Gas Chromatography Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

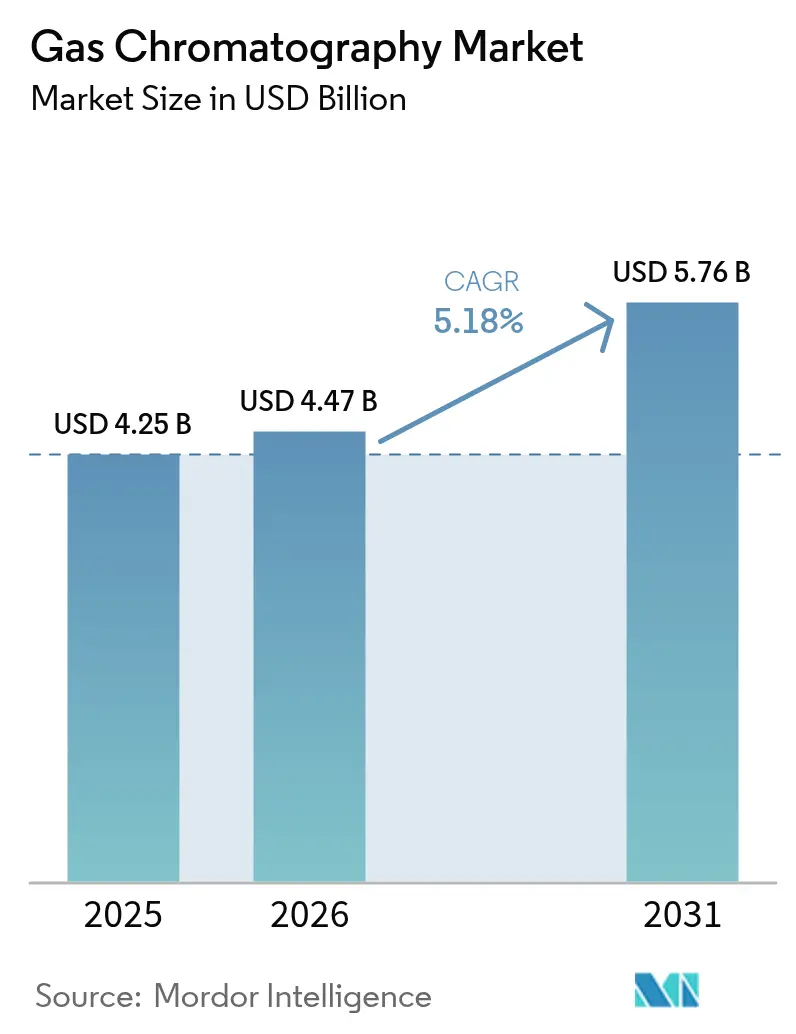

| Market Size (2026) | USD 4.47 Billion |

| Market Size (2031) | USD 5.76 Billion |

| Growth Rate (2026 - 2031) | 5.18% CAGR |

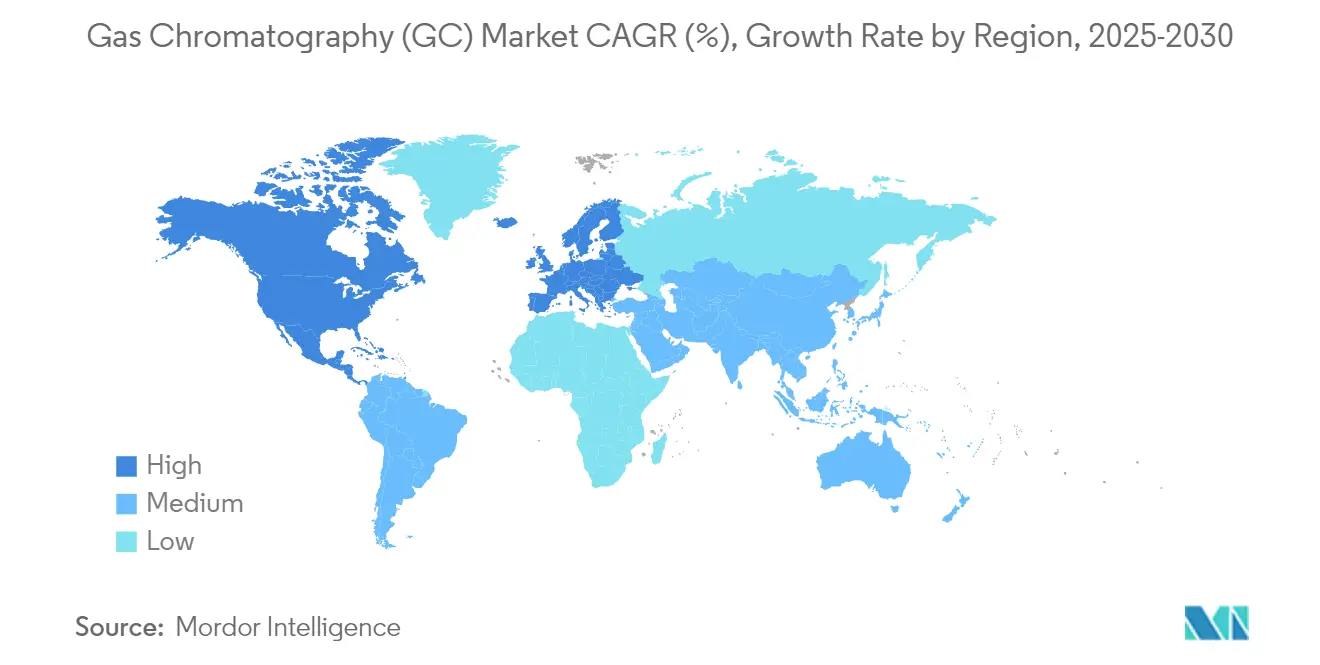

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

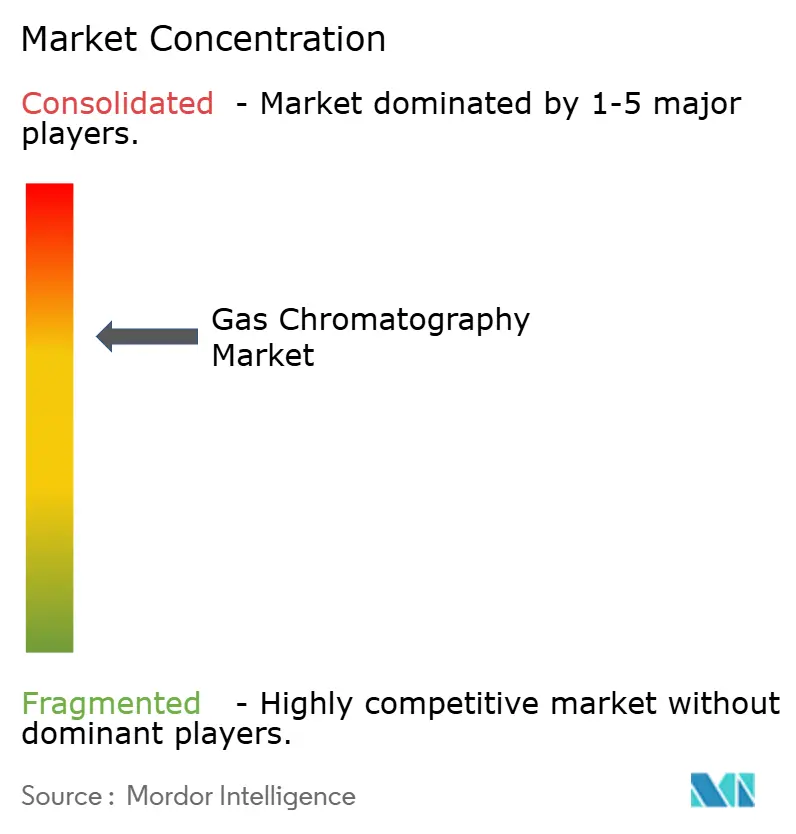

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gas Chromatography Market Analysis by Mordor Intelligence

Gas Chromatography Market size in 2026 is estimated at USD 4.47 billion, growing from 2025 value of USD 4.25 billion with 2031 projections showing USD 5.76 billion, growing at 5.18% CAGR over 2026-2031.

Heightened regulatory scrutiny in environmental and pharmaceutical testing, rapid technology upgrades such as hydrogen-ready systems, and proactive supply-chain strategies around carrier gases underpin this steady trajectory. Laboratories worldwide are moving from helium to hydrogen and nitrogen, trimming operating costs while reducing dependence on scarce noble gas supplies. Integrations with mass spectrometry now dominate capital‐spending agendas because they condense separation and identification into a single run, accelerating throughput and improving data integrity. Portable and micro-GC units are reshaping field analytics, and accessory innovations, particularly gas generators and low-phase-ratio capillary columns, signal that sustainable, autonomous operations will define competitive advantage through 2030.

Key Report Takeaways

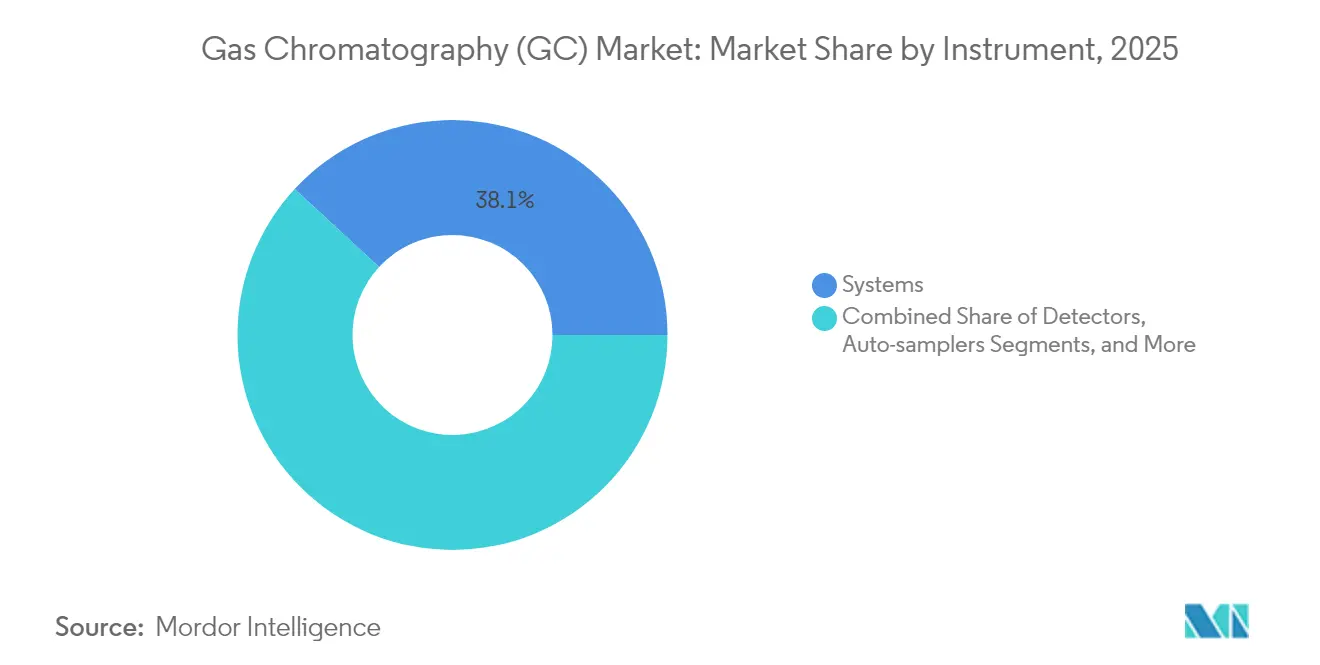

- By instrument type, systems led with 38.12% revenue share in 2025, while portable and micro-GC platforms are projected to grow at 9.25% CAGR through 2031.

- By accessories & consumables, columns commanded 45.88% of the gas chromatography market share in 2025, whereas gas generators are on track for an 8.28% CAGR to 2031.

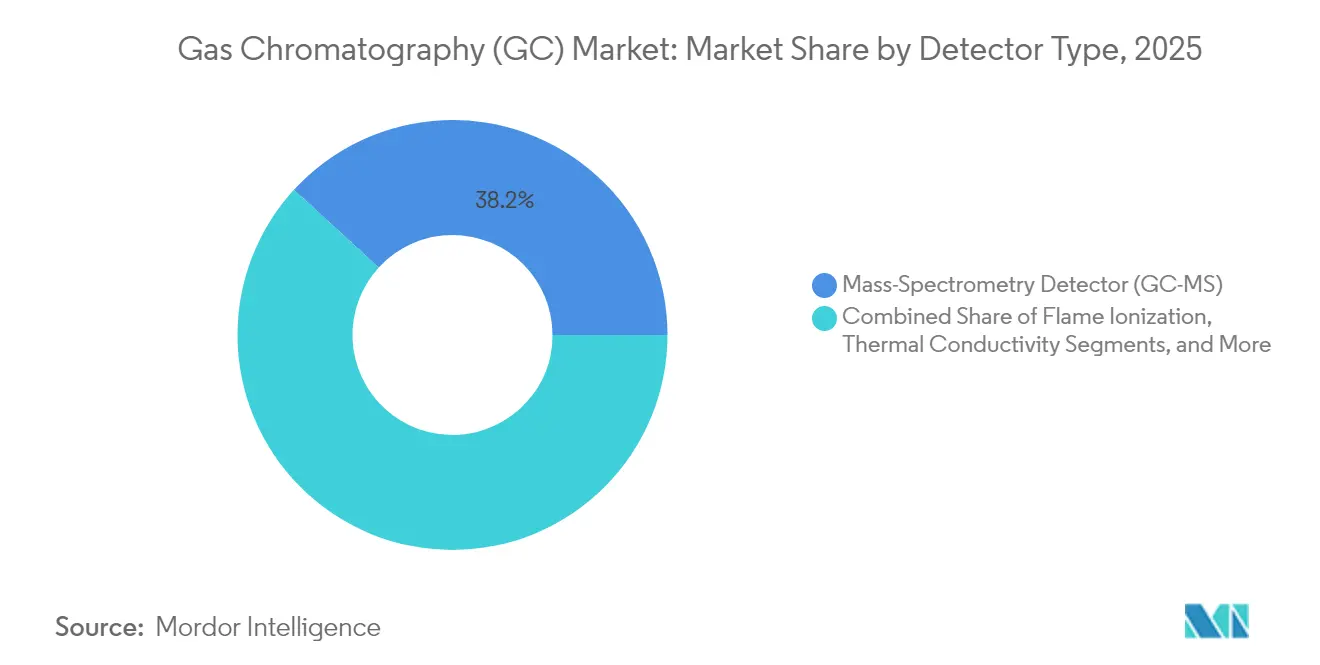

- By detector, flame ionization units accounted for 31.45% share of the gas chromatography market size in 2025, while mass spectrometry detectors are expanding at 9.84% CAGR through 2031.

- By end user, pharmaceutical and biotechnology companies each held 29.60% share in 2025; environmental agencies record the fastest-rising demand with a 8.97% CAGR.

- By geography, North America captured 35.98% of the gas chromatography market in 2025, whereas Asia Pacific is advancing at an 8.29% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Gas Chromatography Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of GC-MS workflows | +1.20% | Global, stronger in North America & Europe | Medium term (2–4 years) |

| Growing role of GC in drug-approval quality controls | +0.90% | Global, concentrated in pharmaceutical hubs | Long term (≥ 4 years) |

| Expansion of shale-gas & petrochemical analytics | +0.80% | North America, Middle East, Asia Pacific | Medium term (2–4 years) |

| Stringent air & water-quality regulations worldwide | +1.10% | Global, led by EU and North America | Long term (≥ 4 years) |

| Shift to hydrogen carrier gas amid global helium shortage | +0.70% | Global | Short term (≤ 2 years) |

| Surge in PFAS/micro-plastic monitoring requirements | +0.60% | North America, Europe, expanding Asia Pacific | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of GC-MS Workflows

Linking gas chromatography with mass spectrometry is now standard practice across regulated industries. Pharmaceutical pipelines rely on GC-MS for impurity profiling, and more than 80% of new-drug dossiers reference integrated chromatography data systems. Environmental agencies use GC-MS to detect contaminants at trace levels, and developments such as atmospheric pressure chemical ionization push sensitivity even further.[1]Journal of the American Society for Mass Spectrometry, “Advances in APCI-GC-MS,” jasms.org These combined capabilities shorten sample preparation steps, free analyst time, and meet regulators’ data-integrity demands, reinforcing the momentum of the gas chromatography market.

Growing Role of GC in Drug-Approval Quality Controls

Stringent process analytical technology guidance from the FDA mandates real-time monitoring, driving investment in rugged GC units that can run continuously on production floors.[2]U.S. Food & Drug Administration, “Process Analytical Technology Guidance,” fda.gov Two-dimensional GC and automated impurity quantitation address increasingly complex biologic formulations, while machine-learning algorithms accelerate peak identification, reinforcing GC’s role in fast-tracking approvals, across the gas chromatography market.

Expansion of Shale-Gas & Petrochemical Analytics

Unconventional energy production depends on real-time GC measurements of volatile organic compounds to comply with EPA emission rules.[3]U.S. Bureau of Labor Statistics, “Occupational Employment and Wage Statistics: Chemists and Materials Scientists,” bls.gov Emerging markets for synthetic aviation fuels and hydrogen blends require bespoke methods, prompting vendors to bundle microreactor add-ons and MEMS-based analyzers for at-line use, further expanding opportunities within the gas chromatography market.

Stringent Air & Water-Quality Regulations Worldwide

PFAS limits as low as 4 ng/L in U.S. drinking water oblige laboratories to attain parts-per-trillion detection performance. The European Union’s pesticide residue alerts similarly push demand for high-sensitivity GC systems, while mandatory gasoline-terminal monitoring drives continuous online GC deployments.

Restraints Impact Analysis of Gas Chromatography Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital expenditure for advanced GC platforms | -0.80% | Global, more pronounced in emerging markets | Short term (≤ 2 years) |

| Shortage of trained chromatographers | -0.60% | Global, acute in North America & Europe | Long term (≥ 4 years) |

| Supply-chain volatility for helium impacting uptime | -0.50% | Global, with higher impact in regions dependent on imported helium | Medium term (2-4 years) |

| Emission-control compliance costs for GC solvents | -0.30% | North America & Europe, expanding to Asia Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure for Advanced GC Platforms

Comprehensive two-dimensional GC-MS systems can top USD 500,000 per unit, and installation plus service contracts can add 30% to total spend. Smaller laboratories delay upgrades, yet leasing programs and shared-instrument initiatives are gaining momentum, softening the financial barrier and supporting broader access across the gas chromatography market.

Shortage of Trained Chromatographers

Testing labs employ 164,490 professionals in the United States, yet vacancies persist as veteran analysts retire faster than universities train replacements.[3] Vendors are responding with intuitive software, automated troubleshooting, and dedicated training centers that compress learning curves.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Gas Chromatography Market Segment Analysis

By Instrument Type:

Portable Systems Drive Field AnalyticsSystems remained the workhorse, contributing 38.12% to 2025 revenue. The gas chromatography market size for these benchtop units will continue to rise, propelled by replacement cycles and integrated detectors. Portable and micro-GC instruments, growing at 9.25% CAGR, meet on-site monitoring needs in emergency response, mining, and fuel distribution. Devices such as the FLIR Griffin G510 deliver laboratory-grade detection in rugged housing. Field deployability saves sample-handling time and supports real-time decision making. Laboratories also add auto-samplers to close skill gaps and standardize throughput, while fraction collectors carve niches in preparative workflows. Detector upgrades and MEMS-based innovations extend analytics to previously inaccessible environments, reinforcing the relevance of portable systems within the gas chromatography market.

A parallel trend is the miniaturization of high-performance modules: on-column heaters, micro-injectors, and rapid cooling designs shrink physical footprints while maintaining chromatographic resolution. The preference for hydrogen carrier gas aligns with portable power budgets and environmental objectives, reinforcing demand for hydrogen-ready micro-GCs. Continuous cost improvements suggest portable platforms will capture a growing slice of gas chromatography market share over the next five years.

By Accessories & Consumables:

Gas Generators Transform Supply ChainsColumns captured 45.88% of the 2025 spend, reflecting their status as consumables with predictable replacement intervals. Low-phase-ratio capillary innovations improve inertness and peak shape for volatile sulfur compounds. Gas generators, however, are racing ahead at an 8.28% CAGR as labs swap cylinders for on-demand hydrogen, nitrogen, and zero air. PEAK Scientific’s takeover of Noblegen extends capacity and global reach in this segment. Column accessories such as guard columns and high-purity connectors keep maintenance workflows efficient. Pressure regulators made from advanced alloys withstand hydrogen service, while RFID-enabled valves automate replacement alerts. Tubing refinements cut dead volume, sharpening peak symmetry and conserving gas. As sustainability priorities climb, premium consumables that reduce waste and extend instrument uptime earn price premiums, directly influencing the gas chromatography market.

By Detector Type:

Mass Spectrometry Dominates InnovationFlame ionization detectors still own 31.45% of detector revenue in 2025 because they are rugged, affordable, and universal for hydrocarbons. Mass spectrometry attachments expand to a 9.84% CAGR, converting existing GCs into hybrid separation-identification platforms. Thermo Fisher’s Stellar mass spectrometer underscores the priority on fast throughput for translational omics. Labs retire older electron-capture detectors in favor of MS or vacuum UV options such as Agilent’s LUMA for better sensitivity toward halogenated pollutants. Ion mobility add-ons further resolve isomers, an advantage for environmental forensics. Thermal conductivity and chemiluminescence detectors occupy specialist niches, but forward R&D dollars overwhelmingly favor selective, high-resolution MS technologies that lift analytical certainty and compliance confidence.

By End User:

Environmental Agencies Lead GrowthPharmaceutical and biotechnology companies account for 29.60% of current demand, reflecting legacy usage patterns. Environmental and wastewater authorities register the strongest expansion tempo at 8.97% CAGR. PFAS regulations, microplastic surveillance, and air toxics compliance require trace-level sensitivity that only GC-MS or GC-IMS systems can deliver. Food and beverage producers escalate pesticide testing, adopting QuEChERS extraction and GC-MS/MS to clear export inspections. Academic centers upgrade to handle multi-omics projects, while forensic and clinical labs introduce steroidomics and toxicology workflows. This diversification boosts resilience while pushing the gas chromatography market toward integrated service models such as instrument-as-a-service subscriptions.

Geography Analysis

North America Gas Chromatography Market

North America contributes 35.98% of global revenue in 2025, anchored by robust EPA mandates, strong pharmaceutical output, and a deep bench of analytically intensive industries. Thermo Fisher’s USD 2 billion domestic expansion plan asserts confidence in sustained equipment demand. The United States enforces PFAS drinking-water limits that require sub-parts-per-trillion detection, driving laboratory upgrades and new installations. Canada and Mexico supplement growth via petrochemical outputs and harmonized environmental protocols, ensuring replacement cycles stay active throughout the forecast window.

Europe Gas Chromatography Market

Europe maintains second-tier leadership through far-reaching environmental directives and stringent food-safety regulations. Union-wide pesticide residue controls and vigorous microplastic initiatives elevate demand for sensitive GC platforms, and hydrogen conversion incentives align with regional energy goals. Germany, the United Kingdom, and France dominate orders, while Italy and Spain grow through agricultural quality testing. The European market rewards low-power, hydrogen-optimized instruments and integrated data integrity modules that simplify compliance with GDPR and GMP provisions.

APAC Gas Chromatography Market

Asia Pacific records the fastest trajectory at 8.29% CAGR, driven by industrialization, rising pharmaceutical output, and progressive monitoring laws. China remains the largest contributor, though vendor sales fluctuated amid macroeconomic headwinds. Japan and India accelerate demand through clean-energy programs and API manufacturing scale-up. South Korea invests in high-tech industries requiring ultra-trace analytics, whereas Australia’s mining sector adopts portable GC units for site survey efficiency. Technology transfer, local production, and government funding schemes expand the addressable base, cementing the region’s role in future gas chromatography market growth.

MEA Gas Chromatography Market

Middle East and Africa register emerging momentum as petrochemical complexes modernize quality labs. GCC investments in refinery upgrades and hydrogen production translate into steady instrument orders, while South Africa’s mining and chemicals sectors rely on GC platforms for process control. Economic variance tempers short-term volumes, but regional alignment with international standards fosters gradual adoption.

South America Gas Chromatography Market

South America presents moderate yet stable expansion. Brazil’s pharmaceutical and petrochemical clusters anchor orders, and Argentine agribusiness drives pesticide residue testing. Regional trade pacts ease cross-border equipment movement, and Chilean copper operations integrate online GC systems for emission compliance. Currency swings and political shifts add volatility, but local distributors offset risk by offering financing and maintenance contracts.

Regulatory Landscape

Gas chromatography is closely tied to regulated quality and safety testing across pharmaceuticals, medical devices, environmental monitoring, and industrial compliance. In medical devices, the FDA recognition shift to ISO 18562-4:2024 (biocompatibility evaluation of breathing gas pathways) creates a key transition milestone, with declarations of conformity to the prior 2017 edition accepted only until July 05, 2026. For sterilized devices, ISO 10993-7 anchors residual ethylene oxide (EO) and related compounds testing, where headspace GC methods are used to support conformity assessments.

For regulated analytical procedures, global validation and data-integrity frameworks continue to standardize how GC and GC-MS results are generated, reviewed, and submitted. The EMA ICH Q2(R2) guideline codifies validation expectations for analytical procedures, including chromatography, with emphasis on specificity, accuracy, and precision for submissions. WHO GXP guidance for chromatography reinforces ALCOA+ data integrity principles, pushing laboratories toward compliant chromatography data systems, controlled audit trails, and standardized workflows that fit GMP and broader quality-system requirements.

Value Chain Analysis

The gas chromatography value chain covers R&D and application development, product design and quality or regulatory compliance, precision component sourcing, instrument manufacturing and assembly, distribution via direct sales and channel partners, and lifecycle services (installation qualification, preventive maintenance, method support, and training). R&D and compliance-driven activities contribute a large portion of value creation because platforms must meet regulated lab expectations for validation, data integrity, and uptime, while still supporting rapid method development for pharmaceuticals, environmental contaminants, and petrochemical analytics.

Upstream dependencies include specialized components (detectors, vacuum components for GC-MS, electronics, valves, and fittings), as well as consumables (columns, liners, septa) and carrier-gas infrastructure (cylinders or on-demand generators). Downstream, instrument OEMs (such as Agilent Technologies, Thermo Fisher Scientific, and Shimadzu) increasingly bundle recurring consumables and software with systems, while specialist suppliers (for example Restek and VICI) support method performance and maintenance cadence. As labs move away from helium toward hydrogen and nitrogen, gas generators and compatible regulators gain prominence in procurement decisions, and post-market services such as safety retrofits, method transfer support, and remote diagnostics become more central to maintaining laboratory uptime.

Competitive Landscape

The gas chromatography market is moderately fragmented. Established brands pursue differentiation via automation, carrier-gas flexibility, and vertically integrated service portfolios. Consolidation continues: PEAK Scientific’s acquisition of Noblegen fortifies its hydrogen and nitrogen generator range. Vendors bundle instruments with consumables and cloud software, creating recurring revenue and lock-in. Portable systems receive disproportionate R&D funding, while benchtop platforms gain features like AI-assisted troubleshooting and predictive maintenance dashboards. Companies that foreground sustainability, lower power draw, hydrogen compatibility, and recyclable consumables gain traction in procurement evaluations, especially within public-sector laboratories.

Tier-one suppliers expand factory footprints to protect supply chains. Thermo Fisher’s multiyear U.S. investment earmarks USD 500 million for R&D that spans environmental, life-science, and industrial domains. Shimadzu’s acquisition of microreactor IP strengthens green transformation credentials, targeting hydrogen and biofuel analytics. Waters inaugurated a Bangalore capability center to cultivate Asia Pacific innovation. These moves signal a strategic pivot toward regionalized manufacturing and distributed R&D.

Service differentiation now complements hardware excellence. Vendors roll out remote diagnostics, automated firmware updates, and subscription-based application support. Training academies mitigate the chromatographer shortage, while cross-platform method libraries ease carrier-gas conversion. Compliance-ready e-records and cybersecurity features appeal to pharmaceutical clients subject to data-integrity audits. Collectively, these initiatives shape a competitive mosaic where technological support and operational resilience define leadership as much as instrument specifications.

Gas Chromatography Industry Leaders

Agilent Technologies, Inc.

Thermo Fisher Scientific, Inc.

Danaher Corporation

Merck KgaA

PerkinElmer, Inc.

- *Disclaimer: Major Players sorted in no particular order

Gas Chromatography Market Companies Covered in this Report

- Agilent Technologies

- Shimadzu

- Thermo Fisher Scientific

- Danaher (Cytiva & Pall)

- PerkinElmer

- Merck

- Waters Corporation

- Teledyne Technologies

- Restek

- Chromatotec

- Scion Instruments

- Sartorius

- Air Liquide (Extended Life Sciences)

- Process Sensing Tech (LDetek)

- Hobre Instruments

- Phenomenex

- Bruker

- LECO

- Markes International

- Falcon Analytical

Market Opportunities and Future Outlook

Carrier-gas independence and operational sustainability point to practical whitespace across both new installations and instrument upgrades. Laboratories are converting methods from helium to hydrogen and nitrogen and expanding the use of gas generators, which matches the report’s focus on gas generators as a fast-growing accessory category. The same transition increases demand for hydrogen-ready consumables (columns, fittings, and regulators) that reduce leak risk and improve reproducibility. Vendor announcements also reflect this direction: Shimadzu introduced the Nexis GC-2060 with cylinder-free design elements, and Agilent launched the 8890B and 8860B GC systems with GC Assist for monitoring and troubleshooting to reduce unplanned downtime.

Regulated workflows remain a near-term driver for higher-sensitivity GC-MS and validated method packages in environmental and healthcare-adjacent testing. The report context cites U.S. drinking water PFAS limits as low as 4 ng/L, and broader air and water-quality enforcement continues to push laboratories toward integrated GC-MS and higher-resolution systems for trace contaminants and persistent organic pollutants. In medical devices, extractables and leachables (E&L) and sterilization-residual programs keep GC-MS usage high, including residual EO testing under ISO 10993-7 and related chemical characterization practices that are often supported by GC-MS, which supports demand for compliant data systems and turnkey application workflows that reduce analyst burden amid the chromatographer skills gap.

Recent Industry Developments in Gas Chromatography Market

- June 2026: Thermo Fisher Scientific introduced the Thermo Scientific Orbitrap Exploris GC S Mass Spectrometer, expanding high-resolution GC-MS capability for applications such as dioxins and persistent organic pollutants testing. The launch reinforces vendor investment in specialized, regulation-driven workflows where sensitivity and confident identification are procurement priorities.

- May 2026: Agilent Technologies launched the 8890B and 8860B gas chromatographs with GC Assist for system monitoring, automated troubleshooting, and remote connectivity. The update targets operational efficiency and data quality in routine laboratories, supporting broader adoption in environments facing uptime constraints and staffing gaps.

- June 2024: Waters published an application note detailing extractables analysis of nasal spray devices using gas chromatography and high-resolution mass spectrometry with soft ionization. The work highlights continued method development around medical device E&L programs, reinforcing demand for GC-MS workflows tied to safety and documentation requirements.

Gas Chromatography Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers revenues generated from gas chromatography hardware and the routine replacement items used to run GC workflows in laboratories. It includes core instruments, detector setups, autosampling components, and chromatography columns used for analytical separations.

Scope exclusions: service contracts, maintenance-only revenues, refurbished equipment sales, and general lab reagents that are not GC-specific are excluded.

Segments Covered in This Report

- By Instrument Type

- Systems

- Detectors

- Auto-samplers

- Fraction Collectors

- Micro & Portable GC

- Other Instruments

- By Accessories & Consumables

- Columns

- Column Accessories

- Pressure Regulators

- Gas Generators

- Fittings & Tubing

- Others

- By Detector Type

- Flame Ionization Detector (FID)

- Thermal Conductivity Detector (TCD)

- Electron Capture Detector (ECD)

- Mass-Spectrometry Detector (GC-MS)

- Others

- By End User

- Pharmaceutical & Biotechnology Companies

- Oil & Gas / Petrochemical Industry

- Environmental & Waste-water Agencies

- Food & Beverage Industry

- Academic & Government Research Institutes

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to map GC demand drivers and day-to-day usage patterns across regulated and industrial testing settings. We typically drew on public and official source types such as US FDA guidance and inspection focus areas, the US EPA methods library for environmental analytes, CDC laboratory guidance, and European Commission documents for food safety and chemical regulation, alongside ISO method references commonly used by laboratories.

To turn these signals into sizing inputs, we also reviewed company annual reports, product brochures, and investor presentations to understand instrument launch cycles and typical replacement behavior for GC columns and consumables. Patent databases were checked to identify detector and portable GC innovation themes, and an import-export shipment level database was used selectively to sanity-check trade flows for instrument categories in key hubs. These are illustrative sources only, and many other public documents and datasets were also used for collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and short surveys with instrument suppliers, channel partners, and end-user labs in pharma quality control, environmental testing, food testing, and oil and gas laboratories. We used these inputs to confirm what gets counted as GC revenue in practice, validate replacement timing for columns and other key consumables, and pressure-test regional demand patterns across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 14% | APAC: 49% |

| Mid tier: 51% | Functional/Unit leaders: 36% | EMEA: 29% |

| Smaller Players: 15% | Managers: 50% | Americas: 22% |

Market-Sizing & Forecasting

For sizing, we used a top-down approach, reconstructing lab testing intensity and installed-base replacement behavior into a revenue pool, then splitting totals into product classes that are commonly purchased together in GC workflows. Because GC demand is tied to routine testing, the model leaned on practical indicators such as regulated method adoption, sample throughput trends in food and environmental laboratories, pharma quality control capacity additions, and the mix shift toward micro and portable GC systems.

The output was then corroborated with selective bottom-up approximations, including sampled average selling prices for common instrument configurations, a reasonableness check on detector attachment rates, and channel feedback on annual column replacement volumes. Where direct visibility was weak, we used gap-handling rules that anchor smaller countries to proxy adoption levels based on lab density and regulatory testing needs, then adjusted using interview feedback. For forecasting, scenario analysis was applied around a base case using variables such as pharma manufacturing expansion, tightening of environmental monitoring, food safety testing intensity, and expected price progression for instruments and consumables, which were further screened through expert consensus.

Data Validation & Update Cycle

Validation was done through multi-step checks so that outliers were caught before finalization. We compared model outputs with independent signals, including reported direction of lab capital spending, observable changes in environmental and food testing enforcement, and trade movement for relevant instrument categories, and then reviewed any large jumps at region and product levels.

Before sign-off, the numbers and assumptions are reviewed by another analyst, and respondents are re-contacted when a key input moves beyond a reasonable range, such as detector mix shifts or unusually high consumables growth. Reports are refreshed annually, and interim updates are made when material events occur, after which a final pre-delivery pass is completed so clients receive the most current view available.

Mordor Intelligence's Gas Chromatography Market Estimate Compared With Other Published Estimates

Published numbers for gas chromatography can look different even when they describe the same broad industry, since the boundaries around instruments, detectors, and recurring consumables are not always applied in the same way. Differences also show up when the base year is not aligned, when currency timing is handled differently, or when growth is projected from a single CAGR assumption rather than linked to lab activity signals.

Reported GC demand signals such as detector attachment patterns, column replacement cadence, and regional lab testing intensity are the checks that keep Mordor Intelligence's estimate aligned to the portion of spending that is directly tied to GC workflows, rather than broader chromatography or general lab supplies. In other publications, the spread is often explained by counting only the instrument chassis, or by bundling adjacent categories like wider lab consumables and services, which can inflate the total even if the core unit volumes appear similar.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.47 B (2026) | |

| Global Consultancy A | USD 4.04 B (2024) | Uses an earlier base year and can weight instrument sales more heavily, with lighter treatment of recurring columns and GC-specific consumables, which pulls the total down versus a workflow-linked scope. |

| Industry Publisher B | USD 4.43 B (2025) | Includes a broader set of accessories and add-ons (such as gas generators and multiple accessory groups) under GC, and applies a longer forecast window, which can lift the counted revenue pool depending on category mapping. |

Taken together, the table shows that most of the gap is explained by scope mapping and base-year alignment, more than by any single demand driver. By keeping the counted revenues tied to identifiable GC purchase behavior and then cross-checking them against practical lab and trade signals, our sizing stays transparent and repeatable across regions and years.

Key Questions Answered in the Report

What is the current value of the gas chromatography market?

The market is valued at USD 4.47 billion in 2026 and is projected to reach USD 5.76 billion by 2031, growing at a 5.18% CAGR.

Which region holds the largest gas chromatography market share?

North America leads with 35.98% of global revenue in 2025 thanks to strict environmental and pharmaceutical regulations.

Why are laboratories shifting from helium to hydrogen carrier gas?

Global helium shortages elevate costs and supply risks, while hydrogen generators cut gas expenses and enable sustainable, high-speed separations.

Which detector technology is growing fastest?

Mass spectrometry detectors are expanding at 9.84% CAGR because they combine separation and identification, essential for trace-level regulatory testing.

What end-user segment shows the highest growth?

Environmental and wastewater agencies lead with a 8.97% CAGR due to new PFAS and microplastic monitoring mandates.

How are companies addressing the shortage of trained chromatographers?

Vendors offer intuitive software, automated troubleshooting tools, and dedicated training centers, reducing onboarding time for new analysts.

Page last updated on: