Cloud Gaming Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

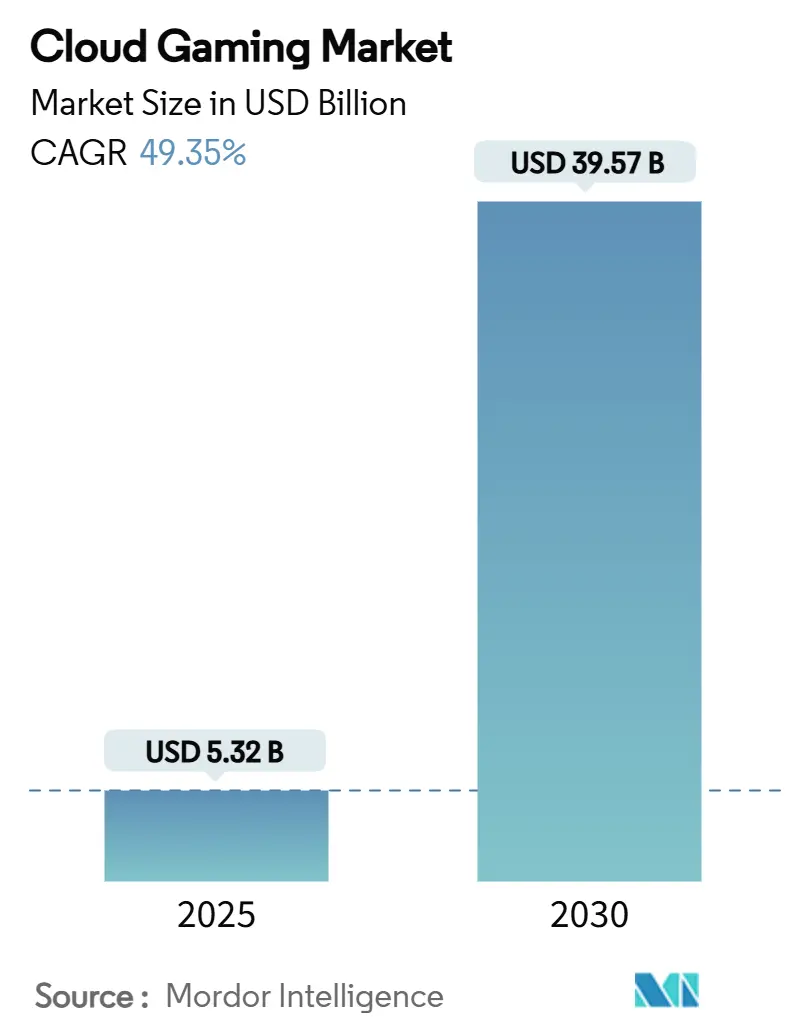

| Market Size (2025) | USD 5.32 Billion |

| Market Size (2030) | USD 39.57 Billion |

| Growth Rate (2025 - 2030) | 49.35% CAGR |

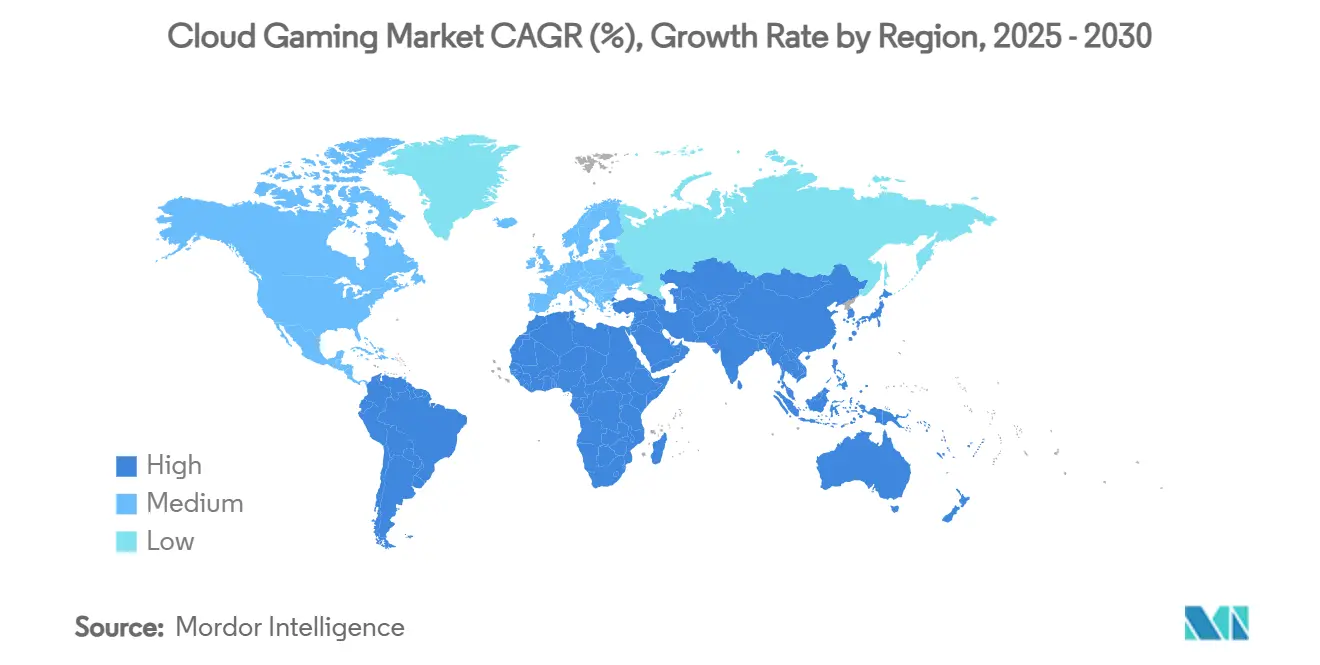

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Cloud Gaming Market Analysis by Mordor Intelligence

The Cloud Gaming Market size is estimated at USD 5.32 billion in 2025, and is expected to reach USD 39.57 billion by 2030, at a CAGR of 49.35% during the forecast period (2025-2030).

Continued 5G roll-outs, edge computing deployments, and generative-AI compression collectively lower latency and bandwidth hurdles, turning advanced gameplay into a true “any-device” experience for casual and competitive users alike. Content owners are pivoting toward cloud-first launches that eliminate console requirements, tripling potential gamer reach in emerging economies where smartphones dominate. Telecom operators are bundling premium gameplay tiers into high-ARPU data plans, translating network investments into incremental revenue while supplying distribution pipes to publishers. Platform rivalry is intensifying: vertically integrated giants leverage first-party IP, whereas specialist providers depend on differentiated rendering pipelines and flexible price tiers to hold niche positions within the wider cloud gaming market.

Key Report Takeaways

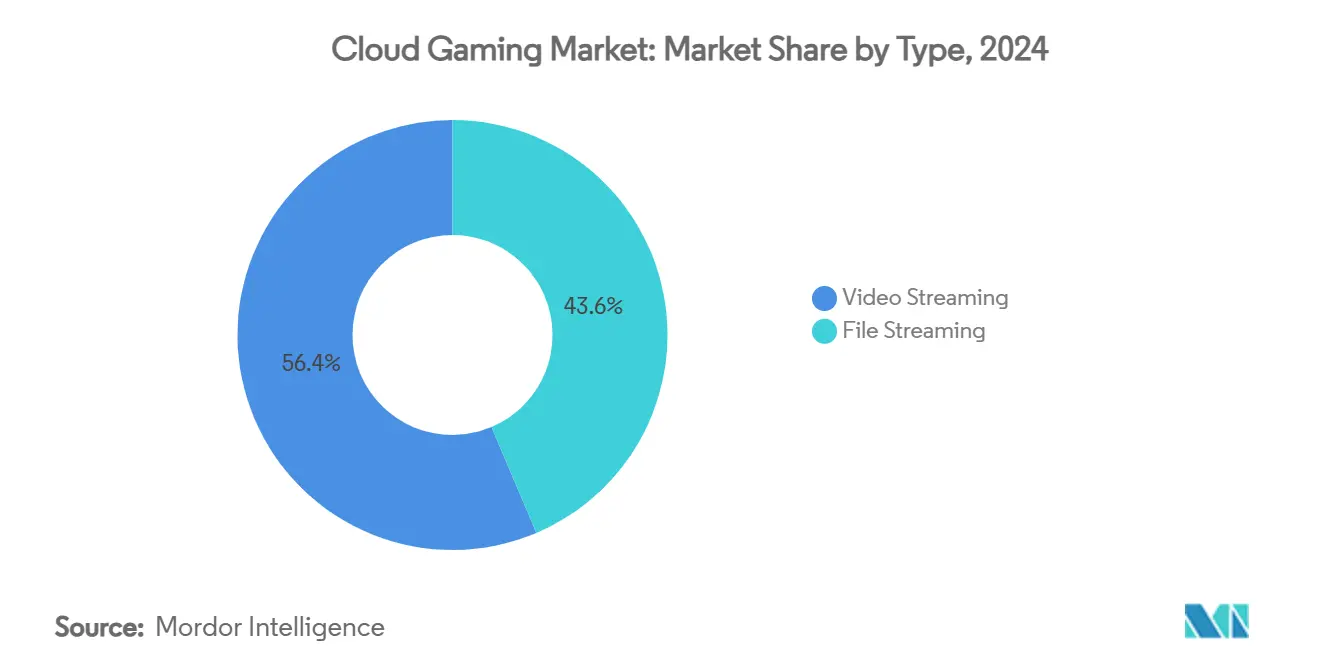

- By type, video streaming commanded 56.38% of the cloud gaming market share in 2024; file streaming is projected to advance at a 44.92% CAGR to 2030.

- By device, smartphones accounted for 44.12% of the cloud gaming market size in 2024, and the segment is expected to grow at a 46.72% CAGR through 2030.

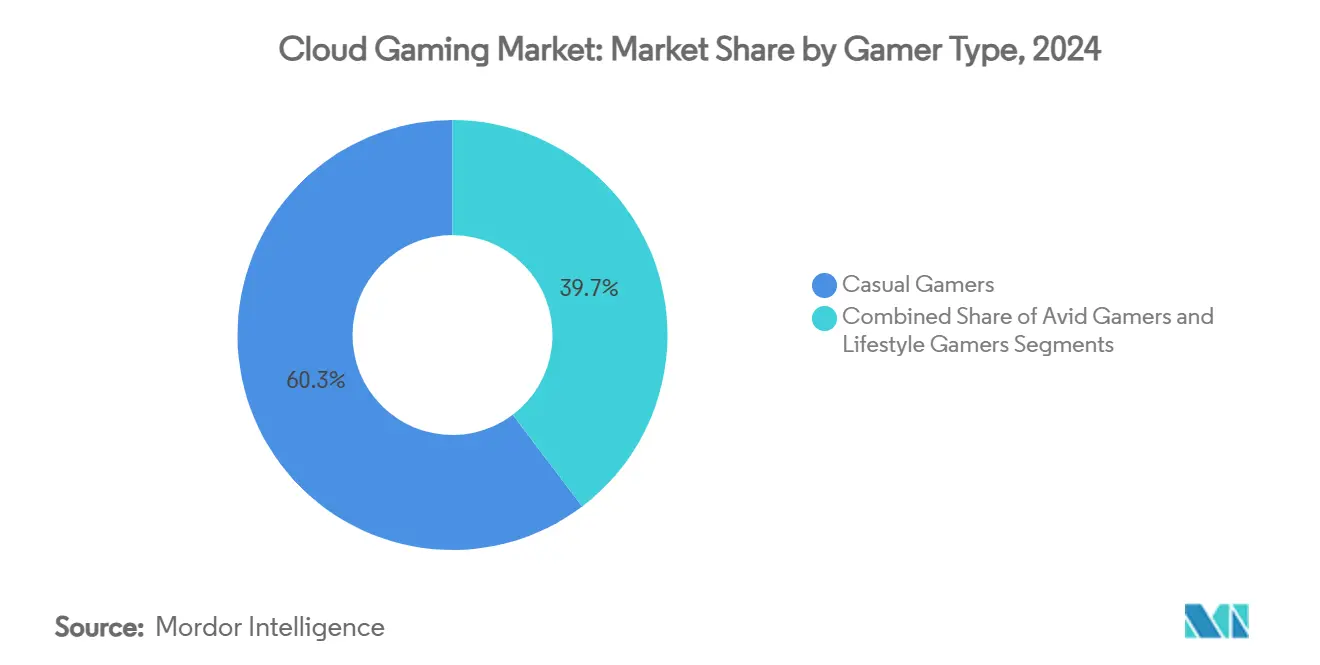

- By gamer type, casual players led with 60.31% of the cloud gaming market size in 2024, while avid gamers represent the fastest-growing cohort with a 46.20% CAGR to 2030.

- By business model, subscription services held 70% of 2024 revenue; ad-supported tiers are forecast to expand at a 41% CAGR through 2030.

- By region, Asia-Pacific captured 35.81% of 2024 revenue; the Middle East and Africa region is poised to rise at a 49.92% CAGR to 2030.

Global Cloud Gaming Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G and Edge roll-outs unlocking low-latency gameplay | +8.0% | APAC core, North America, EU | Medium term (3-4 yrs) |

| AAA publishers adopting cloud-first distribution | +6.5% | Global, with early APAC/Europe | Medium term (3-4 yrs) |

| Telco–gaming bundles monetizing mobile data plans | +5.0% | Europe, APAC core | Short term (≤ 2 yrs) |

| Generative-AI compression cutting bandwidth costs | +3.0% | Global, with early APAC uptake | Long term (≥ 5 yrs) |

Source: Mordor Intelligence

5G and Edge Roll-outs Unlocking Low-Latency Gameplay

Latency drops from more than 100 ms to 20-40 ms once game logic is processed at Multi-Access Edge nodes rather than distant hyperscale data centers, creating console-level responsiveness that had previously been unattainable for shooters and competitive titles. AT&T demonstrates this architecture by embedding GPU blades in metropolitan switching facilities, allowing round-trip packets to remain inside the metro loop before reaching the public backbone [1]AT&T Business, “Multi-Access Edge Computing for 5G,” att.com . Ericsson projects mobile cloud gaming revenue to climb from USD 8 billion in 2025 to USD 19 billion by 2030 as 5G Standalone cores widen capacity for Massive MIMO and beam-forming [2]Ericsson, “Harnessing 5G to Unleash Cloud Gaming,” ericsson.com . The coverage effect is most evident in South Korea and Japan, where nationwide 5G penetration exceeds 90%, encouraging hardcore users to trial cloud platforms without perceivable lag. North American network operators pursue a similar pattern, with city-edge compute clusters positioned no farther than 25 miles from end users in most dense metros. These infrastructure investments collectively solidify a technical baseline on which the cloud gaming market can convert previously skeptical console owners.

AAA Publishers Adopting Cloud-First Distribution

Microsoft’s Game Pass Ultimate streams hundreds of top-tier titles across phones, tablets, PCs, and smart TVs, illustrating a monetization path that extends intellectual property beyond the installed console base. Publishers deploying day-one releases to the cloud increase lifetime unit sales by capturing gamers lacking USD 500 hardware. Second-order benefits include simplified patch pipelines—developers update a single master build rather than multiple platform SKUs—and granular telemetry, which improves real-time balance adjustments. Emerging economies with low console uptake but high smartphone usage, such as India and Indonesia, become realistic launch territories, effectively tripling reachable audiences without physical logistics. However, studios must adapt UI and input mapping for touch screens, gyro sensors, and low-latency Bluetooth controllers to preserve engagement. These strategic shifts reinforce recurring revenue models and consolidate user data pools, thereby elevating switching costs for consumers and strengthening competitive moats inside the cloud gaming market.

Telco–Gaming Bundles Monetizing Mobile Data Plans

European and Asia-Pacific operators package premium gameplay tiers within 5G contracts to stimulate subscriber upgrades and recoup radio-access-network investments. Network slicing allocates dedicated quality-of-service lanes, guaranteeing latency below 30 ms during peak sessions, an approach Ericsson values at USD 11 billion in incremental operator revenue by 2030. Deutsche Telekom, Singtel, and SK Telecom offer multi-screen game libraries alongside unlimited data, reducing acquisition costs for platform partners who leverage telco billing frameworks. Bundles heighten stickiness: churn probability among bundled subscribers falls by 15 percentage points compared with data-only tiers, according to internal operator dashboards shared during analyst briefings. This distribution avenue lowers marketing expenses for service providers, quickening subscription uptake within the wider cloud gaming market while encouraging telcos to market differentiated speed tiers.

Generative-AI Compression Cutting Bandwidth Costs

Convolutional auto-encoders reconstruct high-fidelity frames from narrow bitstreams, slashing throughput demand by up to 40% relative to conventional H.264 at the same resolution, based on Ericsson field tests across 4G and 5G networks. Lower bitrate envelopes enable session stability for commuters on cellular links and reduce cloud egress fees that otherwise erode gross margins. User cohorts on capped data plans report 25% longer average play sessions when AI-compression is active, indicating that bandwidth savings translate directly into engagement. Operators simultaneously free spectrum for additional customer traffic while preserving experiential parity. As compression algorithms mature, mobile video pipelines that underpin the cloud gaming market will accommodate 1440p at 60 fps inside 12 Mbps channels, levels previously restricted to fixed broadband, further narrowing the gap between on-premise and streamed gameplay.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rural latency bottlenecks in South America and Africa | -5.0% | National, with early gains in Brazil, Nigeria, Kenya | Medium term (3-4 yrs) |

| High cloud-GPU rental costs limiting indie platforms | -4.0% | Global, with outsized impact in APAC/EMEA | Short term (≤ 2 yrs) |

| Content-licensing barriers to cross-border expansion (EU) | -2.0% | Europe, with spill-over to APAC | Medium term (3-4 yrs) |

Source: Mordor Intelligence

Rural Latency Bottlenecks in South America and Africa

Sub-40 ms latency remains unachievable across large rural footprints where fiber backhaul and low-density tower grids are scarce, excluding many potential gamers from seamless sessions. Competitive genres such as battle royales and esports titles amplify the issue, penalizing packet jitter with on-screen desynchronization that casual users may tolerate but ranked players reject. Service providers explore hybrid rendering that offloads physics calculations to device CPUs when milliseconds climb beyond threshold values, yet these workarounds complicate code paths and introduce platform fragmentation. Government universal-service programs in Brazil and Kenya prioritize basic connectivity over high-performance streaming, leaving cloud gaming initiatives dependent on private network upgrades. Consequently, adoption curves bifurcate, with urban gamers joining the expanding cloud gaming market while rural populations lag, reinforcing digital divides.

High Cloud-GPU Rental Costs Limiting Indie Platforms

Nvidia commands 70–95% of the global data-center GPU pool, enabling premium pricing that links AI inference demand with cloud gaming supply chains. Rental rates for RTX 40-class instances remain above USD 1.10 per GPU-hour, a threshold at which all-you-can-play subscriptions require user conversion rates exceeding 8% to break even, according to financial disclosures from independent platforms. Larger conglomerates offset compute spend across advertising, retail, and enterprise workloads, squeezing margins for stand-alone entrants. Investment rounds for cloud-native startups increasingly allocate funds toward proprietary compression or FPGA-accelerated pipelines to escape dependency on mainstream GPU vendors. Until component diversity expands, high variable costs will restrain competition and slow geographic rollout schedules, tempering the aggregate growth potential of the cloud gaming market during the next two years.

Segment Analysis

By Type: Video Streaming Consolidates Leadership

Video streaming generated the largest slice of revenue at 56.38% in 2024, benefiting from its device-agnostic architecture that executes all graphics remotely. This share translates into more than USD 2 billion of the cloud gaming market size, affirming consumer preference for friction-free session starts that avoid local downloads. The approach aligns with casual and mid-core usage patterns in Latin America and Southeast Asia where handset specifications often fall below AAA minimums. Video streams render frames in secure data-center racks, then push compressed color buffers to client apps, allowing handset batteries to last longer and mitigating thermal throttling. The model does demand stable 10-25 Mbps connections for 1080p at 60 fps, positioning it heavily in 5G-ready regions.

File streaming holds a smaller footprint yet serves enthusiast users who own gaming laptops or small form-factor PCs. It pre-fetches asset blocks ahead of gameplay, lifting bitrate constraints and enabling native input latency. However, hardware variability complicates support matrices, and patch sizes remain burdensome in limited-data markets. File streaming’s 44.92% CAGR projection signals healthy growth from a small base, driven by visual fidelity demands in esports arenas and premium VR experiences seeking 120 fps. Over time, hybrid delivery that toggles between real-time frames and pre-rendered asset calls may blur the distinction, but video streaming is expected to retain primacy within the cloud gaming market through 2030.

By Device: Smartphones Extend Gamer Reach

Smartphones accounted for 44.12% of 2024 spending, marking them as the foremost access point across Asia-Pacific and Latin America. This penetration equates to USD 1.7 billion of the cloud gaming market size and is forecast to grow at a 46.72% CAGR into the next decade, propelled by declining 5G data rates and an expanding catalog of touch-friendly AAA ports. Accessories such as telescopic controllers and clip-on cooling fans narrow the experiential gap against handheld consoles, while on-device AI upscaling enhances perceived resolution under bandwidth constraints.

TVs and streaming boxes form the second-largest device cohort, commanding 27% revenue owing to the zero-incremental-hardware proposition for households that already own smart displays. Native app integration inside operating systems like LG webOS and Samsung Tizen cuts onboarding friction, though motion-to-photon latency must remain beneath 60 ms to satisfy action-heavy titles. PC browsers and dedicated thin clients complete the device matrix, supplying high refresh-rate monitors to esports participants. Each form factor’s evolving capabilities reinforce cross-screen continuity, reinforcing spend dispersion throughout the cloud gaming market.

By Gamer Type: Casual Users Lead, Avid Users Accelerate

Casual gamers held 60.31% share in 2024. The segment spans puzzle, idle, and story-driven experiences that tolerate 80 ms total lag and sub-4 Mbps streams, encouraging trials on budget smartphones. Publishers tailor onboarding funnels with minimal account creation steps and free trial sessions, capturing broad demographics in India, Brazil, and the Philippines. Continued adoption from this base underpins the volume expansion of the cloud gaming market as entry frictions collapse.

Avid gamers post the highest 46.20% CAGR forecast to 2030, signaling a pivotal shift from cautious experimentation toward main-rig replacement. Once latency thresholds dipped into the 20–30 ms band in urban centers, hardcore communities began migrating ranked matches to the cloud during travel or hardware refresh cycles. Monetization intensity widens because these users consistently purchase DLC and subscribe to premium tiers, raising ARPU by 2-3 times relative to casual cohorts. Their migration lifts requirements for adaptive bitrate, custom key mapping, and HDR support, pressuring service providers to iterate server pipelines. As avid adoption matures, competitive parity across hardware types will further cement loyalty within the cloud gaming market.

Note: Segment shares of all individual segments available upon report purchase

By Business Model: Subscriptions Re-shape Economics

Subscription tiers captured 70% of total revenue in 2024, transforming irregular boxed-game sales into high-visibility recurring cash flows that fund infrastructure build-outs. Family plans and annual bundles decrease churn and increase lifetime value, providing a stable base on which operators forecast server capacity. The predictability enables bulk GPU reservations, lowering unit costs by 8-12% relative to spot pricing and improving gross margins across the broader cloud gaming market.

Free-to-play and ad-supported approaches rise at a 41% CAGR, widening funnels in price-sensitive geographies. PlayerWON’s collaboration with NVIDIA GeForce NOW exemplifies an exchange where users watch rewarded video to unlock 30-minute sessions, while publishers monetize incremental impressions [4]PlayerWON, “Ad-Supported Cloud Gaming Partnership,” playerwon.com . Hybrid monetization baked into game design—battle passes, cosmetic micro-items, and booster packs—complements subscription or ad units, creating layered revenue. Transactional à-la-carte access lingers in specialist communities demanding specific titles without recurring obligations. Balanced portfolios that combine multiple schemes maximize reach and resilience, sustaining the growth rhythm of the cloud gaming market in volatile macro environments.

Geography Analysis

Asia-Pacific held 35.81% of 2024 revenue, led by China, Japan, and South Korea where 5G service covers more than 90% of urban populations. Tencent, KT, and NTT DOCOMO align studio pipelines with aggressive fiber backhaul rollouts, enabling latency under 25 ms across top cities. Bundled subscription offers stitched into mobile post-paid plans accelerate paid user conversion. China’s content regulation pushes local champions to invest in proprietary GPU clusters, insulating the regional cloud gaming market from external supply shocks.

The Middle East and Africa region records the fastest forecast CAGR at 49.92%, albeit starting from a smaller revenue base. Saudi Arabia’s Vision 2030 digital agenda earmarks USD 1 billion for esports and streaming infrastructure, positioning Riyadh as a regional node for edge computing. United Arab Emirates carriers Etisalat and du introduced tiered cloud gaming passes linked to zero-rating policies, sidestepping data-overage anxieties. Yet beyond Gulf Cooperation Council cities, fixed broadband speeds remain below the 25 Mbps threshold that supports stable 1080p streams, highlighting rural divides inside the burgeoning cloud gaming market.

North America and Europe display mature adoption curves where 4G fallback performance remains acceptable, supporting growth even outside primary metro clusters. Microsoft’s Azure-backed streaming fabric achieves single-digit millisecond hops between Chicago hubs and east-coast client devices, prompting console owners to treat cloud access as a travel companion rather than full replacement. European regulators push net-neutrality oversight on network slicing, nudging operators to publish transparent performance SLA tiers. These governance frameworks shape cost pass-through models and ensure competitive parity, sustaining incremental uptake across both continents.

Competitive Landscape

Strategic maneuvering centers on asset leverage. Microsoft integrates Xbox Cloud Gaming with Azure GPU capacity and a first-party catalog featuring Halo and Forza franchises, creating a triple-moat of IP, compute, and user accounts. Sony’s strategy blends PlayStation Studios exclusives with Gaikai technology to extend backward-compatibility libraries without new device purchases. Amazon fuses Luna’s channel subscription model into Prime, subsidizing entry with complimentary trials and Twitch integrations that drive viral discovery.

Independents such as Shadow and Boosteroid pursue elasticity, offering customizable virtual PCs priced per spec tier. Shadow’s Boost and Power plans allow creators to rent RTX 3070-class rigs, simultaneously streaming games and live-editing content [3]Shadow, “Boost & Power Plans Launch,” shadow.tech . Boosteroid partners with ISPs in Eastern Europe to provision micro-edge nodes, squeezing latency to 15 ms inside Kyiv and Bucharest. Nvidia remains the silent juggernaut: GeForce NOW reuses existing data-center deployments, and patent filings on GPU virtualization reinforce technical defensibility that others license at a premium. Market consolidation risk rises as smaller outfits rely on white-label render farms resold by hyperscalers.

White-space opportunities linger around hybrid-rendering middleware that allocates AI inference to client NPUs when available, slashing server workload by 20%. Another niche is competitive esports: specialized firms promise sub-20 ms glass-to-glass pipelines inside single-city rings, charging professional teams premium subscription rates. Enterprise use cases - training simulations, remote CAD - represent an adjacent revenue stream where game engines underpin industrial scenarios, extending total addressable demand beyond entertainment and widening the functional perimeter of the cloud gaming market.

Cloud Gaming Industry Leaders

-

Nvidia Corporation

-

Microsoft Corporation

-

Sony Group Corporation

-

Tencent Holdings Limited

-

Amazon.com Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Microsoft rolled out performance upgrades for Xbox Cloud Gaming on iPhone and iPad, extending average play time by 35% and improving responsiveness.

- March 2025: Tencent, Sony, and Square Enix invested in Ubitus to bolster GPU virtualization and AR/VR streaming capabilities.

- February 2025: Xbox CFO Tim Stuart highlighted subscription and consumption-based models, referencing generative AI for content creation.

- January 2025: Ericsson published consumer research finding high post-trial dropout due to pricing concerns and performance gaps.

Global Cloud Gaming Market Report Scope

Users can engage in video games through cloud gaming by streaming directly from remote servers over the internet, eliminating the need to download or install games on local devices. The market for the study defines the revenues accrued from the sales of various cloud gaming platforms worldwide.

The cloud gaming market is defined based on the revenues generated from the device type being used globally. The analysis draws on market insights from secondary research and primary sources, encompassing key factors that influence growth, including drivers and restraints.

The cloud gaming market is segmented by type (video streaming, file streaming), by device (smartphones, gaming consoles, PC, mobile devices, others), by game type (casual gamers, avid gamers, lifestyle gamers), by geography (North America [United States, Canada], Europe [Germany, United Kingdom, France, Italy, Rest of Europe], Asia-Pacific [China, Japan, India, Rest of Asia-Pacific], Latin America, and Middle East and Africa). The report offers market forecasts and size in value (USD) for all the above segments.

| By Type | Video Streaming | ||

| File Streaming | |||

| By Device | Smartphones | ||

| Tablets | |||

| PCs and Laptops | |||

| Others (Handheld Devices, Gaming Consoles) | |||

| By Gamer Type | Casual Gamers | ||

| Avid Gamers | |||

| Lifestyle Gamers | |||

| By Business Model | Subscription-Based | ||

| Pay-As-You-Play | |||

| Free-to-Play and Ad-Supported | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | United Arab Emirates | ||

| Saudi Arabia | |||

| South Africa | |||

| Rest of Middle East and Africa | |||

| Video Streaming |

| File Streaming |

| Smartphones |

| Tablets |

| PCs and Laptops |

| Others (Handheld Devices, Gaming Consoles) |

| Casual Gamers |

| Avid Gamers |

| Lifestyle Gamers |

| Subscription-Based |

| Pay-As-You-Play |

| Free-to-Play and Ad-Supported |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Rest of Middle East and Africa |

Key Questions Answered in the Report

What is the current Cloud Gaming Market size?

In 2025, the Cloud Gaming Market size is expected to reach USD 5.32 billion.

Who are the key players in Cloud Gaming Market?

Nvidia Corporation, Blacknut, Microsoft Corporation, Numecent Holdings Ltd and Parsec Cloud Inc. (Unity Software Inc.) are the major companies operating in the Cloud Gaming Market.

Which is the fastest growing region in Cloud Gaming Market?

Middle East and Africa is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Cloud Gaming Market?

In 2025, the Asia Pacific accounts for the largest market share in Cloud Gaming Market.

What years does this Cloud Gaming Market cover, and what was the market size in 2024?

In 2024, the Cloud Gaming Market size was estimated at USD 3.13 billion. The report covers the Cloud Gaming Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Cloud Gaming Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: July 7, 2025