Chemiluminescence Immunoassay (CLIA) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 10.93 Billion |

| Market Size (2031) | USD 14.99 Billion |

| Growth Rate (2026 - 2031) | 6.52% CAGR |

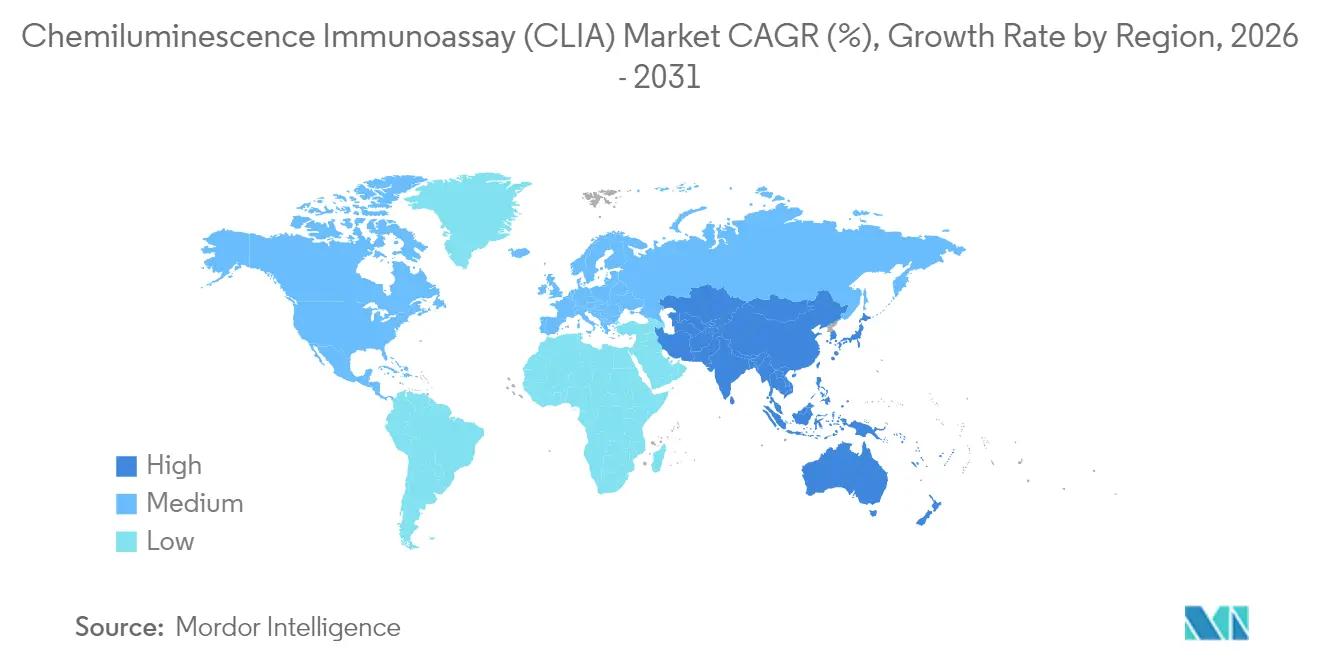

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

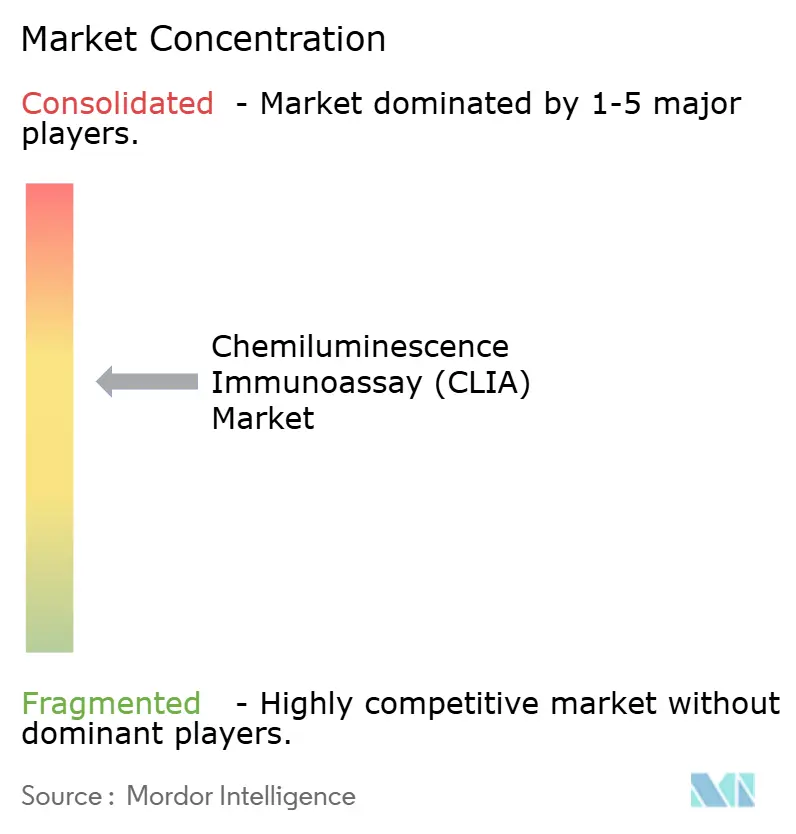

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chemiluminescence Immunoassay (CLIA) Market Analysis by Mordor Intelligence

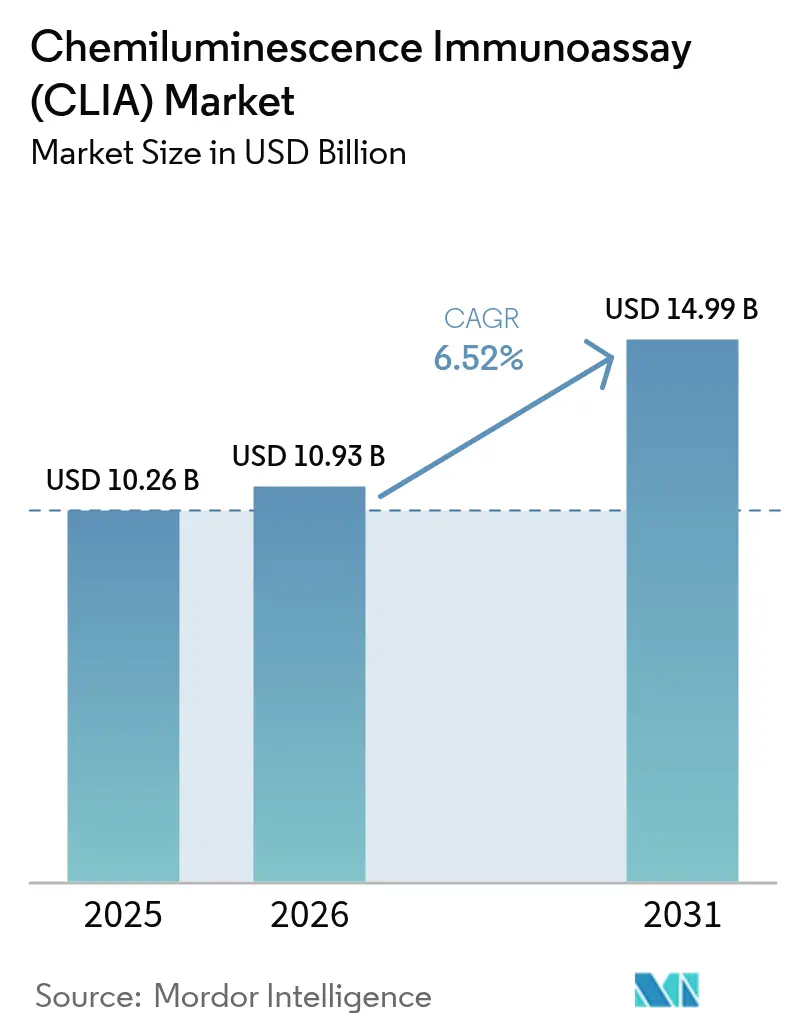

The Chemiluminescence Immunoassay Market size was valued at USD 10.26 billion in 2025 and estimated to grow from USD 10.93 billion in 2026 to reach USD 14.99 billion by 2031, at a CAGR of 6.52% during the forecast period (2026-2031).

This growth reflects rising adoption of precision diagnostics, rapid laboratory automation, and expanding reimbursement for high-sensitivity testing. Asia-Pacific is setting the pace with a 9.80% CAGR, while North America continues to command the largest regional revenue. Vendor strategies now center on multiparametric menu expansion, magnetic-particle innovation, and end-to-end system integration to consolidate testing workflows. Supply-chain concentration for acridinium esters and magnetic particles, together with evolving IVDR and FDA rules, remains the primary operational risk. Simultaneously, the shift toward decentralized testing sites is opening fresh opportunities for compact, high-throughput analyzers tailored to resource-constrained settings.

Key Report Takeaways

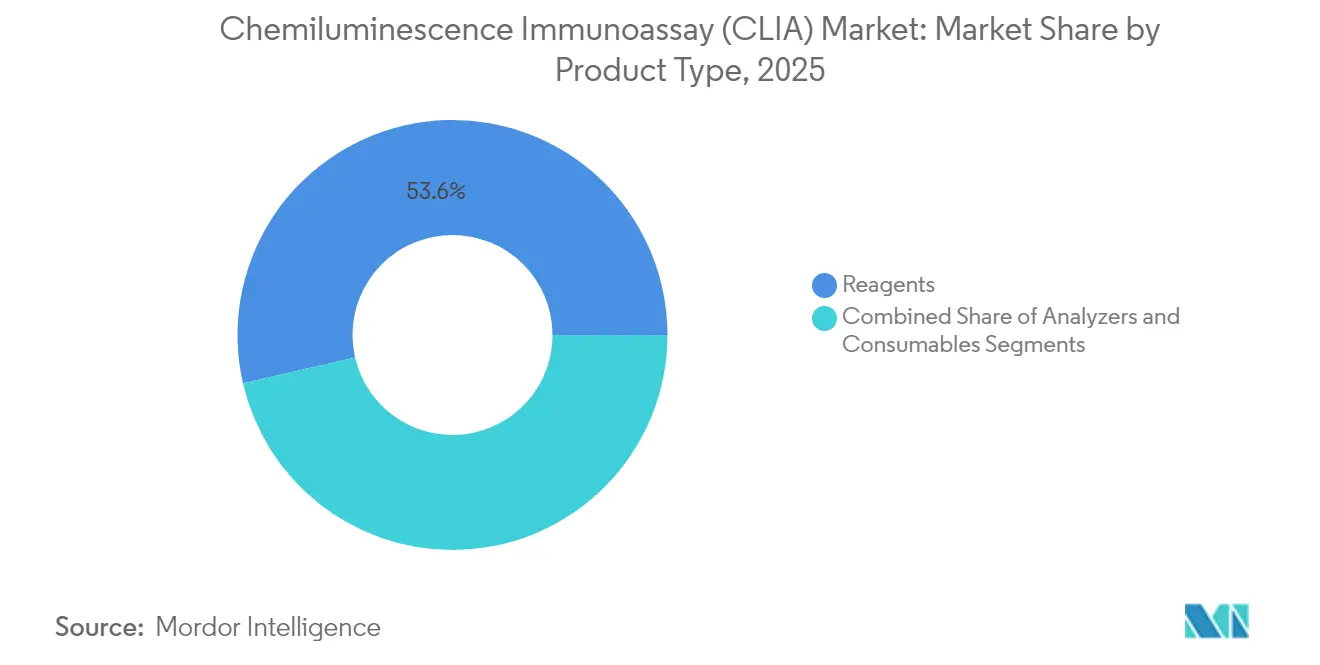

- By product type, reagents led with 53.60% revenue share in 2025; analyzers are advancing at a 6.98% CAGR to 2031.

- By technology, magnetic-particle systems accounted for 45.70% of the chemiluminescence immunoassay market share in 2025, while flash/enhanced CLIA is expanding at an 8.26% CAGR through 2031.

- By application, infectious disease testing held 28.70% share of the chemiluminescence immunoassay market size in 2025 and oncology applications are growing at a 9.04% CAGR between 2026-2031.

- By sample type, blood dominated with an 81.40% share in 2025; saliva sampling is climbing at a 10.32% CAGR through 2031.

- By end user, hospital and clinical laboratories captured 62.30% of revenue in 2025, while reference laboratories record the fastest 8.68% CAGR through 2031.

- By geography, North America retained 35.70% market share in 2025; Asia-Pacific is progressing at a 9.61% CAGR, overtaking Europe by 2028.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Chemiluminescence Immunoassay (CLIA) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of centralized & decentralized diagnostic infrastructure | +1.8% | Asia-Pacific, Middle East & Africa, South America | Medium term (2-4 years) |

| Rising prevalence of chronic & infectious diseases | +1.5% | Global | Long term (≥4 years) |

| Convergence of CLIA analyzers with total-lab automation & LIS | +1.2% | North America, Europe, advanced Asia-Pacific | Medium term (2-4 years) |

| Continuous menu expansion of multiparametric panels | +0.9% | Global | Medium term (2-4 years) |

| Favorable reimbursement & public-health screening programs | +0.8% | North America, Europe, China | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Expanding Diagnostic Infrastructure in Emerging Economies

Rapid investment in hospital modernization, national screening programs, and public–private laboratory networks is driving unprecedented demand for high-throughput CLIA instruments. Large provincial centers in China now install fully automated lines capable of 3,000 tests per hour to serve surrounding county hospitals. India’s tier-2 cities follow similar trajectories, pairing compact analyzers with cloud-based LIS to overcome personnel shortages. Multilateral financing for tuberculosis and hepatitis screening further embeds CLIA capacity in Africa and Latin America. Vendors respond with modular platforms that tolerate unstable power and limited HVAC, safeguarding assay performance across variable climates. Reagent pouch innovations extend shelf life, lowering cold-chain dependence and total cost of ownership.

Rising Prevalence of Chronic & Infectious Diseases

Global incidence of diabetes, cardiovascular disorders, and cancer climbs each year, creating a steady volume of biomarker testing episodes. Simultaneously, recurrent outbreaks of dengue, Zika, and novel respiratory viruses elevate demand for rapid pathogen detection. CLIA platforms deliver attomole-level sensitivity, enabling clinicians to detect disease earlier and tailor interventions more precisely. Single-molecule assays now quantify cardiac troponin within minutes, guiding emergency triage. Oncology labs leverage ultra-low pM detection of PSA, AFP, and pTau217 to monitor therapy response and recurrence risk. These clinical imperatives reinforce recurrent reagent consumption and stimulate continuous menu development.

Technological Convergence with Lab Automation

Total-lab automation architectures link pre-analytical sorting, CLIA modules, and post-analytical archiving without human touchpoints. Barcode and RFID tagging guarantees positive sample identification, eliminating clerical errors. Middleware consolidates quality-control data and transmits verified results to hospital EHRs in near real-time. These dark-lab configurations maintain 24 × 7 operation, boosting throughput and reducing per-test labor cost. Artificial intelligence layers interpret flagging rules, suggest reflex tests, and predict instrument maintenance needs, minimizing downtime. Integration standards such as CLSI AUTO16 now ease connectivity between multi-vendor analyzers and enterprise LIS platforms.

Multiparametric Panel Expansion Driving Lab Consolidation

Assay menus exceeding 200 parameters allow laboratories to consolidate viral panels, hormonal profiles, and tumor markers onto a single CLIA backbone. This breadth supports business models in which regional reference centers process specimens from satellite clinics, capturing economies of scale. Autoimmune panels covering ANA, ENA, and dsDNA cut turnaround times for rheumatologists. Manufacturers invest in novel enzyme-substrate chemistries that preserve analytical sensitivity across multiplex reactions, reducing sample volume requirements. Consolidation accelerates reagent pull-through, entrenching vendor–lab relationships and raising switching costs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lengthy regulatory approval & compliance cycles | −1.4% | Europe, North America | Medium term (2-4 years) |

| Supply-chain concentration for key materials | −0.8% | Global | Short term (≤2 years) |

| Limited cross-platform standardization | −0.4% | Global | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Lengthy Regulatory Approval Cycles

The EU IVDR mandates centralized performance evaluation for every new immunoassay, including extensive post-market surveillance. Many small manufacturers lack resources to compile the required clinical data, delaying European launches by 18–24 months. In the United States, phased LDT oversight compels hospital labs to submit pre-market notifications for in-house assays, redirecting budgets toward FDA-cleared kits. Compliance teams must update quality-management systems, traceability files, and cyber-security documentation to align with tightened requirements[1]Federal Register, “Medical Devices; Laboratory Developed Tests,” federalregister.gov. These layers of review extend time-to-market and may narrow the diversity of available tests.

Supply-Chain Concentration Risks

Fewer than ten firms globally synthesize high-purity acridinium esters and magnetic microbeads at production scale. Any disruption—whether geopolitical tension, natural disaster, or quality lapse—could curtail reagent output for multiple instrument brands simultaneously. Lead times for new GMP-certified capacity exceed 24 months due to specialized reactor needs and regulatory validation. To hedge risk, manufacturers dual-source critical inputs and increase safety inventories, but rising demand still strains supplies. Novel spiro-strained-dioxetane substrates demonstrate superior chemiexcitation but remain dependent on single-site synthesis expertise[2]Omri Shelef et al., “Biocompatible Flash Chemiluminescent Assay,” chemrxiv.org.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Reagents Maintain Revenue Leadership While Analyzers Accelerate

Reagents generated 53.60% of 2025 revenue, benefiting from repeat purchase cycles that underpin the chemiluminescence immunoassay market. Proprietary luminophore formulations command premium pricing and foster razor-and-blade economics. The chemiluminescence immunoassay market size tied to reagents is projected to grow at 6.11% CAGR as menu breadth expands across autoimmune and oncology parameters. Manufacturers enhance stability with enzyme-protected pouches, supporting distribution in high-temperature geographies.

Analyzers, though smaller in current value, advance at 6.98% CAGR on the back of laboratory modernization and network consolidation. Compact benchtop systems target physician-office labs, while high-throughput floor models process up to 3,600 tests per hour for reference centers. Forward-compatible modular designs allow capacity upgrades without footprint expansion. Consumables—calibrators, controls, and microfluidic plates—round out the ecosystem, ensuring traceable results and regulatory compliance.

By Technology Platform: Magnetic-Particle Systems Dominate Adoption

Magnetic-particle architectures captured 45.70% chemiluminescence immunoassay market share in 2025, owing to rapid separation kinetics and low background signal. The chemiluminescence immunoassay market size for magnetic-particle systems is forecast to reach USD 6.73 billion by 2031 at 6.18% CAGR. Sea-urchin-like microbeads increase effective surface area, amplifying enzyme binding and assay sensitivity.

Flash/enhanced CLIA records the fastest 8.26% growth, propelled by sterically hindered dioxetane substrates that generate intense, short-lived photon bursts. This technology slashes incubation times to under five minutes, enabling higher daily throughput. Microplate CLIA retains traction where legacy equipment dominates, whereas CMIA addresses specialized niches requiring femtomolar detection limits such as cardiac troponin in emergency departments.

By Application: Infectious Disease Testing Commands Volume, Oncology Leads Growth

Infectious disease assays comprised 28.70% of 2025 revenue as healthcare systems embed routine viral-load monitoring and antimicrobial stewardship protocols. Multiplex respiratory panels integrate influenza, RSV, and SARS-CoV-2 targets into a single run, optimizing clinician turnaround.

Oncology applications show the highest 9.04% CAGR, reflecting expanded tumor marker usage in screening and treatment monitoring. The chemiluminescence immunoassay market size for oncology is projected to add USD 1.24 billion by 2031. High-sensitivity pTau217 blood tests aid early Alzheimer’s disease differentiation, illustrating CLIA’s reach beyond traditional oncology into neuro-degenerative diagnostics. Autoimmune, cardiovascular, and endocrine disorder testing collectively sustain steady growth through chronic-disease prevalence.

By Sample Type: Blood Remains Dominant as Saliva Gains Acceptance

Blood represented 81.40% of tests in 2025, supported by established phlebotomy infrastructure and rigorous validation datasets. SpinChip’s microfluidic architecture now delivers quantitative results from whole blood within 10 minutes, illustrating efficiency gains.

Saliva assays climb at 10.32% CAGR as non-invasive sampling suits pediatric, geriatric, and home-collection scenarios. Improved pre-analytical buffers mitigate protease degradation, elevating signal consistency. Urine and cerebrospinal fluid maintain niche relevance for hormone and infectious disease panels, with emerging micro-volume cartridges lowering minimum specimen requirements.

By End User: Hospital Laboratories Anchor Demand, Reference Labs Scale Fastest

Hospital and clinical laboratories held 62.30% of 2025 revenue, leveraging integrated automation lines to meet acute-care turnaround targets. Continuous operation models reduce per-test labor cost and enhance equipment utilization.

Reference laboratories post an 8.68% CAGR as healthcare providers outsource complex panels to centralized hubs. High-volume analyzers coupled with AI-driven quality dashboards underpin this expansion. Pharmaceutical firms rely on CLIA for pharmacokinetic profiling in clinical trials, while academic centers deploy open-channel systems for biomarker discovery, underscoring the technology’s versatility across research and service environments.

Geography Analysis

North America generated 35.70% of global revenue in 2025, supported by extensive reimbursement, robust laboratory consolidation, and strong R&D pipelines. U.S. laboratories rapidly adopt companion-diagnostic assays cleared under the FDA’s latest precision-oncology framework, reinforcing menu growth. Canada and Mexico increase spending on chronic-disease programs, further enlarging the chemiluminescence immunoassay market.

Asia-Pacific advances at a 9.61% CAGR, propelled by large-scale public investment in diagnostic infrastructure. China’s tier-one hospitals adopt automated CLIA lines that interface with regional reference labs, while domestic vendors accelerate export ambitions. Japan’s aging demographic sustains high test volumes for cardiac and endocrine markers, and India’s expanding private-hospital networks drive purchasing of mid-throughput analyzers.

Europe maintains solid demand amid IVDR transition. Germany, France, and the United Kingdom standardize oncology and infectious disease screening pathways, anchoring reagent consumption. However, extended conformity assessments temporarily delay new assay launches. Eastern European nations employ EU cohesion funds to upgrade laboratory automation, closing the capacity gap with Western peers. Middle East & Africa and South America exhibit double-digit volume growth from a lower base as governments strengthen disease-surveillance programs and private diagnostics chains expand.

Competitive Landscape

The top suppliers—Roche, Siemens Healthineers, Danaher, and DiaSorin—collectively control significant revenue, signaling moderate concentration. Barriers include high R&D outlays, global service networks, and demanding regulatory pathways. New entrants from China, notably Mindray and SNIBE, penetrate price-sensitive segments by bundling analyzers and starter reagent kits at discounted rates.

Strategic acquisitions focus on niche technologies that extend menu breadth or enable decentralized testing. bioMérieux’s acquisition of SpinChip adds a cartridge-based platform capable of delivering quantitative results from finger-prick blood, enhancing point-of-care reach. Vendors also invest in advanced materials, adopting sea-urchin microbeads and spiro-strained substrates to push sensitivity boundaries.

Product roadmaps increasingly incorporate AI modules for reflex testing suggestions and predictive maintenance. Cloud connectivity facilitates remote calibration updates and real-time performance monitoring, supporting managed-service contracts that lower up-front capital barriers for laboratories. Intellectual-property portfolios around substrate chemistry and magnetic bead design conti nue to differentiate premium platforms from value-tier offerings.

Chemiluminescence Immunoassay (CLIA) Industry Leaders

DiaSorin S.p.A.

Siemens Healthineers AG

Shenzhen Mindray Bio-Medical Electronics Co., Ltd.

Danaher Corporation (Beckman Coulter Inc.)

F. Hoffmann-La Roche AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: bioMérieux acquired SpinChip Diagnostics ASA for EUR 138 million to strengthen its presence in rapid point-of-care immunoassay testing.

- August 2024: Researchers reported a flash chemiluminescent assay using sterically hindered spiro-strained-1,2-dioxetane that boosts chemiexcitation 128-fold while preserving stability.

Global Chemiluminescence Immunoassay (CLIA) Market Report Scope

As per the scope of the report, chemiluminescence (CL) is described as the discharge of electromagnetic radiation owing to the production of light by a chemical reaction. Chemiluminescence immunoassay (CLIA) is an assay incorporating the technique of chemiluminescence with immunochemical reactions. The chemiluminescence immunoassay (CLIA) market is segmented by Product Type (Analyzers, Reagents, and Consumables), Application (Oncology, Autoimmune Disorder, Infectious Disease, Cardiovascular Disease, Endocrine Disorders and Others), End-User (Pharmaceutical and Biotechnology Companies, Hospital and Clinical Laboratories and Others), and Geography (North America, Europe, Asia Pacific, Middle East, and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Analyzers | Automated |

| Semi-Automated | |

| Reagents | Luminophore-Based |

| Enzyme-Enhanced | |

| Consumables |

| Microplate CLIA |

| Magnetic-Particle CLIA |

| Flash/Enhanced CLIA |

| Chemifluorescent Microparticle Immunoassay (CMIA) |

| Oncology |

| Autoimmune Disorders |

| Infectious Diseases |

| Cardiovascular Diseases |

| Endocrine Disorders |

| Others |

| Blood |

| Urine |

| Saliva |

| Other Body Fluids |

| Hospital & Clinical Laboratories |

| Pharmaceutical & Biotechnology Companies |

| Reference & Central Labs |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Analyzers | Automated |

| Semi-Automated | ||

| Reagents | Luminophore-Based | |

| Enzyme-Enhanced | ||

| Consumables | ||

| By Technology Platform | Microplate CLIA | |

| Magnetic-Particle CLIA | ||

| Flash/Enhanced CLIA | ||

| Chemifluorescent Microparticle Immunoassay (CMIA) | ||

| By Application | Oncology | |

| Autoimmune Disorders | ||

| Infectious Diseases | ||

| Cardiovascular Diseases | ||

| Endocrine Disorders | ||

| Others | ||

| By Sample Type | Blood | |

| Urine | ||

| Saliva | ||

| Other Body Fluids | ||

| By End User | Hospital & Clinical Laboratories | |

| Pharmaceutical & Biotechnology Companies | ||

| Reference & Central Labs | ||

| Academic & Research Institutes | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the chemiluminescence immunoassay market?

The market is valued at USD 10.93 billion in 2026 and is forecast to reach USD 14.99 billion by 2031.

Which segment generates the highest revenue?

Reagents generate 53.60% of 2025 revenue because of their recurring consumption pattern.

Which technology platform is growing the fastest?

Flash/enhanced CLIA is expanding at an 8.26% CAGR due to superior signal-to-noise ratios and rapid reaction kinetics.

Why is Asia-Pacific considered a high-growth region?

Robust healthcare investment, expanding laboratory infrastructure, and rising disease-screening programs are driving a 9.61% CAGR in Asia-Pacific.

How are regulatory changes affecting market growth?

The EU IVDR and FDA LDT rule lengthen approval timelines, raising compliance costs and slowing new assay launches.

What competitive strategies are market leaders pursuing?

Leaders focus on menu expansion, AI-enabled automation, and acquisitions that add rapid or decentralized testing capabilities.

Page last updated on: