China Mutual Fund Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 4.82 Trillion |

| Market Size (2026) | USD 5.15 Trillion |

| Market Size (2031) | USD 7.21 Trillion |

| Growth Rate (2026 - 2031) | 6.95% CAGR |

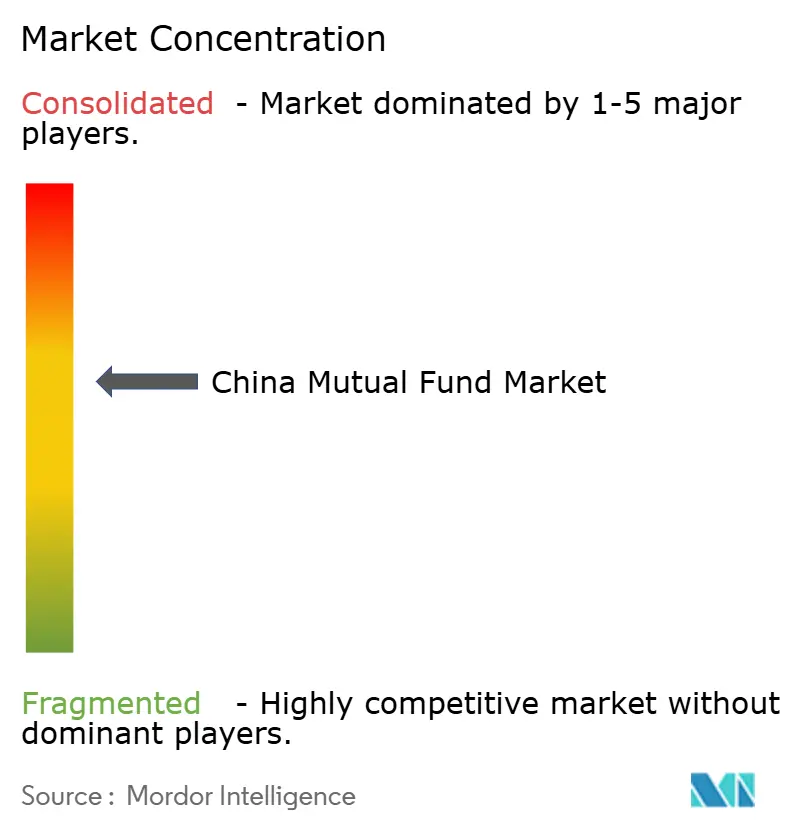

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Mutual Fund Market Analysis by Mordor Intelligence

China mutual fund market size in 2026 is estimated at USD 5.15 trillion, growing from 2025 value of USD 4.82 trillion with 2031 projections showing USD 7.21 trillion, growing at 6.95% CAGR over 2026-2031. Strong household migration from low-yield bank deposits into professionally managed funds, an expanding private pension system, and the rapid uptake of digital distribution channels underpin this upward trajectory. Fee compression is steering investors toward low-cost passive products, yet active management remains dominant as volatility encourages professional security selection. Foreign managers are gaining direct access after regulatory liberalization, creating fresh competitive pressure for domestic firms. The concurrent rise in cross-border quotas deepens investor diversification options, reinforcing growth in equity and thematic funds.

Key Reports Takeaways

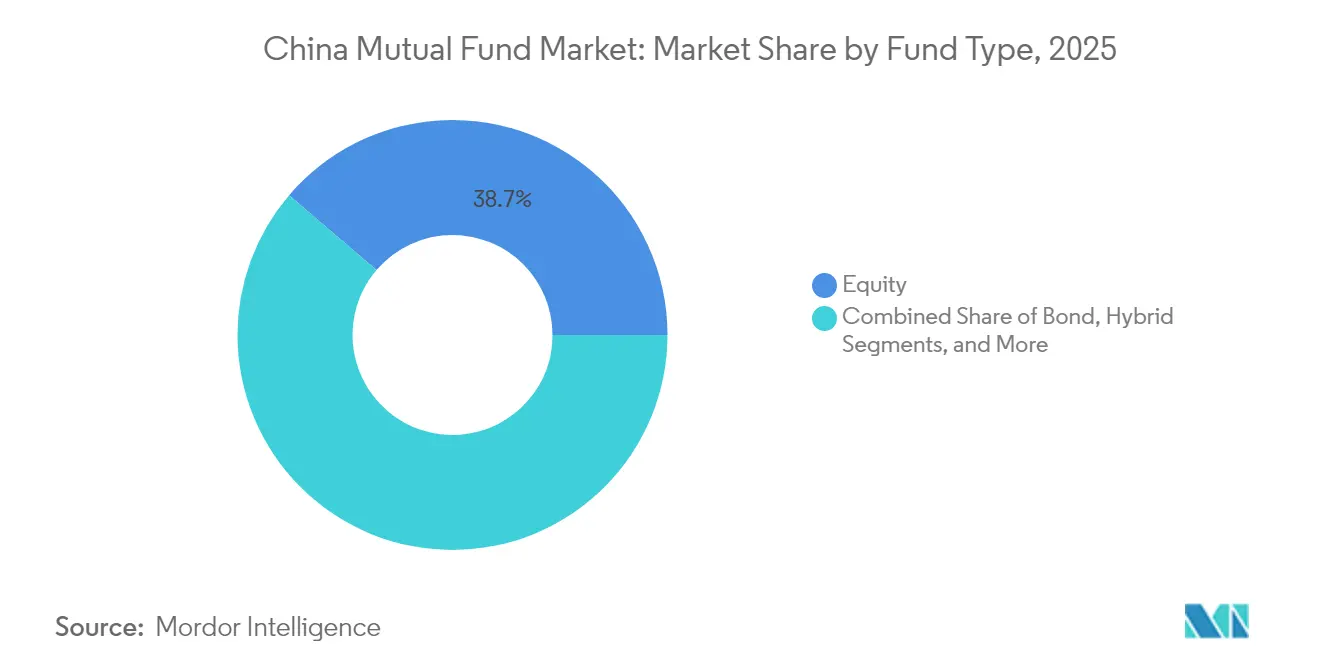

- By fund type, equity funds led with 38.74% of the China mutual fund market share in 2025 and are projected to record the fastest 8.25% CAGR to 2031.

- By investor type, retail participants held 58.35% of the China mutual fund market size in 2025 while also registering the highest 7.85% CAGR through 2031.

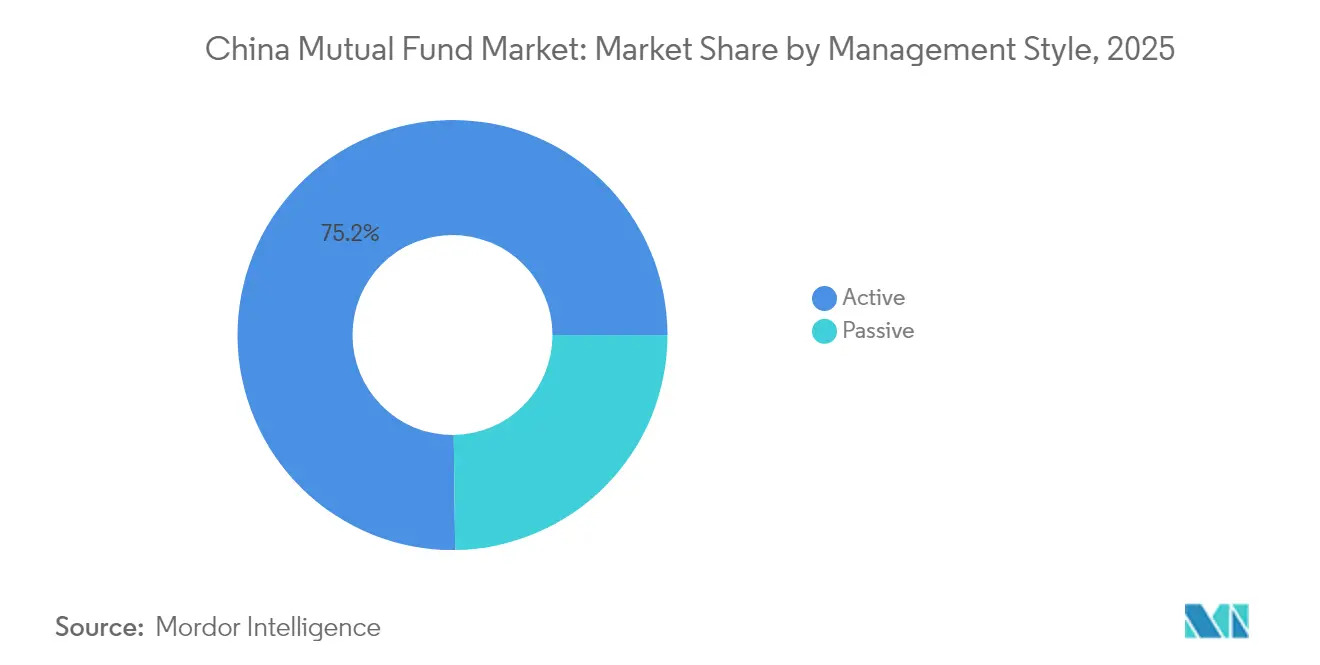

- By management style, active mandates controlled 75.20% share of the China mutual fund market in 2025, whereas passive strategies show the quickest 8.63% CAGR to 2031.

- By distribution channel, online trading platforms commanded 47.10% share of the China mutual fund market in 2025 and are expanding at a leading 9.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Mutual Fund Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising middle-class wealth & shift from deposits to investments | +2.1% | Nationwide; concentration in tier-1 and tier-2 cities | Medium term (2-4 years) |

| Private pension reform funneling assets | +1.8% | Nationwide; early adoption in pilot cities | Long term (≥ 4 years) |

| Regulatory liberalization for foreign-owned fund managers | +0.9% | Nationwide; focus on financial centres | Medium term (2-4 years) |

| Decline in bank WMP yields pushing flows to equity funds | +1.2% | Nationwide; all investor segments | Short term (≤ 2 years) |

| Super-app and robo-advisory micro-investing adoption | +0.7% | Nationwide; higher penetration among younger cohorts | Medium term (2-4 years) |

| Housing Provident Fund boosts household risk appetite | +0.6% | Nationwide; regional variations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Middle-Class Wealth & Shift from Deposits to Investments

Chinese banks cut long-term deposit rates by up to 45 basis points in 2025, lowering headline yields below 1% and prompting savers to reallocate cash into equity and hybrid funds. Growing disposable income among urban households reinforces this pivot, particularly in tier-2 cities where living costs remain moderate. Asset managers report brisk expansion in balanced-risk products that appeal to first-time investors seeking real-return potential. The withdrawal of many fixed-income certificates by large lenders hastened the flow of idle cash into low-threshold money-market and bond funds. Together, these shifts increase penetration of the China mutual fund market and diversify its asset mix.

Private Pension (3rd-Pillar) Reform Funneling Assets

Nationwide rollout of the private pension scheme in December 2024 opened accounts for more than 72.8 million workers, introducing a powerful pipeline of sticky capital[1]Government of China, “Notice on Expanding Private Pension Pilot Nationwide,” gov.cn. Annual tax-deductible contributions up to CNY 12,000 favor systematic investing and longer holding periods that align with mutual fund structures. Regulators authorized 85 equity index funds for pension menus, ensuring broad equity exposure and deepening liquidity across multiple benchmarks. Low early-stage contribution rates signal untapped growth once financial literacy programs take hold. Demographic pressure, with one-third of the population projected to be over 60 by 2035, underscores the urgency to cultivate funded retirement assets and cements the China mutual fund market as a key beneficiary.

Regulatory Liberalization for Foreign-Owned Fund Managers

Revised QFII rules removed local-entity requirements and broadened permissible strategies, inviting 832 overseas institutions to deploy fresh capital by Q1 2024. Wholly foreign-owned enterprises now compete directly in flagship ETF launches, increasing product variety and benchmarking standards. The 2024 Nationwide Negative List eliminated share-holding caps in manufacturing, encouraging sector-specific thematic funds. Enhanced beneficial-owner disclosures, effective November 2024, create transparency yet raise compliance costs that favor well-resourced entrants. Overall, liberalization injects global practices into the China mutual fund market and raises competitive intensity.

Decline in Bank WMP Yields Pushing Flows to Equity Funds

Wealth-management products returned a muted 2.65% in 2024, well below historical norms. Concurrent triple policy rate cuts compressed deposit yields, sharpening the relative attractiveness of equity mandates, where leading China A-share funds posted double-digit gains. Banks have rotated WMP portfolios toward bonds, yet this defensive shift offers limited upside compared with diversified equity funds. Money-market yields slipped in tandem, encouraging investors to extend duration and risk along the product spectrum. The search for higher returns, therefore, channels assets into the China mutual fund market, especially growth-oriented strategies.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High market volatility & policy uncertainty | -1.4% | Nationwide; pronounced in tier-1 cities | Short term (≤ 2 years) |

| Fee compression from dominance of money-market funds | -0.8% | Nationwide; all fund categories | Medium term (2-4 years) |

| Competitive pressure from low-cost ETFs & WM products | -0.6% | Nationwide; developed markets | Medium term (2-4 years) |

| Low retail financial literacy triggers redemption shocks | -0.9% | Nationwide; higher impact in lower-tier cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Market Volatility & Policy Uncertainty

Repeated bouts of price swings caused elevated fund liquidations in 2024, especially among thematic equity mandates. The MSCI China Index whipsawed investors despite a 34% year-end rally, nurturing redemption spikes and short holding periods. Regulatory messaging often changes at short notice, as seen in tighter reviews for outbound investment vehicles that rattled sentiment. Over 100 enforcement actions against securities firms in 2024 underscore a tougher supervisory stance. Geopolitical frictions remain a wildcard, limiting overseas interest in advanced-technology holdings and constraining flows into the China mutual fund market during stress events.

Fee Compression from Dominance of Money-Market Funds

Money-market products still account for a substantial asset base, yet charge management fees well below 0.30%, diluting industry revenues. The 2024 CSRC reforms capped equity-fund fees at 1.2% and set physical ETF fees at 0.15%, igniting a price war that erodes smaller firms’ margins. Trading commission caps now restrict funds to allocate no more than 15% of commissions back to brokers, slicing traditional rebates almost in half. Larger managers absorb these pressures through scale while niche players face consolidation or exit. Persistent yield compression in cash products further squeezes profitability, challenging sustainability for the fragmented cohort that populates the China mutual fund market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fund Type: Equity Dominance Drives Growth

Equity funds controlled 38.74% of the China mutual fund market in 2025 and are set to expand at an 8.25% CAGR over the forecast period, outpacing every other category. This leadership rests on persistent deposit-rate weakness and the rise of new benchmarks such as the CSI A50, which concentrate market interest in technology, consumption, and green energy exposures. Investors position for structural themes including artificial intelligence and energy transition, pushing assets into growth-tilted mandates and broad-based index trackers. Simultaneous increase in QDII quotas enables managers to embed overseas diversification within mixed-asset products, reinforcing equity uptake. Bond funds grow in tandem as monetary easing elevates fixed-income valuations and anchors balanced portfolios. Hybrid strategies remain popular stepping-stones for conservative savers migrating from cash. Meanwhile, money-market funds experience subdued inflows following the drop in seven-day yields to multi-year lows. Together, these trends deepen the China mutual fund market size of each fund type and recalibrate the asset mix toward risk-bearing products.

Technology ETFs capture headline flows, with ten CSI A50 tracker approvals ratifying a growing appetite for transparent low-cost instruments. Active stock-pickers still dominate absolute share through breadth of style and sector weightings, but passive adoption gains pace under fee pressure. ESG overlays become standard as authorities channel capital toward carbon-neutral projects. Managers also extend alternative investment capabilities, integrating commodity and private-market exposures permitted within the QDLP framework. Performance dispersion widens between skillful houses and laggards, encouraging retail investors to scrutinize track records. Consequently, competition among fund types intensifies, amplifying the strategic significance of scale and product innovation within the China mutual fund market.

By Investor Type: Retail Momentum Accelerates

Retail clients held 58.35% of the assets of the China mutual fund market in 2025 and show the fastest 7.85% CAGR through 2031, reflecting widening financial inclusion via mobile platforms. Low minimum subscriptions and automated payroll deductions for private pension accounts nurture disciplined long-term investing. Younger savers gravitate toward themed index funds bundled inside super-apps, marking a generational shift from property-centric wealth accumulation to diversified portfolios. Institutional investors enlarge positions in bond and quantitative mandates to meet asset-liability goals, yet growth lags behind retail due to mature penetration levels. The latest QDII quota increase provides endowments and insurers with greater foreign-asset headroom, boosting demand for global equity and fixed-income products. Concurrent regulatory scrutiny of local government financing exposures raises risk management thresholds for professional investors. In parallel, the rise of corporate annuity plans opens a stable channel of inflows for balanced and fixed-income offerings.

Retail geography broadens beyond coastal hubs as digital connectivity tightens the gap between metropolitan and inland regions, though education deficits persist in lower-tier cities. Investor-protection rules now require distributors to deploy suitability tests and portfolio-stress disclosures, strengthening market integrity. Mass-market acceptance of model-portfolio ETFs provides simplified entry points while shielding investors from single-stock concentration risk. Collectively, these shifts anchor robust expansion in the China mutual fund market size for both retail and institutional cohorts, yet the former remains the main growth lever over the forecast horizon.

By Management Style: Passive Gains Ground

Active mandates comprised 75.20% of assets of the China mutual fund market in 2025, yet the passive cohort is projected to rise at a 8.63% CAGR over the forecast period, fueled by fee transparency and benchmark innovation. New regulatory ceilings on active fees compress revenue premia and incentivize volume-led passive rollouts. Providers such as E Fund have slashed CSI 300 ETF fees to 0.15%, catalyzing record monthly creations. Launch of the ESG-screened CSI A50 enables passive vehicles to mirror flagship index exposure with responsible-investment credentials. Active managers pivot toward concentrated high-conviction strategies in technology and healthcare to justify pricing. They also leverage proprietary data sets and machine learning to sustain alpha, especially in semi-efficient small-cap segments.

Fee wars prompt consolidation as subscale houses struggle to amortize fixed costs. Tier-one firms capitalize on economies of scope by bundling index, smart-beta, and factor products across multiple wrappers. Portfolio transparency regimes that publish daily holdings heighten investor awareness and narrow information asymmetry. Market-making enhancements improve secondary-market liquidity for ETFs, reinforcing passive momentum. While active dominance persists, rising acceptance of buy-and-hold indexing reconfigures the competitive equilibrium inside the China mutual fund market.

By Distribution Channel: Digital Platforms Lead

Online platforms accounted for 47.10% of the China mutual fund market share in 2025 and are forecasted to compound at 9.95% annually to 2031. Frictionless account onboarding via biometric verification cuts processing time to minutes, lifting conversion rates. Super-apps integrate payments, messaging, and brokerage, driving cross-sell synergies and reducing acquisition costs. Banks retain a sizeable footprint, especially for conservative money-market products and payroll-linked pension sales, but ceded share as fee-sensitive clients migrated online. Securities firms focus on advisory-rich services for high-net-worth individuals and institutions, emphasizing customized portfolios that combine onshore and offshore assets. Independent financial advisers gain relevance in lower-tier cities where branch density is sparse yet smartphone penetration is high.

Regulators amplify disclosure standards for digital distributors, obliging layered risk warnings and gamification limits to curb speculative behavior. Robo-advisers deploy goal-based algorithms that rebalance ETF baskets, maintaining risk profiles despite market swings. Open-API frameworks allow fund houses to embed products across multiple ecosystems, diversifying origination channels. These developments collectively enlarge the China mutual fund market and set new benchmarks for customer experience.

Geography Analysis

China’s mutual fund landscape displays notable regional diversity, and usage patterns shift rapidly as digital connectivity rises. Tier-1 cities such as Beijing, Shanghai, and Shenzhen host the highest absolute asset pools due to concentrated wealth and established financial infrastructure. Yet the fastest uptake now emerges from provincial capitals and tier-3 urban clusters, where lower property burdens free disposable income for investment. Retail penetration deepens in southwestern provinces following accelerated 5G rollout that stabilizes mobile trading performance. Nationwide private pension availability catalyzes account openings even in historically under-banked regions, strengthening the China mutual fund market footprint.

Government policy fosters regional thematic interest; technology hubs gravitate toward semiconductor and AI funds while heavy-industry centers favor ESG-linked bond strategies that finance environmental upgrades. Cross-border demand surges uniformly after authorities expanded QDII headroom to USD 167.8 billion in June 2024. This quota uplift enables investors from coastal and interior provinces to access global equities via feeder funds, spreading diversification benefits. Local fiscal strains influence sentiment; provinces with elevated debt service ratios observe slower net inflows, prompting cautious portfolio structures.

Hong Kong remains the principal offshore conduit. Mainland-Hong Kong Mutual Recognition funnels mainland-domiciled funds to sophisticated overseas investors and channels foreign currency into A-share products. Several asset managers secured virtual licenses in Hong Kong to service global clients remotely, widening distribution beyond physical presence requirements. Approval for spot Bitcoin and Ethereum ETFs in the territory positions Chinese fund houses to capture digital-asset flows once cross-border regulatory bridges form. These location-specific dynamics collectively reinforce the national growth outlook for the China mutual fund market.

Competitive Landscape

Industry concentration is moderate: the top five players account for a major share of assets, while more than 150 smaller managers divide the balance. The 2025 merger of China Cinda, Dongfang Asset, and Great Wall Asset into sovereign wealth giant China Investment Corporation reshapes hierarchy and intensifies scale-based competition. Parallel brokerage consolidation between Guotai Junan and Haitong creates an enlarged distribution powerhouse able to cross-sell in-house funds across vast advisory networks.

Technology deployment is a critical success factor. E Fund applies big-data analytics and natural-language processing to filter sentiment signals, enhancing stock-selection edge. ChinaAMC integrates AI-driven compliance monitoring that flags suspicious trading in real time, reducing regulatory risk. Foreign players such as J.P. Morgan Asset Management accelerate local hiring to customize global strategies for domestic indices, yet confront operational costs tied to new beneficial-owner disclosure mandates. Fee compression compels houses to diversify revenue through wealth-management subsidiaries and retirement-solutions arms.

Product innovation defines competitive positioning. ESG and thematic ETFs aligned with national carbon-neutral goals attract policy support and marketing prominence. Managers race to bundle technology-themed funds covering robotics, cloud computing, and artificial intelligence, leveraging recent technology advances to fuel investor enthusiasm[3]ANTARA News Agency, “E Fund launches AI-focused ETFs amid tech rally,” antaranews.com. Large firms acquire boutique quant shops to secure algorithmic talent. Smaller houses seek niche differentiation in fixed-income specialties or cross-border feeder arrangements, yet balance-sheet constraints limit marketing reach. The convergence of regulation, digital disruption, and investor sophistication reinforces polarization between mega-scale incumbents and agile specialists within the China mutual fund market.

China Mutual Fund Industry Leaders

E Fund Management

China Asset Management Co. (ChinaAMC)

ICBC Credit Suisse Asset Management

Harvest Fund Management

Bosera Asset Management

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: China Investment Corporation finalized the integration of China Cinda, Dongfang Asset and Great Wall Asset, creating a sovereign vehicle with expanded asset-management capability.

- February 2025: Chinese insurers obtained an increased USD 39 billion overseas investment quota under QDII to counter low domestic yields.

- January 2025: E Fund Management released a suite of technology-focused ETFs covering artificial intelligence, robotics, and cloud computing; the E Fund CSI Artificial Intelligence ETF attracted strong inflows.

- December 2024: The Government extended the private pension scheme nationwide, giving over 1 billion employees access to 800-plus fund options.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the China mutual funds market as the combined assets under management (AUM) of all open-ended public funds domiciled in mainland China that pool money from retail or institutional investors and invest in listed securities, money-market instruments, or mixed allocations.

Scope Exclusion: Private placement funds, separately managed accounts, and funds domiciled in Hong Kong or overseas feeder structures sit outside this assessment.

Segmentation Overview

- By Fund Type

- Equity

- Bond

- Hybrid

- Money Market

- Others

- By Investor Type

- Retail

- Institutional

- By Management Style

- Active

- Passive

- By Distribution Channel

- Online Trading Platform

- Banks

- Securities Firm

- Others

Detailed Research Methodology and Data Validation

Desk Research

We build the foundation with national statistics from the Asset Management Association of China, China Securities Regulatory Commission disclosures, People's Bank of China monetary reports, International Investment Funds Association yearbooks, and policy papers from the OECD and IMF. Company 10-Ks, IPO prospectuses, and reputable financial press further flesh out competitive moves and product launches.

To cross-verify flows and balance-sheet data, analysts pull quarterly snapshots from D&B Hoovers for manager financials, Dow Jones Factiva for deal news, and Questel for product patent filings in fund-tech. These sources are illustrative; many additional publications support gap checks and clarifications.

Primary Research

Mordor analysts interview portfolio managers, custody banks, fintech platforms, and compliance officers across Beijing, Shanghai, Shenzhen, and Tier-2 cities. They then survey retail investors through online panels to validate adoption rates and fee sensitivity. Insights help us stress-test secondary findings and refine behavioral assumptions.

Market-Sizing & Forecasting

A top-down AUM reconstruction begins with monthly public-fund balances from AMAC, adjusted for RMB-USD moves, before being filtered through redemption patterns and preliminary 2024 audit statements. Select bottom-up roll-ups of leading managers' reported assets provide a reality check.

Key model inputs include new fund registrations, third-pillar pension inflows, average money-market yields versus deposit rates, ETF turnover growth, and digital-platform account openings. A multivariate regression links these drivers to historical AUM; scenarios are projected with exponential smoothing while expert consensus guides elasticity ranges.

Data Validation & Update Cycle

Outputs face three layers of analyst review; variance flags trigger re-runs, and we benchmark against independent liquidity, fee, and flow metrics. Mordor Intelligence refreshes the file annually, inserting interim updates if policy shifts or market shocks move fundamentals.

Why Mordor's China Mutual Funds Baseline Earns Investor Confidence

Published figures often differ because firms pick unequal scopes, FX cuts, and refresh cadences. Our disciplined inclusion of only on-shore public funds and our yearly RMB-USD harmonization keep the baseline steady yet current.

Key gap drivers stem from whether passive ETF pools, cross-border QDII quotas, or corporate wealth products are folded into totals and from how quickly each publisher rolls forward 2024 audit numbers.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.82 T (2025) | Mordor Intelligence | - |

| USD 4.90 T (2025) | Global Consultancy A | Counts ETF pools and corporate wealth products outside mutual-fund rules |

| USD 4.38 T (2024) | Industry Association B | Uses Oct-24 snapshot and excludes cross-border QDII funds; FX not updated |

The comparison shows that by selecting a consistent scope, applying dual-path modeling, and refreshing each year end, Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can readily trace and repeat.

Key Questions Answered in the Report

What is the current size of the China mutual fund market?

The China mutual fund market stands at USD 5.15 trillion in 2026 and is projected to reach USD 7.21 trillion by 2031.

Which fund type holds the largest share?

Equity funds led with 38.74% of the China mutual fund market share in 2025.

How fast are passive strategies growing?

Passive products, primarily ETFs, are expanding at a 8.63% CAGR through 2031 as fee competition intensifies.

Why are digital platforms important for distribution?

Online platforms already account for 47.10% of fund sales and are scaling at 9.95% CAGR because super-apps simplify account opening and cut costs.

How does the private pension reform influence the sector?

Nationwide private pension rollout channels new long-term assets into mutual funds, creating a structural driver that adds an estimated 1.8 percentage points to the forecast CAGR.

What main risks could slow market growth?

High market volatility, fee compression, and low investor literacy can trigger redemption waves and margin pressure, collectively subtracting up to 3.7 percentage points from growth forecasts.

Page last updated on: