Zinc Chemicals Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Volume (2025) | 4.55 Million tons |

| Market Volume (2030) | 5.67 Million tons |

| Growth Rate (2025 - 2030) | 4.47% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Zinc Chemicals Market Analysis by Mordor Intelligence

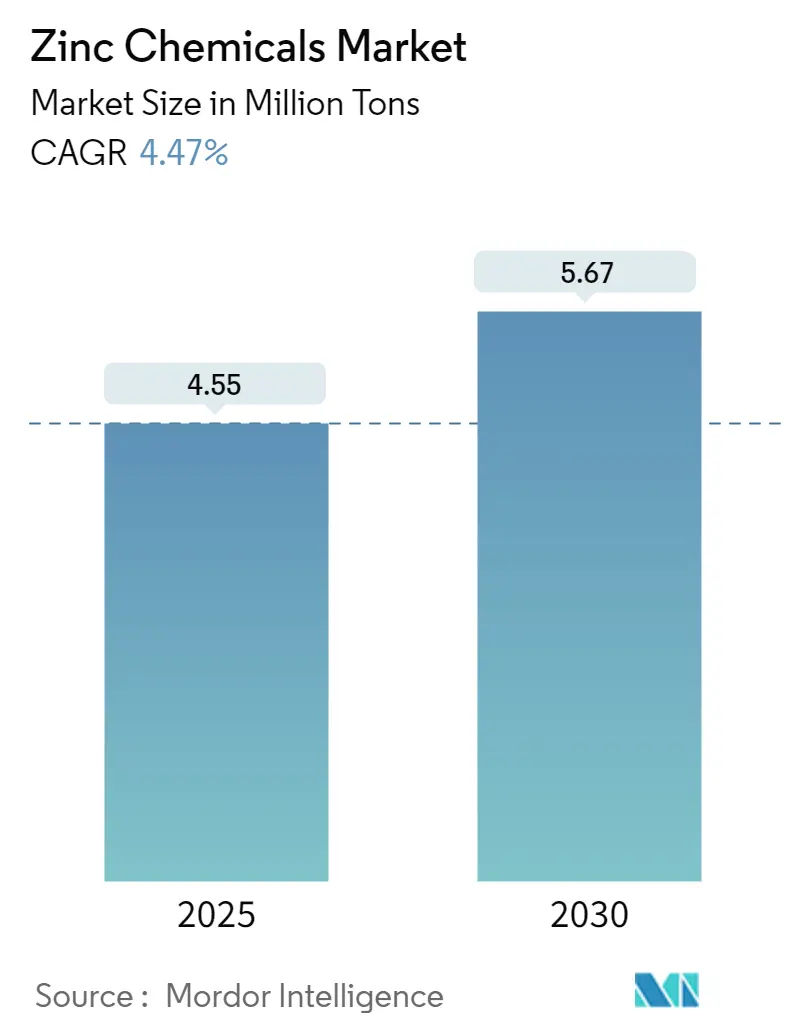

The Zinc Chemicals Market size is estimated at 4.55 million tons in 2025, and is expected to reach 5.67 million tons by 2030, at a CAGR of 4.47% during the forecast period (2025-2030).

The zinc chemical industry is experiencing significant transformation driven by evolving global industrial dynamics and technological advancements. The electronics and semiconductor sector has emerged as a crucial growth driver, with the global electronics market showing robust regional variations in growth rates. According to industry data, while Asia led with 7% growth in 2022, Europe maintained a steady 6% growth rate, demonstrating the sector's resilience and expanding applications of zinc chemicals in electronic components. The increasing integration of zinc-based materials in advanced electronic applications, particularly in semiconductor manufacturing and emerging technologies, has created new avenues for market expansion.

The construction and infrastructure sector continues to be a significant consumer of zinc chemicals, particularly in anti-corrosion applications and protective coatings. Major infrastructure initiatives across various regions are driving demand, with Chile alone targeting construction projects worth USD 24.5 billion by the end of 2024. The growing emphasis on sustainable construction practices and the increasing use of zinc-based protective coatings in green building projects have created new opportunities for market players, particularly in developing economies where infrastructure development remains a priority.

The pharmaceutical and healthcare sectors are witnessing increased adoption of zinc compounds in various applications. The pharmaceutical industry's continued investment in research and development, particularly in zinc nanoparticle applications for medical imaging and cancer treatment, represents a significant shift in market dynamics. The emergence of zinc-based materials in advanced medical applications and therapeutic solutions has opened new growth avenues, with research institutions and pharmaceutical companies increasingly focusing on zinc-based innovations for healthcare applications.

The market is experiencing notable technological advancements in production processes and application methodologies. Manufacturers are increasingly focusing on developing high-purity zinc chemicals for specialized applications, particularly in the electronics and pharmaceutical sectors. The industry is witnessing a shift towards more sustainable production methods and environmentally friendly applications, with companies investing in research and development to meet evolving regulatory requirements and customer preferences. This transformation is particularly evident in the development of new zinc-based materials for emerging applications in renewable energy and environmental protection.

Global Zinc Chemicals Market Trends and Insights

Rising Utilization in the Automotive Industry

Zinc chemicals have emerged as crucial components across various automotive applications, from manufacturing components to enhancing vehicle performance and durability. The compounds are extensively used in the production of automotive engine oils, where zinc oxide's primary function is to reduce engine oxidation, corrosion, and wear. Additionally, zinc chemicals are utilized in manufacturing zinc dithiophosphates and specialist lubricants and grease formulations, such as high-temperature or high-pressure greases specifically designed for automotive applications. The shift toward electric vehicles has further amplified the demand, particularly for zinc chloride batteries, which are emerging as one of the most promising systems for medium to large energy storage applications due to their advantages in energy density, cell voltage, and cost-effectiveness.

The automotive sector's increasing focus on corrosion resistance and durability has led to greater incorporation of zinc chemicals in various manufacturing processes. Zinc oxide blended natural fiber-reinforced bio-composites are being developed and tested to replace industrial automotive glass-fiber sheet molding compounds (GF-SMC) due to their superior properties and environmental friendliness. Furthermore, the shift from zinc-carbon to zinc chloride batteries in the automobile industry is generating significant opportunities for manufacturers in the zinc chloride market. These batteries are particularly attractive due to their cost-effective manufacturing process, making them among the most economical battery options available in the market. The growing adoption of zinc-based coatings for automotive parts protection and the increasing use of zinc compounds in various automotive components continue to drive the market's expansion.

Increasing Demand from the Rubber Tires Industry

The rubber tires industry has emerged as a primary driver for zinc chemicals market growth, particularly due to the essential role of zinc oxide in tire manufacturing processes. According to the International Rubber Study Group (IRSG), the global output of natural rubber reached approximately 6.5 million metric tons during the first six months of 2023, marking a significant increase in production capacity. This growth is further supported by data from the Association of Natural Rubber Producing Countries (ANRPC), which reported a substantial 7.9% increase in worldwide demand for natural rubber to 1.306 million tons in March 2023, indicating robust growth in the tire manufacturing sector. Zinc oxide serves as the preferred activator in the vulcanization or curing process of rubber tire manufacturing and plays a crucial role in enhancing rubber-to-metal adhesion.

The technical advantages of zinc chemicals, particularly zinc oxide, in tire manufacturing continue to drive their increased adoption. Higher loadings of zinc oxide have proven effective in improving hot air/heat aging properties, while maintaining appropriate concentration levels is crucial to prevent scorching problems. The compound's ability to reduce heat buildup and wear in tires makes it an indispensable component in the rubber tire industry. The lack of viable alternative materials for these critical applications further cements the position of zinc chemicals in tire manufacturing. Additionally, the growing popularity of electric vehicles is creating new demands for specialized tires, which in turn is driving the consumption of zinc chemicals in the automotive tire sector. Major tire manufacturers worldwide are expanding their production capacities, particularly in Asia-Pacific countries like China, India, Japan, South Korea, and Thailand, further stimulating the demand for zinc chemicals in tire manufacturing processes.

Segment Analysis: TYPE

Zinc Oxide Segment in Zinc Chemicals Market

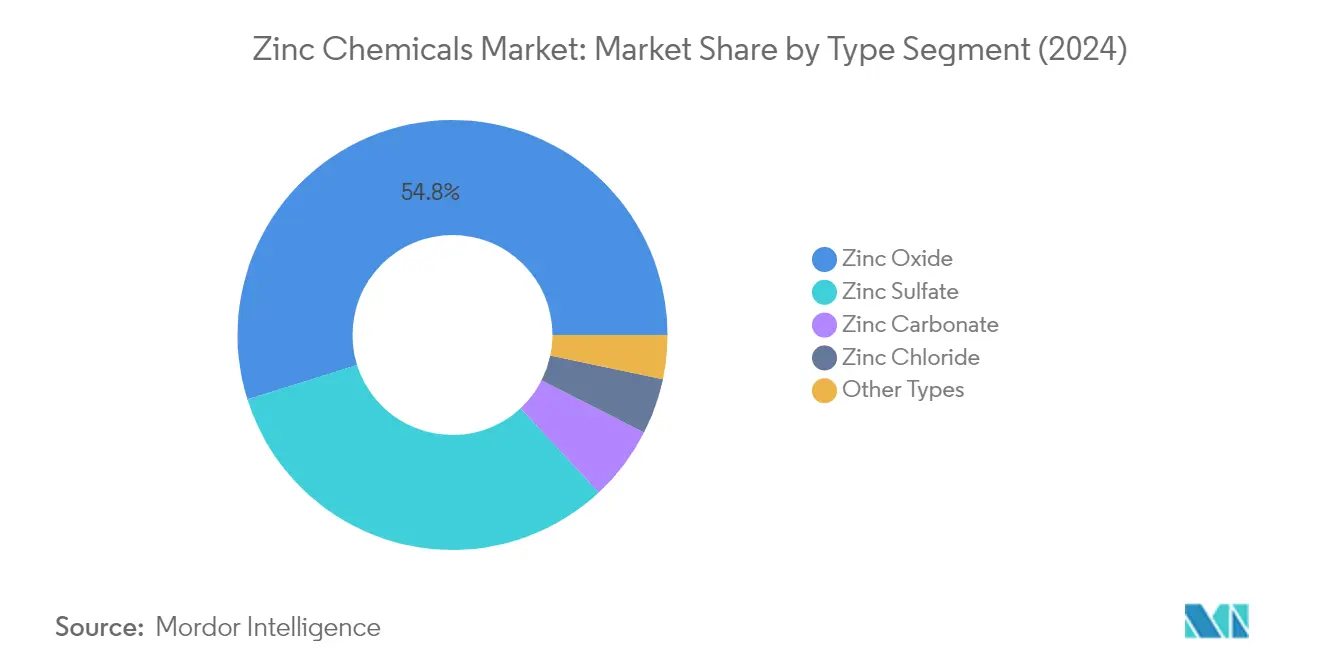

The zinc oxide segment continues to dominate the global zinc chemicals market, holding approximately 55% of the total market share in 2024. This substantial market position is primarily driven by its extensive applications across multiple industries, including rubber processing, paints and coatings, pharmaceuticals, ceramics, and electronics. The segment's prominence is particularly notable in the rubber industry, where it serves as a critical activator in vulcanization processes and helps improve heat dissipation in tire manufacturing. Additionally, zinc oxide's growing utilization in sunscreens and cosmetic products, owing to its UV-absorption properties, along with its increasing application in electronic components and semiconductor manufacturing, further strengthens its market leadership position.

Zinc Sulfate Segment in Zinc Chemicals Market

The zinc sulfate segment is emerging as the fastest-growing segment in the zinc chemicals market, projected to grow at approximately 5% during 2024-2029. This robust growth is primarily attributed to its increasing adoption in agricultural applications as a micronutrient zinc fertilizer to address zinc deficiency in soils and crops. The segment is witnessing strong demand from the agricultural sector, particularly in regions with zinc-deficient soils, as farmers increasingly recognize the importance of zinc supplementation for improved crop yields. Furthermore, the expanding applications of zinc sulfate in animal feed supplements, chemical processing, and the textile industry are contributing to its accelerated growth trajectory.

Remaining Segments in Zinc Chemicals Market

The zinc chemicals market also encompasses zinc carbonate, zinc chloride, and other specialized zinc compounds, each serving distinct industrial applications. Zinc carbonate finds significant applications in the pharmaceutical and cosmetic industries, while zinc chloride is predominantly used in galvanizing fluxes and battery manufacturing. These segments, though smaller in market share, play crucial roles in specific industrial processes and continue to maintain steady demand. The versatility of these zinc compounds in various applications, from water treatment to electronic manufacturing, ensures their continued relevance in the global market landscape.

Segment Analysis: END-USER INDUSTRY

Rubber Processing Segment in Zinc Chemicals Market

The rubber processing segment dominates the global zinc chemicals market, accounting for approximately 32% of the total market volume in 2024. This significant market share is primarily driven by the extensive use of zinc oxide in rubber vulcanization processes, which helps make natural rubber more durable. Zinc chemicals play multiple crucial roles in rubber processing activities, including latex gelation, heat stabilization, light stabilization, and pigmentation. The segment's dominance is further reinforced by the growing demand from tire manufacturing, where zinc oxide is essential for improving durability and performance characteristics. Major tire manufacturers globally continue to maintain steady production levels, contributing to the consistent demand for zinc chemicals in rubber processing applications.

Pharmaceutical Segment in Zinc Chemicals Market

The pharmaceutical segment is projected to exhibit the highest growth rate in the zinc chemicals market during the forecast period 2024-2029, with an expected growth rate of approximately 5%. This accelerated growth is driven by the increasing use of zinc chemicals in treating various health conditions, including lung infections, malaria, asthma, ulcers, and skin infections. The segment's growth is further supported by the rising awareness of zinc deficiency-related health issues and the expanding use of zinc-based pharmaceutical products in dietary supplements. The pharmaceutical industry's continuous research and development activities, particularly in zinc-based medications and supplements, coupled with the growing emphasis on preventive healthcare, are expected to sustain this segment's rapid growth trajectory.

Remaining Segments in End-User Industry

The other significant segments in the zinc chemicals market include agriculture, chemicals and petrochemicals, ceramics, paints and coatings, and other end-user industries. The agriculture segment maintains a strong presence due to the widespread use of zinc-based fertilizers and micronutrients. The chemicals and petrochemicals sector utilizes zinc chemicals in various manufacturing processes and as catalysts. In the ceramics industry, zinc chemicals are essential for improving gloss and preventing crazing of ceramic products. The paints and coatings segment relies on zinc chemicals for their anti-corrosive properties and UV protection capabilities. These diverse applications across multiple industries contribute to the market's overall robustness and stability.

Zinc Chemicals Market Geography Segment Analysis

Zinc Chemicals Market in Asia-Pacific

The Asia-Pacific region represents the largest and most dynamic market for zinc chemicals globally. The region's dominance is driven by robust manufacturing activities across various end-use industries, including rubber processing, agriculture, chemicals, and petrochemicals. Countries like China, India, Japan, and South Korea form the backbone of the regional market, with each contributing significantly through their diverse industrial applications. The presence of major tire manufacturers, a growing agricultural sector, and expanding construction activities continue to fuel the demand for zinc chemicals across these nations.

Zinc Chemicals Market in China

China stands as the powerhouse of the Asia-Pacific zinc chemicals market, commanding approximately 65% of the regional market share. The country's dominance is attributed to its massive industrial base, particularly in sectors like rubber processing, chemicals, and construction. China's robust manufacturing sector, coupled with significant investments in infrastructure development, continues to drive demand. The country's leadership in global tire production and growing emphasis on agricultural productivity further reinforce its position in the zinc chemicals market.

Zinc Chemicals Market in India

India emerges as the fastest-growing market in the Asia-Pacific region, with a projected growth rate of approximately 5% during 2024-2029. The country's growth trajectory is supported by rapid industrialization and increasing investments in manufacturing sectors. India's expanding automotive industry, growing agricultural sector, and government initiatives promoting domestic manufacturing are key factors driving market growth. The country's focus on infrastructure development and rising demand from the pharmaceutical sector further contribute to its accelerated growth in the zinc chemicals market.

Zinc Chemicals Market in North America

The North American zinc chemicals market demonstrates a mature and well-established industrial ecosystem, characterized by advanced manufacturing capabilities and stringent quality standards. The region's market is primarily driven by demand from rubber processing, agriculture, and chemical manufacturing sectors. The United States, Canada, and Mexico each contribute to the regional market dynamics, with varying levels of industrial development and application focus.

Zinc Chemicals Market in United States

The United States dominates the North American market, accounting for approximately 80% of the regional market share. The country's leadership position is supported by its advanced manufacturing infrastructure and diverse industrial base. The presence of major tire manufacturers, a robust agricultural sector, and significant chemical processing capabilities contribute to its market dominance. The country's focus on research and development, coupled with stringent quality standards, maintains its position as a key player in the global zinc chemicals market.

Zinc Chemicals Market in United States (Growth Focus)

The United States also leads the region's growth trajectory with a projected growth rate of approximately 4% during 2024-2029. This growth is driven by increasing demand from various end-use industries, particularly in the rubber processing and agricultural sectors. The country's ongoing investments in infrastructure development and growing emphasis on sustainable agricultural practices continue to create new opportunities. The expanding pharmaceutical and personal care industries further contribute to the market's growth momentum.

Zinc Chemicals Market in Europe

The European zinc chemicals market is characterized by its sophisticated industrial infrastructure and strong focus on technological innovation. The region's market dynamics are shaped by the presence of established manufacturers in Germany, France, the United Kingdom, and Italy. Germany leads the regional market, while France demonstrates the strongest growth potential among European nations. The region's emphasis on sustainable manufacturing practices and stringent environmental regulations continues to influence market development.

Zinc Chemicals Market in Germany

Germany maintains its position as the largest market for zinc chemicals in Europe, supported by its robust automotive and chemical manufacturing sectors. The country's leadership in industrial production, particularly in rubber processing and chemical manufacturing, drives sustained demand. Germany's strong focus on research and development, coupled with its advanced manufacturing capabilities, reinforces its position as a key market in the region.

Zinc Chemicals Market in France

France emerges as the fastest-growing market in Europe, driven by increasing investments in industrial infrastructure and growing demand from end-use industries. The country's expanding chemical manufacturing sector and rising demand from agricultural applications contribute to its growth momentum. France's focus on sustainable development and technological innovation in manufacturing processes supports its accelerated market growth.

Zinc Chemicals Market in South America

The South American zinc chemicals market demonstrates significant potential, with Brazil and Argentina serving as key markets in the region. Brazil emerges as both the largest and fastest-growing market in South America, driven by its extensive industrial base and growing agricultural sector. The region's market development is supported by increasing investments in manufacturing infrastructure and rising demand from various end-use industries, particularly in rubber processing and agricultural applications.

Zinc Chemicals Market in Middle East & Africa

The Middle East & Africa region presents a growing market for zinc chemicals, with Saudi Arabia and South Africa serving as key markets. Saudi Arabia leads the regional market, benefiting from its strong industrial base and ongoing investments in manufacturing infrastructure. The region's market development is driven by increasing industrialization, growing agricultural activities, and rising demand from the construction sector. Saudi Arabia also demonstrates the strongest growth potential in the region, supported by government initiatives to diversify the economy and expand industrial capabilities.

Competitive Landscape

Top Companies in Zinc Chemicals Market

The zinc chemicals market features several established players focusing on continuous innovation and sustainable practices. Companies are investing in research and development to optimize production processes and develop specialized grades of zinc chemicals for various applications, including rubber, pharmaceuticals, and agriculture. Operational excellence is being achieved through the modernization of manufacturing facilities and the adoption of advanced technologies for quality control. Strategic initiatives include strengthening distribution networks across regions and forming partnerships with local distributors to enhance market reach. Geographic expansion is primarily focused on emerging markets in Asia-Pacific, while companies are also investing in capacity additions at existing facilities to meet growing demand. Vertical integration strategies are being employed to secure raw material supply and maintain cost competitiveness in the market.

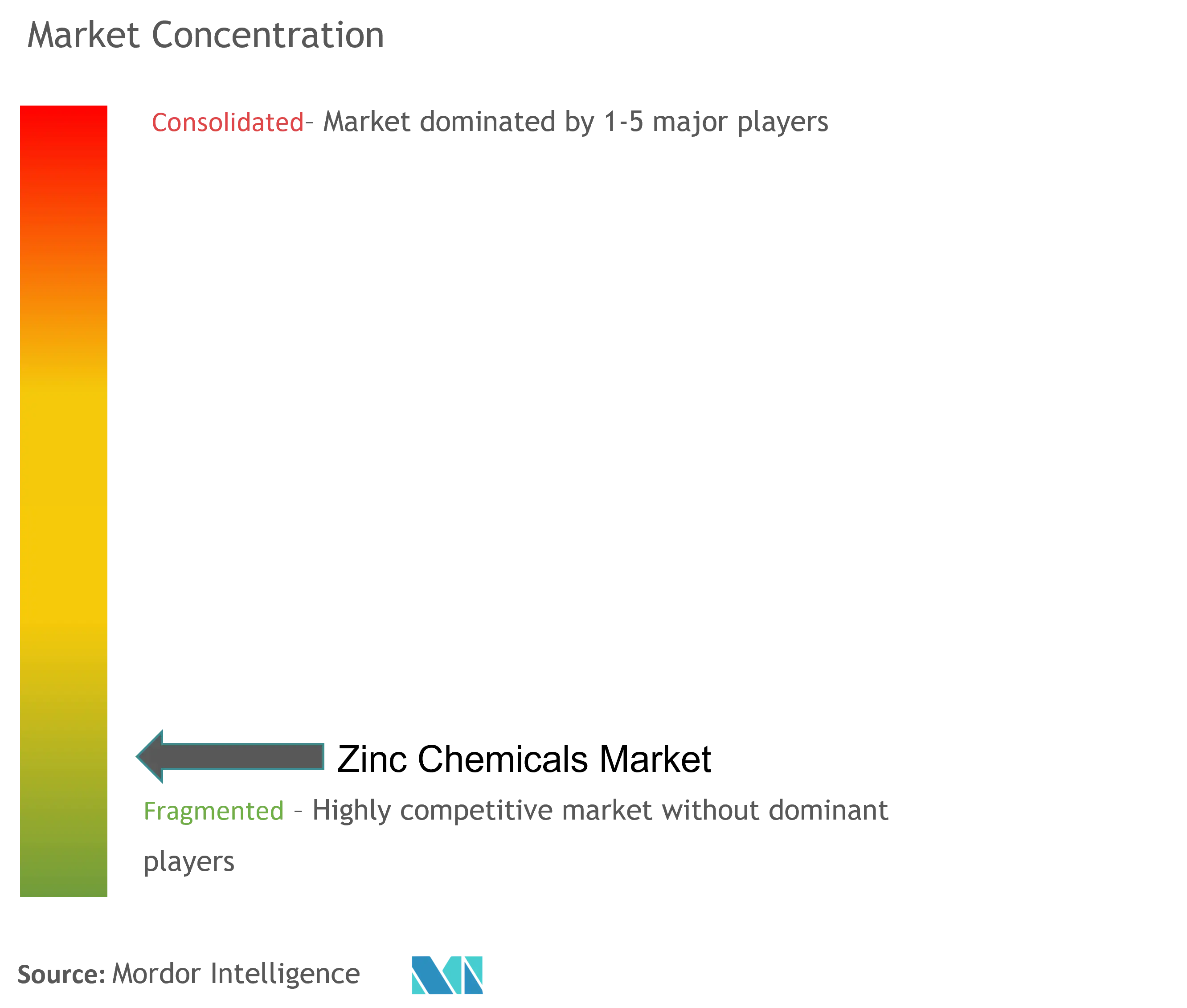

Fragmented Market with Regional Strong Players

The global zinc chemicals market exhibits a partially fragmented structure with a mix of global conglomerates and regional specialists. Leading players like U.S. Zinc, Zochem Inc., EverZinc, and TIB Chemicals AG have established strong positions through their specialized product portfolios and extensive manufacturing capabilities. The market is characterized by the presence of numerous regional and country-level players who compete effectively in their respective geographical territories through local market knowledge and established customer relationships. The competitive dynamics vary significantly across regions, with North America and Europe featuring more consolidated markets compared to the more fragmented Asian market.

Merger and acquisition activities in the market have been strategic in nature, focused on expanding geographical presence and enhancing product portfolios. Companies are increasingly looking at vertical integration opportunities to secure raw material supply and optimize costs. The market has witnessed some notable consolidations, such as Zinc Oxide LLC's acquisition of Zochem Inc., which created a leading position in North America. Regional players are strengthening their market positions through strategic partnerships and joint ventures, particularly in emerging markets where local manufacturing presence is crucial for success.

Innovation and Sustainability Drive Future Success

Success in the zinc chemicals market increasingly depends on developing innovative products and sustainable manufacturing processes. Companies need to focus on developing specialized grades of zinc chemicals that meet evolving customer requirements across different end-use industries. Investment in research and development capabilities is crucial for maintaining a competitive advantage, particularly in high-value applications such as pharmaceuticals and electronics. Building strong relationships with key customers through technical support and customized solutions will be essential for maintaining market share. Environmental compliance and sustainability initiatives are becoming increasingly important factors in maintaining market position.

Market contenders can gain ground by focusing on niche applications and underserved geographical markets. The development of cost-effective manufacturing processes and efficient supply chain management will be crucial for new entrants to compete effectively. Companies need to carefully consider regulatory requirements across different regions and invest in compliance measures. The relatively low threat of substitution for zinc chemicals in many applications provides stability, but companies must continue to innovate to maintain their competitive position. Building strong distribution networks and establishing long-term relationships with key raw material suppliers will be critical for sustainable growth in the market. Additionally, the use of zinc oxide in various applications such as zinc plating chemicals and other zinc compounds is expected to drive further innovation and market expansion.

Zinc Chemicals Industry Leaders

U.S. Zinc

Zochem Inc

EverZinc

TIB Chemicals AG

Weifang Longda Zinc Industry Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- Recent developments in the market studied will be covered in the complete report.

Global Zinc Chemicals Market Report Scope

Zinc is a chemical element and does not rust easily like iron and other metals. Hence, zinc protects iron and other metals from rust. Owing to the versatile and favorable chemical properties of zinc chemical, its application in the automotive, agriculture, and construction industries is rising rapidly.

The zinc chemicals market is segmented by type, end-user industry, and geography. By type, the market is segmented into zinc oxide, zinc sulfate, zinc carbonate, zinc chloride, and other types. By end-user industry, the market is segmented into agriculture, chemicals and petrochemicals, ceramics, pharmaceuticals, paints and coatings, rubber processing, and other end-user industries. The report also covers the size and forecasts for the zinc chemicals market in 27 major countries across various regions. For each segment, the market sizes and forecasts are provided in terms of volume (kilotons).

| Zinc Oxide |

| Zinc Sulfate |

| Zinc Carbonate |

| Zinc Chloride |

| Other Types |

| Agriculture |

| Chemicals and Petrochemicals |

| Ceramic |

| Pharmaceutical |

| Paints and Coatings |

| Rubber Processing |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Turkey | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| Nigeria | |

| Qatar | |

| Egypt | |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| Type | Zinc Oxide | |

| Zinc Sulfate | ||

| Zinc Carbonate | ||

| Zinc Chloride | ||

| Other Types | ||

| End-user Industry | Agriculture | |

| Chemicals and Petrochemicals | ||

| Ceramic | ||

| Pharmaceutical | ||

| Paints and Coatings | ||

| Rubber Processing | ||

| Other End-user Industries | ||

| Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Turkey | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| Nigeria | ||

| Qatar | ||

| Egypt | ||

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the Zinc Chemicals Market?

The Zinc Chemicals Market size is expected to reach 4.55 million tons in 2025 and grow at a CAGR of 4.47% to reach 5.67 million tons by 2030.

What is the current Zinc Chemicals Market size?

In 2025, the Zinc Chemicals Market size is expected to reach 4.55 million tons.

Who are the key players in Zinc Chemicals Market?

U.S. Zinc, Zochem Inc, EverZinc, TIB Chemicals AG and Weifang Longda Zinc Industry Co. Ltd are the major companies operating in the Zinc Chemicals Market.

Which is the fastest growing region in Zinc Chemicals Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Zinc Chemicals Market?

In 2025, the Asia Pacific accounts for the largest market share in Zinc Chemicals Market.

What years does this Zinc Chemicals Market cover, and what was the market size in 2024?

In 2024, the Zinc Chemicals Market size was estimated at 4.35 million tons. The report covers the Zinc Chemicals Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Zinc Chemicals Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: