Ceiling Fan Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 12.89 Billion |

| Market Size (2031) | USD 15.60 Billion |

| Growth Rate (2026 - 2031) | 3.88% CAGR |

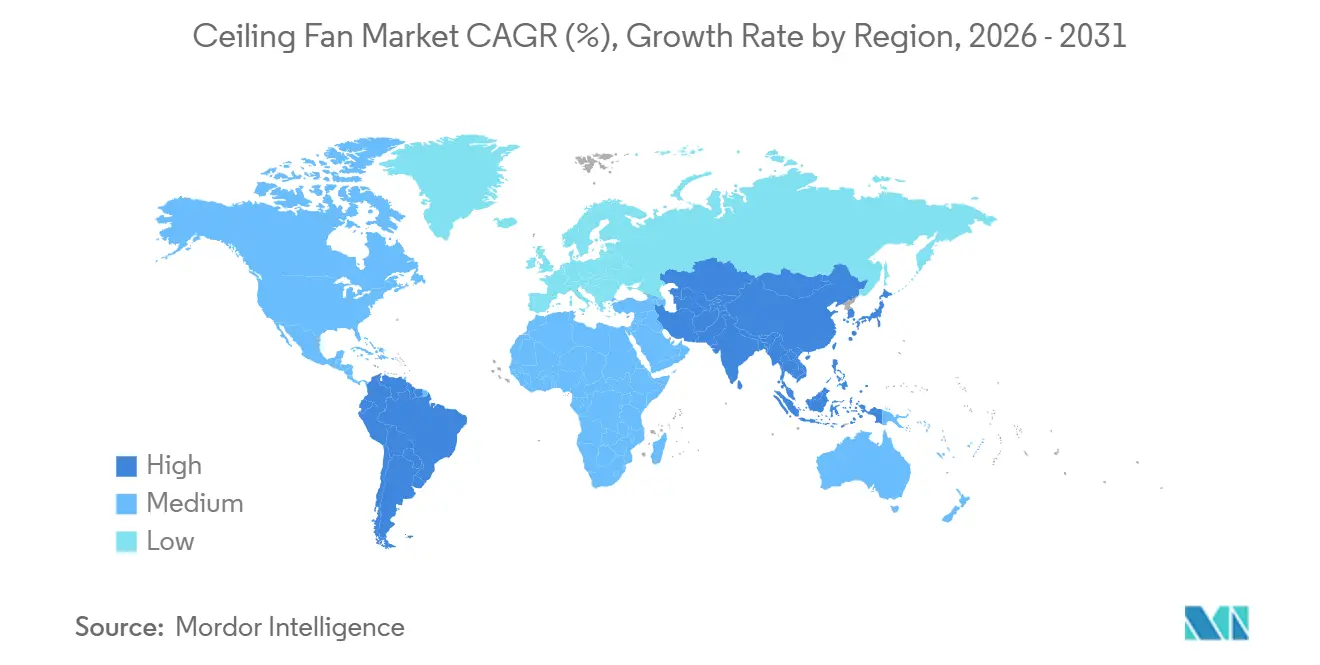

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ceiling Fan Market Analysis by Mordor Intelligence

The Ceiling Fan Market size is projected to expand from USD 12.21 billion in 2025 and USD 12.89 billion in 2026 to USD 15.60 billion by 2031, registering a CAGR of 3.88% between 2026 to 2031.

The shift toward brushless DC (BLDC) motors, the spread of IoT connectivity, and stricter efficiency rules are the dominant growth catalysts, while low-cost room air-conditioners, magnet price spikes, and safety-related recalls temper the upside. Manufacturers are scaling localized BLDC production in India, China, and Southeast Asia to shrink landed costs, and regulators in the United States, India, Singapore, and the European Union have raised minimum-efficiency floors that effectively phase out legacy AC induction designs. Online platforms and quick-commerce services are compressing purchase-to-installation cycles, widening consumer choice, and pressuring traditional retailers. However, market upside is moderated by the growing availability of low-cost room air conditioners, recurring safety-related recalls that raise compliance costs, and persistent consumer price sensitivity in emerging markets. Overall, value growth is increasingly driven by premiumization through smart features, integrated lighting, improved aesthetics, and energy savings, positioning ceiling fans as an integral component of energy-efficient and connected homes and commercial buildings.

Key Report Takeaways

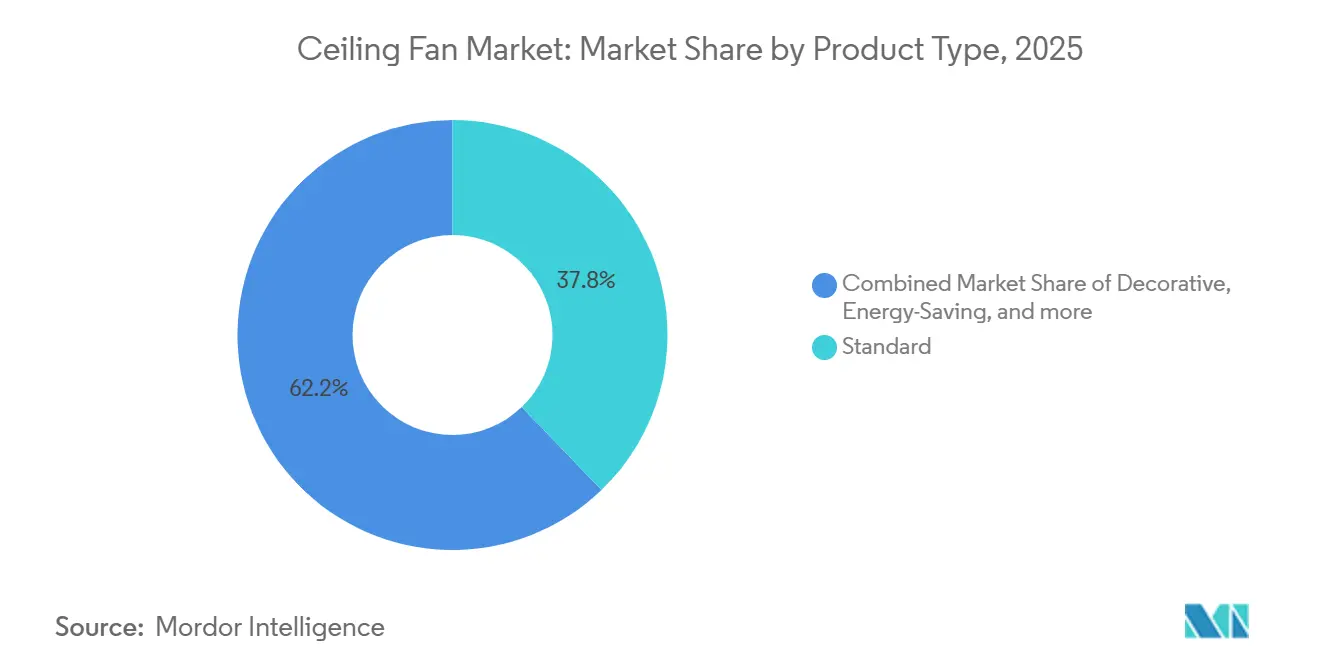

- By product type, standard 3-blade AC models led with 37.81% of the ceiling fan market share in 2025; energy-savings models are forecast to grow at a 5.47% CAGR through 2031.

- By technology, AC motors held 55.49% of the ceiling fan market share in 2025, whereas BLDC motors are projected to expand at a 6.22% CAGR to 2031.

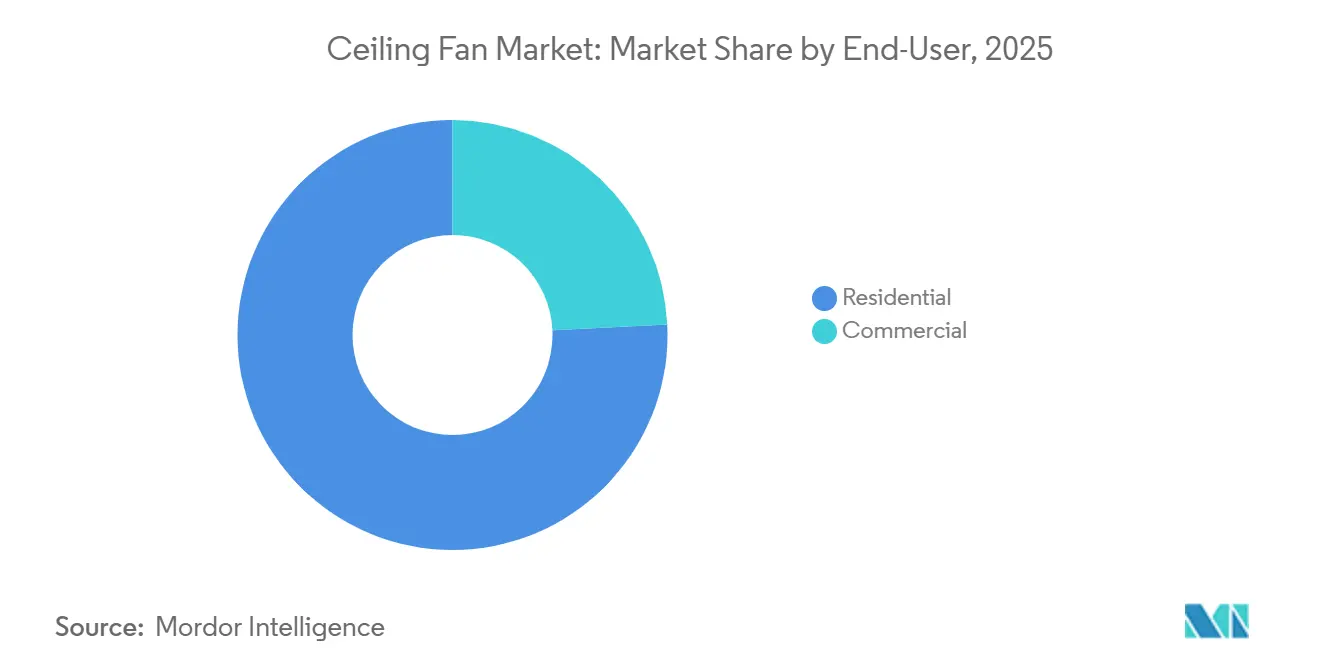

- By end-user, residential applications captured 75.77% of the ceiling fan industry share in 2025, and commercial applications are expected to rise at a 5.32% CAGR through 2031.

- By distribution channel, multi-brand retail stores accounted for 39.74% of the ceiling fan market share in 2025, while online sales are advancing at a 5.87% CAGR to 2031.

- By geography, Asia-Pacific generated 48.52% of the ceiling fan market share in 2025 and is on track for the fastest 5.16% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Ceiling Fan Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening energy-efficiency mandates, accelerating the transition to BLDC ceiling fans | +1.2% | Global; strongest in India, USA, EU, Singapore | Medium term (2-4 years) |

| Rising penetration of smart homes is driving demand for IoT-enabled ceiling fans | +0.8% | North America, Europe, urban Asia | Short term (≤2 years) |

| Scaling of cost-competitive BLDC manufacturing hubs across Asia, lowering product price barriers | +0.9% | India, China; export spill-over to MEA | Medium term (2-4 years) |

| Increasing adoption of green-building standards, promoting passive and energy-efficient cooling solutions | +0.5% | Global; early uptake in Singapore, India, the USA, EU | Long term (≥4 years) |

| Growing use of HVLS ceiling fans in temperature-controlled logistics and cold-chain facilities | +0.3% | North America, Europe, UAE, Singapore, India | Medium term (2-4 years) |

| Public housing programs and rural electrification initiatives are expanding first-time fan ownership | +0.7% | India, Southeast Asia, Sub-Saharan Africa | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Tightening Energy-Efficiency Mandates, Accelerating the Transition to BLDC Ceiling Fans

Global policy tightening is translating directly into higher BLDC penetration. As of 2025, large‑diameter ceiling fans in the U.S. remain subject to federal energy standards set by the Department of Energy, based on the Ceiling‑Fan Energy Index (CFEI) introduced in 2020. Although a new test procedure was implemented in 2023 and proposed updates to raise minimum efficiency standards were drafted in 2024, these updates were withdrawn in 2025.[1]Source: U.S. Department of Energy, “Energy Conservation Program: Test Procedure for Ceiling Fans,” amca.org The India Cooling Action Plan (ICAP) projects that India's ceiling fan stock will grow from 500 million to 1 billion by 2038, underscoring the need for energy-efficient cooling solutions. ICAP is an important element under the National Action Plan on Climate Change (NAPCC) with a mission focused on Enhanced Energy Efficiency (NMEEE), administered by BEE. [2]Department of Science & Technology, “Advancing Energy Efficient Ceiling Fans in India,” dst.gov.in BLDC fans, with lower electricity consumption, longer lifespans, and better speed control, align directly with ICAP’s mission to reduce energy demand and emissions in the cooling sector. Regulatory requirements, combined with increasing consumer awareness of energy costs, are creating a favorable market environment for BLDC ceiling fans, making energy efficiency a central criterion in both product development and purchasing decisions.

Rising Penetration of Smart Homes is Driving Demand for IoT-Enabled Ceiling Fans

The proliferation of IoT-enabled smart ceiling fans is reshaping the ceiling fan market by adding connectivity, convenience, and energy management features. Smart fans equipped with WiFi, Bluetooth, or Zigbee radios are expanding at more than three times the rate of the traditional ceiling fans market, reflecting strong consumer demand for home automation. Products like Hunter’s SIMPLEconnect series, which include Matter-certified radios compatible with Apple, Google, and Amazon ecosystems, demonstrate a trend toward open platform interoperability, eliminating the need for proprietary hubs and making integration seamless[3]Source: Hunter Fan Company, “SIMPLEconnect Launch Brochure,” hunterfan.com. . These connected fans allow users to control speed, lighting, and scheduling remotely via apps or voice assistants, increasing convenience and energy efficiency. The data generated by smart fans also enables advanced features such as usage analytics and predictive maintenance, further enhancing their value proposition. As consumers increasingly seek multifunctional and tech-enabled home appliances, IoT-enabled ceiling fans are driving innovation, creating new revenue streams for manufacturers, and accelerating adoption in both residential and commercial sectors.

Scaling of Cost-Competitive BLDC Manufacturing Hubs Across Asia, Lowering Product Price Barriers

The expansion of low-cost BLDC manufacturing in Asia is significantly reshaping the ceiling fan industry by improving local production and reducing reliance on imports. Ebm Papst’s USD 37.3 million investment in a new Chennai plant and Haier’s capacity in Greater Noida are enabling localized production of EC and BLDC motors, lowering landed costs by up to 25%.[4]Source: ebm papst, “ebm papst Announces Its 3rd Manufacturing Unit in India,” ebmpapst.com. Automated winding lines further reduce labor requirements, giving regional manufacturers a competitive cost advantage over imported fans. At the same time, China’s dominance of NdFeB magnet production, which accounts for 85% of global supply, allows Chinese suppliers to price aggressively in export markets, intensifying competition. To mitigate supply risks, Indian manufacturers are securing multi-year contracts with Japanese magnet producers, even at higher material costs, ensuring steady access to critical components. This combination of localized production, automation, and strategic sourcing is driving wider adoption of BLDC ceiling fans in Asia, making high-efficiency fans more accessible and cost-competitive for both residential and commercial markets.

Increasing Adoption of Green-Building Standards, Promoting Passive and Energy-Efficient Cooling Solutions

Green-building codes are increasingly promoting the use of ceiling fans as a key component of energy-efficient design. In India, the ECBC 2024 requires large new buildings to use fans with a Service Value of at least 4.5 CMM/W, effectively mandating BLDC or high-efficiency units. Singapore’s Green Mark Platinum certification awards extra points for high-efficiency ceiling fans, which can translate into rental premiums of 8–12% for compliant buildings. Similarly, LEED v5 provides credits for passive cooling strategies that reduce HVAC loads by a minimum of 15%, positioning ceiling fans as a critical tool for meeting these standards. As the amount of green-certified commercial floor space is projected to double by 2030, ceiling fans are transitioning from optional comfort devices to essential, code-mandated equipment. This regulatory push is driving both developers and building managers to prioritize high-efficiency and smart ceiling fans, creating strong demand in the commercial real estate market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low-cost room air-conditioners are reducing reliance on ceiling fans in warm regions | -0.6% | India, Southeast Asia, Brazil, the Middle East | Short term (≤2 years) |

| Seasonal sales volatility leading to inventory and pricing pressure | -0.3% | Global, temperate zones most volatile | Short term (≤2 years) |

| Rare-earth magnet supply tightness is increasing BLDC production costs | -0.4% | Global; acute outside China | Medium term (2-4 years) |

| Counterfeit electronic components are driving recalls and compliance risk | -0.2% | North America, Europe; export spill-over | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Low-Cost Room Air-Conditioners are Reducing Reliance on Ceiling Fans in Warm Regions

The growing penetration of low-cost room air conditioners is increasingly challenging ceiling fan demand in urban and emerging markets. Falling prices for inverter ACs, combined with extended financing options, are making mechanical cooling accessible to middle-income households that previously relied primarily on ceiling fans. In India, AC penetration is expected to rise from 8% in 2023 to 15% by 2028, while in Brazil, household AC penetration reached 22.6% in 2024, compressing ceiling-fan replacement cycles as consumers shift usage to secondary rooms or remove fans entirely. Data shows that Brazilian households with ACs reduced ceiling-fan use by 40–50%, and 18% of new AC buyers removed fans within a year. In the MENA region, where AC penetration exceeds 85% in urban areas, fans are relegated to supplementary roles, and AC sales are projected to grow faster than fans through 2028. The rise of ultra-low-cost ACs in India, priced below high-efficiency BLDC fans, further undermines the value proposition of ceiling fans, particularly in cities with reliable electricity, signaling a structural shift in cooling preferences.

Seasonal Sales Volatility Leading to Inventory and Pricing Pressure

Ceiling-fan demand is highly seasonal, with 60–70% of annual sales occurring in the March–June pre-summer and summer months, creating challenges for inventory planning and working-capital management. Unseasonably warm or cool weather can cause significant swings, as seen when Orient Electric experienced a surge in November 2023–February 2024, followed by a collapse in March–April, resulting in 45 days of excess inventory and 12–15% price cuts that compressed margins. In Brazil, distributors increased inventory by 20–30% after a record 33% sales surge in 2024 to hedge against demand volatility, tying up capital and raising financing costs. Crompton Greaves reported only 5% year-on-year growth despite higher shipments, as off-season promotions to maintain distributor fill rates reduced price realization. The rise of e-commerce has amplified seasonality risk, with brands committing inventory 60–90 days in advance for mega-sale events on platforms like Flipkart and Amazon India, sometimes leading to over-shipment and liquidation at 25–30% discounts. Climate volatility further complicates forecasting, as inaccurate long-range temperature predictions can leave distributors with unsold stock, increasing financial pressure and operational inefficiencies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Energy-Saving BLDC Drives Premiumization

Energy-saving fans are expanding at a 5.47% CAGR to 2031, a pace that eclipses the overall ceiling fans market. India’s 2025 star-band reset instantly downgraded yesterday’s premium induction units to 1-star status and triggered a broad replacement cycle that lifts the ceiling fan market share of BLDC models every quarter. Atomberg’s first-mover bet on 100% BLDC manufacturing translated into 60% domestic sub-segment share and FY 2024 revenue of Rs 848 crore (USD 94.38 million), proof that the premiumization narrative travels beyond metros. Decorative fans with designer blades, integrated lighting, and premium finishes are appealing to homeowners upgrading from basic models, with Orient Electric reporting 22% year-on-year growth in fiscal 2025, driven by its Cloud 3 bladeless fan. Energy-saving BLDC fans with BEE 5-star ratings are expanding in India, where recalibrated Service Value thresholds in 2025 have accelerated replacement demand by rendering older induction fans obsolete. High-speed and HVLS fans are gaining traction in industrial and commercial applications, serving workshops, warehouses, and cold-chain facilities, with Hunter Industrial and MacroAir Technologies reporting double-digit order growth in 2024-2025.

Standard three-blade AC fans still delivered 37.81% of 2025 revenue thanks to low entry prices, yet that slice is slipping as subsidies and cost-deflation compress the BLDC premium to single digits in mid-tier models. Hunter Fan’s SIMPLEconnect series and Orient Electric’s Aeroslim IoT fan have demonstrated strong market acceptance, with IoT models commanding 40–50% price premiums and driving margin expansion. Panasonic’s WiFAN DC motor fans, equipped with occupancy sensors, are reducing energy consumption by 15–20% and expanding across Southeast Asia. The CSA’s Matter 1.2 specification has ensured cross-platform compatibility, encouraging OEM adoption and enabling challengers like Dreo to enter North America at competitive prices. While 3-blade AC fans remain dominant in rural and semi-urban markets, declining BLDC manufacturing costs and government subsidy programs, such as India’s pilot fan-replacement schemes, are gradually shifting consumer preference toward high-efficiency, connected fans.

ByTechnology: BLDC Efficiency Drives Market Transition

AC motors retained 55.49% of global ceiling-fan volume in 2025 due to their low material cost (USD 8–12 per motor versus USD 18–28 for BLDC) and established supply chains. However, BLDC fans are growing rapidly at a 6.22% CAGR, fueled by regulatory mandates, falling manufacturing costs, and premiumization trends. Traditional brushed DC motors remain in niche off-grid solar applications, but their share in India dropped from 45% in 2020 to 22% in 2024 as BLDC prices fell below USD 25 per unit. BLDC motors, using permanent-magnet rotors and electronic commutation, deliver 50–60% energy savings, lower battery drain for inverters, and silent operation, with Atomberg Technologies reporting consumption of just 28–35 watts versus 70–75 watts for conventional fans. Energy-efficiency programs such as the U.S. DOE’s 2024 CFEI and India’s 2025 BEE star recalibration further incentivize BLDC adoption by rewarding higher airflow efficiency and rendering older AC or induction-fan models effectively obsolete.

Manufacturing-cost deflation is accelerating BLDC adoption in Asia. Ebm Papst’s Chennai plant (USD 37.3 million) will localize EC/BLDC motor production by 2026, cutting landed costs by 20–25%, while Haier’s Greater Noida investment (USD 420 million) aims for 2.5 million units annually by 2028, positioning India as a regional export hub. Atomberg Technologies scaled its Pune facility to over 1 million units per month, using automated winding and magnet insertion lines that reduce labor content and boost margins despite raw-material inflation. Crompton Greaves’ NUCLEUS BLDC platform and Orient Electric’s BLDC models, which grew over 50% YoY in fiscal 2025, highlight strong market acceptance and 40–50% price premiums over AC fans. Although AC motors remain dominant in rural and semi-urban markets due to lower upfront costs, declining BLDC prices, and government subsidy programs are shifting consumer preference toward high-efficiency, BLDC-equipped ceiling fans.

By End-User: Residential Premiumization Outpaces Baseline Demand

The residential segment accounted for 75.77% of global ceiling-fan demand in 2025, reflecting the category’s historical role as a household appliance, while the commercial segment is growing at 5.32% CAGR through 2031. Commercial buyers, including offices, retail spaces, hotels, and healthcare facilities, prioritize reliability, low maintenance, and BMS integration, with Orient Electric reporting 14% year-on-year growth in its commercial-fan segment in fiscal 2025. Industrial applications such as factories, warehouses, and cold-chain facilities increasingly adopt HVLS fans, which destratify air and reduce HVAC loads, with Hunter Industrial noting double-digit order growth for its Titan HVLS series in 2024–2025. Residential demand is diverging: mass-market households in emerging economies favor low-cost AC-motor fans under USD 24, while affluent urban buyers in North America, Europe, and Asia-Pacific prefer BLDC-plus-IoT models priced at USD 150–400 with app control, voice-assistant integration, and energy monitoring.

Government housing programs are supporting baseline residential demand. India’s PMAY-G initiative sanctioned nearly 4 million homes in fiscal 2024–25, targeting 20 million by 2029, with subsidies typically funding 2–3 ceiling fans per dwelling, adding 6–8 million units annually. The Saubhagya electrification scheme connected 28.6 million households by 2024, and surveys show 78% purchased at least one fan within a year of grid connection. Commercial demand in MENA is rising alongside organized retail expansion, with ceiling fans specified in over 60% of new malls and mixed-use projects, particularly in outdoor terraces, food courts, and loading areas. Industrial HVLS fans are improving cold-chain efficiency, while energy-efficiency regulations in India are accelerating residential replacement cycles, with Orient Electric reporting a 28% year-on-year increase in urban upgrades to BLDC models.

By Distribution Channel: Online Platforms Disrupt Traditional Retail

Multi-brand retail stores captured 39.74% of global ceiling-fan sales in 2025, serving as primary touchpoints in Tier-2 and Tier-3 cities where consumers prefer hands-on evaluation. Online channels are expanding rapidly at a 5.87% CAGR, driven by e-commerce penetration, fast delivery, and digital-native brands. Exclusive brand outlets, operated by manufacturers such as Crompton, Havells, and Orient Electric, act as experiential showrooms, with Orient’s Smart Shop franchise delivering 18% higher average selling prices through consultative demonstrations of BLDC and IoT fans. Other channels, including mom-and-pop electrical shops and regional distributors, capture rural and semi-urban demand, while B2B/project sales to developers and institutions are growing as green-building codes embed fan specifications. Quick-commerce partnerships, like Orient Electric’s collaboration with Zepto, are shortening purchase-to-installation cycles and tapping impulse buyers, with rapid delivery sales growing 140% year-on-year in Q4 fiscal 2025.

Multi-brand retail chains, including Croma, Reliance Digital, and Home Depot, remain dominant where consumers value immediate availability, installation, and hands-on evaluation, though their share is declining as online platforms offer 20–30% discounts and hassle-free returns. Exclusive outlets allow manufacturers to control the customer experience and capture higher margins, with Havells operating over 200 stores targeting premium BLDC and decorative fans. B2B/project channels are accelerating due to ECBC 2024 requirements in India, which mandate BLDC fans with minimum efficiency in new commercial buildings, making developers specify high-efficiency fans by default. Online marketplaces such as Amazon, Flipkart, Noon, and Mercado Libre are emerging as key sales channels for digital-native brands like Atomberg and Dreo, which reported over 65% of sales online in fiscal 2025. The shift to e-commerce increases seasonality risk, as brands must commit inventory 60–90 days in advance for mega-sales, with over-shipping in 2024 leading to post-season liquidation at 25–30% discounts.

Geography Analysis

Asia-Pacific accounted for 48.52% of global ceiling-fan revenue in 2025 and is expected to grow at a 5.16% CAGR, fueled by India’s affordable-housing programs and rural electrification. Subsidies under these schemes generate 6–8 million additional fan units annually, with each household typically purchasing two to three fans. China’s vertically integrated magnet supply supports low-cost BLDC exports to Southeast Asia and Africa, enabling competitive pricing and wider adoption. India remains a key growth driver, as BLDC fans are increasingly replacing legacy AC models in new constructions and replacement cycles. Rising disposable incomes and urbanization further expand the mid- and premium-tier fan segments in Asia-Pacific markets.

North America’s market is largely replacement-driven, with premiumization and Matter-certified smart fans boosting average selling prices. The U.S. DOE’s 2026 test procedure updates push legacy AC models into lower efficiency tiers, encouraging households to upgrade to BLDC fans. South America saw a 33% sales surge in 2024 due to extreme heat, though rapid AC adoption in Brazil is compressing follow-up demand and forcing distributors to hold larger inventories. Europe’s growth is driven by design-focused replacements and stricter Ecodesign standards, with Northern countries prioritizing energy savings and Mediterranean regions using fans to complement rising temperatures. In the Middle East and Africa, GCC nations specify fans for outdoor and semi-conditioned zones in large retail projects, while Sub-Saharan Africa relies on solar-DC models, with off-grid kits projected to exceed 15 million units by 2028.

Competitive Landscape

The ceiling fan market is moderately fragmented, with the largest players holding a minority of global revenue, while many regional specialists and digital-native brands further disperse market share. Established incumbents, including Crompton, Havells, Orient Electric, Hunter Fan, and Panasonic, leverage brand recognition, distribution networks, and proprietary BLDC platforms to defend premium segments. Digital native challengers like Atomberg Technologies and Dreo are gaining ground by offering lower prices, shipping Matter-certified smart fans, and bypassing physical retail through platforms like Amazon and Flipkart. White space opportunities include solar-powered fans for off-grid areas in Sub-Saharan Africa and rural India, and HVLS fans for cold chain warehouses, where double-digit order growth is driven by 12 to 18% energy reductions.

Technology has become the primary battleground for market share. BLDC manufacturing cost reductions, supported by ebm papst’s INR 340 crore Chennai plant and Haier’s INR 3,500 crore (USD 420 million) Greater Noida facility, allow incumbents to scale production and narrow price gaps with AC fans. Matter certification is standardizing smart fan connectivity, reducing the advantage of proprietary ecosystems. Orient Electric reported that BLDC fans represented roughly 20% of its ceiling fan sales in fiscal 2025, growing over 50% year on year, with these models commanding 40 to 50% price premiums over AC equivalents. Emerging disruptors are leveraging direct-to-consumer models and digital marketing to bypass traditional retail, with Atomberg noting that over 65% of its sales in fiscal 2025 were online, and partnerships like Zepto’s 10-minute delivery are capturing impulse buyers.

Supply chain and regulatory factors remain critical risks for the market. China controls over 85% of global neodymium iron boron rare earth magnet production, forcing non-Chinese manufacturers to secure multi-year contracts at 10 to 15% cost premiums. The U.S. Consumer Product Safety Commission issued recalls of over 1.2 million fans in 2024 to 2025 due to counterfeit capacitors, denting consumer trust and raising compliance costs. Brands have responded with 100% incoming component testing, adding 0.50 to 0.80 USD per fan in quality control expenses. Despite these challenges, incumbents and challengers alike are accelerating BLDC and IoT adoption, optimizing supply chains, and exploiting efficiency and connectivity as key differentiators in the global ceiling fan market.

Ceiling Fan Industry Leaders

Hunter Fan Company

Crompton Greaves Consumer Electricals Ltd.

Orient Electric Ltd.

Havells India Ltd.

Emerson Electric Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Atomberg raised INR 212 crore (USD 25 million) in a Series C extension led by Temasek, bringing total funding to USD 150 million. The capital will expand Pune production beyond 1 million BLDC fans per month and support diversification into kitchen appliances, leveraging its BLDC motor expertise.

- April 2025: Panasonic launched its Bayu DC motor ceiling fans in Malaysia, featuring WiFAN app control, ECONAVI occupancy sensors, and nanoe X air purification. Priced at USD 200-335, the series targets affluent urban buyers, with expansion planned to Singapore, Thailand, India, and Indonesia by 2026, combining cooling with air-quality solutions.

Research Methodology Framework and Report Scope

Market Definition and Key Coverage

Our study defines the ceiling fan market as the shipment value of newly manufactured, ceiling-mounted electric fans (≤ 72 in blade span) that circulate ambient air across residential, commercial, and light-industrial spaces. Units powered by AC, DC, or BLDC motors and sold through offline and online retail or project channels are counted at factory gate prices.

Scope exclusion: HVLS fans above 24 ft diameter and portable, wall, pedestal, or exhaust fans are kept outside this assessment.

Segmentation Overview

- By Product Type

- Standard

- Decorative

- Energy-Saving

- High-Speed

- With Integrated Light

- HVLS

- Smart / IoT

- Solar-Powered

- By Technology

- AC Motor

- DC Motor

- BLDC Motor

- By End-User

- Residential

- Commercial

- Industrial

- By Distribution Channel

- B2C/Retail Channels

- Multi-Brand Stores

- Exclusive Brand Outlets

- Online

- Other Distribution Channels

- B2B/Project Channels (direct from the manufacturers)

- B2C/Retail Channels

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, and Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- Rest of Europe

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- Rest of Asia-Pacific

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with motor suppliers in Shenzhen, branded fan assemblers in Chennai, HVAC distributors across the Gulf, and e-commerce category managers in the United States. These conversations validated channel sell-through ratios, BLDC penetration, and average replacement cycles that secondary sources could only hint at.

Desk Research

To size the base year, we reviewed customs records under HS 841451, building completion statistics from sources such as UN Comtrade, the World Bank housing database, and IEA electricity-access dashboards. Trade association briefs from the Fan Manufacturers Association of India and the US DOE appliance rulemakings clarified efficiency standards that sway model mix. Company 10-Ks, IPO papers, and investor decks were scraped through D&B Hoovers and Dow Jones Factiva to pull ASP trends and capacity additions. News wires, patent counts from Questel, and quarterly import shipment tallies rounded out price and volume cross-checks. The list is illustrative; many further open datasets informed corroboration.

Market-Sizing & Forecasting

A top-down build begins with country housing stock, new dwelling additions, and electrification reach; these pools are multiplied by installation rates that our primary calls refined and by region-specific ASPs. Supplier roll-ups and sampled e-tail volume snapshots provide bottom-up reasonableness checks before totals are reconciled. Key drivers we monitor include government star-rating mandates, urban disposable income, online fan share, and BLDC motor cost curves, which feed a multivariate regression to project demand through 2030. Gaps where import data lag are bridged with short-term exponential smoothing anchored to the most recent quarterly shipments.

Data Validation & Update Cycle

Every model pass runs variance scans against historical trade flow trends and retailer sell-out indices. Material outliers trigger re-contact of experts, after which findings go through a two-level analyst review. Reports refresh annually, with interim touch points when policy or commodity shifts exceed predefined thresholds.

Why Mordor's Ceiling Fan Industry Size - Market Report On Share, Growth Trends & Forecasts Analysis Baseline Deserves Trust

Estimates from different publishers often diverge because each firm chooses its own product cut-off, price basis, and refresh cadence. We flag these levers upfront so clients instantly see where figures separate.

Key gap drivers include whether outdoor and HVLS units are folded in, how currency conversions are timed, and if premium smart-fan ASP uplift is captured. Mordor fixes scope first, triangulates volumes with live trade sheets, and updates the model every twelve months, which competitors seldom match.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 12.44 B (2025) | Mordor Intelligence | - |

| USD 14.86 B (2024) | Global Consultancy A | Includes HVLS and outdoor fans, relies on retailer margin mark-ups |

| USD 10.17 B (2024) | Industry Tracker B | Excludes smart fans > USD 200, linear growth from 2023 base, limited primary checks |

The comparison shows that once differing scopes and assumptions are stripped away, Mordor's disciplined variable selection and annual refresh deliver a balanced, transparent baseline that decision-makers can rely on.

Key Questions Answered in the Report

What is the current global ceiling fan market size and growth outlook?

The ceiling fan market size stood at USD 12.89 billion in 2026 and is forecast to reach USD 15.60 billion by 2031, registering a 3.88% CAGR between 2026-2031.

Which technology segment is expanding the fastest?

BLDC motors are the fastest, projected to grow at a 6.22% CAGR through 2031 due to efficiency mandates and falling component costs.

How big is the opportunity in Asia?

Asia-Pacific contributed 48.52% of 2025 revenue and is expected to grow at a 5.16% CAGR, driven by Indian housing programs and localized BLDC production.

What are the key regulatory shifts affecting product design?

The U.S. DOE’s CFEI metric and India’s tightened star-rating bands raise minimum efficiency requirements, effectively steering the industry toward BLDC motors.

Who is leading the smart ceiling fan space?

Hunter, Orient Electric, and Atomberg lead with Matter-certified, app-controlled models, each reporting double-digit growth in connected fan sales.

Which distribution channel is gaining the most share?

Online platforms, including quick-commerce services, are growing at a 5.87% CAGR, eroding the dominance of multi-brand physical retailers.

Page last updated on: