Jam Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 13.28 Billion |

| Market Size (2031) | USD 16.51 Billion |

| Growth Rate (2026 - 2031) | 4.45% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Jam Market Analysis by Mordor Intelligence

The jam market size was valued at USD 12.71 billion in 2025 and estimated to grow from USD 13.28 billion in 2026 to reach USD 16.51 billion by 2031, at a CAGR of 4.45% during the forecast period (2026-2031). This growth is attributed to strong household penetration, increasing consumer interest in premium flavor experimentation, and the consistent introduction of reduced-sugar recipes, even as consumers become more attentive to ingredient transparency. Major manufacturers are focusing on transparent sourcing practices and adopting sustainable packaging solutions while leveraging efficiencies in the global fruit supply chain to safeguard their profit margins. Simultaneously, artisanal brands are capitalizing on digital platforms to establish and expand their market presence. For instance, the Food and Agriculture Organization of the United Nations (FAO) reported that global fruit production in 2023 surpassed 951.91 million metric tons, with bananas ranking as the highest-produced fruit at 139.28 million metric tons[1]Source: Food and Agriculture Organization of the United Nations, "Production volume of fruit worldwide", fao.org. This underscores the pivotal role of fruit in global agriculture and diets, with a rich diversity contributing to the total output. Similarly, bountiful fruit harvests in regions like the Asia Pacific and South America not only stabilize raw material costs but also encourage experimentation with exotic varieties. While concerns about sugar content pose challenges, advancements in technology-driven formulation tools and clearer regulations on alternative sweeteners offer producers a route to healthier product labels.

Key Report Takeaways

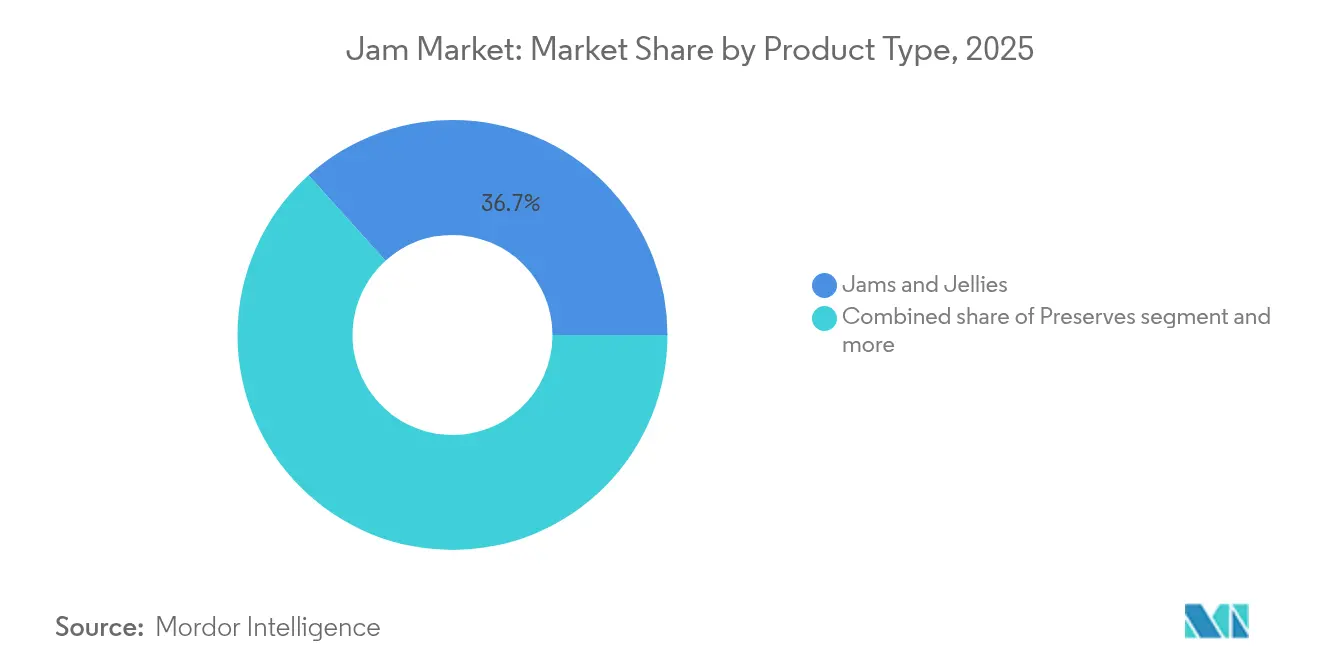

- By product type, jams and jellies led with 36.68% of the jam market share in 2025, while preserves are advancing at a 5.57% CAGR through 2031.

- By category, conventional offerings controlled 90.05% of the jam market size in 2025, yet organic variants are growing at a 6.25% CAGR to 2031.

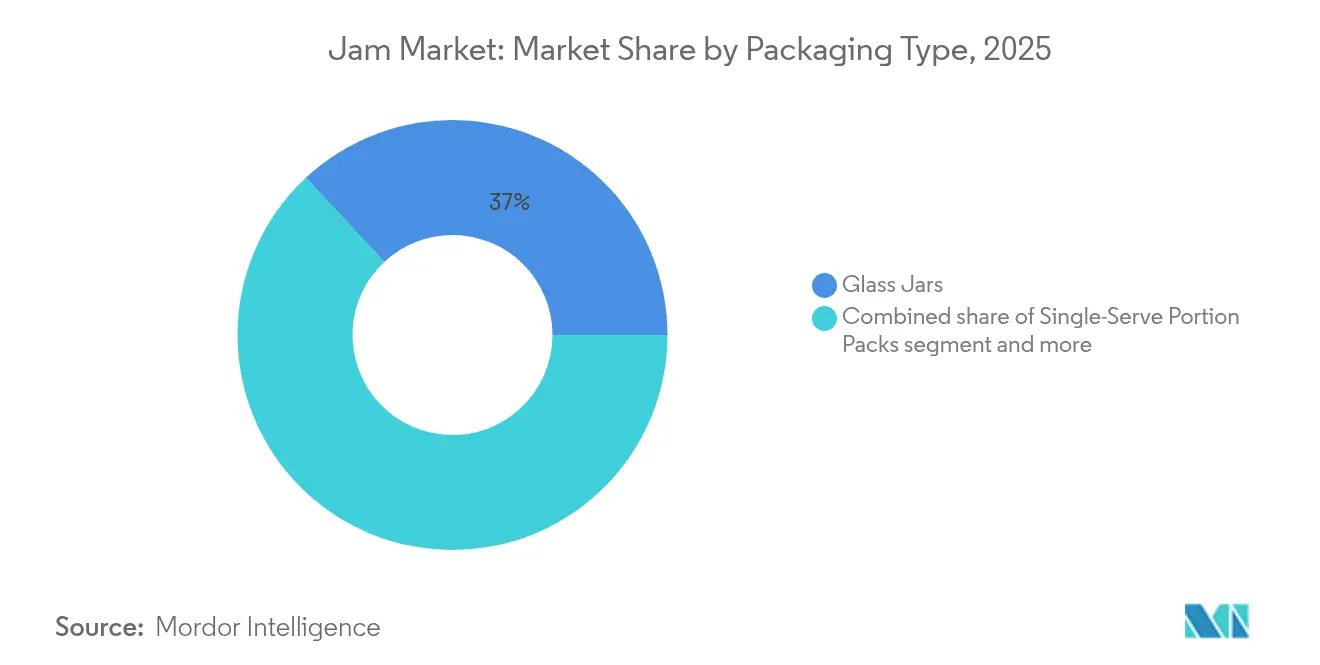

- By packaging type, glass jars accounted for 36.95% of the jam market share in 2025, whereas single-serve portion packs are projected to expand at a 6.07% CAGR to 2031.

- By distribution channel, supermarkets and hypermarkets held 41.98% share of the jam market size in 2025, while e-commerce is climbing at a 5.69% CAGR through 2031.

- By geography, North America captured 41.70% of the jam market share in 2025; Asia Pacific is on track for a 5.38% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Jam Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Innovation in Flavors | 1.0% | Global, with the strongest uptake in North America and Europe | Medium term (2-4 years) |

| Rising Global Fruit Production | 0.8% | Global, particularly Asia Pacific and South America | Long term (≥ 4 years) |

| Increasing Preference for Clean-Label Products | 0.6% | North America & Europe, expanding to the Asia-Pacific | Medium term (2-4 years) |

| Rising Demand for Reduced-Sugar and Sugar-Free Variants | 0.4% | Global, led by developed markets | Short term (≤ 2 years) |

| Growing Interest in Organic and Artisanal Products | 0.3% | North America and Europe, emerging in the Asia-Pacific | Long term (≥ 4 years) |

| Emergence of Convenient Packaging Formats | 0.2% | Global, with early adoption in North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Innovation in Flavors

In the jam and preserves market, flavor innovation stands out as a key differentiator. Manufacturers are now delving into exotic fruit combinations and globally inspired profiles, aiming to resonate with younger consumers. This trend isn't limited to the usual berry and citrus flavors; it's branching out to include adventurous fusions like yuzu-ginger, hibiscus-lime, and intriguing savory-sweet blends. Companies are harnessing natural flavor enhancement technologies, intensifying authentic taste experiences while steering clear of artificial additives. T. Hasegawa's 2025 flavor trends report spotlights brown sugar as the year's standout flavor, pushing premium applications in sweet spreads and paving the way for caramelized fruit preserves. This wave of innovation is especially vibrant in North America and Europe, where consumers are more inclined to pay a premium for distinctive flavor experiences. Regulatory bodies, like the FDA and EU, are backing this trend by approving natural flavor compounds, thus encouraging wider experimentation with botanical and spice-infused variants.

Rising Global Fruit Production

Global fruit production has experienced steady growth, as indicated by Food and Agriculture Organization (FAO) data showing increased yields in key fruit-producing regions. This growth has provided a supportive environment for jam and preserve manufacturers. For instance, the United States Department of Agriculture (USDA) Foreign Agricultural Service reported that global orange production in the 2023/2024 marketing year reached approximately 47 million metric tons, compared to 46.88 million metric tons in the previous year[2]Source: USDA Foreign Agricultural Service, "Citrus: World Markets and Trade July 2024", fas.usda.gov. Enhanced fruit quality and prolonged harvesting seasons, driven by climate adaptation strategies and advanced agricultural techniques, are especially evident in the Asia Pacific and South America. Here, tropical and subtropical fruits are increasingly featured in preserve formulations. Moreover, the growth of fruit production infrastructure in emerging markets has not only lowered raw material costs but also bolstered supply chain reliability. This has empowered manufacturers to explore premium and exotic fruit varieties. As consumers show heightened interest in provenance and seasonal eating, there's a burgeoning market for limited-edition and harvest-specific product lines. Given the long-term nature of agricultural investments, this trend is poised to bolster market growth through 2030, especially as sustainable farming practices continue to enhance both yield and quality.

Increasing Preference for Clean-Label Products

In 2023, the International Food Information Council reported that about 29% of U.S. consumers regularly purchase food and beverages labeled with "clean ingredients"[3]Source: International Food Information Council, "Food & Health Survey 2023", ific.org. This growing preference for clean labels has led manufacturers to reformulate products, opting for natural preservation methods, fruit-derived sweeteners, and techniques that uphold nutritional integrity. Beyond just simplifying ingredients, brands are emphasizing transparent sourcing practices, showcasing partnerships with farms and traceability initiatives to foster consumer trust. Regulatory support, including the United States Food and Drug Administration (FDA) and European Union (EU) clean-label guidelines, provides a framework for marketing claims. At the same time, retailers are advocating for cleaner formulations, accelerating their adoption across multiple distribution channels. This trend is particularly evident in developed markets, where greater consumer awareness and higher purchasing power support the premium pricing.

Rising Demand for Reduced-Sugar and Sugar-Free Variants

As diabetes rates climb and weight management takes center stage, global markets are witnessing a surge in demand for reduced-sugar and sugar-free jam alternatives. In response, manufacturers are turning to innovative sweeteners like stevia, monk fruit, and allulose, crafting formulations that not only taste great but also cut down on calories. The rise of anti-obesity medications has further fueled the appetite for portion-controlled, sugar-conscious foods, prompting jam makers to roll out specialized lines catering to health-savvy consumers. Analyzing consumer food trends reveals a pronounced shift: health considerations are increasingly steering the formulation strategies of packaged foods, especially as dietary guidelines and medical advice evolve. This shift isn't just theoretical; retailers are carving out more shelf space for these healthier alternatives, and shoppers are on the hunt for lower-sugar choices. Bolstering this movement, the regulatory landscape is evolving too, with new nutritional labeling mandates and health claims for alternative sweeteners gaining traction.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Sugar Content Limits Health-Conscious Consumer Interest | -0.5% | Global, most pronounced in developed markets | Short term (≤ 2 years) |

| Consumer Concerns Around Artificial Ingredients and Preservatives | -0.3% | North America & Europe, expanding globally | Medium term (2-4 years) |

| High Cost of Sustainable and Eco-friendly Packaging | -0.2% | Global, with varying regional impact | Long term (≥ 4 years) |

| Limited Recycling and Composting Infrastructure for Sustainable Packaging | -0.1% | Developing markets, some developed regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Sugar Content Limits Health-Conscious Consumer Interest

Health-conscious consumers are increasingly turning away from traditional jams and preserves, linking their high sugar content to health issues like diabetes, obesity, and metabolic disorders. In 2023, the Centers for Disease Control and Prevention reported that approximately 32% of men and 34% of women in the United States were classified as obese. As nutritional awareness campaigns and medical advice stress the importance of sugar reduction, conventional products face mounting challenges in the market. This issue is especially pronounced in developed markets, where consumers are well-informed and have easy access to alternative products. Manufacturers find themselves at a crossroads, needing to meet taste expectations while positioning their products as health-conscious. This often demands hefty investments in reformulation and consumer education to retain market share. The situation is further complicated by the rising popularity of anti-obesity medications and a broader trend towards wellness, pushing consumers to seek food products that resonate with their health-focused choices.

Consumer Concerns Around Artificial Ingredients and Preservatives

Jam and preserve manufacturers face significant formulation challenges as consumer skepticism toward artificial ingredients and chemical preservatives continues to grow. This trend is closely tied to the broader clean-eating movement, which emphasizes the consumption of minimally processed and natural foods, and the increasing demand for ingredient transparency. Consumers are progressively avoiding products that contain artificial colors, flavors, and preservatives, driven by concerns over potential health risks. Furthermore, there is a rising wave of environmental and ethical objections to the use of synthetic food additives, as consumers prioritize sustainability and ethical sourcing in their purchasing decisions. This shift has led to an increased demand for natural alternatives, which, while preferred by consumers, often come with higher production costs and technical complexities in formulation. As a result, manufacturers are under considerable pressure to reformulate their products to align with clean-label expectations—products that are free from artificial ingredients and clearly labeled—while ensuring the taste, texture, and shelf-life that consumers have come to expect from traditional jams and preserves.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Preserves Drive Premium Growth

In 2025, jams and jellies command a dominant 36.68% market share, underscoring their widespread consumer appeal and robust retail distribution networks. Yet, it's the preserves segment that's charting the most impressive growth, boasting a 5.57% CAGR through 2031. This surge is largely attributed to shifting consumer preferences favoring whole-fruit textures and a premium positioning that justifies higher price points. Artisanal branding and clean-label associations further bolster the preserves segment, with consumers equating chunky fruit pieces to superior quality and minimal processing. Meanwhile, marmalade, though occupying a smaller niche, enjoys stable demand, especially in European markets where tradition reigns.

Innovation in the preserves realm is buzzing, with a spotlight on exotic fruit blends and exclusive seasonal releases, both of which amplify excitement and support premium pricing. In a strategic move, Crofter's Organic rolled out its squeezable pouch format in October 2024, targeting the on-the-go consumer while upholding its organic certification, a badge of honor for health-conscious buyers. This growth in the preserves segment mirrors a broader trend in the food industry: a pronounced premiumization, where consumers are increasingly willing to shell out more for perceived quality and authenticity. On the regulatory front, compliance is a breeze for all product types, thanks to the clear guidelines set by the FDA and international food safety standards on manufacturing and labeling.

By Category: Organic Segment Accelerates Despite Conventional Dominance

In 2025, conventional products dominate the market with a commanding 90.05% share, thanks to their well-established supply chains, competitive pricing, and widespread acceptance among diverse consumers. This stronghold is the result of decades of strategic brand building, a vast distribution network, and manufacturing efficiencies that keep retail prices competitive. Meanwhile, the organic segment is on a rapid ascent, boasting a 6.25% CAGR through 2031. This surge is fueled by health-conscious consumers who are increasingly willing to pay a premium for certified organic ingredients and sustainable farming practices.

The growth of the organic segment reflects a broader shift towards clean eating and increased consumer awareness of agricultural practices and their environmental impact. According to data from the Specialty Food Association, organic food has become mainstream, particularly among younger demographics such as millennials and Generation Z (Gen Z), who prioritize sustainability and health in their purchasing decisions. Additionally, organic certifications from the United States Department of Agriculture (USDA) and other international organizations provide credible third-party validation, enhancing the premium positioning and reliability of organic products. These certifications assure consumers of adherence to stringent standards in organic farming and production processes. As this trend progresses, organic products are expected to gain a larger market share, supported by the maturation of supply chains and cost reductions driven by economies of scale, which will further improve accessibility and affordability for consumers.

By Packaging Type: Single-Serve Formats Capture Convenience Demand

In 2025, glass jars command the largest share of the packaging market at 36.95%. This dominance is bolstered by consumer perceptions linking glass to quality, sustainability, and a premium image, justifying its higher price points. Glass packaging not only offers enhanced product protection and an extended shelf life but also aligns with the growing trend of environmental consciousness due to its recyclability. On the other hand, squeezable plastic formats cater adeptly to the convenience segment, especially for families with children and those on-the-go. Yet, it's the single-serve portion packs that are witnessing the most rapid ascent, projected to grow at a 6.07% CAGR through 2031. This surge underscores a rising consumer preference for portion control, convenience, and trial-size offerings.

This inclination towards single-serve aligns seamlessly with evolving snacking habits and a heightened awareness of portion management, especially among urbanites in search of quick breakfast and snack options. Highlighting the industry's commitment to food security, Novolex's TamperFlag container innovations underscore the importance of tamper-evident features, bolstering consumer trust in single-serve offerings. As sustainability takes center stage, manufacturers are increasingly gravitating towards compostable and recyclable alternatives, moving away from conventional plastic packaging. The regulatory landscape, too, champions packaging innovation, with FDA approvals for food contact substances and environmental compliance frameworks steering material choices and labeling mandates.

By Distribution Channel: E-commerce Accelerates Amid Traditional Retail Dominance

In 2025, supermarkets and hypermarkets command a leading distribution position, holding a 41.98% market share. Their success stems from broad geographic reach, competitive pricing, and the allure of one-stop shopping, resonating with mainstream consumers. These outlets leverage strong supplier ties, efficient logistics, and promotional strategies, boosting sales across standard product categories. Meanwhile, convenience stores target urban shoppers and impulse buys, and other channels, like specialty food shops and farmers' markets, focus on premium and artisanal offerings.

Online retail stores are on a growth trajectory, boasting a 5.69% CAGR through 2031. This surge is fueled by shifts in shopping habits post-pandemic and the allure of home delivery. E-commerce platforms break down traditional retail barriers, allowing specialty and artisanal producers to tap into wider markets, especially for niche and premium products. The digital realm is a boon for organic and specialty segments, where consumers hunt for specific brands and attributes. In a nod to the e-commerce wave, Walmart debuted its "bettergoods" private-label specialty line in 2024, underscoring traditional retailers' pivot towards premium offerings. Online sales must adhere to established food safety and labeling norms, but also need to navigate extra shipping and storage regulations during transit.

Geography Analysis

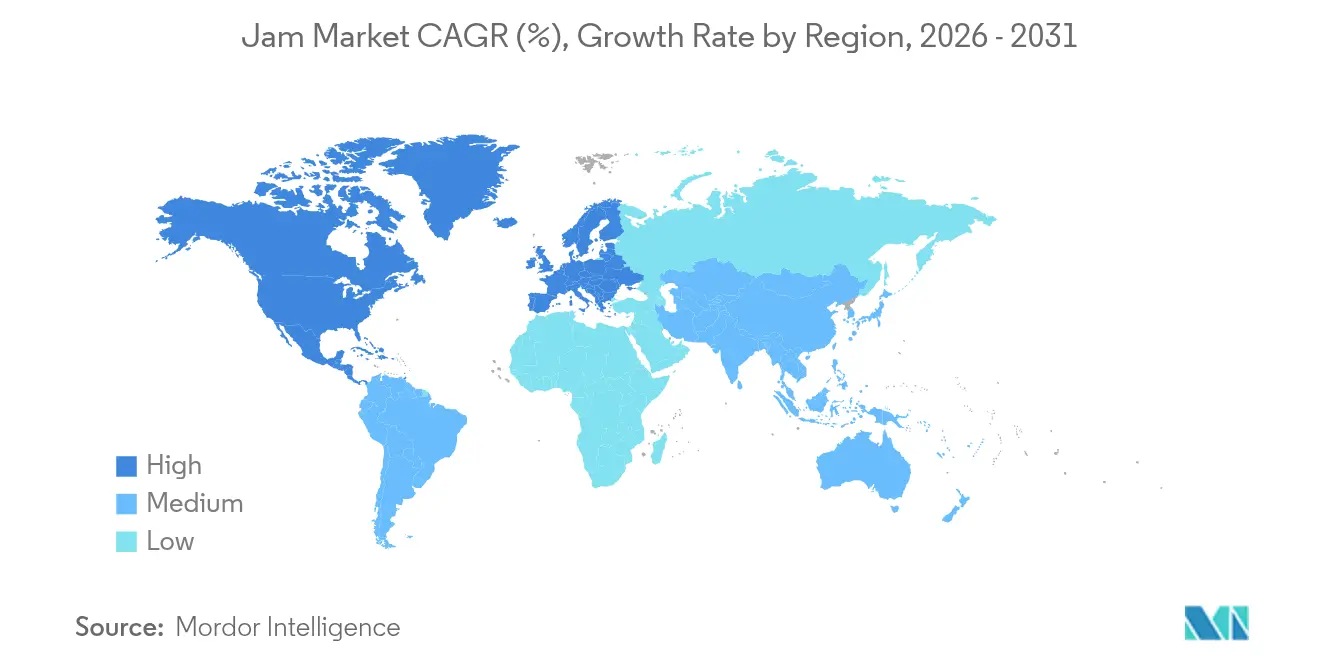

In 2025, North America emerges as the leading segment, commanding a significant 41.70% share of the market. This dominance is attributed to the region's strong brand equity and a deeply ingrained breakfast culture. The rising focus on wellness trends has spurred the introduction of reduced-sugar products and functional spreads, often enriched with ingredients such as chia seeds or added fiber. Retailers are actively refining their shelf layouts to strike a balance between traditional family staples and premium artisanal offerings. This strategic approach not only encourages consumer experimentation but also safeguards the core demand by mitigating the risk of product cannibalization.

The Asia-Pacific region is the fastest-growing segment, with a robust Compound Annual Growth Rate (CAGR) of 5.38% projected through 2031. This growth is driven by factors such as increasing disposable incomes, rapid urbanization, and a growing inclination towards Western breakfast habits. Local companies are innovating by blending traditional and novel flavors, introducing mango and lychee preserves alongside classic berry options. Government investments in cold-chain infrastructure have significantly reduced spoilage, enabling wider distribution networks. Additionally, international brands are tailoring their flavor portfolios to align with regional preferences, ensuring greater resonance with local consumers.Europe continues to play a vital role in the market, supported by its long-standing tradition of marmalade consumption and a strong preference for organic products. The region benefits from the European Union's (EU) cohesive regulatory framework, which simplifies cross-border trade and provides mid-sized brands with opportunities for scalability. Sustainability concerns are driving innovation, with manufacturers adopting recycled-content glass and designing lighter, narrow-neck jars to reduce emissions. Furthermore, the region's linguistic diversity has led to a heightened emphasis on comprehensive labeling, reflecting a commitment to transparency and fostering consumer trust.

Regulatory Landscape

Jam, jelly, and preserves manufacturers operate under tightening food safety, labeling, and residue-compliance regimes that increasingly require auditable data and supplier documentation across global fruit supply chains. In the United States, FDA priorities for 2026 include reforms to food substance regulation and greater transparency, while FSMA-based preventive controls and traceability expectations continue to shape plant recordkeeping and supplier verification for fruit ingredients, sweeteners, and processing aids. GFSI-benchmarked certification schemes used by retailers and foodservice, including FSSC 22000, also continue to update requirements, strengthening standardized food safety management systems and documentation discipline for co-packers and brand owners.

Competitive Landscape

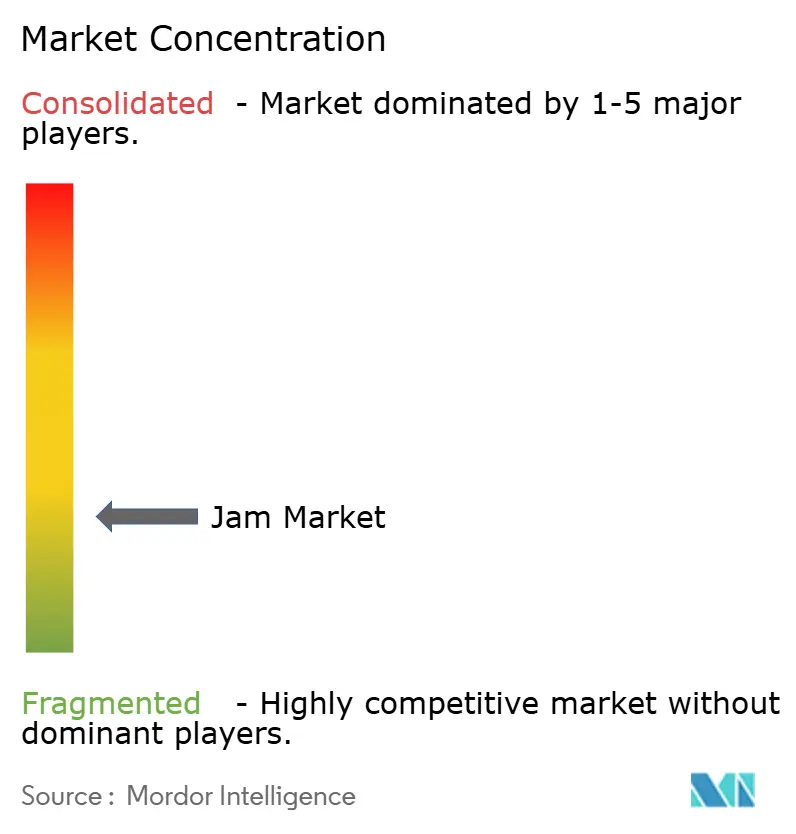

The market structure is moderately fragmented. Global giants like J.M. Smucker use their scale to secure prime retail placements and negotiate better input contracts. Their acquisition of Hostess Brands in 2024 broadens their reach into breakfast and cross-merchandising. Bonne Maman, with its French heritage and distinctive jar design, ensures high shelf visibility. Meanwhile, regional players highlight their origins—like Tasmanian berries and Andalusian oranges—to connect with local consumers.

Innovation focuses on flavor depth, sugar alternatives, and sustainable packaging. Provisur Technologies’ STS 2000 refiner helps both artisanal and industrial processors achieve a cleaner, fruit-forward profile without compromising on throughput. Novolex’s tamper-proof containers expand single-serve choices in foodservice. Data analytics in digital commerce enable niche brands to swiftly spot flavor gaps and introduce limited batches.

Strategic divestitures underscore a sharpened portfolio focus. J.M. Smucker’s decision to sell Bick’s pickles for USD 20 million in 2025 reallocates resources to its primary coffee and sweet-spread lines. Midas Foods’ acquisition of J.M. Exotic Foods brings in seasoning expertise, potentially paving the way for innovative savory-sweet spread hybrids. Co-packing agreements empower smaller brands to scale while retaining their artisanal touch, fostering a vibrant competitive landscape.

Jam Industry Leaders

-

The J.M. Smucker Company

-

Andros Group

-

B&G Foods Inc.

-

Orkla ASA

-

Hero Group

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Reduced-sugar, sugar-free, and clean-label reformulation remains a key opportunity area, supported by both consumer behavior shifts and the compliance environment around labeling, additives, and ingredient transparency. Large branded players are already aligning portfolios with cleaner label cues, including The J.M. Smucker Company's June 2025 commitment to remove FD&C colors from its consumer food products, including sugar-free fruit spreads, by the end of 2027. That agenda creates room for alternative sweetener systems such as stevia, monk fruit, and allulose, along with fruit-forward recipes that help preserve taste and texture while simplifying ingredient decks.

Manufacturers are also using operational modernization and packaging-led differentiation to manage labor constraints, hygiene requirements, and rising sustainability costs. Industry programs are pushing digital adoption and factory optimization, including Enterprise Singapore and IMDA's February 2026 update to the Food Manufacturing Industry Digital Plan (aimed at guiding 1,500 manufacturers) and PMMI and FPSA's 2026 Processing State of the Industry work on investment priorities such as hygienic design, workforce development, and digital tools. For jam and preserves, these efforts are showing up in traceability-ready data systems, recipe and quality management, and packaging upgrades, including portion-controlled formats and tamper-evident solutions, designed for e-commerce shipping, foodservice needs, and premium positioning.

Recent Industry Developments

- July 2026: A media report spotlighted Polaner jams, jellies, and fruit spreads production at B&G Foods' Roseland, New Jersey facility. The feature highlighted the durability of established U.S. manufacturing footprints in supporting shelf-stable spreads distribution and brand continuity while modernizing operations.

- June 2025: Smucker announced a commitment to remove FD&C colors from consumer foods, including sugar-free fruit spreads, with an end-2027 target. The move signals a broad reformulation agenda across branded products and sets the stage for reformulation roadmaps in the category.

- November 2024: Crofters Organic launched an organic squeezable pouch format for jams and preserves in the United States. The range was offered in Berry Harvest and Strawberry and positioned with 33% less sugar than conventional preserves, expanding convenience-led packaging and potentially affecting on-the-go consumption and category dynamics.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of jam, jelly, and preserves sold for household and foodservice use, counted at the point of sale into retail and foodservice channels, and tracked in USD across major consuming regions.

Scope exclusions: We exclude fresh fruit spreads made and sold informally (unregistered cottage sales) and non-fruit savory spreads that are not marketed as jam, jelly, or preserves.

Segmentation Overview

-

By Product Type

- Jams and Jellies

- Marmalade

- Preserves

-

By Category

- Conventional

- Organic

-

By Packaging Type

- Glass Jars

- Squeezable Plastic

- Single-Serve Portion Packs

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Online Retail Stores

- Other Distribution Channels

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Rest of South America

-

Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Sweden

- Belgium

- Poland

- Netherlands

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Thailand

- Singapore

- Indonesia

- South Korea

- Australia

- New Zealand

- Rest of Asia-Pacific

-

Middle East and Africa

- United Arab Emirates

- South Africa

- Saudi Arabia

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set market boundaries, build the initial demand pool, and pressure test assumptions with public benchmarks. We referred to sources such as USDA and Economic Research Service publications for processed fruit and sugar-related context, UN Comtrade for trade flows of relevant prepared fruit products, and FAOSTAT for upstream fruit availability signals that can affect supply conditions.

To translate these signals into a workable sizing model, we also reviewed national statistics offices and customs authorities for category definitions, plus trade associations and food standards bodies for labeling and identity rules that separate jam, jelly, and preserves. Company annual reports, investor decks, and reputable press were used to understand channel mix changes, pricing actions, and promotional intensity. Where needed, a paid subscription for company financials and a shipment-level import and export database were used to cross-check manufacturer exposure by geography and to sanity check the direction of trade-linked volumes. These desk research sources are illustrative only, and other public documents and datasets were also referenced for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on gaps public datasets cannot answer cleanly, including how products get classified in different markets and how pricing moves through retail versus foodservice. We spoke with a mix of brand-side leaders, distributors, retail category teams, and industry specialists across APAC, EMEA, and the Americas, and the responses were used to confirm demand indicators, typical pack sizes, and the realistic pace of premiumization and sugar-reduction shifts.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 15% | APAC: 42% |

| Mid tier: 40% | Functional/Unit leaders: 33% | EMEA: 35% |

| Smaller Players: 21% | Managers: 52% | Americas: 23% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where consumption is reconstructed from a demand pool that blends population, per capita intake patterns for bread and breakfast occasions, and the penetration of packaged fruit spreads in retail baskets. We then corroborate totals using selective bottom-up checks, including sampled brand portfolios, channel checks, and an ASP times volume view built from typical jar sizes and observed shelf price ranges.

A few inputs mattered in this market: household penetration of spreads, the split between conventional and better-for-you variants, distribution mix shifts between supermarkets and online, and pricing progression tied to fruit input costs and sugar inflation. Because some countries report prepared fruit categories in broader groupings, we handled gaps by applying interview-validated allocation keys, then rechecking results against trade direction, shelf-space signals, and manufacturer footprint by region. Forecasts were developed using scenario analysis supported by short-series trend smoothing, with the base case anchored on expected inflation normalization, premiumization pace, and channel growth trajectories that experts considered realistic for the next five years.

Data Validation & Update Cycle

Outputs were cross-checked against independent signals such as trade movements, regional consumption cues, and implied per household spend, then exceptions were reviewed until the variance was reasonable in plain terms. When a country result looked too high or too low, we rechecked category boundaries, currency timing, and the assumed mix of premium versus value products, and we re-contacted sources when the explanation was not strong enough.

Before sign-off, the model is reviewed in multiple steps so calculation logic, unit consistency, and regional roll-ups match the stated scope. Reports are refreshed annually, and interim updates are triggered when material events occur, such as sharp input cost swings or major labeling changes. Right before delivery, a final pass is done so clients receive the most current view available.

Mordor Intelligence's Jam Jelly and Preserves Market Size Versus Other Published Estimates

Published market sizes for jam, jelly, and preserves can vary widely, even when they appear to cover the same category. These differences typically trace back to what is counted as in-scope, the starting year used by each publisher, and how pricing and currency are handled across countries.

By tracking category boundaries and price progression by channel, then refreshing currency conversion timing, Mordor Intelligence keeps the estimate tied to packaged jam, jelly, and preserves sold through defined retail and foodservice routes, rather than mixing in broader prepared fruit products. Some sources also use a narrower geographic set, or they rely on a single base-year revenue snapshot without verifying whether volumes and pack sizes align with typical consumption behavior.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 13.28 B (2026) | |

| Global Consultancy A | USD 1.87 B (2024) | The scope appears narrower, with totals that align more with a limited product or channel definition, and the base year is earlier, which can compress value if inflation and premiumization are not carried through consistently. |

| Industry Publisher B | USD 2.40 B (2025) | The estimate likely uses a tighter inclusion set and a longer forecast window, and it may rely more on high-level revenue baselines without the same level of channel-level price and pack-size checks across regions. |

The spread across publishers is mainly explained by what gets counted as jam, jelly, and preserves, plus how price and currency are applied across markets. Our approach stays repeatable because each step is tied to clear demand indicators, channel logic, and a small set of assumptions that can be rechecked and updated as conditions change.

Key Questions Answered in the Report

What is the forecast value of global jam sales by 2031?

The category is expected to reach USD 16.51 billion by 2031, growing at a 4.45% CAGR.

Which product segment is expanding fastest?

Preserves are on pace for a 5.57% CAGR owing to whole-fruit textures and premium positioning.

Which region shows the strongest growth momentum?

Asia Pacific leads with a 5.38% CAGR through 2031, driven by rising incomes and urbanization.

How large is the online retail share today?

E-commerce currently accounts for a 5.69% CAGR growth, quickly eroding the dominance of physical retail.

What packaging innovation addresses tamper concerns?

Novolex’s TamperFlag single-serve packs feature built-in tamper evidence and recycled content.

Are organic spreads gaining importance?

Yes, organic variants are growing at a 6.25% CAGR as consumers seek clean-label credentials.

Page last updated on: