Automated Barriers And Bollards Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 22.73 Billion |

| Market Size (2030) | USD 27.39 Billion |

| Growth Rate (2025 - 2030) | 3.80% CAGR |

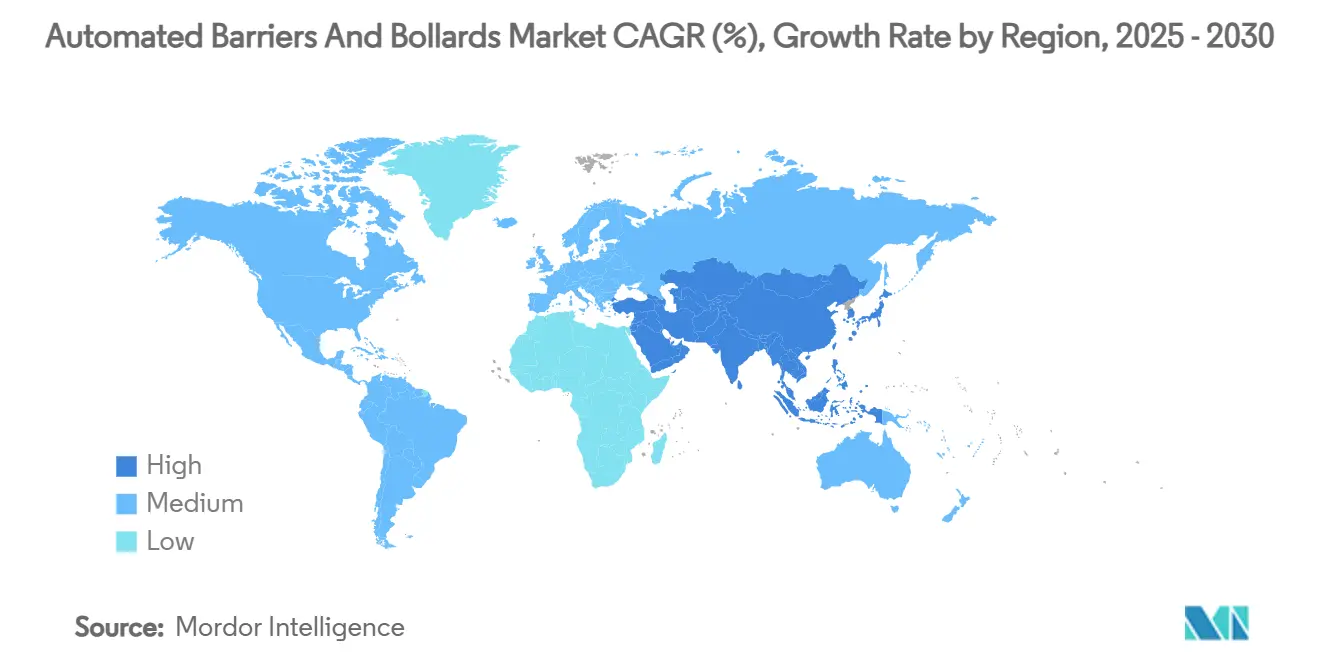

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

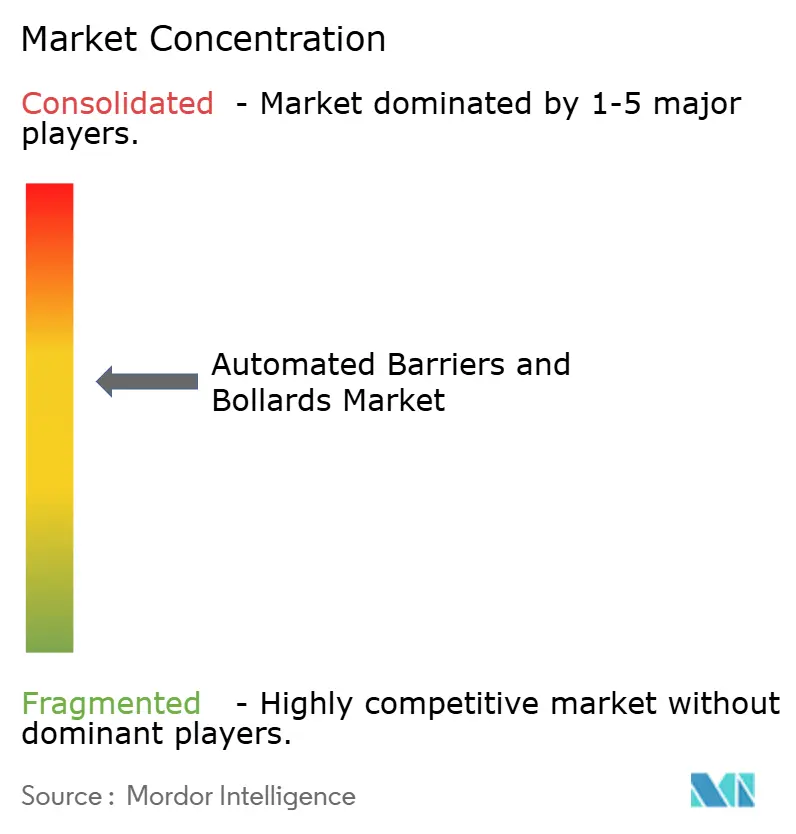

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automated Barriers And Bollards Market Analysis by Mordor Intelligence

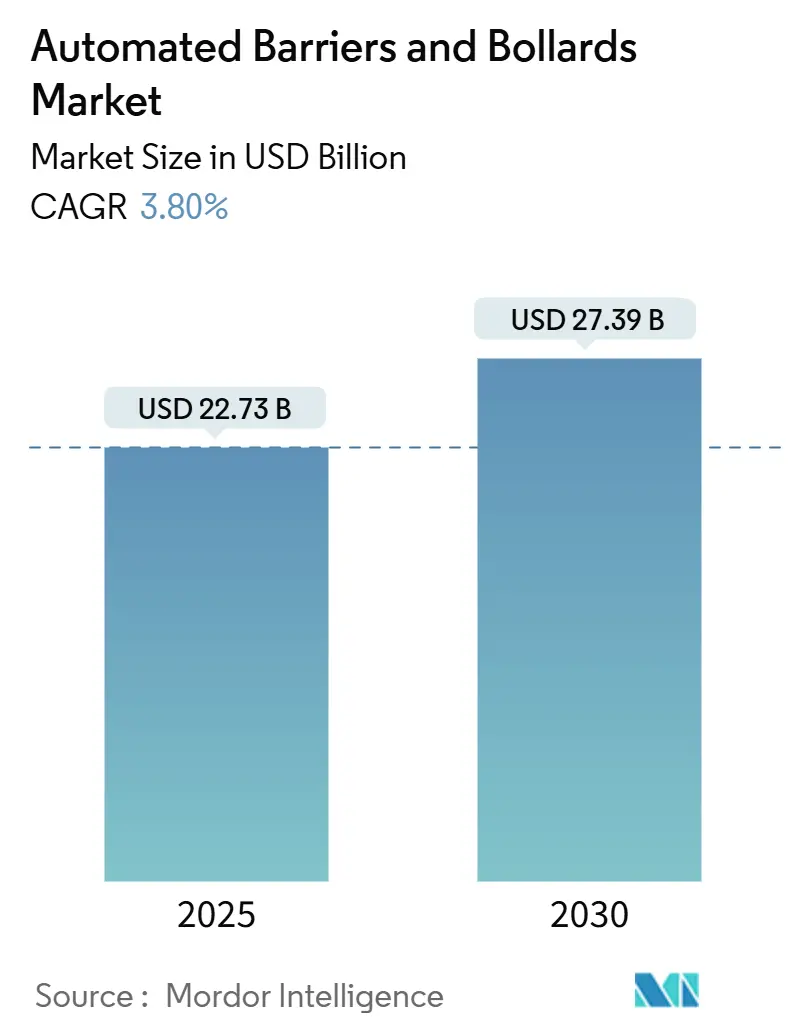

The Automated Barriers and Bollards Market size is estimated at USD 22.73 billion in 2025 and is expected to reach USD 27.39 billion by 2030, at a CAGR of 3.80% during the forecast period (2025-2030). Momentum comes from rising global security mandates, the rapid roll-out of smart-city programs, and airport, rail, and mixed-use campus expansions that call for certified perimeter protection systems. Europe keeps its lead position, while Asia-Pacific records the fastest compound growth on the strength of large-scale infrastructure projects. Product innovation now centers on IoT-ready bollards, solar-powered off-grid models, and software that predicts maintenance needs, reducing lifetime costs of ownership. Competitive intensity is moderate as large incumbents combine strategic acquisitions with proprietary radio protocols and crash-rating upgrades, while smaller specialists carve out share through smart-city pilots and tourist-district roll-outs.

Key Report Takeaways

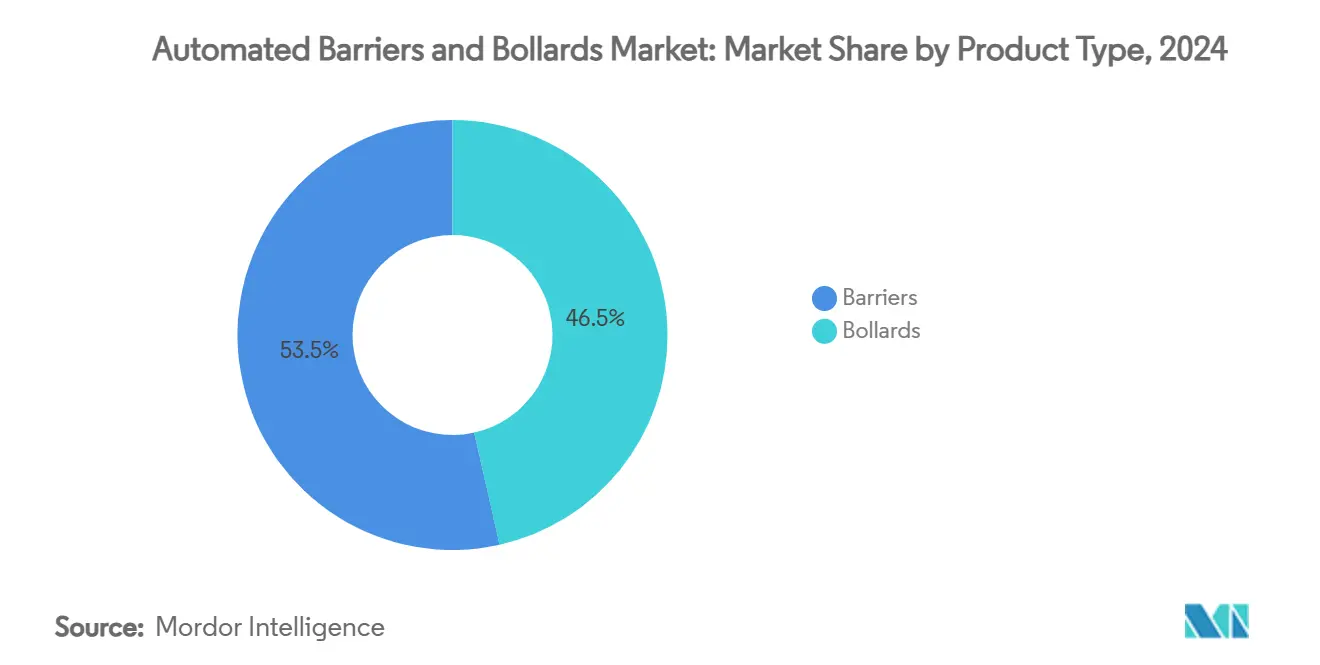

- By product type, barriers commanded 53.5% of Automated Barriers and Bollards market share in 2024, whereas bollards are projected to expand at a 4.75% CAGR through 2030.

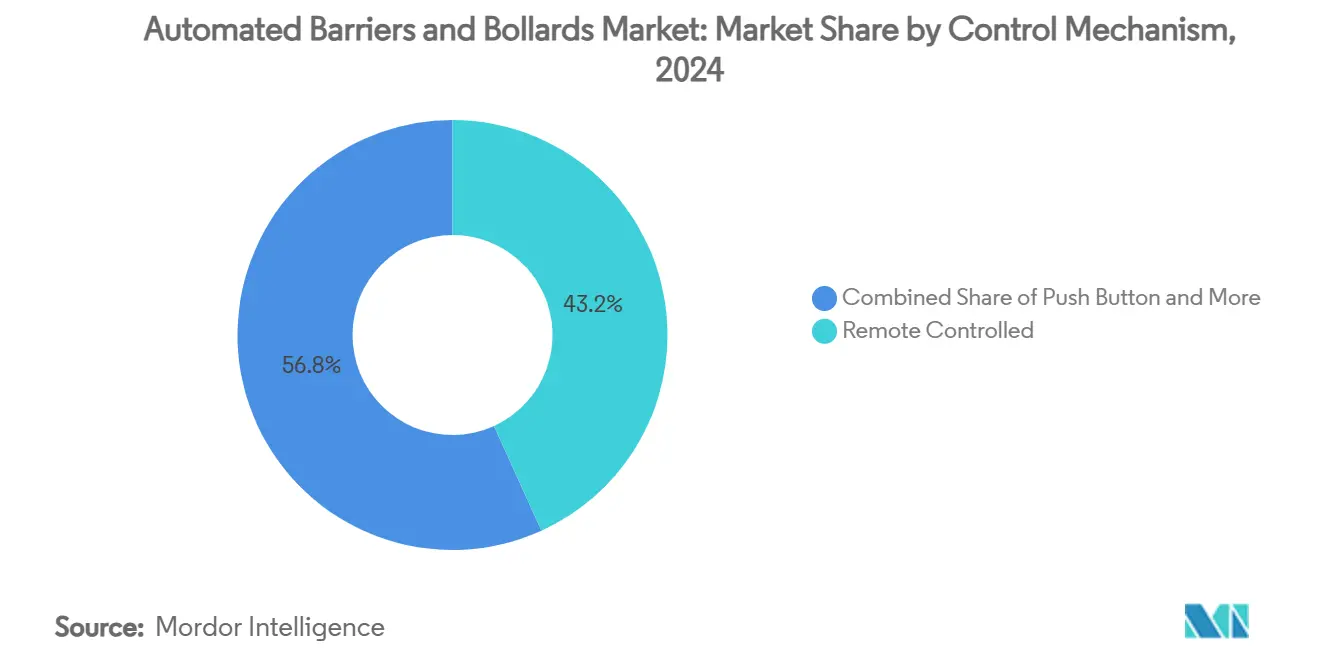

- By control mechanism, the remote-controlled segment held 43.21% revenue share in 2024; loop detectors are the fastest-growing at 4.90% CAGR to 2030.

- By end-user, commercial buildings led with 43.0% share of the Automated Barriers and Bollards market size in 2024, while the “Others” category (including tourism districts and campuses) advances at 5.10% CAGR.

- By geography, Europe accounted for 31.2% of 2024 revenue; Asia-Pacific is forecast to record a 5.60% CAGR through 2030.

Global Automated Barriers And Bollards Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of smart-city projects integrating automated access control | +1.2% | Global, with early adoption in EU & North America | Medium term (2-4 years) |

| Rising security concerns amid increasing vehicle-ramming incidents | +0.8% | Global, concentrated in high-risk urban areas | Short term (≤ 2 years) |

| Expansion of transportation hubs & parking infrastructure | +0.6% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Government mandates for perimeter security at critical infrastructure | +0.4% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Convergence of automated barriers with IoT-enabled predictive maintenance | +0.3% | Global, led by developed markets | Medium term (2-4 years) |

| Growing adoption of solar-powered off-grid rising bollards in smart tourism districts | +0.2% | Global tourism hubs, concentrated in coastal regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Smart-City Projects Integrating Automated Access Control

Smart city initiatives are fundamentally reshaping the automated barriers market by embedding access control systems within broader IoT ecosystems that enable predictive maintenance and real-time monitoring. The integration of sensors within pavement materials during construction minimizes installation damage while providing comprehensive data on traffic dynamics and environmental conditions, as demonstrated in recent IoT-enhanced smart road infrastructure deployments. Cities are increasingly adopting barrier-free tolling systems, such as Kapsch TrafficCom's EUR 12.5 million (USD 13.5 million) Multi-Lane Free Flow implementation in Spain's Basque region, which eliminates physical barriers while maintaining access control through automated vehicle identification. This convergence of access control with smart infrastructure creates new revenue streams for barrier manufacturers who can offer integrated solutions rather than standalone products. The shift toward connected infrastructure also enables remote diagnostics and predictive maintenance, reducing operational costs and improving system reliability. Smart city projects are driving demand for solar-powered bollards in tourism districts and pedestrian zones, where traditional power infrastructure is limited but aesthetic and environmental considerations are paramount.

Rising Security Concerns Amid Increasing Vehicle-Ramming Incidents

Vehicle ramming attacks have become a critical driver for automated barrier adoption, with incidents like the 2025 New Orleans Bourbon Street attack exposing the consequences of inadequate perimeter security where protective bollards had been removed or broken. The Department of Homeland Security's deployment of the DETER portable barrier system at the Indianapolis 500 in 2024 demonstrates how government agencies are prioritizing rapid-deployment solutions that can protect large crowds while maintaining operational flexibility[1]Department of Homeland Security, “DETER Barrier Deployed at Indianapolis 500,” dhs.gov. CISA's updated Vehicle Incident Prevention and Mitigation Security Guide emphasizes the emerging risks from autonomous vehicles and the need for updated security measures to address evolving threats[2]CISA, “Vehicle Incident Prevention and Mitigation Guide,” cisa.gov. The proliferation of ASTM F3016 crash-rated bollards reflects the industry's response to over 60 daily vehicle incursions into storefronts, with commercial real estate owners increasingly recognizing these systems as liability mitigation tools. Insurance companies are beginning to offer premium reductions for properties equipped with certified barrier systems, creating economic incentives beyond regulatory compliance. The focus on vehicle ramming incidents is driving demand for high-security bollards capable of stopping 7.5-ton vehicles at 48 km/h, as offered by manufacturers like CAME.

Expansion of Transportation Hubs & Parking Infrastructure

Transportation infrastructure expansion across Asia-Pacific is creating substantial demand for automated barrier systems, with major airport projects including Shanghai Pudong Airport expansions and new airport constructions in Dalian and Xiamen requiring comprehensive access control solutions. Container terminals are increasingly adopting automated gate operations, as demonstrated by DCT Gdańsk SA's implementation of automated barriers that improve operational efficiency while reducing labor costs. The parking barrier market segment is experiencing accelerated growth driven by rising incomes in emerging markets like China and India. Where consumers are shifting from manual to automated parking solutions. Off-street parking systems in developed markets are also expanding, supported by increased commercial construction activity that requires sophisticated access control capabilities. The integration of RFID technology in urban traffic management systems enables dynamic vehicle identification and access control to restricted zones, supporting the development of automated barriers in smart city environments. Transportation hub expansions are driving demand for barriers that can integrate with existing security systems while providing scalable solutions for future capacity increases.

Government Mandates for Perimeter Security at Critical Infrastructure

Federal agencies are establishing comprehensive standards for vehicle security barriers, with CISA's Dams Sector Active and Passive Vehicle Barriers Guide providing technical specifications for critical infrastructure protection. The Federal Highway Administration's primer on impact protection for transportation infrastructure outlines performance standards and risk management processes that transportation agencies must follow when implementing vehicle security barriers. ASTM standards F2656 and F3016 are becoming mandatory specifications for government procurement, with the DOD Anti-Ram Vehicle Barrier List including only approved manufacturers whose products meet stringent testing requirements. City and county governments are increasingly adopting ASTM F3016 standards for low-speed impact protection, driven by liability concerns and the need to comply with emerging safety codes. The regulatory push is creating market opportunities for manufacturers who can demonstrate compliance with federal standards while offering integrated solutions that address multiple security requirements. Government mandates are particularly influential in the critical infrastructure sector, where compliance is non-negotiable and cost considerations are secondary to security effectiveness.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront installation costs versus manual barriers | -0.6% | Global, particularly in price-sensitive emerging markets | Short term (≤ 2 years) |

| Stringent maintenance & certification requirements in developed markets | -0.4% | North America & EU primarily | Medium term (2-4 years) |

| Radio-frequency congestion interfering with remote-controlled barriers in dense urban cores | -0.3% | Global urban centers, concentrated in megacities | Short term (≤ 2 years) |

| Counterfeiting of low-quality imported bollards undermining premium brands | -0.2% | APAC emerging markets, spill-over to MEA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Installation Costs Versus Manual Barriers

The substantial capital investment required for automated barrier systems creates adoption barriers, particularly in emerging markets where cost sensitivity remains high despite growing security awareness. California Department of Transportation's lifecycle cost analysis reveals that while automated systems offer long-term operational savings, the initial investment can be 3-5 times higher than manual alternatives, creating budget constraints for municipalities and private developers. The complexity of installation often requires specialized contractors and extended project timelines, adding to the total cost of ownership. Competition from local low-cost suppliers in emerging regions further pressures pricing, as these manufacturers offer basic functionality at significantly lower prices, though often without proper certification or long-term support. The high upfront costs are particularly challenging for small-scale applications where the security benefits may not justify the investment, limiting market penetration in residential and small commercial segments. However, the emergence of leasing models and government incentive programs is beginning to address these cost barriers, particularly for ASTM-certified systems that qualify for insurance premium reductions.

Stringent Maintenance & Certification Requirements in Developed Markets

Automated barrier systems face complex maintenance and certification requirements that create ongoing operational burdens, particularly in developed markets where regulatory compliance is strictly enforced. The ASTM certification process requires extensive testing and documentation, with manufacturers needing to demonstrate compliance with specific penetration ratings and impact conditions that vary by application. IoT-enabled predictive maintenance systems, while offering operational benefits, require specialized technical expertise and ongoing software updates that many organizations lack internally. The need for regular recertification and compliance audits creates recurring costs that can exceed the initial equipment investment over the system's lifecycle. Radio frequency congestion in dense urban environments can interfere with remote-controlled barriers, requiring additional technical solutions and maintenance protocols to ensure reliable operation. The complexity of maintaining integrated systems that combine physical barriers with IoT sensors, communication protocols, and software platforms creates dependencies on specialized service providers, increasing operational costs and potential points of failure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Barriers Lead Market Share

Barriers maintain dominance with a 53.5% market share in 2024, driven by their adaptability across diverse applications from transportation hubs to commercial complexes, while bollards emerge as the fastest-growing segment at 4.75% CAGR through 2030. The barrier segment's leadership reflects its versatility in handling high-volume traffic scenarios, particularly in parking facilities and toll collection points where throughput efficiency is paramount. Bollards are gaining traction due to their aesthetic integration capabilities in urban environments and their effectiveness in pedestrian-heavy areas where traditional barriers would impede foot traffic.

The growth differential between these segments reflects evolving security priorities, with bollards increasingly favored for perimeter protection applications where permanent installation and crash resistance are critical[3]Hörmann, “European Bollard Installations,” hoermann.com. CAME's high-security bollards, capable of stopping 7.5-ton vehicles at 48 km/h, exemplify the segment's evolution toward military-grade protection standards. The barrier segment benefits from established supply chains and standardized installation processes, while bollards require more specialized engineering and site-specific customization. Smart city initiatives are driving demand for solar-powered bollards in tourism districts where grid connectivity is limited but security requirements remain high. The convergence of these product types with IoT technology is creating hybrid solutions that combine the traffic management capabilities of barriers with the security features of bollards.

By Control Mechanism: Remote Systems Dominate

Remote-controlled systems command a 43.21% market share in 2024, reflecting the preference for centralized access management in commercial and institutional applications, while loop detectors represent the fastest-growing technology at 4.90% CAGR through 2030. The dominance of remote control systems stems from their operational flexibility and integration capabilities with existing security infrastructure, allowing operators to manage multiple access points from centralized command centers. Loop detectors are gaining momentum due to their automation potential and reduced labor requirements, particularly in high-traffic applications where manual intervention is impractical.

Push button systems continue to serve niche applications where simple, reliable operation is preferred over sophisticated control mechanisms, particularly in residential and small commercial settings. RFID and smart-card systems are experiencing steady growth driven by their integration with broader access control ecosystems and their ability to provide detailed audit trails for security compliance. The "Others" category encompasses emerging technologies, including biometric systems and mobile app-based controls that are beginning to gain traction in premium applications. Hörmann's BiSecur radio technology demonstrates how manufacturers are addressing radio frequency congestion issues through proprietary communication protocols that ensure reliable operation in dense urban environments. The evolution toward loop detector dominance reflects the industry's broader automation trend, where systems that can operate autonomously with minimal human intervention are increasingly preferred for their operational efficiency and reduced labor costs.

By End-user Sector: Commercial Applications Drive Demand

Commercial applications account for 43.0% market share in 2024, supported by stringent security requirements and operational efficiency demands in office complexes, retail centers, and industrial facilities, while the "Others" category expands at 5.10% CAGR through 2030. The commercial segment's leadership reflects the sector's willingness to invest in sophisticated access control systems that can integrate with broader security and building management platforms. Residential buildings represent a stable but slower-growing segment, where cost considerations often limit adoption to premium developments and gated communities.

The "Others" category encompasses emerging applications, including tourism districts, educational institutions, and healthcare facilities that are increasingly adopting automated barrier systems for both security and operational efficiency. The growth in this segment is driven by the proliferation of solar-powered bollards in smart tourism districts where traditional power infrastructure is limited but security and aesthetic considerations are paramount. Commercial applications benefit from economies of scale and standardized installation processes, while residential applications often require customization that increases costs and complexity. The segment dynamics reflect broader trends in urbanization and infrastructure development, where commercial properties are increasingly viewed as potential security targets requiring sophisticated protection systems. Government facilities and critical infrastructure represent a specialized subsegment with unique requirements for crash-rated barriers and compliance with federal security standards.

By Geography: Europe Leads, Asia-Pacific Accelerates

Europe maintains market leadership with a 31.2% share in 2024, supported by established regulatory frameworks and mature infrastructure security protocols, while Asia-Pacific emerges as the fastest-growing region at 5.60% CAGR through 2030. European dominance reflects the region's early adoption of comprehensive security standards and its established base of critical infrastructure requiring perimeter protection. The regulatory environment in Europe, including EU-wide standards for automated access control systems, creates a stable market for certified barrier manufacturers.

Asia-Pacific's accelerated growth is driven by massive infrastructure investments, including airport expansions in Shanghai, Dalian, and Xiamen that require comprehensive access control solutions. The region's rapid urbanization and rising security awareness are creating demand for both traditional barriers and innovative solutions like solar-powered bollards in tourism districts. North America represents a mature market with steady growth driven by government mandates and insurance incentives for ASTM-certified barrier systems. The Middle East and Africa show emerging potential, particularly in countries investing heavily in tourism infrastructure and critical facility protection. South America remains a smaller but growing market, with countries like Brazil and Argentina beginning to adopt automated barrier systems for both security and traffic management applications. The geographic distribution reflects global infrastructure development patterns, with established markets focusing on system upgrades and emerging markets driving new installations.

Geography Analysis

Europe will command a 31.2% market share in 2024, underpinned by comprehensive regulatory frameworks and established infrastructure security protocols that create stable demand for certified barrier systems. The region's leadership stems from the early adoption of EU-wide standards for automated access control, exemplified by the FastPass project's development of harmonized e-gate systems for border control applications. Spain's implementation of Kapsch TrafficCom's EUR 12.5 million (USD 13.5 million) barrier-free tolling system in the Basque region demonstrates the region's commitment to advanced traffic management technologies that eliminate physical barriers while maintaining access control. European manufacturers like Hörmann are pioneering CO2-neutral barrier solutions and proprietary radio technologies that address urban congestion challenges. The region's mature market is characterized by system upgrades and integration with smart city initiatives rather than greenfield installations.

Asia-Pacific represents the fastest-growing region at 5.60% CAGR through 2030, driven by massive infrastructure investments and rapid urbanization that create substantial demand for automated access control systems. Major airport development projects across China, Malaysia, and Indonesia, including Shanghai Pudong Airport expansions and new airport constructions in Dalian and Xiamen, require comprehensive perimeter security solutions. The region's growth is supported by rising incomes in emerging markets like China and India, where consumers are shifting from manual to automated parking solutions. Container terminal automation, as demonstrated by DCT Gdańsk SA's successful implementation, is becoming a standard practice across major Asian ports. The APAC market benefits from government infrastructure spending and the region's leadership in smart city development, creating opportunities for integrated barrier solutions that combine security with traffic management capabilities.

North America maintains a significant market presence supported by federal mandates and comprehensive security standards that drive demand for ASTM-certified barrier systems. The Department of Homeland Security's deployment of the DETER portable barrier system at major events like the Indianapolis 500 demonstrates the region's commitment to advanced security technologies CISA's updated security guidelines and the Federal Highway Administration's impact protection standards create a regulatory environment that favors certified barrier manufacturers. The region's market is characterized by replacement cycles and technology upgrades rather than new installations, with insurance incentives increasingly driving the adoption of crash-rated bollards for commercial real estate protection. The Middle East and Africa show emerging potential, particularly in countries investing in tourism infrastructure and critical facility protection, while South America represents a smaller but growing market with increasing adoption in Brazil and Argentina.

Note: Segments share of all individual segments available upon report purchase

Competitive Landscape

The automated barriers and bollards market exhibits moderate fragmentation with established players competing through technology integration and strategic acquisitions rather than price competition alone. Market leaders like Hill & Smith, FAAC Group, and Hörmann maintain competitive advantages through comprehensive product portfolios and established distribution networks while emerging players focus on IoT integration and smart city applications. The competitive intensity is increasing as manufacturers recognize the need for integrated solutions that combine physical barriers with predictive maintenance capabilities and remote monitoring systems.

Strategic consolidation is reshaping the competitive landscape, exemplified by Hill & Smith's USD 6.25 million acquisition of Capital Steel Service in January 2024 to expand its engineered solutions portfolio. Technology differentiation is becoming critical, with companies like Hörmann developing proprietary BiSecur radio technology to address urban congestion challenges and CAME offering high-security bollards with specific crash ratings. White-space opportunities exist in solar-powered off-grid applications and integrated smart city solutions that combine access control with traffic management. The market is witnessing the emergence of specialized players who focus on niche applications like tourism districts and critical infrastructure, creating opportunities for companies that can demonstrate compliance with evolving security standards while offering innovative deployment models.

Automated Barriers And Bollards Industry Leaders

Automatic Systems

Avon Barrier

Macs Automated Bollard Systems Ltd

Houston Systems Private Limited

Magnetic Autocontrol GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: A vehicle attack on New Orleans’ Bourbon Street revealed gaps where damaged bollards had been removed, spurring a federal review of urban-core perimeter security and fast-tracking replacement budgets in multiple U.S. cities.

- January 2025: Prosegur USA issued guidelines for mitigating vehicular-ramming threats, stressing ASTM-certified products and offering a threat-assessment matrix for facility owners.

- July 2024: The U.S. Department of Homeland Security field-tested its DETER portable barrier at the Indianapolis 500, safeguarding 300,000 spectators while collecting durability data.

- July 2024: Smiths Group logged 38% order growth in its Detection division, crediting strong demand for barrier and scanner packages.

Global Automated Barriers And Bollards Market Report Scope

Automated Barriers and Bollards are gaining popularity because of developing concerns regarding public safety and security in crowded and industrial areas, for example, food courts, theaters, and shows. Boundary entryways are level shafts or bars turned to deal with the progression of vehicles by permitting or stopping the vehicle. Street construction has given an approach to mechanized boundaries to be introduced out and about (center or sideways) globally. Automated barriers and bollards products limitation of vehicle entry in multiple indoor and outdoor construction, for example, tollgates, high-security areas, parking areas of retail outlets, workplaces, hotels, and sports centers.

It also provides a comprehensive analysis of the Segmentation By Product (Push Button, Remote Controlled, RFID Tags Reader, Loop Detectors), By End-user (Residential, Commercial, Industrial), By Geography (North America, Europe, Asia-Pacific, Middle East & Africa and Rest of the world).

The report offers the market sizes and forecasts for the automated barriers and bollards market in value (USD) for all the above segments. Furthermore, the report also provides company profiles of leading market players to understand the competitive landscape of the market.

| Barriers |

| Bollards |

| Push Button |

| Remote Controlled |

| RFID / Smart-Card |

| Loop Detectors |

| Others |

| Residential Buildings |

| Commercial Buidlings |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Indonesia | |

| Rest of Asia-Pacific |

| By Product Type | Barriers | |

| Bollards | ||

| By Control Mechanism | Push Button | |

| Remote Controlled | ||

| RFID / Smart-Card | ||

| Loop Detectors | ||

| Others | ||

| By End-user Sector | Residential Buildings | |

| Commercial Buidlings | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

What is the current Automated Barriers and Bollards Market size?

The current Automated Barriers and Bollards Market size in 2025 is USD 22.73 billion.

Who are the key players in Automated Barriers and Bollards Market?

Automatic Systems, Avon Barrier, Macs Automated Bollard Systems Ltd, Houston Systems Private Limited and Magnetic Autocontrol GmbH are the major companies operating in the Automated Barriers and Bollards Market.

Which is the fastest growing region in Automated Barriers and Bollards Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Automated Barriers and Bollards Market?

In 2025, the North America accounts for the largest market share in Automated Barriers and Bollards Market.

What years does this Automated Barriers and Bollards Market cover?

The report covers the Automated Barriers and Bollards Market historical market size for years: 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Automated Barriers and Bollards Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: