hydrogen blending are raising operating temperatures, further driving the adoption of Ni-Cr-Fe alloys for their durability and cost efficiency. These alloys are steadily replacing high-alloy stainless steels in heat-treating equipment, sustaining strong growth.

Other Types held the largest market share at 46.80%, including nickel-based superalloys, multi-element compositions, Ni-Cr electrical-resistance alloys, and Ni-Ti shape-memory materials. Superalloys dominate turbine disks, blades, and aerospace fasteners, while multi-element variants support power-generation and space propulsion. Ni-Cr alloys are used in industrial heating elements, and Ni-Ti alloys are expanding in medical devices and smart actuators. Additive manufacturing and powder metallurgy are enabling proprietary compositions for extreme environments, supporting premium pricing and long-term contracts. Despite Ni-Cr-Fe alloys' rapid growth, Other Types retain the largest revenue share due to their diverse applications and material continuity.

By End-Use Industry: Aerospace Leads the Market

In 2025, aerospace accounted for 23.44% of the nickel alloys market and is projected to grow at a 7.23% CAGR from 2026 to 2031, driven by rising global aircraft production and engine replacements. Expanding narrow-body backlogs, next-gen wide-body programs, and increased defense spending are boosting demand for superalloy turbine disks, single-crystal blades, combustors, and high-temp fasteners. Engines with higher bypass ratios and geared turbofans, operating at elevated core temperatures, require more creep-resistant nickel alloys to meet fuel efficiency and emissions standards. Additionally, extended fleet service lives are driving MRO activities, sustaining aftermarket demand for forgings, castings, and repair powders.

Additive manufacturing strengthens aerospace's position by enabling weight-optimized designs and internal cooling channels beyond conventional machining. OEMs certifying printed brackets, heat exchangers, and fuel nozzles for mass production are driving powder demand for laser and electron-beam fusion, improving qualification cycles and buy-to-fly ratios. Space launch vehicles and reusable rocket engines further increase the need for high-strength, oxidation-resistant grades capable of repeated thermal cycles. While sectors like energy transition and chemical processing diversify demand, aerospace remains the cornerstone and growth driver of the nickel alloys market due to its unmatched requirements for extreme temperature resilience, fatigue life, and certification-driven material consistency.

Geography Analysis

Asia-Pacific commanded 49.62% of 2025 revenue and is forecast to advance 7.56% annually to 2031, the fastest among all regions. Indonesia produced 1.8 million tons of nickel ore in 2024 and operates 23 HPAL and RKEF facilities that feed both battery-grade matte and stainless pig iron. China remains the largest stainless producer at 33 million tons in 2024, consuming roughly 1.5 million tons of nickel though the shift toward 200-series grades is lowering intensity per ton. India’s defense build-out lifted domestic orders for Inconel forgings awarded by Hindustan Aeronautics in 2024.

North America benefits from the Inflation Reduction Act’s 30% tax credits for battery components and the CHIPS Act’s USD 52 billion outlay for semiconductor fabs that rely on ultra-low-expansion alloys. ATI’s USD 140 million Pennsylvania expansion targets aerospace super-alloy demand and advanced electrical steels. Europe faces embedded-carbon tariffs under the Carbon Border Adjustment Mechanism that could exceed EUR 2,000 per ton for Indonesian nickel, redirecting buyers to Canadian or Finnish suppliers with lower footprints.

South America remains niche, driven by Brazilian offshore pre-salt fields requiring corrosion-resistant subsea hardware rated to 200 MPa at 2,000 m depths. The Middle East and Africa show project-driven demand, epitomized by Saudi Arabia’s USD 7 billion NEOM industrial cluster and South Africa’s platinum processing upgrades that specify nickel-based alloys for sulfuric-acid leaching circuits. Collectively, these geographic vectors give the nickel alloys market a balanced demand base and mitigate over-reliance on any single consuming region.

Competitive Landscape

The global nickel alloys market is moderately consolidated, with the top five players holding a significant market share. Competitive advantage hinges on AS9100 and ASME Section III accreditation, additive-manufacturing prowess, and demonstrably low carbon footprints. Sandvik’s Osprey unit supplies gas-atomized Inconel and Hastelloy powders that allow engine OEMs to qualify topology-optimized parts without investing in atomizers. Smaller players in the market leverage rapid-turnaround service centers and digital inventories to capture spot opportunities when integrated mills quote 12-16-week lead times. Barriers to entry remain high; nuclear qualification demands a decade of creep-rupture data, and aerospace primes enforce exhaustive supplier audits. High-entropy alloys, now under a NASA patent, signal potential technology disruption yet remain at lab-scale. Overall, capital intensity and certification hurdles anchor a durable competitive moat for incumbents across the nickel alloys market.

Nickel Alloys Industry Leaders

ATI

Haynes International

VDM Metals

CRS Holdings, LLC.

thyssenkrupp Materials NA, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Haynes International signed a five-year, USD 120 million deal with Siemens Energy to supply Hastelloy X combustor liners for hydrogen-capable turbines beginning Q2 2026.

- September 2025: VDM Metals inaugurated a USD 95 million wire-drawing facility in Werdohl, Germany, to produce ultra-fine Alloy 625 and C-276 wire using hydrogen-based annealing, cutting CO₂ emissions by 40%.

Global Nickel Alloys Market Report Scope

Nickel alloys are a metal mixture that contains nickel as the primary constituent. Nickel-based alloys are used in steam turbines in power plants, aircraft gas turbines, and other high-performance applications due to advantageous characteristics such as superior corrosion, heat resistance, and high flexibility.

The global nickel alloy market is segmented by alloy type, nickel type, end-user Industry, and geography. By alloy type, the market is segmented into heat-resistant nickel alloys, corrosion-resistant nickel alloys, electrical-resistant nickel alloys, low-expansion nickel alloys, and shape-memory and high-strength alloys. By nickel type, the market is segmented into nickel-chromium-iron alloys, nickel-copper alloys, nickel-iron alloys, nickel-chromium-molybdenum alloys, and other types. By end-use industry, the market is segmented into aerospace, electrical and electronics, oil and gas, chemical processing, automotive, and other end-user industries. The report also covers the market size and forecasts for nickel alloys in 16 countries across major regions. For each segment, the market sizing and forecasts have been done based on revenue (USD).

| Heat-Resistant Nickel Alloys |

| Corrosion-Resistant Nickel Alloys |

| Electrical-Resistance Nickel Alloys |

| Low-Expansion Nickel Alloys |

| Shape-Memory and High-Strength Alloys |

| Nickel-Chromium-Iron Alloys |

| Nickel-Copper Alloys |

| Nickel-Iron Alloys |

| Nickel-Chromium-Molybdenum Alloys |

| Other Types |

| Aerospace |

| Electrical and Electronics |

| Oil and Gas |

| Chemical Processing |

| Automotive |

| Other End-user Industries |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Alloy Type | Heat-Resistant Nickel Alloys | |

| Corrosion-Resistant Nickel Alloys | ||

| Electrical-Resistance Nickel Alloys | ||

| Low-Expansion Nickel Alloys | ||

| Shape-Memory and High-Strength Alloys | ||

| By Nickel Type | Nickel-Chromium-Iron Alloys | |

| Nickel-Copper Alloys | ||

| Nickel-Iron Alloys | ||

| Nickel-Chromium-Molybdenum Alloys | ||

| Other Types | ||

| By End-use Industry | Aerospace | |

| Electrical and Electronics | ||

| Oil and Gas | ||

| Chemical Processing | ||

| Automotive | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the global nickel alloys market in 2026?

The market stands at 500.07 Kilotons in 2026 and is forecast to reach 646.51 Kilotons by 2031.

What is the expected growth rate for nickel alloys through 2031?

Market volume is projected to rise at an 5.27% CAGR over 2026-2031, driven by aerospace, EV batteries, SMRs, and hydrogen turbines.

Which alloy segment holds the largest share?

Heat-Resistant Nickel Alloys (includes superalloys) led with 47.76% share in 2025, thanks to their indispensable role in high-temperature and high-stress environments.

Which end-use industry is growing fastest?

Aerospace demand is set to expand at a 7.23% CAGR, driven by rising global aircraft production and engine replacements.

What region will drive most of the new demand?

Asia-Pacific is projected to advance at 7.56% annually to 2031, underpinned by Indonesian processing capacity and Chinese stainless production.

Page last updated on: