Vietnam Fruits And Vegetables Market Analysis by Mordor Intelligence

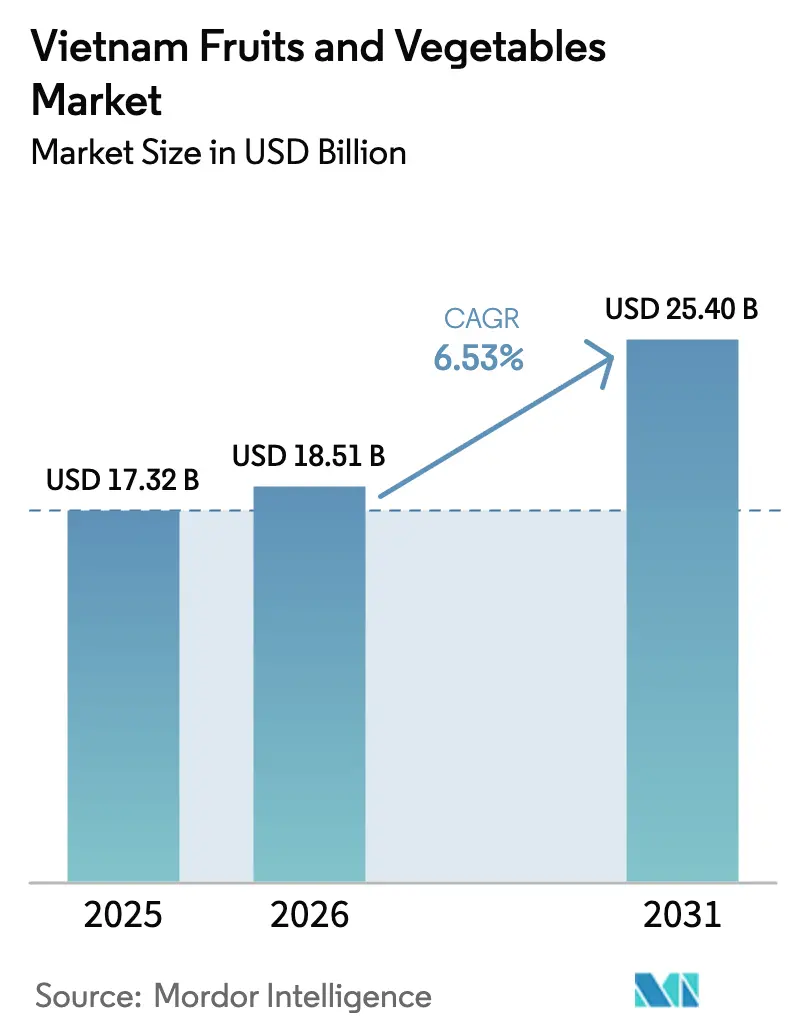

The Vietnam fruits and vegetables market is projected to expand from USD 17.32 billion in 2025 and USD 18.51 billion in 2026 to USD 25.40 billion by 2031, registering a CAGR of 6.53% between 2026 to 2031. Urban shoppers allocated a larger portion of their weekly household budgets to fresh items, accelerating the shift from smallholder plots to organized retail channels. Fruits dominate the market, with durian, dragon fruit, and mango leading in popularity, while berries have experienced the fastest growth due to highland growers utilizing temperate-zone hothouse technology. The European Union-Vietnam Free Trade Agreement (EVFTA) aims to eliminate nearly 99% of all tariffs over time, with the European Union set to remove its duties on Vietnamese goods by 2027. In parallel, investments in cold-chain logistics, packhouses, and quality certification systems are improving post-harvest handling and reducing spoilage rates, supporting both domestic distribution and export readiness. Export-oriented producers are increasingly aligning with GlobalG.A.P. and organic standards to meet the stringent requirements of premium markets, such as the European Union, Japan, and South Korea. At the same time, digital marketplaces and modern wholesale platforms are enhancing price transparency and farmer-market linkages, gradually professionalizing Vietnam’s fresh produce value chain.

Key Report Takeaways

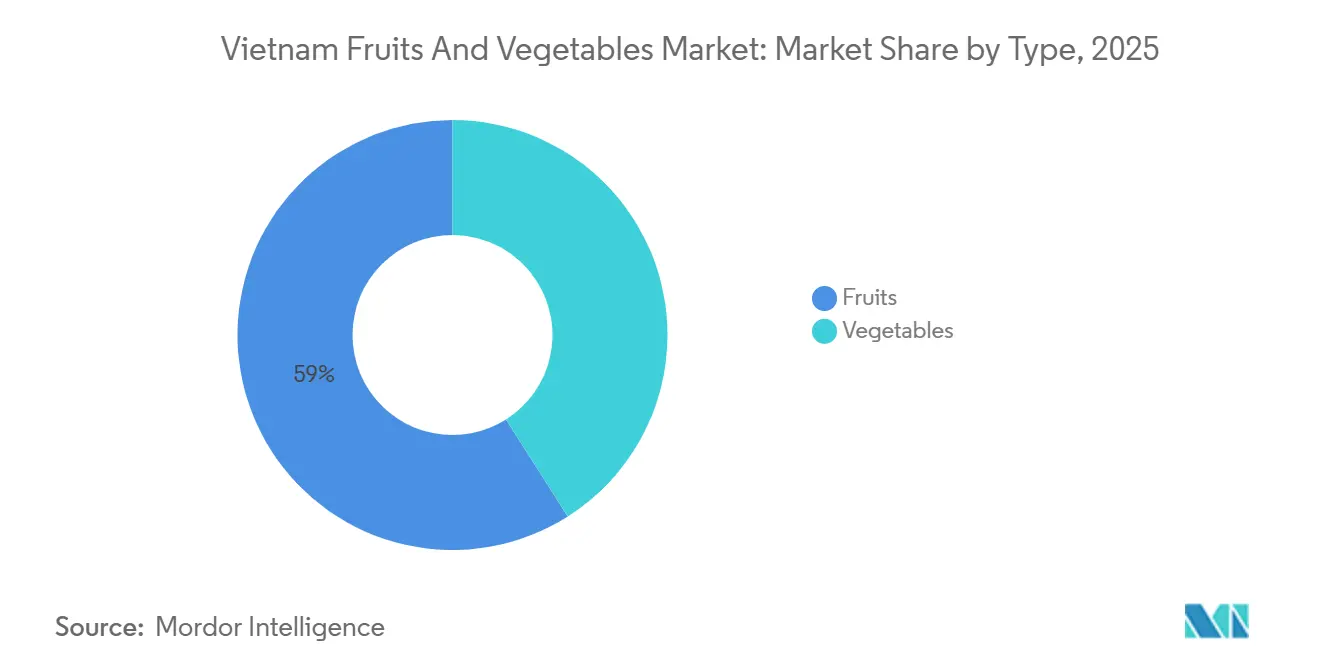

- By type, fruits accounted for 59% of the Vietnam fruits and vegetables market size in 2025 and are forecast to grow at a 7.2% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Vietnam Fruits And Vegetables Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising domestic per-capita intake of fresh produce | +1.2% | National, with the strongest gains in Hanoi, Ho Chi Minh City, and Da Nang | Medium term (2-4 years) |

| Shift from wet-markets to omnichannel retailing | +1.0% | Urban centers, spill over to provincial capitals | Medium term (2-4 years) |

| China-plus-One sourcing push by global buyers | +0.9% | Global, concentrated in the Mekong Delta and Central Highlands export zones | Short term (≤ 2 years) |

| European Union-Vietnam Free Trade Agreement tariff phase-outs | +0.8% | National, with direct gains for exporters in Southern Vietnam | Long term (≥ 4 years) |

| Precision-farming adoption in Mekong Delta | +0.7% | Mekong Delta, early pilots in the Central Highlands | Long term (≥ 4 years) |

| Carbon border adjustment risk for high-footprint crops | +0.6% | National, with urgency for European Union-facing exporters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Domestic Per-Capita Intake of Fresh Produce

Urban Vietnamese households have increased their weekly spending on fresh fruits and vegetables, driven by a growing middle class that prioritizes convenience over price. This demand surge is reshaping supply chains, as supermarkets and app-based platforms require consistent quality and next-day delivery windows that traditional wet markets cannot match. Dalat Hasfarm reported that 40% of its highland vegetable output is now distributed through AEON MaxValu stores, which stock pre-washed salad mixes and portion-controlled packs tailored for two-person households. Protein intake is also rising, yet fresh produce remains the fastest-growing category in household food expenditure, suggesting that health-conscious consumers view fruits and vegetables as complements rather than substitutes to animal products.

Shift from Wet-Markets to Omnichannel Retailing

Modern retail formats, including supermarkets and e-commerce platforms, are investing in cold-chain infrastructure to sell fresh produce, a feature typically absent in wet markets. By 2025, AEON Vietnam planned to open 15 supermarkets and 45 medium-format stores, all equipped with walk-in chillers designed to maintain temperatures between 2 °C and 4 °C. This setup will reduce spoilage by 12 percentage points compared to ambient display conditions. Sumitomo has announced plans to expand Fuji Mart from 20 to 50 stores by 2028, focusing on affluent districts where consumers are willing to pay a 15% premium for traceable produce with QR codes linked to farm records. Additionally, the omnichannel model is facilitating direct-to-consumer sales. For example, cooperatives in Lam Dong Province are bypassing wholesalers and achieving 30% higher margins by selling strawberries through platforms like Shopee Fresh and Lazada.

China-Plus-One Sourcing Push by Global Buyers

Multinational retailers and food-service operators awarded Vietnamese exporters contracts worth an estimated USD 400 million in 2024 as they diversified procurement away from China, a strategy accelerated by geopolitical friction and the need for supply-chain redundancy. Nafoods Group secured a three-year agreement with a European juice processor to supply 12,000 metric tons of passion fruit annually, a volume that necessitated the company's expansion of its contract-farming network by 2,500 hectares in Gia Lai Province. Vina T&T reported that 60% of its coconut exports now serve buyers who previously sourced from Hainan, with monthly shipments reaching 500 metric tons by mid-2024 [1]Source: Vietnam Investment Review, “Vertical Farming Pilot in Hanoi,” vir.com.vn. Smaller exporters are forming consortia to meet minimum-order quantities, a tactic that allows them to compete for contracts that individual farms cannot fulfill.

European Union-Vietnam Free Trade Agreement Tariff Phase-Outs

The European Union-Vietnam Free Trade Agreement (EVFTA) will eliminate duties on 99% of agricultural tariff lines by 2027, reducing the landed cost of Vietnamese dragon fruit in European distribution centers by 12% and enabling price parity with suppliers from Thailand and Ecuador. Vietnam's fruit exports to the European Union reached USD 320 million in 2024, a 28% increase over 2023, with pomelo and passion fruit posting the sharpest gains. The agreement also harmonizes phytosanitary standards, allowing Vietnamese pack-houses that achieve GlobalG.A.P certification to bypass additional inspections at European Union ports, a procedural change that cuts clearance time from 5 days to 36 hours. The European Union market remains sensitive to pesticide residues, and Vietnamese exporters must comply with maximum residue limits that are 40% stricter than those enforced in the Asia-Pacific region. This gap has triggered 14 border rejections since 2024.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging rural labor force | -0.8% | National, most acute in Northern Vietnam and the Mekong Delta | Long term (≥ 4 years) |

| High post-harvest loss | -0.9% | National, concentrated in regions lacking cold-chain infrastructure | Medium term (2-4 years) |

| Fragmented land-holding structure | -0.6% | National, with the highest fragmentation in the Red River Delta | Long term (≥ 4 years) |

| Escalating plant-health incidents | -0.7% | Central Highlands for TR4, Northern Vietnam for citrus greening | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging Rural Labor Force

Farmworkers over 45 years old accounted for 62% of Vietnam's agricultural labor pool in 2025, a demographic imbalance that is tightening harvest-season availability and pushing daily wages up by 8% annually[2]Source: General Statistics Office Vietnam, “Vietnam Household Food Expenditure Survey 2025,” gso.gov.vn. Youth migration to manufacturing hubs in Binh Duong and Dong Nai has left cooperatives scrambling to recruit seasonal workers, with some orchards reporting unfilled positions during peak mango and dragon fruit harvests. The gap is widening productivity differentials, as industrial estates operated by Hoang Anh Gia Lai Agricultural achieve yields 30% higher than neighboring family farms through mechanized pruning and automated irrigation. Training programs launched by the Ministry of Agriculture and Rural Development in 2024 enrolled 5,000 young farmers in precision agriculture courses and retention rates remain below 40%, as graduates opt for urban jobs that pay 50% more.

High Post-Harvest Loss

Vietnam loses 20 to 30% of its fruit and vegetable output between harvest and retail, a leakage driven by inadequate cold-chain coverage and the absence of pack-houses in remote growing areas. The Mekong Delta has only 120 cold-storage facilities with a combined capacity of 180,000 metric tons, which is insufficient to handle the region's annual fruit production of 2 million metric tons. Reefer trucks account for just 15% of the domestic transport fleet, forcing growers to ship produce in ambient containers that expose cargo to temperatures exceeding 35 degrees Celsius during summer months. Logistics costs represent a significant share of product value, which is twice the proportion observed in Thailand, where a more extensive network of cold hubs facilitates multi-stop consolidation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Fruits Dominate but Vegetables Gain Traction in Value-Added Formats

Fruits accounted for 59% of the Vietnam fruits and vegetables market size in 2025 and are forecast to grow at a 7.2% CAGR through 2031. Berries are projected to grow at the fastest rate among all product categories, as highland growers in Lam Dong Province implement hothouse systems that extend the strawberry season from 4 to 9 months and facilitate year-round blueberry production. According to the Ministry of Agriculture and Rural Development of Vietnam, durian acreage reached 112,000 hectares nationwide by late 2024, with annual output hitting 900,000 metric tons, yet frozen durian exports to China faced logistical bottlenecks as only 40 pack-houses held the required permits, constraining shipments to 60% of potential volume [3]Source: Ministry of Agriculture and Rural Development, “Regional Crop Conversion Report 2025,” mard.gov.vn.

The diverse climatic conditions in the country support the cultivation of a wide range of crops, including tropical fruits such as dragon fruit, mango, and litchi, as well as temperate vegetables like tomatoes and cabbage. In recent years, the harvest area for fruit and vegetable production has expanded as farmers increasingly adopt advanced agricultural techniques and technologies to enhance yield and quality. Vietnam is also investing in post-harvest infrastructure to minimize losses and improve export quality. Efforts include the development of cold chain logistics, innovative packaging solutions, and processing facilities to maintain freshness and meet international standards. With these advancements, Vietnam is well-positioned to strengthen its supply capabilities both regionally and globally.

Geography Analysis

The Mekong Delta held a significant market share in 2025, driven by its dominance in dragon fruit, mango, and coconut production, crops that thrive in the region's alluvial soils and year-round water access from the Mekong River's nine distributaries. The region's logistics advantage is eroding, as saltwater intrusion pushed 80 kilometers inland during the 2024 dry season, forcing farmers to invest in desalination ponds that add USD 600 per hectare to operating costs. The Mekong Delta also benefits from Cat Lai Port's reefer capacity, which expanded by 40% in 2025 to handle 180,000 twenty-foot equivalent units annually, cutting dwell time for export containers from 5 days to 48 hours.

The Central Highlands and Central Coast are projected to post the highest regional growth, driven by coffee estates converting marginal land to avocado, passion fruit, and temperate vegetables that command premiums in urban markets. The region's elevation, ranging from 800 to 1,500 meters, creates microclimates suitable for berries and stone fruits that cannot tolerate lowland heat, a geographic advantage that is drawing interest from Japanese and South Korean buyers seeking off-season supply. The Central Coast, centered around Binh Thuan and Ninh Thuan provinces, focuses on dragon fruit production for export.

Northern Vietnam remains a vegetable stronghold, supplying 60% of the leafy greens, tomatoes, and cucumbers consumed in Hanoi and surrounding provinces. Northern Vietnam's proximity to China offers a logistics edge for cross-border trade, with Lao Cai and Lang Son border gates processing 80,000 metric tons of fresh produce monthly, yet informal trade remains prevalent, undermining efforts to enforce phytosanitary standards.

Competitive Landscape

The Vietnam fruits and vegetables market, encompassing producers, importers, and exporters, is characterized by a high concentration of smallholder farms and the absence of vertically integrated players similar to Dole or Del Monte in other Asia-Pacific markets. Competition is intensifying along two key dimensions, efficiency driven by scale and premiums enabled by traceability. Hoang Anh Gia Lai Agricultural manages 7,000 hectares of bananas and 1,500 hectares of durians, achieving per-hectare yields 30% higher than the national average through mechanized pruning and drip fertigation. This productivity advantage enables the company to offer FOB prices 12% lower than those of smaller competitors.

Opportunities are emerging in organic certification and carbon-neutral supply chains, areas where Vietnamese producers lag behind their Thai and Philippine counterparts, despite benefiting from lower labor costs. Technology adoption is becoming a critical differentiator as buyers increasingly demand blockchain traceability and real-time cold-chain monitoring. In 2024, Vina T&T introduced a QR code system that links each durian shipment to its farm coordinates, harvest dates, and pesticide usage logs. This transparency helped the company secure a three-year contract with a Japanese retailer.

Smaller exporters are forming consortia to share the USD 50,000 cost of implementing IoT sensors and cloud-based inventory platforms. This collaborative approach enables them to compete for contracts that require a minimum monthly volume of 200 metric tons. Emerging disruptors include e-commerce platforms such as Kingfoodmart, which bypassed traditional wholesalers in urban fresh produce sales in 2024 by offering same-day delivery and direct farm-to-consumer pricing.

Recent Industry Developments

- December 2025: The Vietnamese government sought to increase banana exports to USD 1 billion. Bananas have been designated as a priority crop under the Project for the Development of Key Fruit Crops, with a vision extending to 2030. The plan includes expanding plantation areas to 165,000–175,000 hectares and increasing production to 2.6–3 million tons by 2030.

- November 2024: Hoang Anh Gia Lai Agricultural and Kingfoodmart signed a strategic partnership to distribute bananas, durians, and pork through Kingfoodmart's network of 80 stores and the OneLife app, which serves 2 million users. The agreement integrates HAGL's 7,000 hectares of banana plantations and 1,500 hectares of durian orchards into a direct-to-consumer channel that bypasses wholesale markets.

- January 2024: Vietnam aims to boost the land area adhering to VietGAP standards by 10-15% annually and to have organic farming occupy 1% of its total cultivated land by 2030. This initiative focuses on various agricultural commodities, including fruits and vegetables. The strategy also focuses on creating clusters that link the production, processing, and consumption of vegetables in targeted localities and regions.

Vietnam Fruits And Vegetables Market Report Scope

Vegetables are edible plant parts such as leaves, stems, roots, or bulbs, while fruits are mature, seed-bearing structures of flowering plants. The report categorizes fruits and vegetables by end user. The Report Includes Production Analysis (Volume), Consumption Analysis (Value and Volume), Import Analysis (Value and Volume), Export Analysis (Value and Volume), Wholesale Price Trend Analysis and Forecast, List of Key Players, and More. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Type

| Vegetables | Cucumbers | Production Analysis | Production Volume | |

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Trade Analysis (Value and Volume) | Import Market Analysis | Import Value and Volume | ||

| Key Supplying Markets | ||||

| Export Market Analysis | Export Value and Volume | |||

| Key Destination Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Tomatoes | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destination Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Cabbage | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destination Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Carrots | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destination Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Fruits | Grapes | Production Analysis | Production Volume | |

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destination Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Apples | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destination Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Banana | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destination Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Mango | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destination Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Durian | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destination Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Dragon Fruit | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destination Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Type | Vegetables | Cucumbers | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||||

| Consumption Analysis (Value and Volume) | |||||

| Trade Analysis (Value and Volume) | Import Market Analysis | Import Value and Volume | |||

| Key Supplying Markets | |||||

| Export Market Analysis | Export Value and Volume | ||||

| Key Destination Markets | |||||

| Wholesale Price Trend Analysis and Forecast | |||||

| Seasonality Analysis | |||||

| Tomatoes | Production Analysis | Production Volume | |||

| Area Harvested and Yield | |||||

| Consumption Analysis (Value and Volume) | |||||

| Import Value and Volume | |||||

| Key Supplying Markets | |||||

| Export Value and Volume | |||||

| Key Destination Markets | |||||

| Wholesale Price Trend Analysis and Forecast | |||||

| Seasonality Analysis | |||||

| Cabbage | Production Analysis | Production Volume | |||

| Area Harvested and Yield | |||||

| Consumption Analysis (Value and Volume) | |||||

| Import Value and Volume | |||||

| Key Supplying Markets | |||||

| Export Value and Volume | |||||

| Key Destination Markets | |||||

| Wholesale Price Trend Analysis and Forecast | |||||

| Seasonality Analysis | |||||

| Carrots | Production Analysis | Production Volume | |||

| Area Harvested and Yield | |||||

| Consumption Analysis (Value and Volume) | |||||

| Import Value and Volume | |||||

| Key Supplying Markets | |||||

| Export Value and Volume | |||||

| Key Destination Markets | |||||

| Wholesale Price Trend Analysis and Forecast | |||||

| Seasonality Analysis | |||||

| Fruits | Grapes | Production Analysis | Production Volume | ||

| Area Harvested and Yield | |||||

| Consumption Analysis (Value and Volume) | |||||

| Import Value and Volume | |||||

| Key Supplying Markets | |||||

| Export Value and Volume | |||||

| Key Destination Markets | |||||

| Wholesale Price Trend Analysis and Forecast | |||||

| Seasonality Analysis | |||||

| Apples | Production Analysis | Production Volume | |||

| Area Harvested and Yield | |||||

| Consumption Analysis (Value and Volume) | |||||

| Import Value and Volume | |||||

| Key Supplying Markets | |||||

| Export Value and Volume | |||||

| Key Destination Markets | |||||

| Wholesale Price Trend Analysis and Forecast | |||||

| Seasonality Analysis | |||||

| Banana | Production Analysis | Production Volume | |||

| Area Harvested and Yield | |||||

| Consumption Analysis (Value and Volume) | |||||

| Import Value and Volume | |||||

| Key Supplying Markets | |||||

| Export Value and Volume | |||||

| Key Destination Markets | |||||

| Wholesale Price Trend Analysis and Forecast | |||||

| Seasonality Analysis | |||||

| Mango | Production Analysis | Production Volume | |||

| Area Harvested and Yield | |||||

| Consumption Analysis (Value and Volume) | |||||

| Import Value and Volume | |||||

| Key Supplying Markets | |||||

| Export Value and Volume | |||||

| Key Destination Markets | |||||

| Wholesale Price Trend Analysis and Forecast | |||||

| Seasonality Analysis | |||||

| Durian | Production Analysis | Production Volume | |||

| Area Harvested and Yield | |||||

| Consumption Analysis (Value and Volume) | |||||

| Import Value and Volume | |||||

| Key Supplying Markets | |||||

| Export Value and Volume | |||||

| Key Destination Markets | |||||

| Wholesale Price Trend Analysis and Forecast | |||||

| Seasonality Analysis | |||||

| Dragon Fruit | Production Analysis | Production Volume | |||

| Area Harvested and Yield | |||||

| Consumption Analysis (Value and Volume) | |||||

| Import Value and Volume | |||||

| Key Supplying Markets | |||||

| Export Value and Volume | |||||

| Key Destination Markets | |||||

| Wholesale Price Trend Analysis and Forecast | |||||

| Seasonality Analysis | |||||

Key Questions Answered in the Report

What is the current and projected value of the Vietnam fruits and vegetables market?

The market was valued at USD 18.51 billion in 2026 and is projected to reach USD 25.40 billion by 2031.

Which region holds the largest share?

The Mekong Delta is considered of high value in 2025 owing to dragon fruit, mango, and coconut output.

How is retail changing the supply chain?

Modern and omnichannel retail captured 32% of fresh-produce sales in 2025, forcing suppliers to meet strict cold-chain and traceability standards.

What are the main export tailwinds?

Duty-free access under the European Union-Vietnam Free Trade Agreement and global China-plus-One sourcing have increased contracts for certified Vietnamese exporters.

Page last updated on: