Multi-Stage Centrifugal Pumps Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

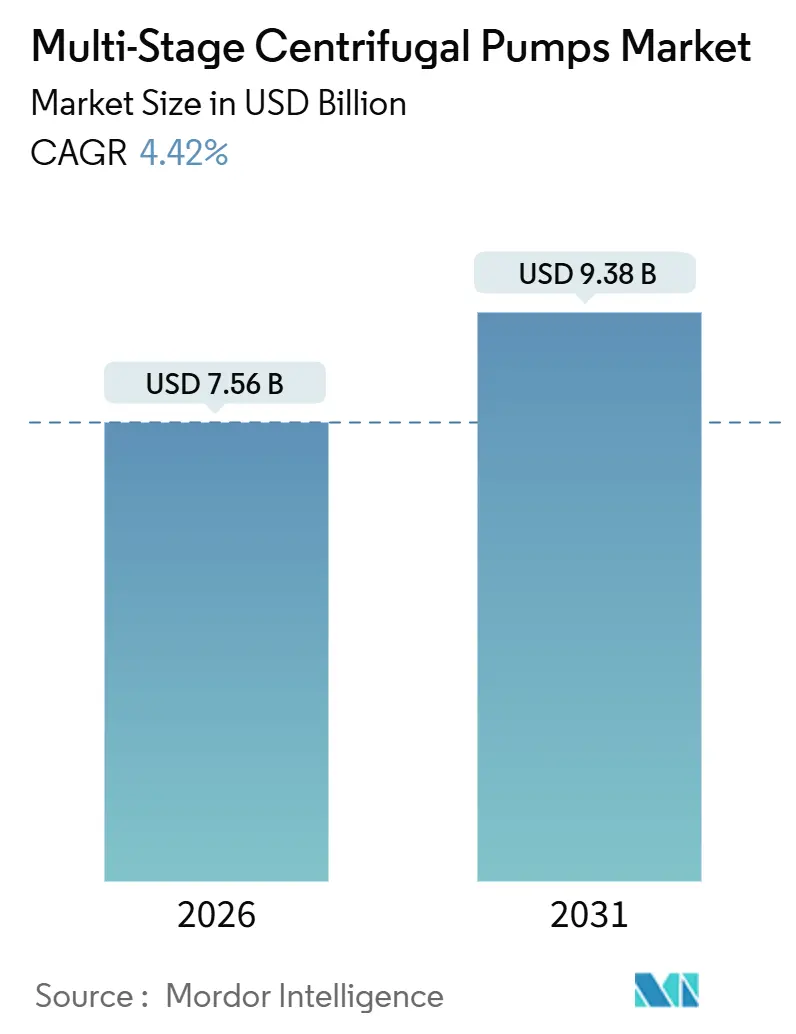

| Market Size (2026) | USD 7.56 Billion |

| Market Size (2031) | USD 9.38 Billion |

| Growth Rate (2026 - 2031) | 4.42% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

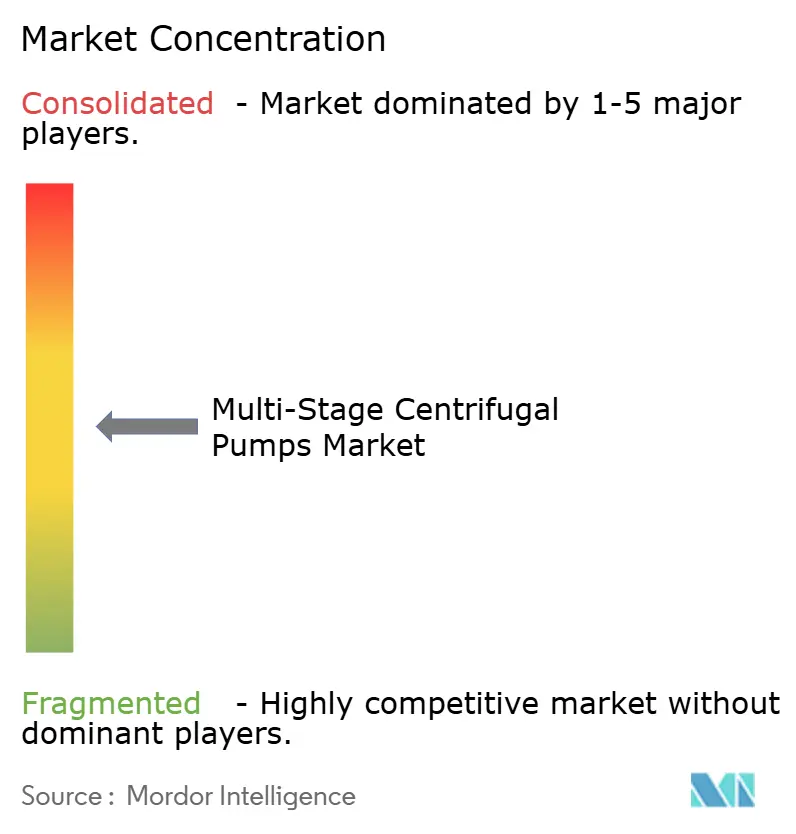

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Multi-Stage Centrifugal Pumps Market Analysis by Mordor Intelligence

The multi-stage centrifugal pumps market size reached USD 7.56 billion in 2026 and is projected to climb to USD 9.38 billion by 2031, translating into a 4.42% CAGR through the forecast period. Rising investment in water infrastructure, the build-out of large-scale desalination capacity, and rapidly tightening energy-efficiency codes are the core growth catalysts. Demand is further reinforced by deep-well oilfield activity that favors high-head pumping along with government incentives that underwrite solar-powered irrigation systems. Suppliers are simultaneously reshaping product portfolios around duplex steels and IIoT-enabled service models, moves that temper margin pressure from raw-material volatility and price-led Asian competition. As these themes converge, the multi-stage centrifugal pumps market is likely to maintain a balanced mix of replacement and green-field demand across public utilities, energy, and process industries.

Key Report Takeaways

- By type, horizontal pumps held 61.0% of the multi-stage centrifugal pumps market share in 2025, whereas vertical pumps are forecast to record the fastest 5.45% CAGR through 2031.

- By stage count, the 2-5 stage category commanded 45.2% share of the multi-stage centrifugal pumps market size in 2025 while above-10-stage units are set to expand at 5.21% CAGR between 2026-2031.

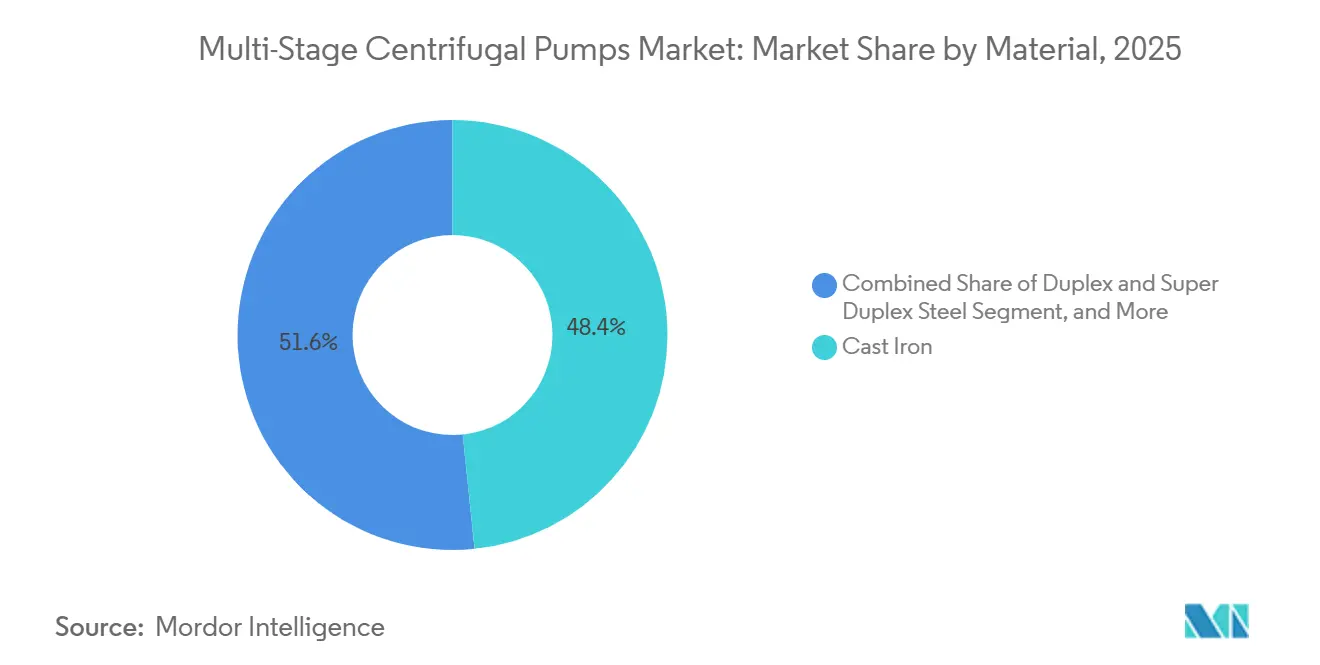

- By material, cast iron captured 48.3% share in 2025 but duplex and super duplex steels will post the highest 5.89% CAGR across 2026-2031.

- By end-user, water and wastewater systems contributed 32.4% revenue in 2025, whereas desalination plants are projected to advance at a 4.99% CAGR to 2031.

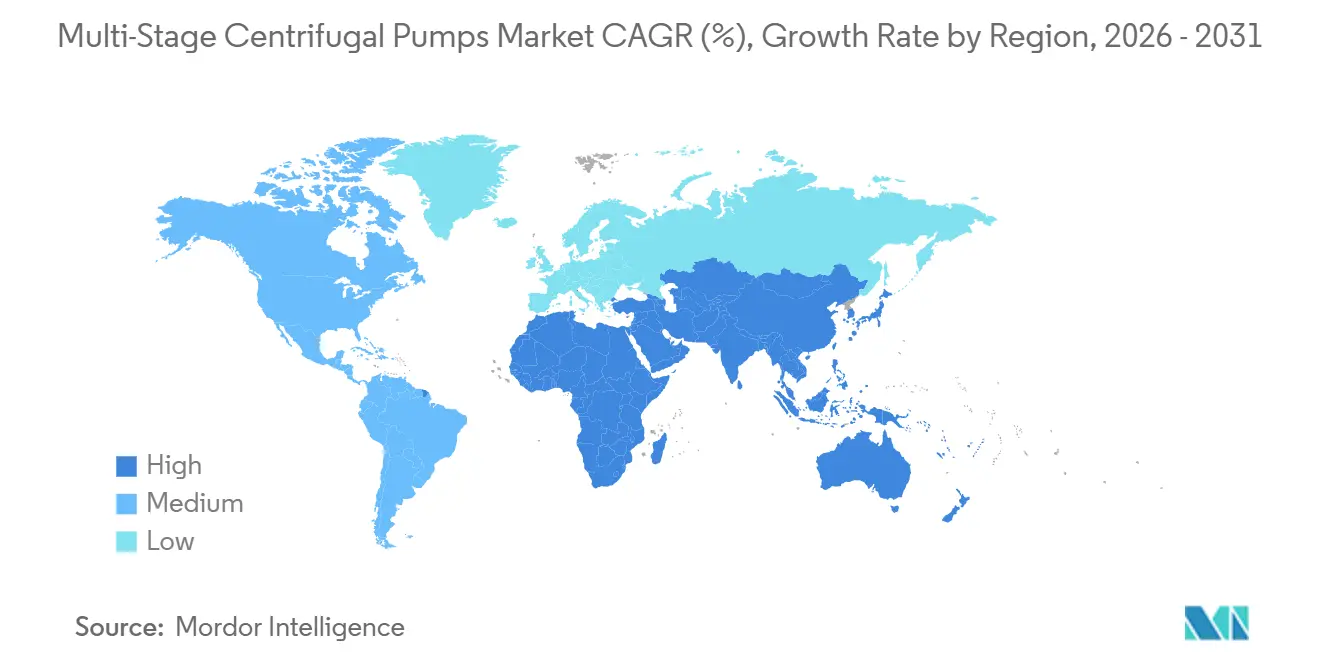

- By geography, Asia Pacific led with 36.7% share in 2025 and the Middle East is expected to grow the quickest at 5.62% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Multi-Stage Centrifugal Pumps Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Water and Wastewater Infrastructure Spending in North America and Europe | +0.70% | North America and Europe, with spillover to Latin America | Medium term (2-4 years) |

| Expansion of Desalination Projects in Water-Scarce Economies | +0.80% | Middle East core, North Africa, and Australia | Long term (≥ 4 years) |

| Increasing Deep-Well Oilfield Projects Requiring High-Head Pumping | +0.50% | Middle East, North America (shale basins), Russia | Medium term (2-4 years) |

| Shift Toward Energy-Efficient Pump Designs Driven by ESG Targets | +0.60% | Global, with early adoption in Europe and North America | Short term (≤ 2 years) |

| Integration of IIoT-Enabled Predictive Maintenance Platforms | +0.40% | Global, led by Europe and North America industrial clusters | Short term (≤ 2 years) |

| Growing Government Subsidies for Rural Irrigation in Asia Pacific | +0.50% | Asia Pacific core (India, China, Southeast Asia) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Water and Wastewater Infrastructure Spending

Public funding for pipe replacement and treatment upgrades is translating directly into demand for pressure-boosting multi-stage units. The United States Bipartisan Infrastructure Law earmarked USD 55 billion for water networks, and over 40% of municipal pumps in the country have surpassed 30-year service life. Similar momentum in Europe is led by Germany’s EUR 2.5 billion (USD 2.67 billion) municipal program and supportive financing from the European Investment Bank.[1]European Investment Bank, “Water Infrastructure Projects,” eib.org Compliance with new U.S. Department of Energy energy-index thresholds that took effect in 2025 is accelerating the swap-out of inefficient single-stage equipment. Together, these dynamics underpin the largest installed-base refresh ever seen in the segment, favoring horizontal configurations that simplify maintenance procedures.

Expansion of Desalination Projects in Water-Scarce Economies

Committed capital topping USD 100 billion across the Gulf Cooperation Council has catalyzed a wave of orders for high-pressure multi-stage pumps capable of operating at 60-80 bar.[2]Public Investment Fund, “Desalination Investments,” pif.gov.sa Flagship sites such as Yanbu 4 and Shuaibah 3 in Saudi Arabia each specify more than a dozen 14-stage duplex-steel models. Outside the Gulf, Egypt’s Abu Qir plant and the United Arab Emirates’ Hassyan project are adopting energy-recovery devices that cut pump power draw by a third. The material mix is shifting accordingly, with duplex and super duplex steels displacing 316L stainless steel as chloride-induced corrosion limits rise.

Increasing Deep-Well Oilfield Projects Requiring High-Head Pumping

Saudi Aramco’s Marjan and Berri expansions, the Vostok Oil megaproject in Siberia, and a rebound in shale completions across the Permian Basin are lifting shipments of above-10-stage pumps rated beyond 4,000 psi.[3]Baker Hughes, “Q4 2025 Earnings Call Transcript,” bakerhughes.com Enhanced oil recovery schemes, such as polymer flooding and CO₂ injection, demand corrosion-resistant metallurgy certified to API 610 11th edition, allowing suppliers such as ANDRITZ to gain share with duplex-steel offerings. Upstream capital outlays directed to artificial-lift systems reached USD 115 billion in 2026 and remain on an upward curve.

Shift Toward Energy-Efficient Pump Designs Driven by ESG Targets

Regulatory pressure, exemplified by Europe’s Ecodesign Directive 2025 motor mandate, is forcing end users to adopt variable-speed drives and permanent-magnet motors. Sulzer’s Energy Optimization Service trims operating power by up to 25% and pays back in under 18 months. Xylem’s e-Series multi-stage line achieves 89% wire-to-water efficiency, and corporate purchasers link such upgrades to corporate Scope 3 commitments. Energy savings translate into a lower lifetime cost of ownership, sustaining the multi-stage centrifugal pumps market even where project capital is constrained.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Raw Material Prices Raising Capex for OEMs | -0.60% | Global, with acute pressure in Asia Pacific manufacturing hubs | Short term (≤ 2 years) |

| Intensifying Competition from Low-Cost Regional Manufacturers | -0.50% | Asia Pacific and Middle East, with spillover to Africa | Medium term (2-4 years) |

| Lengthy Certification Cycles in Nuclear and Power Applications | -0.30% | North America, Europe, China (nuclear-expansion markets) | Long term (≥ 4 years) |

| Rising Adoption of Alternative Positive-Displacement Pump Technologies | -0.40% | Global, concentrated in chemical and food-processing sectors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Raw-Material Prices Raising Capex for OEMs

Nickel and chromium price spikes in 2025 lifted duplex-steel input costs by double digits, squeezing gross margins at suppliers locked into multi-year municipal contracts. Flowserve cited a 220-basis-point margin contraction in 2025 as it struggled to pass through higher alloy surcharges. Currency swings exacerbate planning risk, especially for European OEMs purchasing Asian forgings in U.S. dollars. Some manufacturers now hedge by bulk-buying stainless-steel castings and diversifying supplier bases, yet sustained volatility still weighs on near-term profitability.

Intensifying Competition from Low-Cost Regional Manufacturers

Chinese and Indian producers have captured 12% of Southeast Asian sales by underpricing established brands 20-25% on standard cast-iron units. Quality differentials are narrowing; ISO 9906 Grade 2B pumps from new entrants posted failure rates within 8% of European equivalents in a 5-year field study. Incumbents answer with local assembly plants and extended warranty schemes, but such moves pare back premium pricing, placing a ceiling on average selling prices within the multi-stage centrifugal pumps market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type - Vertical Pumps Gain Ground in Space-Constrained Installations

The vertical subsegment is projected to grow at 5.45% CAGR, a pace that outstrips the overall multi-stage centrifugal pumps market by more than 100 basis points. Horizontal models maintain a 61.0% multi-stage centrifugal pumps market share on the strength of lower installation expense in water treatment and industrial cooling duty. However, high-rise construction and offshore platform projects prioritize compact footprints, tipping procurement toward vertical stacks equipped with integrated drives. Wilo’s Helix EXCEL line, introduced in 2025, saves 40% floor space relative to comparable horizontals, a decisive advantage in premium urban basements. Offshore wells reinforce the same preference; modular vertical assemblies fit 9-inch casings and can descend beyond 3,500 meters to lift fluids in Saudi Aramco’s Marjan field. As end users shift to predictive maintenance, vibration sensors mounted on vertical axes offer cleaner data streams, supporting analytics platforms without costly retrofits.

Horizontal units will continue to dominate power-generation cooling circuits where inline layouts simplify turbine-driven back-up arrangements. Many public utilities own existing spare parts inventories geared toward horizontal pumps, tempering the conversion rate. Nevertheless, the steady rollout of high-density commercial towers in Asia and the Middle East will ensure that vertical solutions steadily erode horizontal share, particularly where building regulations cap mechanical-room footprints. Suppliers that deliver plug-and-play vertical skids with IE4 motors and cloud-ready controllers are positioned to outpace the broader multi-stage centrifugal pumps market.

By Stage - Ultra-High-Head Projects Boost Above-10-Stage Demand

Units carrying 2-5 impellers represented 45.2% of the multi-stage centrifugal pumps market size in 2025, but above-10-stage machines will advance at a 5.21% CAGR through 2031 as desalination, carbon-capture, and deep-reservoir oil lifts proliferate. Saudi Arabia’s Yanbu 4 plant employs 14-stage pumps rated at 75 bar to offset the osmotic pressure of 45,000 ppm seawater, illustrating how multi-stage counts rise in tandem with salinity and head height. Similarly, Norway’s Northern Lights carbon-capture system compresses liquefied CO₂ to 150 bar using 16-stage compressors, a template for future sequestration hubs.

Mid-range 6-10 stage pumps remain workhorses in boiler feedwater and chemical processing, where balanced capital and operating costs matter more than peak discharge pressure. Yet each additional impeller adds mechanical complexity, so OEMs deploy ceramic-coated wear rings and thrust-balancing designs to sustain mean time between overhaul. Digital twins created during computational-fluid-dynamics simulations now predict internal recirculation patterns, enabling OEMs to fine-tune stage counts before casting billets, an emerging efficiency lever within the multi-stage centrifugal pumps market.

By Material - Duplex Steels Capture Share in Offshore and Desalination Duty

Cast iron continues to dominate on unit volume, holding 48.3% share in 2025 thanks to a cost basis near USD 1,200 per metric ton. In contrast, duplex and super duplex steels, running USD 4,500-6,000 per ton, are gaining at a 5.89% CAGR wherever chloride-rich brines or sour hydrocarbons accelerate corrosion. Middle East operators cite 25-year life cycles for duplex-steel pumps certified to NORSOK M-001, a decisive economic argument for offshore platforms that face million-dollar day rates should pumps fail.

Stainless 316L maintains relevance in food, beverage, and pharmaceutical lines that must meet 3-A and ASME BPE-2024 hygienic criteria. Here, electropolished internals and sub-0.8 µm surface roughness are mandatory, and suppliers lead with documentation packages suited for validation audits. Titanium remains a niche solution in coastal power-plant condensers, and nickel alloys appear in acid-handling service, but both lag duplex steels on cost effectiveness. Lifecycle studies published in 2025 affirm that duplex units deliver 40% lower total cost of ownership than 316L in high-salinity duty, evidence that will likely accelerate further material migration across the multi-stage centrifugal pumps market.

By End-User Industry - Desalination Sets the Growth Pace

Municipal water and wastewater treatment contributed 32.4% of revenue in 2025, anchored by funding lines in the United States and Europe that prioritize replacement of aged equipment. Desalination, however, represents the fastest climb, projected at 4.99% CAGR into 2031. The Gulf pipeline alone amounts to USD 100 billion in projects at varying stages of execution, each specifying dozens of high-pressure pumps operating above 60 bar. Outside the Middle East, Egypt, Iraq, and Australia are lining up megaprojects that replicate this capital pattern.

Oil and gas remains structurally important, stimulated by 14% year-on-year growth in electric submersible pump shipments during 2025. Chemical and pharmaceutical processing favor hygienic stainless-steel constructions, while food and beverage lines reward clean-in-place designs that slash sanitation downtime. Power generation’s shift toward flexible turbine load-following, prompted by renewable integration, is catalyzing orders for variable-speed multi-stage feeder pumps. Metals and mining outfits value abrasion-resistant white-iron internals, adopting pumps that extend run-time in tailings and dewatering loops. Collectively, these patterns diversify revenue streams and moderate cyclicality within the multi-stage centrifugal pumps market.

Geography Analysis

Asia Pacific accounted for 36.7% of global revenue in 2025, buoyed by China’s CNY 5.4 trillion (USD 740 billion) rural water program and India’s Jal Jeevan Mission that linked 148 million homes to piped networks by December 2025. Government subsidies under India’s PM-KUSUM scheme funded 180,000 solar-powered agricultural pumps, spotlighting a sizeable off-grid niche. Japan’s Ministry of Health, Labour and Welfare earmarked JPY 1.2 trillion (USD 8.1 billion) to replace aging mains, implying elevated demand for small and mid-size units through 2028. Southeast Asian irrigation projects in Vietnam and Indonesia round out the region’s near-term pipeline. Local manufacturers enjoy cost advantages, yet global brands preserve share in high-specification builds that require third-party certification.

The Middle East is forecast to register the fastest 5.62% CAGR across 2026-2031 as desalination and nuclear power construction drive high-pressure pump procurement. Saudi Arabia’s Yanbu 4 and Shuaibah 3 plants, Qatar’s Facility E, and the UAE’s Hassyan project headline a dense order book for duplex-steel multistage units. Turkey’s Akkuyu nuclear complex adds another 96 primary and secondary cooling pumps to regional demand. Financing from sovereign wealth funds and development banks mitigates commodity-price volatility, ensuring a steady tender cadence.

North America and Europe together represented 38% of 2025 turnovers, with sales propelled by lifecycle-driven replacements mandated by new energy-efficiency standards. The U.S. Department of Energy rules effective January 2025 and Europe’s IE4 motor stipulations effective 2027 advance variable-speed multi-stage adoption. Latin America’s expansion concentrates in Brazil and Argentina where irrigation and mining hold sway, whereas Africa’s outlook is shaped by South Africa’s Lesotho Highlands Water Project Phase II and Kenya’s solar-pump irrigation program. Despite divergent baselines, all regions converge on a common requirement for higher efficiency and lower unplanned downtime, hallmarks of modern multi-stage centrifugal pumps market offerings.

Competitive Landscape

The multi-stage centrifugal pumps market displays moderate concentration. The top five brands control an estimated 35% of revenue, leaving substantial latitude for regional challengers. Global leaders deepen resilience by shifting toward service-recurring business models. Grundfos Machine Health, launched in 2025, bundles vibration analytics and edge gateways on a subscription, delivering 30% downtime cuts for early adopters. Sulzer’s Energy Optimization Service and Xylem’s cloud collaboration with Amazon Web Services similarly convert one-time hardware sales into annuity cash flows.

Localization remains a second pillar. Grundfos’ USD 60 million plant in Coimbatore leverages domestic castings and motors to trim landed costs by 15%. Flowserve opened a pump-overhaul center in Saudi Arabia’s Jubail industrial zone, positioning for nitrogen, hydrogen, and desalination retrofits. Mergers augment aftermarket reach; Sulzer’s Denmark acquisition added 120 technicians and a northern European fleet of service vans.

Disruption is evident at the low end of the price curve. Leo Group and Shimge push cast-iron multi-stage units into Southeast Asia at discounts topping 20%. Kirloskar Brothers and Shakti Pumps target Africa with solar-powered solutions that bypass weak grids, carving out niches beyond the economic reach of Western incumbents. Technology differentiation narrows as Chinese firms file impeller and wear-ring patents and certify to ISO 9906 Grade 2B tolerances. In response, incumbents emphasize nuclear-qualified and API 610-compliant lines where certification hurdles remain high, sustaining their price premium in critical-service applications.

Multi-Stage Centrifugal Pumps Industry Leaders

Kirloskar Brothers Limited

Baker Hughes Company

Circor International Inc.

Ebara Corporation

The Weir Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Grundfos started series production at its USD 60 million Coimbatore, India facility, lifting annual capacity to 500,000 multi-stage pumps.

- September 2025: Weir Group booked a USD 95 million order for 80 polymer-flooding pumps destined for China’s Daqing field, with deliveries running through mid-2027.

- September 2025: Qatar’s Facility E desalination plant commenced operations using 48 Sulzer high-pressure pumps rated 75 bar.

- August 2025: Shakti Pumps secured a USD 45 million contract to supply 12,000 solar multi-stage units for Kenya’s Tana River irrigation scheme.

Global Multi-Stage Centrifugal Pumps Market Report Scope

The market is defined by the revenue generated by selling multi-stage centrifugal pumps offered by market vendors designed to be adopted by end-user industries worldwide.

The multi-stage centrifugal pumps market is segmented by type (horizontal pumps and vertical pumps), by end-user industry (oil & gas, chemicals, food & beverage, water & wastewater, pharmaceutical, power generation, metal & mining, other end-user industries), and geography (North America, Europe, Asia Pacific, Latin America, Middle East and Africa). The report offers market forecasts and size in value (USD) for all the above segments.

The Multi-Stage Centrifugal Pumps Market Report is Segmented by Type (Horizontal Pumps, Vertical Pumps), Stage (2-5 Stage, 6-10 Stage, Above 10 Stage), Material (Cast Iron, Stainless Steel, Duplex and Super Duplex Steel, Other Materials), End-User Industry (Oil and Gas, Chemicals, Food and Beverage, Water and Wastewater, Power Generation, Pharmaceuticals, Metals and Mining, Other End-User Industries), and Geography (North America, South America, Europe, Asia Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD), Based on Availability.

| Horizontal Pumps |

| Vertical Pumps |

| 2-5 Stage |

| 6-10 Stage |

| Above 10 Stage |

| Cast Iron |

| Stainless Steel |

| Duplex and Super Duplex Steel |

| Other Materials |

| Oil and Gas |

| Chemicals |

| Food and Beverage |

| Water and Wastewater |

| Power Generation |

| Pharmaceuticals |

| Metals and Mining |

| Other End-User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Type | Horizontal Pumps | |

| Vertical Pumps | ||

| By Stage | 2-5 Stage | |

| 6-10 Stage | ||

| Above 10 Stage | ||

| By Material | Cast Iron | |

| Stainless Steel | ||

| Duplex and Super Duplex Steel | ||

| Other Materials | ||

| By End-User Industry | Oil and Gas | |

| Chemicals | ||

| Food and Beverage | ||

| Water and Wastewater | ||

| Power Generation | ||

| Pharmaceuticals | ||

| Metals and Mining | ||

| Other End-User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the multi-stage centrifugal pumps market?

The market stood at USD 7.56 billion in 2026 and is projected to reach USD 9.38 billion by 2031.

Which type of pump dominates global sales?

Horizontal multi-stage pumps led with 61.0% share in 2025 due to ease of maintenance and lower installation costs.

Which region is growing the fastest?

The Middle East is set to post the quickest 5.62% CAGR on the back of large desalination and nuclear projects.

What material segment is gaining the most traction?

Duplex and super duplex steels are expanding at 5.89% CAGR as offshore and desalination operators prioritize corrosion resistance.

How are manufacturers improving pump reliability?

Leading OEMs embed IIoT sensors and predictive analytics, cutting unplanned downtime by up to 30% in pilot deployments.

What is driving the shift toward energy-efficient pumps?

Stricter U.S. Department of Energy and European Ecodesign regulations plus corporate ESG targets are pushing adoption of high-efficiency variable-speed systems.

Page last updated on: