United Kingdom Mutual Fund Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

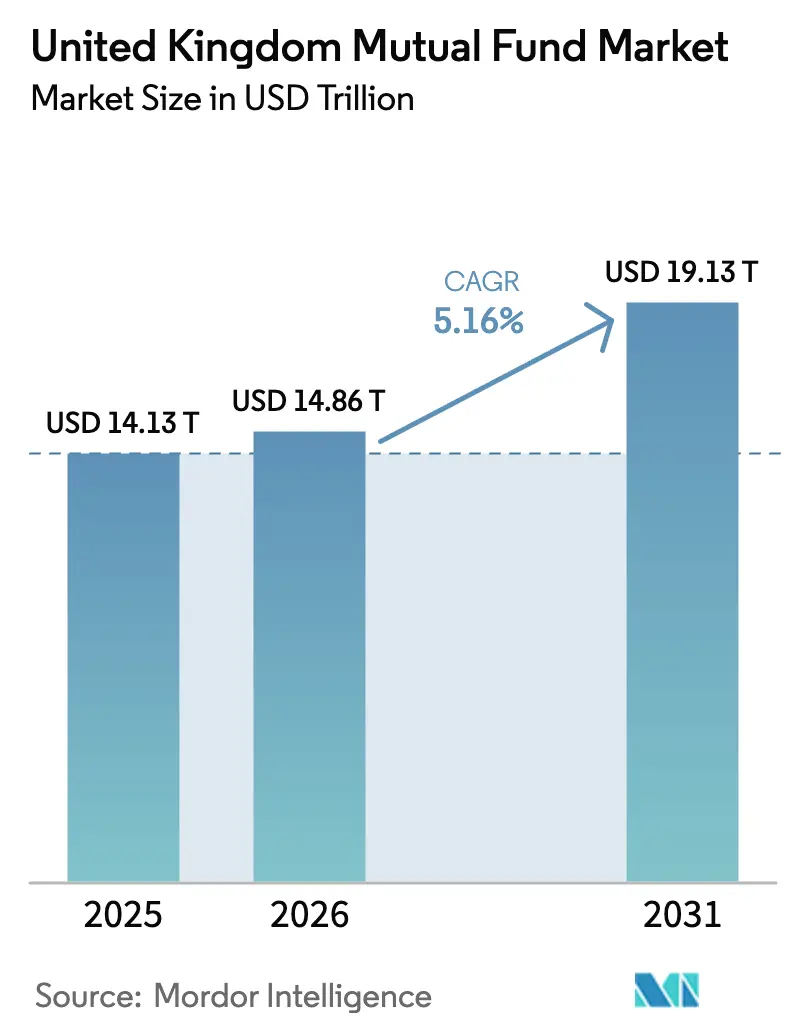

| Base Year Market Size (2025) | USD 14.13 Trillion |

| Market Size (2026) | USD 14.86 Trillion |

| Market Size (2031) | USD 19.13 Trillion |

| Growth Rate (2026 - 2031) | 5.16% CAGR |

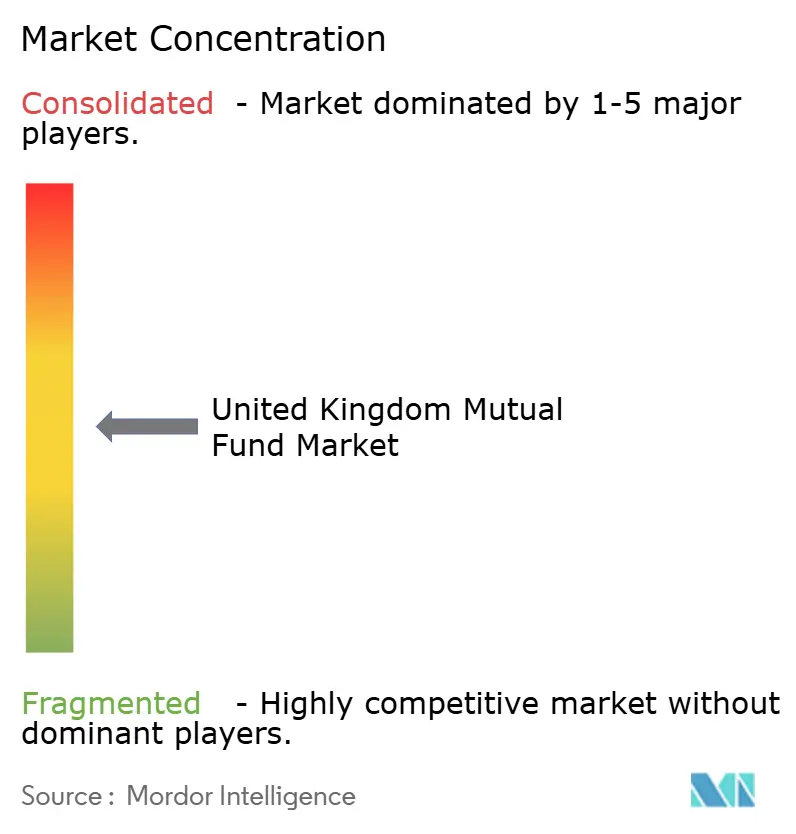

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Mutual Fund Market Analysis by Mordor Intelligence

The United Kingdom mutual fund market size is expected to grow from USD 14.13 trillion in 2025 to USD 14.86 trillion in 2026 and is forecast to reach USD 19.13 trillion by 2031 at 5.16% CAGR over 2026-2031. Robust pension reform, technology-driven distribution, and regulatory modernization are converging to sustain this growth trajectory. The Financial Conduct Authority’s Consumer Duty framework is reshaping fee structures, while the Mansion House Compact channels long-term capital into growth equity [1]Investment Association, “Fund outflows slashed 2024; cautious optimism prevails among investors,” theia.org. . Fee compression is strengthening the appeal of tracker funds, yet product innovation in private-market access vehicles is widening the menu for risk-aware investors. Rising adoption of fund tokenization and AI-enabled portfolio construction improves operational resilience and personalizes retail offerings. Steady policy support for sustainability disclosures further underpins confidence in environmental, social, and governance products.

Key Report Takeaways

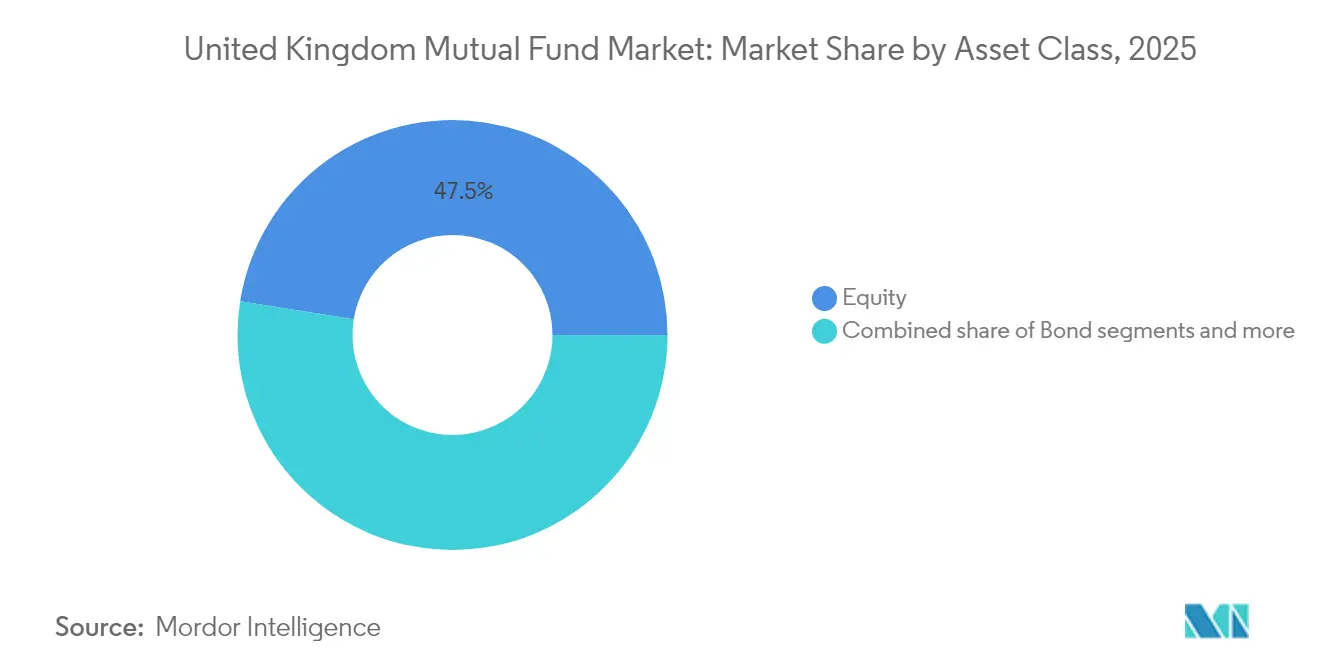

- By asset class, equity funds led with 47.50% of the United Kingdom mutual fund market share in 2025; Long-Term Asset Funds are forecast to grow at a 12.19% CAGR through 2031.

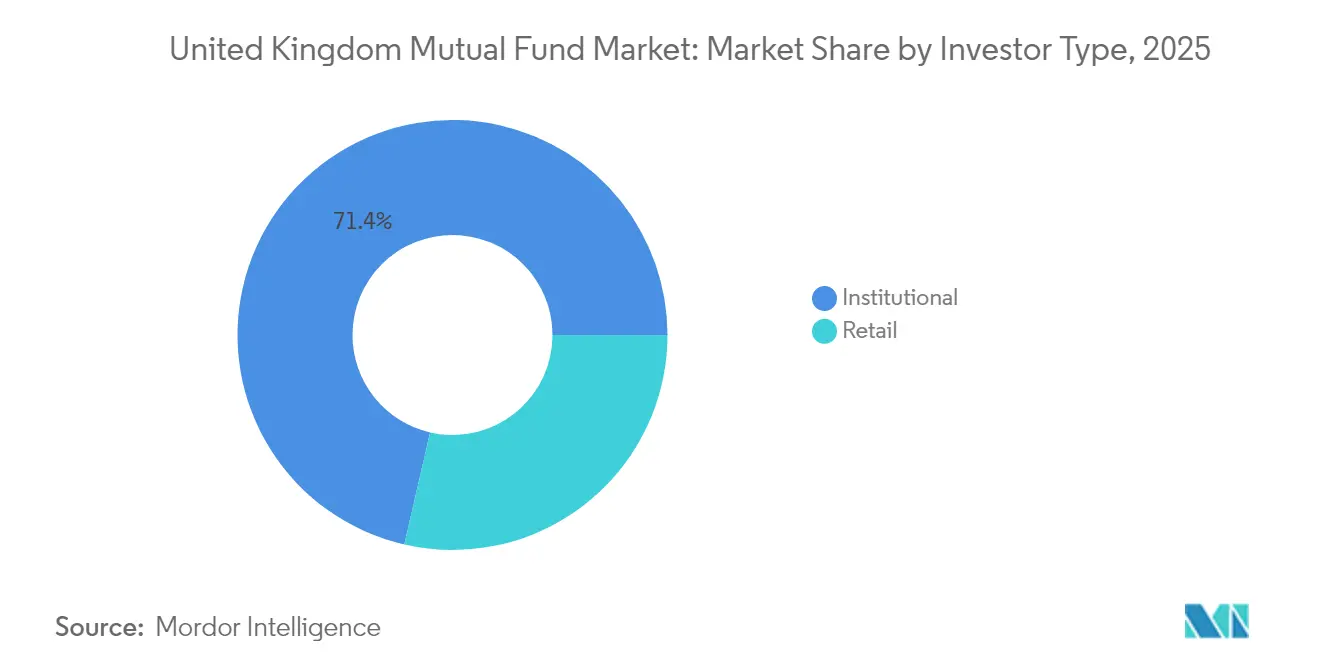

- By investor type, institutional mandates accounted for 71.40% of the United Kingdom mutual fund market size in 2025, while retail flows are projected to expand at a 7.06% CAGR through 2031.

- By distribution channel, online platforms captured 53.60% of the United Kingdom mutual fund market share in 2025, and they are advancing at a 9.62% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Mutual Fund Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shrinking retail cash hoards redirected into funds by FCA “excess-cash” initiative | +1.2% | England & Wales core, spillover to Scotland | Medium term (2-4 years) |

| Defined-contribution auto-enrolment glide-path upgrades favor multi-asset defaults | +1.8% | National | Long term (≥ 4 years) |

| Record tracker-fund inflows driven by fee compression and Consumer Duty disclosures | +1.5% | England & Scotland primary | Short term (≤ 2 years) |

| Pension fund Mansion House Compact to shift 5% of assets into UK growth equity | +2.1% | England core, Northern Ireland emerging | Medium term (2-4 years) |

| AI-enabled hyper-personalized portfolio construction on direct-to-consumer platforms | +0.8% | England & Wales | Long term (≥ 4 years) |

| Emerging Long-Term Asset Fund structure opening private-market access | +1.3% | England primary, Scotland secondary | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shrinking retail cash hoards redirected into funds

Households accumulated sizeable cash positions during the pandemic, but rising inflation eroded deposit returns and spurred a hunt for yield. The FCA’s 2025 guidance on “excess-cash” nudges platforms to flag idle balances and suggest suitable investment options, unlocking fresh inflows to the United Kingdom mutual fund market. Digital prompts and risk-profiling tools simplify fund selection, while Consumer Duty rules ensure transparency around value for money. Banks are collaborating with asset managers to curate low-cost fund baskets, reinforcing the shift from deposits to investments. These behavioral changes are most visible in England and Wales, yet Scotland’s retail base is beginning to mirror the trend[2]Department for Work and Pensions, “Pension fund investment and the UK economy,” gov.uk.

Defined-contribution auto-enrolment glide-path upgrades favor multi-asset defaults

Automatic enrollment now covers more than 10 million workers and is pushing plan sponsors to upgrade default funds. Providers are embedding multi-asset building blocks that blend public and private investments, benefiting from scale purchasing power. The Mansion House Accord further pushes fiduciaries toward private-market allocations, enhancing diversification and return potential for long-term savers. Employers welcome the simplified lifecycle structure, while trustees appreciate the transparent fee mechanics stipulated by Consumer Duty. Over time, these strategies are expected to reduce retirement-outcome dispersion and anchor stickier institutional flows into the United Kingdom mutual fund market.

Record tracker-fund inflows driven by fee compression and Consumer Duty disclosures

Cost comparisons are now front-and-center on platform dashboards, spurring investors to favor low-expense index products. Vanguard’s direct-to-consumer channel exemplifies this trend by pairing zero-commission dealing with straightforward guidance. Active managers are responding by rationalizing share classes and introducing performance-linked pricing. The resulting fee war accelerates the adoption of transparent passive funds, reinforcing the price anchor across the industry. While margin pressure intensifies, scale players still benefit from operating-cost leverage and global replication of successful passive franchises.

Pension fund Mansion House Compact to shift 5% of assets into UK growth equity

The 2025 Mansion House Compact rallied leading schemes to channel at least 5% of portfolios toward domestically listed growth companies. This initiative aims to revitalize local capital markets and stave off delistings prompted by foreign listings. Asset managers are launching engagement-focused UK equity funds aligned with stewardship codes that emphasize sustainable earnings quality and governance. Index providers are also exploring bespoke UK growth composites to benchmark performance. As allocation deadlines loom, demand for small- and mid-cap research coverage is rising, encouraging brokers to expand equity-research capacity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent retail outflows from UK-equity funds despite valuation discounts | −1.4% | England & Scotland primary | Short term (≤ 2 years) |

| High concentration of platform distribution fees squeezing active-manager margins | −0.9% | England core, Wales secondary | Medium term (2-4 years) |

| Rising operational costs from Consumer Duty & Sustainability Disclosure Requirements | −1.1% | National | Short term (≤ 2 years) |

| Regulatory capital strain on small boutiques under IFPR harms product innovation | −0.7% | England & Scotland boutique managers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent retail outflows from UK-equity funds despite valuation discounts

Domestic equities trade at notable discounts to U.S. peers, yet sentiment remains subdued. Brexit aftershocks and macro sluggishness deter retail allocations, while global ETFs offer diversified exposure at lower cost. Headline underperformance perpetuates a negative feedback loop, with press coverage reinforcing outflow momentum. Although the Mansion House Compact aims to reverse this, retail behaviors respond slowly to policy signaling. Re-engaging investors will require tangible evidence of earnings resilience among UK-listed firms.

High concentration of platform distribution fees squeezing active-manager margins

Three dominant supermarkets negotiate rebate structures that erode headline fees, particularly for boutique stock-pickers. Active managers struggle to pass through research costs post-MiFID II unbundling, widening the gap between list and realized margins. Some respond by launching lower-cost quant products, while others pivot to institutional segregated mandates. The FCA’s scrutiny of platform-pricing spreads may encourage fairer economics, but near-term pressure on profitability persists. Larger houses with multi-channel reach wield stronger bargaining power, intensifying competitive imbalance[3]Office for National Statistics, “Regional gross disposable household income,” ons.gov.uk.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Asset Class: Equities dominate but private-market vehicles accelerate

By Investor Type: Institutional weight remains decisive while retail acceleratesEquity funds captured 47.50% of the United Kingdom mutual fund market in 2025, supported by widespread index adoption and institutional allocations. Bond funds accounted for 24.20%, buoyed by liability-driven investments and gilt issuance. Hybrid strategies held 18.10% as target-date solutions became the default for auto-enrolled savers. Money-market products remained at 7.10% amid persistent low policy rates. The “others” bucket—primarily Long-Term Asset Funds—claimed just 3.10% yet is projected to post a 12.19% CAGR through 2031. This pace suggests private-asset vehicles will eat into traditional equity shares, but diversification benefits should empower investors to blend both. Active equity teams are therefore emphasizing stewardship initiatives to retain relevance and defend fee levels.

Historically, equity funds weathered 2019-2024 shocks thanks to broad-based recovery rallies and consistent pension-scheme inflows. Fixed-income allocations grew after the 2022 gilt crisis, when schemes retooled risk budgets. Momentum behind LTAFs stems from the search for yield, retail appetite for real-asset exposure, and regulatory safeguards that calm liquidity worries. Technology also matters; tokenized share classes promise near-instant settlement, lowering administration costs for illiquid holdings. Overall, diversification across asset classes underpins the resilience of the United Kingdom mutual fund market.

By Investor Type: Institutional weight remains decisive while retail accelerates

Institutional mandates represented 71.40% of the United Kingdom mutual fund market size in 2025, reflecting the scale of corporate pensions and insurance general accounts. Retail channels claimed 28.60% but are expanding faster as digital platforms democratize access. Consumer Duty-driven transparency supports this shift by empowering self-directed investors to compare outcomes. Auto-enrolled employees increasingly top up contributions via mobile dashboards, blurring lines between workplace and retail flows. Meanwhile, professional investors are reshaping portfolios toward private markets, boosting the United Kingdom mutual fund market share of alternative strategies.

Institutional flows continue to grow steadily, bolstered by longevity risk management and incremental contribution rates. However, fee renegotiations remain intense, particularly for active mandates facing performance dispersion. Retail growth is forecast at 7.06% CAGR through 2031, amplified by the inclusion of LTAFs in Stocks & Shares ISAs. Cross-selling of ESG funds also widens appeal, with marketing tailored to younger demographics. The interplay between institutional stability and retail momentum adds depth to liquidity profiles across fund structures.

By Distribution Channel: Digital dominance reshapes economics

Online supermarkets occupied 53.60% of the 2025 distribution pie, setting the benchmark for speed, transparency, and pricing discipline. Financial advisers captured 27.80%, providing holistic planning for complex needs such as pension transfers. Banks held 12.00%, constrained by capital rules that incentivize fee-based advisory over balance-sheet product manufacturing. Direct sales from fund houses accounted for 6.60%, largely institutional segregated accounts and niche thematic launches. From 2026-2031, online channels are poised for a 9.62% CAGR, reinforcing their central role in the United Kingdom mutual fund market.

Platform fee wars compress margins yet expand overall volumes as cost savings attract new investors. Consolidation is inevitable because smaller portals lack technology budgets to comply with Consumer Duty evidence requirements. Adviser models are evolving toward hybrid delivery, mixing digital onboarding with periodic human touchpoints. Banks leverage household brands to cross-sell investment accounts alongside mortgages and savings products. Direct channels now experiment with community-led education hubs to differentiate from price-only competition.

Geography Analysis

England commanded 81.10% of assets under management in 2025, sustained by London’s financial hub, robust household wealth, and dense corporate pension funding. Scotland followed with 8.20%, leveraging Edinburgh’s asset-management heritage and energy transition themes that attract sustainable-investment capital. Wales recorded 5.70% share, buoyed by Cardiff’s fintech ecosystem and cross-border advice networks that cater to affluent retirees. Northern Ireland held 5.00% yet delivered the fastest 6.38% CAGR outlook through 2031, aided by digital-skills programs and post-Brexit protocol stability, encouraging services trade.

Regional policy frameworks shape these dynamics. The City of London Corporation champions fintech sandboxes that feed England’s innovation pipeline, while the Scottish Government promotes green-finance incubators aligned with offshore-wind build-outs. Welsh authorities expand financial-literacy curricula to nurture home-grown investor participation. Northern Ireland’s Invest NI agency markets Belfast as a cost-effective operations base for global asset-servicing centers. As infrastructure improves, regional penetration of digital platforms should rise, spreading mutual-fund ownership beyond historic strongholds.

Economic indicators also differ: disposable household income per capita tops USD 37,000 in London versus USD 25,000 in Northern Ireland, influencing ticket sizes and product mix. Nevertheless, tax-advantaged wrappers such as ISAs standardize scopes for entry-level investing. Pension policy uniformity further harmonizes demand for target-date funds across regions. While England’s dominance will persist, growth hotspots in outlying nations amplify resilience and diversify the revenue base of the United Kingdom mutual fund market.

Competitive Landscape

The United Kingdom Mutual Fund Market demonstrates moderate concentration, where a small group of leading firms control a significant portion of total assets. This creates a competitive environment that balances the benefits of scale with the need for continuous innovation. BlackRock holds a leading position due to its dominance in index-tracking strategies and deep penetration into institutional pension schemes. Vanguard has gained rapid momentum in the retail space through its low-cost passive offerings and direct-to-consumer approach. Legal & General Investment Management capitalizes on its role as a default manager for defined contribution schemes and its close ties to an integrated insurance business. However, it is undergoing strategic restructuring through a merger with Legal & General Capital to form a unified global asset management arm targeting substantial long-term operating profits.

Consolidation within the UK mutual fund industry accelerated through 2024 and 2025, reflecting growing pressure for scale and specialization. Notable transactions include BlackRock’s acquisition of a major private market data and analytics provider, enhancing its capabilities in alternative assets. Other significant deals include Oaktree’s purchase of a prominent wealth manager and the formation of a large-scale joint venture between Phoenix Group and Schroders aimed at consolidating workplace pensions. These moves indicate a trend toward vertical integration and strategic partnerships in a maturing market. Firms are seeking to bolster both their retail and institutional offerings through targeted acquisitions and alliances. This consolidation is reshaping the competitive landscape and elevating the importance of differentiated capabilities.

Technology has emerged as a critical factor in competitive positioning across the United Kingdom Mutual Fund Market. Leading firms are increasingly deploying AI-driven portfolio construction tools, exploring tokenised fund structures, and building robust digital distribution platforms. These innovations help attract cost-sensitive retail investors while maintaining strong institutional relationships. The strategic alliance between Wellington, Vanguard, and Blackstone highlights a growing industry shift toward collaboration across public and private markets. Regulatory pressures, including new consumer protection rules, sustainability disclosure requirements, and operational resilience standards, are raising barriers to entry. However, these same regulations are also pushing established players to innovate in product design, compliance infrastructure, and client experience.

United Kingdom Mutual Fund Industry Leaders

BlackRock

Vanguard

LGIM

Fidelity International

Schroders

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Wellington Management, Vanguard, and Blackstone announced a strategic alliance to develop multi-asset investment solutions integrating public and private markets, targeting institutional-caliber diversified portfolios for broader investor access and enhanced income/growth outcomes.

- December 2024: Legal & General set Lifetime Advantage Funds as new default strategy for contract-based DC clients from early 2025, incorporating 15% private markets allocation through L&G Private Markets Access Fund targeting affordable housing, university spinouts, and renewable infrastructure.

- September 2024: Legal & General appointed Eric Adler as Chief Executive Officer of Asset Management, leading a unified global asset manager combining public and private markets businesses with £1.136 trillion AUM and targeting £500-600m operating profits by 2028.

- September 2024: Janus Henderson partnered with Anemoy and Centrifuge to launch its first tokenised fund, exploring blockchain technology for fund distribution and ownership through decentralised finance infrastructure.

United Kingdom Mutual Fund Market Report Scope

A mutual fund is a financial vehicle that pools assets from shareholders to invest in securities like stocks, bonds, money market instruments, and other assets. The report's scope includes understanding the UK mutual fund industry, regulatory environment, MF companies, and their business models, detailed market segmentation, current market trends, changes in market dynamics, growth opportunities, and in-depth analysis of the market size and forecast for the various segments.

The UK mutual funds market is segmented by fund type, and investor type. By fund type, the market is sub-segmented into equity, debt, multi-asset, money market, and other fund types. By investor type, the market is sub-segmented into households, monetary financial institutions, general government, non-financial corporations, insurers & pension funds, and other financial intermediaries. The report offers market size and forecasts for the UK mutual funds market in value (USD) for all the above segments.

| Equity |

| Bond |

| Hybrid |

| Money Market |

| Others |

| Retail |

| Institutional |

| Banks |

| Online Platforms |

| Financial Advisors |

| Direct |

| England |

| Scotland |

| Wales |

| Northern Ireland |

| By Asset Class | Equity |

| Bond | |

| Hybrid | |

| Money Market | |

| Others | |

| By Investor Type | Retail |

| Institutional | |

| By Distribution Channel | Banks |

| Online Platforms | |

| Financial Advisors | |

| Direct | |

| By Region | England |

| Scotland | |

| Wales | |

| Northern Ireland |

Key Questions Answered in the Report

What is the projected value of the United Kingdom mutual fund market in 2031?

The market is forecast to reach USD 19.13 trillion by 2031, reflecting a 5.16% CAGR.

Which asset class currently leads the United Kingdom mutual fund market?

Equity funds dominate with 47.50% of assets under management as of 2025.

How fast are online platforms growing in fund distribution?

Online platforms are expanding at a 9.62% CAGR, moving from 53.60% share in 2025 to a larger footprint by 2031.

What impact does the Mansion House Compact have on investment allocation?

It commits pension funds to direct at least 5% of assets toward UK growth equity, supporting domestic capital formation.

Why are Long-Term Asset Funds significant for retail investors?

LTAFs open access to private markets with FCA-regulated liquidity tools, offering new diversification opportunities.

Page last updated on: