Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

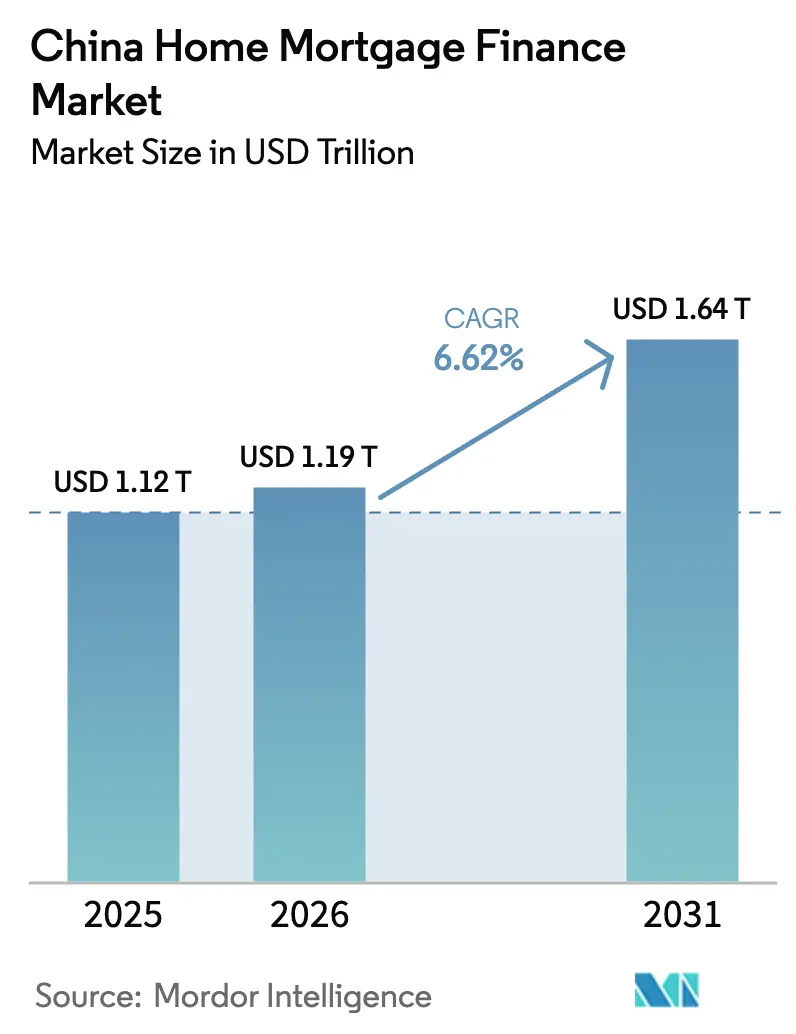

| Base Year Market Size (2025) | USD 1120 Trillion |

| Market Size (2026) | USD 1.19 Trillion |

| Market Size (2031) | USD 1.64 Trillion |

| Growth Rate (2026 - 2031) | 6.62% CAGR |

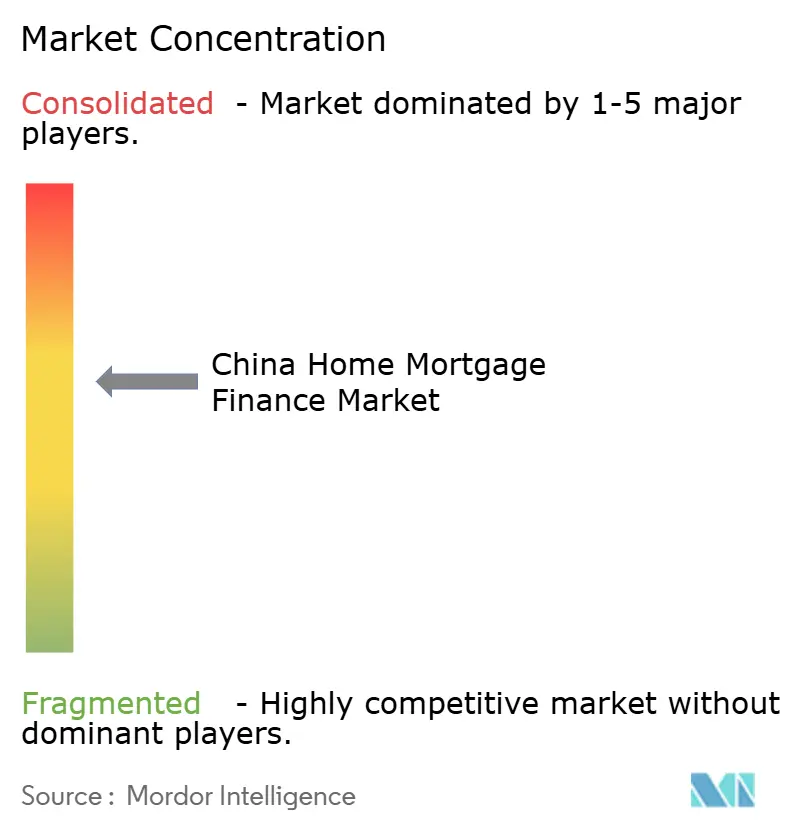

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Home Mortgage Finance Market Analysis by Mordor Intelligence

The Chinese home mortgage finance market size was valued at USD 1120 billion in 2025 and estimated to grow from USD 1194.14 billion in 2026 to reach USD 1644.98 billion by 2031, at a CAGR of 6.62% during the forecast period (2026-2031). The current growth path highlights the market’s resilience as policymakers use targeted rate cuts and down-payment relaxations to steady demand. Lower loan prime rates, the removal of nationwide mortgage-rate floors, and a one-time 50-basis-point reduction applied to outstanding mortgages have lifted affordability for more than 50 million households[1]Government of China, “State Council Briefing on Property Market Stabilisation,” gov.cn. Demand is also diversifying home-improvement loans, green-mortgage products, and refinancing packages, growing faster than traditional purchase loans as homeowners shift toward upgrading existing properties. Simultaneously, digital-first origination channels operated by leading banks and fintechs are compressing processing times, improving risk pricing, and broadening access to mortgage credit. The market’s long-term outlook remains constructive despite demographic pressure because lenders are redeploying capital released through residential mortgage-backed securities (RMBS), and the Housing Provident Fund is stepping up concessional lending.

Key Report Takeaways

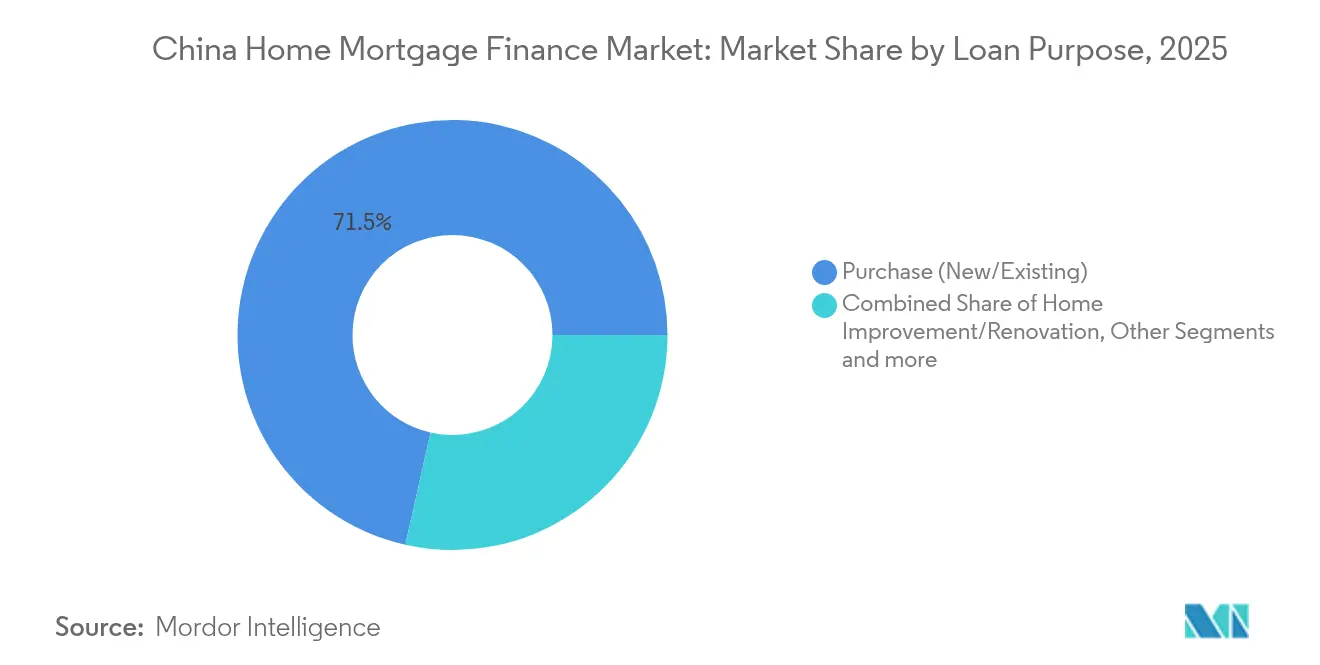

- By loan purpose, purchase mortgages for new and existing homes held 71.48% of the China home mortgage finance market share in 2025, while home-improvement and renovation loans post the fastest 8.52% CAGR through 2031.

- By provider, banks dominated with 84.00% share of the China home mortgage finance market in 2025; the “others” segment, led by digital lenders, records the highest 13.1% projected CAGR.

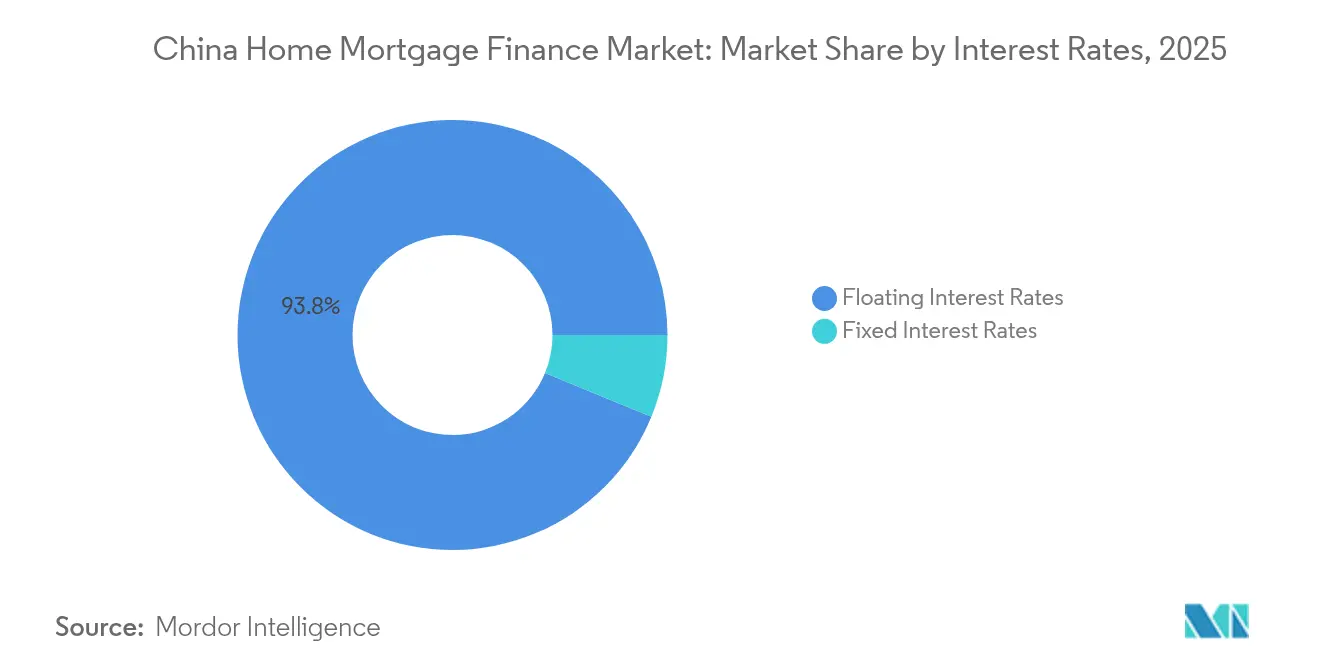

- By interest rate type, floating-rate mortgages accounted for a 93.80% stake of the China home mortgage finance market size in 2025; fixed-rate products are expected to grow at a 10.05% CAGR.

- By loan tenure, mortgages longer than 20 years captured 49.05% of the China home mortgage finance market size in 2025 and are advancing at an 8.22% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Home Mortgage Finance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government policy easing on mortgage rates & down-payments | +1.8% | National; stronger effects in tier-1 cities | Short term (≤ 2 years) |

| Expansion of Housing Provident Fund lending capacity | +1.2% | National; concentrated in urban centers | Medium term (2-4 years) |

| Urbanization-led demand in lower-tier cities | +0.9% | Tier-3 and tier-4 cities | Long term (≥ 4 years) |

| Digital end-to-end mortgage origination by major banks | +0.7% | National; early adoption in major cities | Medium term (2-4 years) |

| Emergence of green-mortgage products tied to building efficiency | +0.5% | National; focus on new construction areas | Long term (≥ 4 years) |

| Mortgage-backed securitization, unlocking bank capital | +0.4% | National; benefits large banks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Policy Easing on Mortgage Rates & Down-Payments

A September 2024 directive from the People’s Bank of China lowered existing mortgage coupons by 50 basis points, trimming annual payments by CNY 150 billion (USD 21.3 billion) and reducing minimum down-payments for first and second homes to 15%[2]People’s Bank of China, “Mortgage Rate Adjustment for Existing Loans,” pbc.gov.cn. By scrapping the nationwide mortgage-rate floor, authorities allowed lenders to compete aggressively on pricing, creating a dual stimulus for new originations and refinancing. These coordinated measures support borrower cash flows and shore up confidence at a time of subdued property sales. Banks now recalibrate funding strategies to balance lower asset yields with volume gains, highlighting the pivotal role of policy in shaping the Chinese home mortgage finance market.

Expansion of Housing Provident Fund Lending Capacity

Outstanding balances in the Housing Provident Fund have significantly increased, while total fund assets have also grown substantially, providing the subsidized scheme with ample capacity to offer long-term, below-market mortgages[3]Ministry of Housing and Urban-Rural Development, “2024 Housing Provident Fund Report,” mohurd.gov.cn. Recent rule changes raised individual borrowing limits and broadened eligibility, allowing the fund to relieve the commercial-bank segment during periods of developer stress. Because loans are priced 100–150 basis points below market, the program catalyzes demand from middle-income households and stabilizes origination volumes in the China home mortgage finance market.

Urbanization-Led Demand in Lower-Tier Cities

More than 60% of China’s GDP and housing stock sit in tier-3 and tier-4 cities, which also host 78% of new housing construction activity. Accelerated urbanization, industrial relocation, and infrastructure build-outs sustain mortgage appetite in these locales even as major metropolitan areas mature. Lenders diversify geographically to tap these pockets of growth, but must account for elevated inventory levels and slower income growth that can raise credit-risk volatility over time.

Digital End-to-End Mortgage Origination by Major Banks

WeBank and similar platforms have demonstrated that machine-learning-driven underwriting can cut processing costs by up to 70%, shrinking the application-approval cycle from weeks to days. Traditional banks are moving quickly to launch comparable mobile-first journeys, embedding real-time credit scoring, optical character recognition for document upload, and e-signature tools. End-to-end digitization enhances borrower experience, lowers compliance errors, and differentiates early adopters in the China home mortgage finance market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prolonged property-developer distress is depressing buyer confidence | -2.1% | National; severe in tier-1 cities | Short term (≤ 2 years) |

| Demographic headwinds are reducing household formation | -1.4% | National; pronounced in aging regions | Long term (≥ 4 years) |

| Surge in early repayments squeezing bank net-interest margins | -0.8% | National; affects all major lenders | Short term (≤ 2 years) |

| Regulatory crackdown on quasi-mortgage consumer loans | -0.6% | National; focus on shadow-banking activity | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Prolonged Property-Developer Distress Depressing Buyer Confidence

Roughly half of private developers remain financially strained, leaving high inventories of unfinished units and deterring off-plan purchases, the historical sales model for new homes. A government “whitelist” mechanism has channeled bank funding to select projects, yet consumers still weigh execution risk carefully, prolonging transaction cycles and tempering the growth trajectory of the China home mortgage finance market.

Demographic Headwinds Reducing Household Formation

Official projections show China’s population dipping below 1.39 billion by 2035, with declining fertility and accelerated aging lowering new-household formation rates. Fewer new households translate to structurally lower baseline demand for primary dwellings and, by extension, mortgages. Lenders are therefore pivoting to renovation finance, green upgrades, and equity-release products to offset anticipated volume softness.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Loan Purpose: Expansion of Enhancement-Focused Lending

Purchase loans for new or existing homes held a 71.48% stake of the Chinese home mortgage finance market in 2025, underscoring their central role in household property transactions. Yet, home-improvement loans register the quickest 8.52% CAGR as owners favor upgrade projects over relocation amid subdued price appreciation. Demand is encouraged by policy subsidies supporting energy-efficient retrofits and urban-renewal grants, nudging lenders to design products that pair renovation finance with building-performance certification. Loan-against-property products serve commercial liquidity needs, whereas construction bridge loans and refinancing packages accommodate borrowers seeking rate optimization under the current low-rate environment.

Growth momentum in the enhancement category signals a maturation of housing consumption patterns. Banks now underwrite larger average balances, given rising material costs and technology-intensive renovations. For credit-risk control, institutions incorporate property-value buffers and stage-payment disbursement schedules tied to verified work completion. These practices safeguard collateral quality while fostering the continued expansion of the China home mortgage finance market.

By Provider: Fintech Challenge to Incumbent Banks

Banks commanded 84.00% the Chinese home mortgage finance market share in 2025, benefiting from deposit-funding advantages and regulatory familiarity. Joint-stock and city commercial banks, however, face margin compression, prompting them to partner with technology vendors to digitize onboarding and reduce operating expenses per loan. Other providers are gaining ground at a 13.1% CAGR by emphasizing seamless mobile interfaces, fast approval cycles, and data-rich credit-scoring models.

Regulatory authorities encourage responsible innovation, granting digital banks-controlled test environments (“regulatory sandboxes”) to pilot smart-contract-based collateral management. The resulting competition accelerates product diversification, improves customer experience, and gradually redistributes volumes within the Chinese home mortgage finance market.

By Interest Rates: Growing Preference for Rate Certainty

Floating-rate mortgages still commanded 93.80% the Chinese home mortgage finance market share in 2025. However, fixed-rate products are forecasted to expand at a robust 10.05% CAGR between 2026-2031 as borrowers seize historically low coupons to stabilize monthly outlays. Banks supply fixed tenures of 3, 5, and 10 years, plus hybrids that switch to floating after an introductory period, thereby broadening choices within the China home mortgage finance market.

Tighter fixed-floating spreads cut the “insurance premium” for payment certainty. Lenders deploy interest-rate swaps and structured deposits to manage the growing share of fixed-rate assets on their balance sheets.

By Loan Tenure: Longer Repayment Horizons Boost Affordability

Mortgages longer than 20 years secured 49.05% of the China home mortgage finance market size in 2025 and are projected to expand at an 8.22% CAGR. Extended schedules reduce monthly payments, making ownership feasible even in high-cost metros such as Beijing and Shenzhen. Products within the 11–20 year range service middle-income cohorts that balance payment comfort with total-interest considerations. Tenures under 10 years appeal mostly to affluent borrowers consolidating short-term liabilities or leveraging rate-cut opportunities to extinguish mortgage debt quickly.

To mitigate long-dated credit-risk exposure, lenders integrate dynamic income verification and periodic collateral re-appraisal during the loan life cycle. Coupled with credit-insurance partnerships, these safeguards preserve asset quality while supporting the affordability objectives that underpin the continued growth of the Chinese home mortgage finance market.

Geography Analysis

Mortgage origination remains concentrated in tier-1 cities, where sizeable loan balances and liquid secondary markets prevail. April 2025 rate cuts dragged first-time buyer coupons in Beijing to 3.05%, spurring a modest revival in transaction volumes. Despite elevated price-to-income ratios, employment density and migration inflow sustain baseline demand, allowing lenders to market premium advisory services alongside standard mortgages.

Tier-2 urban centers such as Hangzhou and Nanjing capture incremental demand released by the relaxation of purchase restrictions and targeted subsidy schemes. Regional banks leverage their granular knowledge of local zoning rules and developer reputations to compete effectively against national lenders. Cross-selling of bundled financial services—wealth management, insurance, and retail payments—further cements customer relationships in this layer of the China home mortgage finance market.

Lower-tier cities shoulder the mantle of medium-term growth as industrial relocation and infrastructure corridors continue to attract rural migrants. Mortgage penetration ratios still trail those of coastal metros, offering headroom for responsible expansion. Nevertheless, lenders apply tighter loan-to-value caps and risk-adjusted pricing to accommodate higher idiosyncratic volatility stemming from demographic outflows and macro-cycle sensitivity.

Competitive Landscape

The competitive landscape of the Chinese home mortgage finance market is moderately consolidated. The “Big Four” state-owned banks—Industrial and Commercial Bank of China, China Construction Bank, Agricultural Bank of China, and Bank of China—control a majority of outstanding balances due to extensive branch footprints and explicit sovereign support. Their scale ensures funding cost advantages but also exposes them to market-wide margin compression as the loan prime rate trend declines. To protect profitability, these incumbents pivot toward fee-based cross-selling, centralized risk analytics platforms, and streamlined back-office operations.

Joint-stock and regional banks occupy a critical middle ground, combining local market intimacy with growing digital competence. Strategic alliances with fintechs supply modern interfaces, alternative credit data, and automated valuation models, helping these lenders defend niches within the Chinese home mortgage finance market. For instance, Ping An Bank leverages the parent group’s integrated finance-and-health ecosystem to embed property-related wellness and insurance solutions, reinforcing customer stickiness.

Digital-native players, most prominently WeBank, deploy cloud-native architectures and application-programming-interface (API) connectivity to underwrite at scale while maintaining lean cost structures. Continuous iteration based on near-real-time customer analytics unlocks product personalization that traditional banks find challenging to replicate quickly. Regulatory endorsement of such innovation, balanced with strict prudential oversight, ensures sector stability as competition intensifies.

China Home Mortgage Finance Industry Leaders

China Construction Bank

Industrial and Commercial Bank of China

Agricultural Bank of China

Bank of China

Bank of Communications

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Ping An Insurance reported a 47.8% profit jump to RMB 126.607 billion for 2024, with Ping An Bank’s corporate-loan book growing 12.4% and non-performing loans steady at 1.06%.

- October 2024: National commercial banks executed a coordinated mortgage-rate cut, setting first- and second-home coupons 30 basis points below the prevailing loan prime rate, impacting more than 90% of outstanding loans.

- September 2024: The People’s Bank of China announced a comprehensive property-support package that lowered existing mortgage rates by 50 basis points and cut minimum down-payments on second homes from 25% to 15%.

- May 2024: Authorities abolished the nationwide mortgage-rate floor and provided CNY 300 billion in funding for state-linked firms to purchase unsold units for conversion into affordable housing.

China Home Mortgage Finance Market Report Scope

Home mortgage finance will back a loan to buy a house with a guarantee, also called collateral. They are used to buy a home or borrow money against the value of your home. A bank, mortgage company, or financial institution to purchase a primary residence, a secondary residence, or an investment residence.

The China home mortgage finance market is segmented by type of lender (banks and House Provident Fund [HPF]), by financing options (personal new housing loan, personal second-hand housing loan, and personal Housing Provident Fund (Portfolio) Loan), and by type of mortgage (fixed and variable). The report offers market size and forecasts for the China Home Mortgage Finance Market in value (USD million) for all the above segments.

By Loan Purpose

| Purchase (New/Existing) |

| Home Improvement/Renovation |

| Loan Against Property |

| Others (Construction, Refinance, etc.) |

By Provider

| Banks |

| Housing Finance Companies |

| Others |

By Interest Rates

| Fixed Interest Rates |

| Floating Interest Rates |

By Loan Tenure

| ≤ 10 Years |

| 11 – 20 Years |

| More than 20 Years |

| By Loan Purpose | Purchase (New/Existing) |

| Home Improvement/Renovation | |

| Loan Against Property | |

| Others (Construction, Refinance, etc.) | |

| By Provider | Banks |

| Housing Finance Companies | |

| Others | |

| By Interest Rates | Fixed Interest Rates |

| Floating Interest Rates | |

| By Loan Tenure | ≤ 10 Years |

| 11 – 20 Years | |

| More than 20 Years |

Key Questions Answered in the Report

What is the current size of the Chinese home mortgage finance market?

It stands at USD 1.19 trillion in 2026 and is projected to reach USD 1.64 trillion by 2031, reflecting a 6.62% CAGR.

How have recent PBOC policies affected mortgage affordability?

A 50 basis-point cut on existing loans and removal of nationwide rate floors lowered monthly payments for more than 50 million households, lifting near-term affordability.

Which loan-purpose segment is growing fastest?

Home-improvement and renovation mortgages expand at an 8.52% CAGR as owners prioritize upgrades over buying new homes.

Why are fixed-rate mortgages gaining traction in China?

Borrowers increasingly value payment certainty and are locking in historically low coupons; fixed-rate products now grow at a 10.05% CAGR.

What role does the Housing Provident Fund play in mortgage finance?

The outstanding balances in the Housing Provident Fund have significantly increased, while total fund assets have also grown, providing the subsidized scheme with ample capacity to offer long-term, below-market mortgages.

How are digital-only banks impacting competition?

Platforms like WeBank use automated underwriting and mobile-first interfaces to cut origination costs and attract tech-savvy borrowers, nudging incumbents to accelerate digital transformation.

Page last updated on: