Cell Banking Outsourcing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

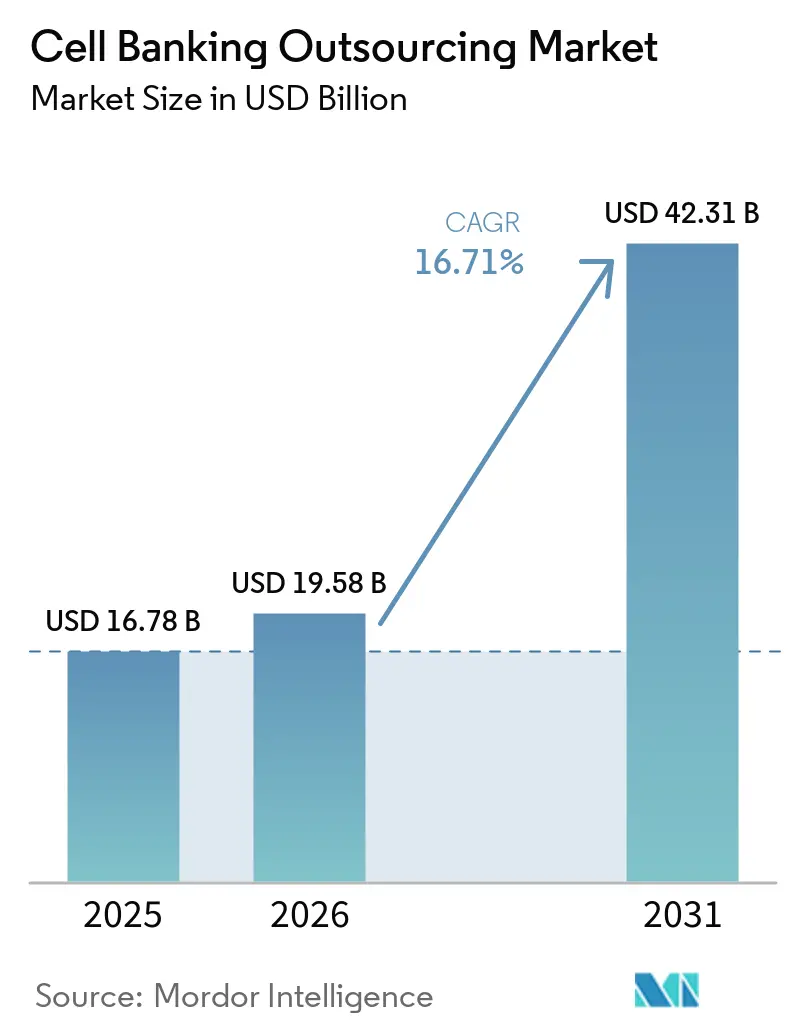

| Market Size (2026) | USD 19.58 Billion |

| Market Size (2031) | USD 42.31 Billion |

| Growth Rate (2026 - 2031) | 16.71% CAGR |

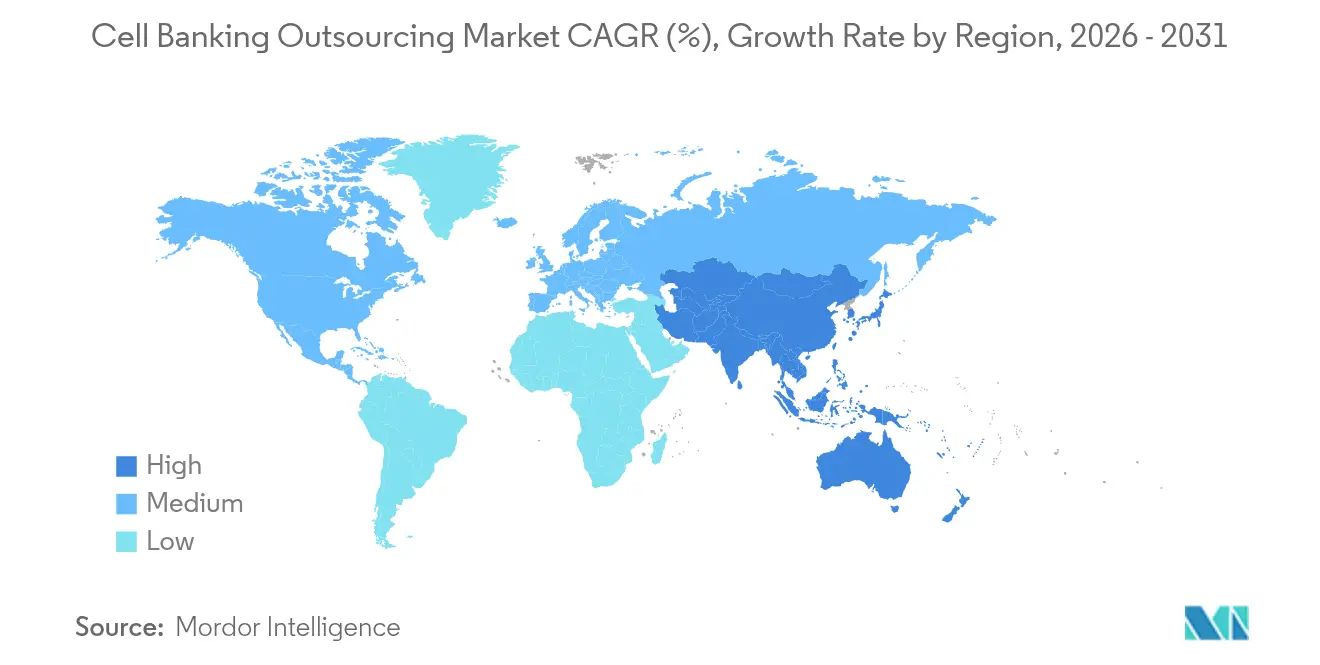

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cell Banking Outsourcing Market Analysis by Mordor Intelligence

The cell banking outsourcing market size is expected to grow from USD 16.78 billion in 2025 to USD 19.58 billion in 2026 and is forecast to reach USD 42.31 billion by 2031 at 16.71% CAGR over 2026-2031. Robust demand for compliant master, working and viral banks underpins this expansion, as biopharma companies accelerate cell and gene therapy pipelines that already include more than 2,500 active U.S. investigational new drug applications. Regulatory authorities in North America and Europe tighten good manufacturing practice (GMP) requirements, steering sponsors toward specialist partners that already operate validated, high-capacity facilities. Stem-cell banking adoption rises sharply in Asia-Pacific, while automated cryogenic logistics and AI-driven quality control lower error rates and shorten release timelines. Capital deployment by global contract development and manufacturing organizations (CDMOs) remains intense, with single-site expansions exceeding USD 1 billion, signaling strategic bets on sustained double-digit growth.

Key Report Takeaways

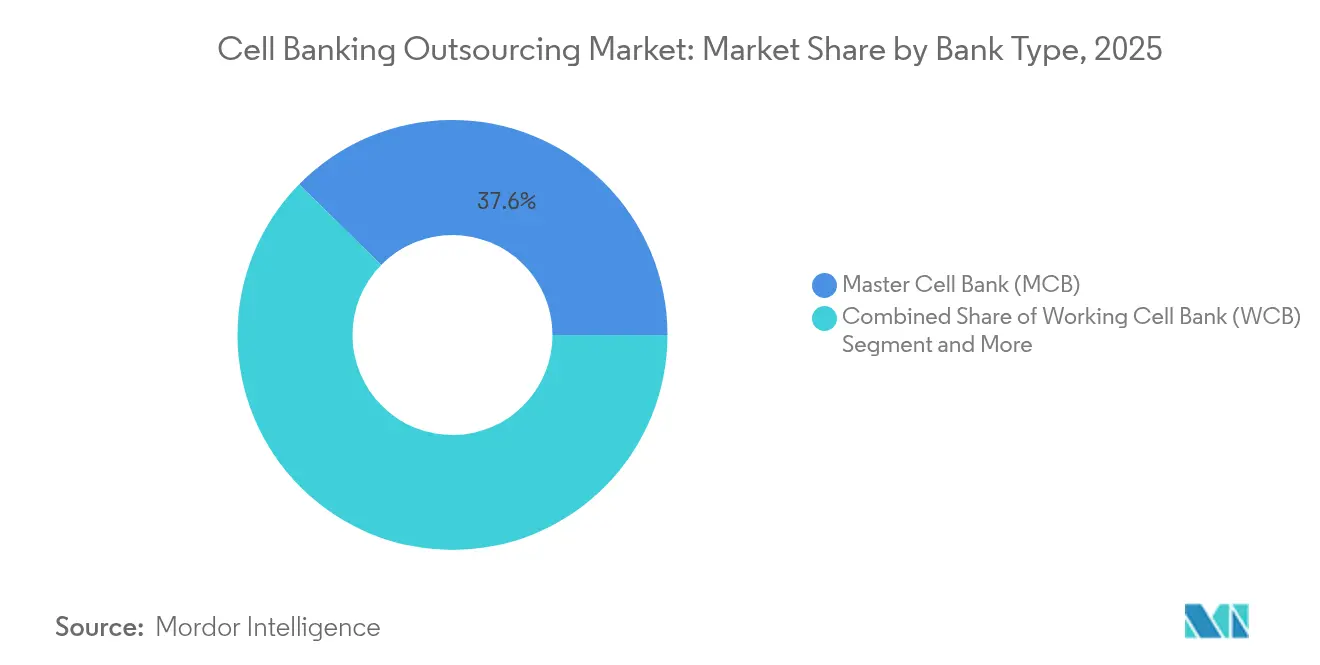

- By bank type, master cell banks held 37.64% of the cell banking outsourcing market share in 2025, while viral cell banks are projected to expand at a 17.52% CAGR through 2031.

- By cell type, stem-cell banking captured 60.12% of the cell banking outsourcing market size in 2025, and induced pluripotent stem cells (iPSCs) are set to advance at a 18.76% CAGR over the forecast period.

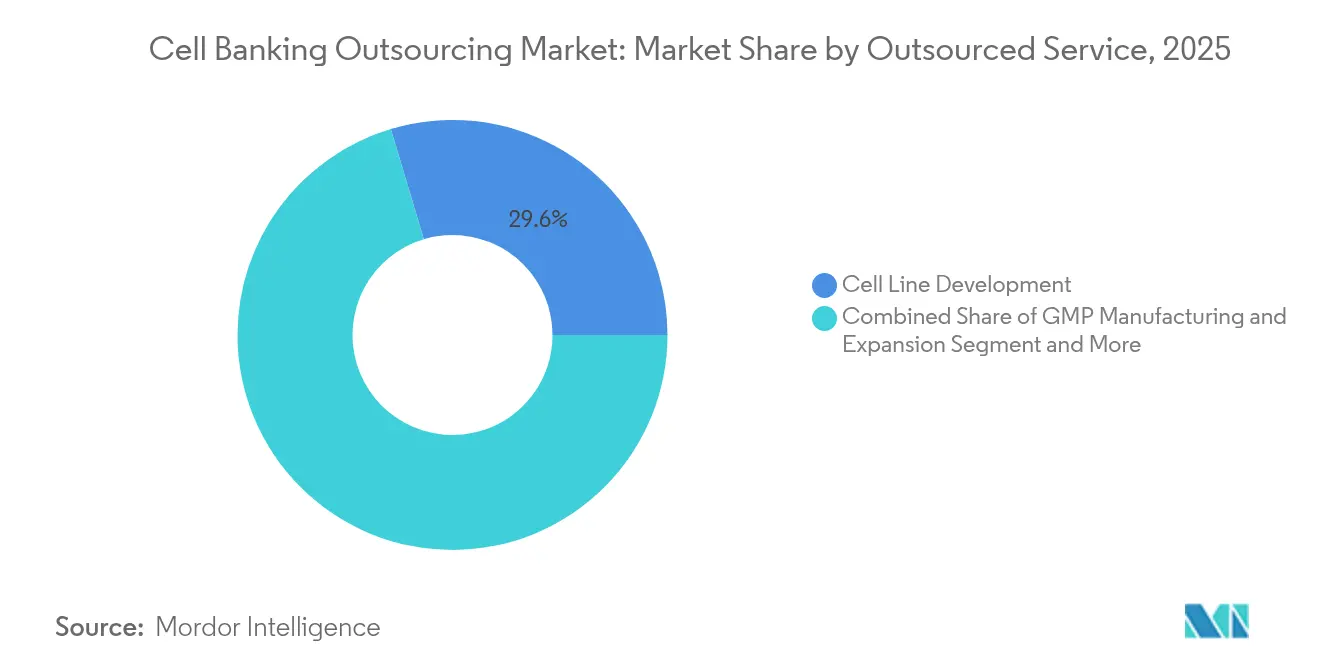

- By outsourced service, cell line development led with 29.63% share of the cell banking outsourcing market size in 2025; logistics and cold-chain management is the fastest-growing service at an 17.44% CAGR.

- By end user, biopharma and biotech companies commanded 51.10% share of the cell banking outsourcing market in 2025, whereas contract research organizations (CROs) register the highest projected CAGR at 17.12% to 2031.

- By geography, North America accounted for 45.25% of the cell banking outsourcing market in 2025, and Asia-Pacific is expanding at an 17.38% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cell Banking Outsourcing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge In Cell & Gene Therapy Pipelines | +3.2% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| Rising Adoption Of Stem Cell Banking | +2.8% | APAC core, spill-over to North America | Long term (≥ 4 years) |

| Increasing Chronic Disease Burden | +2.1% | Global | Long term (≥ 4 years) |

| Regulatory Push For GMP Compliance | +2.5% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| AI-Driven Cell Line Authentication Gains | +1.8% | Global, early adoption in North America | Medium term (2-4 years) |

| Decentralized Clinical-Trial Micro-Banks | +1.4% | North America & EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Cell & Gene Therapy Pipelines

Global investigational activity fuels the cell banking outsourcing market, with the U.S. FDA monitoring more than 2,500 active INDs and preparing for 10-20 novel approvals each year from 2025 onward[1]Cell & Gene, “Cell & Gene Therapies: Will 2025 Represent a Continuation of FDA’s 2024 Developments?” cellandgene.com. Every cell- or gene-based therapeutic requires multiple tiered banks—master, working and viral—driving multi-cycle demand. Allogeneic CAR-T and natural killer platforms magnify the requirement because single donor cells treat numerous patients, necessitating larger, more rigorously characterized banks. Late-stage portfolios are expanding: WuXi Biologics disclosed 51 Phase III programs in 2023, nearly double 2022 levels, and most rely on external banking capacity. Distributed manufacturing nodes outlined in recent FDA draft guidance also require parallel micro-banks at several qualified sites. Manufacturing costs exceeding USD 2.1 million per dose for first-generation CAR-T products highlight the economic incentive to outsource banking and amortize fixed costs.

Rising Adoption of Stem-Cell Banking

Asia-Pacific leads growth as clinical use of cord blood climbs from 30,000 procedures in 2023 to nearly 40,000 in 2024, accompanied by 99% survival in thalassemia treatments. Automated cryopreservation systems deliver consistent cooling rates, improving post-thaw viability and lowering storage failures. Induced pluripotent stem cells circumvent embryonic-cell ethics while retaining pluripotency, making them a preferred option for disease modeling and autologous therapies. Hybrid public-private banks in China and South Korea broaden access while generating revenue streams that sustain large-scale repositories. Next-generation sequencing panels offered by Charles River Laboratories detect latent viral contamination faster than legacy assays, enhancing regulatory confidence.

Regulatory Push for GMP Compliance

Both the European Commission and the U.S. FDA issued updated GMP guidelines in 2024, tightening release specifications, expanding Qualified Person oversight, and codifying risk-based viral testing. Smaller sponsors struggle to finance compliant suites, as single-site builds can reach USD 200 million and require 24-36 months before licensure. Outsourced providers spread those costs across diversified client portfolios, lowering per-project expenditure. Harmonized initiatives such as CoGenT Global encourage dual submissions to multiple authorities, advantaging service partners with multinational footprints. Post-marketing surveillance obligations—88% of EU-approved cell therapies carry additional monitoring—extend the need for long-term GMP storage that specialist banks are optimized to deliver.

AI-Driven Cell-Line Authentication Gains

Convolutional-neural-network image analytics now distinguish pluripotent stem cells from differentiated progeny with accuracy exceeding 95%, reducing labor-intensive manual review. Machine-learning algorithms analyze next-generation sequencing data to flag genomic instability or viral sequences within hours. Providers investing in high-performance computing pools amortize those assets across hundreds of projects, offering turnaround cycles of seven days versus industry averages of three weeks. Blockchain-backed audit trails enhance data integrity, satisfying regulators focused on immutable chain-of-custody documentation. Sponsors benefit from faster lot-release decisions and lower remediation risk.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost Of GMP-Compliant Services | -2.3% | Global, particularly impacting smaller biotech companies | Short term (≤ 2 years) |

| Ethical & Legal Issues Around Embryonic Cells | -1.8% | Variable by jurisdiction, most restrictive in conservative regions | Long term (≥ 4 years) |

| Cryogenic Logistics Capacity Crunch | -1.5% | Global, acute in emerging markets | Medium term (2-4 years) |

| Energy-Efficiency Mandates For ULT Storage | -1.2% | North America & EU, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of GMP-Compliant Services

Building and validating a modern cell-banking suite can exceed USD 200 million, as illustrated by Fujifilm’s 2024 North Carolina expansion that added eight 20,000-liter bioreactors and extensive storage vaults. Service pricing often represents 15-25% of total therapy development budgets, challenging seed-stage ventures. Charles River Laboratories reported revenue headwinds in early 2025 after a client withdrew a commercial contract, highlighting the sensitivity of project flow to cost escalation. Surge demand compresses available slots, giving incumbent providers pricing leverage. Long-term contracts partially offset fixed outlays, yet up-front capital remains a deterrent for new entrants.

Ethical & Legal Issues Around Embryonic Cells

Jurisdictional differences over embryonic-stem-cell research rights complicate global supply strategies. Nations such as Germany impose restrictive consent frameworks, whereas the United Kingdom allows broader use under Human Fertilisation and Embryology Authority oversight. Japan adopted distinct rules in 2025 for embryo-model research, requiring case-by-case review that can extend project timelines. Sponsors therefore pivot toward iPSC or adult-stem-cell platforms to avoid legal gray areas. Banks holding mixed inventories must maintain segregated storage and documentation, raising overhead. Public perception debates also influence funding streams, creating long-range uncertainty for embryonic-cell portfolios[2]Voices in Bioethics, “Cultural Relativity and Acceptance of Embryonic Stem Cell Research,” voicesinbioethics.org.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Bank Type: Viral Banks Drive Next-Generation Therapies

Master cell banks accounted for 37.64% of the cell banking outsourcing market in 2025 as they establish the genetic blueprint for all downstream operations. Viral cell banks, though smaller today, register an 17.52% CAGR through 2031, propelled by CAR-T, oncolytic virus and gene-editing modalities that rely on high-titer vectors. The cell banking outsourcing market size for viral banks is projected to surpass USD 9.2 billion by 2031, reflecting heightened biosafety and sequencing requirements. Outsourced partners deploy BSL-2+/BSL-3 suites, barrier isolators and closed-system bioreactors that minimize cross-contamination risk while scaling yield. Stringent replication-competent virus assays align with evolving FDA guidance, favoring vendors already equipped with quantitative PCR and digital droplet platforms.

Rapid commercialization of virotherapy programs intensifies demand for expedited master and working viral banks. Providers that bundle analytical development, plasmid supply and cryogenic warehousing achieve higher utilization rates and recurring revenue. Smaller sponsors opt for subscription-style agreements that lock-in capacity through licensure, shielding projects from future slot scarcity. These dynamics reinforce the cell banking outsourcing market’s shift toward full-service CDMOs with dedicated viral-bank centers.

By Cell Type: iPSCs Reshape Stem-Cell Banking

Stem-cell repositories controlled 60.12% of overall revenue in 2025, with cord blood, tissue-derived and embryonic lines serving regenerative and immuno-oncology pipelines. Induced pluripotent stem cells log the fastest trajectory at 18.76% CAGR, benefitting from patent expirations that lower licensing fees and from protocols that skip oncogenic integration. The cell banking outsourcing market share for iPSC inventories is expected to cross 16.15% by 2031, up from 7.3% in 2025.

Capital-heavy players such as Fujifilm allocate more than USD 200 million to expand iPSC GMP suites in Wisconsin, adding closed automated thaw-wash-fill systems that prevent operator contact. AI-powered imaging now scores colonies for pluripotency markers in real time, boosting batch acceptance rates. Public-private hybrid banks in China guarantee long-term storage funding through state subsidies while opening fee-for-service tiers to industry users. These structures stabilize cash flow and anchor regional manufacturing clusters.

By Outsourced Service: Logistics Solutions Gain Momentum

Cell line development services remained the single largest revenue source at 29.63% in 2025, as each therapeutic candidate requires a stable, high-yielding line before scaling to clinical or commercial lots. Yet logistics and cold-chain management services post an 17.44% CAGR to 2031, reflecting clinical adoption of autologous and allogeneic living therapies that cannot tolerate temperature excursions. The cell banking outsourcing market size tied to logistics is set to reach USD 6.95 billion by 2031, doubling its 2025 baseline.

IoT-enabled shippers with real-time telemetry track internal dew-point humidity and nitrogen levels, transmitting alerts that trigger contingency routing. Cryoport’s support for 675 clinical trials demonstrates how focused logistics specialists capture share by combining asset-light fleets with proprietary monitoring software. Regulatory agencies now request lane-qualification data during biologics license application review, elevating the strategic value of validated couriers. Consequently, CDMOs integrate in-house dispatch centers or form exclusive partnerships to secure capacity during peak enrollment periods.

By End User: CROs Accelerate Outsourcing Adoption

Biopharma and biotechnology companies represented 51.10% of total demand in 2025, reflecting direct control of therapeutic pipelines and budget authority. CROs, however, show the sharpest upswing at 17.12% CAGR because sponsors shift tactical activities—such as cell bank characterization, stability and release testing—into bundled Phase I-III packages. The cell banking outsourcing market share managed by CROs may reach 20.6% by 2031 from 13.5% in 2025.

BioPlan Associates’ 2024 manufacturing survey found 68% of responding companies expect to increase outsourcing levels within five years, citing specialized analytical expertise and capital avoidance. CROs secure multi-year framework agreements with top CDMOs, negotiating discounted slots and co-marketing bespoke assay panels. This aggregation effect unlocks pricing power and accelerates project timelines, reinforcing the business case for end-to-end outsourced models.

Geography Analysis

North America accounted for 45.25% of the cell banking outsourcing market in 2025, underpinned by FDA leadership in cell-therapy approvals, abundant venture funding and a dense cluster of GMP-qualified vaults. The United States drives regional momentum, hosting expansions by Charles River Laboratories, Thermo Fisher Scientific and Fujifilm that collectively add more than 4 million cryogenic vials of incremental capacity. Canada’s supportive incentives attract early-stage developers, while Mexico’s forthcoming NOM-260-SSA1 standard invites cross-border collaborations and creates new requests for bilingual documentation.

Europe commands approximately 29.15% market share, sustained by German, British and French pharmaceutical hubs. The European Medicines Agency’s post-marketing surveillance requirements necessitate long-term sample retention, creating annuity revenue for banks with EU tissue establishment licenses. Switzerland and the Netherlands strengthen their positions as import gateways by streamlining customs clearance for frozen biologics, reducing transit time and viability loss.

Asia-Pacific records the fastest CAGR at 17.38% through 2031. China leads absolute growth on the back of aggressive cord blood expansion and central-government grants supporting iPSC lines for rare-disease projects. Japan’s expedited Sakigake designation accelerates local approvals, growing demand for release testing and GMP storage under the Pharmaceuticals and Medical Devices Agency framework. India updates its national guidelines in 2025, emphasizing stricter donor screening and documentation, which favors international providers familiar with OECD-aligned practices. South Korea and Australia continue to leverage strong academic networks and rising clinical-trial counts, cementing the region’s strategic importance.

Competitive Landscape

The cell banking outsourcing industry displays moderate consolidation. Charles River Laboratories, Lonza and Thermo Fisher Scientific each operate global networks of GMP banks, high-throughput analytics labs and dedicated cryogenic logistics units. Their scale allows bundled master-to-commercial packages that appeal to sponsors seeking single-invoice simplicity. Fujifilm’s 2025 completion of its USD 1.2 billion Holly Springs facility adds the world’s largest end-to-end mammalian CDMO site, intensifying competition in North America.

Tier-two specialists differentiate through niche capabilities. Cryoport dominates nitrogen-based transport, reporting support for 675 active trials by end-2024, while ATCC invests National Institutes of Health grant funding to build a biomanufacturing suite in Virginia to supply authenticated cell lines. Automation-centric newcomers target high-volume banks for iPSC and gene-edited natural killer cells, integrating robotic liquid-handling and AI-enabled visual QC to lift throughput.

Strategic repositioning shapes the field: WuXi AppTec divested its Advanced Therapies unit to Altaris in late 2024 to focus on small-molecule services, while Thermo Fisher entered the cell-therapy CDMO arena through a New Jersey facility acquisition. Blockchain-anchored chain-of-custody platforms emerge as competitive levers, offering immutable data trails that simplify regulatory audits. Providers that align digital and physical infrastructure are well-positioned to capture share as living-drug commercialization scales.

Cell Banking Outsourcing Industry Leaders

Lonza Group

Charles River Laboratories

Wuxi AppTec

Merck KGaA

Cryo-Cell International

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Fujifilm Corporation inaugurated an additional USD 1.2 billion mammalian-cell CDMO campus in North Carolina, adding eight 20,000-liter bioreactors and 680 jobs, substantially expanding North American viral and master-bank capacity.

- February 2025: Charles River Laboratories signed a multi-year agreement with Singapore General Hospital to establish GMP master cell banks and next-generation-sequencing analytics for cord-blood–derived allogeneic CAR-T cells.

Global Cell Banking Outsourcing Market Report Scope

As per the scope of this report, a cell bank is a place where cells originating from various body fluids and organ tissue are stored for future use. Cells, cell lines, and tissues are collected, stored, characterized, and tested in the cell banking outsourcing sector. The Cell Banking Outsourcing Market is segmented by bank type (master cell banking, working cell banking, viral cell banking), cell type (stem cell banking (cord stem cell banking, embryonic stem cell banking, adult stem cell banking, dental stem cell banking, induced pluripotent stem cell banking), and non-stem cell banking), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report also covers the estimated market sizes and trends for 17 countries across major global regions. The report offers the value (USD) for the above segments.

| Master Cell Bank (MCB) |

| Working Cell Bank (WCB) |

| Viral Cell Bank (VCB) |

| Research & Development Cell Bank |

| End-of-Production Cell Bank |

| Stem Cell Banking |

| Cord Blood & Tissue Stem Cells |

| Embryonic Stem Cells |

| Adult Stem Cells |

| Dental Pulp Stem Cells |

| Induced Pluripotent Stem Cells |

| Non-stem Cell Banking |

| Microbial Cell Banking |

| Mammalian Cell Banking |

| Hybridoma Cell Banking |

| Cell Line Development |

| Characterization & Testing |

| GMP Manufacturing & Expansion |

| Cryopreservation & Storage |

| Logistics & Cold Chain Management |

| Biopharma & Biotech Companies |

| Academic & Research Institutes |

| Contract Research Organizations |

| Hospitals & Transplant Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Bank Type | Master Cell Bank (MCB) | |

| Working Cell Bank (WCB) | ||

| Viral Cell Bank (VCB) | ||

| Research & Development Cell Bank | ||

| End-of-Production Cell Bank | ||

| By Cell Type | Stem Cell Banking | |

| Cord Blood & Tissue Stem Cells | ||

| Embryonic Stem Cells | ||

| Adult Stem Cells | ||

| Dental Pulp Stem Cells | ||

| Induced Pluripotent Stem Cells | ||

| Non-stem Cell Banking | ||

| Microbial Cell Banking | ||

| Mammalian Cell Banking | ||

| Hybridoma Cell Banking | ||

| By Outsourced Service | Cell Line Development | |

| Characterization & Testing | ||

| GMP Manufacturing & Expansion | ||

| Cryopreservation & Storage | ||

| Logistics & Cold Chain Management | ||

| By End User | Biopharma & Biotech Companies | |

| Academic & Research Institutes | ||

| Contract Research Organizations | ||

| Hospitals & Transplant Centers | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving double-digit growth in the cell banking outsourcing market?

Surging cell and gene therapy pipelines, stricter GMP regulations and rapid adoption of AI-based quality controls collectively underpin the 16.71% CAGR forecast through 2031.

Which cell type segment is expanding the fastest?

Induced pluripotent stem cells are advancing at a 18.76% CAGR because they avoid embryonic ethics debates while supporting precision-medicine applications.

Why are logistics providers gaining revenue share?

Living-cell therapies must remain at cryogenic temperatures throughout the supply chain, elevating demand for specialized shippers with real-time tracking and validated routes.

How significant is North America’s participation?

North America commands 45.25% of 2025 global revenue, benefiting from FDA leadership, deep venture funding and significant capacity expansions by leading CDMOs.

What hurdles do emerging biotech firms face when building in-house banks?

Capital outlays exceeding USD 200 million and complex multi-jurisdictional regulations often make outsourcing more economical for early-stage ventures.

Page last updated on: