Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

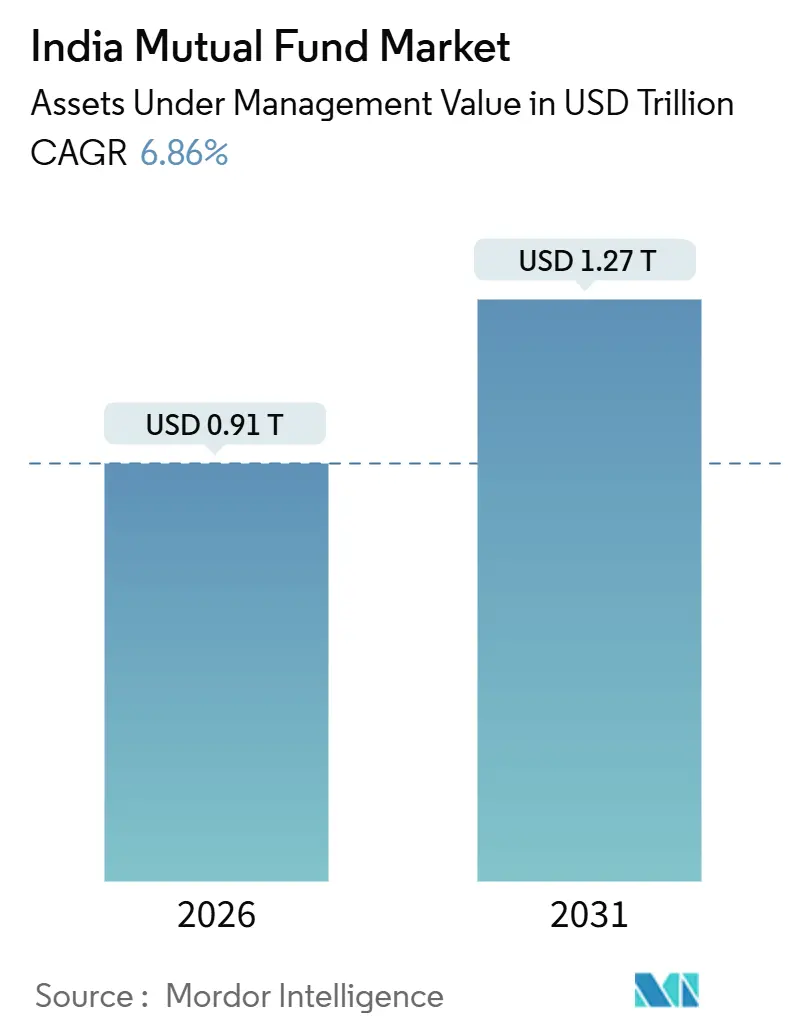

| Market Size (2026) | USD 0.91 Trillion |

| Market Size (2031) | USD 1.27 Trillion |

| Growth Rate (2026 - 2031) | 6.86% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Mutual Fund Market Analysis by Mordor Intelligence

The India Mutual Fund market size stands at USD 0.91 trillion in 2026 and is forecast to reach USD 1.27 trillion by 2031, expanding at a CAGR of 6.86%. The expansion path reflects a normalization from the outsized gains recorded through 2025 as mark-to-market effects fade and flows settle into more disciplined patterns that rely on recurring contributions rather than one-off lump sums. The India Mutual Fund Market continues to benefit from broadening retail participation and digital onboarding that lower entry barriers while improving transaction speed and transparency. Regulatory upgrades to cost disclosure and cyber resilience shift the industry toward clearer fee structures and stronger controls, which support investor confidence and compress unnecessary frictional costs. Passive products gain share on the back of simpler pricing and product clarity, while active managers retain an advantage in segments that reward research depth and liquidity management. Access is more democratic than before, as unique investor accounts increase and beyond the top 30 locations carry a larger slice of industry assets after several years of targeted outreach and digital payments ubiquity.

Key Report Takeaways

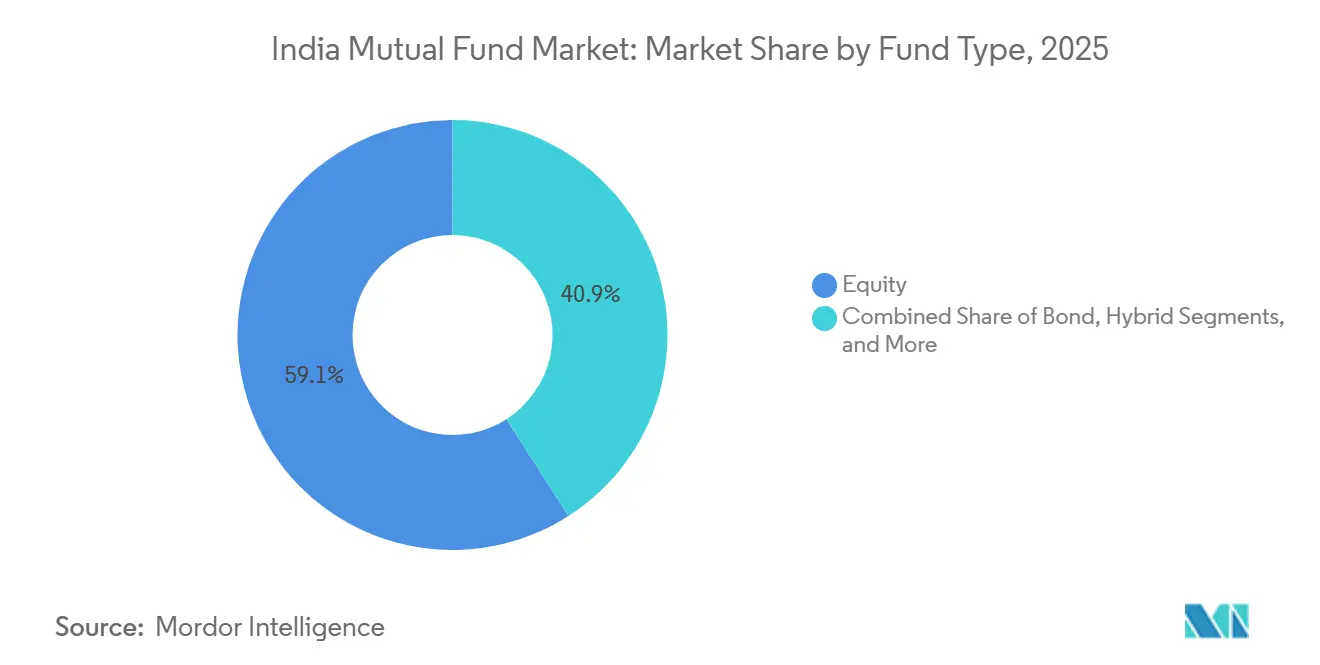

- By fund type, equity led with 59.08% of the India Mutual Fund market share in 2025, while equity is forecasted to expand at an 8.14% CAGR through 2031.

- By investor type, retail commanded 60.39% of the India Mutual Fund market size in 2025, while retail is projected to grow at a 7.36% CAGR through 2031.

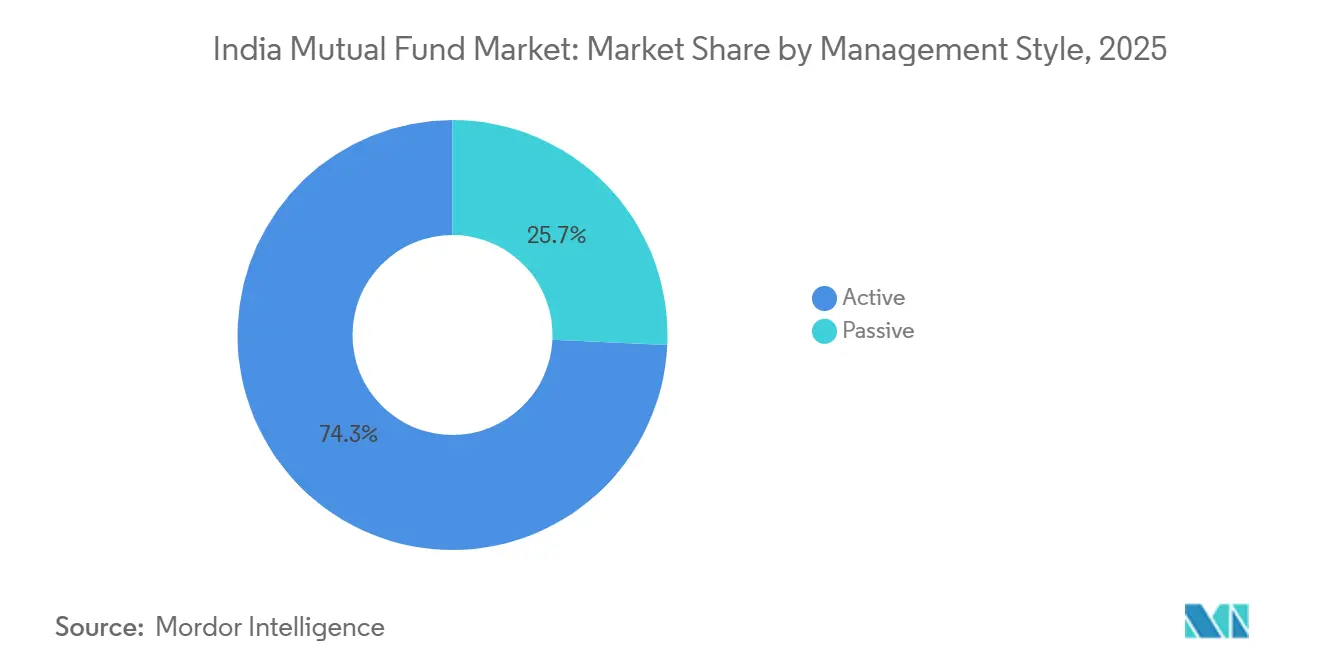

- By management style, active funds held 74.26% of the India Mutual Fund market size in 2025, while passive strategies are the fastest growing at an 8.61% CAGR to 2031.

- By distribution channel, online trading platforms captured 33.42% of the India Mutual Fund market size in 2025, while online platforms are projected to expand at a 9.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Mutual Fund Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising retail participation via SIPs | +1.8% | National, with concentration in metros and rapid spillover to Tier-2/3 cities | Medium term (2-4 years) |

| Rapid digital distribution via fintech & RIA platforms | +1.2% | National, accelerated adoption in Maharashtra, Karnataka, Gujarat, and Tamil Nadu | Short term (≤ 2 years) |

| Favourable tax incentives for equity funds | +0.7% | National, disproportionate benefit to salaried urban households | Long term (≥ 4 years) |

| Regulatory push for transparency & lower costs | +0.9% | National, compliance-driven across all AMCs | Medium term (2-4 years) |

| Shift of pension assets to long-duration debt schemes | +0.6% | National, driven by EPFO and NPS allocation policies | Long term (≥ 4 years) |

| L14: Micro-SIPs through UPI in Tier-3/4 towns | +0.5% | National, concentrated in large Hindi belt states with spillover to rural pockets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Retail Participation via SIPs

Recurring contributions remain the steady backbone of equity inflows, and they held firm even when price volatility picked up during parts of 2025 by smoothing allocation over time and reducing timing risk for new investors. SIP-driven flows have become more prominent within total equity inflows as distributors emphasize rupee cost averaging and long-horizon discipline over one-time deployments. The investor base expanded as new accounts were opened across more locations, with digital KYC and simple mandate registration making it easier to start or scale monthly contributions without paperwork. AMFI’s outreach and disclosures helped keep engagement high during corrections since investors could track scheme behaviour and relative performance on standardized risk and return metrics. The India Mutual Funds Market now carries a larger foundation of long-tenure retail folios that tend to persist through cycles, which supports steadier net inflows even when valuations consolidate.

Rapid Digital Distribution via Fintech & RIA Platforms

Digital channels do most transactions for the India Mutual Fund Market as fintech platforms, AMC apps, and broker ecosystems cut onboarding time and make SIP set-up a short, guided process. AMC case studies show that a very high share of new purchase transactions moved online by fiscal 2026, reflecting the maturing role of Aadhaar-based KYC, DigiLocker, and UPI autopay in account opening and mandate execution. Digital rails also broaden reach beyond metros as vernacular interfaces and lightweight applications gain traction in Tier-2 and Tier-3 cities, closing the distribution gap with low-cost direct plans and standardized disclosures. Exchanges support this shift with industry platforms that give distributors and investors an electronic gateway to transact and monitor holdings across AMCs in a single dashboard. Large AMCs report a high digital share of new SIP originations and purchases, which underlines how the India Mutual Fund Market continues to digitize both front-end acquisition and mid-office processes.

Regulatory Push for Transparency & Lower Costs

SEBI’s new framework for 2026 introduces base expense ratio caps, unbundles statutory charges from capped fees, and tightens brokerage limits, which together reduce opaque costs and improve apples-to-apples comparisons for investors [1]Upstox, “SEBI Mutual Funds Regulations 2026 Highlights,” Upstox, upstox.com. The rules also address redemption-linked pricing and past incentives, and they bring price discipline to execution costs that had varied across cash and derivatives transactions. On the operational side, SEBI’s Cybersecurity and Cyber Resilience Framework sets baselines on security operations and recovery objectives, including red teaming and data localization that extend to service providers in the ecosystem. [2]Securities and Exchange Board of India, “Frequently Asked Questions on Cybersecurity and Cyber Resilience Framework,” SEBI, sebi.gov.in These changes lift the compliance bar while standardizing disclosures so investors can see fee components and incident-handling readiness more clearly across comparable funds. The India Mutual Fund Market experiences a net effect of stronger cost discipline and more robust controls, which help maintain trust and compress administrative drag on investor returns.

Shift of Pension Assets to Long-Duration Debt Schemes

Large retirement pools allocate sizable shares to long-duration fixed income, and that supports liquidity and depth for select debt strategies managed by leading AMCs. The EPFO’s equity exposure via ETFs complements an underlying core allocation to government and high-grade corporate paper that continues to be intermediated by mutual funds in specific mandates. The growth of NPS participation sustains steady flows into long-duration bonds in line with conservative defaults and risk-calibrated models under the regulator’s framework for retirement saving. Corporate treasuries and affluent households also leaned into debt schemes when equity volatility rose during 2025, which increased the relevance of duration management and liquidity in fixed income portfolios run by AMCs. The India Mutual Fund Market benefits structurally as this pool of institutional-grade demand underwrites product development and scale advantages in fixed income that retail investors can access at low cost.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Equity-market valuation volatility is deterring inflows | -1.1% | National, most acute in mid-cap and small-cap segments | Short term (≤ 2 years) |

| SEBI caps on total-expense ratios squeeze margins | -0.4% | National, AMCs with high operational overheads face steeper margin pressure | Medium term (2-4 years) |

| Liquidity stress in small-cap funds requires buffers | -0.6% | National, concentrated risk in schemes with large AUM | Short term (≤ 2 years) |

| Heightened cybersecurity & data privacy risks | -0.3% | National, higher compliance burden for large AMCs and custodians | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Liquidity Stress in Small-Cap Funds Requires Buffers

Stress tests highlighted how liquidity can concentrate in small-cap schemes with larger asset bases, which requires explicit buffers and dynamic rebalancing to protect investors during sharp redemptions. AMFI and AMCs introduced measures such as cash cushions and SIP size caps during stress phases so portfolios can meet outflows without undue market impact [3]Bajaj Finserv Asset Management, “How market crashes impact mutual fund investors,” Bajaj AMC, bajajamc.com. Portfolios diversified into a mix of large, mid, and small-cap positions and kept a small cash allocation that could be tapped for redemptions, while turnover and execution costs were carefully managed. The India Mutual Fund Market adopted these practices in response to measured regulatory prompts and disclosed stress metrics more frequently to ensure transparency for investors tracking liquidity risk. The underlying challenge remains market depth in the least liquid counters, which is why long-hold SIP participation is favoured over large one-time inflows in these categories.

Heightened Cyber-Security & Data-Privacy Risks

SEBI’s cybersecurity framework is now embedded in operating requirements for AMCs and their service partners, and it raises the bar for detection, response, and recovery across critical systems. The framework includes clear expectations on recovery objectives, data sovereignty, and periodic red teaming as part of a structured approach to manage risks from evolving threat vectors. Industry utilities have adjusted data-sharing flows so that consent is unambiguous and access is routed through standardized frameworks for privacy and security. The India Mutual Fund Market is allocating more resources to cybersecurity and vendor assessments because accountability extends to outsourced providers under the regulator’s expectations. Over time, better controls and clearer consent mechanisms should support continued digital adoption without eroding trust in data handling and service continuity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fund Type: Equity Dominance Persists Amid Passive Gains

Equity-oriented funds held 59.08% of total industry assets in 2025 and are projected to grow at an 8.14% annual rate through 2031, which places them ahead of the overall India Mutual Fund Market pace. The mutual fund industry size in India remains anchored by equity because systematic investing structures and broader participation support continued net inflows even during valuation resets. Debt schemes benefited in 2025 when price volatility pushed allocators to stable coupon income and duration strategies managed by established AMCs with deep fixed income teams. Hybrid categories captured flows from investors who prefer diversified exposure inside a single scheme, and that includes arbitrage funds that used spread opportunities when markets were choppy. Passive baskets expanded within the “Others” grouping as commodity ETFs and index replicators attracted cost-sensitive investors who prefer simple, rules-based products under tighter expense caps.

Within equities, category share shifted with cycle conditions as flexi-cap and large-cap styles saw stronger inflows where broader liquidity was available, while small and mid-caps required tighter risk controls during late-2024 and 2025 corrections. Debt categories drew institutional allocations tied to pension and treasury demand, which stabilized flows and underpinned steady AUM growth across long-duration and high-quality credit schemes. Hybrid funds posted consistent growth because they simplify asset allocation for households that want automatic rebalancing and a mix of return sources under changing market conditions. Passive equity funds and ETFs benefited from lower base expense ratios as the 2026 rules took effect, which increases their long-term appeal as building blocks in diversified portfolios. Overall, the India Mutual Fund Market maintains a barbell of active alpha in less efficient segments and passive beta in broader exposures that complement household and institutional objectives.

By Investor Type: Retail Ascendancy Reshapes Flow Dynamics

Retail held 60.39% of total assets in 2025 and is slated to grow at 7.36% through 2031, which signals lasting household participation in the India Mutual Fund Market. The India Mutual Fund industry deepened its reach in 2025 as investor education and SIP-led onboarding brought in consistent contributions across age groups and income cohorts. Institutional allocators kept a stable presence through provident, pension, and treasury flows that support depth in debt categories and strategic exposure to beta through ETFs. The retail mix leaned toward equity and hybrid schemes for long-term goals, while institutions focused on liquidity, duration, and execution in fixed income aligned with policy and risk frameworks. The India Mutual Fund Market now serves a broader base of first-time investors through digital channels and a maturing group of experienced households that fine-tune allocations as objectives evolve.

Within the retail segment, SIP structures are the entry point for most households, and they reduce sensitivity to short-term swings in prices by spreading buys across cycles. As product disclosures, risk meters, and benchmarking get more standardized, households compare schemes on risk-adjusted returns rather than marketing claims, which improves decision quality. Institutions continue to shape flows in debt funds and ETF demand that anchors the passive ecosystem, especially as asset-liability frameworks for retirement schemes drive the need for predictable exposure. AMC reports show strong growth in digital onboarding within retail, with a high share of new SIPs and purchases originating through mobile and web channels in fiscal 2025 and 2026. This two-speed pattern, where institutions set the tone in fixed income and retail powers equity flows, is now a defining feature of the India Mutual Fund Market across cycles.

By Management Style: Active Retains Market Share as Passive Gains Velocity

Active funds held 74.26% of assets in 2025, while passive strategies built momentum from a lower base with an 8.61% projected growth rate to 2031, and that divergence shows the current mix of alpha-seeking and beta-building allocations. Passive ETFs and index funds expanded as base expense caps tightened and disclosures became more comparable across categories ahead of the 2026 implementation timeline. Commodity ETFs grew quickly within passive as investors adopted hedging exposures in simplified wrappers that trade through exchange accounts and standard settlement cycles. The India Mutual Fund Market still relies on active managers in segments with uneven liquidity and higher dispersion, where research depth and execution quality can add value over broad benchmarks. The outcome is a blended approach where passive serves as low-cost core exposure and active allocations target areas with potential for consistent excess returns over a full cycle.

As expense transparency improves, investors evaluate whether a given category is better served by passive exposure or by an active fund that demonstrates repeatable skill, sensible capacity, and clear liquidity practices. AMC performance reporting and standardized risk disclosures support that evaluation by clarifying volatility, drawdowns, and benchmark-relative returns through time. Passive adoption also benefits from distribution through brokerage apps and exchange-linked platforms that let investors consolidate holdings with other securities under unified credentials. Active funds continue to attract flows where bottom-up work and liquidity-aware execution can drive outcomes in categories that do not lend themselves to commoditized replication. This balance underpins the India Mutual Fund Market’s diversity of investment styles, which helps match products to different time horizons and risk preferences.

By Distribution Channel: Online Platforms Disrupt Traditional Intermediaries

L32: Online trading platforms held a 33.42% share of distribution in 2025 and are projected to grow at 9.22% through 2031, which signals a durable shift in how investors access the India Mutual Fund Market. AMCs report that nearly all purchase transactions are now executed digitally for select fund houses, and that shift came with accelerated onboarding speed and lower costs to serve. Exchange-backed transaction platforms enable distributors and investors to place orders across many AMCs from a single interface, which streamlines execution and portfolio tracking. Major AMCs show that digital share in new SIP originations and purchases crosses a strong majority, and that confirms the distribution pivot to mobile- and web-first journeys. The size of mutual fund industry in India, therefore, continues to expand alongside digital channels as investors adopt direct plans and standardized disclosure formats that fit self-directed and assisted journeys.

Traditional bank-led and IFA-led channels still play an important role for affluent clients and lump-sum placements that require guided conversations on taxes, asset location, and rebalancing. Securities firms use brokerage apps to cross-sell mutual funds into existing investor bases where KYC is pre-verified, and payment rails are already set, which also aids ETF adoption within demat ecosystems. National and regional distributors maintain reach in towns and districts where physical presence builds trust, even as they lean on digital mid-office tools for servicing. The India Mutual Fund Market is converging on a hybrid distribution model where high-touch advisory and low-cost execution coexist under clearer rules and higher cybersecurity standards. Over time, tightened BER caps and disclosure norms should keep pushing execution toward digital channels while advice differentiates on planning, behaviour coaching, and complex needs.

Geography Analysis

The India Mutual Fund Market remains concentrated in the top 30 cities, which accounted for a significant majority of AUM in 2025, while the share of locations beyond the top 30 continued to climb after a multi-year push on digital rails and outreach. B30 assets posted faster growth than the national average during fiscal 2019 to 2025, and that trajectory reflects rising participation in state capitals and district hubs where banking and mobile connectivity scaled up in tandem. Payment adoption helped close the collection gap for SIP mandates as UPI and standardized KYC reduced onboarding time and manual paperwork that had limited reach in the past. As investor education content is localized into regional languages, mutual funds became more approachable for first-time buyers in Tier-2 and Tier-3 cities who value predictability and consistent contributions for long-term goals. These developments support the India Mutual Fund Market’s steady broadening beyond historical core metros, even as the largest cities still drive the direction of flows and performance in aggregate.

Metros like Mumbai, Delhi NCR, Bengaluru, and Hyderabad continue to lead by asset share because they host corporate treasuries, high-income cohorts, and institutional allocators that transact larger tickets and diversify across categories, including passive. Ahmedabad and other Gujarat hubs contribute a growing share as entrepreneurs and family businesses incorporate mutual fund allocations alongside traditional bank deposits and securities holdings. Chennai and Pune reflect different investor mixes across manufacturing and information services, which shows how local industry composition shapes the tilt toward debt, hybrid, or equity categories. AMC branch networks and distributor density remain highest in metro clusters, yet most new account originations now flow through digital channels even where branches are present. The India Mutual Fund Market thus sits on a dual track where metros anchor absolute assets and non-metros deliver faster percentage growth off a smaller base.

B30 growth requires consistent education, easy service access, and standardized disclosures so investors can compare products without ambiguity on cost or risk across categories. With improved cyber resilience and clarified data stewardship, digital channels can keep scaling in smaller cities while protecting investors from misuse of personal and portfolio data. Utility platforms run by exchanges help keep transactions reliable and reduce operational breakage for distributors serving suburban and rural clients with limited back-office capacity. AMC reports show how hybrid distribution models blend branch-led advice for complex needs with app-based execution for everyday transactions in B30 coverage. This approach should sustain the India Mutual Fund Market’s widening footprint as connectivity and trust improve outside the largest metros over the next several years.

Competitive Landscape

The India Mutual Fund Market operates with moderate concentration, where leading AMCs contribute a large share of incremental assets, yet more than fifty registered players compete for flows across active, passive, and hybrid categories. Scale brings advantages in distribution reach, digital transaction penetration, and product breadth, and that helps top players acquire customers at lower cost while maintaining service standards. AMC disclosures show rising digital shares of new purchases and SIPs, which reduces friction for cross-sell and upsell inside large customer bases that incumbents already serve. Passive leadership is anchored by large sponsors with exchange-linked distribution and institutional relationships that reinforce ETF scale and liquidity. These structures encourage a two-tier competition pattern where cost leadership and alpha differentiation coexist under stronger disclosure and cybersecurity expectations.

Strategic moves since 2025 include AMC-led digital acceleration and product shelf expansion in passive and thematic exposures as investors adopt low-cost beta and targeted equity baskets. Exchange utility platforms remain central to distribution, which benefits brokers and AMCs that integrate orders, statements, and service events under one login and consistent service levels. International expansion by leading AMCs focuses on GIFT City and select overseas centres to serve non-resident investors and offer offshore wrappers linked to domestic expertise where regulation permits. Regulatory changes on expense caps and cybersecurity increase operating leverage for well-prepared platforms and encourage consolidation among sub-scale schemes that do not meet tighter cost-to-serve thresholds. The India Mutual Fund Market is likely to see further scheme simplification and clarity of positioning as disclosures and standardized metrics make duplicative products less viable.

Partnerships and corporate actions continue to reshape mid-tier franchises with distribution-led strategies and product upgrades where sponsors bring reach and brand to bear on existing AMC platforms. Innovation in data and technology supports marketing and service workflows in large AMCs, including targeted engagement and portfolio nudges that aim to improve investor outcomes while reducing operational overhead. Passive lineups broaden through sector and factor funds that allow tactical allocation within diversified portfolios as expense caps and transparent tracking data improve comparability. As competitive dynamics mature, leaders invest in cybersecurity and compliance infrastructure to match the rising scale of digital flows while maintaining service availability and trust. The India Mutual Fund Market, therefore, balances scale-driven efficiency with product and service specialization across a wide field of competing brands.

India Mutual Fund Industry Leaders

SBI Mutual Fund

HDFC Mutual Fund

ICICI Prudential Mutual Fund

Nippon India Mutual Fund

Aditya Birla Sun Life Mutual Fund

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: SEBI approved the SEBI Mutual Funds Regulations 2026, which lower base expense ratios in select categories, unbundle statutory levies from caps, and rationalize brokerage limits, with implementation from April 1, 2026.

- November 2025: IndusInd International Holdings and Invesco completed a joint sponsor arrangement for Invesco Mutual Fund under a partnership designed to extend reach and product depth across growth segments.

- October 2025: Invesco launched the Invesco India Consumption Fund as part of a 2025 rollout that added differentiated equity exposure to household spending trends and business cycles.

- September 2025: AMFI directed MF Central to halt direct investor data sharing with third-party apps pending consent and security clarifications, which reset access pathways and focused integrations on consented frameworks.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the Indian mutual fund market as the total value of assets under management (AUM) held in open-ended and close-ended schemes registered with the Securities and Exchange Board of India (SEBI), including equity, debt, hybrid, money-market, exchange-traded, and fund-of-fund vehicles.

Scope exclusion: Portfolio management services, alternative investment funds, and pure insurance-linked products are outside this boundary.

Segmentation Overview

- By Fund Type

- Equity

- Bond

- Hybrid

- Money Market

- Others

- By Investor Type

- Retail

- Institutional

- By Management Style

- Active

- Passive

- By Distribution Channel

- Online Trading Platform

- Banks

- Securities Firm

- Others

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed fund managers, distributors, fintech platforms, and investor-education counselors across Mumbai, Bengaluru, Ahmedabad, and selected Tier-2 cities. These discussions validated flows into systematic investment plans, channel mix shifts, and fee compression, and helped fine-tune assumptions around passive-fund uptake and B30 city penetration.

Desk Research

We began by consolidating monthly AUM disclosures published by the Association of Mutual Funds in India (AMFI), SEBI handbook statistics, and Reserve Bank of India household savings tables, which give the cleanest, regulator-audited view of fund pools. Macroeconomic inputs such as GDP growth, disposable income, and bank-deposit trends were sourced from the Ministry of Finance's economic survey and World Bank open data.

For contextual signals, we drew on tier-one news and filings curated through Dow Jones Factiva, fund prospectus data from D&B Hoovers, and peer-reviewed journals that track retail participation and digital distribution.

This list is illustrative; many additional public and proprietary sources informed data collection, cross-checks, and clarifications.

Market-Sizing & Forecasting

We anchor the top-down model on FY-end AUM reported by AMFI, reconstruct historical pools through net inflow/outflow and market-return adjustments, and then project demand using multivariate regression on per-capita income, SIP ticket growth, digital account openings, and equity market depth. Supplier roll-ups of leading asset managers' reported AUM and sampled average selling price × unit data act as selective bottom-up sense checks. Where bottom-up totals undershoot the regulatory pool, gap factors are distributed to under-reported retail and fintech channels before final triangulation.

Data Validation & Update Cycle

Outputs undergo variance scans against fresh AMFI releases, foreign-fund flow alerts, and currency shifts. Senior analysts re-open models when deviations exceed preset thresholds; the report refreshes annually, with interim patches after material regulatory or macro events.

Why Mordor's India Mutual Fund Baseline Commands Reliability

Published estimates often diverge because firms track different asset buckets, convert rupees at varied rates, or quote revenue rather than AUM.

Key gap drivers include: some studies fold in alternative assets or PMS money, others exclude money-market schemes; a few convert INR to USD at spot rates from previous quarters; and several project on straight-line growth without regressing against savings-rate cyclicality. Mordor's approach fixes scope to SEBI-registered mutual funds only, applies rolling-average FX, and refreshes drivers every quarter, bringing our 2025 baseline to USD 0.85 trillion.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.85 T (2025) | Mordor Intelligence | - |

| USD 0.77 T (2024) | Global Consultancy A | Includes select PMS assets and earlier base year |

| USD 0.71 T (2024) | Industry Research Firm B | Excludes money-market funds; uses year-end spot FX |

| USD 2.50 B (2024) | Trade Journal C | Measures fund-manager fee revenue, not AUM |

Taken together, the comparison shows that once scope purity, FX hygiene, and driver refresh cadence are harmonized, Mordor Intelligence delivers a balanced, transparent baseline clients can trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the India Mutual Fund Market outlook to 2031?

The India Mutual Fund market size is USD 0.91 trillion in 2026 and is projected to reach USD 1.27 trillion by 2031 at a 6.86% CAGR, supported by SIP-led retail flows, digital distribution, and tighter cost transparency.

Which investor cohort leads assets in the India Mutual Fund Market?

Retail investors held 60.39% of assets in 2025 and remain on track for a 7.36% CAGR, reflecting persistent SIP adoption and digital onboarding across metros and Tier-2/3 cities.

How is regulation changing the cost and transparency for India mutual funds?

SEBI’s 2026 framework lowers base expense ratios in key categories, unbundles levies from caps, and tightens brokerage limits, which improves comparability and compresses costs for investors.

What role do passive products play in the India Mutual Fund Market?

Passive strategies are expanding with an 8.61% projected growth rate to 2031 as tighter expense caps and clear disclosures make index funds and ETFs attractive core building blocks in diversified portfolios.

How are digital channels changing distribution in India?

L51: Online platforms held a 33.42% share in 2025 and are forecast to grow at a 9.22% CAGR through 2031, with exchange utilities and AMC apps enabling fast onboarding, direct-plan access, and integrated portfolio management.

Where is geographic growth coming from within India?

L53: Locations beyond the top 30 cities posted faster growth during fiscal 2019 to 2025 and now account for a larger share of assets due to payments ubiquity, regional content, and hybrid branch-digital servicing models.

Page last updated on: