Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

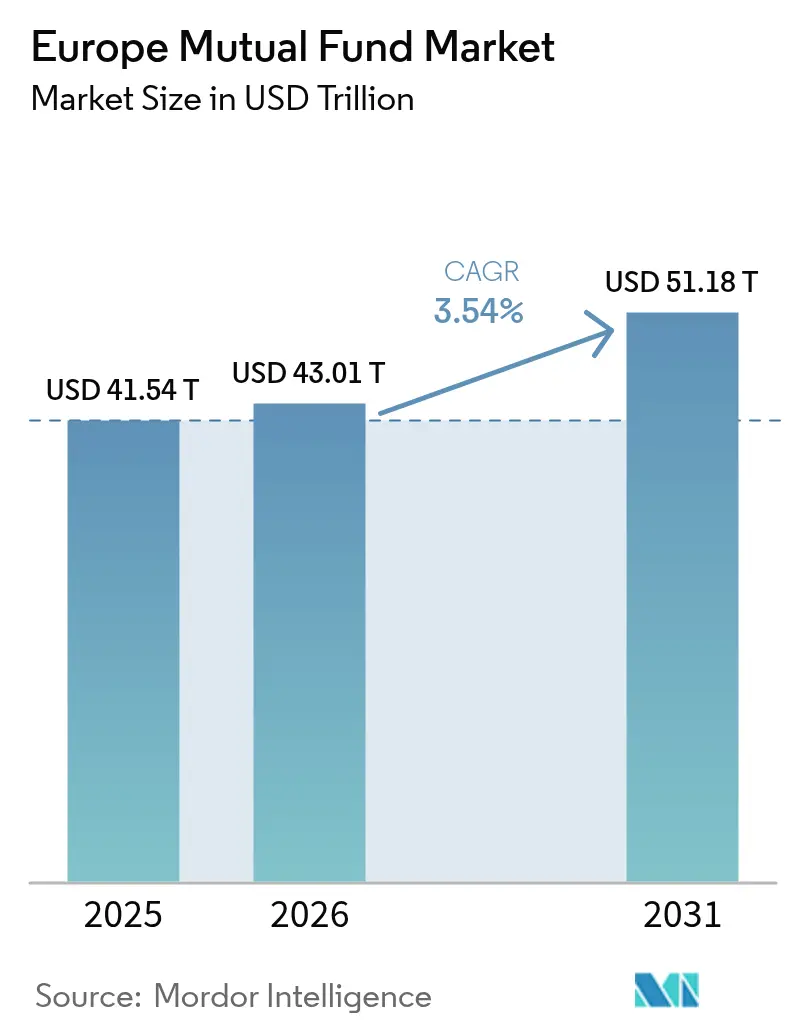

| Base Year Market Size (2025) | USD 41.54 Trillion |

| Market Size (2026) | USD 43.01 Trillion |

| Market Size (2031) | USD 51.18 Trillion |

| Growth Rate (2026 - 2031) | 3.54% CAGR |

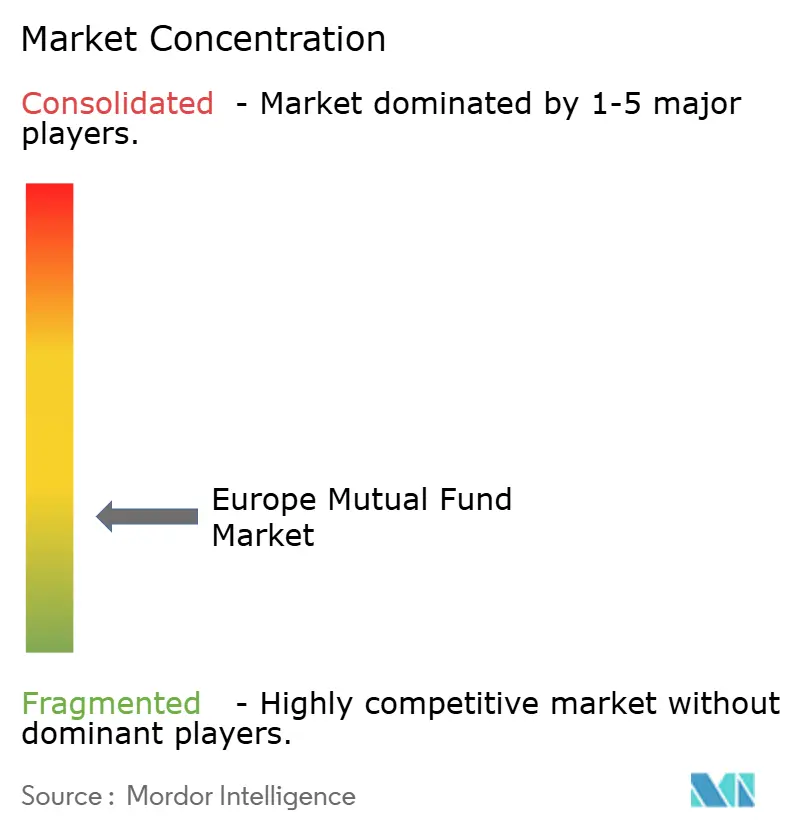

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Mutual Fund Market Analysis by Mordor Intelligence

Europe Mutual Fund Market size in 2026 is estimated at USD 43.01 trillion, growing from 2025 value of USD 41.54 trillion with 2031 projections showing USD 51.18 trillion, growing at 3.54% CAGR over 2026-2031. Steady asset growth rests on a blend of supportive regulation, rising digital distribution, and deepening investor appetite for ESG strategies. Fee compression remains a headwind, yet scale economies, product innovation, and cross-border passporting are helping managers protect margins. The European Securities and Markets Authority’s stricter ESG-name guidelines, combined with the Sustainable Finance Disclosure Regulation’s Article 8 and Article 9 classifications, are channelling new money into compliant products while accelerating product rationalization among laggards. Capital Markets Union reforms continue to trim frictions in multi-jurisdictional marketing and settlement, giving the Europe mutual fund market wider access to both retail and institutional flows. Technology adoption from robo-advice to fund-unit tokenization is widening the addressable audience, cutting distribution costs, and providing data-rich servicing models that improve client retention. Macroeconomic normalization is reviving bond-fund demand as investors seek duration and credit-spread capture without abandoning equity allocations. With the top five managers controlling only 30.80% of assets, competitive intensity remains high, creating room for specialized boutiques to scale on thematic and alternative strategies.

Key Report Takeaways

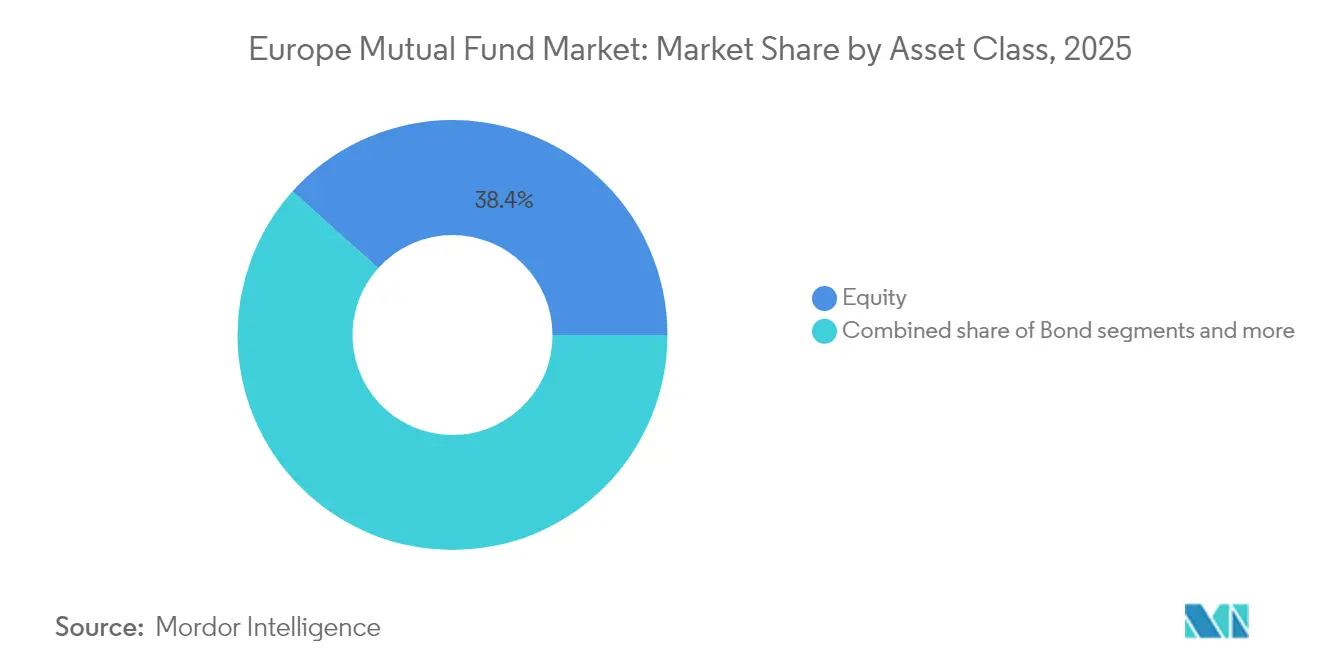

- By asset class, equity funds captured 38.35% of the Europe mutual Fund Market size in 2025, while bond funds are forecast to post the fastest 9.98% CAGR through 2031.

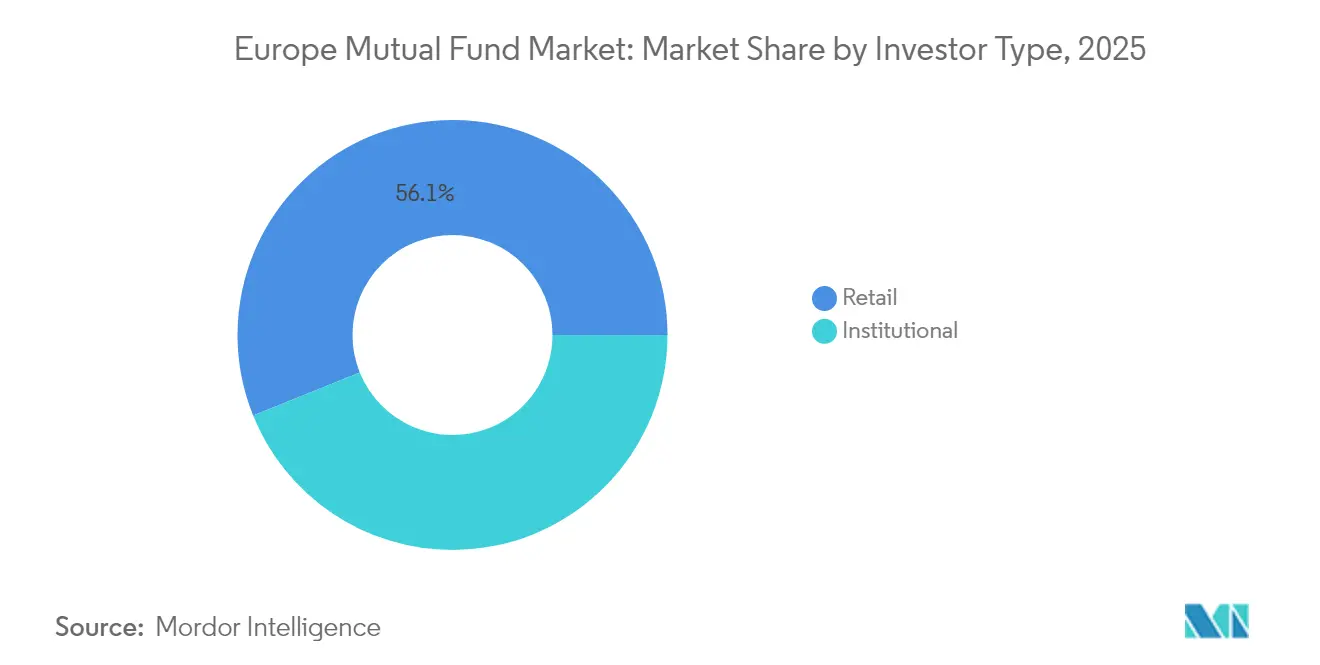

- By investor type, retail investors accounted for 56.10% of the Europe mutual Fund Market size in 2025, whereas institutional assets exhibit the highest projected 7.49% CAGR to 2031.

- By distribution channel, banks led with 44.20% of the Europe mutual Fund Market size in 2025, but online platforms are advancing at a 16.85% CAGR through 2031.

- By geography, the United Kingdom commanded 26.18% of the Europe mutual Fund Market size in 2025, yet Spain is poised to expand at a 9.14% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Mutual Fund Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ESG-aligned fund shift | +1.2% | Core EU with spillover to UK | Medium term (2-4 years) |

| Persistently low rates until 2027 | +0.8% | Eurozone core | Short term (≤ 2 years) |

| Capital Markets Union expansion | +0.6% | EU-27 excluding UK and Switzerland | Long term (≥ 4 years) |

| Rising robo-advisory adoption | +0.9% | Nordic leadership | Medium term (2-4 years) |

| Tokenization of fund units | +0.3% | Luxembourg-centered pilot markets | Long term (≥ 4 years) |

| ELTIF 2.0 cross-border passporting | +0.4% | EU-27 retail | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

ESG-aligned fund shift

Demand for sustainable strategies has vaulted Article 8 and Article 9 funds to the forefront of the Europe mutual fund market, pulling in USD 191–195 billion (EUR 180 billion) of net inflows during 2024, or 75% of aggregate mutual fund subscriptions[1]Autorité des Marchés Financiers, “Annual Report 2024 – Asset Management,” amf-france.org. . ESMA’s 2024 naming guidance tightened eligibility, forcing widespread reclassifications and temporary outflows from marginal products before stabilizing with more robust disclosure. Larger managers have exploited their research scale to meet the Sustainable Finance Disclosure Regulation’s Principal Adverse Impact demands, thereby shielding fee structures from the wider compression trend. France’s taxonomy-driven incentives catalyzed fresh thematic launches, including climate-transition and biodiversity strategies that command premium pricing. Institutional allocators now use ESG credentials as a gating criterion for manager selection, steering mandates toward platforms with proven stewardship frameworks. Retail investors, empowered by transparent impact metrics delivered through digital dashboards, are allocating a growing share of recurring monthly savings plans to sustainability-labeled funds. The evolving EU taxonomy, poised to add nuclear and gas to transition activities in 2025, is expected to unlock adjacent product lines and maintain inflow momentum into the Europe mutual fund market.

Rising robo-advisory adoption

Digital platforms that automate portfolio construction are carving out double-digit market-share gains, particularly across Nordic retail channels where 18% of assets already sit in automated mandates[2]Nordea Asset Management, “Nordic Investment Trends 2024,” nordea.com.. Algorithmic advice, now blessed by clarified MiFID II suitability rules, enables cost-effective offerings that charge 0.25–0.75% versus 1.5–2.5% at traditional branches. Germany’s BaFin green-lit 12 new robo licenses during 2024, signaling regulatory comfort with algorithmic services so long as governance and transparency standards are met. Vanguard’s European robo business logged 40% asset growth year-on-year, driven by tax-loss harvesting and low minimums that appeal to mass-affluent savers. Banks have responded by embedding white label robo modules into mobile apps, defending their 44.87% distribution share while bluntly lowering operating costs. Customer experience improvements, including straight-through KYC and biometric onboarding, shorten the investment funnel and accelerate AUM conversion. As artificial-intelligence engines mature, robo platforms will integrate ESG scoring and personalized retirement glide paths, raising the ceiling on digital penetration within the Europe mutual fund market.

Expansion of EU Capital Markets Union reforms

The third CMU action plan boosted cross-border passporting notifications by 25% in 2024, widening the Europe Mutual Fund Market’s addressable investor base across EU jurisdictions[3]European Commission, “Capital Markets Union Progress Report 2024,” ec.europa.eu. . Standardized withholding-tax procedures shaved operational friction, especially for Luxembourg and Irish UCITS seeking multi-country distribution. ESMA’s move toward a consolidated tape for funds improved price transparency, leveling the field for retail investors historically disadvantaged by fragmented data. Harmonized depositary rules under UCITS V let small and mid-sized managers secure pan-European custody at scale-economy pricing, lowering entry barriers for thematic and alternative strategies. The forthcoming European Single Access Point is set to centralize corporate-disclosure data, streamlining fund due diligence processes for institutions. Germany’s withholding-tax complexities remain a lingering bottleneck, showing that local idiosyncrasies can temper CMU benefits. Despite uneven rollout, aggregate cost savings from CMU initiatives support positive operating-leverage effects that underpin the 3.58% CAGR expectation for the Europe mutual fund market.

Cross-border passporting efficiencies post-ELTIF 2.0

ELTIF 2.0 slashed minimum ticket sizes from USD 10,700 to USD 1,070 (EUR 10,000 to EUR 1,000), unlocking an estimated USD 577.5 billion (EUR 500 billion) of European retail savings for infrastructure, private equity and real-estate strategies. Luxembourg’s CSSF approved 15 new structures in 2024, many marketed across borders in turnkey wrappers that simplify KYC and settlement. Enhanced liquidity provisions, including mandated redemption windows and secondary-market access, calmed past concerns about long lockups. Amundi’s inaugural retail infrastructure ELTIF attracted USD 2.31 billion (EUR 2 billion) in six months, illustrating pent-up appetite for alternatives among mass-affluent savers. Alignment with EU taxonomy goals enables managers to notch both sustainability and diversification credentials, creating halo effects that resonate with institutional consultants. Banks bundle ELTIFs alongside retirement offerings, using simplified disclosure templates to satisfy MiFID II cost-clarity requirements while deepening wallet share. Over time, retail alternative inflows are likely to mitigate the demographic drawdown drag on traditional equity allocations in the Europe mutual fund market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fee compression from passive products | -0.9% | Global with UK and Netherlands leadership | Short term (≤ 2 years) |

| SFDR Level 2 disclosure uncertainty | -0.4% | EU-27 with limited UK spillover | Medium term (2-4 years) |

| Heightened cybersecurity and data-privacy risk | -0.3% | Global with GDPR focus | Long term (≥ 4 years) |

| Demographic shift to decumulation | -0.6% | Germany and Italy core | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fee compression from passive products

Index-tracking vehicles continue to siphon flows from higher-fee active peers, dragging average mutual-fund expense ratios in Germany down to 1.15% in 2024 from 1.45% in 2020. Vanguard’s European ETF book surged 35% to USD 207.9 billion (EUR 180 billion), emboldened by government-backed savings plans that waive transaction fees for ETF allocation. Fixed-income ETFs now offer 0.05% headline TERs, forcing active bond managers to justify fees north of 0.75% with demonstrable alpha or bespoke mandates. Product rationalization accelerated, with 15% of European fund ranges consolidated or liquidated during 2024, shedding sub-scale offerings that cannot compete on price. Managers responded by introducing factor-based hybrids and performance-fee share classes, but these measures often cannibalize legacy revenue streams. Margin contraction has intensified M&A rationales as mid-tier platforms search for cost synergies and digital operating leverage. Sustained price competition is forecast to shave 0.9 percentage points off aggregate CAGR potential for the Europe Mutual Fund Market over the next two years.

Demographic shift to decumulation among aging investors

Europe’s median age continues to rise, shifting household financial priorities from capital accumulation to income generation and capital preservation. German and Italian retirees are redeeming equity-heavy mutual-fund positions in favor of drawdown strategies, tilting net flows away from growth products. Pension reforms that expand defined-contribution coverage blunt the outflow, but younger cohorts save less than their elders did at comparable life stages, slowing absolute AUM growth. Managers are launching target-date and managed-payout funds, yet these conservative allocations earn lower all-in fees, compressing top-line revenue even when assets stabilize. Italy’s recent pension reforms accelerate liquidity needs, compelling managers to hold more cash or shorter-duration bonds, which erodes return potential. Robo-advisors cater to aging clients with automated withdrawal schedules, adding competitive pressure on traditional distributors that rely on human advice for retiree segments. Overall, demographic decumulation is projected to trim 0.6 percentage points from the Europe Mutual Fund Market’s forecast CAGR by 2030.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Asset Class: Equity Leadership Meets ESG Transformation

Equity funds commanded 38.35% of the Europe mutual fund market share in 2025, reflecting a sustained appetite for growth themes and the rapid mainstreaming of ESG mandates. Bond funds followed closely at 35.42% as investors sought duration and inflation hedges amid ECB tightening cycles that nudged yields off historic lows without triggering recession. Hybrid allocations captured 15.62%, appealing to balanced-profile savers who value downside buffers during volatile rate regimes. Money-market strategies maintained 8.01% as corporate treasurers parked cash to earn improved overnight returns in a recovering rate backdrop. Alternative UCITS, though only 2.60%, grew swiftly on infra-debt and private-credit replication funds that promise diversification plus liquidity. The forecast 6.18% CAGR for equity funds implies that the Europe mutual fund markett size for equities could surpass USD 22.27 trillion by 2031 if current inflow momentum persists. Regulatory clarity under the Digital Operational Resilience Act requires each asset-class platform to invest in cyber infrastructure, lifting compliance spend to USD 2.88 million (EUR 2.5 million) per manager on average.

Equity funds are increasingly Article 8 or Article 9-labeled, with ESG screening embedded into standard prospectus language rather than marketed as stand-alone features. Bond funds benefit from renewed institutional allocations to investment-grade credit, particularly in the UK, where pension fund LDI unwind has freed balance-sheet capacity for traditional mutual-fund vehicles. Hybrid strategies leverage automated rebalancing engines to maintain risk bands, offering comfort to retail investors wary after the 2022-2023 volatility episodes. Money-market offerings reinvented themselves through tokenized share classes that settle on blockchain within minutes, reducing counterparty and settlement risk while meeting MiFID cost-transparency rules. Alternative UCITS continue to harvest relative-value and macro-trend opportunities, attracting institutions that want daily dealing with lower operational due diligence overheads than private fund structures. As a result, the Europe mutual fund market size dedicated to alternatives is projected to triple by 2030, albeit from a low base, contributing marginally but meaningfully to overall diversification. Cross-asset correlations will dictate product development velocity, encouraging managers to bundle multi-asset ESG, climate, and factor overlays into turnkey wrappers for both retail and institutional clients.

By Investor Type: Retail Resilience and Institutional Precision

Retail investors held 56.10% of aggregate AUM in 2025, cementing their pivotal role in the Europe mutual fund market. Digital on-ramps, fee transparency, and the rise of low-minimum thematic funds are expanding participation among first-time investors across Spain, France, and the Nordics. Workplace auto-enrolment schemes are steering incremental salary deferrals into diversified multi-asset funds, mitigating demographic headwinds from aging populations. Regulators have mandated cost-breakdown dashboards, empowering individuals to compare TERs and steering flows toward competitive vehicles, including ELTIFs newly available at USD 1,155 (EUR 1,000) minimums. Meanwhile, institutional investors, responsible for 43.90% of assets, deploy precision mandates driven by solvency and accounting constraints, often insisting on customized ESG exclusions aligned with fiduciary duty. Norwegian and Dutch pension funds boosted European equity exposure by double digits in 2024, capitalizing on sector leadership in renewable-energy and tech enablers. The convergence of retail and institutional preferences on sustainability enables economies of scale for managers, though institutional clients negotiate fee breaks that temper revenue uplift.

Retail growth, forecast at 7.12% CAGR through 2031, depends on continued fintech penetration and robust investor-protection frameworks that maintain confidence after market drawdowns. Robo-platforms educate younger cohorts via gamified apps, while banks deploy hybrid advisory models that blend human coaching with algorithmic rebalancing to preserve legacy relationships. Institutional inflows remain lumpy, tied to AL rebalancing and regulatory capital shifts, yet structured-product wrappers linked to mutual-fund baskets are gaining traction among insurers seeking capital-efficient yield. Harmonized reporting standards under the Corporate Sustainability Reporting Directive foster cross-segment product portability, enabling managers to clone retail strategies for institutional bespoke tranches with minimal incremental cost. Both investor segments now expect real-time ESG metrics and scenario-analysis dashboards, a demand that pressures back-office data infrastructures but strengthens client stickiness once implemented. Fee negotiations gravitate toward performance-linked structures, particularly among institutional allocations to active ESG equity, thereby aligning economics with alpha delivery. Robust custody and trustee supervision help reinforce trust, ensuring that the Europe mutual fund market retains its central position in European household portfolios despite growing ETF competition.

By Distribution Channel: Digital Disruption Reshapes the Value Chain

Banks continued to dominate with a 44.20% share in 2025, yet online platforms logged a blistering 16.85% CAGR that is forecast to persist through 2031. Swift digital onboarding, low fees, and intuitive UX attract millennials and Gen-Z savers who now account for a rising slice of monthly systematic investment plans. Financial advisors remained relevant at 17.60%, serving the complex needs of high-net-worth clients who value estate planning, tax optimization, and bespoke ESG tilts. Direct-to-fund distribution channelled 12.40% of flows, largely via asset-manager websites offering zero-commission subscriptions funded by payment-for-order-flow economics. Open-banking legislation unlocked third-party data aggregation, allowing fintechs to present 360-degree balance sheets and push personalized mutual fund nudges based on cash flow analytics. Banks strike back by embedding robo modules and upgrading mobile interfaces, illustrated by UBS’s digital wealth arm adding 45% AUM in 2024 after integrating AI chatbots for goal planning. Tokenized units traded 24/7 on permissioned blockchains reduce settlement latency, enhancing liquidity perception and appealing to younger investors accustomed to real-time finance.

Platform competition compresses front-end fees but multiplies asset velocity, as frictionless switching rebalances portfolios faster and increases advisory-engagement touchpoints. Regulators monitor inducement models to ensure that zero-commission offers do not hide indirect costs, compelling platforms to display total expense ratios prominently. Banks leverage their balance sheets to wrap funds in insurance-linked savings, an approach that bundles capital guarantees with fund upside, preserving margins even when headline fees fall. Financial-advisor networks adopt holistic wellness frameworks, integrating cash flow planning, pension projections, and ESG preferences into a unified dashboard that enhances stickiness. Direct channels evolve toward community-driven investing with social-sharing features, gamifying progress toward goals, and viralizing thematic fund launches. AML/KYC protocols become API-based, shortening account-opening times to minutes and aligning with European e-ID initiatives, thereby boosting subscription conversion rates. Ultimately, digital engagement deepens investor education and expands the Europe mutual fund market size by tapping unbanked or under-invested cohorts across the continent.

Geography Analysis

The Europe mutual fund market reflects a diverse and evolving landscape, with the United Kingdom, Germany, and France holding leading positions. The UK continues to leverage London’s financial depth and global distribution despite Brexit, while reforms like Mansion House have streamlined fund approvals. Regulatory divergence has spurred innovation, including climate-transition funds aimed at domestic pensions, while fintech clusters and favorable FX dynamics attract international flows. Germany benefits from a strong institutional base and retail engagement driven by tax incentives and ESG product credibility. Established asset managers, favorable savings vehicles, and green-finance alignment with national policy goals propel France’s market. Together, these core markets form the backbone of mutual fund growth across the region.

Southern and Western European countries, Spain, Italy, and the BENELUX bloc, are contributing increasingly to market expansion. Spain leads in forecast growth due to pension reforms and rapid digital adoption among younger savers, while banks drive fund flows through new third-pillar structures. Italy's market skews conservative due to demographics, cs yet sees rising interest in managed payout and target-date solutions, with Milan growing as a fund-servicing hub. BENELUX countries, though small by investor domicile, play an outsized role in fund administration, with Luxembourg acting as a central hub for cross-border UCITS distribution. Regulatory agility and infrastructure advantages make BENELUX a crucial logistical base for global sponsors. These countries' strategic positions support the broader efficiency and competitiveness of the European fund ecosystem.

In Northern and Emerging Europe, innovation and convergence are key growth drivers. The Nordics lead in digital adoption, ESG integration, and tokenization pilots, with strong state and retail alignment around green finance. High incomes and mobile-friendly platforms sustain steady contributions, while local regulators support cutting-edge product experimentation. Emerging markets like Poland and the Czech Republic are catching up via employer-sponsored schemes and improved market access through cross-listed UCITS. Fintech partnerships and digital-only offerings are reducing entry barriers and broadening investor bases. Currency-hedged products and tax reforms enhance appeal among more sophisticated investors. These regions, though varied in maturity, are increasingly important engines of growth for the Europe mutual fund market.

Competitive Landscape

Competition in the Europe mutual fund market remains moderate, with the top five managers holding 30.80% of combined assets, leaving meaningful headroom for mid-sized and niche specialists. BlackRock leads at 9.8%, leveraging broad passive, active, and alternative capabilities and the Aladdin risk-analytics platform that deepens institutional partnerships. Amundi follows at 7.3%, combining scale manufacturing with local-market proximity and recently finalized partnerships that expand U.S. distribution while funneling ESG UCITS back into Europe. Vanguard’s cost-leadership model magnifies passive pressure, while DWS and UBS round out the top five through robust regional wealth networks and focused thematic strategies. Fee compression stimulates consolidation; Goldman Sachs Asset Management’s acquisition of NN Investment Partners underscores the trend toward bolting on European distribution and ESG competence.

Strategic differentiation increasingly rests on sustainable-investing credentials, data-science prowess, and digital client engagement. Firms pour capital into AI infrastructure to automate portfolio construction, classify ESG controversies, and personalize reporting, thereby spreading fixed costs across larger asset bases. Tokenization pilots, such as DWS’s money-market-fund launch on Polygon, showcase attempts to redefine liquidity and settlement speed, forging first-mover advantages in operational efficiency. Partnerships between asset managers and fintechs, typified by Intesa Sanpaolo’s 10-year pact with BlackRock’s Aladdin Wealth, signal a shift toward ecosystem playbooks rather than purely organic buildouts. Middle-office outsourcing gains traction as managers focus on alpha-generation and distribution, handing non-core functions to specialized providers who enjoy economies of scale across multiple sponsors.

Regulation acts as both a moat and a catalyst: MiFID II cost-transparency requirements elevate switching sensitivity, rewarding firms with clean-share structures and competitive TERs; SFDR compliance costs hamper small entrants yet advantage incumbents that amortize data frameworks across hundreds of strategies. Cross-border marketing efficiencies from CMU lower marginal expansion cost, enabling scalable platforms to penetrate secondary markets quickly and crowd out local boutiques without a differentiated edge. Specialty managers able to articulate high-conviction thematic or alternative expertise maintain pricing power despite ongoing fee wars. Overall, innovation, cost discipline, and regulatory fluency determine winners and dictate how quickly the Europe mutual fund market consolidates or fragments over the next five years.

Europe Mutual Fund Industry Leaders

BlackRock

Amundi

DWS Group

Schroders

Allianz Global Investors

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: BlackRock completed its USD 2.55 billion acquisition of Preqin, the alternative investment data provider, significantly enhancing its private markets research capabilities and institutional client servicing infrastructure across European markets.

- December 2024: Amundi announced a strategic partnership with Victory Capital Management to expand its US distribution capabilities while launching 5 new ESG-focused UCITS funds targeting European institutional investors with a combined seed capital of USD 577.50 million (EUR 500 million).

- November 2024: Intesa Sanpaolo signed a 10-year digital wealth management agreement with BlackRock to deploy the Aladdin Wealth platform across its Italian retail banking network, potentially affecting USD 173.25 billion (EUR 150 billion) in client assets.

- October 2024: DWS Group launched Europe's first tokenized money market fund on the Polygon blockchain, enabling fractional ownership and 24/7 trading capabilities for institutional clients seeking enhanced liquidity management.

Europe Mutual Fund Market Report Scope

The report's scope includes an understanding of the European mutual fund industry, regulatory environment, MF companies and their business models, detailed market segmentation, product types, current market trends, changes in market dynamics, and growth opportunities. In-depth analysis of the market size and forecast for the various segments.

Europe's mutual fund companies are segmented by fund type (equity, debt, multi-asset, money market, other fund types), investor type (households, monetary financial institutions, general government, non-financial corporations, insurers and pension funds, and other financial intermediaries), and geography (Luxembourg, Ireland, Germany, France, the United Kingdom, the Netherlands, Italy, and the Rest of Europe).

The report offers market size and forecasts for Europe's mutual fund industry in value (USD) for all the above segments.

By Asset Class

| Equity |

| Bond |

| Hybrid |

| Money Market |

| Others |

By Investor Type

| Retail |

| Institutional |

By Distribution Channel

| Banks |

| Online Platforms |

| Financial Advisors |

| Direct |

By Geography

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| BENELUX (Belgium, Netherlands, Luxembourg) |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) |

| Rest of Europe |

| By Asset Class | Equity |

| Bond | |

| Hybrid | |

| Money Market | |

| Others | |

| By Investor Type | Retail |

| Institutional | |

| By Distribution Channel | Banks |

| Online Platforms | |

| Financial Advisors | |

| Direct | |

| By Geography | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe Mutual Fund Market in 2026?

It reached USD 43.01 trillion in 2026 and is projected to grow at a 3.54% CAGR to USD 51.18 trillion by 2031.

Which asset class holds the biggest share of European mutual-fund assets?

Equity funds lead with a 38.35% share, reflecting sustained demand for growth and ESG-tilted strategies.

Which distribution channel is growing fastest across Europe?

Online investment platforms post the quickest expansion, advancing at a 16.85% CAGR through 2031 as digital engagement deepens.

Why is Spain considered a high-growth mutual-fund market?

Pension reforms that shift responsibility to individuals, coupled with mobile-first platforms, fuel a 9.14% forecast CAGR for Spanish-domiciled assets.

How are demographic trends influencing mutual-fund flows?

Aging populations in Germany and Italy are shifting assets toward income-focused and decumulation strategies, moderating overall equity inflows.

What role does tokenization play in European mutual funds?

Pilot projects such as tokenized money-market funds promise near-instant settlement and fractional ownership, potentially reshaping liquidity and investor access.

Page last updated on: