Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

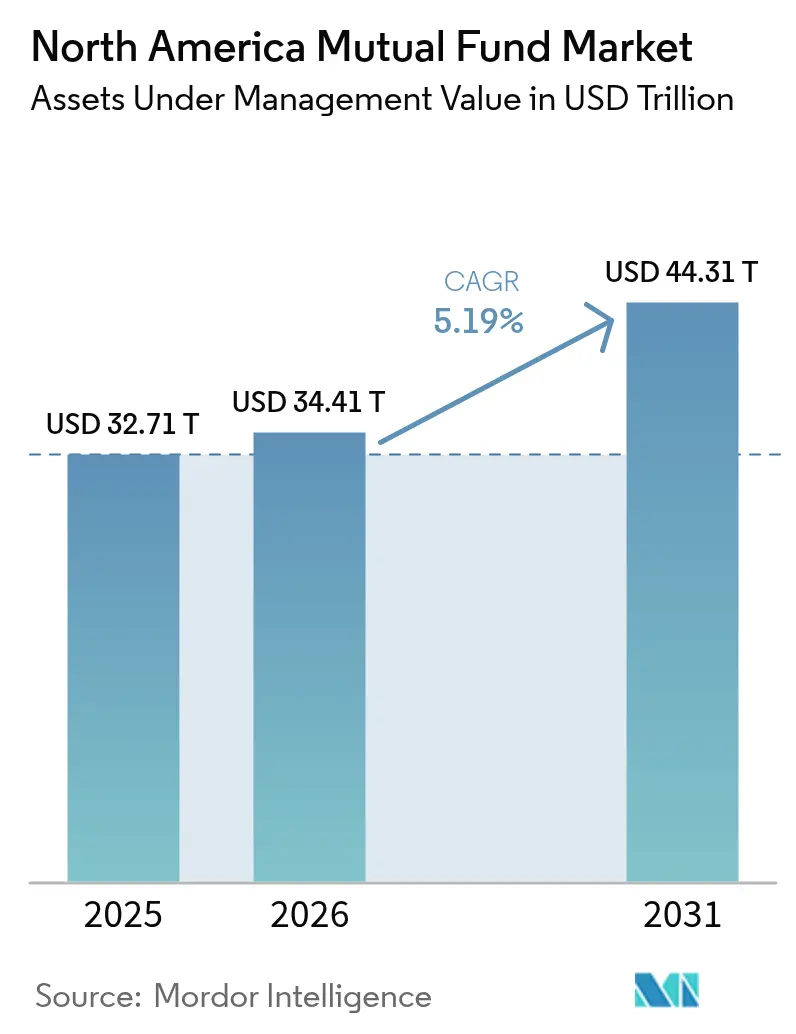

| Base Year Market Size (2025) | USD 32.71 Trillion |

| Market Size (2026) | USD 34.41 Trillion |

| Market Size (2031) | USD 44.31 Trillion |

| Growth Rate (2026 - 2031) | 5.19% CAGR |

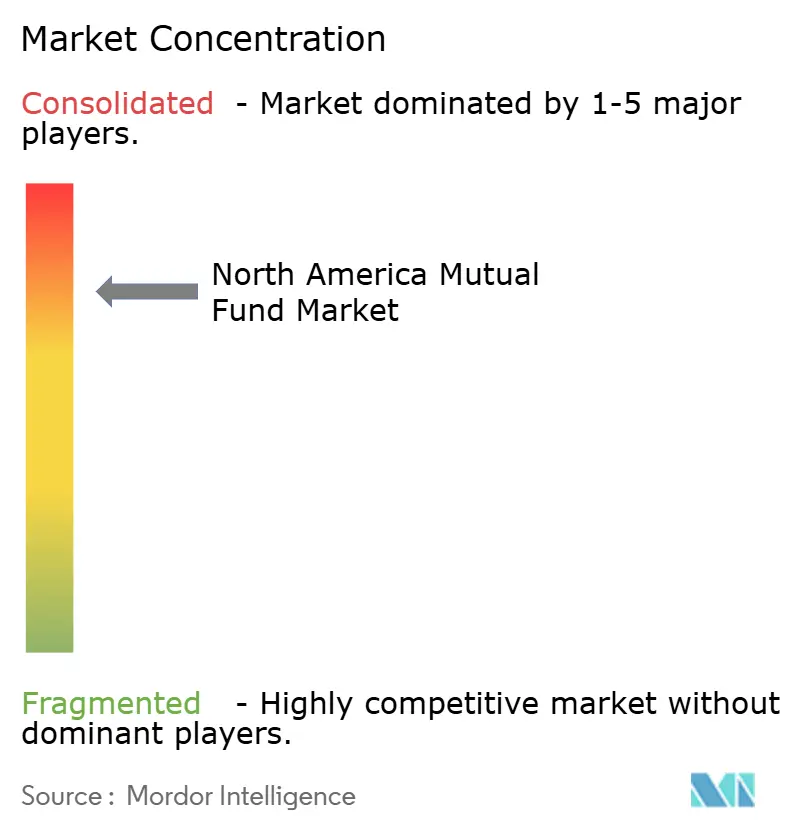

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Mutual Fund Market Analysis by Mordor Intelligence

The North American mutual fund market size was valued at USD 32.71 trillion in 2025 and estimated to grow from USD 34.41 trillion in 2026 to reach USD 44.31 trillion by 2031, at a CAGR of 5.19% during the forecast period (2026-2031). Rising retirement‐plan contributions, a marked shift toward passive index strategies, and sustained demand for money market funds in a higher-rate environment collectively underpin this trajectory. Policy changes have also reshaped product design and distribution, most notably the 2024 U.S. money-market reforms that accelerated consolidation among large fund complexes. Rapid digital adoption is lowering advice barriers and widening access for younger investors, while regulatory latitude in Canada and demographic momentum in Mexico create fresh regional opportunity pockets. However, fee compression is nearing structural limits, compelling managers to pursue scale or specialized alpha to sustain margins.

Key Report Takeaways

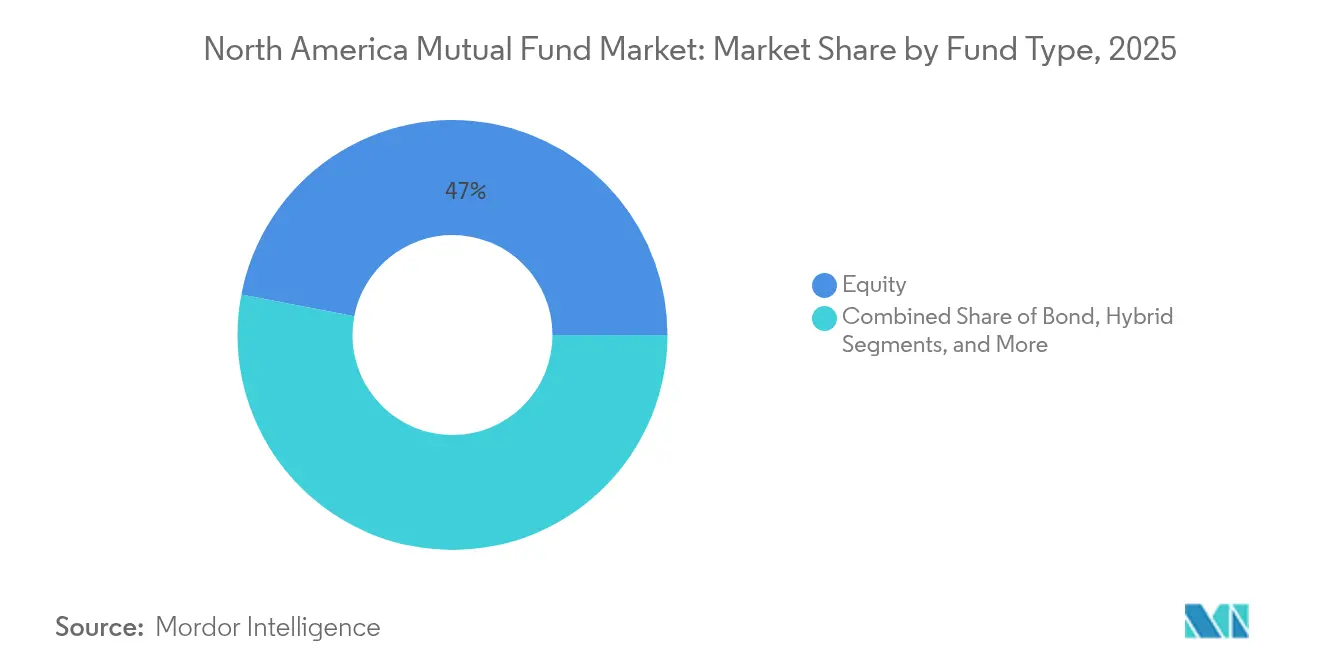

- By fund type, equity funds held 46.98% of North America mutual fund market share in 2025; the “Others” bucket, led by alternative strategies, is projected to post the fastest 9.63% CAGR through 2031.

- By investor type, retail investors commanded 66.28% of the North America mutual fund market size in 2025 and are set to grow at a 5.87% CAGR, outpacing institutional flows.

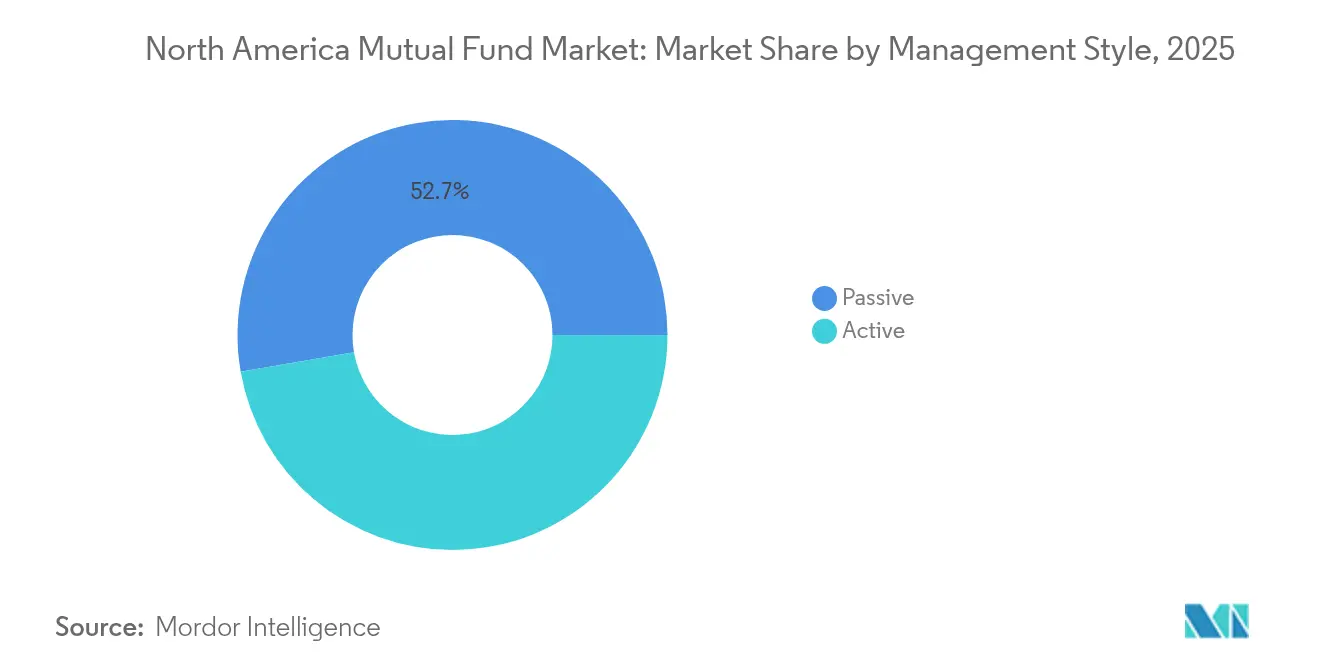

- By management style, passive products controlled 52.74% of assets of the North America mutual fund market in 2025, with a 5.64% CAGR expected through 2031.

- By distribution channel, securities firms led with a 36.55% share of the North America mutual fund market in 2025, whereas online trading platforms are forecasted to expand at a 7.22% CAGR to 2031.

- By country, the United States retained a dominant 91.08% share of the North America mutual fund market in 2025, while Mexico is on track for a 7.72% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Mutual Fund Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Deposit-to-money-market migration amid higher policy rates | +1.2% | United States institutional segment | Short term (≤ 2 years) |

| Retirement-plan inflows into mutual funds & target-date series | +1.8% | United States and Canada | Long term (≥ 4 years) |

| Surge in passive index-based mutual funds & sleeve structures | +1.5% | Global, led by North America | Medium term (2–4 years) |

| Retirement-based auto-contributions anchor sticky inflows | +0.9% | United States and Canada | Long term (≥ 4 years) |

| Family-office uptake of private-credit interval funds | +0.6% | United States wealth centers | Medium term (2–4 years) |

| Canadian alt-fund derivative latitude boosts product innovation | +0.3% | Canada | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Deposit-to-Money-Market Migration Amid Higher Policy Rates

The 2024–2025 easing cycle failed to stem the flow of bank deposits into money market funds, as investors prioritized yield and daily liquidity. Institutional prime funds shrank after the SEC’s October 2024 liquidity-fee rule, falling from 25 to 9 vehicles while assets declined by 49%[1]U.S. Securities and Exchange Commission, “Money Market Fund Reform,” sec.gov. Larger complexes with automated fee-calculation systems absorbed the change, widening the scale gap over niche managers. As money market yields stay attractive relative to deposits, the North American mutual fund market continues to channel short-term cash into low-risk funds, underpinning baseline asset growth.

Retirement-Plan Inflows into Mutual Funds & Target-Date Series

Target-date mutual funds surpassed USD 4 trillion in assets, aided by default enrollment rules that funnel new workplace contributions into age-based portfolios. The Department of Labor's 2007 regulations establishing target-date funds as qualified default investment alternatives created a structural tailwind that continues to drive growth. Their average annualized return of 7.3% over 15 years and falling expense ratios—now 29 basis points—reinforce stickiness. Vanguard, Capital Group, Fidelity, and T. Rowe Price dominate flows by coupling robust glide-path design with aggressive fee cuts, ensuring the continued expansion of passive-indexed share classes inside employer plans.

Surge in Passive Index-Based Mutual Funds & Sleeve Structures

Passive assets crossed the symbolic 50% threshold of total U.S. fund holdings, driven by defined contribution migration and ETF tax efficiency. This shift reflects the transition from defined benefit to defined contribution plans and the proliferation of ETF structures that offer superior tax efficiency and lower costs. Concentrated megacap weightings, however, challenge active managers to outperform benchmarks in large-cap spaces. Advisers increasingly rely on sleeve or model portfolios blending passive cores with niche active satellites, enabling specialist boutiques to win mandates in small-cap, credit, or thematic exposures while the North America mutual fund market tilts further toward low-fee indexing. The rise of sleeve structures and model portfolios has enabled advisors to combine passive core holdings with active satellite strategies, creating new opportunities for specialized managers who can demonstrate consistent alpha generation in less efficient market segments.

Family-Office Uptake of Private-Credit Interval Funds

The democratization of private markets through interval funds represents a significant structural shift, with major asset managers launching products to capture retail demand for alternative investments. Interval funds opened private credit to high-net-worth channels, reaching an estimated USD 220 billion asset base by 2025. Franklin Templeton’s USD 904.5 million FLEX fund launch illustrates strong demand for secondary private equity exposure through registered tender-offer vehicles. Vanguard’s tie-up with Blackstone and Wellington exemplifies hybrid portfolios combining listed and unlisted assets, indicating a structural broadening of product choice in the North American mutual fund market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fee compression & margin squeeze leading to consolidation | -0.8% | United States passive segment | Medium term (2–4 years) |

| ETF & SMA cannibalization of traditional mutual fund flows | -1.1% | United States and Canada | Long term (≥ 4 years) |

| Complexity and cost of distribution shelf access | -0.4% | United States wealth channels | Medium term (2–4 years) |

| Boomer decumulation creating secular redemption overhang | -0.7% | United States and Canada retail | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fee Compression & Margin Squeeze Leading to Consolidation

Average asset-weighted fund expenses fell to 0.34% in 2024 from 0.36% a year earlier as large managers passed through incremental savings to investors. Vanguard alone trimmed fees on 87 funds, reinforcing the deflationary race[2]Vanguard Group, “Vanguard Reduces Expense Ratios,” vanguard.com. A Carne Group survey reveals that 65% of asset management executives anticipate significant margin pressure over the next two years, with 73% of traditional managers planning to rationalize products, particularly actively managed public funds. With index expense ratios approaching zero, managers are pivoting toward active ETFs, alternatives, or scale-driven mergers—evidenced by Franklin Templeton’s integration of Putnam and BlackRock’s USD 12 billion HPS deal—to protect economics inside the North America mutual fund market.

ETF & SMA Cannibalization of Traditional Mutual Fund Flows

Citigroup projects ETFs could siphon USD 6 trillion–10 trillion in mutual-fund assets within ten years as investors prioritize liquidity and after-tax returns. Deloitte foresees a 13-fold rise in active ETF assets by 2035, signaling that wrapper choice rather than strategy governs new allocations. Mutual fund ownership among investors has declined from 72% in 2018 to 62% in 2023, with younger investors increasingly favoring self-directed investing and ETF structures. Separately managed accounts (SMAs) also gain favor among high-net-worth clients seeking transparency and customization, further pressuring legacy open-end structures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fund Type: Equity Dominance Faces Alternative Asset Disruption

Equity funds retained 46.98% of the North America mutual fund market share in 2025, reflecting their entrenched role in retirement and wealth portfolios. Bond funds attracted inflows amid higher yields, while money market offerings grappled with operational changes following SEC liquidity-fee mandates. The “Others” category—comprising interval, real-asset, and thematic funds—captured just a sliver of the North America mutual fund market size in 2025, yet is set to rise at a 9.63% CAGR through 2031 as investors hunt diversification and inflation hedges.

The democratization of private credit, real estate, and secondary strategies via registered interval structures is shifting allocations beyond public equities and core bonds. As target-date providers rebalance toward fixed income near retirement, equity weightings will gradually dilute, although tax-advantaged wrappers and megacap concentration keep equity funds pivotal to overall growth. Money market funds, despite fewer institutional prime options, continue to serve corporate treasuries and retail cash management needs, anchoring short-duration demand within the North American mutual fund market.

By Investor Type: Retail Resilience Anchors Market Growth

Retail investors held 66.28% of the assets of the North America mutual fund market share in 2025, driving a 5.87% CAGR outlook that outstrips institutional expansion. Automatic enrollment and escalation in 401(k) plans funnel predictable contributions, offsetting aging baby-boomer withdrawals. Online brokerages report 31% of retail customers trading funds digitally, signaling channel convergence between advice and self-direction.

Institutional buyers negotiate deeper fee breaks and bespoke mandates, pressuring traditional share classes while embracing collective trusts and SMA formats. Yet household savings trends among millennials and Gen Z support ongoing retail primacy. These cohorts favor mobile platforms and passive building blocks, influencing product design and marketing across the North America mutual fund market.

By Management Style: Passive Revolution Reaches Maturity

Passive style management controlled 52.74% of assets of the North America mutual fund market share in 2025, with a 5.64% CAGR through 2031 still eclipsing active growth. Scale efficiencies let index giants maintain near-zero fees, accelerating asset capture from cost-sensitive segments. Active managers focus on less efficient arenas—small-cap, international, and alternatives—where skilled security selection can justify higher pricing.

Active ETFs offer a hybrid route: daily transparency and tradability alongside discretionary security selection. Already 8% of U.S. ETF assets, these funds absorbed one-third of 2025 inflows, helping active shops repackage strategies without cannibalizing flagship mutual fund lines. As performance dispersion widens in niche corners, investors may recalibrate allocations, slowing passive encroachment within the North American mutual fund market.

By Distribution Channel: Digital Disruption Accelerates Platform Growth

Securities firms topped distribution with a 36.55% share in the North America mutual fund market in 2025, leveraging advisory depth and product breadth. Yet online trading platforms are forecasted to compound at 7.22% annually to 2031 as younger cohorts demand intuitive, low-cost execution. Charles Schwab’s integration of TD Ameritrade brought USD 115 billion net new assets in Q4 2024 alone, illustrating scale synergies.

Banks retain a conservative investor base but face erosion from robo-advisers that bundle automated planning with transparent pricing. Across channels, 95% of providers now deploy artificial intelligence to streamline onboarding and service, embedding technology as a core competitive requisite in the North American mutual fund market.

Geography Analysis

The United States accounted for 91.08% of the North American mutual fund market in 2025, supported by the world’s largest defined-contribution ecosystem and a mature regulatory regime under the Investment Company Act of 1940. Ongoing SEC modernization—such as revised N-PORT and N-CEN reporting—improves transparency while lowering compliance friction, sustaining industry scale advantages. Yet mutual-fund ownership slipped to 62% of households in 2023 as younger investors pivot to ETFs and direct indexing, foreshadowing slower organic growth. Fee wars are most acute in the United States, compelling consolidation and ancillary service expansion.

Canada represents a distinct regulatory laboratory. The Canadian Securities Administrators’ derivative and crypto proposals invite innovative strategies that may not yet be clear under U.S. rules. The Canadian Investment Regulatory Organization’s 2025 integrated fee model aims to align oversight costs with dealer size, potentially lowering barriers for boutique managers. Such flexibility could bolster cross-border flows as U.S. investors seek differentiated exposures.

Mexico is the region’s fastest-growing locale, projected at an 7.72% CAGR to 2031. A young population, an expanding middle class, and a domestic revenue orientation make Mexican equities defensive against global trade shocks. With market valuations implying 8.5% expected annualized U.S.–dollar returns, international firms continue to scale local distribution partnerships. Nevertheless, fund penetration remains low, requiring sustained investor-education and infrastructure build-out to capture the full promise within the North America mutual fund market.

Regulatory Landscape

In the United States, mutual funds operate under the Investment Company Act of 1940 with oversight from the SEC. Recent rulemaking continues to tighten operational expectations around data, privacy, and investor protection. The SEC adopted amendments to Regulation S-P (privacy and safeguarding), with a compliance deadline of June 3, 2026 for registered investment advisers, raising requirements around incident response and customer information protection for fund complexes and their outsourced service providers.

In Canada, the Canadian Securities Administrators (CSA) is streamlining and modernizing investment fund oversight, while also updating distribution and disclosure mechanics. CSA final amendments to modernize the continuous disclosure regime for investment funds took effect April 22, 2026, and additional CSA amendments to the principal distributor model across NI 31-103, 81-101, 81-102, and 81-105 come into force October 1, 2026. These changes influence how fund manufacturers structure dealer relationships, compensation, and shelf access.

Value Chain Analysis

The North America mutual fund value chain runs from product structuring and portfolio management (asset managers and sub-advisers) through trading and risk oversight, then into fund administration functions such as transfer agency, NAV calculation, custody, audit, and regulatory reporting. For money market and other liquid strategies, operational readiness for rule-driven liquidity tools and associated reporting has become a differentiator, particularly for large complexes that can support automated compliance, data management, and fee-calculation capabilities.

Distribution remains a central control point in the chain, anchored by intermediaries such as broker-dealers and securities firms, banks, retirement-plan recordkeepers, and fund platforms that provide client access while bundling onboarding, servicing, and transaction infrastructure. Competitive dynamics increasingly center on platform-based models that combine advice, digital account opening, and model portfolios, shifting bargaining power toward scaled distributors and large managers that can offer low fees, broad share-class lineups, and integrated servicing across the region.

Competitive Landscape

Large-scale managers dominate the North American mutual fund market through unrivaled distribution reach, data-driven operations, and fee leadership. Vanguard’s mutual ownership model channels operational savings straight to shareholders, reinforcing its virtuous-cycle asset growth while sustaining the industry’s lowest expense ratios. BlackRock counters with Aladdin-powered analytics and an aggressive push into private markets, punctuated by its USD 12 billion acquisition of HPS Investment Partners that created a USD 220 billion private-credit franchise [3]CNBC, “BlackRock to Acquire HPS Investment Partners,” cnbc.com.

Second-tier players compete via domain specialization. Fidelity leverages retirement-plan servicing and active research capabilities, while American Funds sustains advisor-centric distribution bolstered by long-tenured performance. T. Rowe Price emphasizes target-date and active equity prowess. Each is diversifying into alternatives or active ETFs to mitigate margin erosion.

Technology has become a decisive separator: AI-driven client profiling, straight-through processing, and cloud-native platforms shrink servicing costs and elevate user experience. Partnerships such as Vanguard’s alliance with Blackstone and Wellington offer retail investors institutional-grade private assets, underscoring a blurring line between public and alternative markets. Smaller firms face twin pressures of rising compliance spend and shelf-access costs; many pursue mergers or niche thematic mandates to survive. Franklin Templeton’s purchase of Putnam and Guggenheim’s sale of its equity funds to New Age Alpha illustrate rationalization trends within the North America mutual fund market.

North America Mutual Fund Industry Leaders

Vanguard

Fidelity Investments

American Funds

T. Rowe Price

BlackRock

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Product whitespace is most visible where traditional mutual fund building blocks are being combined with alternatives and private-market access in regulated formats. Interval and tender-offer structures have moved into the mainstream for wealth channels, evidenced by the February 2025 launch of the Franklin Lexington Private Markets Fund (FLEX) with USD 904.5 million in initial assets, and by large-manager efforts to blend listed and unlisted exposures, including the April 2025 strategic alliance among Vanguard, Wellington Management, and Blackstone to co-develop multi-asset solutions.

A second opportunity area is distribution and operating-model modernization as digital adoption extends from execution into advice and servicing. Securities firms still lead mutual fund distribution with a 36.55% share in 2025, but growth in online trading platforms and model-portfolio usage creates room for managers that integrate cleanly with intermediaries while building more direct, platform-led client relationships. At the same time, regulatory focus on cybersecurity and AI-related representations supports demand for scalable compliance, privacy controls, and resilient operational infrastructure, which can help managers defend margins as fee levels have already compressed materially (0.34% average asset-weighted expenses in 2024).

Recent Industry Developments

- June 2026: Vanguard adds T. Rowe Price Associates, Inc. as advisor to three active equity funds: Vanguard Explorer Fund, Vanguard Variable Insurance Fund - Small Company Growth Portfolio, and Vanguard Growth and Income Fund. The move broadens active equity capabilities within a major fund complex, strengthening product diversification and external expertise to boost performance in legacy active strategies.

- June 2026: BlackRock & Trumid enter a multi-year partnership to integrate Trumid's credit trading workflows into BlackRock Aladdin OEMS. This collaboration directly impacts fixed-income trading workflow integration for Aladdin users and enhances liquidity access and execution efficiency for corporate bond trading via the Aladdin platform.

- June 2026: BlackRock launched the iShares Bitcoin Premium Income ETF BITA for bitcoin exposure with monthly option premium generation. This marks a direct entry of digital-asset exposure into mainstream ETF lineup and expands crypto-adjacent income strategy offerings for investors seeking yield from digital assets.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the North America mutual fund market is defined as the total assets under management held in regulated, open-ended mutual funds across the United States, Canada, and Mexico, measured in current US dollars.

Scope exclusions: ETFs, segregated or separately managed mandates, private funds, and defined benefit pension plan assets are excluded.

Segmentation Overview

- By Fund Type

- Equity

- Bond

- Hybrid

- Money Market

- Others

- By Investor Type

- Retail

- Institutional

- By Management Style

- Active

- Passive

- By Distribution Channel

- Online Trading Platform

- Banks

- Securities Firm

- Others

- By Country

- United States

- Canada

- Mexico

Data Sources, Market Sizing, and Validation

Desk Research

We started by mapping the regulated mutual fund universe and its reporting standards, because mutual fund assets are disclosed regularly but not always in the same format across sources. Public references were used to anchor base-year totals and category splits, such as the Investment Company Institute (ICI) Fact Book, securities regulator publications in the United States and Canada, central bank and national statistics releases that explain household saving and investment patterns, and fund association dashboards that track flows and net assets.

Next, the desk work focused on building a consistent time series that can be forecasted without overfitting. We used company annual reports and investor presentations for product positioning and distribution changes, and reputable press for material events that can shift flows quickly. A few paid data subscriptions were also used for company financials and news screening, plus patent databases only when product structure changes needed clarification. The sources listed here are illustrative and not exhaustive, and many additional references were used for data collection, cross-checks, and clarification.

Primary Interviews and Surveys

Interviews and short surveys were run with a mix of fund manufacturers, distribution intermediaries, and market observers who follow fund flows, portfolio shifts, and fee changes. We used these conversations to confirm what should be counted as a mutual fund versus an adjacent vehicle, how currency translation is handled for cross-border funds, and which investor channels are gaining traction across North America.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 17% | |

| Mid tier: 47% | Functional/Unit leaders: 34% | |

| Smaller Players: 22% | Managers: 49% |

Market-Sizing & Forecasting

The market size was constructed using a top-down approach where regulated fund industry totals are rebuilt from reported net assets and AUM series, and then filtered to the mutual fund-only pool for the United States, Canada, and Mexico. To keep the totals realistic, results were corroborated with selective bottom-up approximations, including sampled fund family roll-ups, channel checks on distribution mix, and sanity checks using observed AUM changes versus net flow direction.

In the model, a few practical inputs do most of the work, and they are refreshed each cycle. These include mutual fund net flows, valuation effects linked to equity and bond market levels, the shift between active mutual funds and low-cost wrappers, fee pressure that can influence product conversion, and currency movement for cross-border holdings. Where a data series was not available at the same frequency across countries, we used the closest official cadence and then aligned it to year-end values so the forecast starts from a comparable base.

Forecasts were built with scenario analysis supported by simple trend fitting on the main drivers, and then adjusted based on what primary respondents expect for flows and risk appetite. This keeps the forecast explainable, since the main question is whether growth comes more from market performance or from sustained net inflows.

Data Validation & Update Cycle

Before finalizing the numbers, we cross-checked the outputs against independent signals such as published industry net asset totals, flow summaries, and country-level savings and retirement contribution direction. If a year showed an abnormal jump or drop, the assumptions were reviewed again and follow-up calls were triggered to confirm whether the move was performance-led, flow-led, or caused by reclassification.

A second analyst review is completed before sign-off, focusing on year-over-year consistency and whether the drivers used in the model match what is being observed in the market. Reports are refreshed annually, and interim updates are made when there are material events like sharp rate changes, major regulatory shifts, or large market drawdowns. Right before delivery, a final pass is done so clients receive the most current view available.

Mordor Intelligence's North America Mutual Fund Market Size Compared Against Other Published Estimates

Published estimates for mutual fund market size in North America can differ even when they use similar words, because the counted asset pool is not always the same. Differences usually come from what products are included, which countries are grouped into North America, and whether the figure is reported as mutual fund-only assets or as a broader investment company total.

The main gap comes from mixing mutual funds with ETFs and other registered investment vehicles, and Mordor Intelligence treats the market as open-ended mutual fund AUM only, leaving ETFs and closed-end structures out even when they are reported in the same official tables.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 32.71 T (2025) | |

| Industry Association A | USD 28.50 T (2024) | Uses US mutual fund net assets for a year-end snapshot, which does not cover Canada and Mexico and is not aligned to the 2025 base year used in the model. |

| Industry Association B | USD 39.20 T (2024) | Reports total net assets for US-registered investment companies, which bundles mutual funds with ETFs, closed-end funds, and other structures, so the scope is wider than mutual funds alone. |

Looking at the spread, the higher figure is mainly a scope expansion, while the lower one is mostly a geography and base-year mismatch. By keeping the asset pool tied to mutual funds only and then aligning the time base to the study year, the estimate stays easier to trace back to reported AUM and the flow and market drivers used in the forecast.

Key Questions Answered in the Report

What is the current size of the North America mutual fund market?

The market stands at USD 34.41 trillion in 2026 and is forecasted to reach USD 44.31 trillion by 2031.

Which fund type is growing fastest?

Alternative and specialty funds grouped under “Others” are projected to grow at a 9.63% CAGR through 2031, outpacing equity and bond segments.

How much of the market is now in passive strategies?

Passive products hold 52.74% of the North America mutual fund market assets and continue to expand at a 5.64% CAGR.

Why are money market funds attracting deposits despite lower rates?

Elevated policy rates still offer competitive yields over bank deposits, and regulatory reforms favor large, well-resourced sponsors that can handle new liquidity-fee rules.

Which geography is expanding the quickest?

Mexico leads with an expected 7.72% CAGR to 2031, supported by favorable demographics and growing capital-market infrastructure.

How are asset managers coping with fee compression?

Most pursue scale through mergers, diversify into active ETFs or private-market products, and deploy technology to cut operating costs and enhance client experience.

Page last updated on: