Liquid Ring Vacuum Pump Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

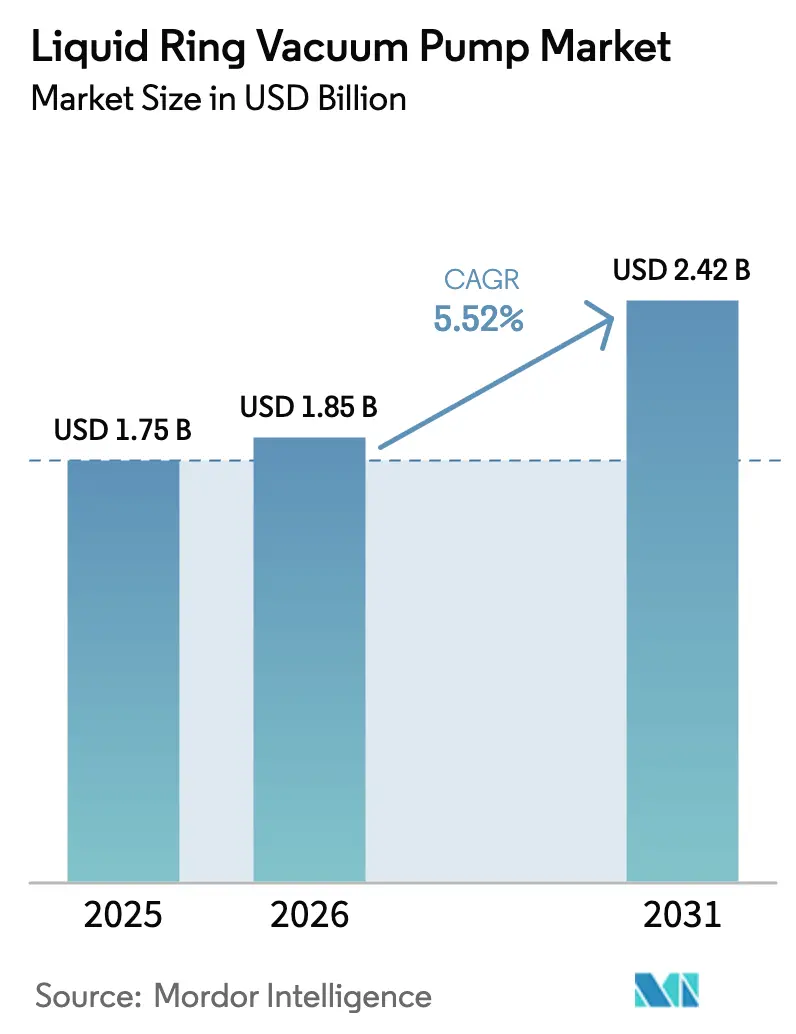

| Market Size (2026) | USD 1.85 Billion |

| Market Size (2031) | USD 2.42 Billion |

| Growth Rate (2026 - 2031) | 5.52% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Liquid Ring Vacuum Pump Market Analysis by Mordor Intelligence

The liquid ring vacuum pump market size was valued at USD 1.75 billion in 2025 and estimated to grow from USD 1.85 billion in 2026 to reach USD 2.42 billion by 2031, at a CAGR of 5.52% during the forecast period (2026-2031). Growth has centered on Asia-Pacific chemical capacity additions, continued migration of pharmaceutical producers to solvent-recovery systems, and steady pulp-and-paper recycling investments. Stainless-steel construction gained prominence as operations processed more corrosive streams, while two-stage configurations took share in applications requiring deeper vacuum. Mid-scale capacities (501–5,000 m³/h) dominated demand because they match most stand-alone process units and offer balanced capital and operating costs. Competitive intensity rose as global leaders added water-efficient retrofits, and regional manufacturers leveraged price agility to win cost-sensitive orders. Nevertheless, tightening energy-efficiency rules in the European Union and western North America curbed uptake in light-duty cycles that could instead shift toward dry screw alternatives.

Key Report Takeaways

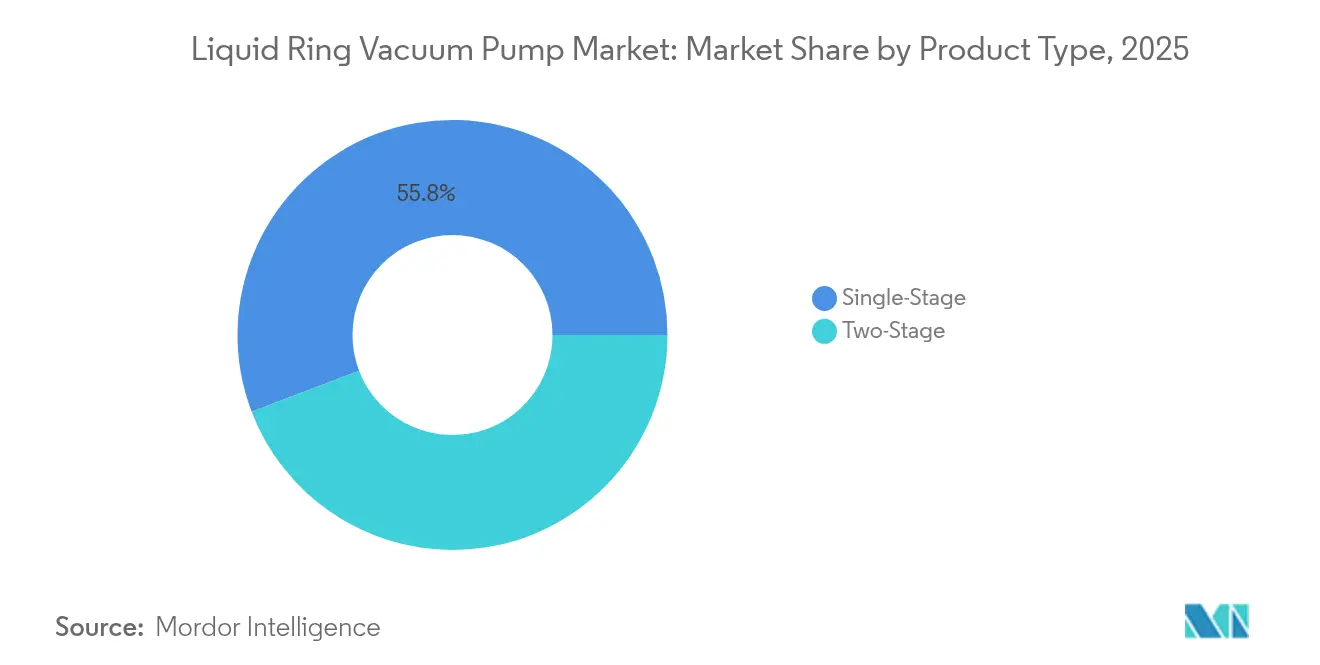

- By product type, single-stage units led with 55.80% of liquid ring vacuum pump market share in 2025, while two-stage models are projected to advance at 6.55% CAGR to 2031.

- By material, stainless steel captured 48.90% revenue share in 2025; other materials are forecast to expand at a 7.02% CAGR through 2031.

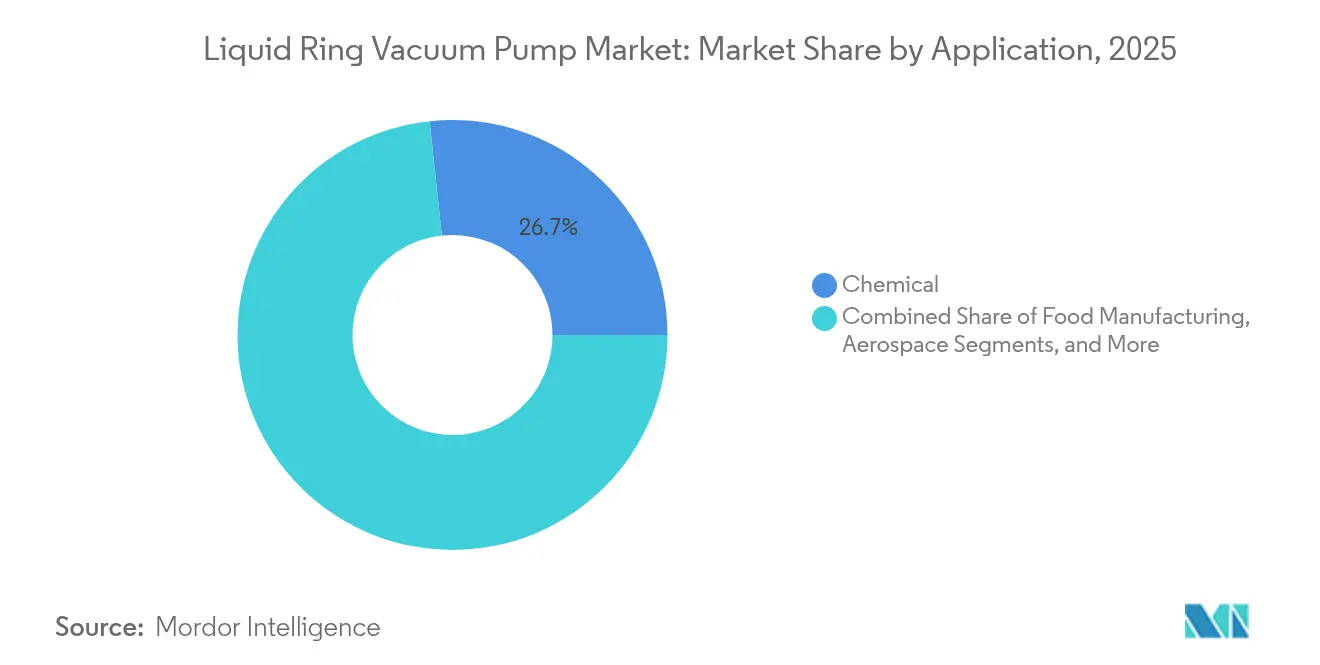

- By application, chemical processing held 26.70% share of the liquid ring vacuum pump market size in 2025, yet pharmaceutical uses are growing at 7.66% CAGR to 2031.

- By capacity, the 501–5,000 m³/h range accounted for 38.90% share in 2025 and remains the volume leader, whereas >15,000 m³/h systems are set to post a 6.76% CAGR through 2031.

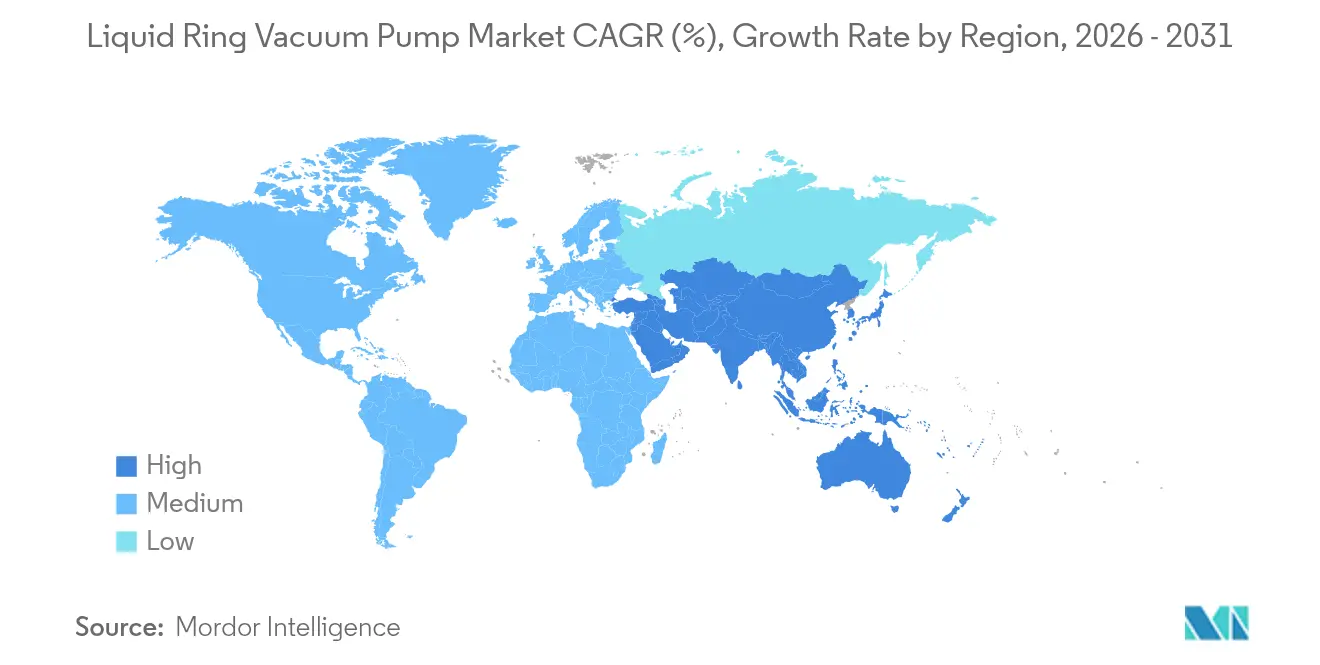

- By geography, Asia-Pacific dominated with 43.00% share in 2025 and is advancing at 7.32% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Liquid Ring Vacuum Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid expansion of chemical processing capacity in APAC | +1.8% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Transition from dry-vacuum systems to water-efficient liquid-ring retrofits | +0.7% | Global, concentrated in drought-prone regions | Short term (≤ 2 years) |

| Tightening solvent-emission norms in pharma and food packaging | +0.9% | North America and EU, expanding to APAC | Long term (≥ 4 years) |

| Surge in pulp-and-paper recycling mills | +0.6% | North America, Europe, emerging in APAC | Medium term (2-4 years) |

| Growth of green-hydrogen electrolyzer vacuum stations | +0.8% | EU and North America, pilot projects in APAC | Long term (≥ 4 years) |

| Demand for large-capacity pumps in lithium-refining projects | +0.5% | APAC, South America, emerging in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid expansion of chemical processing capacity in APAC

Asia-Pacific chemical producers continued adding world-scale plants that require reliable vacuum to manage wet, corrosive streams. China’s ethylene projects alone specified 15–25 large liquid ring systems per complex, boosting aggregate demand through 2030. [1]Chemical & Engineering News, “China dominates global ethylene capacity additions,” cen.acs.org India’s specialty-chemical push similarly elevated vacuum requirements for distillation and crystallization. Integrated chemical parks favored centralized vacuum stations where liquid ring units deliver continuous performance with minimal downtime. System orders often bundled digital monitoring to maximize runtime, creating new service revenue for OEMs.

Tightening solvent-emission norms in pharma and food packaging

The United States Environmental Protection Agency mandated 99.5% solvent recovery for pharmaceutical vents in 2024, prompting widespread upgrades from oil-sealed or dry pumps to liquid ring models that can use compatible seal liquids and avoid contamination risks.[2]MD-Kinney, “Liquid Ring Two-Stage KLRC,” md-kinney.com European regulators adopted analogous thresholds, and early adopters reported 15–20% solvent recovery improvements. Adoption extended to food packaging lines handling food-grade solvents where contamination controls are equally stringent.

Surge in pulp-and-paper recycling mills

North American mills added more than 2 million tons of recycling capacity in 2024, each installing 8–12 liquid ring pumps to manage deinking and dewatering stages. The pumps’ tolerance for suspended solids lengthened service intervals by 25% versus dry alternatives, lowering downtime costs. Similar upgrades proceeded in Europe as mills sought energy savings through higher vacuum consistency.

Growth of green-hydrogen electrolyzer vacuum stations

Gigawatt-class electrolyzer projects in Germany and the United States specified liquid ring units for moisture-laden stack evacuation. The technology’s compatibility with water seal liquids met strict purity demands, avoiding hydrocarbon traces that can poison fuel cells. Each GW facility required four to six units, forming a niche yet lucrative pocket for OEMs with corrosion-resistant designs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High water-consumption charges in drought-prone regions | -0.4% | Western North America, Australia, parts of APAC | Short term (≤ 2 years) |

| Energy-efficiency penalties vs. dry screw tech in light-duty cycles | -0.3% | EU, North America (energy-regulated markets) | Medium term (2-4 years) |

| Scarcity of foundry-grade recycled stainless steel | -0.2% | Global, acute in APAC manufacturing hubs | Long term (≥ 4 years) |

| Rising PFAS-ban compliance cost for process-water disposal | -0.1% | North America, EU, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High water-consumption charges in drought-prone regions

Industrial water prices touched USD 8.50 per m³ in California during 2024, making continuous-flow liquid ring pumps costly to operate. Users adopted closed-loop circuits that trimmed makeup water by up to 90%, but upfront expense slowed replacement schedules. Some light-duty applications migrated entirely to dry screw designs to avoid water fees, squeezing market volume growth in these areas.

Energy-efficiency penalties versus dry screw technology

Liquid ring designs consumed roughly 30% more electricity than dry screw pumps at partial loads, a disadvantage magnified by European power tariffs of USD 0.17 per kWh in 2024. Carbon-price regimes placed additional cost on kilowatt-hours, steering batch-process operators toward high-efficiency dry units. Nevertheless, where condensable vapors prevailed, users valued liquid ring performance stability over theoretical power savings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Two-Stage Systems Gain Traction

Single-stage units held 55.80% of liquid ring vacuum pump market share in 2025 owing to their simplicity and lower capital expense. The configuration met vacuum needs up to 26 inHg for concrete, paper, and general process duties. Two-stage models, however, expanded at 6.55% CAGR, securing orders in pharmaceutical drying and specialty-chemical distillation where ultimate pressures below 29 inHg are mandatory.

The two-stage architecture delivered deeper vacuum without oil seals, minimizing product contamination and enabling solvent recovery. Although capex was higher, operators accepted the premium for quality and regulatory compliance. Single-stage designs retained favor in abrasive or dirty service because fewer components simplified maintenance cycles exceeding 8,000 hours between failures.

By Material: Stainless Steel Accelerates

Stainless steel captured 48.90% share in 2025, reflecting process industries’ shift toward corrosive and high-purity streams. Growth ran at 7.02% CAGR through 2031 as 316L grades became standard in pharmaceutical installations to satisfy FDA cleanability audits. Cast iron continued serving cost-sensitive spheres-pulp, paper, and general industry-where chemical attack risk remained low.

Alloy and composite pumps filled narrow niches such as offshore marine duty or environments demanding weight reduction. Yet stainless technology dominated bids where contamination was unacceptable, and market leaders widened their stainless portfolios with magnetic-drive options that eliminated shaft-seal leakage.

By Application: Pharmaceutical Sector Accelerates

Chemical processing applications maintained 26.70% of 2025 volume, anchoring the liquid ring vacuum pump market. Still, pharmaceutical projects delivered a 7.66% CAGR edge, propelled by emission restrictions and solvent-recovery mandates. The segment regularly specified closed-loop seal-liquid circuits that recycle captured solvents, bolstering payback economics.

Food manufacturing also adopted the technology to ensure contamination-free vapor handling while meeting hygiene codes. Aerospace autoclave and automotive paint operations generated stable orders, and offshore oil producers valued liquid ring tolerance for wet, sour gases.

By Capacity Range: Mid-Scale Systems Prevail

The 501–5,000 m³/h bracket controlled 38.90% of 2025 demand, balancing capital cost with the flow needs of single process units. Large modules above 15,000 m³/h are forecast at 6.76% CAGR as integrated parks centralize vacuum generation. Conversely, lab-scale ≤500 m³/h pumps targeted pilot facilities and R&D lines.

Package builders marketed modular mid-scale skids that can be paralleled, enabling phased capacity expansion. Larger capacities bundled redundant stages and advanced controls to safeguard uptime for multi-unit complexes.

Geography Analysis

Asia-Pacific retained 43.00% share in 2025 and was on track for a 7.32% CAGR as petrochemical, specialty-chemical, and semiconductor projects proliferated. China expanded ethylene output by more than 20 million t annually, each complex integrating extensive liquid ring infrastructure. India’s chemical sector was projected to reach USD 300 billion by 2025, with specialty-chemical plants demanding stainless pumps tolerant of aggressive solvents. Southeast Asian relocation of mid-tier chemical manufacturing further supported regional demand.

North America experienced steady replacements tied to pharmaceutical capacity and shale-derived petrochemicals. Energy-efficiency credits encouraged retrofits to closed-loop designs, while oil-sands and gas-processing operations in Canada favored large stainless units suited for abrasive, water-laden gases. Mexico’s chemicals growth on near-shoring also lifted sales of mid-scale systems.

Europe focused on energy-optimized packages that integrated heat recovery and variable-speed drives. German, Swiss, and Irish pharma clusters upgraded to two-stage stainless equipment for validation compliance. The Middle East’s petrochemical build-outs under Vision 2030 adopted large cast-iron and stainless assemblies engineered for 24/7 desert duty, and South American lithium refining started specifying high-capacity lines, signalling future export opportunity for global OEMs.

Competitive Landscape

The liquid ring vacuum pump market remained moderately concentrated. Atlas Copco, Flowserve, and Nash leveraged broad product lines, global parts depots, and digital monitoring suites. Atlas Copco’s 2025 purchase of Kyungwon Machinery deepened semiconductor ties in Korea and supported localized service.[4]Water Online, “Atlas Copco Launches Intelligent, Durable And Efficient Range Of Liquid Ring Vacuum Pumps With Dual VSD Technology,” wateronline.com Flowserve expanded aftermarket retrofits that blend closed-loop water circuits with heat exchangers, addressing drought-zone customers. Nash promoted magnet-drive units to curb seal failures in corrosive media.

Regional challengers Guangdong Kenflo and PPI Pumps captured commodity orders by offering simplified cast-iron models with shorter lead times. Japanese builder Miura introduced a resin-casing pump cutting weight 20%, targeting marine markets where weight savings trimmed fuel use. Patent filings concentrated on magnetic bearings and integrated variable-speed drives, promising 8-12% energy savings and extended overhaul intervals.

Strategic focus shifted toward application engineering in green-hydrogen, lithium processing, and recycled pulp where process nuances demanded tailored materials and vacuum depths. Service revenue grew as customers opted for predictive maintenance subscriptions to minimize unplanned stops.

Liquid Ring Vacuum Pump Industry Leaders

Atlas Copco AB

Flowserve Corporation

Ingersoll Rand Inc.

Graham Corporation

Busch SE (Busch Vacuum Solutions)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Miura launched the MEA-37E resin-casing pump, reducing assembly weight 20% for offshore platforms.

- May 2025: Oak Ridge National Laboratory patented a vacuum-assisted extrusion method that cut polymer porosity 75% and opens new pump applications.

- February 2025: Graham Corporation announced a USD 17.6 million plant expansion after securing a USD 2.1 million U.S. Navy vacuum-system contract.

- January 2025: Atlas Copco completed the USD 465 million acquisition of Kyungwon Machinery to reinforce regional coverage in semiconductor fabrication.

Global Liquid Ring Vacuum Pump Market Report Scope

Across numerous industries, liquid ring vacuum pumps are pivotal, ensuring reliable and efficient vacuum processes. Liquid Ring Vacuum Pumps are known for their reliability and simple construction. The research also examines underlying growth influencers and significant industry vendors, all of which help to support market estimates and growth rates throughout the anticipated period. The market estimates and projections are based on the base year factors and arrive at using top-down and bottom-up approaches.

The liquid ring vacuum pump market is segmented by type (Single-Stage and Two-Stage), by material (Cast Iron, Stainless Steel and Other Materials), by application (Chemical, Food Manufacturing, Aerospace, Automotive, Pharmaceutical, Pulp & Paper, Oil & Gas and Other Applications) and geography (North America, Europe, Asia Pacific, South America, and Middle East & Africa). The market size and forecasts are provided in terms of value (USD) for all the above segments.

| Single-Stage |

| Two-Stage |

| Cast Iron |

| Stainless Steel |

| Other Materials |

| Chemical |

| Food Manufacturing |

| Aerospace |

| Automotive |

| Pharmaceutical |

| Pulp and Paper |

| Oil and Gas |

| Other Applications |

| ?500 |

| 501-5,000 |

| 5,001-15,000 |

| >15,000 |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

| By Product Type | Single-Stage | ||

| Two-Stage | |||

| By Material | Cast Iron | ||

| Stainless Steel | |||

| Other Materials | |||

| By Application | Chemical | ||

| Food Manufacturing | |||

| Aerospace | |||

| Automotive | |||

| Pharmaceutical | |||

| Pulp and Paper | |||

| Oil and Gas | |||

| Other Applications | |||

| By Capacity Range | ?500 | ||

| 501-5,000 | |||

| 5,001-15,000 | |||

| >15,000 | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Southeast Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What was the value of the liquid ring vacuum pump market in 2026?

The market was valued at USD 1.85 billion in 2026.

Which application segment is expanding fastest?

Pharmaceutical manufacturing is growing at an 7.66% CAGR through 2031 as producers adopt solvent-recovery vacuum systems.

Why do Asia-Pacific countries dominate demand?

Aggressive chemical capacity additions in China and specialty-chemical growth in India require robust vacuum solutions, giving the region 43.00% market share in 2025.

Are energy-efficiency regulations a major threat?

Yes, in energy-regulated markets liquid ring pumps face a 30% power-consumption penalty versus dry screw units, curbing uptake in light-duty cycles.

Which capacity range sells the most units?

Mid-scale models rated 501–5,000 m³/h hold 38.90% share because they meet typical process-unit requirements while offering cost balance.

How are suppliers addressing water-scarcity concerns?

Leading OEMs now offer closed-loop seal-water systems that cut usage by up to 90%, allowing continued pump deployment in high-tariff regions.

Page last updated on: