China Home Loan Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

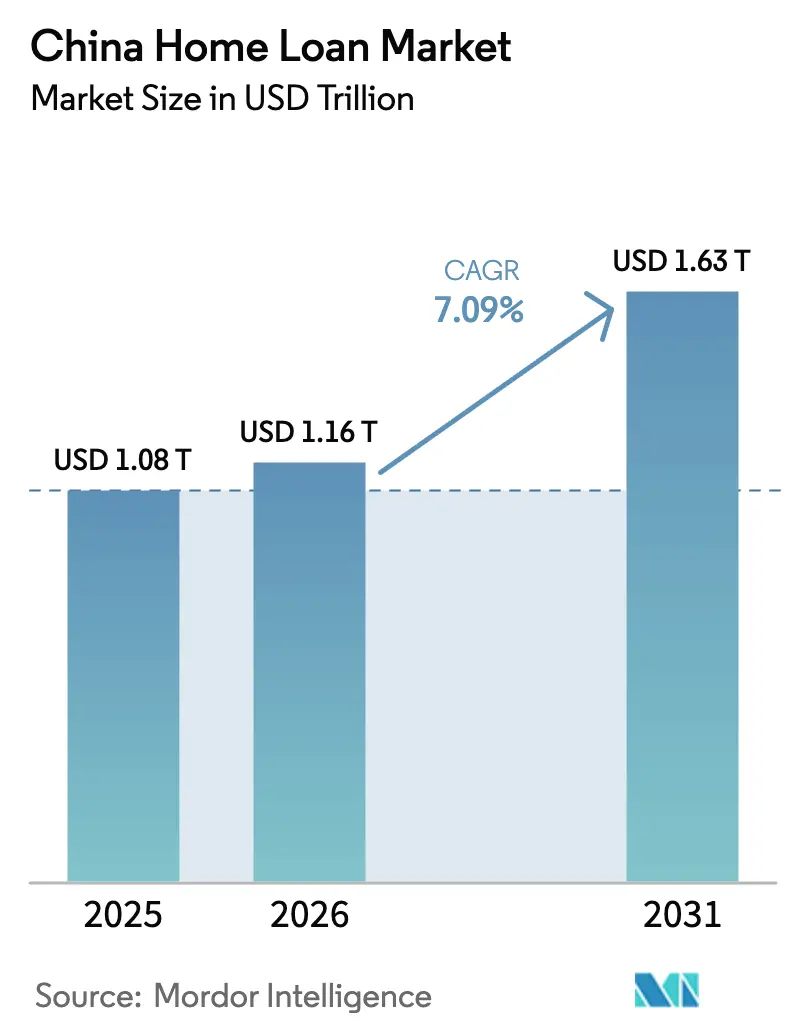

| Base Year Market Size (2025) | USD 1.08 Trillion |

| Market Size (2026) | USD 1.16 Trillion |

| Market Size (2031) | USD 1.63 Trillion |

| Growth Rate (2026 - 2031) | 7.09% CAGR |

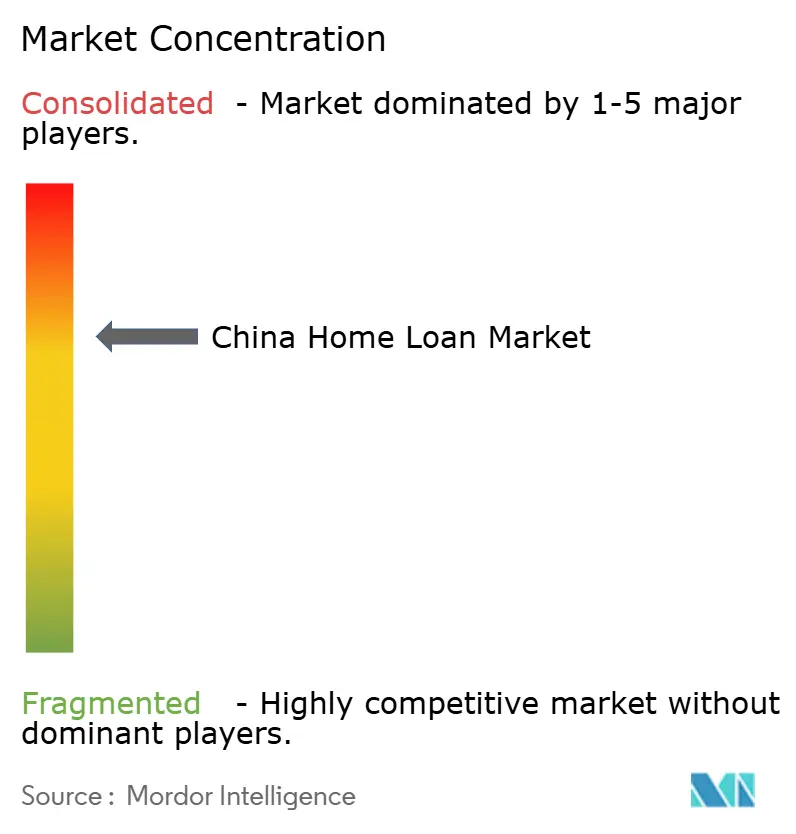

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Home Loan Market Analysis by Mordor Intelligence

The China home loan market size is expected to grow from USD 1.08 trillion in 2025 to USD 1.16 trillion in 2026 and is forecast to reach USD 1.63 trillion by 2031 at 7.09% CAGR over 2026-2031. Policy loosening has been decisive: the People’s Bank of China (PBOC) cut the 5-year Loan Prime Rate (LPR) multiple times in 2024 and removed mortgage-rate floors, while the State Council lowered minimum down payments to 15% for first-time buyers. Liquidity injections such as a CNY 300 billion affordable-housing facility and larger quotas for the Housing Provident Fund have kept credit flowing and cushioned property-developer stress. At the same time, early digitization gains, especially the adoption of AI-driven origination platforms at WeBank and MYbank, are compressing approval times and broadening borrower coverage. Consolidation momentum—encouraged by regulators to shore up capital—signals a structurally tighter yet more resilient competitive arena.

Key Report Takeaways

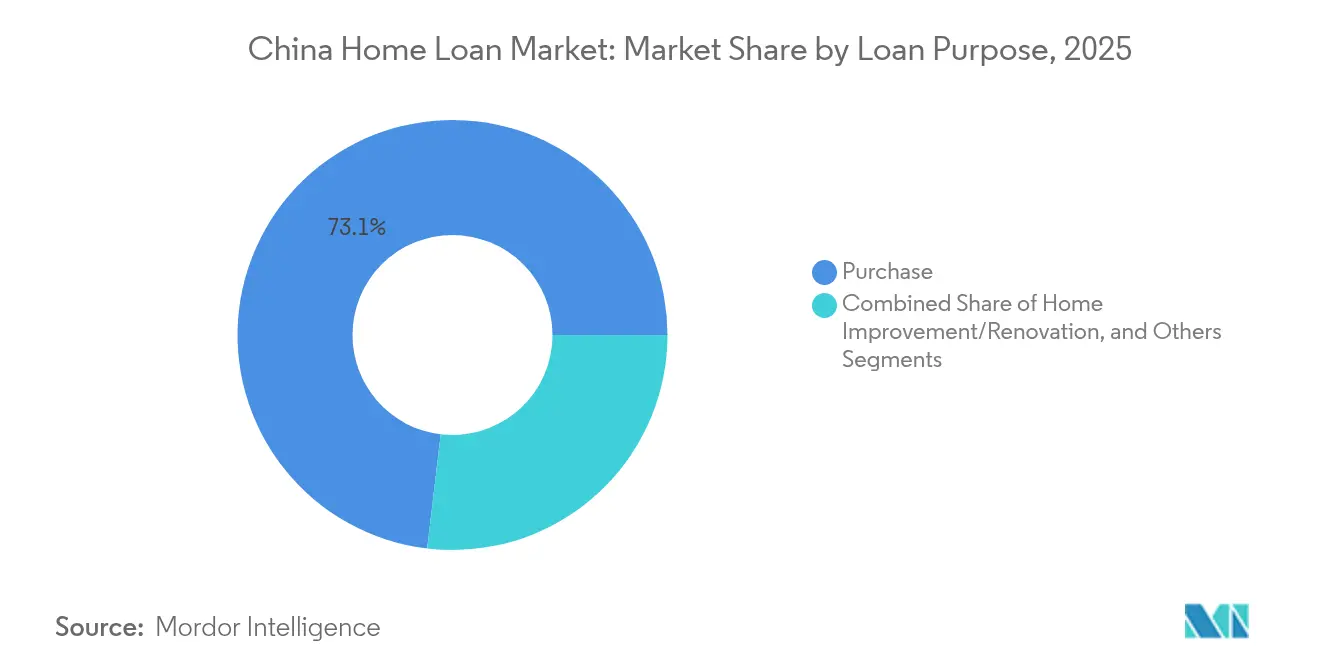

- By loan purpose, purchase loans for new and existing homes held a 73.12% share of the Chinese home loan market in 2025, whereas home-improvement loans are projected to advance at a 8.88% CAGR to 2031.

- By provider, banks controlled 86.23% of the China home loan market share in 2025; the “Others” segment is set to expand at 13.55% CAGR through 2031.

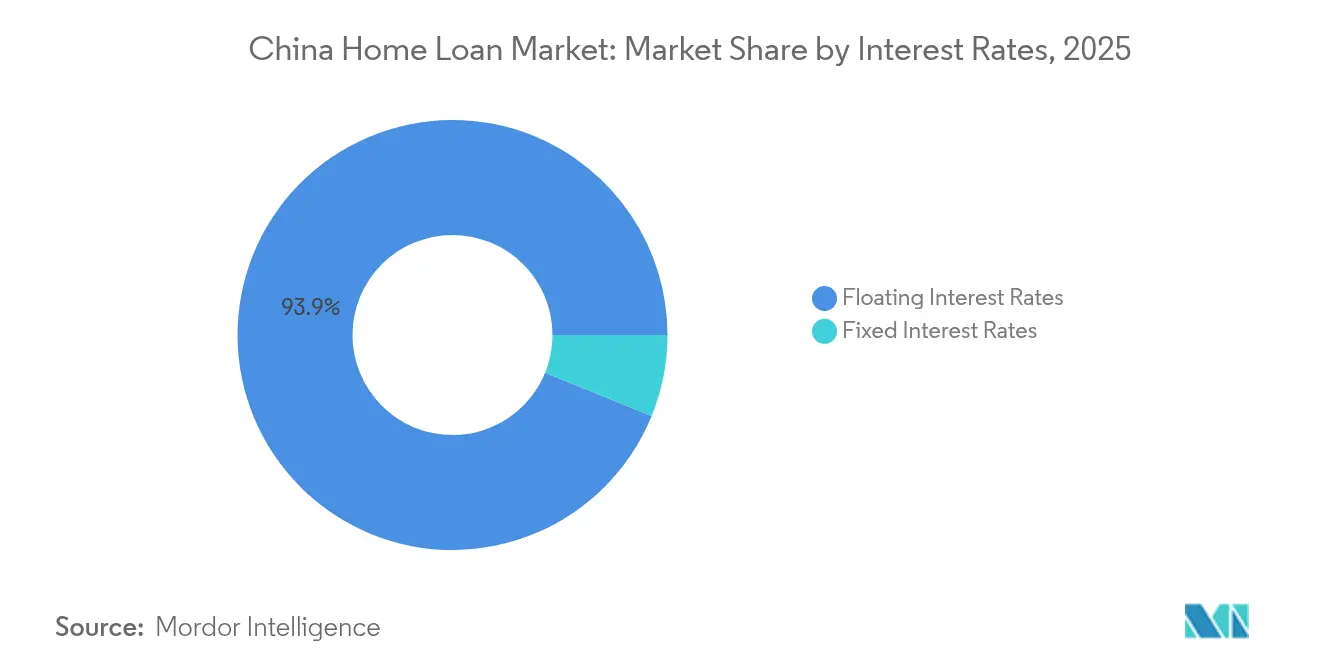

- By interest rate structure, floating-rate products captured 93.85% share of the China home loan market size in 2025, while fixed-rate mortgages are expected to post a 10.36% CAGR through 2031.

- By loan tenure, terms above 20 years accounted for 51.69% of the China home loan market size in 2025; the 11-20 year bracket is projected to grow at an 8.54% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with China representing one among them. The global report on home loan market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

China Home Loan Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Easing mortgage rate & down-payment policies | +1.8% | Tier-1 and national spill-over | Short term (≤ 2 years) |

| LPR cuts & accommodative monetary stance | +1.5% | National | Medium term (2-4 years) |

| Housing Provident Fund expansion | +1.2% | Stronger in tier-2/3 cities | Long term (≥ 4 years) |

| AI-driven digital mortgage origination | +0.9% | Urban centres | Medium term (2-4 years) |

| “Quality-home” upgrade demand (green/smart) | +0.6% | Tier-1 cities, expanding to tier-2 markets | Long term (≥ 4 years) |

| Emerging reverse-mortgage solutions for seniors | +0.3% | National, pilot programs in major cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Easing Mortgage Rate & Down-Payment Policies

The PBOC’s decision to abolish mortgage-rate floors and trim minimum down payments to 15% for first-time buyers marked the boldest easing since 2008[1]People’s Bank of China, “About Mortgage Rate Floors,” pbc.gov.cn. Immediate traction is visible in Beijing, Shanghai, Shenzhen, and Guangzhou, where first-home rates dropped to 3.05%. The measures entice sidelined buyers back into the market, improve affordability for upgraders, and underpin transaction volumes. Local authorities tailor the parameters by city, balancing stimulus with financial-stability safeguards. Confidence benefits from explicit central-government backing, yet the long-term sustainability of ultra-low rates still depends on broader economic recovery.

LPR Cuts & Accommodative Monetary Stance

The 5-year LPR slipped from 4.2% to 3.5% over 2024, illustrating a structural pivot toward demand-side support [2]Trading Economics, “China Cuts 5-Year LPR,” tradingeconomics.com. Banks have been instructed to re-price outstanding mortgages lower by roughly 50 basis points, amplifying household cash-flow relief. Fiscal coordination—primarily through larger affordable-housing budgets—reinforces the transmission. Nevertheless, net-interest-margin compression is pressing banks toward tighter cost controls, limiting the room for deeper cuts absent stronger GDP or trade momentum.

Housing Provident Fund Expansion

Outstanding mortgages funded via the Housing Provident Fund rose in 2024 as banks grew cautious on property exposure. The fund’s sub-market rates and government guarantee diversify risk away from commercial balance sheets. Digitalized workflows have slashed approval times, spurring adoption in tier-2 and tier-3 cities. Yet contribution inflows hinge on wage growth, exposing the fund to macro-cycle swings.

AI-Driven Digital Mortgage Origination

WeBank’s cloud-native model now serves 400 million retail users and 4.5 million SMEs, validating AI as a scalable origination engine. Ping An Bank’s in-house algorithms automate document checks and credit scoring, lifting productivity and extending credit to data-light gig-economy borrowers [3]The Asian Banker, “Ping An Bank Deploys AI,” theasianbanker.com. Regulatory sandboxes facilitate rapid rollout, though data-privacy scrutiny and potential algorithmic bias remain closely watched by the China Banking and Insurance Regulatory Commission.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Housing-price volatility & underwater risk | -1.4% | Pronounced in tier-1 | Short term (≤ 2 years) |

| Surge in early mortgage prepayments | -0.8% | Major urban centers | Medium term (2-4 years) |

| Lending-cap rules on banks’ real-estate exposure | -0.7% | National | Long term (≥ 4 years) |

| Credit-risk rise among gig-economy borrowers | -0.5% | Urban centers, particularly tier-1 and tier-2 cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Housing-Price Volatility & Underwater Risk

Price declines across major cities in 2024 triggered pockets of negative equity that raised delinquency risk and curtailed fresh lending [4]National Bureau of Statistics, “Residential Price Trends 2024,” stats.gov.cn. Lenders responded by front-loading risk buffers and hiking down payments for high-beta districts. Underwater households accelerated repayments, shrinking outstanding portfolios when credit expansion is most needed. Targeted micro-policy relief—such as differentiated rate caps—offsets part of the stress but cannot fully shield balance sheets if broad deflation were to persist.

Surge in Early Mortgage Prepayments

Prepayment volumes spiked in 2024 as borrowers reallocated savings to debt reduction amid weak investment yields. The phenomenon strained mortgage-backed securities cash flows and compressed fee income at originators. Banks now face a balancing act: discouraging uneconomic prepayments while avoiding punitive barriers that could spark consumer backlash.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Loan Purpose: Purchase Loans Drive Market Foundation

Purchase loans accounted for 73.12% of the Chinese home loan market in 2025. Benefiting from preferential down-payment rules and LPR-linked pricing, this segment underpins primary-residence demand. The China home loan market size for home-improvement financing is far smaller but is charting a 8.88% CAGR to 2031 as households refurbish ageing stock and tap subsidies for green upgrades.

Policy emphasis on energy-efficient retrofits broadens lender product suites, while digital portals simplify small-ticket loan origination. Conversely, construction and refinancing loans stay muted because developers face funding constraints, and rate differentials between legacy and new mortgages are narrow. Green-building programs spearheaded by local governments nudge lenders to offer rate discounts, a trend likely to add depth to the renovation niche.

By Provider: Traditional Banks Face Digital Disruption

Banks held 86.23% of the Chinese home loan market share in 2025, underscoring systemic dominance. Other providers are scaling at 13.55% CAGR, propelled by data-driven risk analytics that unlock underserved borrower pools.

Traditional banks are counter-punching through cloud-migration projects and API partnerships; Ping An Bank’s upgraded mobile platform trimmed average approval to under 3 days while ICBC rolled out pre-approval chatbots across 300 cities. Housing Finance Companies, although specialized, lack capital heft and are increasingly seeking tie-ups or merger opportunities to stay relevant. For pure-play fintechs, profitability hinges on maintaining asset-quality discipline as they extend deeper into tier-3 markets.

By Interest Rates: Floating Rates Dominate Amid Policy Volatility

Floating-rate loans, benchmarked to the LPR, made up 93.85% of the Chinese home loan market share in 2025, reflecting borrower expectations of further easing. Yet rising economic uncertainty is nudging a subset of customers toward rate certainty, driving a 10.36% CAGR outlook for fixed-rate products.

Lenders are experimenting with hybrid mortgages that lock a fixed rate for the first 3-5 years before reverting to a float. Such designs preserve margin flexibility for banks yet give borrowers payment stability in the early years. Regional regulators retain discretion to impose minimum spreads, creating scope for competitive positioning across provinces.

By Loan Tenure: Long-Term Financing Reflects Affordability Pressures

Loans above 20 years represented 51.69% of the Chinese home loan market share in 2025, a testament to stretched price-to-income ratios in first-tier hubs. Medium-tenure buckets (11-20 years) are expanding at 8.54% CAGR as borrowers aim to cut lifetime interest while staying within manageable monthly outlays.

Demographic shifts matter: younger households favor longevity to maximize leverage, whereas older cohorts match tenures with projected retirement cash flows. Banks have rolled out step-up repayment schedules and partial principal-holiday options to accommodate income volatility. Parallel pilot programs in reverse-mortgage products could, over time, smooth the exit path for ageing owners, though cultural acceptance remains low.

Geography Analysis

Market depth varies sharply by region. Tier-1 cities retain the largest absolute share of the Chinese home loan market, buoyed by high household incomes, robust employment, and comparatively liquid secondary markets. Beijing’s average first-home rate dipped to 3.05% after the September 2024 policy reset, catalyzing a modest pickup in transactions. However, underwater risk is most acute here, reinforcing risk-adjusted pricing discipline.

Tier-2 and tier-3 cities now deliver the strongest volume momentum thanks to preferential Local Government financing packages and Housing Provident Fund penetration. The China home loan market size within these cohorts is forecast to outgrow tier-1 aggregates over 2026-2031 as lower entry prices intersect with urbanization inflows. Banks, seeing thinner margins in saturated coastal megacities, are redeploying origination capacity inland and partnering with municipal platforms to de-risk exposure.

Western and northeastern provinces remain structurally weaker because of net population outflows and limited industrial diversity. Even so, central-government infrastructure grants and industrial-relocation incentives may gradually brighten credit demand in selected prefectures. Fintech uptake is patchier in these regions as network coverage lags, allowing large state-owned banks to preserve incumbent strengths for the near term.

Mordor Intelligence provides coverage of the home loan market across other key regional markets. Detailed country-level analysis extends to India, United States, and Brazil incorporating local coverage and market participation, as required.

Competitive Landscape

The market structure is concentrated: the top banks hold major shares in the market, and together with leading joint-stock lenders, they account for a considerable market share. Regulatory pushes for consolidation—evidenced by regional bank rescue mergers—support financial stability but also entrench dominance.

Digital-first challengers have seized share in unsecured and SME lending and are now attacking mortgage niches by leveraging AI credit engines that tap alternative data sets. WeBank’s 2023 results highlight a cost-to-income ratio of around 27%, far below traditional peers, enabling competitive pricing. Still, deposit-gathering constraints curb their scale relative to the behemoths.

Strategically, large banks emphasize end-to-end digitization: ICBC won Asia-Pacific’s “Best Consumer Digital Bank” award in May 2024 after deploying a generative-AI-powered virtual assistant. Meanwhile, the Agricultural Bank of China accelerated county-level mortgage expansion in 2025, leveraging branch density to serve peri-urban migration corridors. Foreign banks, despite policy liberalization, continue to lose ground due to compliance burdens and geopolitical frictions.

China Home Loan Industry Leaders

Industrial & Commercial Bank of China (ICBC)

China Construction Bank

Agricultural Bank of China

Bank of China

Postal Savings Bank of China

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Agricultural Bank of China disclosed above-peer loan growth in county markets.

- March 2025: Ping An Insurance posted a 47.8% YoY profit jump; Ping An Bank’s NPL ratio stood at 1.06%.

- March 2025: China Construction Bank extended CNY 190 million to a Suzhou tech firm under a new M&A pilot.

- September 2024: PBOC launched a programme to cut rates on 50 million existing mortgages by 50 basis points.

China Home Loan Market Report Scope

A home loan is an amount an individual borrows from a financial institution such as a housing finance company to buy a new or resale home, construct a home, or renovate or extend an existing one. China's Home Loan Market is segmented By Purpose (Home Purchase, Refinance, Home Improvement, Construction, Other (Re-Sale, etc.), By End User (Employed Individuals, Professionals, Students, Entrepreneurs, Other (Homemakers, Unemployed, Retired, etc.)), By Tenure Period (less than 5 years, 6-10 years, 11-24 years, and 25-30 years). The report offers market size and forecasts for the Mom and Pop Stores Market in value (USD Million) for all the above segments.

| Purchase (New/Existing) |

| Home Improvement/Renovation |

| Others (Construction, Refinance, etc.) |

| Banks |

| Housing Finance Companies |

| Others |

| Fixed Interest Rates |

| Floating Interest Rates |

| Less Than or Equal To 10 Years |

| 11 – 20 Years |

| Longer Than 20 Years |

| By Loan Purpose | Purchase (New/Existing) |

| Home Improvement/Renovation | |

| Others (Construction, Refinance, etc.) | |

| By Provider | Banks |

| Housing Finance Companies | |

| Others | |

| By Interest Rates | Fixed Interest Rates |

| Floating Interest Rates | |

| By Loan Tenure | Less Than or Equal To 10 Years |

| 11 – 20 Years | |

| Longer Than 20 Years |

Key Questions Answered in the Report

What is the current value of the China home loan market?

The China home loan market is valued at USD 1.16 trillion in 2026.

How fast is the China home loan market expected to grow?

It is projected to expand at a 7.09% CAGR, reaching USD 1.63 trillion by 2031.

Which segment is growing the fastest within the Chinese home loan market?

Home-improvement and renovation loans are forecasted to grow at a 8.88% CAGR through 2031.

Why do floating-rate mortgages dominate China’s market?

Floating-rate loans account for 93.85% of the market because borrowers expect further LPR cuts and value rate flexibility.

How are digital banks impacting the China home loan industry?

Digital-native lenders like WeBank are shortening approval times, widening borrower access, and are forecast to grow their loan books at double-digit CAGRs, challenging traditional banks.

What risks could restrain market growth?

Key risks include housing-price volatility that creates underwater mortgages and a surge in early prepayments that erode banks’ interest income.

Page last updated on: