China Cloud Gaming Technology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

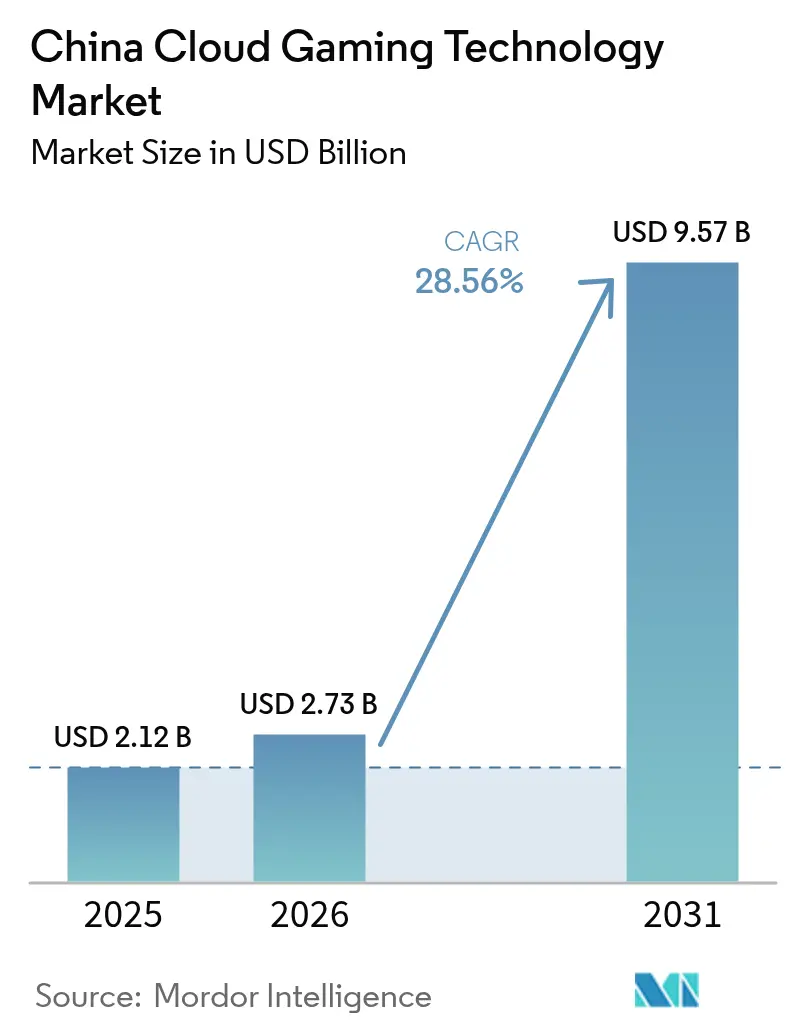

| Base Year Market Size (2025) | USD 2.12 Billion |

| Market Size (2026) | USD 2.73 Billion |

| Market Size (2031) | USD 9.57 Billion |

| Growth Rate (2026 - 2031) | 28.56% CAGR |

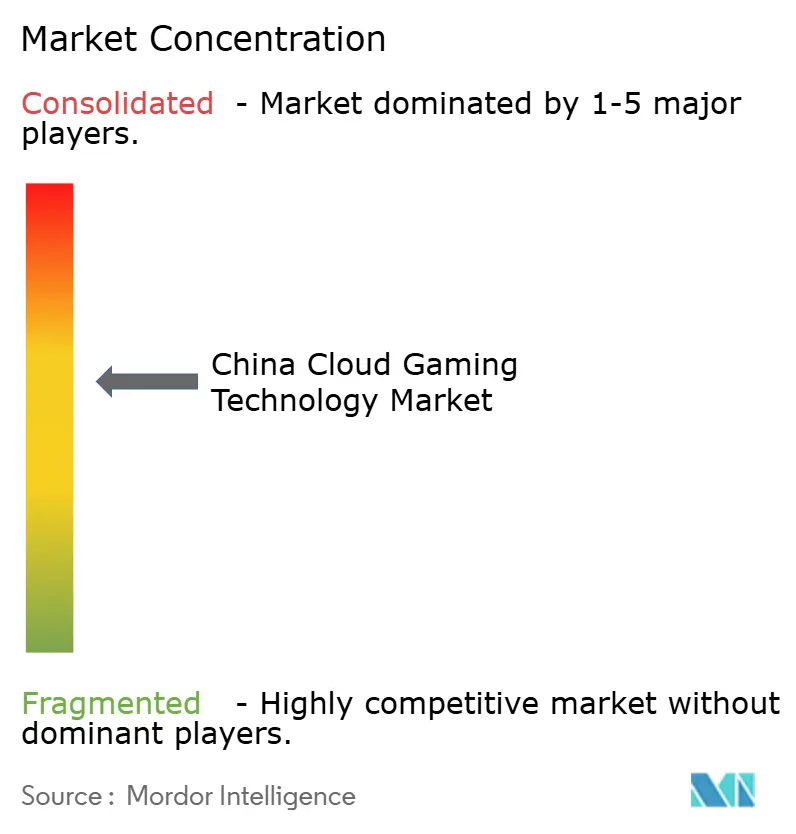

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

China Cloud Gaming Technology Market Analysis by Mordor Intelligence

The China Cloud Gaming Technology Market size is expected to grow from USD 2.12 billion in 2025 to USD 2.73 billion in 2026 and is forecast to reach USD 9.57 billion by 2031 at 28.56% CAGR over 2026-2031.

The sharp growth reflects accelerating 5G standalone roll-outs, rising edge-node density, and strategic bundling by state-owned carriers. Smartphones already dominate usage and are likely to maintain their lead as handset graphics and battery performance continue to improve. Edge-enabled hybrid rendering is narrowing latency gaps, enabling premium AAA titles to reach a broader audience on mid-tier devices. Domestic platforms benefit from preferential licensing, while foreign publishers rely on joint ventures to navigate content approvals. Server hardware costs remain a margin pressure, but domestic chip design and efficient GPU scheduling offset part of the impact.

Key Report Takeaways

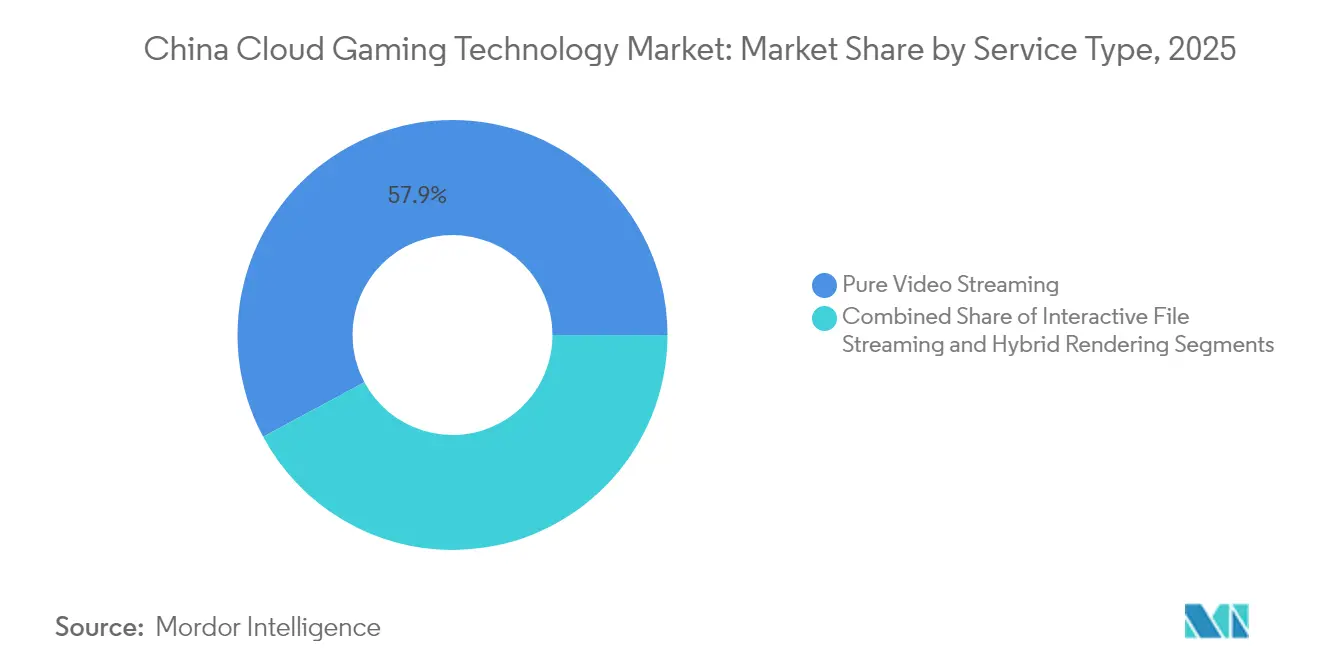

- By service type, pure video streaming led with 57.85% revenue share in 2025, while hybrid rendering is projected to advance at a 32.1% CAGR through 2031.

- By device, smartphones captured 43.65% of the China cloud gaming technology market share in 2025; connected TVs are forecast to post the fastest 33.1% CAGR to 2031.

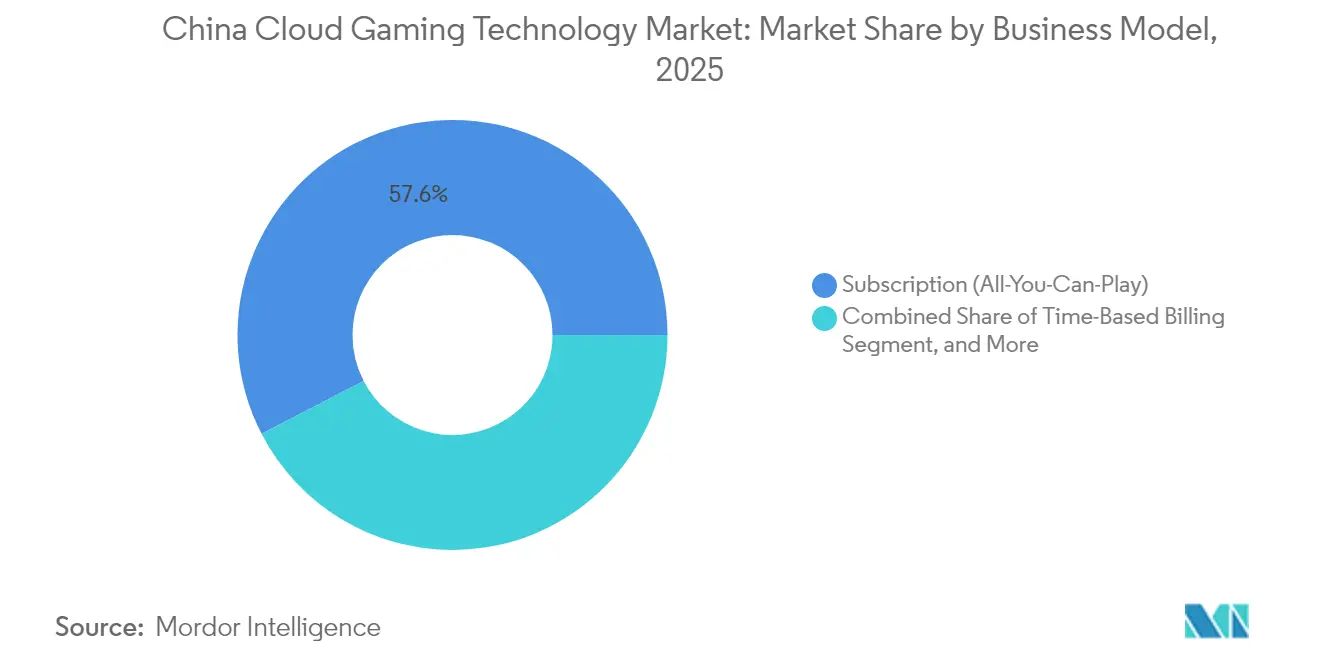

- By business model, consumer subscriptions held 57.60% of the China cloud gaming technology market size in 2025, whereas B2B whitelabel SDK/PaaS solutions are poised for a 34.0% CAGR during 2026-2031.

- By gamer type, casual gamers accounted for a 60.55% share of the China cloud gaming technology market in 2025; lifestyle gamers represent the fastest-growing group with a 34.6% CAGR outlook.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Cloud Gaming Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Upgrades to 5G SA networks & edge nodes enabling <20 ms latency | +8.50% | Beijing, Shanghai, Shenzhen expanding to Tier-2 cities | Medium term (2-4 years) |

| Carrier cloud-bundling accelerating user acquisition | +6.20% | Nationwide with early gains in China Mobile and China Telecom coverage | Short term (≤2 years) |

| Flagship AAA mobile titles re-released in cloud-native form | +7.80% | Nationwide with premium uptake in urban centers | Medium term (2-4 years) |

| Smart-TV OEM pre-installation expanding living-room reach | +4.30% | Nationwide, stronger in high household-penetration areas | Long term (≥4 years) |

| Generative-AI content localisation shortening launch cycles | +3.70% | Nationwide, focused on international IP adaptation | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Upgrades to 5G standalone networks and edge nodes

China Telecom devoted RMB78 billion to next-generation cloud-network infrastructure in 2024, lifting data-center and edge-node density to cut round-trip latency below 20 ms in major cities. Research from Sharif University of Technology shows that such latency levels enable a single edge server to support 23 concurrent players, improving unit economics and gameplay responsiveness.[1]Sharif University of Technology, M. Liu et al., “Edge-Cloud Collaboration for Real-Time Gaming,” sharif.edu As coverage widens to Tier-2 cities, more users will experience console-grade quality on entry phones, reinforcing subscription uptake.

Carrier cloud-bundling

China Mobile integrates its Migu Cloud Gaming application with 5G data plans, leveraging a 303 million subscriber base to remove separate payment steps and app-store fees. Bundled plans reduce acquisition costs for publishers, expand cross-selling opportunities, and unlock rural demand where credit-card penetration is low. Similar offers from China Telecom and China Unicom normalise cloud gaming as a standard network feature.

Cloud-native re-releases of flagship AAA mobile titles

MiHoYo re-engineered Genshin Impact and Honkai: Star Rail for browser-based streaming, trimming download sizes, and easing device GPU requirements. The cloud builds increase reach among mid-range Android owners and encourage return play through seamless updates. Proprietary back-end servers give MiHoYo tighter control of performance, while revenue spikes from in-game events validate the approach for other publishers.

Smart-TV OEM pre-installation of cloud gaming apps

LG, Hisense, and TCL now preload cloud gaming portals on new smart-TV lines. LG’s alliance with Xbox illustrates the model: users pair a Bluetooth controller and start play without consoles or downloads.[2]LG Electronics, “Xbox Partnership Expands on LG Smart TVs,” lg.com Chinese makers replicate the template, tapping a household smart-TV base topping 75%. The living room context promotes multiplayer sessions and family subscriptions, adding incremental hours to operator platforms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Licensing quotas & censorship limiting title libraries | -5.80% | Nationwide, stricter in content-sensitive regions | Long term (≥4 years) |

| U.S. GPU export controls inflating server-side capex | -4.20% | Nationwide, higher impact on international partnerships | Medium term (2-4 years) |

| Consumer price-sensitivity vs. data-egress fees compressing margins | -3.10% | Nationwide, higher impact in lower-tier cities | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Licensing quotas and censorship

The National Press and Publication Administration approved 1,400 titles during 2024, well below publisher submissions, leaving many foreign games in limbo.[3]National Press and Publication Administration, “Approved Game List 2024,” npaa.gov.cn Platforms must embed anti-addiction systems and real-name log-ins to comply with the Protection of Minors in Cyberspace rules. Domestic studios enjoy shorter approval pathways, tilting competitive balance toward Tencent and NetEase and limiting library diversity for multinational platforms.

US GPU export controls

Restrictions on advanced Nvidia and AMD accelerators raise server costs by 25-40%. Providers turn to domestic chipmakers for mid-range GPUs and refine hybrid rendering to reduce per-session GPU minutes. Although performance parity is improving, export limits slow capacity expansion and raise subscription break-even thresholds.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hybrid rendering disrupts video-only streaming

Pure streaming held 57.85% of 2025 market share, anchoring the early China cloud gaming technology market through broad device reach. Hybrid rendering, however, is forecast to post a 32.1% CAGR to 2031 as edge nodes offload physics and input prediction tasks closer to players. This split workload cuts bandwidth needs and elevates frame stability during peak traffic windows.

Research at Sharif University confirms that edge collaboration supports 23 simultaneous users per node at <20 ms, sharpening economics for operators. As the Eastern Data Western Compute backbone brings hyperscale facilities online, providers dynamically allocate compute to hotspots, giving hybrid approaches further headroom. Interactive file streaming remains a transitional option for mid-spec devices, yet is likely to be eclipsed as telcos densify edges.

By Device: Smartphones extend lead while connected TVs accelerate

Smartphones accounted for 43.65% of the China cloud gaming technology market share in 2025, and the segment is projected to grow at a 32.6% CAGR to 2031. Handset ASPs above RMB3,000 now ship with advanced cooling and ray-tracing GPUs, making long sessions viable. Tablets attract strategy gamers seeking larger displays without sacrificing mobility, while PCs retain high-precision e-sports users.

Connected TVs and OTT boxes transform living rooms into casual gaming zones by pre-installing portals. LG-Xbox and Huawei-Peng Game collaborations illustrate the model, building recurring revenue from family plans. Dedicated cloud handhelds, such as Tencent’s Sunday Dragon 3D One, demonstrate premium demand, although volumes remain niche.

By Business Model: B2B white label outpaces retail subscriptions

The subscription bundle captured 57.60% of the China cloud gaming technology market size in 2025, mirroring video-on-demand pricing. Whitelabel SDK/PaaS offerings for carriers, smartphone OEMs, and streaming platforms are forecast to compound at a 34.0% CAGR, letting partners add gaming with lower capex. Revenue-share deals favour operators that supply identity management and billing rails.

Time-based billing persists where users value flexibility, and micro-transaction passes overlay item sales onto cloud access. NetEase’s low-price item strategy on The Legend of the Condor Heroes aims to broaden the player pool while keeping overall spending moderate. As average playtime rises, hybrid monetisation mixes will diversify operator income.

By Gamer Type: Lifestyle gamers drive engagement

Casual gamers formed 60.55% share f the China cloud gaming technology market base in 2025, drawn by instant play and no hardware upgrades. Lifestyle gamers, integrating games with social and content creation, are projected to record a 34.6% CAGR through 2031. Tencent’s integration of Genshin Impact with QQ groups facilitates livestream chats and event access, nurturing community identity.

Avid gamers, though smaller in number, remain high-spending users. Cloud platforms segment storefronts to surface content by intensity level, improving retention and advertising yield. Personalized lobbies and creator tools convert passive players into active contributors, reinforcing stickiness across demographics.

Geography Analysis

Tier-1 cities stand at the forefront of China cloud gaming technology market. Beijing’s China Unicom–Huawei 5G-Advanced network now covers 85% of the urban area, enabling 10-gigabit cell capacity for stadium-level crowds. Similar upgrades in Shanghai and Shenzhen are concentrating premium users and early adopter spending.

The Eastern Data Western Compute programme builds hyperscale data centres in Gansu and Inner Mongolia, routing compute loads to renewable-energy sites and lowering PUE values. China Telecom’s dispatching centres balance tasks nationwide, extending consistent latency envelopes to interior provinces. As nodes proliferate, providers can introduce tiered plans aligned with regional bandwidth affordability.

Lower-tier cities and rural counties represent the next demand wave. Smartphone penetration and 5G coverage expand monthly, and telco-bundled plans offset price sensitivity. Localised content, lighter in file size and tuned for variable bandwidth, helps providers cultivate new cohorts. Social features, including UGC mini-games within QQ and WeChat, bridge cultural preferences across geographies.

Regulatory Landscape

China cloud gaming operates under multi-agency oversight spanning content approvals, telecom licensing, and security compliance. The National Press and Publication Administration (NPPA) governs game publishing approvals and ongoing compliance requirements for online games, and its publication of domestic network game approval batches (for example, March 2026 approvals) reinforces that catalogue access remains tied to the formal approval pipeline. Platforms also implement real-name registration and anti-addiction controls aligned with China’s minors protection requirements, which shape session design, onboarding, and identity integration.

On the technical and operational side, regulators and standards bodies have been formalizing service expectations for cloud gaming. NRTA’s GY/T 396-2023 sets general technical requirements for cloud gaming, including a platform-network-terminal-security architecture and technical performance expectations such as GPU-based rendering and specified audio-video encoding support. MIIT-linked standards add measurement and network quality governance, including YD/T 6747-2026 (effective 2026-09-01) for cloud gaming network quality evaluation and MPS GA 1277.17-2026 (effective 2026-07-01) for security management requirements, which increases the need for auditable security controls and service-quality instrumentation across cloud gaming stacks.

Competitive Landscape

The competition in the China cloud gaming technology market centres on vertically integrated ecosystems. Tencent combines game IP, Cloud Elastic GPU services, and WeChat distribution for an end-to-end moat. NetEase balances self-developed hits with global licensing, adopting a stair-step revenue cadence that cushions between blockbuster launches. ByteDance’s partial pullback narrows the field but also frees independent studios to license Moonton technology stacks.

Telecom operators add platform depth. China Mobile’s Migu leverages network and carrier billing, while China Telecom prioritizes edge-node density for latency leadership. Hardware suppliers such as Huawei pre-install cloud clients on HarmonyOS devices and bundle three-month trials, helping shorten user onboarding funnels.

International partnerships reinforce content pipelines and technical expertise. Tencent’s 25% stake in a new Ubisoft subsidiary secures franchises while providing cloud back-end support for overseas launches. Microsoft’s renewed NetEase deal returns Blizzard titles to China, expanding catalogue breadth. White-space opportunities remain for mid-tier publishers and middleware firms that enable cross-platform saves and controller standardization.

China Cloud Gaming Technology Industry Leaders

-

Tencent Holdings

-

NetEase Inc.

-

37 Interactive Entertainment

-

Perfect World Games

-

Shanda Games

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Network quality evaluation and standardized technical baselines create whitespace for managed compliance and quality-assurance layers sold into carriers, OEMs, and platforms. With YD/T 6747-2026 taking effect from September 2026 and GY/T 396-2023 specifying end-to-end technical requirements, vendors that package monitoring, QoE analytics, encoding compliance (for example, AVS/AVS2 support), and integrated security and anti-addiction capabilities into B2B whitelabel SDK/PaaS offerings can shorten deployment cycles for partners that want to add cloud gaming without building the full control plane.

Compute and edge infrastructure programs are also expanding the addressable performance envelope for premium cloud gaming experiences beyond early adopter metros. China Mobile’s East Data, West Computing-linked Jiashan intelligent computing center moved into commercialization on June 30, 2026, and the same infrastructure buildout supports high-performance, latency-sensitive workloads alongside AI. In parallel, platform-side progress toward sub-20 ms round-trip latency in major cities, highlighted around Tencent START in 2026, supports new device and distribution formats (including cloud-first hardware concepts) and supports smart-TV and multi-terminal bundles where instant-play is a key value proposition.

Recent Industry Developments

- May 2026: Tencent Cloud announced a strategic cooperation with Kingnet Network to support full cloud migration and technical engine development for the Rebirth of the Warrior (Rehuo Jianghu) IP, using Tencent Cloud capabilities such as EdgeOne. The deal reflects continued consolidation of cloud gaming enabling infrastructure around large cloud platforms that can bundle edge acceleration, security, and tooling for live-operated games.

- April 2026: Tencent signed a Game Cooperation Framework Agreement with Kingnet Network, with the cooperation term running through December 31, 2028. A multi-year framework of this type helps stabilize content and technology collaboration planning, supporting longer-lived roadmaps for cloud-based distribution and operations.

- November 2024: China Unicom Beijing and Huawei activated a large-scale 5G-Advanced intelligent network covering 85% of Beijing’s urban area. The upgrade strengthens the low-latency access layer required for cloud gaming at scale and provides a template for capacity-led rollouts in other major cities.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers the revenue generated in China from technology and service delivery that enables cloud-based game rendering and streaming to end devices over a network, including platforms and supporting service layers used to run and access cloud games.

Scope exclusions: We exclude traditional local-download gaming revenue and general-purpose cloud infrastructure revenue that is not directly attributable to cloud gaming delivery.

Segmentation Overview

-

By Service Type

- Pure Video Streaming

- Interactive File Streaming

- Hybrid Rendering (Edge Off-load)

-

By Device

- Smartphones

- Tablets

- Connected TVs and OTT Boxes

- PCs and Laptops

- Dedicated Cloud-Gaming Consoles

- Other Devices

-

By Business Model

- Subscription (All-You-Can-Play)

- Time-Based Billing

- Game-Specific Micro-Transaction Pass

- B2B Whitelabel SDK / PaaS

-

By Gamer Type

- Casual Gamers

- Avid Gamers

- Lifestyle Gamers

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to anchor the model to real-world signals that can be checked and refreshed, especially for China where policy and licensing can change demand patterns quickly. We relied on public materials such as MIIT releases on 5G rollout, National Bureau of Statistics indicators tied to digital services, and China Customs trade data that helps infer device and network hardware flows linked to cloud access behavior.

We also reviewed technical and adoption references from sources such as ITU publications, IEEE and other peer-reviewed journals on streaming performance and latency thresholds, and patent databases that show where investment is concentrated in interactive streaming and edge compute. In addition, company filings, investor presentations, app-store and platform announcements, and reputed press coverage were used to validate timing of launches and monetization shifts, supported by paid subscriptions for company financials, news intelligence, and patent lookups where helpful. This list is not exhaustive, and many other public sources were reviewed to collect, validate, and clarify inputs during the study.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with platform-side leaders, telecom and data center ecosystem participants, game operations teams, and channel partners active in China. We used these conversations to confirm what revenue streams are counted as cloud gaming technology, pressure-test adoption assumptions by device and service type, and then align the forecast logic with how buyers and operators expect pricing and usage to move over time.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 17% | |

| Mid tier: 55% | Functional/Unit leaders: 30% | |

| Smaller Players: 19% | Managers: 53% |

Market-Sizing & Forecasting

Sizing starts with a top-down build that reconstructs the addressable demand pool in China by linking cloud gaming usage readiness to network and device realities, and then translating that into monetized activity. The model is then corroborated through selective bottom-up approximations, such as sampled price points by business model and rough volume checks by service type, so totals can be adjusted if a mismatch shows up.

Key inputs used in the model include 5G coverage and quality indicators (as they influence playable latency), data center and edge capacity signals that affect streaming reliability, active gamer mix by engagement level, device mix shifts (smartphones, PCs, connected TVs), and monetization mechanics like subscription take-up and time-based billing intensity. Since disclosure is uneven, gaps are handled by using conservative ranges agreed in interviews, and then applying those ranges consistently across similar service types before they are stress-tested against observed pricing and adoption direction.

For forecasting, scenario analysis is used so adoption and ARPU-like assumptions can move differently under policy, content availability, and network performance paths. Those scenarios are kept grounded by expert consensus on how quickly hybrid rendering, interactive file streaming, and pure video streaming are likely to scale in China, and the final forecast is selected after checking which path best fits the current signals.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent indicators, and then followed by structured variance checks so outliers are not carried into the final tables. When a value looks off, the assumptions are reopened, cross-checked against alternate public series, and then re-tested through quick re-contacts with relevant interviewees.

Before sign-off, the model goes through multiple analyst reviews that look for unit consistency, pricing logic issues, and year-to-year jumps that do not match known market events. Reports are refreshed annually, with interim updates triggered by material shifts such as licensing actions, major platform changes, or network investment surprises. Right before delivery, we do a fresh pass to ensure the numbers reflect the latest available signals.

Mordor Intelligence's China Cloud Gaming Technology Market Size Measured Against Other Published Estimates

Published market values for cloud gaming in China often do not match because each publisher draws the line differently on what is being counted, and the timing of the data snapshot also changes the outcome. Differences also come from how pricing is treated, especially when subscription bundles, time-based billing, and mixed monetization are all present at the same time.

Some external estimates cover only consumer-facing cloud gaming revenue and may also treat the market as a narrower streaming service total. In Mordor Intelligence, the market includes pure video streaming, interactive file streaming, and hybrid rendering across devices and business models, and B2B whitelabel SDK or PaaS revenue is counted only when it is directly tied to cloud gaming delivery.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.12 B (2025) | |

| Trade Journal A | USD 1.87 B (2024) | Uses an industry tracker figure reported for 2024 and often reflects a narrower market view that is closer to consumer cloud gaming industry revenue, with limited visibility into service type splits and business-model normalization. |

| Global Consultancy B | USD 1.78 B (2026) | Presents a forward-year country projection embedded in a wider regional model, and the China value can differ based on regional allocation assumptions, device mix weights, and how subscription revenue is annualized into the forecast year. |

The spread in the table is mainly explained by year selection and what gets counted inside the revenue pool, not by arithmetic mistakes. By keeping service types and monetization mechanics explicit, and then checking totals against network readiness and device mix signals, the final estimate stays traceable to repeatable inputs that clients can pressure-test.

Key Questions Answered in the Report

What is the current revenue of the cloud gaming technology in China?

The cloud gaming technology in China generated USD 2.73 billion in 2026 and is on track for USD 9.57 billion by 2031.

Which device segment leads adoption?

Smartphones lead with 43.65% usage in 2025 and are forecast to maintain a prominent growth through 2031.

How fast is hybrid rendering growing?

Hybrid rendering is the fastest service type, projected to rise at a 32.1% CAGR from 2026-2031 as edge nodes proliferate.

What business model shows the highest growth?

B2B whitelabel SDK/PaaS solutions are expected to post a 34.0% CAGR as carriers and OEMs embed cloud gaming in their services.

How do licensing rules affect foreign publishers?

Strict NPPA quotas and content checks slow title approvals, reducing foreign catalogue depth and giving domestic studios a compliance advantage.

Which regions are next for rapid adoption?

As the Eastern Data Western Compute initiative reallocates capacity westward, Tier-2 and lower-tier cities will gain improved latency and wider game libraries, unlocking new subscriber growth.

Page last updated on: