Subscription-Based Gaming Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 13.1 Billion |

| Market Size (2031) | USD 20.38 Billion |

| Growth Rate (2026 - 2031) | 9.25% CAGR |

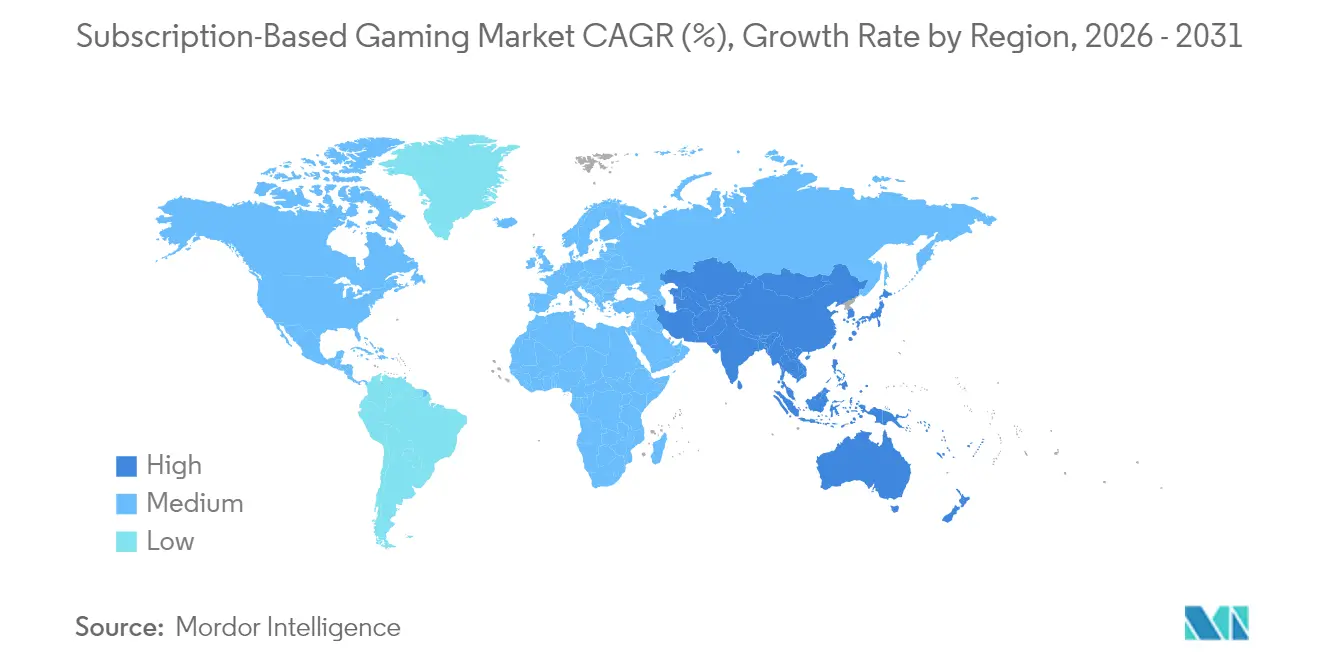

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Subscription-Based Gaming Market Analysis by Mordor Intelligence

The subscription-based gaming market size is expected to grow from USD 11.99 billion in 2025 to USD 13.1 billion in 2026 and is forecast to reach USD 20.38 billion by 2031 at 9.25% CAGR over 2026-2031. The growth curve mirrors a wider pivot across digital entertainment from ownership toward on-demand access, an evolution fueled by the rollout of 5G networks, maturing edge-compute infrastructure, and content libraries that now launch cloud-native AAA titles on day one. Platform holders are reallocating budgets from loot-box mechanics to recurring revenue models in response to tightening regulations, which further accelerates the adoption of subscription plans over one-time purchases. Cross-platform account portability, improved payment localization in emerging markets, and bundled telco offers that wrap connectivity with game passes continue to enlarge the global subscriber base. As a result, the subscription-based gaming market is moving from an early-adopter niche to a mainstream revenue generator across consoles, PCs, and mobile devices.

Key Report Takeaways

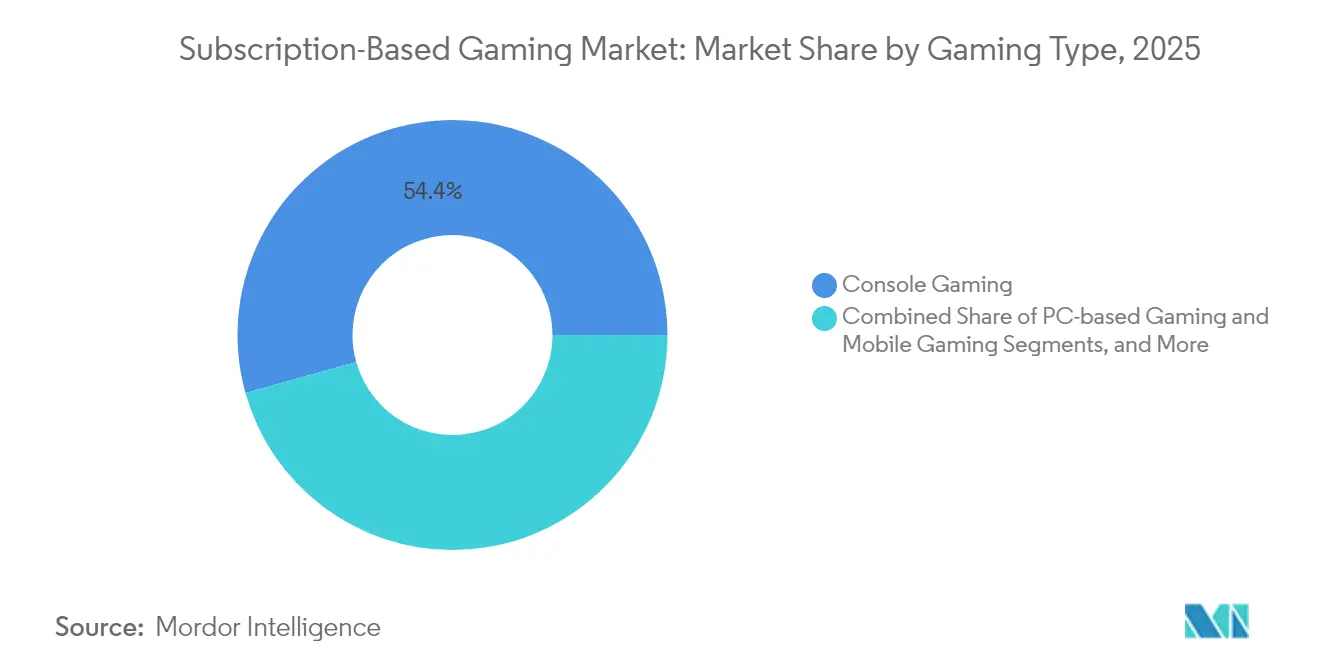

- By gaming type, console commanded 54.35% of subscription-based gaming market share in 2025, while mobile is forecast to expand at a 9.95% CAGR through 2031.

- By platform type, download-to-device services held 60.32% share of the subscription-based gaming market size in 2025; cloud streaming is advancing at an 11.05% CAGR to 2031.

- By subscription tier, premium plans accounted for 48.55% of 2025 revenue, whereas family tiers are tracking a 10.05% CAGR to 2031.

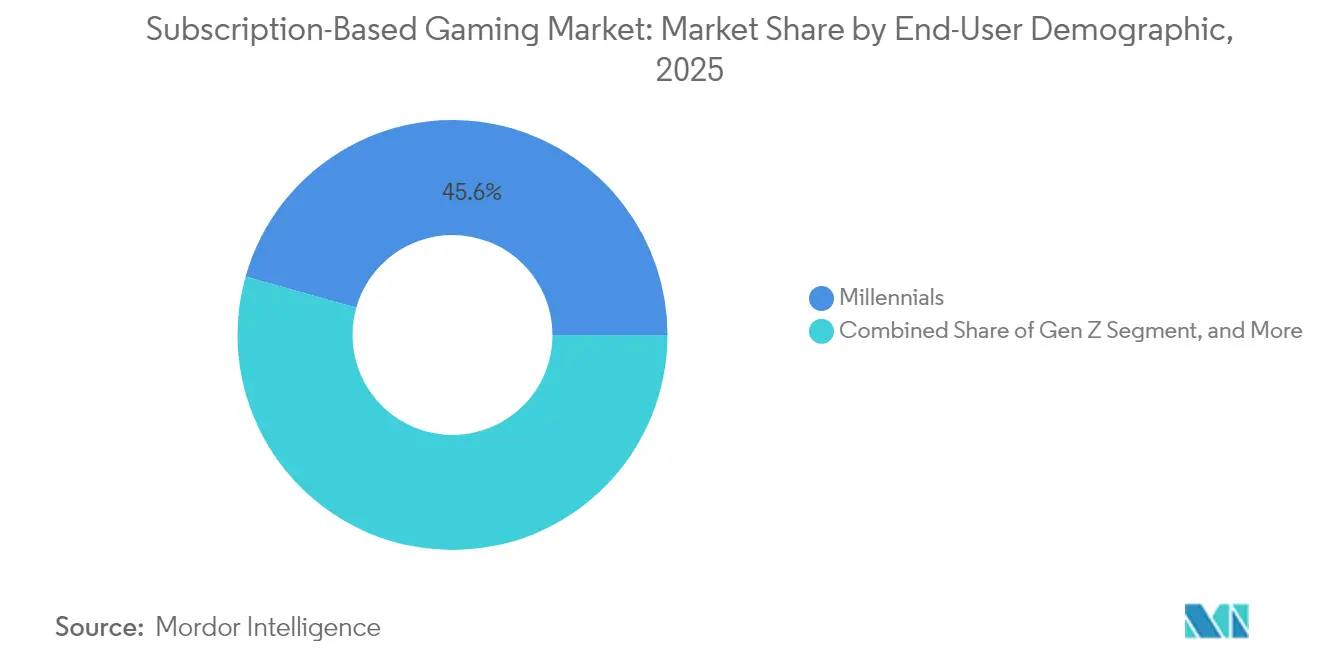

- By end-user demographic, millennials captured 45.62% of subscription-based gaming market share in 2025; Gen Z usage is growing at a 10.35% CAGR through 2031.

- By geography, North America led with 72.35% revenue share in 2025, but Asia-Pacific is projected to record the fastest 10.6% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Subscription-Based Gaming Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-native AAA launches | +1.8% | Global – early lift in North America and Europe | Medium term (2-4 years) |

| Cross-platform account portability | +1.5% | Global – strongest in Asia-Pacific mobile markets | Short term (≤ 2 years) |

| Device-inclusive family plans | +1.2% | North America and Europe core – expanding to LATAM | Medium term (2-4 years) |

| Bundled telco-gaming offers | +2.1% | Asia-Pacific, MEA, and LATAM | Long term (≥ 4 years) |

| Gen-AI personalized curation | +1.4% | Global – advanced rollouts in developed economies | Medium term (2-4 years) |

| Regulatory caps on loot-boxes | +1.8% | Europe and select Asia-Pacific jurisdictions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cloud-Native AAA Launches Accelerate Paid Adoption

Subscribing now guarantees immediate access to blockbuster releases, turning a service once defined by back-catalog access into a launch-day destination. [1]Nasdaq, “GameSquare Completes FaZe Clan Acquisition,” nasdaq.com Publishers like Microsoft funnel more than USD 1 billion per year into day-one Game Pass additions, a commitment that elevates perceived value, supports higher price points, and lowers churn. Cloud-native pipelines remove boxed-product risk, enable simultaneous global launches, and support real-time updates that lengthen engagement cycles. As latency gaps close, fidelity matches local installs, and players increasingly accept streaming as a default. The subscription-based gaming market thus gains momentum from content that historically required USD 70 out-of-pocket purchases.

Cross-Platform Account Portability Boosts Perceived Value

Seamless identity and inventory migration across console, PC, and mobile erodes the psychological cost of switching hardware.[2]Microsoft Corp., “Xbox Game Pass,” microsoft.com Xsolla’s purchase of AcceleratXR underscores the arms race around back-end tooling that keeps progress persistent regardless of device. For consumers in Asia-Pacific, where session hopping between handset and home screen is common, portability transforms a monthly fee into a long-term asset. Implementing this feature demands unified authentication layers and cross-store entitlements, investments few smaller rivals can match. The result is a widening performance gap that favors scaled services in the subscription-based gaming market.

Device-Inclusive Family Plans Expand Addressable Base

Family tiers bundle 4-6 concurrent streams, shared libraries, and parental controls at up to 60% lower per-capita cost than standalone accounts. Households persuade multiple members to join under one master plan, driving higher penetrations at near-zero incremental acquisition spend. Because cancellations require consensus from several users, retention improves measurably versus single-seat subscriptions. The model also dovetails with cross-generational play trends, making the subscription-based gaming market more resilient to seasonal spending swings.

Bundled Telco-Gaming Offers in Emerging Markets

Carrier billing sidesteps credit-card barriers in Indonesia, India, and Nigeria, unlocking hundreds of millions of potential subscribers. Operators include gaming passes within data plans, guaranteeing both bandwidth and content for one fee, while platform owners gain low-cost distribution into prepaid user pools. These bundles also integrate network-level quality-of-service that mitigates cloud-gaming latency. Over the long term, telco alliances will contribute the biggest additive lift to subscription-based gaming market revenue across mobile-first economies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising content-licensing costs | -1.6% | Global – pressure most acute on smaller and regional platforms | Medium term (2-4 years) |

| App-store commission policies | -1.1% | Global mobile markets – strongest on iOS and Android ecosystems | Short term (≤ 2 years) |

| Limited broadband capacity slows cloud streaming | -1.4% | Emerging markets with lower fixed-line and 5G penetration | Long term (≥ 4 years) |

| Subscription fatigue from overlapping gaming passes | -0.8% | North America and Europe where multiple services compete | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Content-Licensing Costs Squeeze Margins

The check writers funding day-one launches now face escalating bid prices as multiple services compete for the same signature franchises. Microsoft already spends more than USD 1 billion annually on Game Pass licensing, a figure that sets the industry benchmark. Smaller entrants without similar budgets either accept thinner catalogs or pivot to niche content, narrowing their audience ceiling inside the subscription-based gaming market. Over time, differentiation will hinge on proprietary intellectual property and in-house studios that can lower per-title acquisition costs.

App-Store Commission Policies Limit Mobile Pass Profitability

Standard 30% fees on iOS and Android reduce gross margins and force either higher retail prices or scaled-back content investment. Direct-to-consumer web billing and region-specific regulation offer partial relief, yet uncertain timelines keep mobile subscription economics volatile. For now, service providers bundle incentives such as loyalty points or cross-platform perks to offset the commission drag, but profitability gaps remain a headwind for the broader subscription-based gaming market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Gaming Type: Console Strength Meets Mobile Velocity

Console subscriptions generated 54.35% of 2025 revenue, underscoring the deep catalog, high-fidelity graphics, and exclusive launch pipelines that appeal to core gamers. Within this cohort, the subscription-based gaming market size for consoles climbed to USD 6.52 billion in 2025 and is pacing an 7.7% CAGR through 2031. Xbox Game Pass and PlayStation Plus extend back-compatibility libraries that push perceived value well beyond the monthly fee. Conversely, mobile subscriptions—currently a smaller slice—are expanding at a 9.95% CAGR as smartphone penetration eclipses 90% in several Southeast Asian countries. Cloud streaming bridges hardware gaps, delivering console-quality titles on midrange devices and pulling younger demographics into paid ecosystems.

Mobile’s ascent also reflects shorter session loops, social sharing norms, and incremental payment habits shaped by free-to-play culture. Bundled telco passes lower friction, while identity portability keeps progress intact across handset upgrades, reducing churn risk. PC subscriptions occupy a middle ground, leaning on storefronts like Steam to test curated passes, though competition from both mobile accessibility and console exclusivity remains intense. The interplay among these three form factors continues to shape the trajectory of the subscription-based gaming market, encouraging hybrid offerings that let one account roam freely across screens.

By Platform Type: Download Supremacy Faces Cloud Challenge

Download-to-device services still hold 60.32% of overall revenue because local installation assures performance regardless of connectivity, a fact valued by latency-sensitive competitive players. At the same time, cloud streaming platforms are racing ahead with an 11.05% CAGR, lifted by 5G backhaul, edge compute, and codecs that now deliver 60 fps gameplay at 1080p on mid-tier networks. That momentum is steering content owners to dual-release strategies, offering both download and stream options within one subscription, thereby hedging against bandwidth disparities.

Hybrid architecture has become central to value propositions. Subscribers download for offline play yet retain the freedom to stream instantly on devices lacking storage. The subscription-based gaming market, therefore, is no longer an “either-or” platform battleground but a continuum where infrastructure quality, not consumer preference, decides the dominant access mode. As fiber deployment widens and cross-device handoff tightens, pure streaming could overtake downloads, but for now coexistence defines the competitive landscape.

By Subscription Tier: Premium Price Gives Way to Family Economics

Premium tiers represent 48.55% of top-line revenue, fueled by early access, exclusive cosmetics, and ad-free experiences that justify a USD 16-20 monthly fee in developed markets. Yet the strongest growth lives inside family-oriented plans, rising at 10.05% CAGR as households opt to share one subscription across multiple profiles. Those plans often cost just 40-60% of the combined individual outlay, tilting upgrade math in their favor. Content holders respond by adding parental dashboards, cloud-based save partitions, and age ratings that coexist under a single license.

Basic tiers remain a gateway in price-sensitive regions; however, upsell funnels built around seasonal battle passes coax gamers toward richer packages. The subscription-based gaming market accommodates this laddered approach by linking cross-tier benefits: points earned in basic can be redeemed at a discount when upgrading to premium, while family plans inherit premium perks. Over time, tier engineering is expected to follow a “good-better-best” template refined in video and music streaming.

By End-User Demographic: Millennials Anchor, Gen Z Accelerates

Millennials account for 45.62% of current subscribers, retaining loyalty to franchises they grew up with and possessing disposable income that supports monthly fees. They are also the generation most likely to purchase premium hardware, reinforcing console segment dominance. Gen Z, however, demonstrates the swiftest adoption curve at a 10.35% CAGR, driven by social co-op modes, influencer-led discovery, and preference for cross-play convenience. Content personalization powered by AI resonates with their demand for curated experiences over massive backlogs.

Gen X and baby boomers form a smaller yet profitable segment seeking variety and convenience, making them receptive to family bundles that require minimal setup. Multi-generational households amplify cross-selling opportunities, with younger members introducing subscription services and older members maintaining renewal because of shared engagement. Demographic dynamics thus shape marketing, content acquisition, and feature roadmaps as the subscription-based gaming market matures.

By Revenue Model: Hybrid Strategies Capture Wallet Share

Pure subscription access, while transparent, leaves revenue on the table once a player exhausts must-try titles. Hybrid models blend flat-rate libraries with optional season passes, cosmetics, or expansion packs, achieving higher average revenue per user without alienating cost-sensitive audiences. Publishers reap diversified income streams while giving subscribers the choice to spend more for cosmetic prestige or stick to included content. Regulatory scrutiny dampens the appeal of randomized loot boxes, favoring non-gambling add-ons such as fixed-price battle passes.

In practice, services gate certain samplers behind a subscription wall and then monetize additional DLC through one-off fees. The subscription-based gaming market thereby mirrors evolving film and music ecosystems where base access is table stakes and premium tiers unlock exclusive perks. As cross-media franchises rise, expect synergistic bundles that fuse games with comics, film, and physical merchandise, widening the canvas for hybrid monetization.

Geography Analysis

North America generated 72.35% of 2025 revenue and continues to anchor the subscription-based gaming market owing to universal broadband, high console ownership, and frictionless digital wallets. Cross-platform account syncing is near standard, reinforcing ecosystem stickiness and justifying higher monthly pricing. Canada shows above-average family-plan penetration and benefits from favorable exchange rates that stretch purchasing power. Regulatory focus remains light compared with Europe, yet probes into app-store commissions and child protections may reshape fee economics.

Asia-Pacific recorded the fastest 10.6% CAGR and will add the largest absolute subscriber count through 2031. Smartphone ubiquity gives mobile the edge, while telco bundles combined with direct carrier billing unlock segments historically outside the banking system. Indonesia, India, and Vietnam exemplify this trajectory, with gaming time in Southeast Asia rising 53% during 2024. Japan, though more mature, leads in loyalty-program integrations that tie point systems to subscription renewals. China remains complex: domestic titans Tencent and NetEase dominate, yet regulatory caps on screen time and foreign content approvals temper growth. Europe stands as a mature yet policy-shifting territory; Belgium and Netherlands restrict loot-boxes, encouraging publishers to pivot to service passes. Localization in languages, payment preferences, and content ratings increases operational cost, but successful adaptation yields durable positions in a region with high average revenue per user. Latin America is an emerging prize: Brazil’s volume of downloads paired with improved payment rails signals readiness for broader subscription uptake. Africa, with the gaming market hitting USD 1.8 billion in 2024, shows 12.4% annual growth, 90% of which is mobile-driven, indicating a greenfield scenario for bundle-centric offerings

Competitive Landscape

The subscription-based gaming market features moderate concentration where ecosystem giants leverage exclusives and deep wallets to secure day-one launches. Microsoft devotes more than USD 1 billion each year to Game Pass content, ensuring a steady cadence of high-profile titles that sustain engagement. Sony counters with a tiered PlayStation Plus that layers cloud streaming, classic libraries, and discounted add-ons to retain its console audience. Nintendo remains selective, channeling a curated catalog into its Online Expansion Pack and banking on first-party nostalgia.

Outside the console triumvirate, Netflix has inserted itself by offering 70 mobile titles as part of a broader entertainment package, evidencing the blurring lines between media verticals. Xsolla’s acquisition of AcceleratXR highlights the importance of infrastructure that supports cross-platform portability and frictionless payments. Meanwhile, GameSquare’s merger with FaZe Clan demonstrates how esports influence and creator networks can amplify subscriber acquisition funnels.[3]Xsolla, “Gaming and Payments in Asia,” xsolla.com

Smaller hopefuls either occupy niche lanes—retro arcades, indie-only selections—or exit the field under scale pressure, as illustrated by Utomik’s 2025 shutdown. Telco-backed entrants emerge in Africa and Southeast Asia, wielding billing integration and zero-rating data allowances as competitive wedges. Over the medium term, competitive advantage will hinge on proprietary IP, AI-driven personalization, and cross-media franchises that extend beyond pure gameplay. For consumers, the escalating battle promises richer catalogs and bundled perks, reinforcing the appeal of the subscription-based gaming market.

Subscription-Based Gaming Industry Leaders

Microsoft Corporation (Xbox Game Pass)

Sony Group Corporation (PlayStation Plus)

Nintendo Co., Ltd. (Nintendo Switch Online)

Apple Inc. (Apple Arcade)

Electronic Arts Inc. (EA Play)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Utomik announced the shutdown of its cloud gaming subscription service, citing competitive pressures from larger content-rich platforms.

- November 2024: Miniclip acquired Easybrain for USD 1.2 billion, expanding its casual and mobile subscription offerings.

- November 2024: Modern Times Group completed the USD 620 million acquisition of Plarium, strengthening cross-platform subscription capabilities.

- September 2024: FaZe Clan and G FUEL revived a multi-year licensing deal that grants FaZe Media an equity position in the energy-drink brand.

Global Subscription-Based Gaming Market Report Scope

The study tracks the demand in the subscription-based gaming market, which is emerging as a viable source of revenue for console and cloud-based gaming vendors. Cloud-based gaming revenues are also factored into the market sizing, considering their mode of operation.

The gaming subscriptions market is segmented by type (console gaming, PC-based gaming, and mobile gaming ) and geography (North America, Europe, Asia Pacific, and Rest of the World). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Console Gaming |

| PC-based Gaming |

| Mobile Gaming |

| Cloud Streaming |

| Download-to-Device |

| Basic |

| Premium |

| Family/Group |

| Gen Z (10-24 yrs) |

| Millennials (25-40 yrs) |

| Gen X and Older (41+ yrs) |

| Pure-play Subscription |

| Hybrid (Subscription + Micro-transactions) |

| North America | United States |

| Canada | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Rest of Asia Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Gaming Type | Console Gaming | |

| PC-based Gaming | ||

| Mobile Gaming | ||

| By Platform Type | Cloud Streaming | |

| Download-to-Device | ||

| By Subscription Tier | Basic | |

| Premium | ||

| Family/Group | ||

| By End-User Demographic | Gen Z (10-24 yrs) | |

| Millennials (25-40 yrs) | ||

| Gen X and Older (41+ yrs) | ||

| By Revenue Model | Pure-play Subscription | |

| Hybrid (Subscription + Micro-transactions) | ||

| By Geography | North America | United States |

| Canada | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the subscription-based gaming market by 2031?

The market is expected to reach USD 20.38 billion by 2031, expanding at a 9.25% CAGR

Which region is growing fastest for subscription-based gaming?

Asia-Pacific is pacing an 10.6% CAGR through 2031, driven by mobile-first usage and telco bundles.

Why are family subscription tiers gaining popularity?

Family plans offer shared access for multiple users at up to 60% cost savings, boosting household penetration and retention.

How do regulatory actions affect subscription growth?

Restrictions on loot-boxes in Europe and parts of Asia push publishers toward transparent recurring revenue, benefiting subscription adoption.

Which platform model is growing faster, download or cloud streaming?

Cloud streaming is expanding at an 11.05% CAGR as 5G and edge computing improve latency, though downloads still dominate revenue today.

Page last updated on: