Chromebook Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

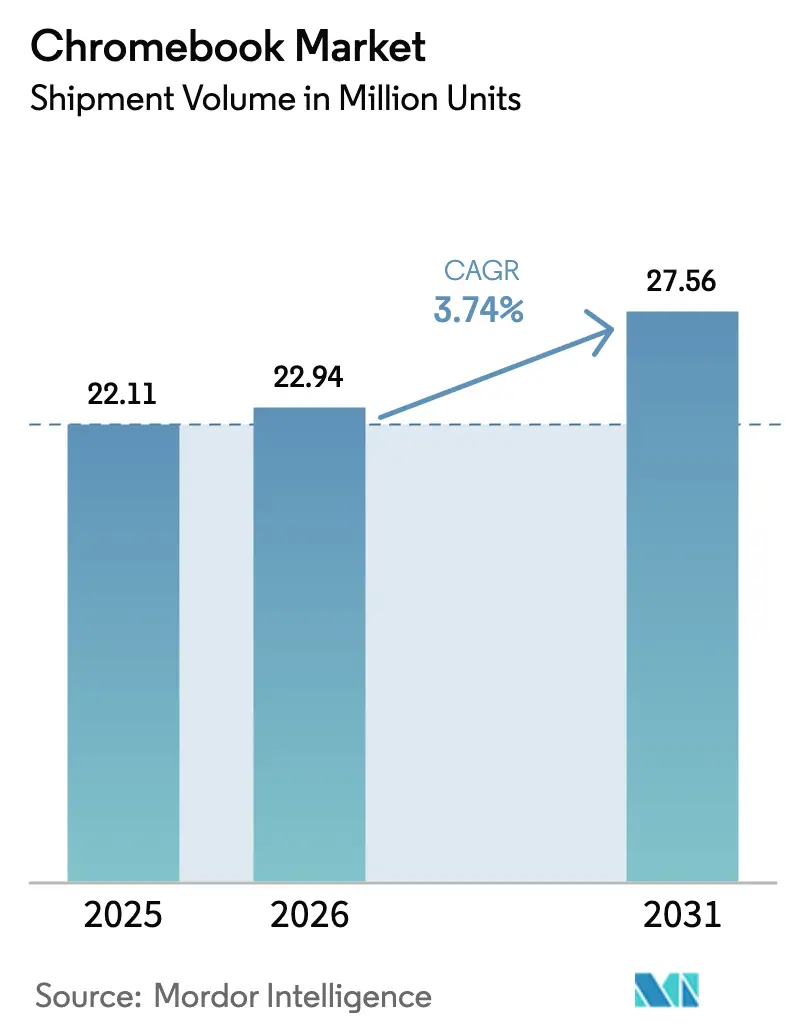

| Market Volume (2026) | 22.94 Million units |

| Market Volume (2031) | 27.56 Million units |

| Growth Rate (2026 - 2031) | 3.74% CAGR |

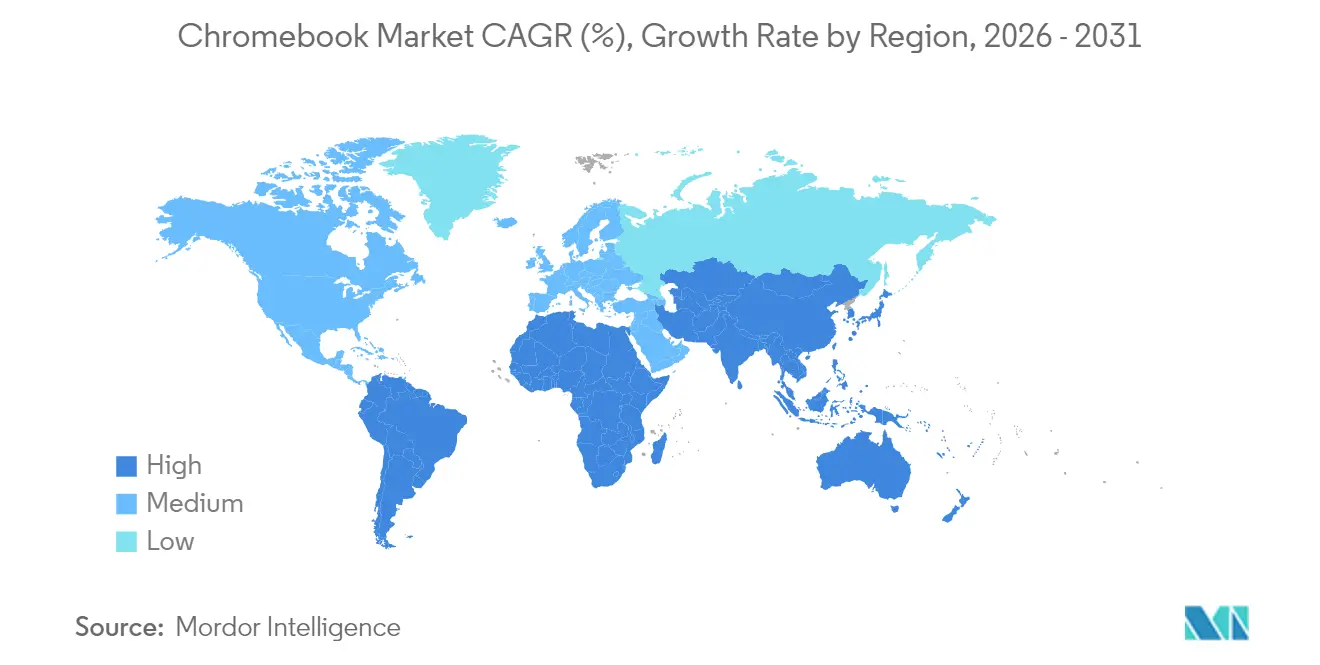

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chromebook Market Analysis by Mordor Intelligence

The chromebook market size was valued at 22.11 million units in 2025 and estimated to grow from 22.94 million units in 2026 to reach 27.56 million units by 2031, at a CAGR of 3.74% during the forecast period (2026-2031). Demand is normalizing after the pandemic-era surge, yet consistent device refresh cycles, expanding corporate pilots and widening geographic penetration keep volume on a steady uptrend. Supply-side innovation is equally supportive; tighter ChromeOS-Android convergence, on-device generative-AI and 3 nm ARM chipsets are reshaping value propositions and helping Chromebooks move beyond browser-centric workflows. At the same time, tariff-driven supply-chain realignment pushes vendors to diversify assembly into Mexico, Vietnam and India, adding resilience as well as regional cost advantages. Together, these forces underpin measured but dependable expansion for the chromebook market through the end of the decade.

Key Report Takeaways

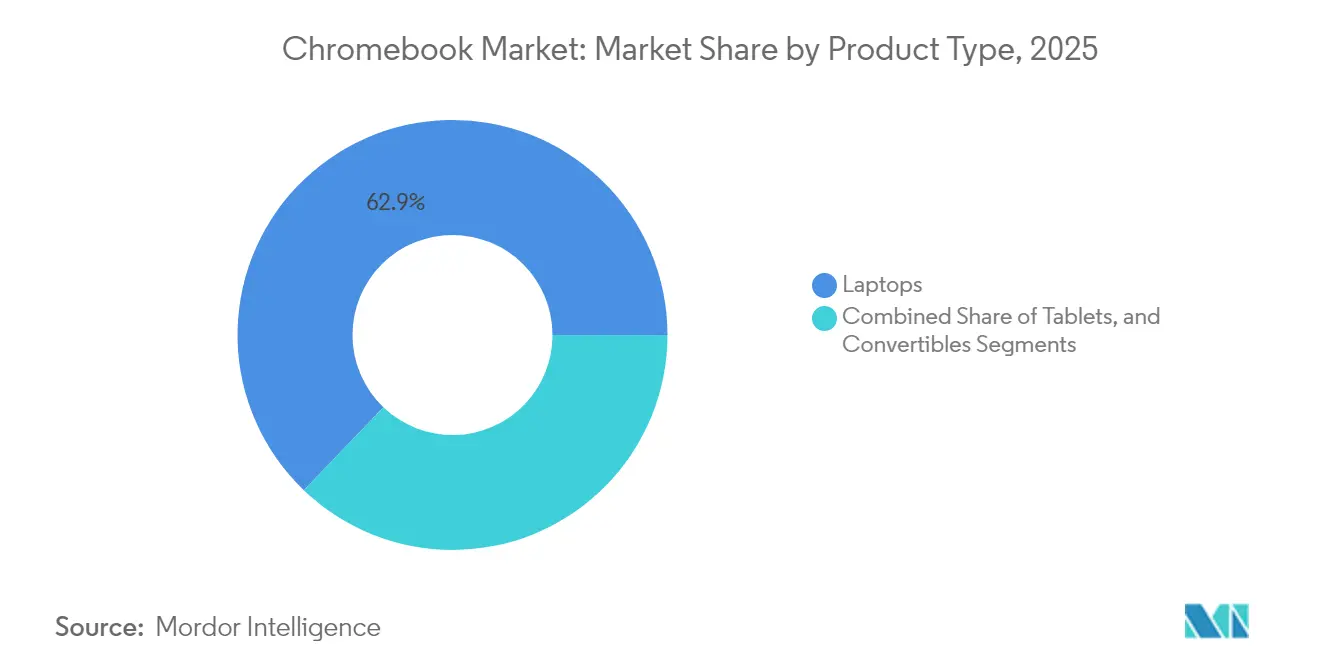

- By product type, laptops held 62.85% of chromebook market share in 2025, while tablets are projected to post the fastest 9.05% CAGR to 2031.

- By end-user, education commanded 57.70% of the chromebook market size in 2025; corporate deployments are set to grow the quickest at 7.75% CAGR.

- By processor architecture, x86 platforms accounted for 70.95% chromebook market share in 2025, although ARM solutions are forecast to expand at an 8.15% CAGR.

- By distribution channel, online retail captured 55.10% share of the chromebook market in 2025 and should advance at a 5.62% CAGR over the forecast horizon.

- By geography, North America led with 51.95% chromebook market share in 2025, whereas Asia-Pacific is on track for the fastest 4.55% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Chromebook Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| K-12 budget prioritisation for one-to-one computing | +1.2% | North America, India, Brazil | Medium term (2-4 years) |

| Lower total cost of ownership versus Windows/macOS | +0.8% | Global | Long term (≥ 4 years) |

| Remote and hybrid-work device refresh cycles | +0.6% | North America, EU, Asia-Pacific | Short term (≤ 2 years) |

| Hardware innovation – Chromebook Plus and AI features | +0.7% | Global | Medium term (2-4 years) |

| On-device generative-AI enabling offline productivity | +0.5% | Global | Long term (≥ 4 years) |

| Digital-inclusion programmes favouring ARM Chromebooks | +0.4% | Asia-Pacific, MEA, Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

K-12 budget prioritisation for one-to-one computing

Device programmes are moving from emergency procurement to sustainable refresh planning. In 2025, 93% of US districts intend to buy Chromebooks, up from 84% in 2023, and 68% now draw funds from local or state revenues rather than federal allocations. Comparable momentum is visible in Japan’s NEXT GIGA initiative and Brazil’s industrial digitalisation roadmap, both of which keep the chromebook market firmly embedded in national education agendas. Predictable multi-year funding streams underpin recurring orders, while repair-and-reuse ecosystems extend fleet life, creating a virtuous cycle of steady demand.

Lower total cost of ownership versus Windows/macOS

Enterprises measure Chromebooks against traditional PCs on help-desk visits, patch cadence and endpoint security. An Intel field study recorded 90% fewer hardware-related service calls for ChromeOS devices compared with legacy configurations. Google’s 10-year auto-update commitment, announced in 2024, further reduces lifecycle risk[1] Google LLC, “ChromeOS Extends 10-Year Automatic Updates,” blog.google. Cost benefits stretch beyond procurement: Cameyo-powered virtual app delivery cuts VDI spend by 54% relative to conventional solutions. Collectively, these savings help the chromebook market penetrate cost-sensitive enterprise and public-sector segments.

Remote and hybrid-work device refresh cycles

Commercial PC spending is shifting from ad-hoc pandemic buys to structured fleet modernisation. HP reported a 5% year-over-year rise in Personal Systems revenue to USD 9.2 billion in Q1 FY2025, linked partly to ChromeOS uptake in managed deployments. New Chromebook Plus models, equipped with Intel 12th Gen Core i3 or AMD Ryzen 3 CPUs and 8 GB RAM minimum, meet heavier multitasking needs yet stay under the USD 700 price ceiling favoured by procurement teams. Chrome Enterprise Core policy controls let IT crews administer mixed fleets from a single console, reinforcing the chromebook market’s relevance in hybrid organisations.

Hardware innovation – Chromebook Plus and AI features

Hardware roadmaps showcase rapid specification climbs. MediaTek’s Kompanio Ultra provides 50 TOPS of on-device AI and is fabbed on a 3 nm node, boosting battery life and thermals[2]MediaTek Inc., “Kompanio Ultra Processor Launches,” mediatek.com. Quick Insert keys and locally-run Gemini AI models deliver creative tools without persistent internet connections, addressing a longstanding offline-functionality gap. Partnerships with Samsung, Lenovo and Acer keep premium configurations below USD 700, widening appeal without eroding the value segment. As these advancements diffuse, they inject fresh growth into the chromebook market over the medium term.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| US education market nearing saturation post-COVID | -0.9% | North America | Short term (≤ 2 years) |

| Competition from low-cost Windows laptops and tablets | -0.7% | Global | Medium term (2-4 years) |

| Limited offline software ecosystem | -0.4% | Global | Long term (≥ 4 years) |

| Regulatory scrutiny of AUE / device lifespans | -0.3% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

US education market nearing saturation post-COVID

Many American districts now manage fleets purchased in 2020-2022 that are only mid-cycle. Automatic Update Expiration policies add replacement pressure, yet budget holders stretch refresh dates through repair programmes and used-device marketplaces. Tariffs of up to 125% on China-sourced laptops increase landed costs, forcing schools to weigh cybersecurity against fiscal limits. As a result, the chromebook market’s US education segment is slowing, shifting the growth spotlight to overseas schools and corporate rollouts.

Competition from low-cost Windows laptops and tablets

Microsoft’s Copilot+ PC blueprint, based on Qualcomm Snapdragon X, pushes sub-USD 600 AI-ready Windows devices into the same price band as Chromebook Plus. Local disruptors such as India’s Primebook also bundle 4G and Android apps at aggressive price points, intensifying choice for budget-conscious buyers. Meanwhile, iPad and Android tablets now support full office suites and detachable keyboards, eating into the convertible Chromebook niche. The chromebook market must therefore sustain a tight value proposition to fend off these rivals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Tablets Accelerate Despite Laptop Dominance

Laptop form factors accounted for 62.85% chromebook market share in 2025, confirming institutional trust in clamshell productivity. Still, tablet and 2-in-1 formats are forecast to register a 9.05% CAGR as touch-optimised curricula and field-service tasks gain prominence. The chromebook market size for tablets will broaden as Lenovo’s Duet line and Acer’s Tab 311 marry pen input with detachable keyboards. Early-grades classrooms favour rugged 10-inch tablets for handwriting exercises, while secondary schools keep laptops for coding and essay work. Enterprises test convertibles for sales teams that need whiteboard sketching yet plug into monitors at desks. Vendors thus keep fleshing out hinge mechanisms, stylus garages and MIL-STD durability to serve both extremes.

Wider gesture-based navigation in ChromeOS M124 makes tablets more fluid, narrowing the UX gap with iPadOS. MediaTek Kompanio 838 SOCs power fanless detachables that last a full school day without recharge, supporting districts that lack desk-level charging. On the consumer side, budget shoppers value Netflix HD playback and Android gaming on a single device, nudging household penetration. As the chromebook market expands, a stable tablet niche is now part of the long-term demand baseline rather than a fringe experiment.

By End-user: Corporate Adoption Challenges Education Dominance

Education remained the largest buyer with a 57.70% slice of the chromebook market size in 2025, but corporate workloads are scaling at an 7.75% CAGR through 2031. Financial services, logistics and contact-centre operators are piloting Chrome Enterprise Core to cut endpoint security incidents and license fees. HP’s Elite Dragonfly Chromebook, qualified for Intel vPro Enterprise, shows how premium builds can pass strict IT audits while still leveraging Google’s zero-trust model. SaaS-oriented firms now deploy mixed fleets where Chromebooks handle browser workflows and thin-client duties, freeing Windows laptops for heavy desktop apps.

Government usage is also climbing, especially where digital-sovereignty mandates highlight open-source components and cloud-managed security. In Latin America, state procurement agencies bundle Chromebooks with LMS platforms to deliver teacher training at scale. Consumers remain a smaller slice of the chromebook industry but upgrade interest is rising as AI-assisted writing and image tools reach entry-level SKUs. Overall, the end-user mix is becoming more balanced, cushioning the chromebook market against education cyclicality.

By Processor Architecture: ARM Gains Ground Against x86 Dominance

x86 chips still powered 70.95% of 2025 shipments, thanks to institutionally-validated Intel and AMD roadmaps. Yet ARM designs are moving faster, adding 8.15% CAGR on the back of 3 nm process nodes and integrated NPUs. MediaTek’s Kompanio Ultra tops 50 TOPS while sipping power, letting vendors offer thinner fanless designs that meet eight-hour classroom mandates. Qualcomm’s partnership portfolio is widening, and Google’s planned Android-ChromeOS merge leans on existing ARM optimisation. Together, these shifts will lift the ARM share of the chromebook market from niche to mainstream by decade-end.

OEM strategy is diversifying. Lenovo bids ARM for sub-USD 300 models in India, while Acer uses Intel vPro for enterprise SKUs. This bifurcation lets buyers choose between longevity and raw performance or cost and battery life. Software parity is narrowing as containerised Windows apps run sandboxed on ARM via Cameyo, easing migration barriers. Consequently, processor choice is becoming a deliberate TCO decision within the chromebook market rather than a compatibility compromise.

By Distribution Channel: Online Retail Dominates Institutional Shifts

Online stores captured 55.10% of 2025 unit sales and are growing at 5.62% CAGR, propelled by district-level bulk buys conducted through vendor portals. Direct-to-educator schemes streamline logistics, while corporate procurement exploits web-based configurators for rapid deployment. The chromebook market’s channel blend is evolving, yet value-added resellers retain mindshare where imaging services, warranty aggregation and financing remain critical. TD SYNNEX posted USD 4 billion in education revenue in fiscal 2022, highlighting the integrator role in bundling software and professional development.

Offline electronics chains still matter for walk-in consumers who want hands-on time before purchase, especially in emerging markets unfamiliar with ChromeOS. Hybrid channel models, where retailers fulfil stock but OEMs handle warranty registration online, smooth the buyer journey. Over time, continued e-commerce growth will push even large public tenders toward digital auction models, keeping the chromebook market’s distribution stack in flux.

Geography Analysis

North America kept a 51.95% stake in the chromebook market in 2025, although growth is flattening as school saturation sets in. Enterprise pilots, tariff-avoiding Mexico assembly lines and proactive ChromeOS Flex conversions now lead the regional story. Provincial Canadian boards remain expansion hotspots, adding bilingual content frameworks that rely on home-grown ChromeOS apps. Meanwhile, US districts are stretching fleet life via repair programmes rather than fresh buys, making the replacement business more cadence-driven than volume-spiking. Higher per-unit ASPs for Chromebook Plus and Dragonfly Enterprise help vendors preserve revenue even as absolute unit growth softens.

Asia-Pacific is the fastest climber at 4.55% CAGR, buoyed by India’s state tenders, Indonesia’s school digitisation push and Japan’s NEXT GIGA second-wave rollouts. Local brand competition is fierce; Primebook markets a 4G-enabled Android-compatible notebook under USD 250, pressuring global OEMs on value propositions. In Korea and Singapore, fibre penetration and government cloud services anchor demand for premium builds. Elsewhere, digital inclusion schemes funded by multilateral lenders bundle ARM Chromebooks with teacher training, raising baseline volumes and lifting the chromebook market across ASEAN and South Asia.

Europe delivers steady mid-single-digit growth as GDPR-minded enterprises turn to ChromeOS for sandboxed browsing. France sees consistent sell-through where Lenovo’s IdeaPad Slim 3 often tops Amazon charts. Post-Brexit customs checks prompt UK distributors to raise buffer stock, ensuring supply continuity for academy trust upgrades. Central-European governments allocate recovery funds to modernise classroom IT, inserting Chromebooks into tender lots alongside iPads. Across the region, sustainability legislation that targets repairability and extended lifecycles dovetails with Google’s 10-year update promise, reinforcing the chromebook market’s value claim.

Competitive Landscape

The chromebook market shows moderate concentration. HP, Lenovo and Dell lead on the back of global logistics, but emerging challengers are expanding the choice set. HP’s Personal Systems group posted USD 9.2 billion revenue in Q1 FY2025, underscoring scale benefits that translate into preferential component pricing [3]HP Inc., “Q1 FY2025 Results,” hp.com. Dell leverages its ProSupport suite to woo corporate converts, while Lenovo focuses on sub-USD 400 education SKUs in price-sensitive geographies. Their aggregated volume gives them leverage, yet value gaps are opening for newcomers.

Specialists are exploiting niches. Oregon-based CTL Corporation acquired ITAD provider 3R Technology to bundle lifecycle services with education sales. Framework Computer launched a USD 999 modular Chromebook that lets users replace ports, screens or keyboards in minutes, appealing to sustainability-driven institutions. These moves increase customer choice and pressure incumbents to add circular-economy features.

Platform convergence could scramble vendor rankings. Google’s forthcoming ChromeOS-Android merge will privilege manufacturers already fluent in smartphone design, potentially elevating Samsung and Asus in future cycles. Processor alliances add another vector; MediaTek’s Kompanio Ultra gives ARM-centric OEMs an edge in thin-and-light categories, while Intel’s vPro Enterprise keeps security-aware enterprises in the x86 fold. Overall, competition is pivoting from mere price to cohesive hardware-software-service packages, reshaping the chromebook market through 2030.

Chromebook Industry Leaders

HP Inc.

Dell Technologies Inc.

Lenovo Group Limited

Acer Inc.

Samsung Electronics Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: MediaTek unveiled the Kompanio Ultra processor delivering 50 TOPS AI performance on a 3 nm node, bringing flagship-class efficiency to ARM Chromebooks.

- January 2025: Acer introduced the Spin 512, Spin 511 and Chromebook 511 with MIL-STD 810H durability and Wi-Fi 7 for schools, starting at USD 429.99.

- January 2025: ASUS rolled out the next-generation Chromebook CR Series targeting education and SMB buyers, focusing on reinforced chassis and spill-resistant keyboards.

- October 2024: Google debuted Chromebook Plus models with Quick Insert keys and Gemini AI-powered Help Me Write, with Samsung Galaxy Chromebook Plus priced at USD 699 and Lenovo Duet at USD 340.

Global Chromebook Market Report Scope

A chromebook is a laptop that operates on Chrome OS, an operating system developed by Google. Unlike traditional laptops that typically run Windows or macOS, Chromebooks are designed primarily for internet-based activities and rely heavily on cloud computing.

The study tracks the revenue accrued through the sale of chromebook products by various players across the globe. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

The Chromebook market is segmented by product type (tablets, laptops, and convertibles), end-user(education, corporate, and others), and geography (North America, Europe, Asia Pacific, Middle East & Africa, and Latin America). The market sizes and forecasts regarding value (USD) for all the above segments are provided.

| Laptops |

| Tablets |

| Convertibles / 2-in-1 |

| Education |

| Corporate / Enterprise |

| Consumer |

| Government and Public Sector |

| x86 (Intel, AMD) |

| ARM (MediaTek, Qualcomm, etc.) |

| Institutional Contracts |

| Online Retail |

| Offline Retail |

| Value-Added Resellers / Systems Integrators |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Product Type | Laptops | ||

| Tablets | |||

| Convertibles / 2-in-1 | |||

| By End-user | Education | ||

| Corporate / Enterprise | |||

| Consumer | |||

| Government and Public Sector | |||

| By Processor Architecture | x86 (Intel, AMD) | ||

| ARM (MediaTek, Qualcomm, etc.) | |||

| By Distribution Channel | Institutional Contracts | ||

| Online Retail | |||

| Offline Retail | |||

| Value-Added Resellers / Systems Integrators | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the chromebook market?

Global shipments reached 22.94 million units in 2026 and are projected to rise to 27.56 million units by 2031.

Which end-user segment is growing fastest for Chromebooks?

Corporate deployments are advancing at 7.75% CAGR, outpacing education’s mature base.

How long will Chromebooks receive software updates?

Google guarantees automatic updates for 10 years from platform release, extending lifecycle value.

Are ARM-based Chromebooks becoming mainstream?

Yes, ARM devices are forecast to grow at 8.15% CAGR as 3 nm SOCs deliver high AI performance and long battery life.

Page last updated on: