Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

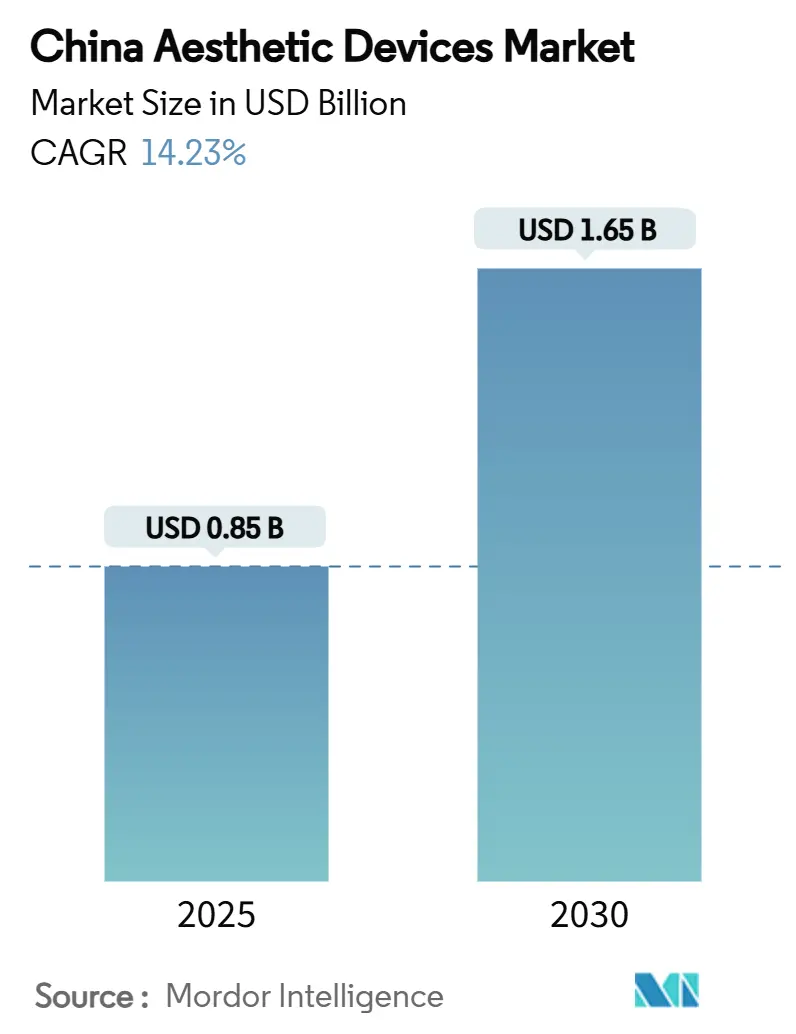

| Market Size (2025) | USD 0.85 Billion |

| Market Size (2030) | USD 1.65 Billion |

| Growth Rate (2025 - 2030) | 14.23% CAGR |

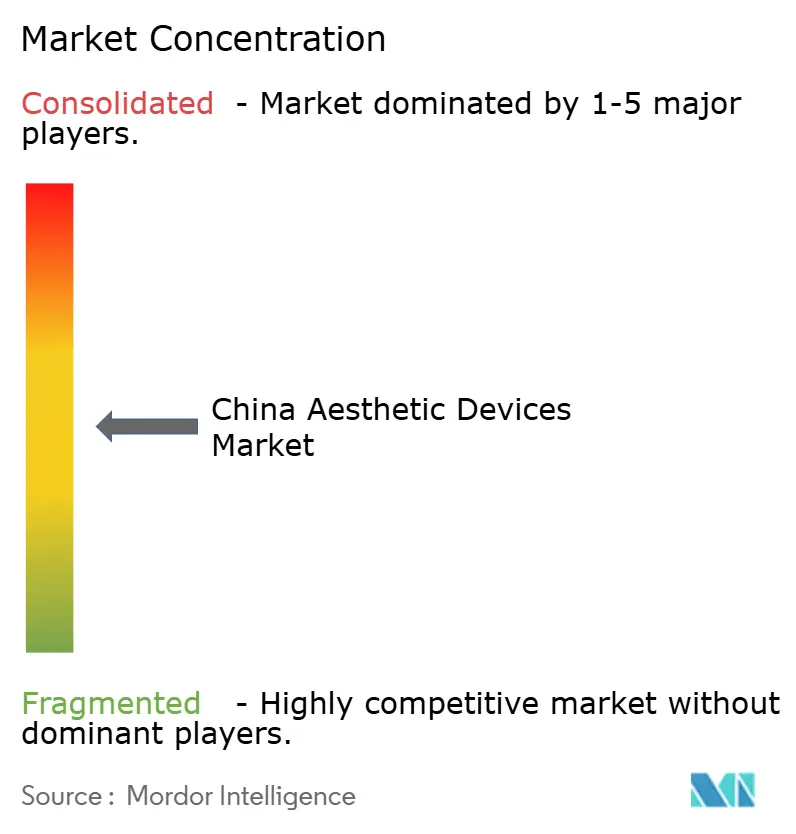

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Aesthetic Devices Market Analysis by Mordor Intelligence

The China Aesthetic Devices Market size is estimated at USD 0.85 billion in 2025, and is expected to reach USD 1.65 billion by 2030, at a CAGR of 14.23% during the forecast period (2025-2030).

Sustained consumer demand, rapid product innovation, and favorable regulatory initiatives underpin this trajectory. Energy-based technologies keep the category dynamic by offering non-invasive solutions that match risk-averse preferences, while social commerce funnels a growing stream of first-time patients into clinics and home-use channels. Rising urban incomes and heightened appearance awareness sustain premium price segments, even as local manufacturers close performance gaps with international brands. Government support for domestic innovation, combined with accelerated approval pathways, ensures a steady pipeline of advanced devices that sharpen competitive intensity.

Key Report Takeaways

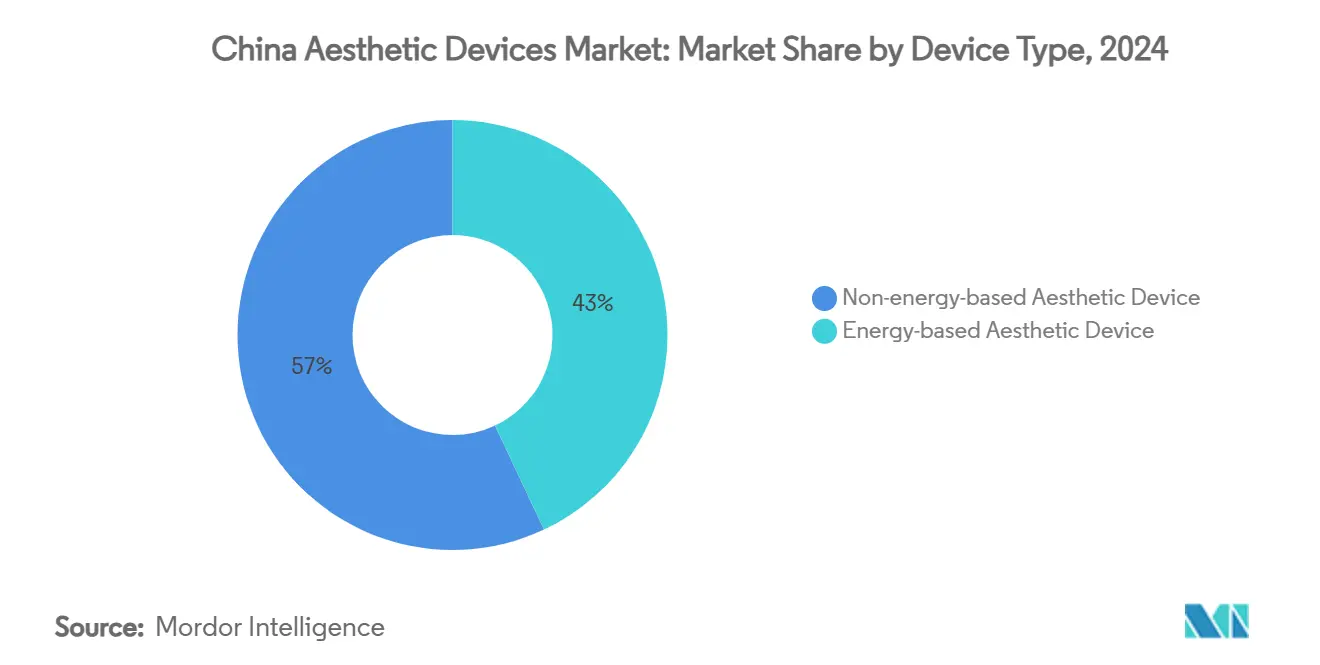

- By device type, energy-based platforms held 43.01% of the China aesthetic devices market share in 2024, and radiofrequency systems are projected to post the fastest 18.45% CAGR through 2030.

- By application, body contouring commanded a 26.91% share of the China aesthetic devices market size in 2024, and skin resurfacing and tightening are advancing at a 16.86% CAGR to 2030.

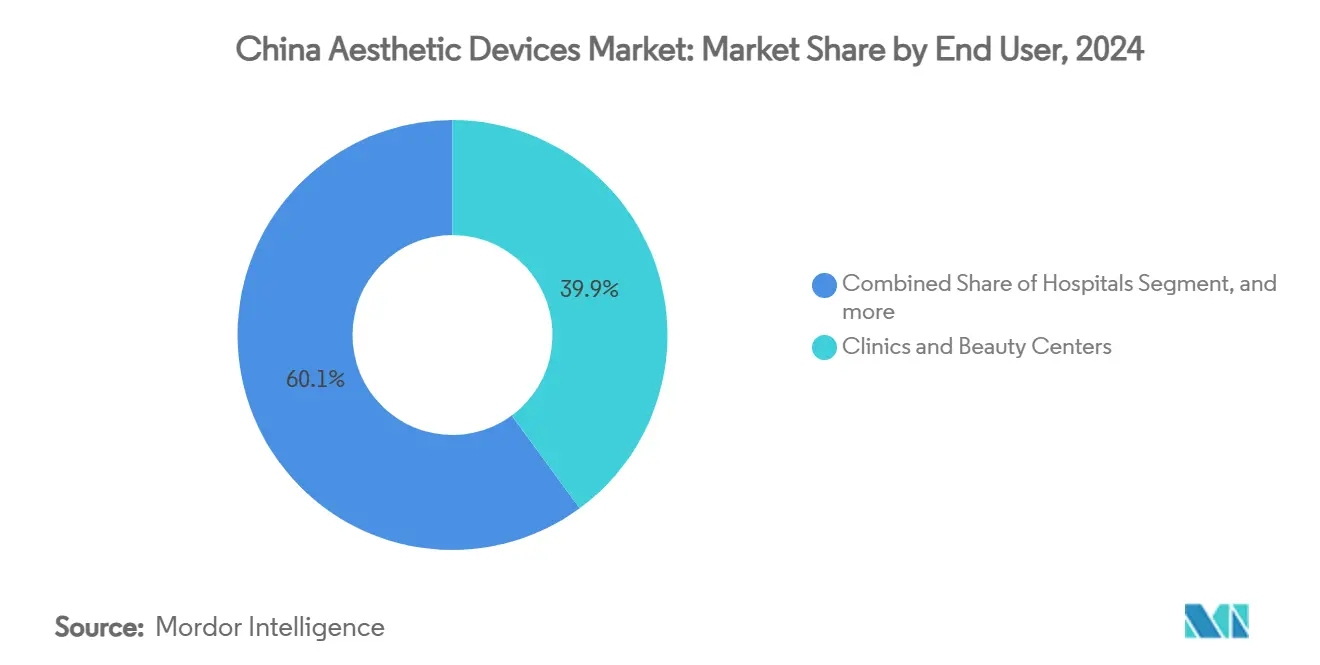

- By end user, clinics and beauty centers retained a 39.92% share of the China aesthetic devices market in 2024, while home settings are expanding at a 19.77% CAGR through 2030.

China Aesthetic Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of obesity and weight-related concerns | +2.8% | National; tier-one cities strongest | Medium term (2-4 years) |

| Growing popularity of minimally invasive cosmetic treatments | +3.2% | Urban centers; spreading to tier-two cities | Short term (≤2 years) |

| Accelerated innovation in energy-based device technologies | +2.1% | National; R&D hubs in Beijing, Shanghai, Shenzhen | Long term (≥4 years) |

| Social commerce and live-streaming driving patient acquisition | +1.9% | National; mobile-first demographics | Short term (≤2 years) |

| Regulatory acceleration via NMPA early-access pathways | +1.7% | Hainan Free-Trade Port, Greater Bay Area | Short term (≤2 years) |

| Aging population fueling demand for age-related interventions | +2.3% | National; 60+ cohort concentration | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Obesity and Weight-Related Concerns

Adult obesity rates have risen each year, with tier-one cities displaying the steepest growth. Non-invasive fat reduction methods such as radiofrequency lipolysis and cryolipolysis offer surgery-free alternatives that resonate with preventive-health positioning. Disposable-income growth intensifies willingness to pay for body sculpting treatments, now framed as health investments rather than luxury indulgences. Pipeline innovations reinforce momentum; for example, Raziel Therapeutics’ RZL-012 injectable is in Phase 3 trials and targets a 2027 mainland launch, blending pharmaceutical and device capabilities.[1]Lihi Segal, “RZL-012 Phase III Expansion,” biopharma-apac.com Government wellness campaigns that emphasize healthy weight further bolster demand for medically supervised contouring.

Growing Popularity of Minimally Invasive Cosmetic Treatments

“Light medical beauty” continues to dominate consumer preferences as 91% of surveyed patients maintained or increased spending in 2024. Gradual enhancement aligns with cultural aesthetics that favor subtle improvements over dramatic change. Platforms such as Little Red Book amplify peer reviews and treatment diaries, accelerating mainstream acceptance. AI-enabled diagnostic tools, including VISIA systems, personalize device protocols and improve outcomes. Streamlined NMPA pathways for minimally invasive tools lower entry barriers for new modalities that reduce downtime and adverse events, driving faster replacement cycles within clinics.

Accelerated Innovation in Energy-Based Device Technologies

Platform consolidation allows clinics to offer multiple therapies using a single console, enhancing throughput and return on investment. Next-generation radiofrequency units integrate real-time tissue impedance monitoring that adjusts energy delivery micro-seconds before thermal damage, improving both safety and patient comfort. Domestic producers now deliver comparable efficacy at 30% lower average selling prices, supporting urban and suburban diffusion. Patent filings in China surpassed 520 cumulative applications for energy-based aesthetics, signaling sustained R&D commitment. Combination therapies such as RF-microneedling or RF-ultrasound widen indications and lengthen treatment programs, solidifying recurring revenue streams.

Social Commerce and Live-Streaming Driving Patient Acquisition

Douyin-hosted live streams enable physicians and KOLs to showcase treatment sessions in real time, compressing the research-to-booking cycle. Brands broadcast results, safety tips, and pricing transparency, nurturing trust before clinic visits. Interactive Q&A features address hesitations on the spot, raising conversion rates. Device makers deploy turnkey content packages that clinics can white-label, further scaling reach. Datasea’s installation of 5G AI acoustic systems across 263 beauty salons demonstrates how edge connectivity enhances immersive patient education experiences.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Concerns over adverse events and patient safety | -1.4% | National; home-use devices most affected | Medium term (2-4 years) |

| Proliferation of counterfeit and unregulated devices | -2.1% | National; higher risk in lower-tier cities | Short term (≤2 years) |

| Margin compression from volume-based procurement policies | -1.6% | National; public-hospital tenders | Short term (≤2 years) |

| Operator skill gaps and inadequate training programs | -1.2% | National; smaller clinics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Concerns Over Adverse Events and Patient Safety

Expanded use across diverse operator skill levels heightens complication risk and media scrutiny. Scientific studies report cases such as subcutaneous fat atrophy after injectables in Asian patients with thinner adipose layers, underscoring the need for population-specific dosing.[2]Young Jin Kim, “Subcutaneous Fat Atrophy in Asian Patients,” Journal of Cosmetic Dermatology, onlinelibrary.wiley.com NMPA has tightened post-market surveillance, obliging manufacturers to submit periodic safety updates and incident analyses. Clinics invest in certified training programs to safeguard reputations. Home-use device makers now integrate skin-type sensors and auto-shutoff features to mitigate misuse, yet liability concerns temper adoption speed.

Proliferation of Counterfeit and Unregulated Devices

Lower-tier cities and online marketplaces continue to see a supply of imitation devices that mimic branding and firmware of licensed products. Counterfeits often undercut genuine units by 60%, luring cost-sensitive buyers but exposing them to safety risks. Sophisticated reverse-engineering capabilities create near-identical housings, complicating enforcement efforts. Government raids and awareness campaigns have increased yet remain reactive because new listings emerge rapidly. Authorized manufacturers now embed blockchain-based serialization to help clinics and consumers verify authenticity via mobile apps before purchase.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Energy-Based Technologies Lift Market Performance

Energy-based equipment led with 43.01% share of China aesthetic devices market in 2024, reflecting its ability to address multiple indications through non-invasive means. Radiofrequency devices are forecast to register an 18.45% CAGR through 2030, aided by AI-guided temperature modulation that ensures consistent dermal heating without epidermal damage. Laser systems remain indispensable for hair removal and tattoo clearance, while ultrasound expands into abdominal lipolysis segments. Cost-effective local brands further democratize access by pricing 25–30% below foreign equivalents without compromising core safety standards. In contrast, non-energy options such as dermal rollers grow at a single-digit pace as consumers gravitate toward solutions promising longer-lasting collagen remodeling. Regulatory classification as Class III medical devices imposes stringent manufacturing controls, raising barriers for newcomers but elevating quality perception across the China aesthetic devices market.

Second-generation RF platforms combine microneedles, ultrasound imaging, and impedance sensing within one chassis, allowing physicians to tailor protocols in minutes. Clinics appreciate reduced capital expenditure associated with multi-modality systems, influencing purchasing cycles every 24–36 months instead of 48 months previously. Domestic champions pursue export licenses for Southeast Asia, leveraging economies of scale realized at home. Meanwhile, importers reposition premium devices as foundational technologies for advanced combination protocols, preserving higher margins in top-tier urban clinics.

By Application: Body Contouring Sets the Pace for Revenue Growth

Body contouring held 26.91% share of China aesthetic devices market size in 2024, driven by rising obesity and a cultural premium on slim silhouettes. Treatment demand aligns closely with sedentary city lifestyles, pushing clinics to acquire cryolipolysis and monopolar RF systems that can debulk localized adiposity in 30-minute sessions. Multi-session package offerings create predictable revenue streams and encourage patient loyalty. Pollution-related skin stress and accelerated photoaging in dense megacities underpin the 16.86% CAGR projected for skin resurfacing and tightening, where fractionated lasers and fractional RF dominate.

Facial contouring gains traction among Gen Z consumers seeking 3D-morphable refinements, often complimented by AI-driven skin analysis that guides parameter selection. Home-use IPL hair removal handsets expand incremental revenue as median disposable incomes rise in tier-two cities. Breast enhancement remains relatively niche, constrained by a preference for understated change and ongoing surveillance of implant safety. Tele-consultation platforms increasingly link dermatologists to rural consumers for follow-ups, extending device usage horizons and broadening practitioner reach within the China aesthetic devices market.

By End User: Home Settings Shift Delivery Models

Clinics and beauty centers led with 39.92% share of China aesthetic devices market size during 2024, yet the fastest growth lies in home settings, forecast at 19.77% CAGR through 2030. Privacy, convenience, and tighter consumer time budgets push users toward compact devices featuring skin-cooling tips and intelligent pulse control that lower burn risk. Product manuals integrate QR codes linking to real-time chat support, addressing safety queries instantly. Hospitals concentrate on complex procedures requiring anesthesia or physician oversight, but many elective patients still migrate to specialist clinics that offer shorter wait times and flexible payment plans.

Regulations stipulate distinct safety standards for home-use devices, prompting manufacturers to introduce multi-level password locks and child-safety modes. Unlike leveraged proprietary sapphire cooling to secure 70% share in domestic hair removal handsets, illustrating the importance of differentiated ergonomics and perceived comfort. Clinics respond by bundling at-home maintenance devices within treatment packages, cultivating omnichannel customer relationships that extend outcomes and protect retention margins. As features converge, the line between professional and consumer segments blurs, reshaping end-user economics visible across the China aesthetic devices market.

Geography Analysis

Tier-one cities Beijing, Shanghai, Guangzhou, and Shenzhen concentrate the bulk of expenditure due to higher incomes, advanced infrastructure, and embedded beauty culture. International firms locate flagship training centers in these hubs to showcase the latest platforms and capture early adopters. NMPA early-access initiatives in Hainan and the Greater Bay Area have approved more than 270 innovative devices, effectively shortening commercialization cycles for category leaders. These zones function as live sandboxes where clinics pilot premium protocols before broader rollout.

Tier-two conurbations such as Chengdu and Hangzhou display double-digit procedure growth as social-commerce exposure narrows the acceptance gap with coastal megacities. Local governments offer subsidies for medical-aesthetic industrial parks, luring component suppliers and escalating regional device clusters that feed national distribution. Lower-tier markets remain sensitive to price and frequently resort to installment payments, which domestic manufacturers address with entry-level units adapted for lower electrical loads prevalent in older commercial real estate.

Northern provinces prioritize skin whitening and anti-aging regimens due to colder climates that accentuate transepidermal water loss. Southern regions emphasize body contouring solutions to address swimwear aesthetics favored in warmer weather. Manufacturing nodes in Guangdong, Jiangsu, and Zhejiang support just-in-time logistics, reducing lead times to less than seven days for most SKUs and bolstering the export share of Chinese-made aesthetics equipment. Emerging medical tourism corridors between Hong Kong and mainland clinics facilitate cross-border procedure packages, integrating duty-free device purchases with post-treatment care.

Rural expansion is catalyzed by 5G broadband reach and mobile health apps that host virtual dermatology consultations. Portable, battery-operated devices designed for intermittent power conditions find traction in county-level hospitals where staff rotate across multi-disciplinary roles. As disposable income disparities gradually narrow, inland consumers gain access to promotions streamed via live-commerce, fueling incremental sales without heavy physical infrastructure. These geographic nuances jointly shape penetration patterns and revenue allocation within the broader China aesthetic devices market.

Competitive Landscape

The market remains moderately fragmented, yet merger and acquisition activity is ramping as firms pursue scale advantages that can satisfy volume-based procurement directives. Domestic manufacturers benefit from Made in China 2025 grants that offset R&D expenses and accelerate NMPA dossier preparation. Foreign brands pivot to premium clinic channels where patient willingness to pay offsets import tariffs and maintains brand equity. Cost-competitive local products now match 97% of key performance benchmarks of top imported platforms, narrowing differentiation to software, service quality, and practitioner training.

Technology integration stands at the heart of competitive strategy. Leading firms embed AI algorithms into handheld applicators, allowing automatic fluence calibration based on live dermoscopic imaging. Cloud-linked dashboards feed anonymized treatment data back to R&D teams, shortening product iteration cycles. Start-ups with direct-to-consumer models leverage viral social-commerce tactics to bypass distributor margins and gain rapid national coverage. In response, incumbents partner with e-commerce marketplaces to host brand flagship stores and offer same-day device fulfillment in major cities.

Home-use categories witness the sharpest rivalry. Ulike’s sapphire-cooled IPL handsets achieved EUR 1.3 billion (USD 1.5 billion) revenue in 2024, prompting competitors to unveil copycat cooling technologies. To protect share, the brand rolled out a tiered warranty scheme and synchronized mobile app that tracks shot counts, reminding users when consumables approach end of life. Clinic-oriented players such as Runhu Medical emphasize integrated service packages that include certification courses, extended maintenance, and upgrade credits, enhancing stickiness among professional users. The confluence of policy backing, consumer sophistication, and platform technology ensures the competitive landscape remains dynamic through the forecast horizon.

China Aesthetic Devices Industry Leaders

Lumenis

Candela Medical

Bausch Health Companies Inc.

AbbVie (Allergan Aesthetics)

Medytox

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Raziel Therapeutics launched Phase 3 clinical trials in China for RZL-012, an injectable fat reduction treatment targeting submental fat, with commercial launch expected by 2027 through partnership with JuveStar Biotech. This development represents a convergence of pharmaceutical and device-based approaches to aesthetic treatments, potentially disrupting traditional body contouring markets.

- January 2025: Advanced Aesthetic Technologies secured NMPA approval for Algeness VL, the first agarose-based dermal filler approved in China, marking a significant regulatory milestone for innovative biomaterial applications in aesthetic medicine. The Class III medical device approval demonstrates NMPA's willingness to embrace novel technologies that offer enhanced biocompatibility and natural results.

- September 2024: GC Aesthetics launched the YOUTHLY brand in China, offering premium breast implants, including the Round Collection, PERLE, and Luna XT, catering to diverse patient needs.

- September 2024: Allergan Aesthetics, an AbbVie company, received approval from the China National Medical Products Administration (NMPA) for Botox Cosmetic to treat masseter muscle prominence (MMP) in adults.

China Aesthetic Devices Market Report Scope

The scope of the Chinese aesthetic devices market includes all kinds of medical devices that are used for various cosmetic procedures. These procedures include plastic surgery, hair removal, excess fat removal, anti-aging, aesthetic implants, skin tightening, etc., that are aimed at beautification, alteration, and enhancement of the body. The Chinese aesthetic devices market is segmented by product (energy-based aesthetic device (laser-based aesthetic device, radiofrequency (RF) based aesthetic device, light-based aesthetic device, ultrasound aesthetic device), non-energy based aesthetic devices (botulinum toxin, dermal fillers and aesthetic threads, microdermabrasion, and implants), and other products), application (skin resurfacing and tightening, body contouring and cellulite reduction, hair removal, facial aesthetic procedures, breast augmentation, and other applications), and end user (hospitals, clinics and beauty centers, and home settings). The report offers the value (in USD million) for the above segments.

By Type of Device

| Energy-based Aesthetic Device | Laser-based Aesthetic Device |

| Radiofrequency-based Aesthetic Device | |

| Light-based Aesthetic Device | |

| Ultrasound Aesthetic Device | |

| Other Energy-based Aesthetic Devices | |

| Non-energy-based Aesthetic Device | Botulinum Toxin |

| Dermal Fillers & Threads | |

| Microdermabrasion | |

| Implants | |

| Other Non-energy-based Aesthetic Devices |

By Application

| Skin Resurfacing & Tightening |

| Body Contouring & Cellulite Reduction |

| Facial Aesthetic Procedures |

| Hair Removal |

| Breast Augmentation |

| Other Applications |

By End User

| Hospitals |

| Clinics & Beauty Centers |

| Home Settings |

| By Type of Device | Energy-based Aesthetic Device | Laser-based Aesthetic Device |

| Radiofrequency-based Aesthetic Device | ||

| Light-based Aesthetic Device | ||

| Ultrasound Aesthetic Device | ||

| Other Energy-based Aesthetic Devices | ||

| Non-energy-based Aesthetic Device | Botulinum Toxin | |

| Dermal Fillers & Threads | ||

| Microdermabrasion | ||

| Implants | ||

| Other Non-energy-based Aesthetic Devices | ||

| By Application | Skin Resurfacing & Tightening | |

| Body Contouring & Cellulite Reduction | ||

| Facial Aesthetic Procedures | ||

| Hair Removal | ||

| Breast Augmentation | ||

| Other Applications | ||

| By End User | Hospitals | |

| Clinics & Beauty Centers | ||

| Home Settings | ||

Key Questions Answered in the Report

Which device category currently dominates the China aesthetic devices market?

Energy-based platforms held 43.01% share in 2024, reflecting broad indication coverage and clinic preference for multi-modality systems.

What growth rate is expected for home-use aesthetic devices in China?

Home settings are forecast to expand at a 19.77% CAGR between 2025 and 2030, outpacing all professional channels.

Which application generates the highest revenue today?

Body contouring and cellulite reduction account for 26.91% of 2024 revenue, driven by rising obesity and non-invasive fat reduction demand.

How is regulation supporting innovation in China?

NMPA early-access programs in Hainan and the Greater Bay Area have cleared over 270 novel devices since 2017, shortening market entry timelines for advanced technologies.

Why are energy-based technologies preferred over injectables for some users?

They deliver lasting collagen remodeling with minimal downtime, meeting cultural preferences for subtle, progressive improvements.

What regional factors shape device adoption across China?

Tier-one cities adopt first due to higher incomes, while tier-two hubs grow rapidly through social-commerce exposure and local manufacturing incentives.

Page last updated on: