Chromoendoscopy Agents Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 158.84 Million |

| Market Size (2030) | USD 206.51 Million |

| Growth Rate (2025 - 2030) | 5.39% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

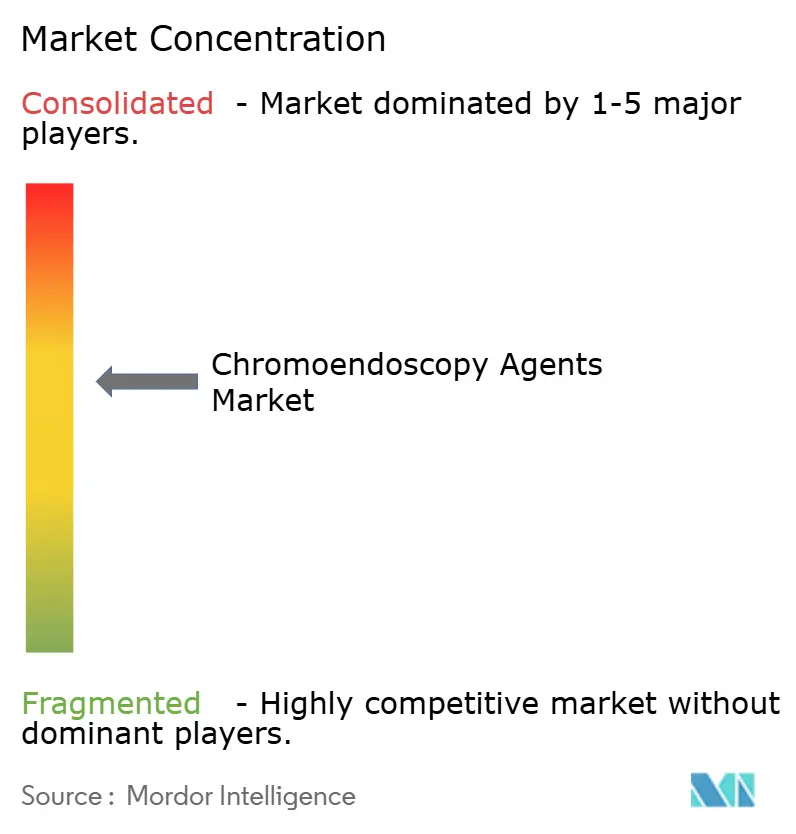

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chromoendoscopy Agents Market Analysis by Mordor Intelligence

The chromoendoscopy agents market size reached USD 158.84 million in 2025 and is forecast to climb to USD 206.51 million by 2030, reflecting a 5.39% CAGR. Market growth is propelled by the routine use of high-definition colonoscopy, the surge in inflammatory bowel disease (IBD) surveillance, and expanding regulatory support for oral-tablet dye formulations. Hospitals and ambulatory surgery centers are adopting targeted biopsy protocols to lower histopathology costs while maintaining diagnostic accuracy, strengthening the value proposition for the chromoendoscopy agents market.[1]Anderson J.C., “Cap-Assisted Chromo-Colonoscopy: Are 2 Techniques Better Than None?,” American College of Gastroenterology, journals.lww.com Supplier investments in convenient delivery formats and AI-assisted visualization platforms create additional momentum. Headwinds stem from virtual chromoendoscopy uptake and reimbursement ambiguity for traditional dye spraying, yet the integration of computer-aided detection preserves long-term demand for dye-based contrast agents.[2]Misawa M., Kudo S.-E., Mori Y., “Implementation of Artificial Intelligence in Colonoscopy Practice in Japan,” JMA Journal, jmaj.jp

Key Report Takeaways

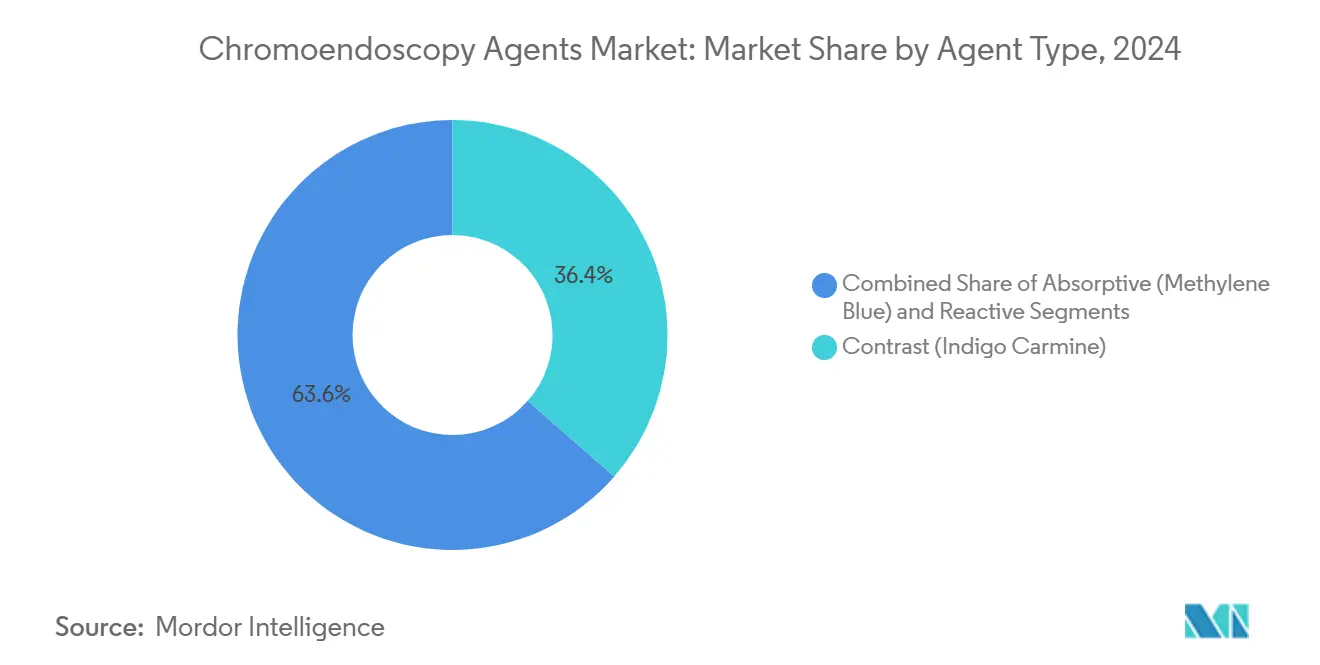

- By agent type, Contrast (Indigo Carmine) led with 36.44% of chromoendoscopy agents market share in 2024, while Absorptive (Methylene Blue) posted the fastest 9.11% CAGR through 2030.

- By formulation, liquid solutions accounted for 53.48% of the chromoendoscopy agents market size in 2024, whereas oral tablets are advancing at an 8.37% CAGR to 2030.

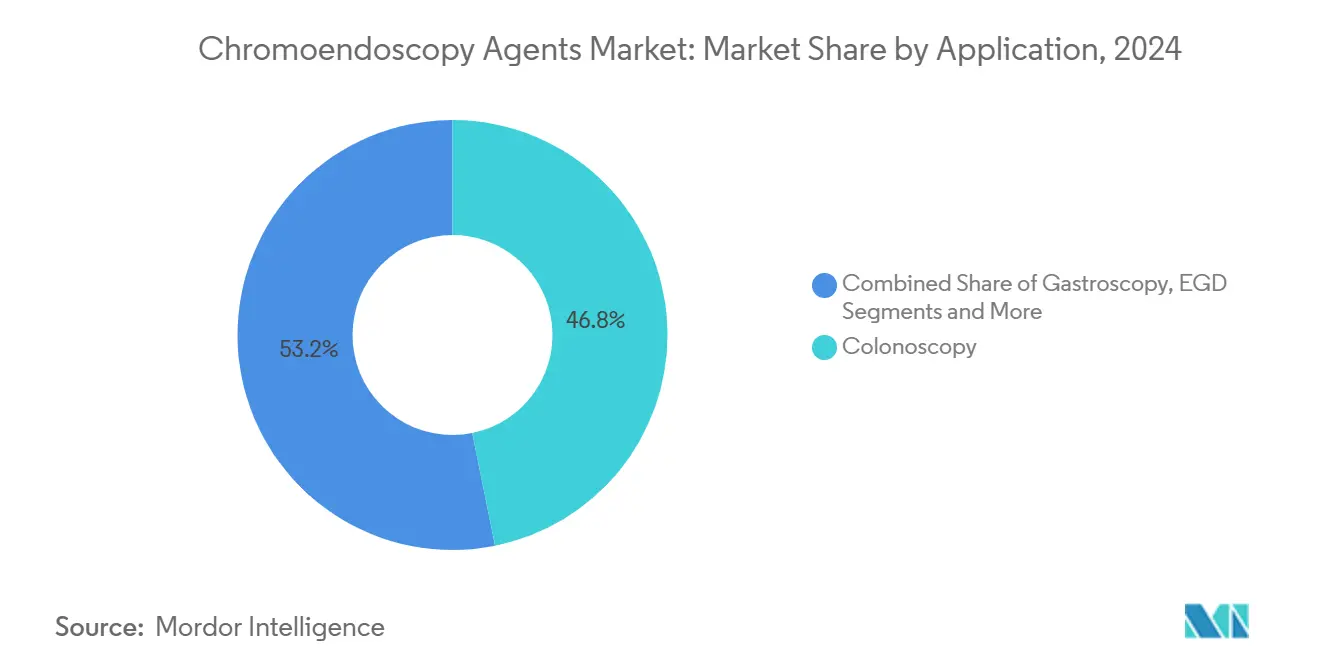

- By application, colonoscopy represented 46.83% of the chromoendoscopy agents market size in 2024 and IBD surveillance is expanding at a 9.23% CAGR through 2030.

- By end-user, hospitals held 49.77% share in 2024 and ambulatory surgery centers are growing at an 8.72% CAGR to 2030.

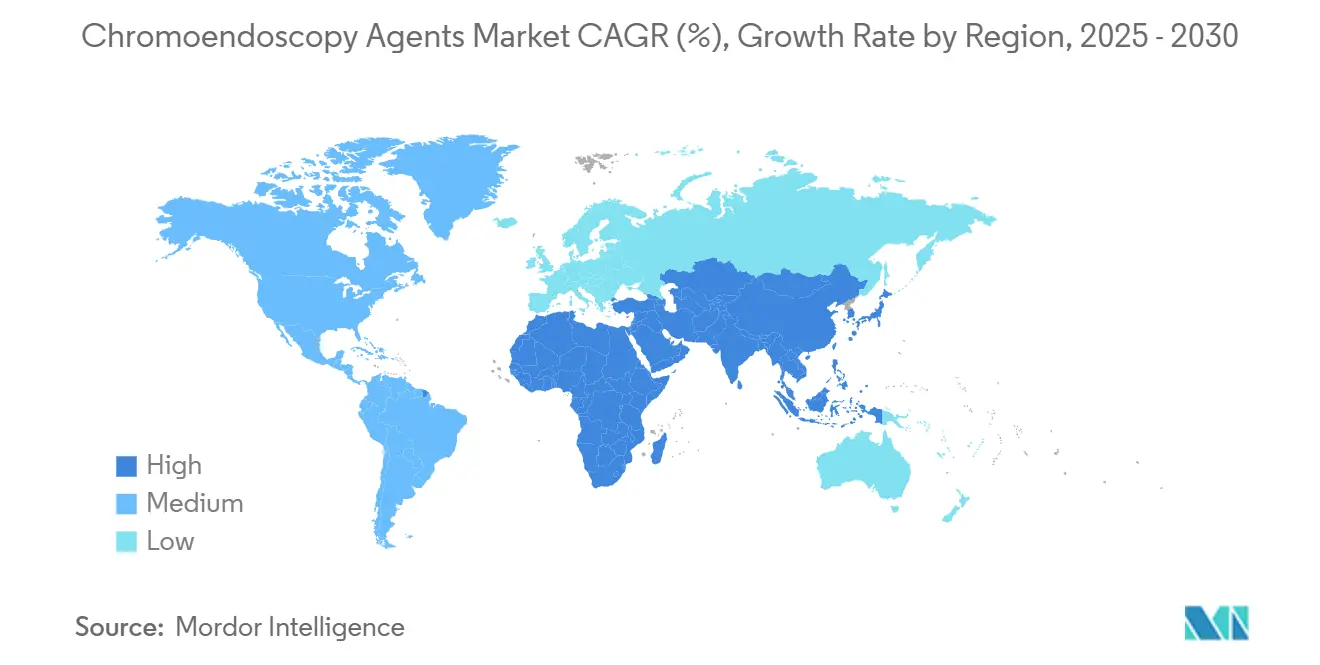

- By geography, North America commanded 31.36% share in 2024, while Asia-Pacific is set to grow at a 7.58% CAGR through 2030.

Global Chromoendoscopy Agents Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High-Definition (HD) Colonoscopy Adoption Boosts Dye Demand | +1.2% | Global, with North America & Europe leading | Medium term (2-4 years) |

| Rising Inflammatory Bowel Disease (IBD) Surveillance Volumes | +0.9% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Regulatory Approvals Of Per-Oral Dye Tablets (E.G., MB-MMX) | +0.8% | Europe & North America, expanding to APAC | Short term (≤ 2 years) |

| Shift Toward Targeted Biopsy Protocols To Cut Histology Costs | +0.7% | Global healthcare systems | Medium term (2-4 years) |

| Expansion Of Ambulatory Endoscopy Centers In Emerging Markets | +0.6% | Asia-Pacific, Latin America, MEA | Long term (≥ 4 years) |

| AI-Assisted Lesion Detection Complements Dye-Based Chromoendoscopy | +0.5% | Developed markets initially, global expansion | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High-Definition (HD) Colonoscopy Adoption Boosts Dye Demand

HD imaging magnifies subtle mucosal patterns, so adding contrast agents lifts adenoma detection rates by 8-12% versus standard white light, especially for flat lesions.[3]Lui T.K.-L. et al., “Endocuff With or Without Artificial Intelligence-Assisted Colonoscopy in Detection of Colorectal Adenoma,” American College of Gastroenterology, journals.lww.comEndoscopists gravitate toward chromo-enhanced protocols because quality scores and reimbursement increasingly track detection performance. Combining AI with HD-chromoendoscopy pushes adenoma detection beyond 58%, compared with 46% for HD alone. Growth in ambulatory centers that collectively performed more than 14 million U.S. colonoscopies in 2024 widens the addressable pool. The marginal dye cost is dwarfed by avoided expenses tied to missed lesions, sustaining uptake.

Rising Inflammatory Bowel Disease (IBD) Surveillance Volumes

IBD patients show a 2-3-fold higher colorectal neoplasia risk, triggering surveillance colonoscopy every 1-3 years. Dye-spray chromoendoscopy detects 53.9% more sessile serrated lesions in ulcerative colitis than narrow-band imaging and HD white light alone. As IBD prevalence rises in developing regions that adopt Western diets, overall procedure volumes climb. Water-assisted colonoscopy further heightens mucosal clarity, amplifying dye demand. Personalized risk-based surveillance intervals intensify repeat usage among high-risk cohorts.

Regulatory Approvals Of Per-Oral Dye Tablets (e.g., MB-MMX)

The European Medicines Agency cleared Lumeblue, a 25 mg methylthioninium chloride tablet, creating a turnkey chromoendoscopy prep that eliminates topical spraying steps. Oral dosing raises adenoma or carcinoma detection from 48% to 56% without safety trade-offs. Simplified logistics appeal to community gastroenterologists and high-volume centers alike. Multiple oral agents for Barrett’s esophagus and upper-GI screening are in the pipeline, signaling sustained formulation innovation.

Shift Toward Targeted Biopsy Protocols To Cut Histology Costs

Targeted biopsies guided by chromoendoscopy capture lesions with 73% fewer samples yet equal dysplasia detection versus random protocols, trimming laboratory fees and pathologist workloads. AI algorithms that classify lesions with 97.8% sensitivity support “diagnose-and-leave” strategies for diminutive polyps. Value-based reimbursement accentuates this cost-efficiency focus.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reimbursement Uncertainty For Traditional Dye Spraying | -0.8% | North America & Europe primarily | Short term (≤ 2 years) |

| Rapid Uptake Of Virtual Chromoendoscopy Replacing Dyes | -1.1% | Global, led by developed markets | Medium term (2-4 years) |

| Dye-Related Safety & Toxicity Concerns (E.G., Indigo Carmine) | -0.4% | Global regulatory oversight | Long term (≥ 4 years) |

| Supply Chain Bottlenecks For Pharmaceutical-Grade Dye Precursors | -0.6% | Global manufacturing dependencies | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Reimbursement Uncertainty For Traditional Dye Spraying

Distinct payment codes for dye-based procedures are rare; U.S. providers often absorb extra time and consumable outlays within standard colonoscopy reimbursements. As payers scrutinize incremental value, adoption can stall unless cost savings from fewer biopsies are clearly demonstrated.

Rapid Uptake Of Virtual Chromoendoscopy Replacing Dyes

Narrow-band and linked-color imaging reach 97.8% sensitivity for neoplastic lesions without consumables, eroding the appeal of dye spraying. Because the capability ships standard on new scopes, hospitals face no incremental capital or training cost.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Agent Type: Indigo Carmine Leads Despite Methylene Blue’s Rapid Ascent

Contrast (Indigo Carmine) secured 36.44% of the chromoendoscopy agents market share in 2024, reflecting decades of clinical familiarity and superior pooling properties for colorectal visualization. Absorptive (Methylene Blue), propelled by its new oral formulation, is forecast to post a 9.11% CAGR to 2030. Reactive dyes such as Lugol’s iodine remain niche yet indispensable in squamous dysplasia screening.

Supply chain hiccups for Indigo Carmine and cross-functional products like Eleview, which blends Methylene Blue with submucosal lifting fluid, are reshaping clinician preferences. As a result, segment contribution to the overall chromoendoscopy agents market size is expected to rebalance in favor of absorptive dyes by the decade’s end.

By Formulation: Liquid Solutions Dominate While Oral Tablets Accelerate

Liquid solutions held 53.48% of the chromoendoscopy agents market size in 2024. Clinicians appreciate immediate staining control during complex resections. Powder concentrates serve tertiary centers that tailor dilution for research protocols.

Oral tablets, led by Lumeblue, are advancing at an 8.37% CAGR, spurred by the removal of spraying complexity and the predictable staining they deliver to community practice settings. FDA clearance for injectable Methylene Blue in 2025 broadens formulation choice, underscoring a competitive shift toward convenience and safety.

By Application: Colonoscopy Dominance Challenged by IBD Surveillance Growth

Colonoscopy accounted for 46.83% of chromoendoscopy agents market size in 2024 because colorectal cancer screening remains a cornerstone of preventive care. Evidence-based guidelines now recommend contrast enhancement for quality benchmarking.

IBD surveillance, however, is on track for a 9.23% CAGR, aided by superior dye-guided dysplasia detection and fewer biopsy specimens per procedure. Barrett’s esophagus protocols and upper-GI use cases continue to niche-expand as acetic acid and Lugol’s iodine find renewed clinical interest.

By End-User: Hospitals Lead While ASCs Drive Growth

Hospitals retained a 49.77% share in 2024, benefiting from complex case mixes that require advanced visualization and sizeable histopathology budgets. Subspecialty clinics operate as early adopters and training hubs.

Ambulatory surgery centers are forecast to add an 8.72% CAGR on rising procedure volumes and payer preference for lower-cost sites. Their throughput-oriented workflows dovetail with dye-guided accuracy that trims repeat procedures. Olympus-backed training initiatives in emerging markets further accelerate ASC demand.

Geography Analysis

North America held 31.36% of the chromoendoscopy agents market share in 2024. Clinical quality programs tie adenoma detection rates to physician credentialing, validating dye use despite unpaid consumable costs. Yet, the absence of CPT codes for dye spraying creates reimbursement friction. Virtual chromoendoscopy adoption and cost-containment initiatives temper the growth trajectory, though AI integration may reinvigorate dye relevance.

Europe benefits from unified regulatory momentum; EMA approval of oral Methylene Blue tablets has broadened access and convenience for screening programs. National health services increasingly cite histology cost savings from targeted biopsy when weighing coverage. Post-Brexit logistics and heterogeneous reimbursement rules generate patchwork adoption speeds across the continent.

Asia-Pacific is projected to post the fastest 7.58% CAGR through 2030. Governments invest in screening infrastructure as colorectal cancer incidence rises. Japan’s decision to reimburse AI colonoscopy in 2024 sets a precedent for combined AI-dye protocols. China’s early detection campaigns and the proliferation of endoscopy-dedicated ambulatory centers underpin sustained volume growth. Supply-demand mismatches for dyes could emerge if local production lags rapid uptake.

Competitive Landscape

The chromoendoscopy agents market is moderately fragmented; no firm holds dominant global sway. Large pharmaceutical manufacturers exploit scale efficiencies to ensure dye precursor availability, while niche endoscopy companies create value through formulation innovation. Patent-protected oral tablets such as Lumeblue offer near-term exclusivity, but generic entry is expected once exclusivity lapses.

Strategic deals center on digital convergence. Olympus’s USD 83 million purchase of Odin Vision embeds cloud-AI analytics into its hardware ecosystem, sharpening differentiation. Bracco’s rationalization of its barium contrast line signals a broader portfolio shift toward higher-margin, procedure-enabling agents.

Supply-chain resilience is gaining prominence. Firms with multi-region production sites weathered the 2024 Indigo Carmine shortage more effectively, retaining customer loyalty. Continuous manufacturing technologies and forward-integrated distribution networks are becoming competitive necessities.

Chromoendoscopy Agents Industry Leaders

Cosmo Pharmaceuticals N.V.

American Regent Inc.

Provepharm Life Solutions

Daiichi Sankyo Co., Ltd.

Macsen Laboratories

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Nexus Pharmaceuticals received FDA approval for Methylene Blue Injection, USP, expanding therapeutic and potential chromoendoscopy use cases.

- July 2024: Bracco Diagnostics announced an expanded barium product portfolio and disclosed plans to file for FDA clearance of a fourth formulation later in the year.

Global Chromoendoscopy Agents Market Report Scope

| Contrast (Indigo Carmine) |

| Absorptive (Methylene Blue) |

| Reactive (Lugol’s Iodine, Acetic Acid) |

| Liquid / Solution |

| Powder Concentrate |

| Oral Tablet / Capsule |

| Ready-to-spray Device Cartridges |

| Colonoscopy |

| Gastroscopy |

| Esophagogastroduodenoscopy (EGD) |

| Barrett’s Esophagus Surveillance |

| Inflammatory Bowel Disease Surveillance |

| Hospitals |

| Ambulatory Surgery Centers (ASCs) |

| Specialty Gastroenterology Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Agent Type | Contrast (Indigo Carmine) | |

| Absorptive (Methylene Blue) | ||

| Reactive (Lugol’s Iodine, Acetic Acid) | ||

| By Formulation | Liquid / Solution | |

| Powder Concentrate | ||

| Oral Tablet / Capsule | ||

| Ready-to-spray Device Cartridges | ||

| By Application | Colonoscopy | |

| Gastroscopy | ||

| Esophagogastroduodenoscopy (EGD) | ||

| Barrett’s Esophagus Surveillance | ||

| Inflammatory Bowel Disease Surveillance | ||

| By End-User | Hospitals | |

| Ambulatory Surgery Centers (ASCs) | ||

| Specialty Gastroenterology Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the chromoendoscopy agents market?

The chromoendoscopy agents market size stands at USD 158.84 million in 2025.

How fast is global demand for chromoendoscopy dyes expected to grow?

Revenue is projected to rise at a 5.39% CAGR, taking the market to USD 206.51 million by 2030.

Which dye dominates clinical practice in colorectal screening?

Indigo Carmine maintains leadership with 36.44% share thanks to its strong contrast pooling properties.

Why are oral tablet formulations gaining attention?

EMA-approved Lumeblue tablets remove spraying steps, improve efficiency, and are driving an 8.37% CAGR for the oral segment.

Which region is expanding the quickest?

Asia-Pacific is the fastest-growing geography, forecast to post a 7.58% CAGR through 2030 on rising endoscopy volumes.

What limits wider adoption of traditional dye spraying?

Lack of dedicated reimbursement codes and competition from virtual chromoendoscopy temper use in some health systems.

Page last updated on: