Chemiluminescence Immunoassay Analyzer Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.35 Billion |

| Market Size (2031) | USD 4.64 Billion |

| Growth Rate (2026 - 2031) | 6.73% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

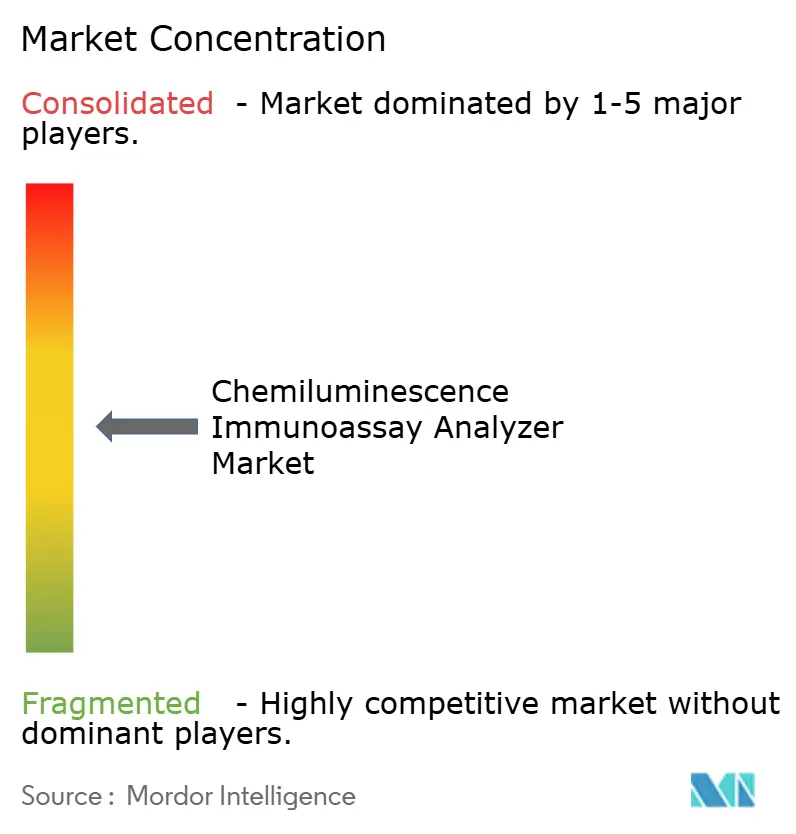

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chemiluminescence Immunoassay Analyzer Market Analysis by Mordor Intelligence

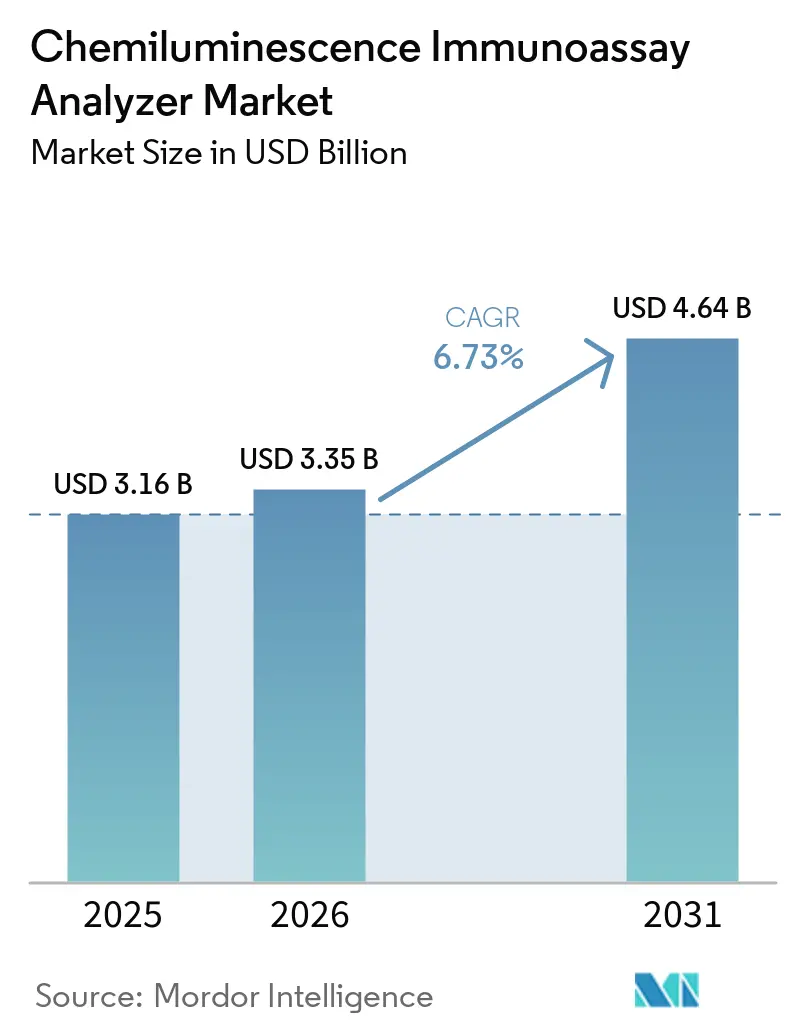

The Chemiluminescence Immunoassay Analyzer Market size is projected to expand from USD 3.16 billion in 2025 and USD 3.35 billion in 2026 to USD 4.64 billion by 2031, registering a CAGR of 6.73% between 2026 to 2031.

The chemiluminescence immunoassay analyzer market is being supported by steady demand for quantitative and high-sensitivity biomarker testing across hospital core laboratories, reference laboratories, and specialty care settings. Demand is also moving toward systems that combine higher throughput with lower operator involvement, which keeps replacement activity active even in mature laboratory networks. Multiplex assay development, decentralized testing expansion, and broader assay menu depth are widening the range of routine clinical use cases that can be handled on the same installed platform base. The competitive field remains led by large global diagnostics groups, but the chemiluminescence immunoassay analyzer market is also seeing stronger pressure from Chinese manufacturers that are improving throughput, menu breadth, and price positioning across mid-tier and emerging-country accounts. Supply constraints in optical and microfluidic components and shortages of skilled laboratory staff still limit near-term adoption at some sites, yet those same pressures are making highly automated systems more attractive to buyers.

Key Report Takeaways

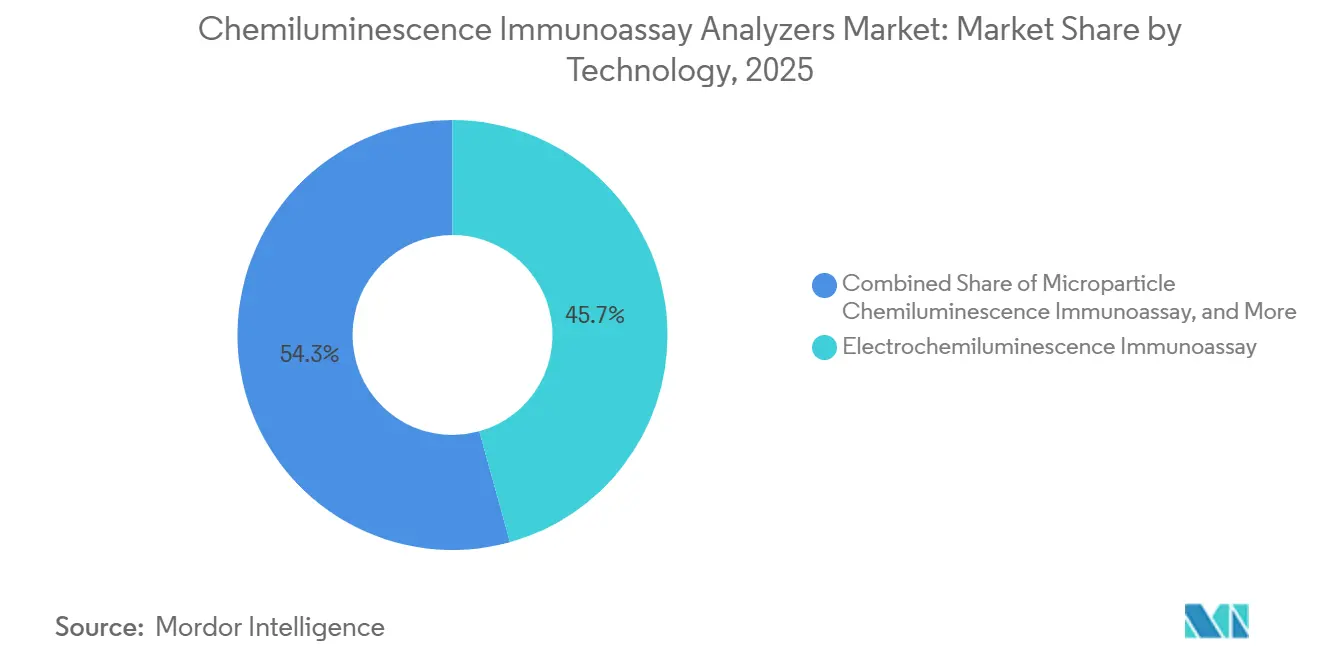

- By technology, electrochemiluminescence immunoassay led with 45.73% revenue share in 2025, while microparticle chemiluminescence immunoassay is forecast to expand at an 8.32% CAGR through 2031.

- By throughput, mid-throughput analyzers accounted for 47.23% share in 2025, while high-throughput analyzers are advancing at a 9.03% CAGR through 2031.

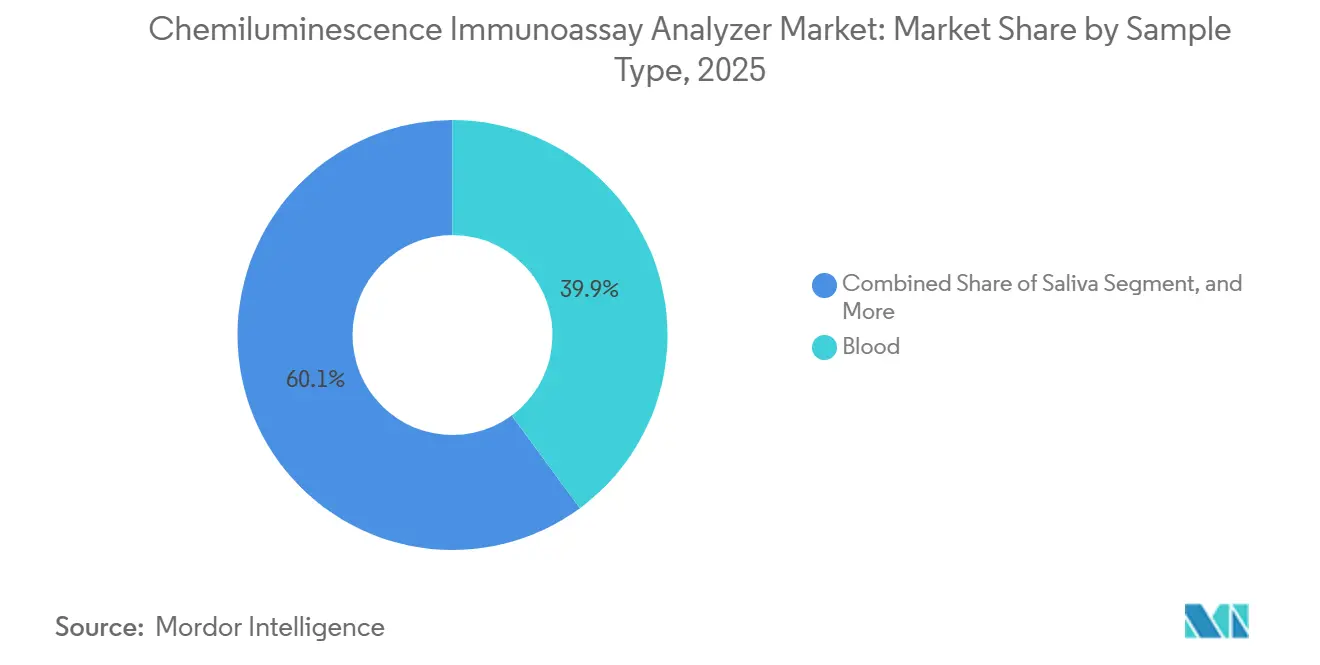

- By sample type, blood represented 39.88% share in 2025, while saliva is forecast to grow at a 7.04% CAGR through 2031.

- By application, therapeutic drug monitoring and toxicology captured 31.23% share in 2025, while oncology is projected to expand at a 7.94% CAGR through 2031.

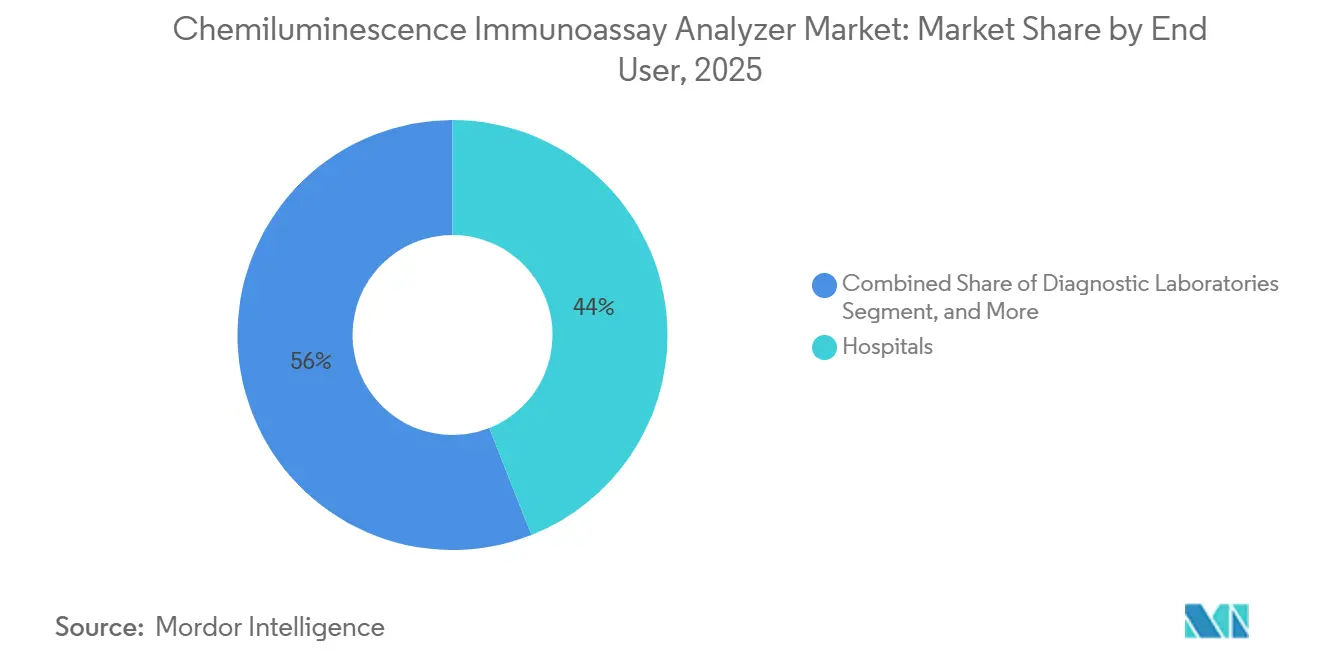

- By end user, hospitals held 44.01% share of the chemiluminescence immunoassay analyzer market size in 2025 and are also the fastest-growing buyer group at an 8.19% CAGR through 2031.

- By connectivity, LIS and HL7 integration accounted for 36.41% share in 2025, while remote monitoring and IoT connectivity are forecast to grow at a 6.87% CAGR through 2031.

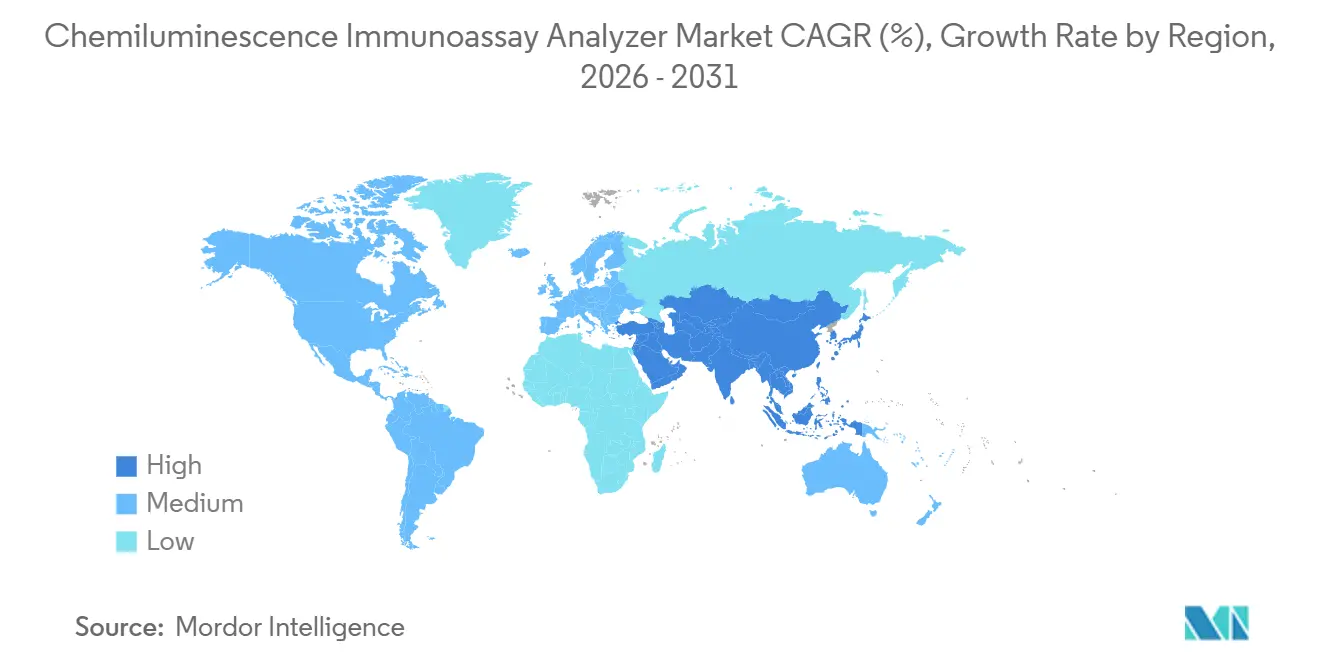

- By geography, North America held 41.71% of the chemiluminescence immunoassay analyzer market share in 2025, while Asia-Pacific is projected to expand at an 8.85% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Chemiluminescence Immunoassay Analyzer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for High-Sensitivity Biomarker Detection | +1.8% | Global, with strong relevance in North America and Europe | Medium term (2-4 years) |

| Shift Toward Fully Automated High-Throughput Workflows | +1.5% | Global, with faster acceleration in Asia-Pacific | Medium term (2-4 years) |

| Expansion of Decentralized and Stat Testing Networks | +1.2% | Middle East and Africa, South America, Asia-Pacific emerging markets | Medium term (2-4 years) |

| Growth in Multiplex Assay Adoption | +1.0% | North America, Europe, China | Medium term (2-4 years) |

| Connectivity Demand for LIS, Middleware, and Traceability | +0.8% | North America, Europe | Short term (≤ 2 years) |

| Reagent Stability and Low Sample Volume Supporting Efficiency | +0.7% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for High-Sensitivity Biomarker Detection

The chemiluminescence immunoassay analyzer market is benefiting from the need to detect biomarkers at very low concentrations in oncology, cardiology, endocrinology, and specialty disease monitoring. Clinical use is moving toward assays that support early detection, repeated monitoring, and tighter treatment decisions, which raises the value of platforms with stronger analytical sensitivity. A 2026 review in Sensors & Diagnostics reported 8-plex electrochemiluminescence systems with detection limits from 15 fg/mL to 230 fg/mL, along with full clinical sensitivity and specificity for acute myocardial infarction biomarker panels across 260 samples.[1]Yu Liu, Chunyan Liu, Zhihui Dai, and Weiliang Guo, “Recent Advances in Multiplexed Electrochemiluminescence Immunoassays,” Sensors & Diagnostics, pubs.rsc.org As high-sensitivity cardiac protocols move beyond large hospitals into urgent care and faster-response settings, laboratories need analyzers that can meet those analytical thresholds without losing workflow consistency. Vendors that improve luminophore chemistry and reduce background signal are likely to hold stronger positions in future assay development partnerships and premium testing menus.

Shift Toward Fully Automated High-Throughput Laboratory Workflows

The chemiluminescence immunoassay analyzer market is also being driven by hospital network consolidation and the need to keep instruments running with fewer staff interventions. Large laboratories now prefer walkaway systems that can handle continuous loading, routine maintenance, and integrated chemistry and immunoassay work with limited operator time. Siemens states that its Atellica CI analyzer reduces manual workflow steps by 75% and requires fewer than 5 minutes of daily hands-on maintenance, which directly supports this purchasing shift.[2]Siemens Healthineers, “Atellica CI Analyzer,” Siemens Healthineers, siemens-healthineers.com Roche also expanded high-capacity integrated testing with the cobas c 703, which delivers up to 2,000 tests per hour on the cobas pro solution and was cleared in 2026.[3]Roche Diagnostics, “Roche Receives FDA 510(k) Clearance for cobas c 703 and cobas ISE neo, Next-Generation Analytical Units Enhancing Efficiency and Capability for Laboratories,” Roche Diagnostics, diagnostics.roche.com This pattern is pushing some mid-sized laboratories to buy smaller versions of high-volume architectures, which is helping high-throughput systems grow faster than the broader installed base.

Expansion of Decentralized and Stat Testing Networks

The chemiluminescence immunoassay analyzers market is gaining support from satellite laboratories, urgent care centers, outpatient networks, and other settings that need fast turnaround without relying fully on central laboratories. Demand in these settings is centered on compact systems that keep analytical performance close to core-lab standards while using small sample volumes and short run times. A 2025 Lab on a Chip study validated a spatially resolved electrochemiluminescence platform for cardiac and traumatic brain injury biomarkers from small-volume samples with performance that was comparable to central laboratory instruments. bioMérieux’s January 2025 acquisition of SpinChip Diagnostics also showed that large diagnostics companies view near-patient immunoassay as a meaningful growth path rather than a side offering. These decentralized systems are not replacing central laboratory analyzers, because they often create more confirmatory, monitoring, and follow-up test volume for the main installed base.

Growth in Multiplex Assay Adoption for Consolidated Testing

The chemiluminescence immunoassay analyzer market is also being lifted by multiplex testing, which allows several analytes to be measured from the same specimen and reduces total work per clinical case. This matters in oncology, infectious disease, cardiac testing, and donor screening, where physicians increasingly prefer broader clinical information from one collection event. The 2026 Sensors & Diagnostics review showed that spectrum-resolved systems could detect AFP, CEA, and cTnI in one run, while bead-based arrays achieved full clinical sensitivity and specificity for 4-target acute myocardial infarction panels. Roche’s cobas MPX-E assay also consolidated HIV 1/2, HCV, HBV, and HEV detection into one donor screening workflow, showing how multiplex logic is moving into routine use at commercial scale. As multiplex output becomes more common, laboratories also need stronger middleware, routing rules, and traceability features, which links assay consolidation to digital workflow upgrades.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Total Cost of Ownership for Small and Mid-Sized Laboratories | -0.9% | South America, Middle East and Africa, South Asia | Medium term (2-4 years) |

| Skilled Operator Shortages for Maintenance and Calibration | -0.7% | North America, Europe | Medium term (2-4 years) |

| Regulatory Fragmentation Across Multi-Country Procurement Markets | -0.5% | Asia-Pacific, Middle East and Africa, South America | Long term (≥ 4 years) |

| Component Sourcing Vulnerability for Optical, Microfluidic, and Semiconductor Inputs | -0.4% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Total Cost of Ownership for Small and Mid-Sized Laboratories

The chemiluminescence immunoassay analyzer market still faces a clear barrier in the form of high ownership costs for smaller laboratories and rural providers. The cost is not limited to the instrument, because buyers also carry reagent commitments, calibration materials, service contracts, staff training, and maintenance expenses over the full platform life. Proprietary reagent tie-ins limit the room for smaller facilities to lower running costs even after the instrument has been installed and partly amortized. This pressure is strongest in settings where reagent rental models and financing options are limited, which slows replacement cycles and delays first-time adoption. The result is that many smaller facilities remain on lower-capacity or older systems even when fully automated analyzers would reduce cost per test over a longer operating period.

Skilled Operator Shortages for Maintenance and Calibration

The chemiluminescence immunoassay analyzer market is also constrained by shortages of clinical laboratory staff who can maintain complex optical and calibration systems over long operating cycles. The shortage is most visible in North America and Western Europe, where financially strong institutions can buy advanced analyzers but still struggle to secure trained technical staff. This gap affects maintenance quality, calibration consistency, and uptime planning, especially on semi-automated or mixed-workflow systems that need closer operator oversight. Siemens highlights the value of low-touch maintenance on its Atellica CI analyzer, which shows why labor constraints are pushing buyers toward more autonomous platforms. The effect is not a broad slowdown across all products, because labor scarcity is actually strengthening the case for fully automated analyzers while making the middle tier less attractive.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: ECL Leads While Microparticle Platforms Accelerate

Electrochemiluminescence immunoassay held 45.73% of the chemiluminescence immunoassay analyzer market share in 2025, which kept it as the leading technology across high-sensitivity hospital and reference laboratory testing. Its strong position reflects years of installed base expansion on Roche and Siemens platforms that support broad assay menus in oncology, endocrinology, infectious disease, and general immunodiagnostics. The technology remains attractive because it combines strong sensitivity, broad menu compatibility, and stable routine performance in high-volume environments. That mix keeps reagent attachment rates high and makes customers less willing to shift to a different platform family after initial installation.

The chemiluminescence immunoassay analyzer market is still seeing technology growth beyond the leading ECL segment, especially in microparticle chemiluminescence formats. Microparticle chemiluminescence immunoassay is projected to grow at an 8.32% CAGR through 2031, which shows that buyers continue to value flexible assay expansion and strong routine testing economics. Abbott’s Alinity i platform has helped support this direction through continued assay menu expansion in cardiac and infectious disease testing, which reinforces the commercial depth of microparticle-based workflows in routine labs. Chemiluminescence enzyme immunoassay also remains commercially relevant where ambient reagent handling and simpler logistics matter more than the highest possible sensitivity. Within the chemiluminescence immunoassay analyzers industry, the practical divide is less about one format fully replacing another and more about matching chemistry design to menu breadth, laboratory scale, and operating model.

By Throughput: Mid-Capacity Is The Installed Backbone, High-Throughput Is The Growth Engine

Mid-throughput analyzers represented 47.23% of the chemiluminescence immunoassay analyzer market size in 2025, which shows how closely this tier fits the needs of standard hospital laboratories and larger outpatient facilities. These systems serve sites that must balance assay breadth, physical footprint, turnaround time, and capital cost without moving to the largest mega-lab architecture. Their installed advantage is practical rather than temporary, because many institutions do not need ultra-high capacity across every shift. Mid-throughput platforms also tend to support broad menus and manageable service requirements, which helps them stay entrenched in routine procurement cycles.

The chemiluminescence immunoassay analyzer market is expected to see its strongest throughput growth in the high-throughput tier, which is projected to advance at a 9.03% CAGR through 2031. This reflects continued reference laboratory consolidation in North America and Europe and new central laboratory construction across Asia-Pacific. SNIBE states that its MAGLUMI X10 reaches 1,000 tests per hour per module, which shows how aggressive capacity expansion has become in tender-driven and large-hospital settings. Buyers in these large sites are increasingly skipping the middle tier when they replace legacy systems, because they want room for menu growth and higher sample peaks from the start. Low-throughput analyzers still keep a clear niche in smaller clinics, rural settings, and outreach laboratories where compact design and moderate daily volumes matter more than step-change capacity.

By Sample Type: Blood Anchors Clinical Volumes, Saliva Emerges As A Differentiated Growth Matrix

Blood held 39.88% share in 2025, which kept it as the main specimen matrix across the chemiluminescence immunoassay analyzers market. Serum and plasma remain central to endocrine panels, troponin testing, infectious disease serology, therapeutic drug monitoring, and many oncology markers. Long-standing clinical validation and laboratory workflow familiarity continue to favor blood-based testing for the highest-volume routine applications. Whole blood and urine also hold defined roles in point-of-care and toxicology settings, but they do not match the breadth of blood-derived immunoassay use in centralized laboratories.

The chemiluminescence immunoassay analyzer market is also seeing a gradual shift toward noninvasive and differentiated matrices, with saliva projected to grow at a 7.04% CAGR through 2031. An Analyst review published in 2026 highlighted progress in microfluidic paper-based salivary diagnostic systems, especially for decentralized and lower-resource clinical environments. This supports the idea that saliva can become more useful in screening, triage, and repeat monitoring, where patient comfort and collection simplicity matter. Cerebrospinal fluid remains a low-volume, but clinically important matrix, especially in neurology, yet blood-based alternatives are starting to reduce dependence on lumbar puncture in some research pathways. Siemens Healthineers’ 2026 launch of Atellica IM pTau217 and BDTau blood-based assays signaled how neurological biomarker testing is moving toward more accessible specimen use.

By Application: TDM And Toxicology Anchors Revenue While Oncology Accelerates

Therapeutic drug monitoring and toxicology accounted for 31.23% share in 2025, which made it the largest application area in the chemiluminescence immunoassay analyzer market. Its scale comes from routine use in transplant care, anti-epileptic drug verification, poisoning assessment, forensic screening, and broader medication monitoring. This application remains resilient because it spans acute care, long-term disease management, emergency response, and regulated testing environments. Laboratories also value it because many of these assays require dependable repeat testing and fast result delivery within established clinical pathways.

The chemiluminescence immunoassay analyzer market is set to see faster expansion in oncology, with that application projected to rise at a 7.94% CAGR through 2031. Growth is being supported by wider use of tumor marker surveillance, closer monitoring of targeted therapies, and rising interest in broader cancer-related biomarker panels. A 2026 paper in Sensors and Actuators B: Chemical described a dual-signal electrochemiluminescent immunosensor for simultaneous AFP and PIVKA-II detection in hepatocellular carcinoma, which reflects active innovation at the assay level. Infectious disease, endocrinology, cardiovascular, and autoimmune applications continue to supply large and steady routine volumes across the installed base. The result is an application mix where one broad testing block anchors current revenue while cancer diagnostics adds the strongest near-term growth pull.

By End User: Hospitals Are Both The Largest And Fastest-Growing Buyer Segment

Hospitals represented 44.01% of the chemiluminescence immunoassay analyzer market size in 2025 and remained the largest buyer group across the installed base. They are also projected to grow at an 8.19% CAGR through 2031, which makes them both the leading and fastest-expanding end-user segment. This pattern reflects health system consolidation, centralized procurement, and broad test menu demand across inpatient, outpatient, emergency, and specialty departments. Hospitals also tend to sign larger reagent and service agreements, which deepens platform commitment once a supplier is selected.

The chemiluminescence immunoassay analyzer market still relies heavily on diagnostic laboratories outside hospital walls, because those facilities handle large outsourced routine volumes and support network efficiency. Specialty clinics are adding more on-site immunoassay capability in areas such as endocrinology and oncology, where same-day treatment decisions are becoming more common. Academic and research institutes continue to matter because they help validate new biomarkers and support early assay adoption in specialized workflows. Contract research organizations also add a more stable demand layer through clinical trial processing, immunogenicity testing, and biomarker qualification work. In the chemiluminescence immunoassay analyzers industry, this end-user mix keeps demand broad, but hospitals still set the tone for the biggest equipment and reagent commitments.

By Connectivity: LIS/HL7 Forms The Standard Baseline, Remote Monitoring Gains Traction

LIS and HL7 integration held 36.41% share in 2025, which made interoperability the leading connectivity requirement in the chemiluminescence immunoassay analyzer market. Buyers now expect analyzers to move results cleanly into laboratory and hospital information systems without manual intervention or fragmented data handling. This is important for audit readiness, traceability, reflex testing, and multi-site reporting across large health systems. The EU Laboratory Report Specification published through the EURIDICE framework is reinforcing structured exchange expectations and digital reporting consistency in European laboratory settings.

The chemiluminescence immunoassay analyzer market is also moving toward remote monitoring and IoT connectivity, which is forecast to grow at a 6.87% CAGR through 2031. Laboratories and vendors both benefit from tools that support predictive maintenance, remote diagnostics, quality control review, and faster response to performance drift. Middleware remains important because many laboratories still operate mixed fleets and older information systems that need a bridge layer before new analyzers can be fully integrated. Cybersecurity and compliance features are also becoming more visible in buying decisions as data governance standards become stricter across healthcare networks. This means connectivity is no longer a supporting feature, because it now affects uptime, audit quality, service efficiency, and the useful life of the installed base.

Geography Analysis

North America held 41.71% of the chemiluminescence immunoassay analyzer market share in 2025, which kept it as the largest regional block. The region benefits from strong reimbursement structures, deep hospital relationships with major OEMs, and a large installed base tied to recurring reagent contracts. The United States remains the anchor country, supported by a steady flow of assay launches and system upgrades from major suppliers in 2025 and 2026. Those additions raise platform utilization without always requiring instrument replacement, which strengthens long-term customer retention.

Europe remained the second-largest regional market in the chemiluminescence immunoassay analyzer market and continued to be shaped by regulation as much as by laboratory demand. EU IVDR requirements are pushing replacement and revalidation activity for legacy systems, especially where older platforms need updated documentation and compliance support. Western Europe also favors global suppliers that can manage multi-country tenders, broad service coverage, and integrated product portfolios across several testing categories. The EURIDICE laboratory reporting framework is reinforcing structured data exchange and traceability requirements, which adds another layer of value to connectivity-ready analyzers.

Asia-Pacific is projected to grow at an 8.85% CAGR through 2031, which makes it the fastest-growing regional segment in the chemiluminescence immunoassay analyzer market. China is a major driver because procurement reforms are changing buying behavior and giving more weight to price, local service, and domestic manufacturing strength. India is also adding momentum through private diagnostic chain expansion and broader use of integrated immunoassay systems in urban tertiary hospitals. Japan, South Korea, and Australia continue to contribute stable demand for mid-to-high technology platforms and advanced assay menus. The Middle East and Africa and South America remain smaller in absolute size, but centralized diagnostic investment in Gulf countries and ongoing laboratory growth in Brazil and Argentina keep these regions relevant for long-term expansion.

Competitive Landscape

The chemiluminescence immunoassay analyzer market is moderately concentrated, with F. Hoffmann-La Roche, Abbott Laboratories, Siemens Healthineers, and Danaher maintaining strong positions through installed base depth, menu breadth, and long reagent relationships. Competition is strongest around throughput, automation quality, assay menu expansion, and digital integration rather than simple instrument placement alone. Closed architectures still give leading suppliers an advantage because once an analyzer is adopted, the related reagent stream tends to remain attached over multiple years. At the same time, Chinese manufacturers such as Mindray, SNIBE, and Maccura are increasing pressure in price-sensitive and mid-tier accounts where buyers want more choice without giving up broad routine functionality.

Strategic moves in 2025 and 2026 show that the chemiluminescence immunoassay analyzer market is being shaped by both hardware upgrades and portfolio extension. Roche strengthened its high-capacity proposition in 2026 with FDA clearance for the cobas c 703 and cobas ISE neo analytical units on the cobas pro system, which expanded integrated testing efficiency for larger laboratories. bioMérieux moved into near-patient immunoassay through its acquisition of SpinChip Diagnostics in January 2025, which added a fast whole-blood platform with central-lab-grade sensitivity for acute cardiac testing. QIAGEN also highlighted ongoing work with DiaSorin on the LIAISON QuantiFERON-TB Gold Plus II, showing how assay partnerships are being used to lift throughput and menu value on existing platforms. These moves show that vendors are not relying on one route to growth because they are combining system automation, test menu depth, and adjacent platform acquisition.

The chemiluminescence immunoassay analyzer market still has clear white space in multiplex specialty assays, decentralized quantitative testing, and connectivity upgrades for older installed systems. Suppliers that can combine broad routine menus with lower-touch maintenance and better digital workflow support are likely to defend share more effectively in mature regions. Cost-focused entrants still have room to grow, but they need credible service networks, regulatory progress, and menu reliability to displace established suppliers at scale. No single company controls the market outright, which is why competition remains active even though the leading groups hold durable positions across hospital and reference laboratory accounts.

Chemiluminescence Immunoassay Analyzer Industry Leaders

Abbott Laboratories

bioMérieux SA

Danaher Corporation

F. Hoffmann-La Roche Ltd.

Siemens Healthineers AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Roche received FDA 510(k) clearance for the cobas c 703 and cobas ISE neo analytical units on its cobas pro integrated solution, the cobas c 703 delivers up to 2,000 tests per hour with 70 reagent positions, addressing staffing shortages through fully automated monthly operator maintenance cycles.

- March 2026: Roche's Ionify steroid assay panel, Estradiol, DHEA, DHEA-S, Progesterone, 17-OHP, and Androstenedione on the cobas i 601 analyzer, received CLIA Moderate Complexity FDA classification, broadening routine laboratory access to mass spectrometry-based steroid hormone testing without the need for specialized operators.

- February 2026: Abbott's Alinity i NT-proBNP assay received FDA 510(k) clearance, enabling chemiluminescent microparticle immunoassay-based heart failure biomarker quantification with 30-day on-instrument reagent stability on the Alinity i system.

- January 2026: Siemens Healthineers received FDA clearance for the Atellica IM Total PSA II, tPSAII, assay, strengthening prostate cancer monitoring capabilities on the Atellica IM platform after a 222-day extended FDA review cycle.

Global Chemiluminescence Immunoassay Analyzer Market Report Scope

Chemiluminescence Immunoassay (CLIA) analyzers are diagnostic medical devices that measure antigen-antibody complex formations through the emission of light (luminescence). By using chemical probes that generate light proportional to disease markers in a sample, these high-throughput systems provide rapid, highly sensitive clinical testing for infectious diseases, oncology, and endocrinology.

The Chemiluminescence Immunoassay (CLIA) Analyzer Market is segmented across several dimensions. By Technology, it includes Electrochemiluminescence Immunoassay, Microparticle Chemiluminescence Immunoassay, and Chemiluminescence Enzyme Immunoassay. By Throughput, the market is divided into High-Throughput, Mid-Throughput, and Low-Throughput systems. By sample type, CLIA analyzers are used for Blood, Serum and Plasma, Urine, Saliva, and Cerebrospinal Fluid. By Application, they support testing in Infectious Diseases, Endocrinology, Oncology, Cardiovascular Testing, Autoimmune Disorders, and Therapeutic Drug Monitoring and Toxicology. By End User, the market serves Hospitals, Diagnostic Laboratories, Specialty Clinics, Academic and Research Institutes, and Contract Research Organizations. By connectivity, CLIA analyzers integrate with LIS and HL7, Middleware, Remote Monitoring and IoT, and Cybersecurity and Compliance Features.

Geographically, the market is segmented into North America (United States, Canada, Mexico); Europe (Germany, United Kingdom, France, Italy, Spain, and Rest of Europe); Asia-Pacific (China, Japan, India, Australia, South Korea, and Rest of Asia-Pacific); Middle East & Africa (GCC, South Africa, and Rest of Middle East & Africa); and South America (Brazil, Argentina, and Rest of South America).

| Electrochemiluminescence Immunoassay |

| Microparticle Chemiluminescence Immunoassay |

| Chemiluminescence Enzyme Immunoassay |

| High-Throughput |

| Mid-Throughput |

| Low-Throughput |

| Blood |

| Serum and Plasma |

| Urine |

| Saliva |

| Cerebrospinal Fluid |

| Infectious Diseases Testing |

| Endocrinology |

| Oncology |

| Cardiovascular Testing |

| Autoimmune Disorders |

| Therapeutic Drug Monitoring and Toxicology |

| Hospitals |

| Diagnostic Laboratories |

| Specialty Clinics |

| Academic and Research Institutes |

| Contract Research Organizations |

| LIS and HL7 Integration |

| Middleware Integration |

| Remote Monitoring and IoT |

| Cybersecurity and Compliance Features |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology | Electrochemiluminescence Immunoassay | |

| Microparticle Chemiluminescence Immunoassay | ||

| Chemiluminescence Enzyme Immunoassay | ||

| By Throughput | High-Throughput | |

| Mid-Throughput | ||

| Low-Throughput | ||

| By Sample Type | Blood | |

| Serum and Plasma | ||

| Urine | ||

| Saliva | ||

| Cerebrospinal Fluid | ||

| By Application | Infectious Diseases Testing | |

| Endocrinology | ||

| Oncology | ||

| Cardiovascular Testing | ||

| Autoimmune Disorders | ||

| Therapeutic Drug Monitoring and Toxicology | ||

| By End User | Hospitals | |

| Diagnostic Laboratories | ||

| Specialty Clinics | ||

| Academic and Research Institutes | ||

| Contract Research Organizations | ||

| By Connectivity | LIS and HL7 Integration | |

| Middleware Integration | ||

| Remote Monitoring and IoT | ||

| Cybersecurity and Compliance Features | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the chemiluminescence immunoassay analyzer market?

The chemiluminescence immunoassay analyzer market was valued at USD 3.16 billion in 2025 and is projected to be USD 3.25 billion in 2026.

How fast is chemiluminescence immunoassay analyzer demand expected to grow through 2031?

The market is forecast to reach USD 4.64 billion by 2031 at a CAGR of 6.73% from 2026 to 2031.

Which technology segment leads revenue in chemiluminescence immunoassay analyzer?

Electrochemiluminescence immunoassay led with 45.73% share in 2025, supported by its strong sensitivity and broad use in hospital and reference laboratories.

Which end users are driving the strongest equipment demand?

Hospitals are the largest and fastest-growing buyer group, with 44.01% share in 2025 and an 8.19% CAGR through 2031.

Which region is growing fastest for chemiluminescence immunoassay analyzers adoption?

Asia-Pacific is the fastest-growing region, with an expected 8.85% CAGR through 2031, supported by procurement shifts, private diagnostics expansion, and new laboratory buildouts.

Page last updated on: