Civil Aerospace Training And Simulation Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

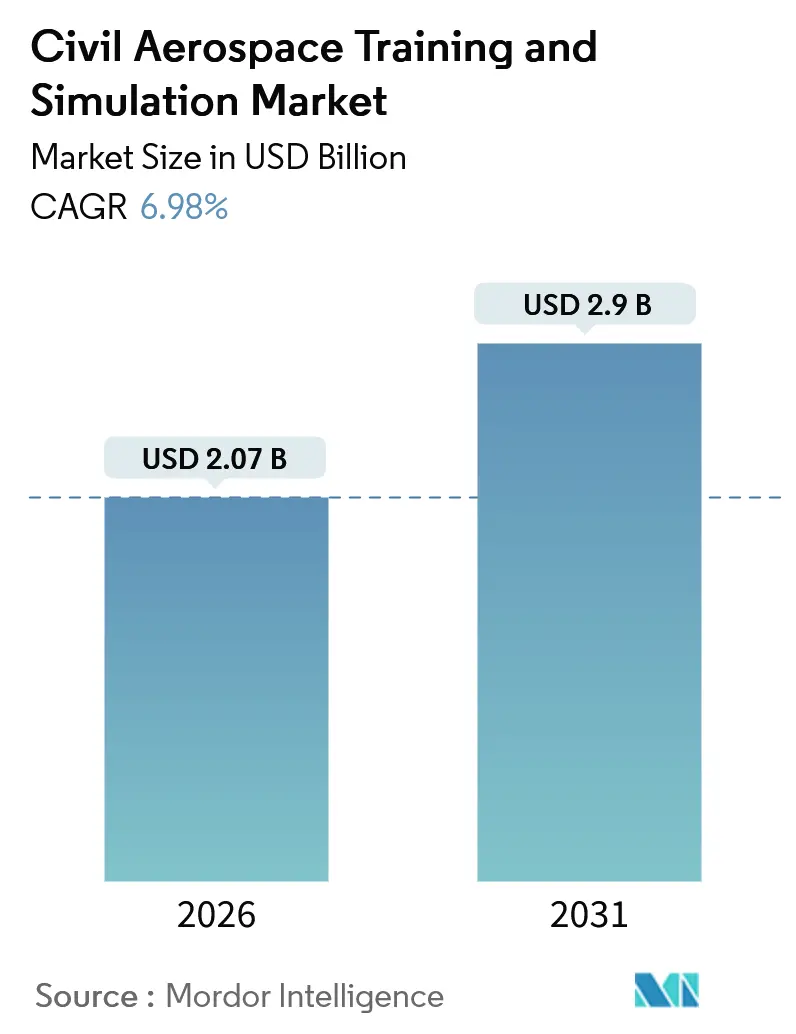

| Market Size (2026) | USD 2.07 Billion |

| Market Size (2031) | USD 2.9 Billion |

| Growth Rate (2026 - 2031) | 6.98% CAGR |

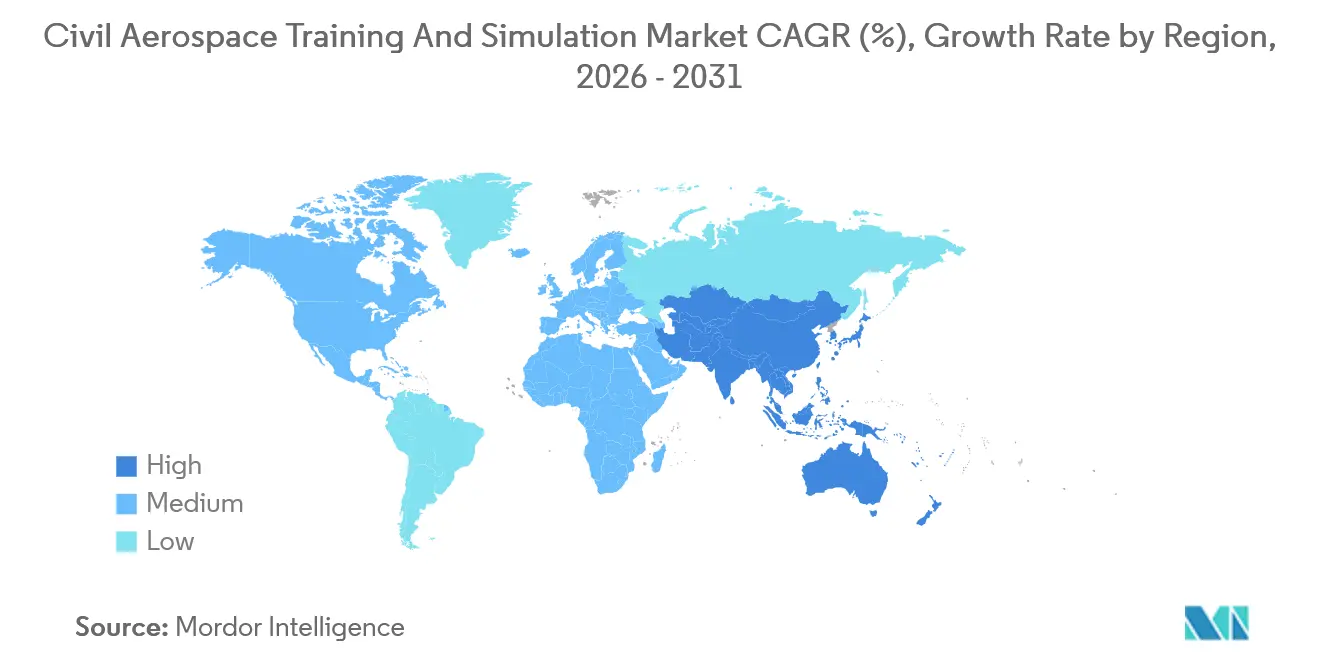

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Civil Aerospace Training And Simulation Market Analysis by Mordor Intelligence

The civil aerospace simulation and training market size stands at USD 2.07 billion in 2026 and is projected to reach USD 2.90 billion by 2031, growing at a 6.98% CAGR over the forecast period. Steady growth reflects airlines’ need to qualify record numbers of flight-deck and maintenance personnel while keeping revenue aircraft in service. This balance favors high-fidelity synthetic environments over fuel-intensive live flying. Regulatory authorities in the United States and Europe continue to expand the proportion of recurrent checks that can be completed in simulators, further enhancing the economics of the civil aerospace simulation and training market. At the same time, rapid adoption of digital-twin software and portable VR trainers compresses learning cycles and broadens access in secondary cities where full-flight devices were previously unaffordable. Rising cybersecurity expenditures and a deepening shortage of certified instructors temper momentum, but have not altered the upward trajectory, especially in the Asia-Pacific region, where China and India have set ambitious pilot-production targets.

Key Report Takeaways

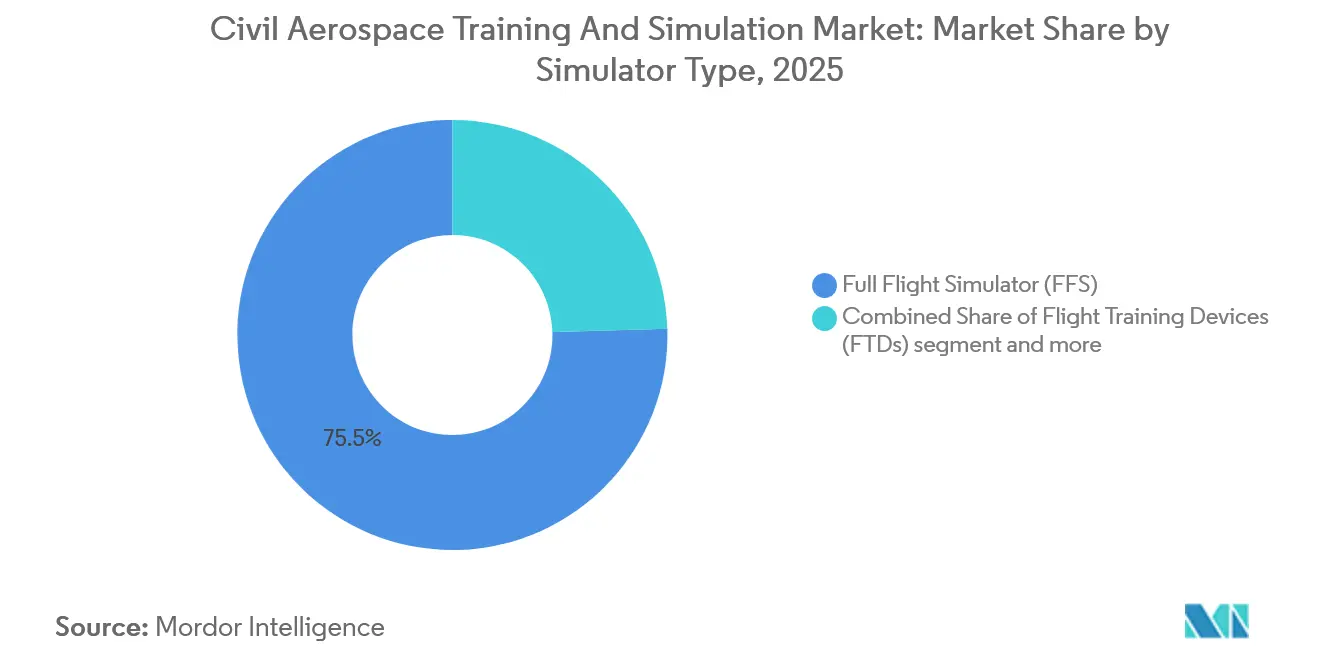

- By simulator type, full flight simulators captured 75.47% of the civil aerospace simulation and training market share in 2025; other simulator types, led by VR and fixed-base trainers, are forecast to expand at a 7.24% CAGR through 2031.

- By application, commercial aviation accounted for 72.13% of the revenue in 2025, while the space segment is poised for a 7.11% CAGR on the back of Artemis and commercial astronaut programs.

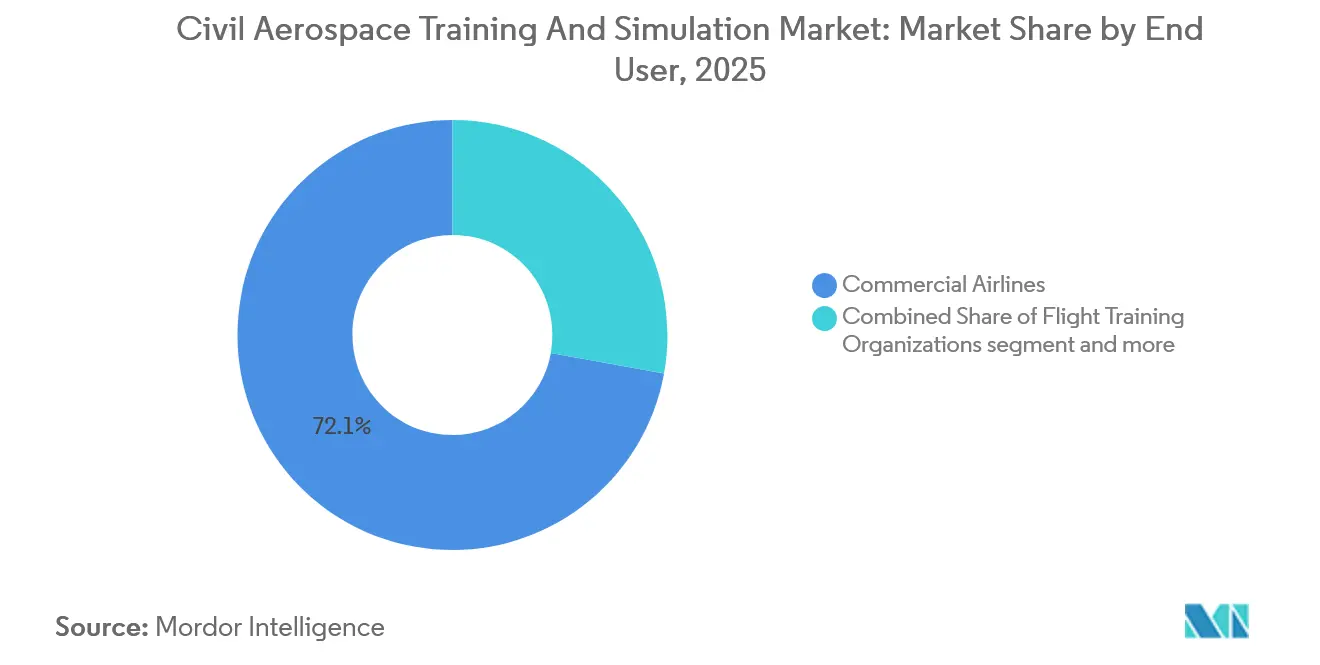

- By end user, commercial airlines accounted for 57.24% of spending in 2025; space agencies are the fastest-growing cohort, with a growth rate of 7.82% per year.

- By Geography, North America dominated the market with 47.17% in 2025; however, the Asia-Pacific region is expected to record a brisk 7.75% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Civil Aerospace Training And Simulation Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global demand for trained pilots, technicians, and cabin crew | +2.1% | Asia-Pacific, Middle East, spill-over to Africa | Medium term (2–4 years) |

| Increasingly stringent safety and regulatory training requirements | +1.2% | North America, European Union, cascading to Asia-Pacific and Middle East | Long term (≥ 4 years) |

| Cost advantages of simulation-based training compared to live aircraft operations | +1.6% | Europe, Japan, Africa, South America | Short term (≤ 2 years) |

| Growing adoption of VR- and AR-based portable simulators for early stage training | +1.5% | North America, European Union, China, India, South Korea | Short term (≤ 2 years) |

| Use of digital twin technologies to personalize and optimize training outcomes | +1.3% | North America, Western Europe, Singapore, Japan, Australia | Medium term (2–4 years) |

| Expansion of airline fleets and introduction of new aircraft types increasing transition training needs | +1.8% | Asia-Pacific, Middle East, global fleet operators | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Demand for Trained Pilots, Technicians, and Cabin Crew

The worldwide fleet expansion has outpaced the talent pipelines. Boeing’s 2025 outlook indicated a need for 649,000 new commercial pilots by 2043, with 42% of them located in the Asia-Pacific region. China aims to recruit an additional 100,000 pilots by 2035 to operate nearly 4,930 transport aircraft. India’s airlines ordered more than 1,000 narrowbody jets between 2023 and 2025, forcing carriers to reserve simulator slots years in advance.[1]Directorate General of Civil Aviation India, “Annual Report 2024-2025,” dgca.gov.in Maintenance technicians also require recurrent composite repair and avionics updates for new-generation airframes, while cabin crews must certify in high-density evacuation procedures. These combined needs funnel students into the civil aerospace simulation and training market far more quickly than legacy training centers can scale, fueling demand for both fixed-site Level-D devices and mobile VR units that alleviate peak load.

Growing Adoption of VR- and AR-Based Portable Simulators for Early Stage Training

Head-mounted displays are shifting ab-initio curricula from brick-and-mortar schools to modular spaces. Loft Dynamics gained EASA approval in 2024 for an untethered VR helicopter simulator that operators can deploy aboard offshore platforms or in temporary classrooms. CAE’s 2025 rollout of the CAE Rise augmented-reality suite overlays checklists onto cockpit mock-ups, thereby reducing cognitive load during the first 50 hours of training. The US Air Force’s Pilot Training Next project cut time-to-wings by 30%, a metric that civilian schools emulate to accelerate throughput. VR devices cost barely 2% of a Level-D simulator, enabling smaller academies to tap into the civil aerospace simulation and training market without incurring heavy debt. Airlines in secondary cities now lease such equipment to pre-screen cadets, freeing full-motion bays for high-stakes checks.

Use of Digital Twin Technologies to Personalize and Optimize Training Outcomes

FlightSafety integrated Honeywell’s Forge engine into its A320 simulators in 2025 to capture eye-tracking and stress biomarkers, allowing difficulty levels to adapt in real time. Thales deployed similar machine-learning feedback for Air France, forcing repetition of recurrent errors until pilots hit proficiency thresholds.[2]Thales Group, “TopSky Training Suite Deployment,” thalesgroup.com NASA’s Artemis simulators replicate real-time spacecraft telemetry, allowing astronauts to rehearse abort scenarios under authentic fault conditions. Airlines report that competency-based progress reduces type-rating hours to 32 from 40, allowing pilots to return to revenue flying sooner. These efficiencies strengthen the civil aerospace simulation and training market by converting fixed training budgets into higher student volume without raising capital expenditures.

Expansion of Airline Fleets and Introduction of New Aircraft Types Increasing Transition Training Needs

Boeing delivered 528 jets in 2025, including the first 777-9, which features touchscreen avionics that differ markedly from the legacy widebody layouts. Airbus shipped 735 aircraft and debuted the A321XLR, whose extended-range fuel-management protocols require new certification modules. Each new cockpit architecture obliges airlines to order a dedicated full-flight simulator, generating steady replacement demand in the civil aerospace simulation and training market. Regional carriers adopting Embraer E2 and Comac C919 variants face the same constraint, often relying on manufacturer-run centers that bundle training with aircraft purchase. Consequently, simulator OEMs book multi-year backlogs that lock in revenue visibility through 2031.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital costs associated with full flight and Level-D simulators | -0.9% | Emerging markets in Africa, South America, Southeast Asia | Long term (≥ 4 years) |

| Regulatory certification and approval backlogs delaying simulator deployment | -0.8% | European Union, United States, dual-certification seekers in Asia-Pacific | Medium term (2–4 years) |

| Rising cybersecurity and data-protection costs for cloud-connected training systems | -0.6% | European Union, North America, growing scrutiny in Asia-Pacific and Middle East | Short term (≤ 2 years) |

| Limited availability of qualified simulator instructors and examiners constraining training capacity | -0.7% | Asia-Pacific (India, China, Indonesia), Africa, secondary markets in North America and EU | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Capital Costs Associated with Full-Flight and Level-D Simulators

A Level-D simulator for aircraft like the 737 MAX or A320neo involves significant capital investment and recurring maintenance costs, reflecting its advanced technical requirements. Banks in Southeast Asia and Africa demand pre-sold hours as collateral, yet airlines hesitate to sign lengthy contracts without proof of availability, trapping small schools in a financing loop. Leasing eases capital expenditures (capex) but carries rate premiums that erode thin margins. For widebody simulators, utilization below 4,000 hours turns the asset uneconomic, concentrating capacity in megahubs and leaving outlying regions underserved.

Limited Availability of Qualified Simulator Instructors and Examiners

Global examiner numbers rose only 2% in 2025 against a 6% jump in pilot candidates.[3]International Civil Aviation Organization, “Global Aviation Training Report 2025,” icao.int India alone held a 3,200-pilot waitlist for type rating check rides despite open simulator slots. US instructors earn significantly less than airline first officers, which limits lateral movement into teaching. FlightSafety’s 2024 equity-linked hiring plan will take 18 months to lift capacity. During peak hiring periods, airlines retain seasoned captains for line flying, thereby compounding the bottleneck and restraining the expansion of the civil aerospace simulation and training market.

Segment Analysis

By Simulator Type: Full-Flight Dominance Meets Portable Disruption

Full-flight simulators accounted for 75.47% of the civil aerospace simulation and training market in 2025. Regulatory frameworks, such as FAA 14 CFR Part 60, compel their use for type ratings and recurrent checks, ensuring baseline demand even during traffic downturns. Yet, the civil aerospace simulation and training market size for other simulator types is projected to expand at a 7.24% CAGR, reflecting airlines' shifting of ab-initio and refresher tasks to VR headsets and fixed-base devices.[4]Loft Dynamics, “EASA Certification Press Release,” loftdynamics.com

Growth in portable systems reduces capital intensity while widening geographic reach. Loft Dynamics’ untethered platform eliminates hydraulic motion and fits inside shipping containers for pop-up classrooms. Redbird Flight Simulations logged a 40% rise in fixed-training-device orders among US Part 141 schools in 2025. As regulators gradually credit more synthetic hours, the civil aerospace simulation and training market gains a two-tier structure: high-fidelity bays for high-stakes checks and scalable VR labs for volume throughput.

Note: Segment shares of all individual segments available upon report purchase

By Application: Commercial Scale Versus Space Velocity

Commercial aviation generated 72.13% of 2025 revenue, supported by active airframes that require more than 10,000 simulator hours annually. Airlines replace motion systems every 10-12 years to keep pace with cockpit software baselines, cushioning OEM order books. The civil aerospace simulation and training market size for space applications, while much smaller, is expanding at a 7.11% CAGR as NASA, SpaceX, and Blue Origin commission bespoke lunar, docking, and microgravity trainers.

Space simulators differ fundamentally from aircraft simulators, modeling one-sixth gravity dynamics and several-second communication latency. ESA’s Columbus module upgrade in 2025 incorporated fluid-dynamics emulation, allowing astronauts to rehearse capillary-action experiments. Commercial providers see early opportunity in sub-orbital tourist briefings, where fixed-base cabins run high-volume familiarization loops. Over the decade, space could represent a meaningful share of civil aerospace simulation and training market growth if funding for Artemis follow-on missions and private stations stays intact.

By End User: Airlines’ Volume Versus Space Agencies’ Urgency

Commercial airlines accounted for 57.24% of spending in 2025, reflecting their fleet size and the legally mandated six- to twelve-month proficiency cycles. A simulator, operating extensively at a defined hourly rate, amortizes within a standard four-year period, reinforcing internal procurement strategies for major carriers such as Emirates and United. Flight training organizations occupy the middle ground, capturing cadets and regional pilots but suffering a margin squeeze when airlines insource capacity.

Space agencies, though only 7.82% of 2025 dollars, post the fastest rise as Artemis and Gaganyaan compress development timelines. ISRO’s contract with Thales for a Gaganyaan crew-module simulator highlights the premium agencies pay for mission-specific fidelity. As more governments fund lunar surface and Mars flyby concepts, the civil aerospace simulation and training market is poised to gain high-value, low-volume orders that balance commercial cyclicality.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America retained 47.17% of the 2025 revenue, driven by OEM clusters, a dense network of over 200 training centers, and FAA rules that allow up to 50% of recurrent checks to be credited to simulators. Utilization frequently tops 5,000 hours a year per device, ensuring swift payback and steady aftermarket demand for software refreshes. Growth moderates toward replacement of aging bays rather than greenfield builds, with incremental upside tied to 777X and eVTOL simulator launches.

The Asia-Pacific is the locomotive of the civil aerospace simulation and training market, forecasted to grow at a 7.75% annual rate to 2031, as China, India, Indonesia, and Vietnam embark on historic fleet expansions. Beijing funds concessional loans that cut interest costs for training academies, while India’s 100% FDI allowance spurred a CAE-InterGlobe joint venture in 2024 with eight simulators online in Delhi and Bangalore. Indonesia’s Lion Air ordered six 737 MAX devices in 2025, citing the logistical advantage of localizing type-rating capacity.

Europe, under EASA, exhibits lower headline growth but steady revenue from the five-year revalidation cycle, which compels upgrades to match aircraft software baselines. Middle East mega-carriers operate captive centers that also serve as third-party hubs for African and South Asian pilots, leveraging geographic centrality to achieve high-yield utilization. Africa remains under-penetrated after South African Airways shuttered its Johannesburg center, forcing trainees to travel abroad, an expense that dampens demand. South America is concentrated in Brazil, where Azul sustains a small but profitable cluster of A320 and 737 simulators in São Paulo.

Competitive Landscape

The civil aerospace simulation and training market remains moderately concentrated, with CAE Inc., FlightSafety International Inc., RTX Corporation, Thales Group, and TRU Simulation + Training Inc. collectively controlling the majority of the market share. These incumbents anchor long-term service contracts that bundle hardware sales with maintenance, updates, and instructor staffing, yielding sticky cash flows; the majority of CAE’s 2024 civil revenue is derived from services rather than product sales.

Challengers exploit software innovation. Loft Dynamics offers an EASA-approved VR platform that bypasses motion systems, slashing capital outlay by 80% and opening up white space in remote locations. Collins Aerospace filed a 2025 patent for a holographic-display hybrid simulator that preserves tactile feedback while halving the floor space needed. Cybersecurity compliance becomes a competitive lever; large providers absorb thousands of annual costs to satisfy NIST and prospective EASA Part-IS rules, cost levels that smaller firms struggle to meet.

Airlines are also entering the fray. Emirates invested USD 200 million in an 11-bay Dubai center that sells surplus hours to third parties, while United Airlines added 12 devices in 2024 to accommodate a 500-aircraft backlog. Such insourcing limits addressable hardware sales for OEMs but expands aftermarket opportunities in parts and software, keeping overall civil aerospace simulation and training market revenue on an upward slope.

Civil Aerospace Training And Simulation Industry Leaders

CAE Inc.

FlightSafety International Inc.

Thales Group

RTX Corporation

TRU Simulation + Training Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: HAVELSAN signed an agreement with The Boeing Company to integrate the B737 MAX-8 Full Flight Simulator into its production line, utilizing a Boeing simulation data package acquired through direct procurement for enhanced technical capabilities.

- November 2025: Riyadh Air procured two CAE 7000XR full-flight simulators to facilitate pilot training for Airbus A321neo operations, ensuring advanced simulation capabilities for enhanced training efficiency.

- June 2025: Acron Aviation secured a Full Flight Simulator (FFS) contract with All Nippon Airways Co., Ltd. (ANA), Japan's largest airline, thereby enhancing its training capabilities.

Global Civil Aerospace Training And Simulation Market Report Scope

An aerospace simulator is a software or hardware system designed to simulate various aspects of aerospace operations. These simulators are used for training pilots, conducting research, testing aircraft systems, and exploring aerospace concepts. Aerospace simulators can range from simple desktop applications to full-motion flight simulators used by commercial airlines and military organizations. They typically incorporate realistic graphics, physics models, and control interfaces to provide an immersive and interactive experience.

The market is segmented by simulator type, application, end user, and geography. By simulator type, the market is segmented into full flight simulators (FFS), flight training devices (FTD), and other training devices. By application, the market is segmented into commercial aviation and space. By end user, the market is segmented into commercial airlines, flight training organizations, space agencies, and others. The report also covers the market sizes and forecasts for the civil aerospace simulation and training market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Full Flight Simulator (FFS) |

| Flight Training Devices (FTDs) |

| Other Simulator Types |

| Commercial Aviation |

| Space |

| Commercial Airlines |

| Flight Training Organizations |

| Space Agencies |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Simulator Type | Full Flight Simulator (FFS) | ||

| Flight Training Devices (FTDs) | |||

| Other Simulator Types | |||

| By Application | Commercial Aviation | ||

| Space | |||

| By End User | Commercial Airlines | ||

| Flight Training Organizations | |||

| Space Agencies | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the civil aerospace simulation and training market?

It is valued at USD 2.07 billion in 2026 and is projected to hit USD 2.90 billion by 2031.

How fast is the market expected to grow?

The forecast CAGR is 6.98% between 2026 and 2031.

Which simulator category dominates spending?

Full flight simulators hold 75.47% of 2025 revenue due to regulatory mandates.

Which region will add the newest simulator capacity?

Asia-Pacific, driven by China’s and India’s pilot-production targets, is forecast to grow at 7.75% a year through 2031.

What is the biggest restraint on market expansion?

High capital costs for Level D devices restrict adoption in emerging markets.

Which technology is cutting training hours the most?

Digital-twin analytics embedded in simulators are reducing type-rating time by up to 20%.