Trachoma Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

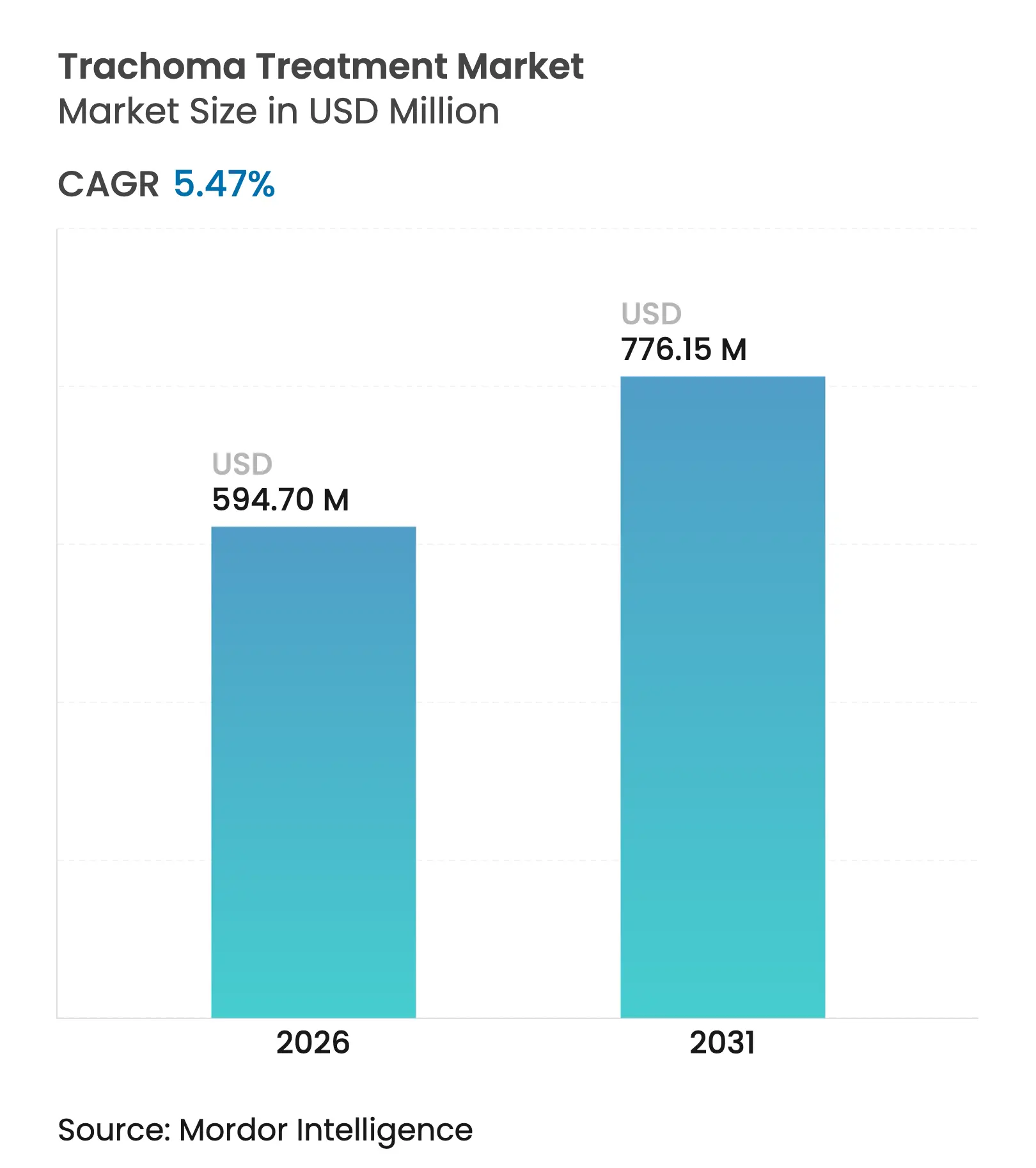

| Market Size (2026) | USD 594.7 Million |

| Market Size (2031) | USD 776.15 Million |

| Growth Rate (2026 - 2031) | 5.47 % CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Middle East and Africa |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Trachoma Treatment Market Analysis by Mordor Intelligence

Trachoma treatment market size in 2026 is estimated at USD 594.7 million, growing from 2025 value of USD 563.86 million with 2031 projections showing USD 776.15 million, growing at 5.47% CAGR over 2026-2031. This growth reflects the continuing global push toward the WHO SAFE 2030 elimination goals, stronger donor commitments, and deeper public-private coordination in endemic countries. Mass drug-administration (MDA) campaigns dominate demand patterns, underscored by Pfizer’s donation of more than 1 billion azithromycin doses through the International Trachoma Initiative (ITI). The trachoma treatment market is therefore expanding largely on the back of high-volume community treatments rather than price escalation. Therapeutic diversification is gathering pace as governments and NGOs hedge against macrolide resistance and seek formulations suited to fragile settings. At the same time, supply-chain vulnerabilities tied to active pharmaceutical ingredient (API) concentration in a handful of Chinese facilities continue to pose strategic risks that could slow market growth if geopolitical tensions disrupt manufacturing or logistics.

Key Report Takeaways

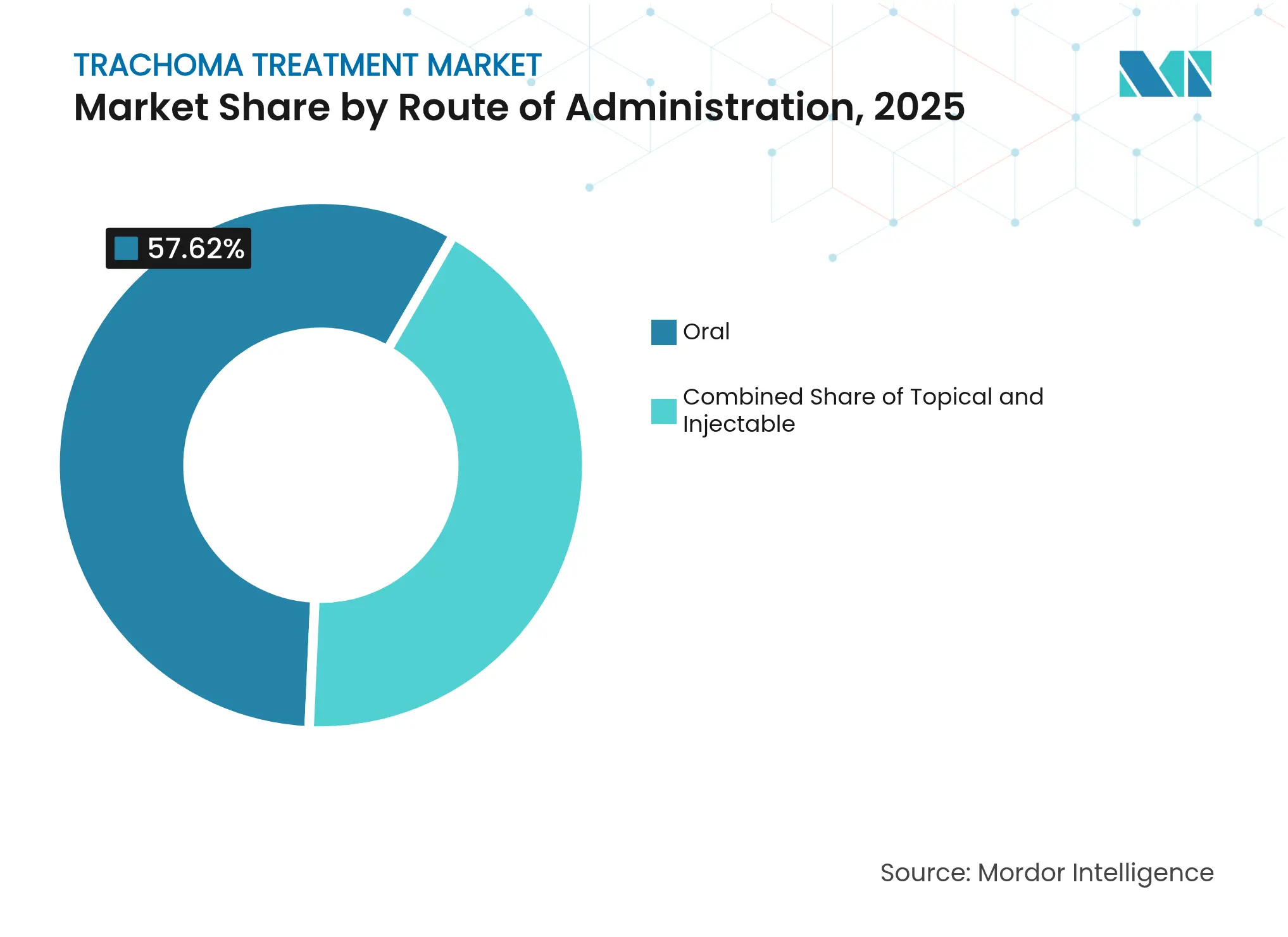

- By route of administration, oral formulations held 57.62% of trachoma treatment market share in 2025, whereas parenteral/injectable products are projected to post the fastest 5.92% CAGR through 2031.

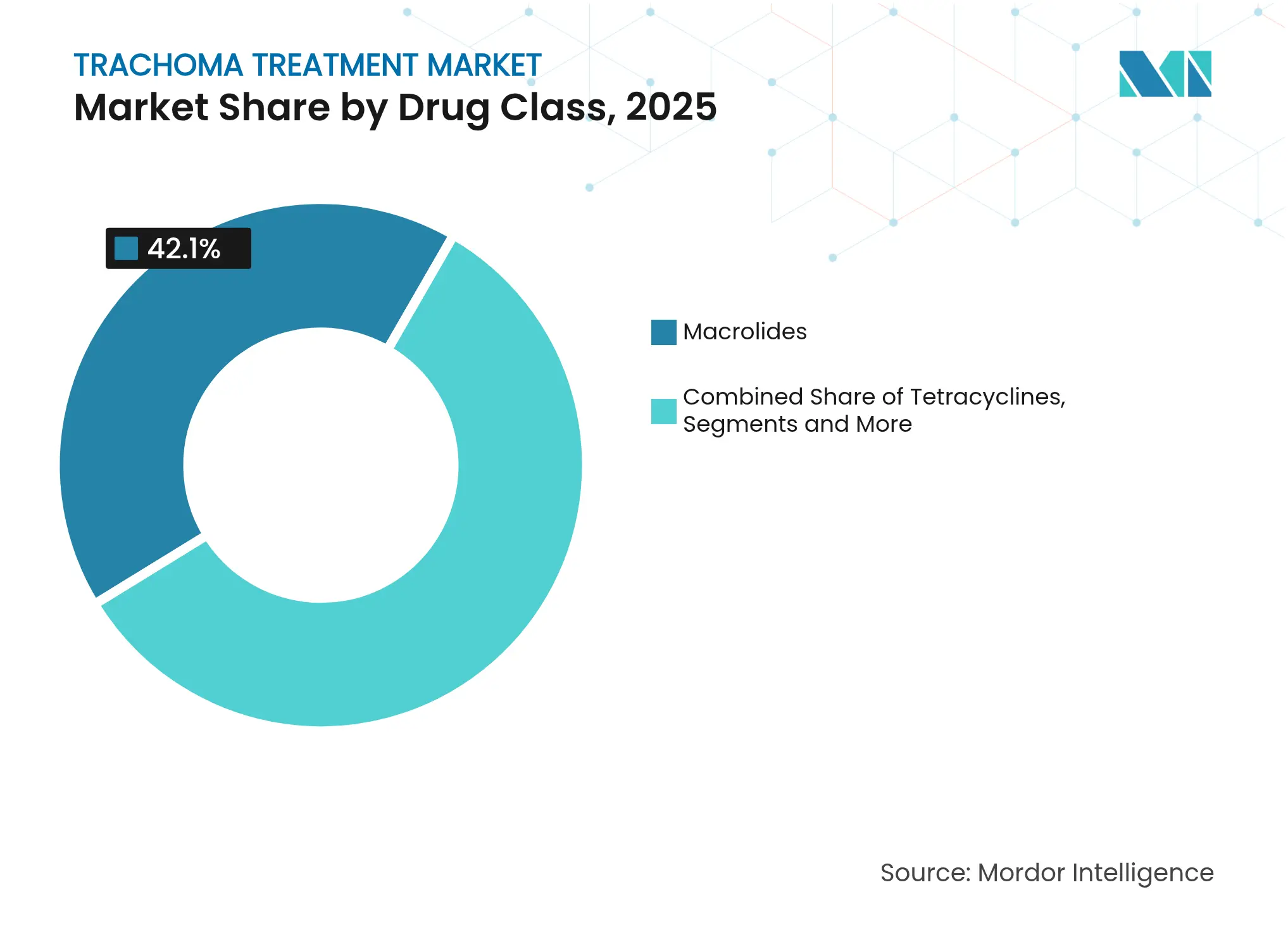

- By drug class, macrolides led with 42.10% revenue share in 2025, while fluoroquinolones are anticipated to record a 6.01% CAGR to 2031.

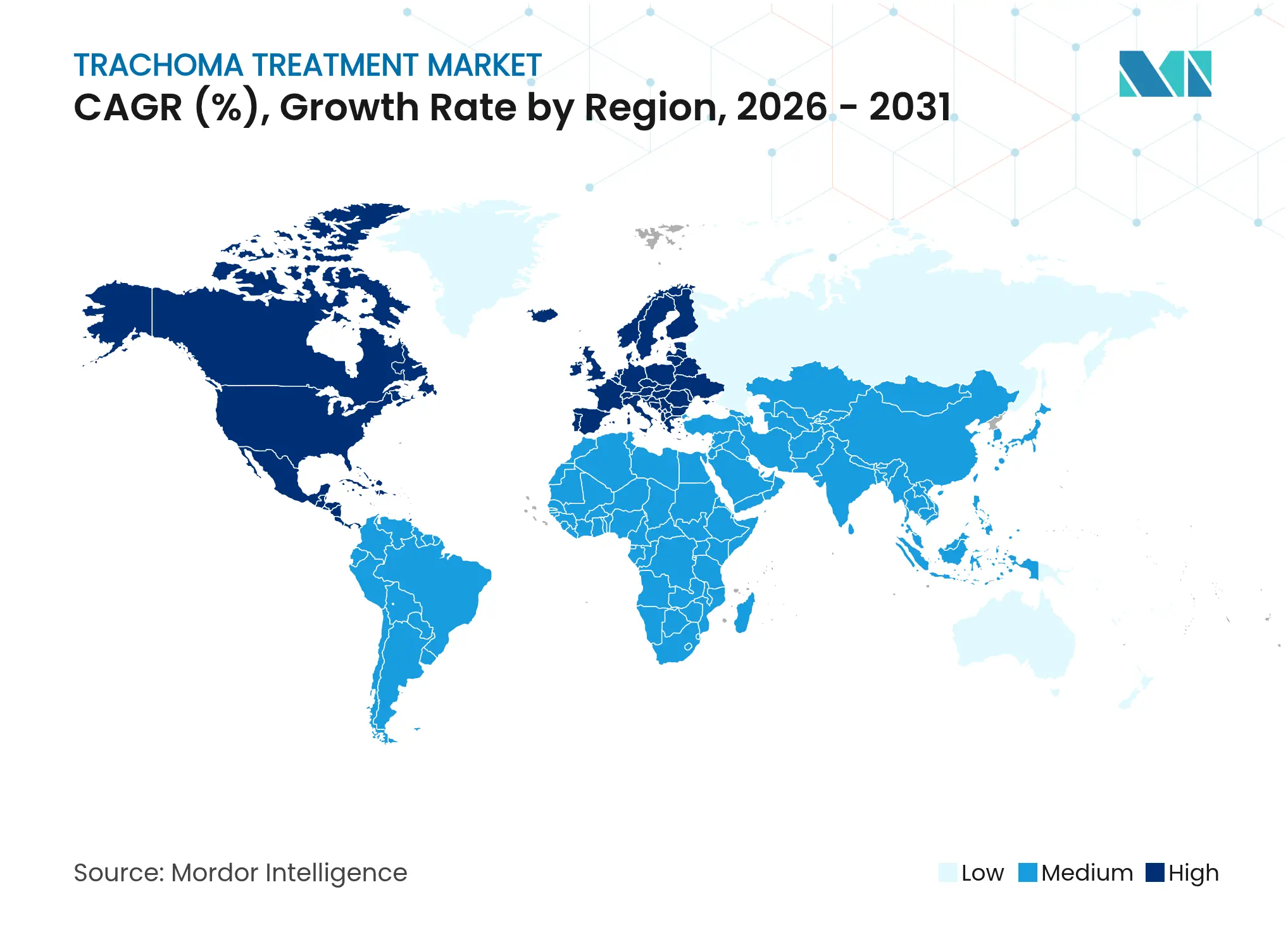

- By geography, North America commanded 41.60% share of the trachoma treatment market size in 2025, but Asia-Pacific is forecast to expand at a 6.22% CAGR over the same horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Trachoma Treatment Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising prevalence in endemic countries

Rising prevalence in endemic countries

| +1.2% | Sub-Saharan Africa, Central Asia | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+1.2%

|

Geographic Relevance

:

Sub-Saharan Africa, Central Asia

|

Impact Timeline

:

Medium term (2-4 years)

|

Expanded government-led mass drug-administration

programmes

Expanded government-led mass drug-administration

programmes

| +1.8% | Global, concentrated in Africa and Asia | Short term (≤ 2 years) | |||

WHO SAFE 2030 renewal targets

WHO SAFE 2030 renewal targets

| +1.1% | Global | Long term (≥ 4 years) | |||

Increasing NGO & donor funding for ophthalmic NTDs

Increasing NGO & donor funding for ophthalmic NTDs

| +0.9% | Low- and middle-income countries | Medium term (2-4 years) | |||

AI-enabled smartphone screening adoption

AI-enabled smartphone screening adoption

| +0.6% | Remote endemic areas globally | Long term (≥ 4 years) | |||

Micro-dose azithromycin R&D for children

Micro-dose azithromycin R&D for children

| +0.4% | High-burden pediatric settings | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Prevalence of Trachoma in Endemic Countries

Trachoma remains endemic in 40 countries and continues to affect mobile pastoral populations, conflict-exposed communities, and underserved rural districts, creating a persistent client base for therapeutics. The Global Trachoma Mapping Project reported 116 million residents in areas with active prevalence ≥5% as of 2023. Ethiopia illustrates the challenge: prevalence still reached 40.4% in parts of Oromia in 2024 despite six annual MDAs, and coverage in Goro district stood at only 75.8%, below WHO’s 80% threshold [1]PLOS Neglected Tropical Diseases, “To Eliminate Trachoma: Azithromycin Mass Drug Administration Coverage and Associated Factors,” PLOS.ORG . Such data underpin the steady uptake of trachoma treatment in established programmes while opening new demand in previously unmapped pockets. Climate-linked migration further complicates surveillance, pushing health agencies toward broader, more frequent distribution rounds that amplify drug volumes and safeguard elimination timelines.

Expanded Government-Led Mass Drug-Administration Programmes

National ministries of health are now integrating trachoma control fully into domestic budgets, moving past sole reliance on donated products and external implementing partners. Uganda cut its at-risk population from 10 million to below 300 000 by scaling government-financed MDA, bolstering procurement stability for suppliers. WHO prequalification has lowered regulatory barriers, exemplified by ACI’s azithromycin 500 mg approval in Bangladesh in 2025 for trachoma use, giving buyers confidence in local generics. This policy shift expands the trachoma treatment market by converting intermittent donations into predictable revenue-generating tenders, thus justifying manufacturing investments and raising local capacity for future demand spikes.

WHO SAFE 2030 Renewal Targets

Renewed milestones keep the trachoma treatment market on a clear, decade-long horizon that supports capital allocation for new production lines, pediatric formulations, and resilient supply routes. The 2025-2028 WHO action plan embeds regulatory-system strengthening and encourages domestic manufacturing in endemic countries, which is likely to diversify the supplier base. The extended deadline also syncs with key patent expirations, creating space for cost-competitive generics that can plug procurement gaps without undermining elimination objectives. This predictability fosters innovation in controlled-release ocular systems and low-dose regimens tailored to community campaigns.

Increasing NGO & Donor Funding for Ophthalmic NTDs

Donor consortia led by the Bill & Melinda Gates Foundation, USAID, the UK Foreign, Commonwealth & Development Office, and The END Fund collectively channel upward of USD 500 million each year toward neglected tropical disease programmes, with significant shares earmarked for trachoma. Their financing frameworks guarantee multi-year purchase orders that mitigate demand volatility and reduce credit risk for manufacturers. NGOs increasingly bundle trachoma drugs with wider NTD packages, unlocking economies of scale in production and shipping while sealing longer-term offtake deals for suppliers able to meet quality standards.

AI-Enabled Smartphone Screening Adoption

Computer-vision algorithms embedded in low-cost smartphones now allow community health workers to grade conjunctival photographs for signs of active disease within seconds, boosting case detection in remote villages with limited specialist coverage. Real-time geospatial analytics align drug shipments closely with emerging hotspots, cutting wastage from blanket distribution and lifting drug-use efficiency. The data generated also feed into national dashboards, helping ministries adjust MDA frequency and dose forecasting, ultimately creating a tighter fit between therapeutic supply and epidemiologic reality.

Micro-Dose Azithromycin R&D for Children

Height-based micro-dosing trials show improved pharmacokinetics and fewer gastrointestinal adverse events among infants, prompting formulation research targeting children under six months. Such products could yield premium pricing and extend macrolide utility by lowering total community exposure per MDA round. Manufacturers able to navigate pediatric-specific bioequivalence and palatability challenges are likely to enjoy first-mover advantages, particularly in regions where children comprise 35%-40% of the at-risk population.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Low community awareness in hyper-endemic pockets

Low community awareness in hyper-endemic pockets

| -0.8% | Remote rural areas in Africa and Asia | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

-0.8%

|

Geographic Relevance

:

Remote rural areas in Africa and Asia

|

Impact Timeline

:

Medium term (2-4 years)

|

Ocular & systemic side-effects driving non-adherence

Ocular & systemic side-effects driving non-adherence

| -0.6% | Global repeat-treatment districts | Short term (≤ 2 years) | |||

Emerging macrolide resistance in C. trachomatis

Emerging macrolide resistance in C. trachomatis

| -1.1% | Areas with prolonged MDA exposure | Long term (≥ 4 years) | |||

Conflict-linked supply-chain disruption in Sahel &

Yemen

Conflict-linked supply-chain disruption in Sahel &

Yemen

| -0.7% | Conflict-affected regions | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Low Community Awareness in Hyper-Endemic Pockets

Suspicion toward externally sourced medications persists in pastoral and nomadic groups, dampening MDA participation despite adequate supply. Ethnographic surveys in Ethiopia attribute sub-80% coverage to fear of side-effects and limited knowledge about trachoma transmission. Health teams must therefore allocate extra funds for social-mobilization efforts, prolonging campaign timelines and elevating per-capita distribution costs. Persistent gaps force repeat rounds that push demand higher in unit terms but create logistical fatigue and risk drug expiries when uptake lags.

Emerging Macrolide Resistance in C. trachomatis

The MORDOR trial and follow-up genomic analyses show rising macrolide resistance markers in settings with six or more consecutive annual MDAs, threatening to erode azithromycin’s efficacy. If first-line regimens falter, programs may pivot toward multi-dose tetracyclines or fluoroquinolones, complicating last-mile distribution and pushing costs up. Manufacturers face strategic uncertainty: expansion of azithromycin capacity carries risk, while rapid switchovers to alternative classes demand new supply chains and training materials almost overnight.

Segment Analysis

By Route of Administration: Oral Dominance Faces Injectable Innovation

Oral regimens control 57.62% of trachoma treatment market share in 2025 because single-dose azithromycin tablets or suspensions are easy to hand out during door-to-door campaigns without specialized infrastructure. The approach compresses operational costs, enabling health workers to treat an entire village in a single visit and sustain high compliance. However, the parenteral channel is tracking a 5.92% CAGR to 2031, underpinned by deployment in conflict zones where water scarcity, population displacement, and theft of oral medicines undermine the tablet model. Injectables allow clinicians in mobile clinics to administer precise doses in a controlled setting, although cold-chain requirements elevate expenses. Topical agents, while still niche, gain traction for postoperative prophylaxis in trichiasis surgery programs and for patients contraindicated for systemic macrolides. Recent advances such as semifluorinated alkane carriers have boosted conjunctival penetration by 30% compared with traditional oil-in-water suspensions, cutting dosage frequency and potentially improving adherence.

Longer term, controlled-release ocular inserts and nano-gel patches could redefine treatment paradigms. Pilot data indicate that biodegradable ocular discs delivering azithromycin over seven days achieve therapeutic tissue levels equal to a single oral gram, opening the possibility of one-time clinic-based interventions that bypass systemic exposure altogether. For suppliers, such novel devices unlock patent-protected revenue streams outside the crowded oral generics arena while dovetailing with surgical outreach campaigns. Over the next decade, these innovations are expected to carve out around 5% of the trachoma treatment market by value as they target settings with rising macrolide resistance or systemic side-effect concerns.

Note: Segment shares of all individual segments available upon report purchase

By Drug Class: Macrolides Lead Despite Resistance Concerns

Macrolides still led the segment with 42.10% share of the trachoma treatment market size in 2025 given their proven efficacy, single-dose convenience, and established donation pipelines. Pfizer’s ongoing commitment to donate Zithromax through 2030 stabilizes supply but dampens commercial opportunities for other players, especially in low-income contexts where free product can suppress paid volumes . Fluoroquinolones, led by moxifloxacin and gatifloxacin, are the fastest-growing class at 6.01% CAGR thanks to their efficacy against macrolide-resistant strains and favorable ocular penetration profiles. National guidelines in Ghana, Benin, and parts of Sudan now recommend fluoroquinolone eye drops for surgical prophylaxis, widening their use beyond back-up therapy.

Tetracyclines retain a stable niche in older community programmes that began before the advent of azithromycin donations. Their multi-day dosing demands higher health-worker time and often lower compliance, yet they remain vital where macrolide stock-outs occur or in pregnant women when erythromycin is contraindicated. Sulfonamides are largely legacy products but remain part of the WHO Essential Medicines List; periodic stock-outs of frontline agents keep limited demand alive, particularly in remote Amazonian and Melanesian pockets. Finally, ophthalmic anti-infectives that bundle antibiotic and anti-inflammatory action attract procurement interest during surgical camps, signalling cross-over demand that can lift overall sales volumes during intensive trichiasis correction drives.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific represents the most dynamic demand center, with trachoma treatment market growth projected at a 6.22% CAGR through 2031 as governments integrate trachoma into universal-health-coverage benefit packages and step up surveillance post-elimination validation . India’s 2024 validation prompted neighboring Nepal and Pakistan to scale pilot elimination zones, sparking procurement spikes for azithromycin and starter quantities of fluoroquinolones. Bangladesh’s ACI now feeds local and export needs after WHO prequalification, trimming freight times and insulating buyers from Red Sea shipping disruptions.

North America, driven almost entirely by Australia’s remote Aboriginal communities, held 41.60% of trachoma treatment market share in 2025. The Pharmaceutical Benefits Scheme enables premium pricing-sometimes 25% higher than UNICEF tender rates-creating outsized revenue relative to patient volumes. Canada and the United States have long been non-endemic, but procurement for humanitarian response teams, especially for Pacific Island deployments, still contributes a trickle of demand. Elsewhere, the Middle East & Africa cluster accounts for the bulk of tablets distributed each year, although lower procurement prices restrain revenue growth. Countries like Ghana reached elimination validation by 2025, yet ongoing surveillance campaigns continue to secure buffer stocks.

South America’s market remains small but strategically important for suppliers tapping Andean and Amazonian program budgets that favor locally warehoused inventory to avoid customs delays. Logistics challenges, including river-based transport and sporadic internet connectivity, create openings for distributors with deep rural reach; these intermediaries often package trachoma drugs alongside malaria and leishmaniasis portfolios, achieving route economies that lower per-dose delivery costs.

Competitive Landscape

Market Concentration

Global supply is moderately concentrated, with Pfizer, Teva, Abbott, Novartis Sandoz, Sun Pharma, and ACI dominating WHO-prequalified azithromycin volumes, while regional players fill in tetracycline and fluoroquinolone niches. Pfizer’s donations, channelled via the International Trachoma Initiative, dampen commercial demand yet maintain goodwill and brand visibility across 27 recipient countries. Generic entrants often win paid tenders when programs graduate from donation dependence; Bangladesh’s ACI landed export deals to Sudan and Papua New Guinea after securing prequalification status in 2025.

Technology differentiation is emerging as the next battleground. Novartis Sandoz is piloting QR-encoded blister packs that link into digital adherence platforms, while Teva co-develops AI triage apps with university partners to bundle drug supply with diagnostic license fees. Alcon’s approval of Tryptyr for dry-eye disease underscores a broader strategy of capturing surgical adjunct markets and could spill over into trachoma postoperative care. Meanwhile, biotech start-ups like Tarsus are advancing micro-dose ocular inserts aimed at pediatric segments, promising once-weekly applications that reduce systemic exposure.

Supply-chain resilience has become a corporate focal point. Leading API suppliers Zhejiang Huahai and HEC Group have faced heightened scrutiny following pandemic-related shipping bottlenecks, prompting buyers to diversify toward Indian and Bangladeshi intermediates. Regional fill-finish capacity expansion in Kenya and Nigeria is under discussion, with public-private partnerships crossing NTD and malaria verticals to justify shared sterile-injectables lines. Firms capable of aligning with these localization policies and meeting WHO GMP audits are poised to secure multi-year framework agreements.

Trachoma Treatment Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2023: AbbVie expanded its collaboration with Capsida Biotherapeutics to engineer AAV-based ocular gene therapies for diseases with high unmet need.

- January 2023: Pfizer and the International Trachoma Initiative celebrated donation of the one-billionth Zithromax dose under WHO’s SAFE strategy.

- January 2023: WHO issued a global call for greater investment in neglected tropical diseases, spotlighting trachoma as a priority.

Table of Contents for Trachoma Treatment Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Prevalence Of Trachoma In Endemic Countries

- 4.2.2Expanded Government‐Led Mass Drug Administration Programmes

- 4.2.3WHO SAFE 2030 Renewal Targets

- 4.2.4Increasing NGO & Donor Funding For Ophthalmic NTDS

- 4.2.5AI-Enabled Smartphone Screening Adoption

- 4.2.6Micro-Dose Azithromycin R&D For Children

- 4.3Market Restraints

- 4.3.1Low Community Awareness In Hyper-Endemic Pockets

- 4.3.2Ocular & Systemic Side-Effects Driving Non-Adherence

- 4.3.3Emerging Macrolide Resistance In C. Trachomatis

- 4.3.4Conflict-Linked Supply-Chain Disruption In Sahel & Yemen

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter’s Five Forces

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Buyers

- 4.7.3Bargaining Power of Suppliers

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD Mn)

- 5.1By Route of Administration

- 5.1.1Oral

- 5.1.2Topical

- 5.1.3Parenteral / Injectable

- 5.2By Drug Class

- 5.2.1Macrolides

- 5.2.2Tetracyclines

- 5.2.3Ophthalmic Anti-infectives

- 5.2.4Sulfonamides

- 5.2.5Fluoroquinolones

- 5.3By Geography

- 5.3.1North America

- 5.3.1.1United States

- 5.3.1.2Canada

- 5.3.1.3Mexico

- 5.3.2Europe

- 5.3.2.1Germany

- 5.3.2.2United Kingdom

- 5.3.2.3France

- 5.3.2.4Italy

- 5.3.2.5Spain

- 5.3.2.6Rest of Europe

- 5.3.3Asia-Pacific

- 5.3.3.1China

- 5.3.3.2Japan

- 5.3.3.3India

- 5.3.3.4Australia

- 5.3.3.5South Korea

- 5.3.3.6Rest of Asia-Pacific

- 5.3.4Middle East & Africa

- 5.3.4.1GCC

- 5.3.4.2South Africa

- 5.3.4.3Rest of Middle East & Africa

- 5.3.5South America

- 5.3.5.1Brazil

- 5.3.5.2Argentina

- 5.3.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market‐level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1AbbVie (Allergan)

- 6.3.2Pfizer

- 6.3.3Teva Pharmaceutical Industries

- 6.3.4Novartis (Sandoz)

- 6.3.5Merck & Co.

- 6.3.6Apotex

- 6.3.7Fresenius Kabi

- 6.3.8Azurity (Arbor)

- 6.3.9Sun Pharma

- 6.3.10Lupin

- 6.3.11Cipla

- 6.3.12Aurobindo Pharma

- 6.3.13Bausch + Lomb

- 6.3.14Viatris (Mylan)

- 6.3.15Johnson & Johnson Vision

- 6.3.16Takeda (Shire)

- 6.3.17GlaxoSmithKline

- 6.3.18Hikma Pharmaceuticals

- 6.3.19Dr. Reddy’s Laboratories

- 6.3.20Endo International

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Trachoma Treatment Market Report Scope

Trachoma is a bacterial infection and the leading cause of preventable blindness, according to the report. The treatment for this disease includes antibiotics and surgeries. The trachoma treatment market is segmented by route of administration (oral and topical), drug class (macrolides, tetracycline, ophthalmic anti-infectives, and sulfonamides), and geography (North America, Europe, Asia-Pacific, the Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers value (in millions of dollars) for the above segments.