Chlorella Ingredients Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

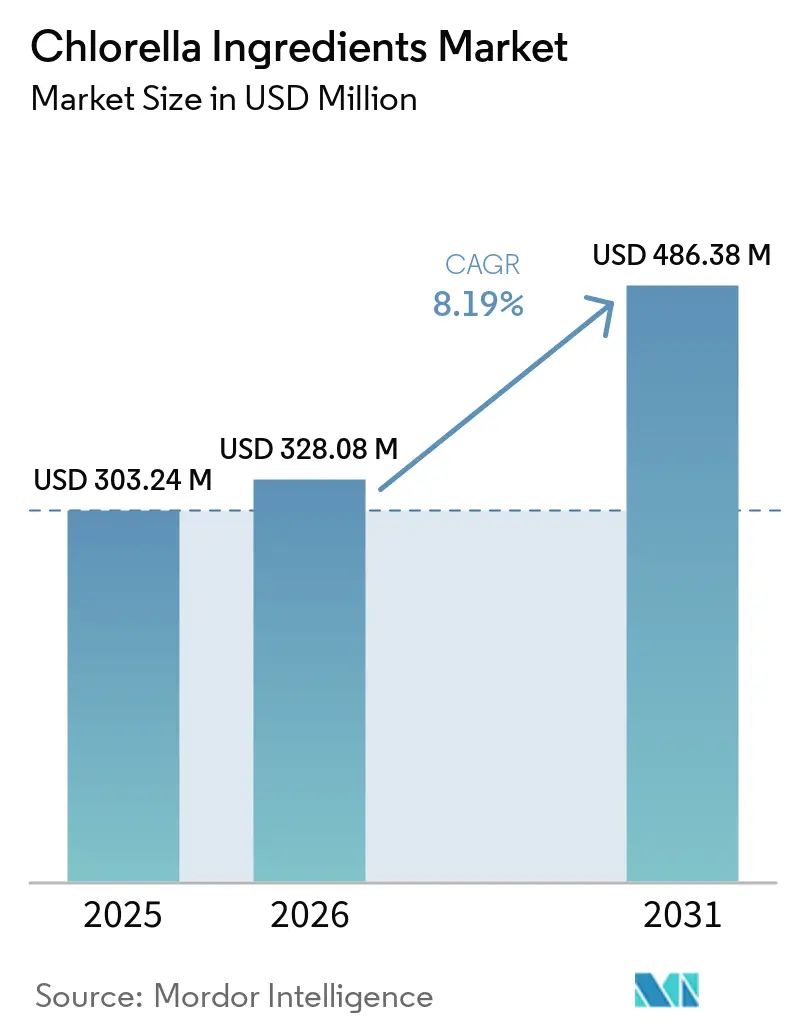

| Market Size (2026) | USD 328.08 Million |

| Market Size (2031) | USD 486.38 Million |

| Growth Rate (2026 - 2031) | 8.19% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Chlorella Ingredients Market Analysis by Mordor Intelligence

The chlorella ingredients market size in 2026 is estimated at USD 328.08 million, growing from 2025 value of USD 303.24 million with 2031 projections showing USD 486.38 million, growing at 8.19% CAGR over 2026-2031. The upward trajectory reflects consumer migration toward natural, sustainable nutrition, expanding use in personal care, and regulatory milestones such as the United States Food and Drug Administration’s (FDA) May 2025 approval of algae-based color additives. Intensifying clean-label commitments, maturation of vegan nutrition, and investments in cell-wall disruption technologies are unlocking new product formats and broadening application scope. Asia-Pacific anchors production scale, while North America and Europe accelerate premium demand, creating a balanced global growth profile for the chlorella ingredients market. Competitive focus has shifted toward vertical integration, quality certification, and advanced cultivation to overcome bioavailability barriers and capture emerging cosmetics demand. The chlorella ingredients market is moderately fragmented, allowing opportunities for both established producers and new technology-driven players. Long-standing Asian companies use their years of cultivation experience, unique strains, and knowledge of local regulations to ensure a steady supply.

Key Report Takeaways

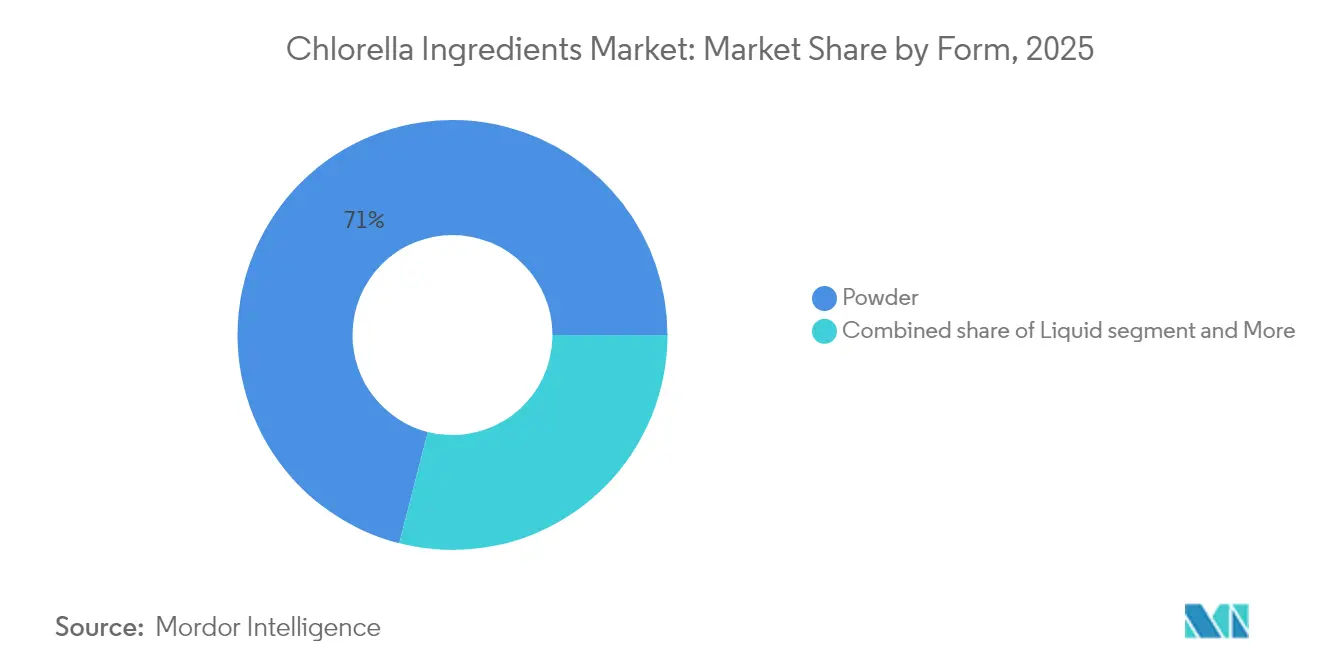

- By form, powder held 71.02% of the chlorella ingredients market share in 2025; liquid is forecast to expand at a 9.95% CAGR through 2031.

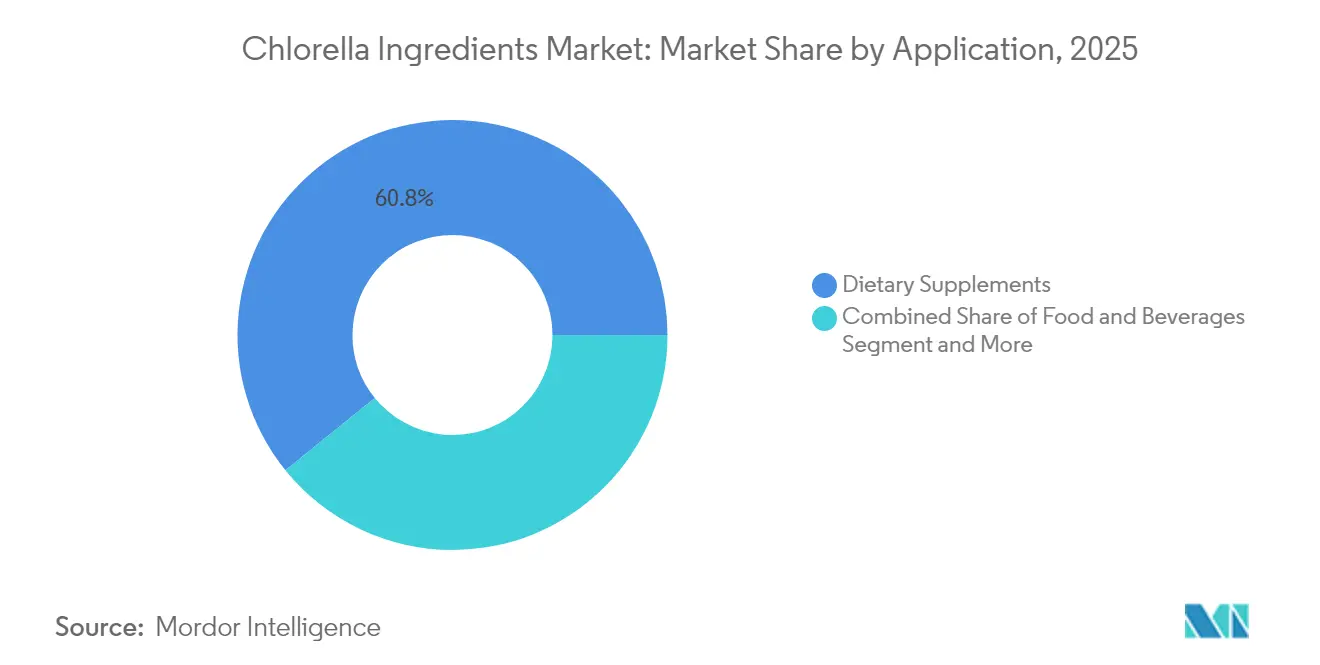

- By application, dietary supplements accounted for 60.83% of the chlorella ingredients market size in 2025, whereas cosmetics and personal care are advancing at a 9.92% CAGR between 2026-2031.

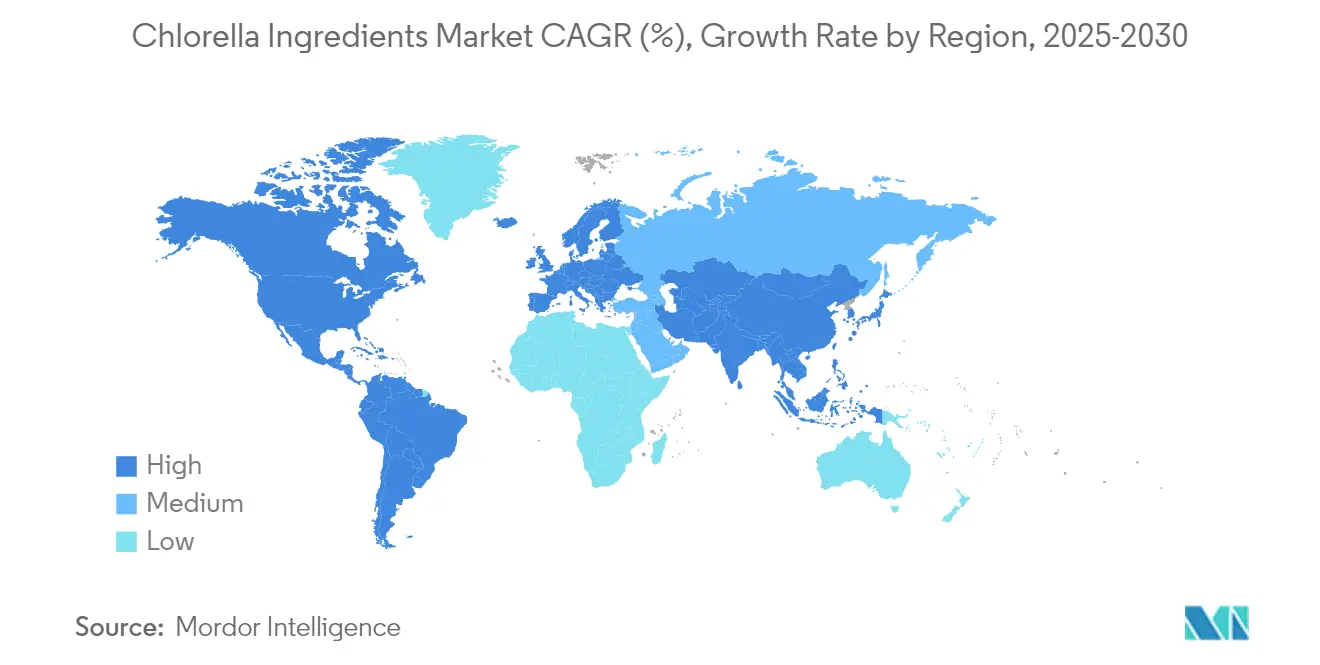

- By geography, Asia-Pacific led with 33.81% revenue share in 2025, while the Middle East and Africa region is projected to grow fastest at a 9.87% CAGR over the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Chlorella Ingredients Market Trends and Insights

Drivers Impact Table*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Clean-Label trend boosting demand for natural superfoods | 2.1% | Global, with strongest adoption in North America and Europe | Medium term (2-4 years) |

| Rising adoption of vegan and plant based nutrition | 1.8% | Global, led by North America, Europe, Asia-Pacific urban centers | Long term (≥ 4 years) |

| Growing popularity of algae-based functional ingredients | 1.5% | Asia-Pacific core, spill-over to North America and Europe | Medium term (2-4 years) |

| Expanding demand for chlorella based dietary supplements in preventive healthcare | 1.4% | Global, with early gains in Japan, Taiwan, North America | Long term (≥ 4 years) |

| technological advancement in cultivation and processing | 1.2% | Asia-Pacific production hubs, technology transfer to Middle East and Africa | Short term (≤ 2 years) |

| Demand for chlorella in cosmetics and personal care products due to antioxidant properties | 0.9% | North America and Europe premium markets, expanding to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising adoption of vegan and plant-based nutrition

The global chlorella ingredients market is growing steadily, driven by the increasing popularity of vegan and plant-based diets. In 2024, plant-based product sales experienced double-digit growth, reflecting a strong consumer shift toward healthier and more sustainable food options. According to The Food Institute, global plant-based retail sales reached USD 28.6 billion in 2024, marking a significant rise [1]Source: Food Institute, "Global Plant-Based Sales Reach $28.6 Billion," foodinstitute.com. This growth is largely influenced by younger, health-conscious individuals and flexitarians who are looking for complete plant-based protein sources. Countries like India (9%), Mexico (9%), Israel (5%), Canada (4.6%), and Ireland (4.1%) have some of the highest percentages of vegans, as reported by the World Population Review for 2025 [2]Source: World Population Review, "Veganism by Country 2025," worldpopulationreview.com. Chlorella powder, which contains 40–70% protein by dry weight and provides a full amino acid profile along with vitamin B12, is particularly appealing for addressing nutritional gaps in vegan diets.

Growing popularity of algae-based functional ingredients

The increasing demand for algae-based functional ingredients is driving the widespread use of microalgae like chlorella in various food products. Regulatory approvals, such as GRAS (Generally Recognized as Safe) status in both the EU and the US for several species, have helped microalgae move beyond niche supplements into mainstream food applications [3]Source: European Commission, "More than 20 algae species can now be sold as food or food supplements in the EU," ec.europa.eu. Recent advancements in extraction methods now allow for the preservation of bioactive compounds like lutein, chlorophyll, beta-glucans, and sulfated polysaccharides. These compounds provide health benefits such as antioxidant, anti-inflammatory, and immune system support. Chlorella ingredients are now being used in products like functional flours, dairy alternatives, and nutrient-rich seasoning blends. Food-tech companies are improving chlorella protein isolates and lipid-rich components through fermentation and enzymatic processes. These methods help reduce unwanted flavors and improve the overall taste and texture of products.

Clean-Label trend boosting demand for natural superfoods

The growing demand for natural and clean-label superfoods is boosting the popularity of chlorella as a versatile and visually appealing ingredient in various food categories, including beverages, baked goods, and dairy alternatives. Consumers are increasingly favoring natural, plant-based ingredients over synthetic additives, which positions chlorella as a premium choice. For example, in May 2025, the FDA approved the use of microalgae-based colorants in shades of blue, green, and yellow, which has encouraged food manufacturers to adopt these natural alternatives [4]Source: FDA Gov, "FDA Approves Three Food Colors from Natural Sources," fda.gov. This is particularly evident in the beverage industry, where major brands are replacing artificial dyes with natural alternatives. Chlorella derivatives, like chlorophyllin sodium-copper complex, are being used not only for their vibrant colors but also for their nutritional benefits, enhancing consumer trust and promoting transparency. Retailers are incorporating algae-based ingredients into their private-label products, making clean-label formulations a standard expectation in the market.

Expanding Demand for chlorella based dietary supplements in preventive healthcare

The increasing demand for chlorella dietary supplements is driven by its growing reputation as a natural, whole-food source of preventive nutrition backed by scientific research. In Japan, chlorella has been a staple in functional foods for years, thanks to its proven benefits in managing cholesterol levels, boosting immunity, and reducing oxidative stress, as supported by peer-reviewed studies. This success has inspired global supplement manufacturers to include chlorella in various forms, such as powders, extracts, and tablets, in their product offerings. These companies often highlight clinical research to support health claims about their products. In North America, the wellness trend that gained momentum after 2024 has further increased interest in natural health solutions, with consumers focusing more on immunity and minimally processed, whole-food-based supplements. In Europe and Australia, innovative formats like sachets combining chlorella with prebiotics or adaptogens are becoming popular for convenient, on-the-go wellness.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Regulatory complexity around algae ingredients | -1.3% | Global, particularly stringent in Europe and North America | Medium term (2-4 years) |

| Limited shelf life and storage requirements | -0.9% | Global, acute in tropical and humid regions | Short term (≤ 2 years) |

| Lack of standardized testing and certification bodies | -0.7% | Emerging markets, gradual harmonization in developed markets | Long term (≥ 4 years) |

| Poor solubility in water-based beverage | -0.6% | Global beverage applications, innovation-dependent resolution | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited shelf life and storage requirements

The chlorella ingredients market faces challenges due to the short shelf life and specific storage needs of chlorella powders. These powders are highly sensitive to factors like oxidation and moisture, which can lead to a decline in quality, including changes in color, taste, and nutrient content. For example, chlorophyll pigments may fade, and heat-sensitive nutrients like vitamin B12 can degrade over time. To preserve product quality, chlorella powders must be stored in cool, dry, and light-protected conditions, which increases packaging and transportation costs, especially in regions with hot or humid climates. Even with advanced packaging solutions like nitrogen-flushed barrier packs, most manufacturers, such as Sun Chlorella Corp., limit the shelf life to 24–36 months. This is significantly shorter compared to synthetic alternatives. These limitations make it difficult to use chlorella in products that require a long shelf life, such as emergency food supplies or military rations.

Regulatory complexity around algae ingredients

Regulatory complexity presents a significant restraint on the growth of the chlorella ingredients market, as varying global standards increase compliance burdens and slow time-to-market. In the U.S., the FDA’s proposed removal of self-affirmed GRAS status now mandates full dossier submissions and agency evaluations, giving an edge to established firms like Parry Nutraceuticals and Roquette Klötze, which already possess GRAS notifications. In the EU, chlorella products fall under novel food regulations, requiring extensive toxicological studies and stability data, with approval timelines often exceeding three years an especially high hurdle for smaller players and startups. Meanwhile, Japan implemented stricter Good Manufacturing Practice (GMP) requirements for supplements in June 2024, increasing operational oversight and the cost of compliance. Similarly, China updated its health food registration rules in October 2024, demanding more robust evidence for safety and efficacy, including origin traceability and functionality tests.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Powder Dominance and Liquid Momentum

Powder variants accounted for 71.02% of the chlorella ingredients market in 2025, buoyed by easier handling, compatibility with existing dry-mix lines, and competitive shipping economics. Spray-drying improvements that limit heat exposure help preserve chlorophyll integrity, ensuring vibrant color for bakery and confectionery use. Cost-effective packaging lines further entrench powder’s convenience for bulk customers. Liquid chlorella is demonstrating the highest 9.95% CAGR, driven by ready-to-drink and functional shot launches that benefit from enhanced bioavailability. Advances in aseptic filling and pH-neutral stabilization reduce microbial risk, broadening channel presence in chilled juice, smoothie, and sports drink aisles. Each format’s differentiated value proposition underscores how the chlorella ingredients market is evolving toward application-specific optimization rather than one-size-fits-all solutions.

To address challenges with beverage solubility, powder suppliers are investing in advanced milling techniques and agglomeration processes, which improve how well the powder dissolves in liquids. This has helped overcome previous limitations in using chlorella in clear drinks. Meanwhile, liquid chlorella producers are collaborating with flavor experts to mask its natural marine taste, making it more appealing to a broader audience. For both powder and liquid forms, the process of breaking down chlorella’s tough cell walls remains a critical factor in ensuring product quality. Manufacturers that achieve higher levels of cell-wall disruption are able to offer products with better nutrient availability, giving them a competitive edge.

By Application: Supplement Leadership and Cosmetics Acceleration

In 2025, dietary supplements made up 60.83% of the chlorella ingredients market size. This dominance is mainly due to strong consumer trust in these products, their straightforward regulatory approval, and the well-known health benefits of chlorella, such as boosting immunity and providing antioxidants. Capsules and tablets are particularly popular because they offer precise dosing and come in packaging that protects the quality of chlorella’s pigments. Additionally, powdered forms, like smoothie sachets and single-serve stick packs, are becoming increasingly popular among health-conscious and active individuals who prefer convenient and clean protein options that fit their busy lifestyles.

The cosmetics and personal care segment is projected to grow the fastest, with an expected CAGR of 9.92% through 2031. This rapid growth is driven by the rising use of chlorella in products like anti-aging serums, face masks, and sunscreen. Brands are leveraging chlorella’s rich nutrient profile to create high-quality skincare products. The growing trend toward eco-friendly beauty products allows companies to charge premium prices, while chlorella’s lower environmental impact compared to traditional plant-based ingredients appeals to environmentally conscious consumers. Functional food and beverage applications are also expanding, although the strong taste of chlorella remains a challenge for manufacturers.

Geography Analysis

Asia-Pacific led the chlorella ingredients market in 2025, contributing 33.81% of the total revenue. This dominance is driven by large-scale photobioreactor installations in countries like Japan, China, and Taiwan, where decades of experience in chlorella cultivation have resulted in advanced techniques and strong local consumer trust. In Japan, the Foods with Function Claims program provides a clear framework for promoting health benefits on product labels, which has significantly boosted the growth of dietary supplements. In China, producers are increasingly adopting fermentation methods to conserve freshwater and maximize production efficiency. Government nutrition policies and widespread consumer acceptance in the region ensure that Asia-Pacific remains a hub for innovation in the chlorella ingredients market.

North America presents significant opportunities for high-profit margins, driven by consumer demand for clean-label products and strong purchasing power. The upcoming FDA ruling in May 2025, which supports the use of microalgae as a color additive, is expected to encourage its adoption in mainstream food and beverage categories. This has already led to increased formulation trials by major beverage and confectionery brands. Retailers in the region emphasize transparency in supply chains, with many US buyers requiring detailed documentation and third-party audits to ensure product quality. Partnerships between ingredient manufacturers and consumer-packaged-goods companies, such as Brevel’s collaborations, highlight the importance of combining expertise across different segments to drive growth.

In Europe, although the market is heavily regulated, companies that meet compliance standards gain a competitive advantage and secure their position in the market. The region’s focus on sustainability aligns well with chlorella’s low-carbon footprint, allowing brands to position their products as premium and environmentally friendly. The Middle East and Africa region is experiencing the fastest growth, with a projected CAGR of 9.87%. This growth is fueled by rising disposable incomes, government initiatives to improve food security, and investments in controlled-environment agriculture. Collaborations with Gulf Cooperation Council importers help address logistical challenges, such as maintaining cold chains. In Latin America, the market is still in its early stages but shows potential, particularly in the growing functional beverage sectors in Brazil and Mexico.

Competitive Landscape

The chlorella ingredients market is moderately fragmented, providing opportunities for both established players and new entrants with advanced technologies. Leading companies like Sun Chlorella, Phycom BV, and Aliga Microalgae dominate the market, leveraging their years of expertise in cultivation and proprietary strains to maintain a steady supply. Asian companies, in particular, benefit from their long-standing experience and familiarity with local regulations. At the same time, innovative start-ups from regions like Israel, the United States, and the Netherlands are focusing on advanced fermentation techniques and photobioreactor designs to enhance production efficiency and nutrient quality.

Vertical integration is becoming a key strategy for companies in this market. By managing the entire process from cultivation to processing and final product formulation, companies can ensure better traceability and cost control. Many suppliers are also obtaining dual certifications, such as ISO 22000 for food safety, along with kosher, halal, and organic certifications, to expand their market reach. Additionally, companies are investing in intellectual property, particularly in areas like cell-lysis technology and high-purity pigment extraction, to create a competitive edge and protect their innovations.

Partnerships and collaborations are playing a significant role in driving market growth. Ingredient suppliers are working closely with beverage companies to address challenges like solubility, while cosmetics manufacturers are co-developing standardized extracts for products with anti-aging claims. The market is also witnessing increased merger and acquisition activity as larger companies look to establish a presence in high-growth segments. Regulatory compliance remains a critical factor for success, with companies holding certifications like FDA GRAS Notices, EFSA approvals, and Japanese FOSHU clearances gaining a competitive advantage.

Chlorella Ingredients Industry Leaders

-

Phycom BV

-

Sun Chlorella Corp

-

Aliga Microalgae

-

E.I.D. – Parry (India) Limited

-

Allmicroalgae Natural Products S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Algenuity has set up its European headquarters in Rotterdam, the Netherlands. The new facility in the Netherlands will enable the production of white Chlorella biomass, with an annual capacity of up to several thousand tons in dry weight.

- June 2024: Brevel, Ltd., a microalgae protein company, has inaugurated its inaugural commercial plant. Spanning an impressive 27,000 square feet (2,500 square meters), the new facility is poised to churn out hundreds of tons of microalgae protein powder, catering to the booming global alternative protein market.

- April 2024: Paris-based Edonia raised EUR 2 million in funding to focus on creating plant-based ingredients derived from microalgae, such as chlorella and spirulina. These ingredients are expected to cater to the growing demand for sustainable and innovative food solutions in various industries.

Global Chlorella Ingredients Market Report Scope

Chlorella belongs to Chlorophyta and chlorophyll division, whose shape is spherical. It is a kind of algae that is consumed as a superfood. The chlorella ingredients market is segmented by Application, Food and Beverages, Animal Feed, and Dietary Supplements. By Geography, the market is segmented into North America, Europe, Asia-Pacific, Rest of the world. The report offers market size and forecasts in value (USD million) for the above segments.

| Powder |

| Liquid |

| Others |

| Dietary Supplements |

| Food and Beverages |

| Animal Feed |

| Cosmetics and Personal Care |

| Pharmaceutical |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Rest of Asia Pacific | |

| South America | |

| Middle East and Africa |

| By Form | Powder | |

| Liquid | ||

| Others | ||

| By Application | Dietary Supplements | |

| Food and Beverages | ||

| Animal Feed | ||

| Cosmetics and Personal Care | ||

| Pharmaceutical | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Rest of Asia Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the chlorella ingredients market?

The market is worth USD 328.08 million in 2026 and is expected to grow at an 8.19% CAGR to 2031.

Which form holds the largest chlorella ingredients market share?

Powder leads with 71.02% share in 2025 because of its processing flexibility and long shelf stability.

Which application is growing fastest?

Cosmetics and personal care products are advancing at a 9.92% CAGR due to demand for natural anti-aging ingredients.

How fast is the Middle East and Africa chlorella ingredients market expected to grow?

The region shows the highest regional CAGR at 9.87% for 2026-2031, driven by rising health awareness and new biotechnology investments.

Page last updated on: