Centrifugal Blowers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.21 Billion |

| Market Size (2031) | USD 3.96 Billion |

| Growth Rate (2026 - 2031) | 4.35% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Centrifugal Blowers Market Analysis by Mordor Intelligence

The centrifugal blowers market size in 2026 is estimated at USD 3.21 billion, growing from 2025 value of USD 3.07 billion with 2031 projections showing USD 3.96 billion, growing at 4.35% CAGR over 2026-2031. Robust spending on wastewater infrastructure, clean-energy projects and petrochemical capacity expansions keep equipment demand resilient even as end-users face stricter energy-efficiency mandates. High-pressure models capture premium orders where precise aeration, pneumatic conveying and underground ventilation are mission-critical. Technology differentiation pivots on magnetic bearings, integrated variable-speed drives and digital condition monitoring, all of which reduce lifetime operating costs and shorten payback periods. Supply-side consolidation, exemplified by the Chart Industries–Flowserve merger, is reshaping how service portfolios and aftermarket parts are bundled, giving larger vendors a scale advantage in global bid tenders.

Key Report Takeaways

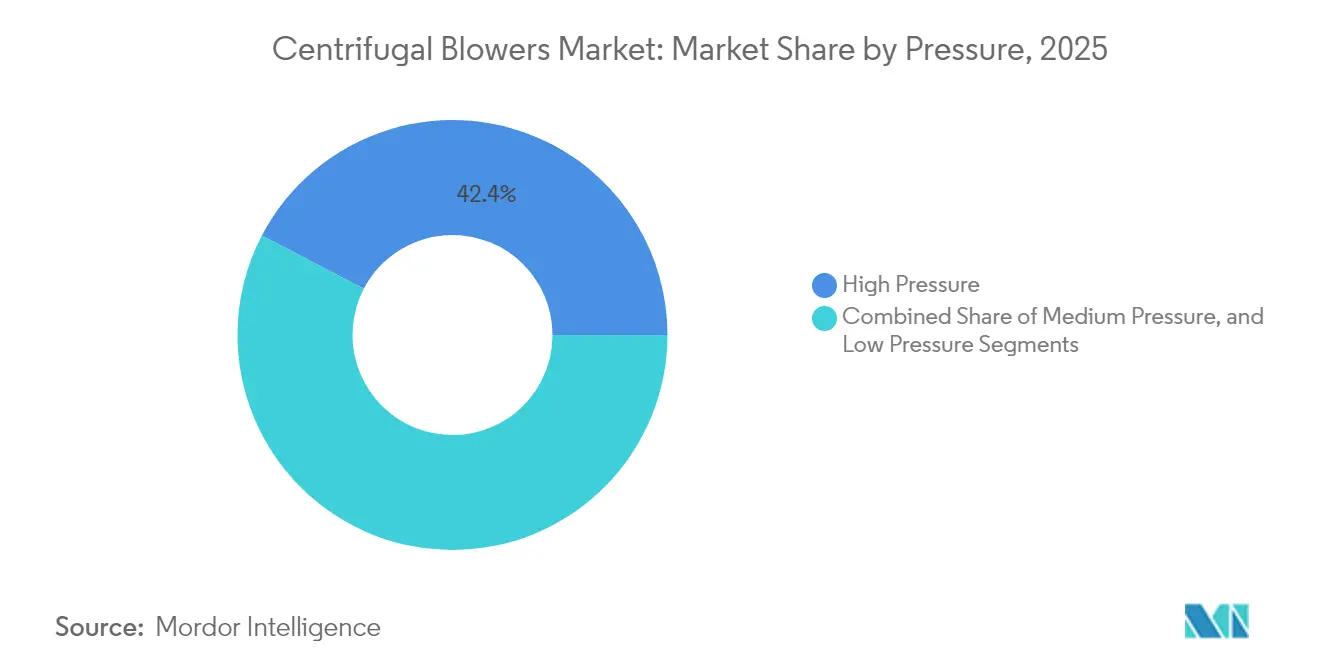

- By pressure, high-pressure configurations held 42.35% of centrifugal blowers market share in 2025 and are growing at a 4.71% CAGR to 2031.

- By stage, multistage units accounted for 36.62% of centrifugal blowers market share in 2025, while high-speed turbo machines log the fastest 5.28% CAGR.

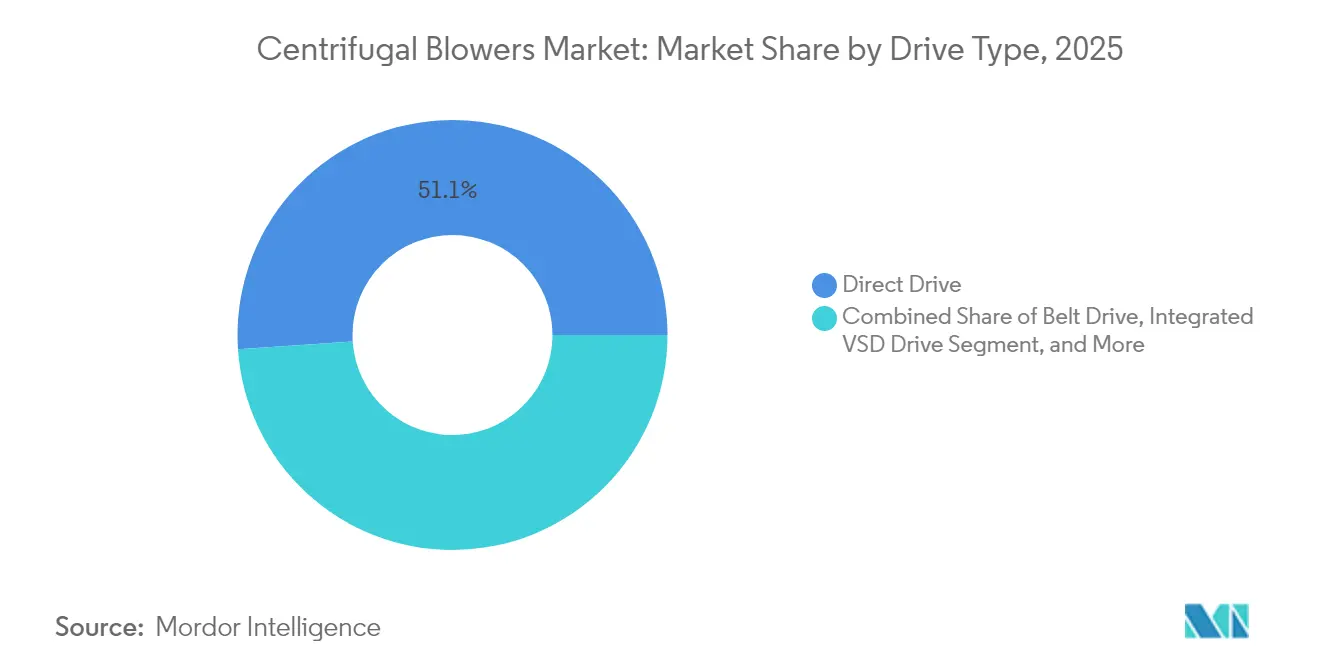

- By drive type, direct drive systems led with 51.05% share in 2025; integrated VSD packages post a 5.53% CAGR through 2031.

- By end use, water and wastewater treatment captured 27.12% of the centrifugal blowers market size in 2025 and advances at a 4.58% CAGR.

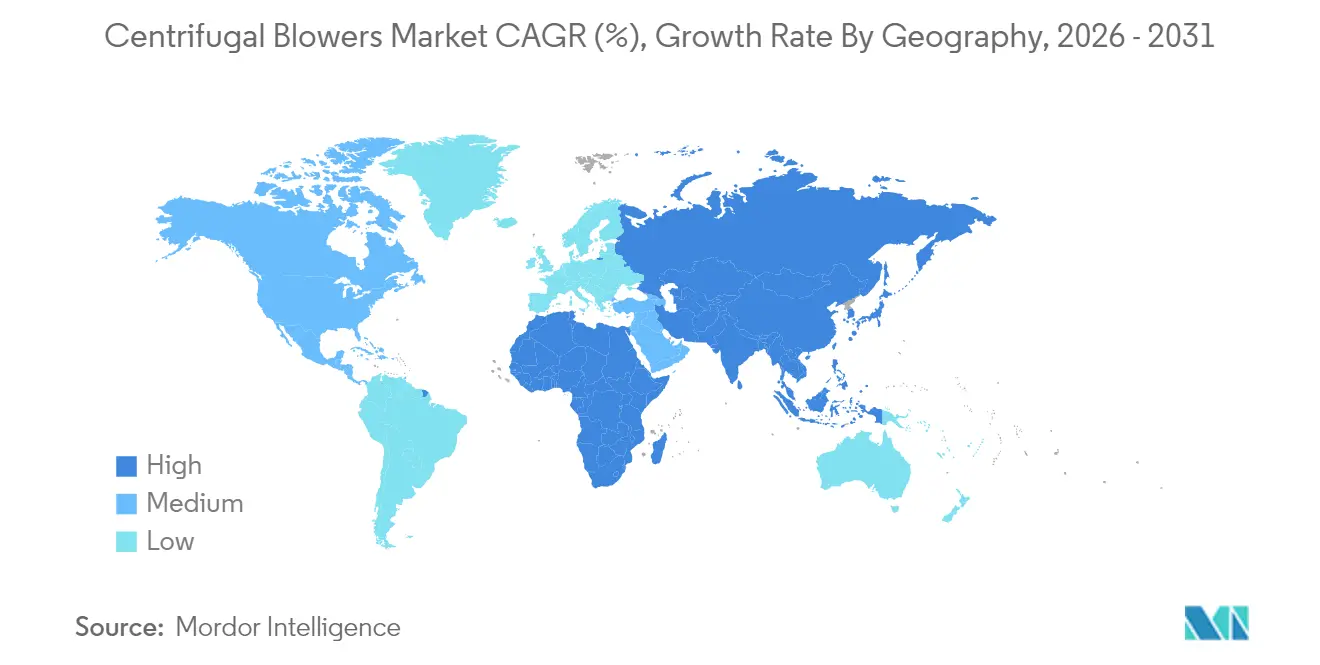

- By geography, Asia-Pacific dominated with 47.55% share of market size in 2025 and expands at a 4.47% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Centrifugal Blowers Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy-efficiency regulations and retrofits | +1.2% | Global - early adoption in North America and EU | Medium term (2-4 years) |

| Expansion of global wastewater capacity | +0.9% | Global - core activity in Asia-Pacific and North America | Long term (≥ 4 years) |

| Chemical and petrochemical build-out in APAC | +0.8% | Asia-Pacific, spill-over to Middle East and Africa | Medium term (2-4 years) |

| Biogas and hydrogen blending requirements | +0.6% | Global - early gains in North America and Europe | Long term (≥ 4 years) |

| OEM-integrated IIoT blower packages | +0.4% | Global - led by developed markets | Short term (≤ 2 years) |

| Urban low-noise HVAC incentives | +0.3% | North America and EU, expanding to urban Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Energy-efficiency regulations and retrofits

California’s Title 20 rules that took effect in April 2024 set a 1.00 Fan Energy Index threshold, prompting industrial owners to swap legacy fans for variable-speed centrifugal packages. Con Edison pays up to USD 1 million per account each year toward qualified HVAC upgrades, further compressing payback periods. Although the U.S. Department of Energy withdrew a federal standard in January 2025, state codes and EU Ecodesign requirements continue to push global operators toward high-efficiency impeller and motor combinations. Suppliers with factory-integrated drives and predictive analytics win bids because owners want documented performance and remote compliance reporting. These moves adds to the projected growth for the centrifugal blowers market.

Expansion of global wastewater treatment capacity

Only 58% of the world’s 268 billion m³ of wastewater received safe treatment in 2022, creating an urgent build-out agenda. The South Bay plant is doubling throughput to 50 million gpd under a USD 600 million program that specifies oil-free high-efficiency aeration blowers. U.S. Clean Water SRF allotments reached USD 851.2 million in fiscal 2024, while the Drinking Water SRF provided USD 494.4 million, underwriting hundreds of municipal tenders. Sulzer’s HST turbocompressors showed 34% energy savings at a Derby plant in the U.K., demonstrating why utilities upgrade instead of repairing dated roots blowers. Capacity growth combined with energy-reduction targets adds 0.9 percentage points to the market growth curve.

Chemical and petrochemical capacity build-out in Asia-Pacific

India plans to lift petrochemical output to USD 300 billion by 2025 and raise capacity from 29.62 million tons to 46 million tons by 2030 under a INR 10 lakh-crore stimulus. Middle Eastern majors pursue downstream integration and invest in Chinese joint ventures, redirecting capital from gasoline to specialty chemicals. Malaysia’s 2030 roadmap seeks specialty-chemicals hub status, sustaining demand for corrosion-resistant blowers across solvent recovery, catalyst regeneration and pneumatic conveying lines. New crackers, refineries and fertilizer complexes lock in multiyear service contracts, lifting regional equipment orders and adding to CAGR projections.

Biogas and hydrogen blending demand

The U.S. hydrogen roadmap targets 7 to 9 million tonnes per year of clean hydrogen by 2030, while Europe aims for 34 million tonnes by 2040, and electrolyzers and reformers require oil-free, hydrogen-compatible blowers that handle low-density gas without flame-flash risks.[1]U.S. Department of Energy, “Pathways to Commercial Liftoff: Clean Hydrogen,” climateprogramportal.org, Hydrogen Europe, “Clean Hydrogen Production Pathways Report 2024,” hydrogeneurope.eu Biogas plants mix hydrogen to upgrade methane, creating corrosive H₂S environments that favor duplex stainless or Hastelloy internals. Early adopters in California’s dairy clusters and Germany’s biomethane hubs showcase field performance, adding to the centrifugal blowers market expansion forecast.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and maintenance cost of turbo units | -0.7% | Global - strongest in emerging markets | Medium term (2-4 years) |

| Competition from alternative blower types | -0.5% | Global - varies by application | Short term (≤ 2 years) |

| Critical-alloy price volatility | -0.4% | Global - supply chain concentrated in select regions | Short term (≤ 2 years) |

| Shortage of magnetic-bearing technicians | -0.3% | Global - acute in developing markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High capital and maintenance cost of high-speed turbo blowers

Magnetic-bearing turbo models list well above multistage or rotary-screw alternatives. Atlas Copco’s Q1 2025 update showed softness in large compressor bookings where budget pressure is acute.[2]Atlas Copco AB, “Quarterly Report Q1 2025,” atlascopcogroup.comField support for high-speed rotors requires specialized diagnostic rigs that many regional OEM partners lack. KPMG’s sector review cites EV/2024E EBITDA multiples of 15.6× for process-flow assets, a premium that eventually trickles down to end-user costs. This cost hurdle adversaly impacts the centrifugal blowers market.

Competition from alternative blower technologies

Positive-displacement and rotary-screw designs now cover flow-pressure windows once dominated by centrifugal impellers. Aerzen’s Delta Hybrid 2.0 targets 8-15 psig at high efficiency, challenging centrifugal incumbency in municipal aeration. Atlas Copco’s oil-free ZS screw line pushes maintenance-free uptime to food plants that previously specified centrifugal stages. Technology overlap erodes differentiation, trimming the growth potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pressure: Sustained premium for high-pressure applications

High-pressure machines held 42.35% share of the centrifugal blowers market in 2025 and are forecast to grow 4.71% annually through 2031. Plants handling pneumatic transport, catalyst regeneration and underground ventilation prioritize pressure stability, which supports higher margins on duplex-steel casings and precision-machined impellers. Mining operators, including Epiroc customers, add automation that relies on stable airflow to clear dust and methane pockets.

The centrifugal blowers market size for medium-pressure units remains sizeable as general manufacturing, cement kilns and biomass boilers require dependable airflow without extreme pressure levels. Low-pressure models continue to serve HVAC and simple combustion air but face retrofit losses as owners adopt high-efficiency axial designs. Hydrogen-ready and biogas projects accelerate demand for high-pressure stainless or nickel-alloy blowers that resist embrittlement, improving the revenue mix even as volumes shift among pressure classes.

By Stage/Configuration: Multistage reliability meets turbo momentum

Multistage configurations delivered 36.62% of centrifugal blowers market size in 2025 by offering rugged performance and easy overhaul. Operators appreciate rotational speeds below 4,000 rpm that allow field balancing and straightforward bearing swaps. However, high-speed turbo packages are gaining at a 5.28% CAGR owing to magnetic-bearing impellers finding application in high precision edn-use application. Utility-scale wastewater plants adopt these oil-free units to cut energy bills and avoid lube-oil disposal.

Single-stage overhung wheels still dominate low-pressure HVAC jobs, while integrally-geared models find favor where floor space is tight and discharge pressure falls between multistage and turbo capabilities. OEMs integrate cloud sensors across all configurations, enabling runtime comparisons that guide buyers toward the optimum life-cycle-cost curve. As predictive analytics quantify savings, centrifugal blowers market share is expected to tilt gradually toward turbo designs that sustain performance guarantees.

By Drive Type: Direct drive steadies the base; VSD gains velocity

Direct-coupled motors delivered 51.05% share of the centrifugal blowers market in 2025 due to simplicity, limited alignment issues and widespread technician familiarity. Belt drives survive in brownfield plants where shaft geometry cannot accommodate direct coupling. Integrated VSD packages grow at 5.53% CAGR because utilities reward demand-response capability and because Title 20 rules tighten part-load fan efficiency.Modern VSD firmware supports harmonic filtering and remote fault diagnostics, reducing downtime.

Magnetic-bearing drives occupy the frontier, eliminating oil seals and enabling higher tip speeds. Food, pharma and semiconductor fabs cite contamination-free airflow as the driver for early adoption. As more service centers invest in magnetic-bearing balancers, centrifugal blowers market share for these premium drives should widen, especially in hydrogen production skids and biogas digesters that value oil-free performance.

By End-use Industry: Water treatment anchors diversified demand

Water and wastewater facilities accounted for 27.12% of centrifugal blowers market share in 2025 and advance 4.58% per year to 2031. Biological nutrient removal and stricter outflow permits force municipalities to upgrade aeration capacity. The USD 600 million South Bay expansion doubles daily volume, adding high-efficiency blowers with oxygen-transfer guarantees.

Chemicals and petrochemicals rank second as India, China and the Middle East commission new crackers and fertilizer lines. Mining, cement and steel contribute a steady baseline, although order timing follows commodity price swings. Commercial buildings leverage Con Edison incentives to retrofit fans, while food and beverage processors specify oil-free stages to avoid product taint. This diversity cushions the centrifugal blowers market against downturns in any single sector and allows OEMs to balance capacity across product lines.

Geography Analysis

Asia-Pacific held 47.55% of centrifugal blowers market share in 2025 and is forecast to grow 4.47% annually to 2031. India’s petrochemical capacity expansion from 29.62 million tons to 46 million tons drives continuous bids for high-pressure process air. Chinese refinery additions and Southeast Asian specialty-chemicals projects bolster regional order books. Malaysia’s chemicals roadmap and tax incentives attract global polyolefin players that need corrosion-resistant blowers for slurry-loop reactors. Local casting clusters in Gujarat and Shandong shorten lead times and cushion freight costs, sustaining competitive landed pricing.

North America remains a mature but opportunity-rich territory. The South Bay wastewater upgrade and similar SRF-funded projects keep municipal demand steady. California’s Title 20 and New York utility incentives accelerate replacement of fixed-speed fans with VSD units. Hydrogen hubs financed through the Infrastructure Investment and Jobs Act require oil-free blowers for electrolyzers, opening a pipeline of orders that extends through the decade.

Europe delivers consistent but policy-linked growth. Sulzer recorded 15.6% order uptick in Europe, the Middle East and Africa during 2024 driven by wastewater mandates and refinery turnarounds. The bloc’s 34 million-tonne hydrogen goal by 2040 necessitates pressure-stable, oil-free air for PEM and alkaline stacks. The Middle East supplements volumes as ADNOC and Saudi Aramco shift toward ammonia and chemicals, each requiring dedicated blower trains for air separation, sulfur recovery and nitric-acid loops.

Competitive Landscape

Global suppliers pursue scale, technology depth and stable aftermarket revenue. Chart Industries and Flowserve plan to merge into a USD 19 billion enterprise, combining USD 3.7 billion in service sales that smooth equipment-cycle volatility. Ingersoll Rand closed 13 acquisitions worth USD 450 million in 2023, including Roots, which fortifies its low-pressure lineup and opens cross-selling into municipal bid lists.

Technology differentiation centers on magnetic bearings, integrated analytics and composite impellers. Loar Holdings’ EUR 365 million purchase of LMB Fans & Motors adds aerospace-grade designs that meet extreme reliability requirements for pharmaceutical isolators and nuclear glove boxes. Atlas Copco posted 3% organic order growth in its gas-and-process compressor segment, illustrating that process-critical buyers prioritize oil-free, high-speed solutions.

Service offerings evolve toward continuous monitoring. Ebara and Verizon collaborate on cyber-secure telemetry for blower fleets, an attractive value-add for utilities concerned about OT vulnerabilities. Smaller regional assemblers pivot to contract machining or focus on aftermarket parts to avoid direct competition. The centrifugal blowers market therefore balances consolidation at the top with a long tail of niche suppliers, preserving customer choice even as global portfolios expand.

Centrifugal Blowers Industry Leaders

Howden Group

Illinois Blower Inc

Atlantic Blowers, LLC

Piller Blowers & Compressors

Alfotech Fans

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Chart Industries booked USD 1.32 billion in Q1 orders, lifting backlog past USD 5 billion

- April 2025: Atlas Copco launched an oil-free rotary screw compressor for ultra-clean air applications .

- March 2025: Sulzer reported CHF 3.531 billion (USD 4.35 billion) in 2024 sales, up 10.8%, powered by Flow division blowers

- February 2025: Chart Industries and Flowserve agreed to merge, creating a USD 19 billion process-technology leader

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the centrifugal blowers market as revenue generated from sales of new mechanical devices that use a rotating impeller to accelerate air radially outward before discharging it at a right angle, across industrial, commercial, and environmental applications worldwide. According to Mordor Intelligence, the baseline year is 2025, when the market was valued at USD 3.07 billion; forecasts extend to 2030.

Scope exclusion: axial flow fans, regenerative blowers, and turbo-compressors fall outside this remit.

Segmentation Overview

- By Pressure

- High Pressure

- Medium Pressure

- Low Pressure

- By Stage/Configuration

- Single-Stage

- Multistage

- High-Speed Turbo

- Integrally Geared

- By Drive Type

- Direct Drive

- Belt Drive

- Integrated VSD Drive

- Magnetic-Bearing Drive

- By End-use Industry

- Mining

- Cement

- Pulp and Paper

- Construction

- Steel

- Chemicals and Petrochemicals

- Power Generation

- Water and Wastewater Treatment

- Food and Beverage

- HVAC and Commercial Buildings

- Other Industries

- By Geography

- North America

- United States

- Canada

- South America

- Brazil

- Argentina

- Europe

- Germany

- United Kingdom

- France

- Italy

- Russia

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Africa

- South Africa

- Nigeria

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed plant maintenance managers, OEM sales directors, and procurement leads in water and wastewater, cement, mining, and pulp and paper facilities across Asia-Pacific, North America, and Europe. These conversations verified installed base turnover rates, average selling prices, and emerging preferences for integrated VFD drives, which we then reconciled with secondary indicators.

Desk Research

We first mapped the universe of equipment counts and trade flows using freely accessible authorities such as UN Comtrade shipment codes, Eurostat PRODCOM industrial output tables, the US International Trade Commission's HTS archive, and regional energy statistics released by the International Energy Agency. Standards and regulatory references from OSHA, China's Ministry of Ecology and Environment, and India's CPCB clarified pressure and efficiency thresholds that shape demand. Paid platforms, notably D&B Hoovers for manufacturer revenues and Dow Jones Factiva for deal flow, enriched company-level calibration. The sources listed illustrate our approach; many additional publications were reviewed to cross-check datapoints, fill gaps, and maintain currency.

Market-Sizing and Forecasting

One blended top-down build started with 2024 industrial production, capital expenditure, and wastewater infrastructure budgets; we reconstructed demand pools and applied penetration rates for blower replacement cycles. Select bottom-up spot checks, supplier roll-ups, and regional channel audits validated totals before adjustment.

Key variables include: - new cement kiln capacity (m2), - mining ore throughput (Mt), - municipal wastewater treated volume (billion m3), - average selling price shifts tied to high-speed turbo adoption, - regional electricity prices influencing energy-efficient upgrades.

A multivariate regression model projects 2026 to 2030 growth, with coefficients benchmarked through primary expert consensus. Where supplier counts were incomplete, ratios from proxy regions were cautiously imputed and flagged for review.

Data Validation and Update Cycle

Outputs pass three tiers of variance checks, peer review, and senior analyst sign-off. We refresh the dataset annually and trigger interim updates after material events such as major capacity announcements or regulatory changes; a pre-publication sweep ensures clients receive the latest validated view.

Why Mordor's Centrifugal Blowers Baseline Earns Trust

Published estimates often differ because firms choose distinct product baskets, pricing curves, currency bases, and update cadences. By anchoring scope strictly to centrifugal blowers sold as new OEM units and re-benchmarking prices every six months, Mordor reduces mismatch risk.

Key gap drivers we observe include: some studies bundle axial fans and turbo-compressors, others freeze exchange rates, and a few model demand from installed horsepower rather than invoiced value, producing wider spreads when energy-efficient retrofits surge.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.07 B (2025) | Mordor Intelligence | - |

| USD 3.33 B (2025) | Global Consultancy A | Treats radial fans as interchangeable products |

| USD 2.40 B (2024) | Industry Journal B | Excludes sales through engineering, procurement, and construction (EPC) contracts |

| USD 3.57 B (2025) | Research Boutique C | Uses list prices without regional ASP normalization |

In short, Mordor Intelligence delivers a balanced, transparent baseline grounded in clearly defined scope, regularly refreshed variables, and cross-validated inputs that decision-makers can replicate and interrogate with confidence.

Key Questions Answered in the Report

What is the projected size of the centrifugal blowers market by 2031?

The centrifugal blowers market is expected to reach USD 3.96 billion by 2031 on a 4.35% CAGR.

Which pressure class leads revenue today?

High-pressure machines held 42.35% share in 2025 and remain the fastest-growing pressure segment at 4.71% CAGR.

Why are variable-speed drives gaining traction?

Utility incentives and Title 20 efficiency rules push owners to adopt integrated VSD packages that cut power use at part load, supporting a 5.53% CAGR for this drive segment.

How is wastewater investment influencing blower demand?

Large projects such as the USD 600 million South Bay upgrade require high-efficiency aeration blowers, reinforcing water treatment as the top end-use segment.

What role does clean hydrogen play for blower suppliers?

Electrolyzers and low-carbon reformers need oil-free, hydrogen-compatible blowers, opening a significant new application stream as the United States targets up to 9 million tons per annum of capacity by 2030.

Which regions are expanding fastest in the centrifugal blowers market?

Asia-Pacific leads with a projected 4.47% CAGR, driven by petrochemical build-outs in India, refinery additions in China and specialty-chemical investments across Southeast Asia.

Page last updated on: