Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

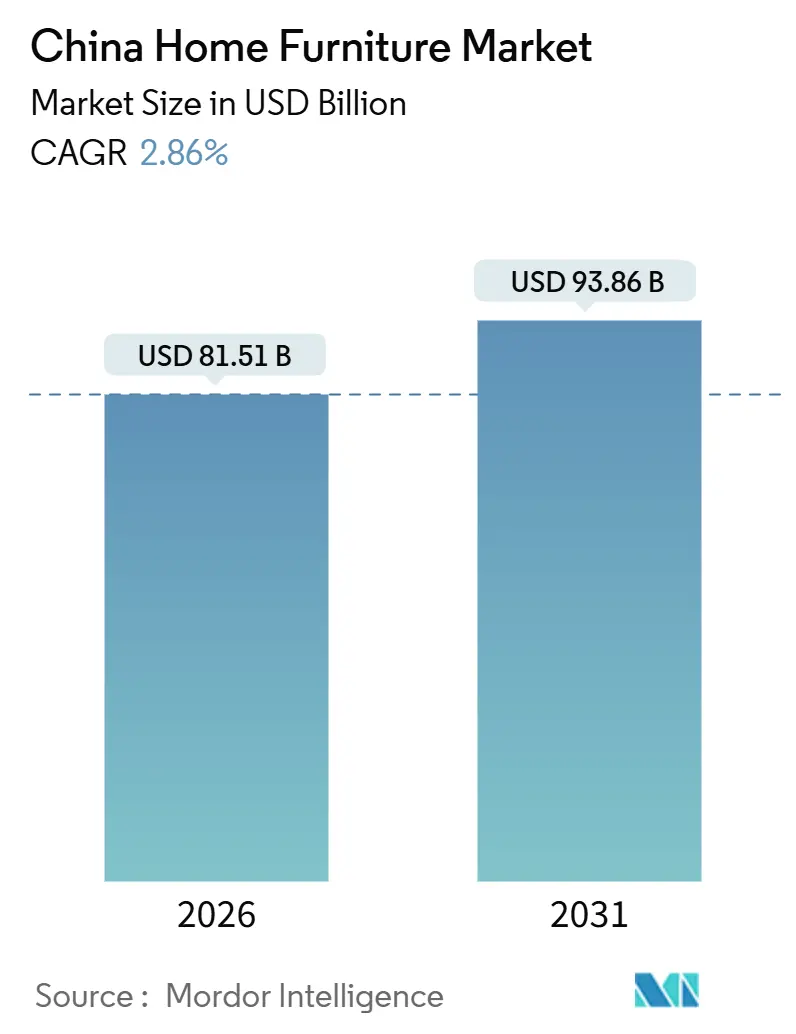

| Market Size (2026) | USD 81.51 Billion |

| Market Size (2031) | USD 93.86 Billion |

| Growth Rate (2026 - 2031) | 2.86% CAGR |

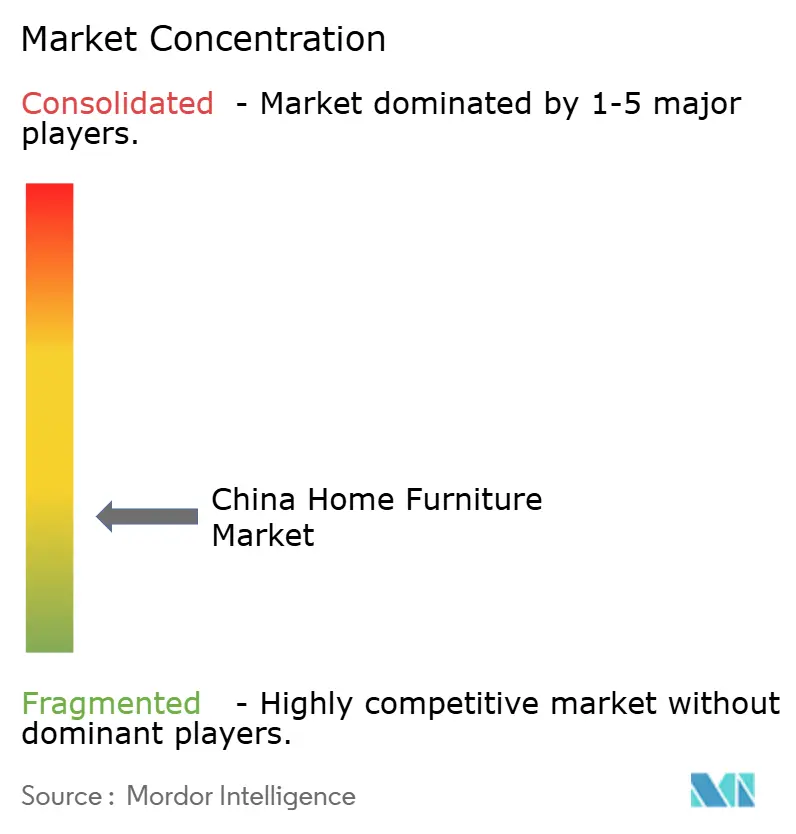

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Home Furniture Market Analysis by Mordor Intelligence

The China Home Furniture Market size is estimated at USD 81.51 billion in 2026, and is expected to reach USD 93.86 billion by 2031, at a CAGR of 2.86% during the forecast period (2026-2031).

The demand mix is shifting from new-home purchases to renovation-led replacement cycles as national trade-in subsidies scale, and local programs target aging-in-place upgrades. Smart features, elderly-friendly designs, and circular-economy models are moving into the mainstream and support higher average selling prices in the premium tier. Supply chains continue to diversify into Southeast Asia and Mexico to mitigate tariff exposure, while core components and design remain anchored in China. Online channels gain traction through livestream commerce and augmented reality (AR) visualization, compressing delivery times and improving conversion, while offline retail recalibrates to smaller formats and service-led experiences.

Key Report Takeaways

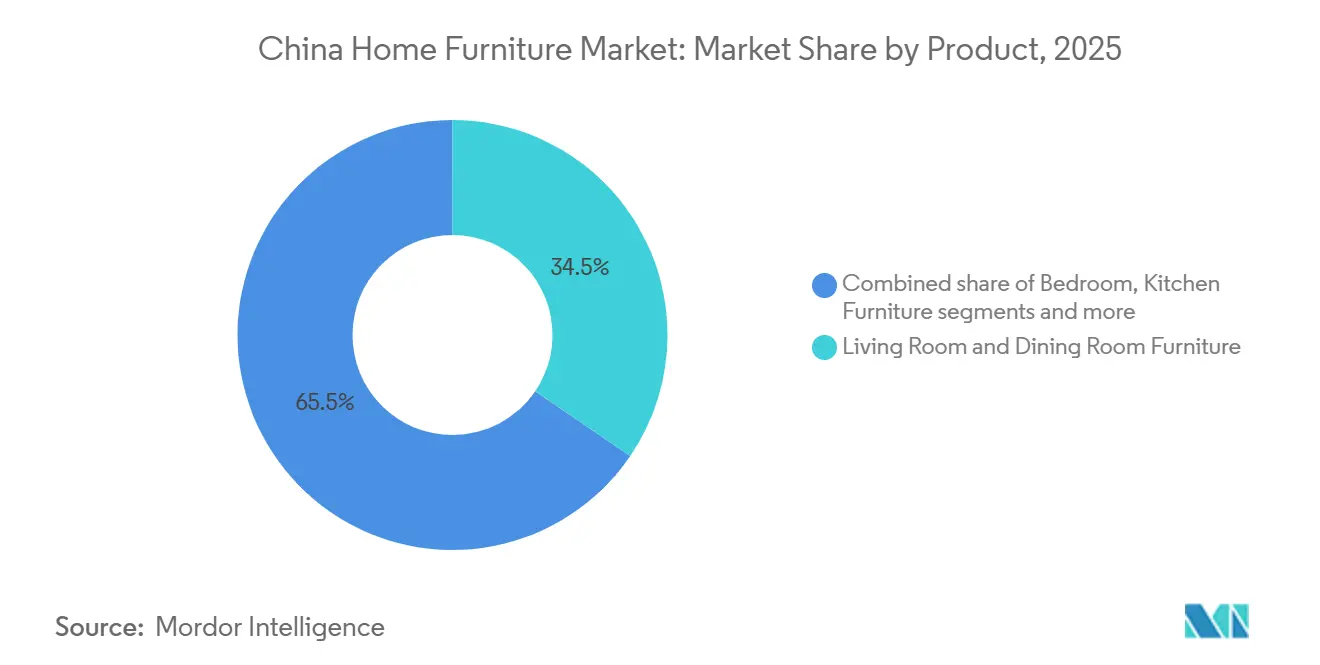

- By product type, living room and dining room furniture led with a 34.52% revenue share in 2025, while home office furniture recorded the fastest growth at a 3.51% CAGR through 2031.

- By material, wood held a 49.81% share in 2025, and plastic and polymer posted the highest growth at a 2.98% CAGR through 2031.

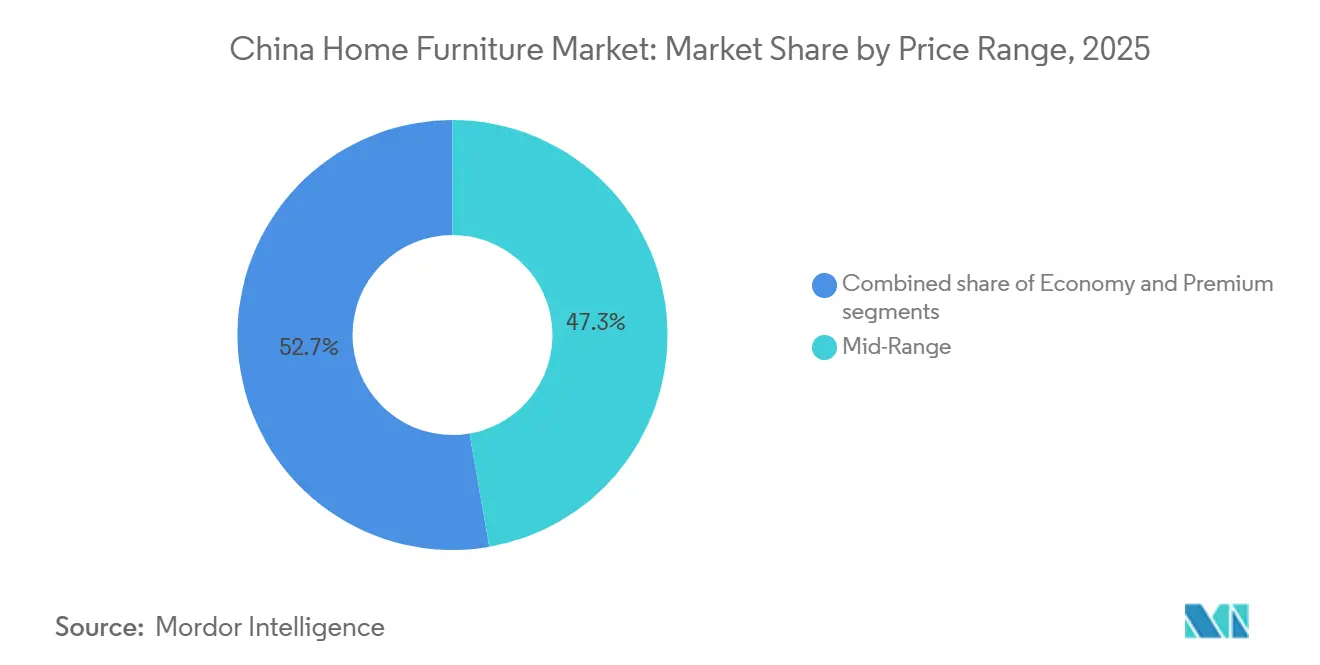

- By price range, mid-range products accounted for a 47.27% share in 2025, while premium products advanced at a 3.14% CAGR through 2031.

- By distribution channel, home centers captured a 39.33% share in 2025, and online channels expanded at a 4.02% CAGR through 2031.

- By geography, Eastern China represented a 35.13% share in 2025, and Western China registered the fastest growth at a 3.34% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Home Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Trade-in subsidies for the urban middle class | +0.9% | National, with early gains in Guangzhou, Foshan, Shanghai, and Beijing | Short term (≤ 2 years) |

| Second-hand-home renovations surge | +0.7% | APAC core in Eastern China, spill-over to Central and Western regions | Medium term (2-4 years) |

| E-commerce logistics for bulky goods | +0.6% | Tier-1 and Tier-2 cities, with broader national coverage by 2027 | Medium term (2-4 years) |

| Smart-home connected furniture growth | +0.5% | First-tier cities, expanding to Tier-2 | Medium term (2-4 years) |

| Eco-certified wood and bamboo adoption | +0.2% | Global export markets and the domestic premium segment | Long term (≥ 4 years) |

| Elderly-friendly home-mod subsidy programs | +0.1% | National, concentrated in aging cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Urban Middle-Class Trade-In Subsidies Drive Replacement Cycles

A national consumer goods trade-in program is converting incremental renovation intent into realized furniture demand. The program was formalized in January 2025 and provides rebates of 15% for general purchases, 20% for energy or water-efficient products, and up to 30% for aging-in-place items, with provincial caps and an enterprise co-discount structure that can deliver total savings near 40% on eligible kitchen renewals. Retail sales of furniture by enterprises above a designated size rose 20.2% year over year from January to April 2025, with April up 26.9%, outpacing broader retail and confirming velocity in replacement cycles. Authorities report the policy has leveraged trillions of yuan in related consumption and will be extended into 2026, sustaining demand for subsidy-eligible product lines and compressing purchase cycles in mid-range and premium price bands. Brands that pre-certify products, simplify redemption, and coordinate logistics capture the lion’s share of traffic as consumers prioritize convenience and eligibility transparency. This policy wave favors the China home furniture market as a whole, and it strengthens the premium tier where energy and aging-friendly compliance is more common.[1]Ministry of Commerce, “Notice on 2025 Home Decoration, Kitchen and Bathroom Renewal Work,” Ministry of Commerce, mofcom.gov.cn

Surge in Second-Hand-Home Renovations Unlocks Installed-Base Monetization

Renovation demand is rising as households focus on upgrading older units rather than furnishing new builds. Between 2019 and 2024, hundreds of thousands of residential compounds underwent upgrades that benefited tens of millions of households, creating steady replacement demand for space-optimized kitchens, wardrobes, and bathroom units. Reports show old-house refurbishment requests rising double digits year over year, with partial kitchen and bathroom remodels climbing faster as buyers in tier-two and tier-three cities pursue targeted improvements. Projects financed by owners and municipalities result in complete refurnishing as floor plans change and utilities are modernized. Policymakers signal an integrated approach to new and resale housing, including the acquisition of existing units for affordable housing, which increases the pipeline for bulk procurement of standardized furniture sets. Companies that tailor modular ranges and deliver fast, low-disruption installations are well positioned to convert this installed base in the China home furniture market.

Rapid E-Commerce Logistics for Bulky Goods Compresses Last-Mile Friction

Last-mile capabilities for large items have improved, making online purchasing of sofas, cabinets, and beds more practical for urban households. Online sales of home-related goods reached CNY 1.02 trillion in 2024, and online furniture accounted for a larger share of leading retailers’ revenue as livestream content, AR try-ons, and white-glove delivery support the category experience. National Express delivery rules now formalize packaging and collaboration requirements, lowering friction in fulfillment and returns while aligning with green standards. IKEA’s e-commerce pivot in China, including a major marketplace partnership, illustrates how incumbents blend platform ecosystems with store networks to enhance reach and service for bulky SKUs. Digital content such as 3D models and AR showrooms increases engagement and reduces returns, which supports margins in a category where logistics costs can be high. These developments reinforce the structural channel shift within the China home furniture market in favor of online discovery and omnichannel conversion.[2]Xilinmen as cited via China Daily, “From Furniture to Technology,” China Daily, chinadaily.com.cn

Growth of Smart-Home Connected Furniture Elevates Unit Economics

Connected furniture is evolving from novelty to expected functionality in urban homes. A notable example is L4 intelligent certification under the national furniture intelligence assessment standard for a sleep system that dynamically adjusts firmness and integrates aromatherapy and lighting, signaling maturity in sensor integration and control algorithms. Premium adjustable beds and app-connected components command higher prices and grow share in bedroom and home office spending. Brands that deploy AI-driven design and rapid-installation services use smart features to bundle entire room solutions and to lock customers into compatible ecosystems. Younger buyers show strong interest in integrated systems and use online platforms to research and configure options before committing. As price points normalize and interoperability improves, connected offerings expand beyond first-tier cities and broaden the addressable base within the China home furniture market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile timber and metal input costs | -0.5% | National, acute in export hubs | Short term (≤ 2 years) |

| Property-market slowdown in lower-tier cities | -1.3% | Most acute in Tier-3 and Tier-4 cities, spill-over to national new construction | Medium term (2-4 years) |

| Stricter VOC and formaldehyde standards for SMEs | -0.3% | National, heavier in SME clusters | Medium term (2-4 years) |

| Ultra-low-cost cross-border platform competition | -0.4% | Export-facing regions and mass-market exporters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Timber and Metal Input Costs Compress Margins and Planning

Exposure to imported timber introduces currency and freight volatility into unit economics, especially for solid wood and veneer-rich ranges. Domestic timber output remains insufficient relative to consumption, which increases reliance on supply from North America, Europe, and Southeast Asia and raises sensitivity to regulatory and logistics shocks. Stricter limits on hazardous substances under GB 18584-2024 accelerate a shift to certified plantations and low-emission materials, which improves compliance but adds cost pressure during the transition. Metal components also face cycles driven by energy costs and environmental curbs on smelting, which can tighten supply at peak demand. Large integrated manufacturers mitigate some of this risk through long-term contracts and internal component production, while small and medium firms adapt through flexible sourcing or rationalized portfolios. These input dynamics heighten the need for precise forecasting and modular design in the China home furniture market to avoid working-capital strain and obsolescence.

Property-Market Slowdown in Lower-Tier Cities Erodes New-Home Furnishing Demand

Residential sales contracted over 2024 and weakened further in early 2025, with new construction starts declining sharply, reducing the flow of newly furnished homes. The impact is uneven, with first-tier cities showing resilience while lower-tier markets struggle with inventory and price corrections that dampen discretionary spend. The share of completed home purchases has risen as buyers avoid off-plan risks, which shifts furnishing patterns away from complete packages to targeted upgrades. A national push to stabilize the housing market and repurpose existing units into affordable housing will take time to translate into broad-based furniture demand. Renovation and trade-in policies help offset this headwind by focusing spend on replacement and room-by-room upgrades. The net effect is slower growth for new-construction-dependent categories in the China home furniture market and faster growth for modular and retrofit-friendly lines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Home Office Gains While Living and Dining Remain the Anchor

Living room and dining room furniture accounted for 34.52% of the China home furniture market size in 2025 as household budgets continued to prioritize seating, tables, and entertainment units that define shared spaces. This category bundles effectively with kitchen and storage, which helps multi-category retailers capture value across a project and leverage trade-in eligibility to pull forward replacements. Home office posted a 3.51% CAGR to 2031 as hybrid work practices persist in tier-two hubs and drive demand for ergonomic seating, height-adjustable desks, and compact storage that fits secondary rooms. Bedroom, the next largest category, benefits from smart sleep and mattress upgrades that command higher prices and link to wellness priorities among urban buyers. Kitchen projects monetize subsidized renewal work, where fast installation and certified materials reduce disruption and meet compliance standards. Bathroom furniture grows as households refresh fixtures and storage under a partial-renovation model that is suited to occupied apartments. Outdoor furniture adds incremental volume through balcony and rooftop use cases as urban living adapts to limited space. This mix sustains category diversity and supports the China home furniture market through multiple demand channels.

Growth in home office is reinforced by digital content that helps buyers compare ergonomic options and visualize setups in smaller rooms. Bedroom adoption of connected features, including adjustable frames and environmental controls, points to steady premiumization within sleep products. Kitchen and dining upgrades align with stacked subsidies that reduce out-of-pocket costs for qualified components, which shortens decision cycles and increases ticket sizes for bundled solutions. Bathroom storage and vanities win share when brands offer compact, moisture-resistant designs that install quickly in older buildings. Outdoor lines gain traction through lightweight and weather-resistant materials that support e-commerce shipping and easy assembly. Installation services and service-level guarantees differentiate offers across categories as consumers expect low-disruption experiences in occupied homes. Category leaders invest in modularity to simplify upgrades without full replacements, which is aligned with renovation-prone demand. These dynamics help the China home furniture market maintain breadth while repositioning for replacement-led cycles.

By Material: Certified Wood Stays Dominant as Plastic and Polymer Improve Logistics Economics

Wood retained a 49.81% share of the China home furniture market in 2025 as consumers continued to value solid-wood aesthetics and durability, and as engineered panels improved performance and compliance. Adoption of certified timber and low-emission panels accelerated under GB 18584-2024, which set stricter limits on formaldehyde and other hazardous substances and drove a shift to water-based coatings. Plastic and polymer posted a 2.98% CAGR through 2031 as weight advantages reduced shipping costs and supported online distribution for bulky items. Metal frames and components remain common in seating and storage as durability complements wood or polymer surfaces in high-use rooms. Bamboo accelerated as a renewable alternative in export-facing lines, supported by processing advances and growing acceptance in stress-bearing applications. The materials mix reflects a balance between compliance, logistics efficiency, and consumer preference, which stabilizes supply in the China home furniture market.

Certified sourcing initiatives support export access and green procurement. Companies enrolled in responsible-wood programs gain credibility with hotel and institutional buyers and reduce friction in customs for developed markets. Plastic and polymer designs take a share in online channels as lighter SKUs reduce damage and lower last-mile costs. Metal lines track energy dynamics and environmental restrictions on smelting, which affect pricing and availability at times of peak demand. Bamboo products benefit from rapid growth cycles and strong carbon absorption, which enhance sustainability narratives in premium ranges. Better upstream choices and compliance discipline across materials enhance brand resilience and margin quality in the China home furniture industry.

By Price Range: Premium Growth Leans on Smart Features and Design Services

Mid-range accounted for 47.27% of 2025 sales as households balanced function, durability, and modularity at accessible price points. Premium advanced at a 3.14% CAGR through 2031 and captured buyers seeking design-led solutions, integrated smart features, and materials with certified provenance. Trade-in incentives and renovation subsidies channel demand toward compliant, longer-lasting products, which supports higher average selling prices and service bundles. Premium ranges attach services such as in-home design, expedited installation, and system integration, which create differentiation beyond materials. Mid-range lines compete through value engineering, flat-pack designs, and omnichannel visibility that ease selection and delivery. Economy ranges face pressure from low-cost online competition, where logistics and price transparency drive rapid comparisons. These trends underpin a gradual shift to quality and service in the China home furniture market.

Premium adoption is also supported by aging-in-place programs that reimburse a portion of eligible products and improve accessibility and safety in existing homes. Smart sleep systems and app-controlled lighting capture high-income buyers who value wellness and convenience, anchoring premium bedroom and living room sets. Renovation-focused services compress timelines from weeks to days for targeted areas, which helps consumers manage disruption and accelerates turnover for installers. Design platforms and pre-certified components reduce administrative friction under subsidy programs and drive upsell of sustainable materials. Mid-range products benefit when technology costs decline and once-premium features migrate down the price ladder. These dynamics support broader category participation while progressively raising quality expectations in the China home furniture market.

By Distribution Channel: Online Scales on Livestream Commerce and AR Visualization

Home centers held a 39.33% share in 2025 as shoppers continued to test comfort, inspect finishes, and compare modular solutions in person. Online posted a 4.02% CAGR through 2031 as livestream selling, interactive content, and managed delivery reduced frictions associated with bulky items. Category content on large platforms grew rapidly and drove pre-purchase research and brand consideration for smart and modular products. Marketplaces and retailer apps invested in 3D models and AR try-ons that help buyers visualize fit and color in tight urban spaces, which lowers return rates. White-glove delivery, timed appointments, and stand-alone assembly services improve the experience threshold for online channels. Omnichannel strategies blend showroom touchpoints with digital journeys and flexible fulfillment, which lifts conversion and retention. These channel dynamics widen the addressable base for the China home furniture market.

Offline formats are also evolving toward smaller urban locations with curated assortments, design services, and pickup options that complement digital discovery. Regulations on packaging and green delivery spur investments in electric fleets and coordinated carrier protocols that enhance service and reduce cost. Marketplace partnerships give manufacturers instant reach without building proprietary last-mile networks, particularly in larger cities. Specialty stores retain importance in premium where material selection and bespoke configurations require in-person engagement. Online and offline integration strengthens service differentiation and stabilizes margins in a category with high logistics intensity. As best practices spread, channel selection reflects product complexity, basket size, and service expectations. The result is a more balanced and resilient go-to-market model for the China home furniture market.

Geography Analysis

Eastern China accounted for 35.13% of market in 2025 as integrated clusters supported manufacturing density, supplier networks, and export channels. The region’s legacy strengths include panel processing, upholstery, and a deep set of accessory suppliers that reduce lead times for custom orders. As tariffs reshape export routes, producers in coastal hubs recalibrate toward domestic demand, EU buyers, and Belt and Road destinations. Investment in design and R&D rises as firms move up the value chain and reduce reliance on pure OEM. Compliance with new substance limits and safety standards is stricter in large clusters where scale supports testing and certification infrastructure. These factors allow Eastern China to remain an anchor of the China home furniture market while it adjusts to slower new-home sales and diversifying exports.

Southern China remains a core export and innovation base with multinational networks that reduce tariff impact and ensure coverage across regions. Leading manufacturers operate plants in Vietnam and Mexico, enabling near-market production for North America and ASEAN and improving delivery speed. Domestic sales experienced pressure as household sentiment weakened, but renovation-driven purchases and subsidy alignment helped keep factory lines utilized. Compliance capabilities and vertical integration provide cost stability during material swings and environmental restrictions. Partnerships with marketplaces and logistics providers support bulky-goods e-commerce in major urban centers. Over the medium term, the region is expected to benefit from premiumization, smart integration, and green procurement, which favor larger and more compliant operators in the China home furniture market.

Western China marks the fastest regional growth at a 3.34% CAGR through 2031 as inland manufacturing scales and westbound logistics mature. Xinjiang suppliers leverage local resources and rail corridors to Central Asia and Europe, which reduces transit time and bypasses some tariff-sensitive routes. Central China’s metro hubs add capacity for customization and serve growing urban populations in adjacent provinces. Northern clusters maintain cost advantages in panel furniture and support value segments in lower-tier cities. North-East cities stabilize with refurbishment demand in older housing stock, which drives targeted purchases in kitchens and bathrooms. These regional patterns diversify production footprints and open new export paths while the China home furniture market continues to balance domestic replacement cycles with selective international orders.

Competitive Landscape

Competition is fragmented across thousands of enterprises, with consolidation pressure rising due to environmental compliance and export headwinds. Scale players expand overseas capacity to manage tariffs while maintaining core component production and design in China. National substance limits and safety standards tighten quality controls and increase barriers to entry, which supports share gains for manufacturers with in-house labs and certified supply chains. Marketplace partnerships and smaller urban showrooms provide reach and service without expensive big-box footprints. In premium, smart integration, sustainability credentials, and design IP help justify higher prices and insulate margins. These strategies support resilience for leaders in the China home furniture market while smaller firms either specialize or exit.[3]CIRS C&K Testing, “Limit of Hazardous Substances of Furniture (GB 18584-2024),” CIRS, cirs-ck.com

Several operators advanced international expansion and innovation. One producer detailed a multi-country production footprint spanning Asia, Europe, and North America, reducing lead times and navigating stacked tariffs on specific categories. A major cabinet and whole-home customization brand opened new showrooms in the Middle East to tap construction and remodeling demand linked to regional development plans. Smart sleep brands obtained national-level intelligent product certifications for connected systems and integrated those into broader bedroom portfolios. These moves show how companies in the China home furniture market align capacity, channel presence, and product features with shifting demand and rules of trade.[4]Man Wah Holdings, “Annual Report 2024/25,” Man Wah, manwahholdings.com

Certification and green sourcing are now strategic levers. Enrollment in FSC initiatives and procurement of certified timber support access to international tenders and hospitality projects. Compliance with GB standards on hazardous substances, flammability for children’s furniture, and structural safety reduces regulatory risk in domestic markets and simplifies export documentation. Companies that link design platforms with subsidy eligibility, aging-in-place requirements, and smart integrations deepen customer stickiness and capture repeat purchases over the life of a home. As standards and consumer expectations rise together, product leadership and compliance capabilities determine who scales in the China home furniture market.

China Home Furniture Industry Leaders

Oppein Home Group

Kuka Home

Suofeiya Home Collection

Man Wah Holdings

IKEA (China)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Oppein Home Group inaugurated four flagship showrooms in Saudi Arabia in Riyadh, Al Hasa, Buraydah, and Madinah, extending its whole-house customization footprint in a market with rising home-improvement demand linked to Vision 2030 programs.

- December 2025: Man Wah Holdings acquired US upholstery maker Gainline Recline Intermediate Corp., adding local capacity in the United States during a period of elevated tariffs on Chinese-origin upholstered goods.

- November 2025: Kuka Home announced plans to invest in a new overseas production base in Kendal Industrial Park, Indonesia, consistent with China-plus-one diversification in the furniture value chain.

- September 2025: IKEA China outlined a restructuring that includes closing seven large-format stores from February 2026 and opening more small-format locations in major cities while growing marketplace partnerships.

China Home Furniture Market Report Scope

The China home furniture market comprises a wide range of furniture products designed to meet the functional, aesthetic, and lifestyle needs of households across urban and rural settings. The market is segmented by product, material, price range, distribution channel, and geography. By product, the market is segmented into living room & dining room furniture, bedroom furniture, kitchen furniture, home office furniture, bathroom furniture, outdoor furniture, and other furniture. By material, the market is segmented into wood, metal, plastic & polymer, and others. By price range, the market is segmented into economy, mid-range, and premium. By distribution channel, the market is segmented into home centers, specialty furniture stores, online, and other distribution channels. By geography, the market is segmented into Eastern China, Northern China, Southern China, Central China, Western China, and North-East China. The report offers the market size in value terms in USD for all the above-mentioned segments.

By Product

| Living Room & Dining Room Furniture |

| Bedroom Furniture |

| Kitchen Furniture |

| Home Office Furniture |

| Bathroom Furniture |

| Outdoor Furniture |

| Other Furniture |

By Material

| Wood |

| Metal |

| Plastic & Polymer |

| Others |

By Price Range

| Economy |

| Mid-Range |

| Premium |

By Distribution Channel

| Home Centers |

| Specialty Furniture Stores |

| Online |

| Other Distribution Channels |

By Geography

| Eastern China |

| Northern China |

| Southern China |

| Central China |

| Western China |

| North-East China |

| By Product | Living Room & Dining Room Furniture |

| Bedroom Furniture | |

| Kitchen Furniture | |

| Home Office Furniture | |

| Bathroom Furniture | |

| Outdoor Furniture | |

| Other Furniture | |

| By Material | Wood |

| Metal | |

| Plastic & Polymer | |

| Others | |

| By Price Range | Economy |

| Mid-Range | |

| Premium | |

| By Distribution Channel | Home Centers |

| Specialty Furniture Stores | |

| Online | |

| Other Distribution Channels | |

| By Geography | Eastern China |

| Northern China | |

| Southern China | |

| Central China | |

| Western China | |

| North-East China |

Key Questions Answered in the Report

What is the current size and growth outlook for the China home furniture market?

The China home furniture market size is USD 81.51 billion in 2026 and is projected to reach USD 93.86 billion by 2031 at a 2.86% CAGR, reflecting a shift from new-home furnishing to renovation-driven replacement cycles.

Which segments lead demand within the China home furniture market?

Living and dining room furniture leads by share, while the home office posts the fastest growth as hybrid work persists and buyers in tier-two hubs invest in ergonomic and modular setups.

How are distribution channels evolving in the China home furniture market?

Home centers still hold the largest share, but online is the fastest-growing channel due to livestream selling, AR visualization, and integrated white-glove delivery that reduce last-mile friction.

What regulations are shaping product strategy in the China home furniture market?

GB 18584-2024 tightens limits on hazardous substances and is pushing the adoption of low-VOC materials and certified wood, while additional standards for safety and flammability are narrowing compliance gaps for children’s products.

Which regions are driving growth across the China home furniture market?

Eastern China remains the volume anchor with deep supply chains, while Western China grows fastest as Xinjiang leverages Belt and Road logistics to expand exports to Central Asia and Europe.

What differentiates premium offerings in the China home furniture market?

Premium lines integrate smart features, certified materials, and service bundles such as design and rapid installation, which support higher prices and better unit economics during renovation-led purchase cycles.

Page last updated on: