China Table Grapes Market Size and Share

China Table Grapes Market Analysis by Mordor Intelligence

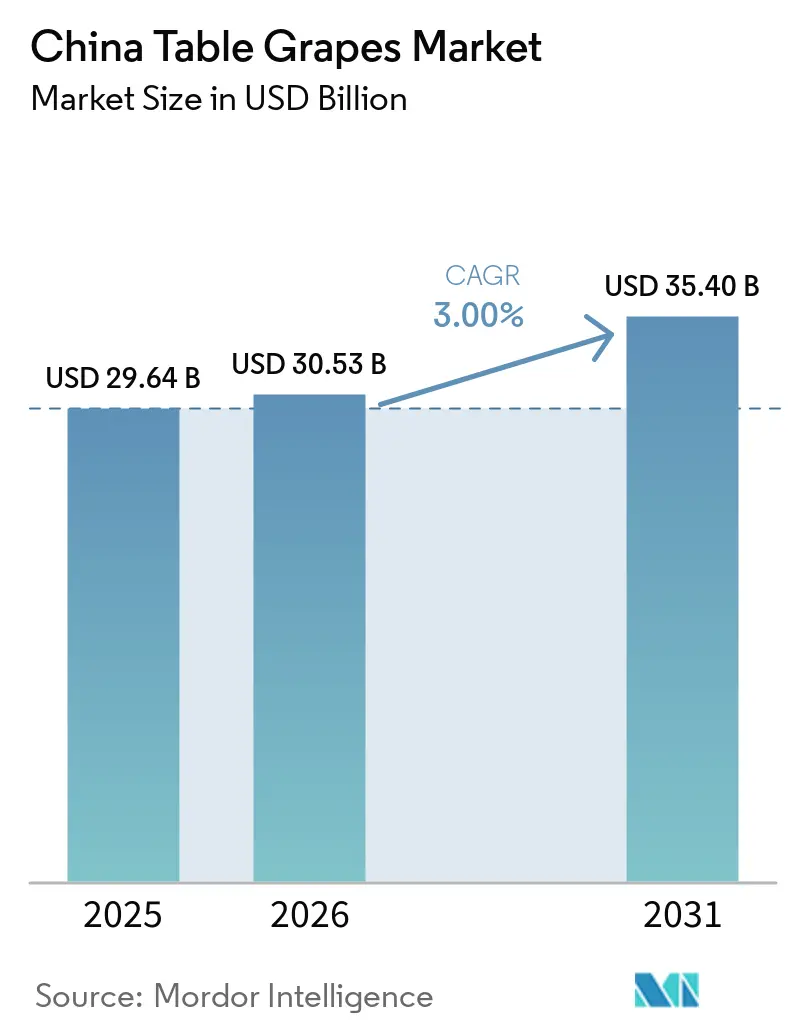

The China table grapes market size is projected to grow from USD 29.64 billion in 2025 to USD 30.53 billion in 2026 and USD 35.40 billion by 2031, with a CAGR of 3.0% from 2026 to 2031. Policy incentives for protected cultivation, improved cold-chain logistics, and focused export strategies are transforming supply chains and enabling China’s transition from a net importer to a regional export leader. Government-supported greenhouse subsidies are extending the harvest season, while the licensing of proprietary seedless cultivars is enhancing grower profitability and improving shelf life. Social-commerce platforms are reducing farm-gate-to-retail margins, increasing producer incomes, and boosting product visibility among urban consumers. Additionally, campaigns promoting chronic-disease prevention are encouraging fruit-based diets, driving demand for premium products in Tier 1 and Tier 2 cities.

Key Report Takeaways

- China's grape industry benefits from diverse regional climates, including Xinjiang's high-quality production, Yunnan's year-round supply, and the Coastal regions' export efficiency, enabling it to sustain its position as a leading global producer and trader.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China contributes to a system defined not by any single country or region but by the interaction of many. The global table grape market data by Mordor Intelligence represents that combined structure.

China Table Grapes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Favorable government incentives for protected cultivation | +0.6% | National, early gains in Xinjiang, Yunnan, and Shaanxi | Medium term (2-4 years) |

| Rising disposable income and premium-fruit spending | +0.5% | National, Tier 1 and Tier 2 cities | Long term (≥ 4 years) |

| Heightened health and wellness awareness | +0.4% | National, urban clusters | Long term (≥ 4 years) |

| Expansion of cold-chain logistics nationwide | +0.5% | National, central and western provinces | Medium term (2-4 years) |

| Licensing of proprietary premium grape varieties | +0.3% | National, strongest in Yunnan, Guangxi, and coastal provinces | Medium term (2-4 years) |

| Live-stream and social-commerce channels boosting farmer margins | +0.4% | National, rural e-commerce hubs in Yunnan, Shandong, and Fujian | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Favorable Government Incentives for Protected Cultivation

Government-supported investments in irrigation and modern farming infrastructure are enhancing protected cultivation practices in China’s table grapes market. In the key grape-producing region of Turpan in Xinjiang, authorities allocated ¥958 million (USD 134 million) in 2025 to develop grid infrastructure, facilitating water-saving irrigation across 630,000 mu of vineyards. This investment has enabled the implementation of efficient micro-spray systems, reducing dependence on traditional flood irrigation methods. These systems enhance water-use efficiency, lower operational costs for growers, and stabilize production in arid climatic conditions.

Rising Disposable Income and Premium-Fruit Spending

Rising income levels in China are driving increased demand for premium fruit, boosting higher-value segments within the table grapes market. According to the National Bureau of Statistics of China, per capita disposable income reached CNY 41,314 (USD 5,700) in 2024, reflecting a 5.3% year-on-year increase[1]Source: State Council Information Office of China, “SCIO Briefing on China’s Economic Performance in 2024,” english.scio.gov.cn. This consistent income growth is fostering a shift from traditional grape varieties to premium, seedless, and branded cultivars that command higher prices. Urban consumers are placing greater emphasis on quality, food safety, and product origin, leading to stronger demand for produce grown under protected cultivation. This trend allows growers to sustain price premiums and supports the development of a value-tiered market structure within China’s table grapes industry.

Heightened Health and Wellness Awareness

Increasing awareness of lifestyle diseases and a heightened regulatory emphasis on food safety are influencing consumer preferences in China’s fresh produce market. Consumers are placing greater importance on nutritional value, health benefits, and product origin, leading to a preference for safe, traceable, and high-quality fruits. Improved quality standards and traceability systems are enhancing transparency throughout the supply chain, fostering trust in certified produce. This trend is driving demand for premium table grapes grown under controlled conditions. For instance, retailers are providing fruits with scannable codes, allowing consumers to confirm origin and safety information prior to purchase.

Expansion of Cold-Chain Logistics Nationwide

The expansion of cold-chain infrastructure is enhancing the distribution efficiency of perishable fruits in China. According to data from the China Federation of Logistics and Purchasing, the demand for cold-chain logistics in China reached 365 million metric tons in 2024, marking a 4.3% year-on-year increase[2]Source: Cold Chain News, “China’s Cold Chain Logistics Sector Achieves Strong Growth in 2024,” coldchainnews.com. This growth highlights the rapid development of temperature-controlled transport and storage systems. It facilitates the faster movement of grapes from key production regions, such as Xinjiang, to major consumption hubs, thereby reducing spoilage and preserving product quality. Furthermore, new refrigerated transport routes are increasingly linking inland orchards with coastal cities, ensuring a consistent supply and broader market access for fresh table grapes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pest and disease pressure despite Integrated Pest Management (IPM) adoption | –0.3% | National, acute in humid southern provinces | Short term (≤ 2 years) |

| Intense price competition from oversupply of Shine Muscat | –0.4% | National, centered in Yunnan, Guangxi, and Guangdong | Short term (≤ 2 years) |

| Soil degradation from over-fertilization and water stress | –0.2% | National, severe in Xinjiang, Shaanxi, and Hebei | Long term (≥ 4 years) |

| Labor availability and rising wage costs in rural regions | –0.3% | National, most acute in eastern coastal provinces | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Pest and Disease Pressure Despite Integrated Pest Management (IPM) Adoption

Pest and disease pressures continue to pose significant challenges to grape production in China, even with the implementation of integrated pest management practices. Persistent fungal diseases, such as downy mildew and gray mold, often require repeated pesticide applications, which heightens the risk of resistance development and regulatory compliance issues. According to China’s updated national food safety standard, GB 2763-2026, the government has established 10,749 maximum residue limits for 585 pesticides in food, significantly tightening regulatory requirements for fruit producers. This rigorous framework increases the risk of residue non-compliance, particularly for growers dealing with recurring infestations, while also driving up production costs and exacerbating disparities between smallholders and technologically advanced farms.

Intense Price Competition from Oversupply of Shine Muscat

The rapid expansion of Shine Muscat cultivation has led to a significant oversupply in China’s table grape market, intensifying price competition and reducing grower margins. According to the United States Department of Agriculture, farm-gate prices for Shine Muscat grapes fell to RMB 8–10 per kilogram (USD 1.1–1.4) in 2025, down from RMB 12–14 per kilogram (USD 1.7–1.9) in 2024, indicating supply-driven price declines[3]Source: USDA Foreign Agricultural Service, “Fresh Deciduous Fruit Annual – China (CH2025-0220),” fas.usda.gov. This ongoing oversupply constrains profitability and heightens market volatility, particularly for smaller producers. Widespread cultivation has oversaturated wholesale channels, making it challenging for growers without differentiated or licensed varieties to maintain margins and remain competitive.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Geography Analysis

Xinjiang remains a dominant production base due to its arid climate and high sunlight exposure, which enhance sugar accumulation and berry quality. According to the United States Department of Agriculture, China’s table grapes production reached 14.2 million metric tons in the 2024–2025 season, reflecting continued expansion in key growing regions. Investments in water-saving irrigation systems are stabilizing yields under arid conditions. However, the region's distance from export ports increases logistics costs, emphasizing the importance of cold-chain infrastructure to maintain quality and competitiveness in long-distance distribution.

Yunnan benefits from subtropical climatic conditions that enable multiple harvest cycles annually, providing early-season supply advantages and improving market timing. Favorable weather patterns allow growers to supply grapes ahead of peak harvest periods in northern regions, capturing better pricing and strengthening regional competitiveness. The ability to harvest more than once supports a consistent market presence but requires careful crop and disease management. Increasing adoption of premium varieties and improved cultivation practices is enhancing fruit quality. However, the rapid expansion in planted area is intensifying supply pressure and contributing to greater price volatility across seasons.

Shaanxi benefits from favorable agroclimatic conditions and a temperate climate, which support consistent grape cultivation and stable fruit quality. Coastal provinces, including Fujian and Shandong, leverage strong export connectivity and advanced logistics infrastructure. According to Trade Map data, China exported 0.80 million metric tons of fresh grapes in 2025, indicating robust international demand and well-established trade routes. Coastal access facilitates faster shipment cycles and minimizes post-harvest losses, enhancing export competitiveness. In contrast, inland regions are increasingly prioritizing varietal improvement and cultivation efficiency to meet evolving market demands and ensure a consistent supply.

The table grape market is analyzed by Mordor Intelligence across multiple other geographies. This is complemented by country-specific insights for Spain, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

The industry comprises numerous small-scale growers with limited land holdings and differing levels of technological adoption, leading to variability in quality and supply consistency. These growers often face challenges in achieving economies of scale and maintaining uniform standards. Vertically integrated companies, including Xinjiang Turpan Horticulture Group Co., Ltd., Yunnan Haisheng Agriculture Co., Ltd., and Shanxi Yancheng Trading Co., Ltd., operate across planting, packing, and distribution, enabling them to streamline operations and secure shelf space in national supermarket chains.

Leading agribusiness firms are focusing on advanced cultivation techniques, post-harvest infrastructure, and supply chain integration to enhance their competitiveness. In 2024, Sun World International LLC expanded its global licensing network to include over 2,700 licensed growers and 180 marketers. This initiative bolstered the commercialization of proprietary table grape varieties and improved supply chain reach. The expansion promotes the broader adoption of premium seedless cultivars and strengthens product differentiation across markets. These advancements create higher entry barriers for smaller growers and drive technological upgrades, aligning production with changing consumer preferences for quality and consistency.

Major players are consolidating their market position by focusing on branding, implementing standardized quality protocols, and aligning more closely with modern retail and e-commerce channels. This approach allows them greater control over pricing and product consistency. The growing use of digital procurement platforms and stricter quality standards is transforming supplier selection processes. This trend increasingly benefits organized producers with advanced post-harvest capabilities, while smaller growers must improve operational efficiency and comply with standardized supply requirements to remain competitive in the market.

Recent Industry Developments

- February 2026: China has introduced the updated GB 2763-2026 National Food Safety Standard for Maximum Residue Limits, which sets 10,749 residue limits for 585 pesticides. This regulation raises compliance requirements for table grape growers in China, promoting stricter residue management, strengthening domestic consumption, and export competitiveness.

- December 2024: Sun World International LLC has expanded its global licensing network to include more than 2,700 growers and 180 marketers. This expansion promotes the adoption of proprietary seedless grape varieties in key production regions, enhancing the availability of premium grapes and supporting varietal differentiation in the market.

- November 2024: Brazil has gained approval to export table grapes to China following a protocol agreement between Brazil's Ministry of Agriculture and Livestock (Mapa) and Chinese customs officials. This development creates an opportunity to meet Chinese consumer demand for table grapes.

China Table Grapes Market Report Scope

Table grapes are grapes grown specifically for fresh fruit consumption, distinct from grapes cultivated for wine, juice, jelly, jam, or raisin production. The China table grapes market report is segmented by geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The report includes production analysis (production volume, area harvested, and yield), consumption analysis (value and volume), trade analysis (value and volume), import market analysis (import value and volume, key supplying markets), export market analysis (export value and volume, key destination markets), wholesale price trend analysis and forecast, regulatory framework, and logistics and infrastructure. The market forecasts are provided in terms of value (USD) and volume (metric tons).

| Production Volume | Area Harvested and Yield | |

| Consumption Analysis (Value and Volume) | ||

| Trade Analysis (Value and Volume) | Import Market Analysis | Import Value and Volume |

| Key Supplying Markets | ||

| Export Market Analysis | Export Value and Volume | |

| Key Destinations Markets | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Production Analysis | Production Volume | Area Harvested and Yield | |

| Consumption Analysis (Value and Volume) | |||

| Trade Analysis (Value and Volume) | Import Market Analysis | Import Value and Volume | |

| Key Supplying Markets | |||

| Export Market Analysis | Export Value and Volume | ||

| Key Destinations Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

Key Questions Answered in the Report

How large will the China table grapes market be by 2031?

The China table grapes market size is forecast to reach USD 35.40 billion by 2031, expanding at a 3.0% CAGR from 2026 to 2031.

Why did Shine Muscat prices fall in 2026?

Accelerated plantings in Yunnan, Guangxi, and Guangdong created oversupply, pushing wholesale prices down 50% from RMB 110 per kilogram (USD 15.2 per kilogram) to RMB 50 per kilogram (USD 6.9 per kilogram).

How does the 2026 residue law affect growers?

GB 2763-2026 sets stricter limits on 10,749 residues, requiring more precise spraying and lab testing that raise compliance costs but improve food safety.

What are the most serious vineyard pests right now?

Downy mildew and gray mold are the primary threats, developing fungicide resistance that raises input costs and endangers export compliance.

Page last updated on: