Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

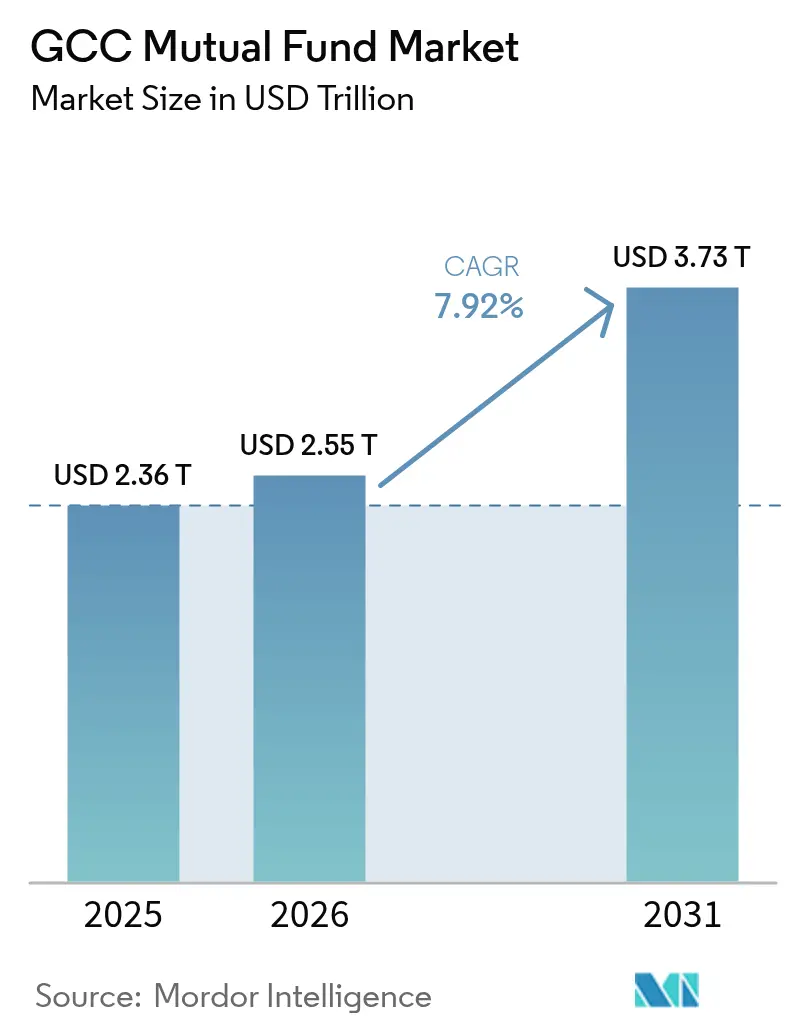

| Base Year Market Size (2025) | USD 2.36 Trillion |

| Market Size (2026) | USD 2.55 Trillion |

| Market Size (2031) | USD 3.73 Trillion |

| Growth Rate (2026 - 2031) | 7.92% CAGR |

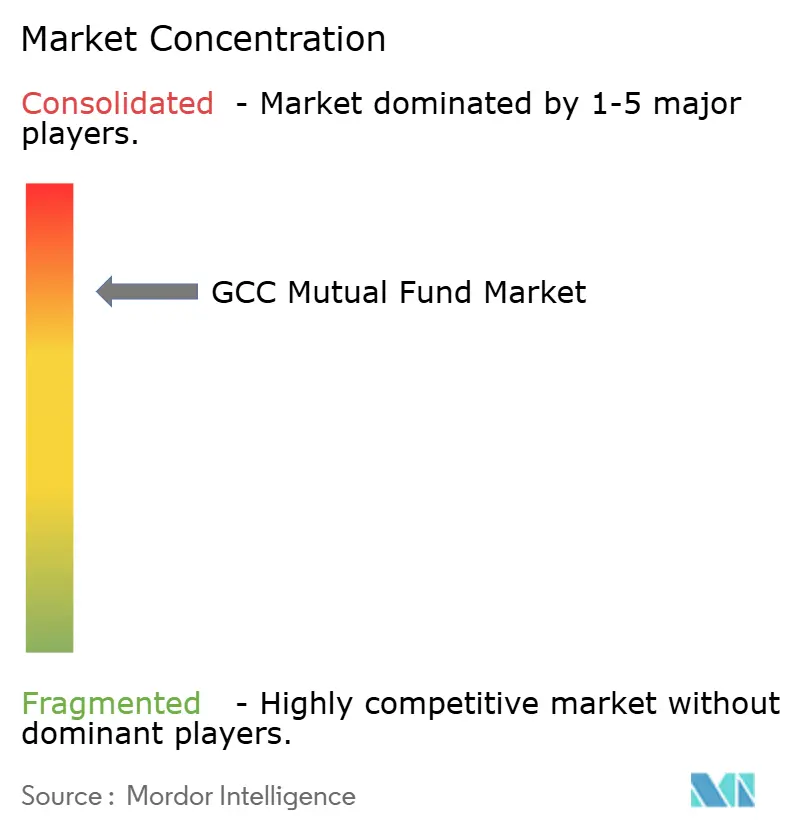

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Mutual Fund Market Analysis by Mordor Intelligence

The GCC mutual fund market size was valued at USD 2.36 trillion in 2025 and estimated to grow from USD 2.55 trillion in 2026 to reach USD 3.73 trillion by 2031, at a CAGR of 7.92% during the forecast period (2026-2031). Robust oil-revenue buffers accelerated economic diversification, and an expanding IPO pipeline are unlocking larger investable universes, while sovereign wealth funds seed local managers to deepen liquidity across public and private asset classes. Retail adoption is climbing as open-banking mandates and digital platforms lower onboarding frictions, and Sharia-compliant innovations align with regional investor preferences. Competitive intensity is rising as global firms establish onshore entities, prompting incumbents to invest in artificial-intelligence portfolio tools and fee-efficient share classes. The interplay of regulatory harmonization, cross-border settlement systems, and rising ESG mandates is expected to keep the GCC mutual fund market on a steady growth trajectory.

Key Report Takeaways

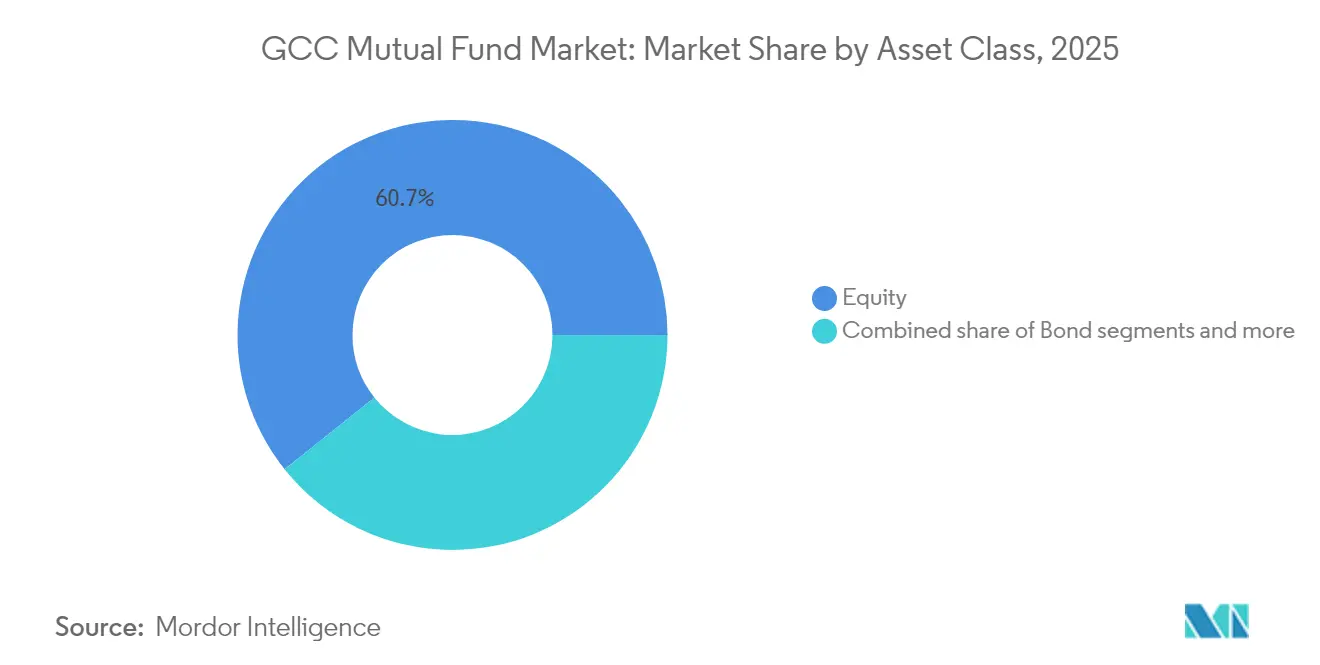

- By asset class, equity funds led with 60.73% of GCC mutual fund market share in 2025; bond and sukuk funds are forecast to expand at a 9.55% CAGR through 2031.

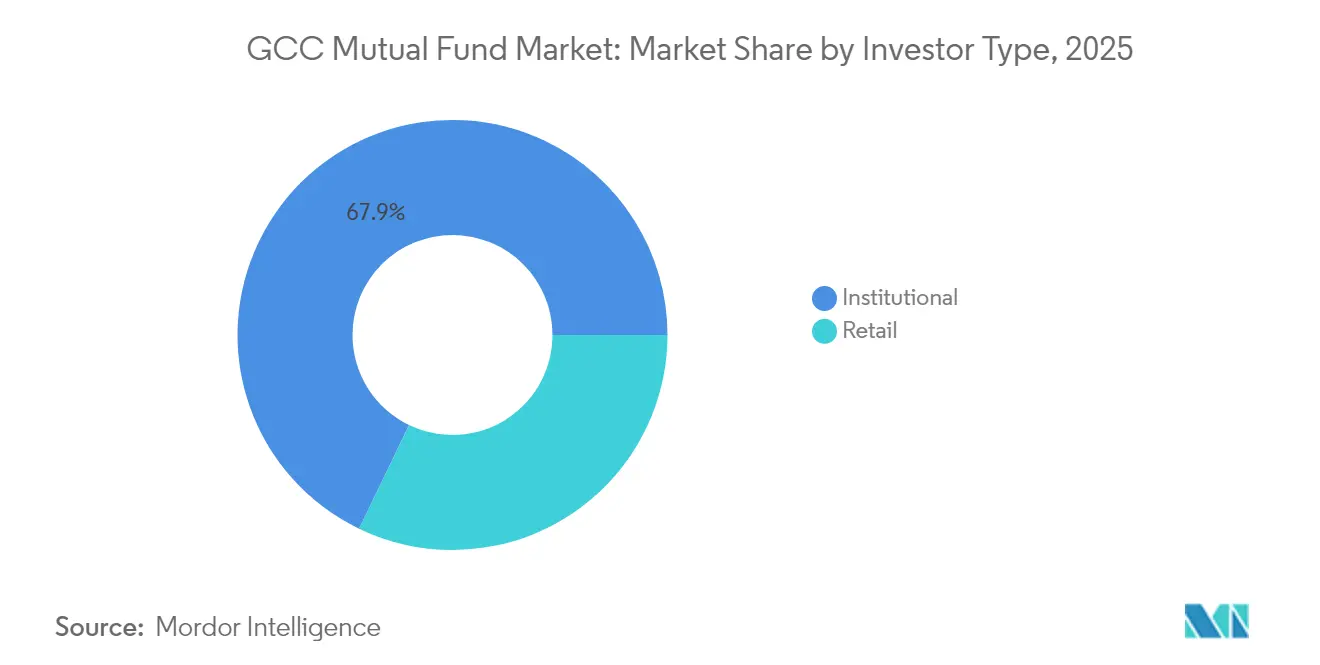

- By investor type, institutional investors held 67.85% of the GCC mutual fund market size in 2025, while the retail segment is advancing at an 8.62% CAGR to 2031.

- By distribution channel, banks captured 75.62% of the GCC mutual fund market share in 2025, whereas online platforms recorded the highest projected CAGR at 13.25% until 2031.

- By geography, Saudi Arabia commanded 75.10% of the GCC mutual fund market size in 2025; the UAE is growing fastest at 9.6% CAGR through 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

GCC Mutual Fund Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising IPO pipeline expanding investable universe | +1.2% | Saudi Arabia, UAE core with spillover to Qatar, Kuwait | Medium term (2-4 years) |

| Surge in Sharia-compliant savings products | +1.8% | GCC-wide, strongest in Saudi Arabia, UAE | Long term (≥ 4 years) |

| Sovereign debt issuance boosting fixed-income AUM | +1.5% | Saudi Arabia, UAE, Qatar primary markets | Medium term (2-4 years) |

| Open-banking rules widening retail access | +1.1% | UAE, Saudi Arabia early adoption, regional rollout | Short term (≤ 2 years) |

| SWF seeding of local fund managers | +0.9% | Saudi Arabia, UAE, Qatar sovereign-led initiatives | Long term (≥ 4 years) |

| High net-worth migration into GCC | +0.8% | UAE, Saudi Arabia primary destinations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising IPO Pipeline Expanding Investable Universe

Saudi Arabia's Tadawul exchange processed 32 new listings in 2024, while the UAE's exchanges added 18 companies, creating expanded opportunity sets for equity-focused mutual funds[1]Reuters Staff, “Saudi Aramco unit plans IPO to raise up to $2 bln,” reuters.com. . This pipeline expansion directly correlates with mutual fund AUM growth as managers gain access to previously unavailable sectors, including renewable energy, healthcare technology, and logistics infrastructure. The strategic implication extends beyond asset availability—new listings often carry higher volatility and information asymmetries that favor active management strategies over passive indexing. Regional exchanges are implementing fast-track listing procedures for qualifying companies, reducing time-to-market from 18 months to 8-12 months. Saudi Aramco's subsidiary IPO plans and similar large-scale listings create anchor opportunities for institutional fund strategies while providing retail funds with diversification beyond traditional banking and petrochemical exposures.

Surge in Sharia-Compliant Savings Products

Islamic finance assets in the GCC reached USD 1.8 trillion in 2024, with mutual fund products representing the fastest-growing segment within this universe[2]Islamic Financial Services Board, “Islamic Financial Services Industry Stability Report 2024,” ifsb.org. . Regulatory bodies, including Saudi Arabia's CMA and the UAE's SCA, have streamlined Sharia-compliant fund approval processes, reducing certification timelines from 6 months to 3 months while expanding eligible investment categories. The competitive advantage lies in demographic alignment—over 85% of GCC retail investors express preference for Sharia-compliant investment options, yet traditional product offerings have historically underserved this demand. Technology integration through platforms like Alpaca's partnership with ZAD enables automated Sharia screening and real-time compliance monitoring, reducing operational costs while improving investor confidence. Fund managers are developing hybrid structures that combine conventional investment strategies with Islamic principles, accessing broader institutional capital while maintaining religious compliance.

Sovereign Debt Issuance Boosting Fixed-Income AUM

GCC governments issued USD 89 billion in sovereign bonds and sukuk during 2024, with Saudi Arabia accounting for USD 31 billion and the UAE contributing USD 22 billion. This issuance expansion creates primary market opportunities for fixed-income mutual funds while establishing benchmark yield curves that support secondary market development. The strategic shift reflects fiscal diversification beyond oil revenues, with debt-to-GDP ratios remaining manageable across major GCC economies. Kuwait's recent debt law permitting KWD 30 billion (USD 97 billion) in borrowing over 50 years signals sustained issuance activity that will benefit bond fund strategies. Fixed-income funds are positioning for duration management opportunities as central banks navigate inflation pressures while maintaining currency pegs to the US dollar.

Open-Banking Rules Widening Retail Access

The UAE's Central Bank implemented comprehensive open banking regulations in 2024, requiring banks to provide API access for licensed fintech platforms, directly reducing customer acquisition costs for mutual fund distributors[3]Central Bank of the UAE, “Open Banking Regulations 2024,” centralbank.ae.. Saudi Arabia's SAMA followed with similar requirements, creating standardized data-sharing protocols that enable seamless account aggregation and investment onboarding. This regulatory shift eliminates traditional banking intermediation advantages, allowing specialized wealth management platforms to access customer financial data with consent. The competitive implication favors technology-enabled distributors over traditional branch networks, as customer onboarding times decrease from weeks to hours. Regulatory compliance frameworks ensure data security while promoting innovation, with successful implementations reducing distribution costs by 40-60% for digital-first fund platforms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fee compression from passive & robo advice | -1.4% | GCC-wide, strongest in UAE & Saudi Arabia | Short term (≤ 2 years) |

| Limited bond-market liquidity | -0.8% | Smaller GCC bond markets | Medium term (2-4 years) |

| Foreign-ownership caps on listed equities | -1.1% | Varies by country; most restrictive in Kuwait, Saudi Arabia | Medium term (2–4 years) |

| Compliance costs under evolving regulations | -0.9% | GCC-wide; particularly relevant in UAE and Bahrain | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fee Compression from Passive & Robo Advisers

Global ETF assets reached USD 14.64 trillion in Q1 2025, with expense ratios averaging 0.15% compared to 0.85% for actively managed mutual funds, creating sustained pressure on traditional fund management fee structures[4]Investment Company Institute, “Worldwide Regulated Open-End Fund Assets Q1 2025,” ici.org. . GCC-based robo-advisory platforms including Sarwa and Wahed Invest, are expanding automated portfolio management services with fees below 0.50%, forcing traditional managers to justify premium pricing through alpha generation or specialized services. The strategic response involves product differentiation through alternative asset classes, private market access, and enhanced advisory services that justify higher fee structures. Deloitte's 2025 Investment Management Outlook identifies actively managed ETFs as a growing compromise solution, combining cost efficiency with active management strategies. Regional fund managers are exploring outcome-based fee structures and performance-linked pricing to maintain margins while competing with passive alternatives.

Limited Secondary-Market Liquidity in GCC Bonds

GCC corporate bond markets exhibit average daily trading volumes below USD 50 million compared to USD 2 billion in developed markets, constraining active management strategies and increasing tracking error risks for bond funds. This liquidity constraint particularly affects smaller GCC states where government bond issuance remains sporadic and corporate credit markets lack depth. Fund managers face elevated bid-ask spreads and position-sizing limitations that reduce portfolio optimization capabilities while increasing transaction costs. The regulatory response includes market-making incentive programs and electronic trading platform development, though implementation timelines extend beyond 2027 for meaningful impact. Bahrain's debt-to-GDP ratio exceeding 130% creates additional credit risk considerations that compound liquidity challenges for funds with significant Bahraini exposure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Asset Class: Equity Dominance Faces Sukuk Momentum

Equity funds held 60.73% of % GCC mutual fund market share in 2025 as buoyant IPO activity and index inclusions propelled allocations. Bond and sukuk vehicles, however, are growing fastest at a 9.55% CAGR, lifting their slice of the GCC mutual fund market size alongside sovereign issuance growth. In the near term, money-market strategies provide liquidity management tools for institutions, while hybrid balanced funds capture risk-averse retail inflows. Over the outlook horizon, alternative structures such as REITs and private-credit funds should diversify revenue streams for asset managers eager to escape fee compression threats. Premia Partners’ BOCHK Saudi Government Sukuk ETF launch in July 2025 offered passive access to local sovereign Islamic bonds. Goldman Sachs followed with sector-specific GCC ETFs targeting healthcare and technology exposures. Regulatory reforms in Saudi Arabia shortened approval processes, unlocking innovative structures that blend passive baskets with Islamic screens. Collectively, these dynamics support asset-class breadth, enhancing portfolio-construction flexibilities for the GCC mutual fund market.

By Investor Type: Institutional Command With Retail Acceleration

Institutional investors controlled 67.85% of the GCC mutual fund market size in 2025, benefiting from pension, insurance, and sovereign allocations. Retail segments are expanding at an 8.62% CAGR, fueled by digital onboarding and wealth-migration inflows. Family offices increasingly blend direct investments with commingled funds to fine-tune tactical exposures while preserving governance control. Regulators in Saudi Arabia have refined investor-classification rules, widening access to sophisticated funds without compromising suitability safeguards. High-net-worth migration, supported by the UAE golden visa and Saudi Premium Residency programs, injects fresh capital into regional wealth-management channels. Digital advisors capitalize on this trend by delivering curated portfolios through multi-language interfaces and automated compliance checks. The resulting demographic diversification amplifies product-development opportunities and sustains demand resilience across the GCC mutual fund market.

By Distribution Channel: Bank Supremacy Meets Digital Disruption

Banks distributed 75.62% of GCC mutual fund market share in 2025, relying on entrenched client relationships and integrated financial-planning services. Yet online platforms are on track for 13.25% CAGR, compressing acquisition costs and democratizing access. Financial advisors retain a niche among affluent clients seeking personalized guidance. Direct-to-customer channels remain embryonic but show promise as managers develop proprietary portals to sidestep intermediary fees and deliver richer investor analytics. Kristal. AI’s 2024 UAE entry demonstrates how algorithm-driven allocation and fractional investing can erode traditional bank moats. Major banks counter with omnichannel experiences that integrate robo modules alongside human advice. Regulators enforce uniform suitability and disclosure standards, leveling the competitive field while protecting investors within the GCC mutual fund market.

Geography Analysis

Saudi Arabia dominates with 75.10% market share in 2025, supported by the Kingdom's Vision 2030 economic diversification initiatives and expanding capital market depth. The Saudi stock exchange's inclusion in MSCI and FTSE indices has attracted international institutional flows that benefit local fund management companies through increased assets under management and fee generation. The UAE captures the fastest growth at 9.6% CAGR through 2031, driven by Abu Dhabi Global Market's regulatory innovations and Dubai International Financial Centre's expanding fund management ecosystem. Qatar, Kuwait, Oman, and Bahrain collectively represent approximately 15% market share, with varying growth trajectories based on regulatory development and economic diversification progress.

JPMorgan's reclassification of Qatar and Kuwait as developed markets in February 2025 signals institutional recognition of regulatory and market infrastructure improvements that should attract additional international fund flows. Kuwait's recent political and regulatory reforms, including the dissolution of parliament and implementation of comprehensive legal frameworks, have driven stock market gains exceeding 10% year-to-date while positioning the country for expanded mutual fund activity. The AFAQ payment system's implementation across GCC countries is reducing cross-border transaction costs and settlement times, facilitating regional fund distribution and portfolio diversification strategies.

Competitive Landscape

The GCC mutual fund market is characterized by a high level of concentration, where a small group of players controls most assets under management. This concentration creates an oligopolistic environment that benefits firms with greater scale, stronger compliance infrastructure, and extensive distribution networks. Leading Saudi-based asset managers such as SNB Capital, Riyad Capital, and Al Rajhi Capital leverage their affiliations with major banks to maintain dominant positions. In the UAE, players like Emirates NBD Asset Management and SHUAA Capital have adopted regional growth strategies and cross-border offerings to remain competitive. Across the market, firms are focusing on Sharia-compliant product innovation, expanding into alternative asset classes, and enhancing digital distribution capabilities. These efforts help justify higher fee models and provide differentiation from low-cost passive investment options.

Technology is becoming the central axis of competition, as asset managers increasingly adopt AI tools and automation to optimize operations. Advanced systems for portfolio construction, compliance oversight, and investor engagement are being deployed to reduce costs while enhancing service quality. This tech-driven shift is essential to staying competitive in a market where investor expectations around speed, transparency, and customization continue to rise. At the same time, regulatory changes are easing regional expansion, creating openings for cross-border fund distribution and the launch of niche investment strategies. Areas like private credit and ESG-themed products offer new growth avenues for firms willing to innovate. The market is also seeing movement toward blockchain integration, as demonstrated by the ADGM-Chainlink collaboration to develop tokenization frameworks for fund operations.

A new wave of disruptors is gaining traction by offering digital-first, Sharia-compliant investment services that appeal to retail investors. Fintech platforms like Sarwa and Wahed Invest are combining robo-advisory models with religiously aligned investment strategies to deliver affordable and accessible wealth management solutions. These platforms are successfully targeting younger, tech-savvy demographics through strong mobile interfaces, low fees, and transparent offerings. Their rise signals a shift in market dynamics, where traditional players must evolve to retain relevance among a diversifying investor base. The increasing sophistication of these challengers is also driving incumbents to accelerate their own digital transformation agendas. As the market evolves, firms with both technological agility and deep regulatory understanding will be best positioned to lead.

GCC Mutual Fund Industry Leaders

SNB Capital

Riyad Capital

Al Rajhi Capital

Emirates NBD Asset Management

SHUAA Capital

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Saudi Capital Market Authority published updated Investment Funds Regulations, streamlining approval processes for innovative fund structures and reducing regulatory compliance timelines from 6 months to 3 months. The reforms enable faster product launches while maintaining investor protection standards, particularly benefiting alternative asset and ESG-focused fund strategies.

- July 2025: Premia Partners launched the BOCHK Saudi Arabia Government Sukuk ETF on Saudi Exchange, providing the first passive exposure to Saudi sovereign Islamic bonds. The ETF addresses institutional demand for liquid Sharia-compliant fixed-income exposure while establishing benchmark pricing for the broader sukuk market.

- June 2025: The Investment Company Institute reported that global regulated open-end fund assets reached USD 74.45 trillion in Q1 2025, with ETFs accounting for USD 14.64 trillion and continuing to attract net inflows at the expense of traditional mutual funds. The data underscores fee compression pressures facing GCC fund managers.

- March 2025: Seviora, Temasek's asset management unit, established Abu Dhabi Global Market office following co-investment activities with Mubadala, signaling increased international asset manager interest in UAE-based operations and regional fund distribution strategies.

GCC Mutual Fund Market Report Scope

An understanding of the GCC mutual fund industry, regulatory environment, MF companies, and their business models, along with detailed market segmentation, product types, current market trends, changes in market dynamics, and growth opportunities. In-depth analysis of the market size and forecast for the various segments. The GCC Mutual Fund Industry is Segmented Based on the Fund Category (Equity, Money Market, Real Estate, and Other (Bonds, Commodities, Mixed)) and by Geography (Saudi Arabia, Qatar, Kuwait, Abu Dhabi, and Dubai). The report offers Market size and forecasts for the GCC Mutual Fund Market in value (USD) for all the above segments.

By Asset Class

| Equity |

| Bond |

| Hybrid |

| Money Market |

| Others |

By Investor Type

| Retail |

| Institutional |

By Distribution Channel

| Banks |

| Online Platforms |

| Financial Advisors |

| Direct |

By Geography

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Oman |

| Bahrain |

| By Asset Class | Equity |

| Bond | |

| Hybrid | |

| Money Market | |

| Others | |

| By Investor Type | Retail |

| Institutional | |

| By Distribution Channel | Banks |

| Online Platforms | |

| Financial Advisors | |

| Direct | |

| By Geography | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Oman | |

| Bahrain |

Key Questions Answered in the Report

How large is the GCC mutual fund market in 2026?

It is valued at USD 2.55 trillion and is expected to reach USD 3.73 trillion by 2031, reflecting a 7.92% CAGR.

Which asset class holds the biggest slice of mutual fund assets in the Gulf?

Equity funds lead with 60.73% GCC mutual fund market share in 2025.

Which Gulf country grows fastest for mutual fund assets?

The UAE posts the highest forecast growth at a 9.6% CAGR through 2031.

What is driving retail participation in GCC mutual funds?

Open-banking regulations and digital platforms that cut onboarding times and minimum investment thresholds.

What new regulations are easing fund launches in Saudi Arabia?

July 2025 CMA reforms trimmed approval timelines for innovative structures to three months, fostering faster product rollouts.

Page last updated on: