Percutaneous Coronary Intervention Guidance Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.14 Billion |

| Market Size (2031) | USD 3.33 Billion |

| Growth Rate (2026 - 2031) | 9.23% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Percutaneous Coronary Intervention Guidance Devices Market Analysis by Mordor Intelligence

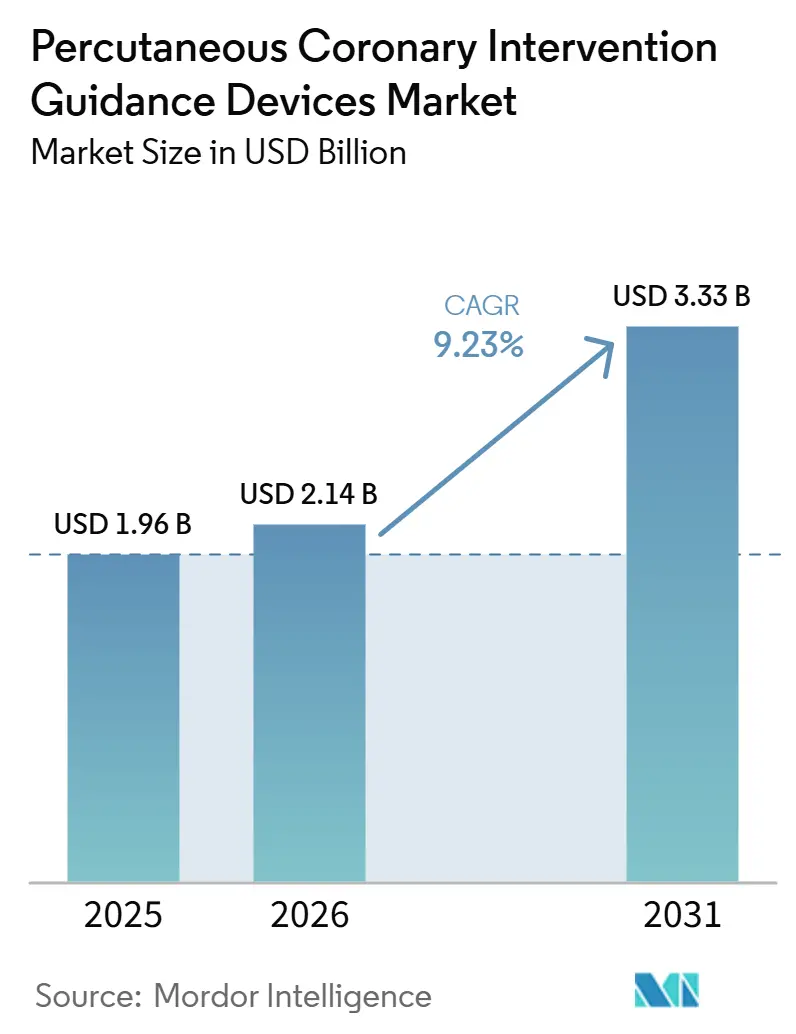

The Percutaneous Coronary Intervention Guidance Devices Market size is projected to expand from USD 1.96 billion in 2025 and USD 2.14 billion in 2026 to USD 3.33 billion by 2031, registering a CAGR of 9.23% between 2026 to 2031.

The percutaneous coronary intervention guidance devices market is moving into a more standardized adoption cycle because major cardiology guidelines now treat intravascular imaging as a core part of complex PCI rather than an optional add-on. Demand is also being reinforced by the rising burden of calcified and chronic total occlusion lesions, where angiography alone often misses lesion severity and where imaging-guided treatment improves measurable outcomes. The commercial case is becoming stronger as integrated consoles combine IVUS, OCT, and physiology guidance on one platform, while AI tools reduce interpretation time and help operators make more consistent sizing and planning decisions. Reimbursement support in mature markets continues to favor adoption in complex cases, especially in settings where hospitals can align imaging use with coding and payment structures. Even so, the percutaneous coronary intervention guidance devices market still faces uneven uptake because catheter cost, software monetization limits, and workforce shortages continue to slow broader use outside high-volume centers.

Key Report Takeaways

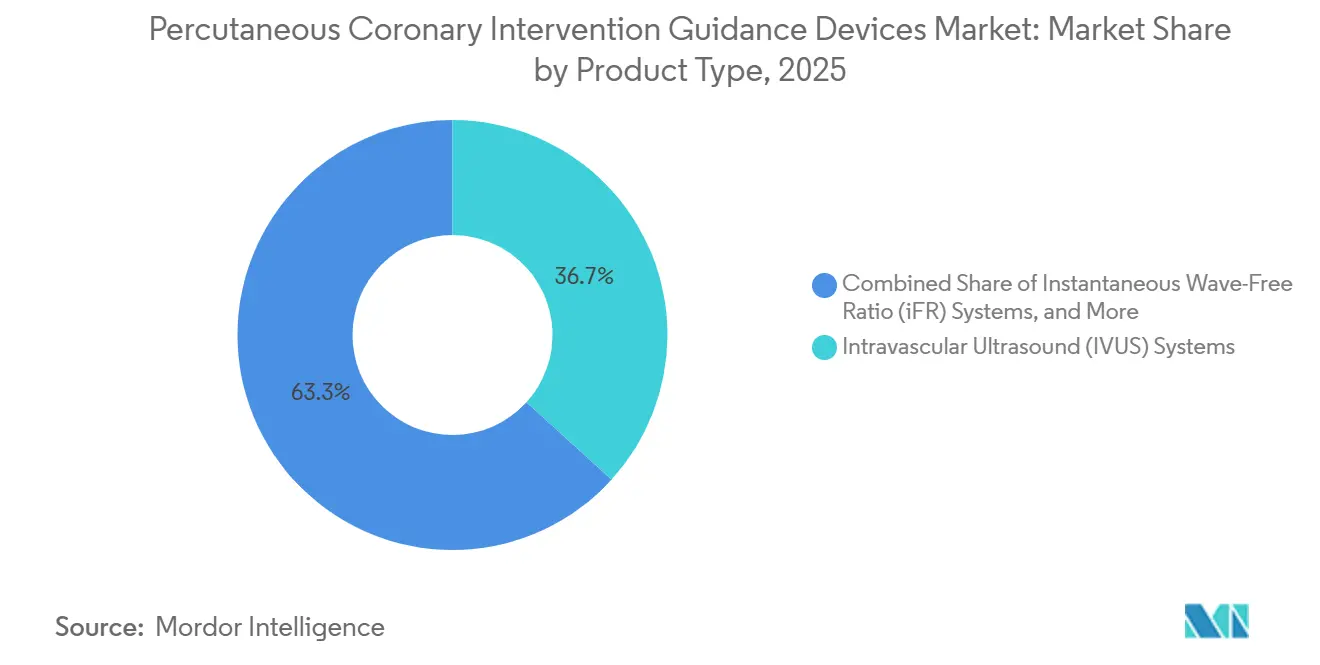

- By product type, intravascular ultrasound systems led with 36.74% revenue share in 2025, while iFR systems are projected to expand at a 10.45% CAGR through 2031 in the percutaneous coronary intervention guidance devices market.

- By technology, IVUS-based guidance held 34.68% share in 2025, while FFR and iFR physiological guidance are forecast to grow at a 12.89% CAGR through 2031.

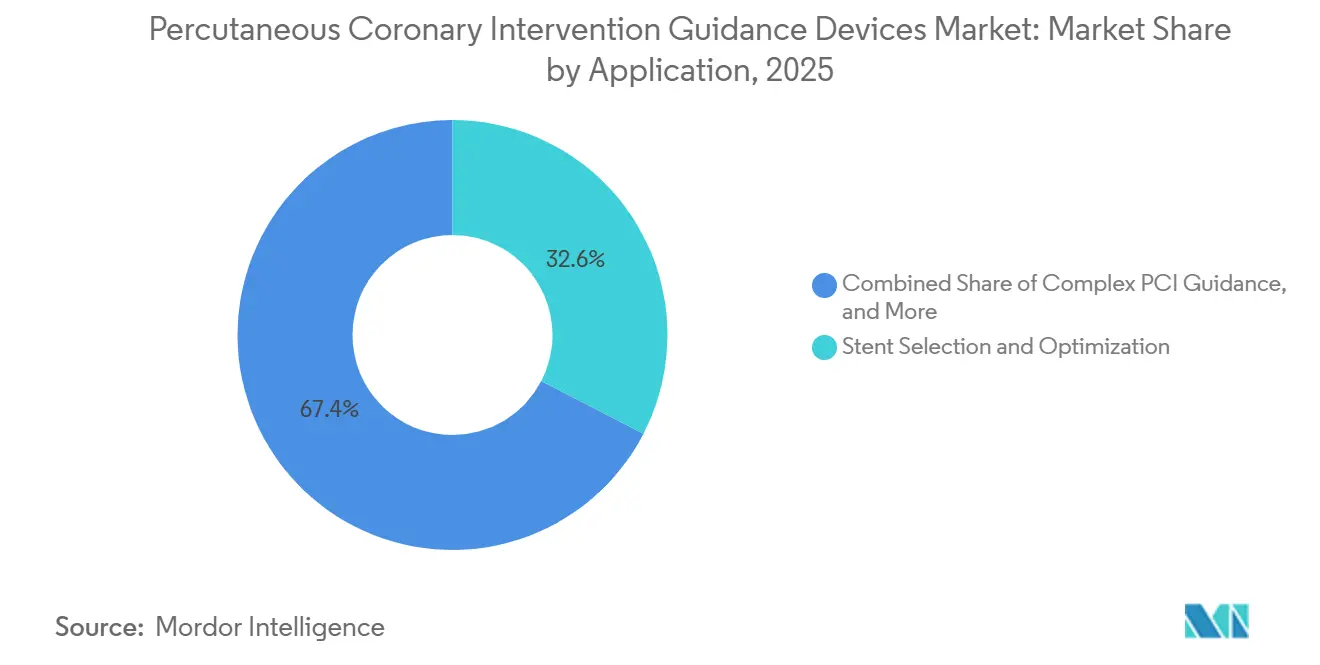

- By application, stent selection and optimization accounted for 32.59% share in 2025, while complex PCI guidance is advancing at a 11.72% CAGR through 2031 in the percutaneous coronary intervention guidance devices market.

- By end user, hospitals held 60.43% share in 2025, while ambulatory surgical centers are projected to record a 13.67% CAGR through 2031.

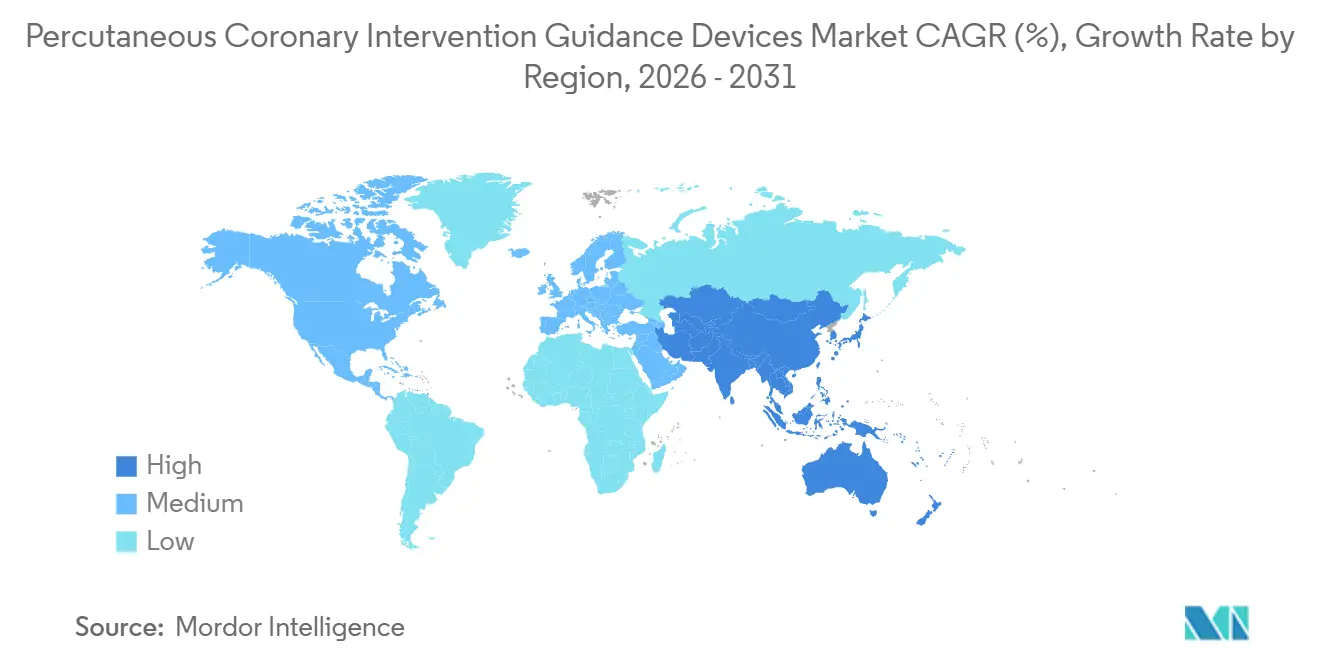

- By geography, North America captured 39.58% in the percutaneous coronary intervention guidance devices market in 2025, while Asia-Pacific is projected to expand at 14.73% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Percutaneous Coronary Intervention Guidance Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Burden of Complex Lesions and Calcified Disease | +2.2% | Global, strongest in aging populations across North America, Europe, and Japan | Medium term (2-4 years) |

| Shift Toward Image-Guided and Physiology-Guided PCI | +2.0% | Global, with early gains concentrated in North America and Europe | Short term (≤ 2 years) |

| AI-Assisted Lesion Assessment and Workflow Automation | +1.8% | North America and Europe leading, with spillover to core Asia-Pacific markets | Medium term (2-4 years) |

| Reimbursement Support for Intravascular Imaging | +1.6% | North America, Western Europe, and Japan | Short term (≤ 2 years) |

| Hybrid IVUS-OCT and Multimodality Console Adoption | +1.4% | North America and Europe, with early gains in South Korea and Japan | Medium term (2-4 years) |

| Cath Lab Standardization in Tertiary Centers | +1.0% | Core Asia-Pacific, with spillover to the Middle East, Africa, and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Burden of Complex Coronary Lesions and Calcified Disease

The percutaneous coronary intervention guidance devices market is benefiting from a larger pool of patients with calcified and anatomically complex lesions that are difficult to assess with angiography alone. Moderate to severe calcification is present in 20% to 30% of patients undergoing invasive coronary angiography, and prevalence rises sharply in older men, which keeps imaging demand structurally tied to aging populations.[1]“Calcific Coronary Lesions, Management, Challenges, and a Comprehensive Review,” The same pattern appears in chronic total occlusion treatment, where the PROGRESS-CTO Registry reported moderate or severe calcification in 49.6% of lesions across 16,916 CTO PCI procedures enrolled between 2012 and 2025.[2] “Calcium Modification Strategies in Treatment of Calcified Coronary Chronic Total Occlusions, Insights from the PROGRESS-CTO Registry,” Clinical evidence has also become harder for hospitals to ignore because the ECLIPSE Trial showed that intravascular imaging guidance lowered 1-year target vessel failure to 9.3% from 13.2% in severely calcified lesions. That outcome keeps the percutaneous coronary intervention guidance devices market tied not only to procedure volume growth, but also to the rising share of procedures that require better lesion preparation, calcium scoring, and post-stent assessment.

Shift Toward Image-Guided and Physiology-Guided PCI

The percutaneous coronary intervention guidance devices market is also being lifted by a wider shift from angiography-only workflows toward imaging-guided and physiology-guided PCI. Integrated systems now let physicians access IVUS, OCT, and pressure-based tools on one console, which reduces setup burden and supports more consistent cath lab workflows. A 2025 meta-analysis covering 22 clinical trials found that intravascular imaging-guided PCI reduced cardiac death by 45%, target lesion failure by 29%, and definite stent thrombosis by 48% against angiography guidance alone.[3]“Artificial Intelligence in Intravascular Imaging for Percutaneous Coronary Interventions, A New Era of Precision,” The OCTIVUS Trial also showed that patients who achieved stent optimization had a 52% relative reduction in target vessel failure, and the benefit was strongest under OCT guidance.[4]“Impact of Artificial Intelligence-Enhanced Optical Coherence Tomography Software on Percutaneous Coronary Intervention Decisions,” These results are changing procurement behavior because hospitals now see guidance platforms as tools that support both better outcomes and closer compliance with updated practice standards.

AI-Assisted Lesion Assessment and Workflow Automation

AI is becoming a practical adoption driver in the percutaneous coronary intervention guidance devices market because it reduces the time and expertise needed to interpret pullbacks and complete procedural planning. The strongest immediate value is workflow efficiency, since lower-volume programs often hesitate to use intravascular imaging when interpretation depends on a small number of highly experienced operators. A 2025 study found that Abbott’s Ultreon AI-OCT system improved stent sizing accuracy by 2.83 times and reduced interpretation time against conventional software. The FLASH Trial also demonstrated non-inferiority of AI-QCA-assisted PCI to OCT-guided PCI in post-procedural minimal stent area across 400 patients in 13 South Korean centers. As a result, the percutaneous coronary intervention guidance devices market is starting to expand from a hardware-led category into a software-enabled platform space where efficiency and consistency matter almost as much as image quality.

Reimbursement Support for Intravascular Imaging in Mature Markets

The percutaneous coronary intervention guidance devices market continues to gain from payment structures that reward imaging use in the most complex procedures. In the United States, the FY2026 inpatient payment framework kept separate payment support for IVUS and FFR in the hospital inpatient setting, while stented PCI MS-DRG payments reached USD 22,929. CMS also finalized new complex PCI code 92930 for 2026, which gives greater recognition to multi-lesion and bifurcation work where intravascular guidance is most often used. Japan remains the clearest example of how reimbursement can change clinical behavior, with more than 80% of PCI procedures performed under intravascular imaging guidance. This keeps the percutaneous coronary intervention guidance devices market more responsive to policy design in mature systems than many other device categories.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital and Recurring Catheter Cost | -1.8% | Global, most acute in price-sensitive emerging markets | Short term (≤ 2 years) |

| Shortage of Trained Interventional Cardiologists | -1.4% | North America and Europe, with rising relevance in South Asia | Medium term (2-4 years) |

| Variable Reimbursement and Prior Authorization Friction | -1.0% | Asia-Pacific outside Japan and South Korea, the Middle East, Africa, and South America | Long term (≥ 4 years) |

| Limited Reimbursement for Adjunct Analytics Software | -0.8% | North America and Western Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital and Recurring Catheter Cost

The percutaneous coronary intervention guidance devices market remains constrained by the full ownership cost of consoles, software, and single-use catheters. Hospitals do not only evaluate the base platform price, but they also judge whether recurring catheter use can be justified across a broad PCI caseload under bundled payment structures. Boston Scientific’s 2026 reimbursement guide notes that IVUS and FFR are not separately billable in ambulatory surgical centers, which leaves institutions to recover costs through coding structures that many ASC administrators still find difficult to use. That issue is even more acute in emerging markets, where capital budgets are tighter, and imaging is reserved for the highest-risk cases rather than normalized across routine procedures. As a result, the percutaneous coronary intervention guidance devices market still depends heavily on premium hospitals and referral centers that can support both hardware acquisition and steady disposable pull-through.

Shortage of Trained Interventional Cardiologists

Workforce limits are another structural restraint on the percutaneous coronary intervention guidance devices market because procedure growth cannot accelerate if trained operators do not keep pace. The 2025 interventional cardiology fellowship match left 71 positions unfilled across 49 programs, which SCAI described as evidence of a shrinking trainee pipeline. This shortage has a direct effect on guidance adoption because advanced imaging and physiology tools are used most consistently by teams with stronger training depth and case volume. The same gap is also pushing hospitals toward AI-enabled systems that can help less experienced operators interpret pullbacks and plan stent sizing more efficiently. Even so, the percutaneous coronary intervention guidance devices market cannot fully offset the impact of staffing shortages when recruitment, retention, and training remain under pressure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: IVUS Dominance Sustains While Wire-Free Physiology Closes the Gap

Intravascular ultrasound systems accounted for 36.74% of the percutaneous coronary intervention guidance devices market share in 2025, which kept IVUS as the leading product type. That lead reflected long physician familiarity, a mature catheter supply chain, and strong use in ostial and left-main disease, where OCT flush requirements can limit practicality. The segment also benefited from the shift toward higher-definition IVUS catheters in complex PCI, where physicians want deeper vessel assessment together with clearer plaque and calcium visualization. OCT remained the second-largest product category, and comparative evidence continued to narrow perceived outcome differences between the two modalities. A 2024 meta-analysis across 6 randomized controlled trials and 4,402 patients found no significant difference between OCT-guided and IVUS-guided PCI in MACE, cardiac mortality, or stent thrombosis.

The percutaneous coronary intervention guidance devices market is seeing its fastest product-type momentum in iFR systems, which are projected to grow at a 10.45% CAGR through 2031. The main appeal is the adenosine-free workflow, since it reduces procedure time, avoids added drug use, and simplifies the protocol for routine physiology assessment. FFR systems still hold a complementary role, but the competitive pressure around wire-free and angio-derived options is becoming clearer. The FLAVOUR II Trial published in 2025 showed that an angiography-derived FFR-guided strategy was non-inferior to IVUS guidance for 12-month clinical outcomes, which supports a gradual shift away from some wire-based cases. Accessories and disposables remain central to the percutaneous coronary intervention guidance devices industry because guidewires, imaging catheters, and flush kits keep recurring revenue tied closely to console placement and physician loyalty.

By Technology: Physiological Guidance and AI Expand the Platform Mix

IVUS-based guidance held a 34.68% technology share in 2025, supported by its installed base and its practical value in lesions that need plaque burden and calcification depth assessment. The modality remains especially important in cases where OCT contrast flushing is less suitable, which gives IVUS a durable role in more complex coronary anatomy. This leadership also reflects the fact that many hospitals have already built their workflow around IVUS consoles before the current wave of AI and multimodality launches. At the same time, the technology mix is widening as hospitals compare image-led guidance with physiology-led strategies for selected lesions. This leaves the percutaneous coronary intervention guidance devices market less dependent on a single guidance method than it was only a few years ago.

FFR and iFR physiological guidance is forecast to grow at a 12.89% CAGR through 2031, which makes it the fastest-growing technology group. The CathWorks ALL-RISE Trial, presented at ACC.26, randomized 1,930 patients across 59 global sites and showed that FFRangio delivered similar clinical outcomes to invasive wire-based physiology assessment. AI-enabled PCI guidance is also becoming more credible as a technology layer rather than a marketing feature. A study in the Journal of the Society for Cardiovascular Angiography & Interventions found that Abbott’s Ultreon AI platform produced more accurate, less variable, and more time-efficient PCI planning decisions than conventional software across operator experience levels. This shift gives the percutaneous coronary intervention guidance devices industry a broader competitive field, where imaging depth, physiology integration, and software productivity all influence capital spending decisions.

By Application: Complex PCI Becomes the Highest-Growth Clinical Use Case

Stent selection and optimization contributed 32.59% of application revenue in 2025, which made it the largest use case in the percutaneous coronary intervention guidance devices market. This position is logical because post-stent sizing, expansion, and apposition checks are the clearest point at which intravascular guidance can show immediate procedural value. The OCTIVUS Trial reinforced that value by showing that stent optimization was linked to a 52% relative reduction in target vessel failure. Hospitals can therefore justify imaging use more easily when the benefit is tied directly to a measurable procedural endpoint. This application remains the base layer of demand because it connects clinical improvement, physician confidence, and payment support in the most visible way.

Complex PCI guidance is projected to expand at a 11.72% CAGR in the percutaneous coronary intervention guidance devices market through 2031, making it the fastest-growing application. Growth is tied to the rising share of multi-vessel disease, bifurcations, left-main interventions, and calcified lesions in contemporary PCI caseloads. The 2025 guideline upgrade for intravascular imaging in complex and left-main PCI within acute coronary syndrome has strengthened this shift by treating advanced guidance as standard practice in high-risk anatomy. Lesion assessment is also gaining relevance as AI software automates plaque characterization and calcium measurement, and deep-learning tools have already shown expert-comparable plaque segmentation in validated OCT datasets. CTO and bifurcation planning remain more specialized, but AI-based planning tools described in 2025 also showed reduced procedural time and radiation exposure, which may gradually widen adoption beyond expert centers.

By End User: Outpatient Migration Reshapes Buying Patterns

Hospitals held 60.43% of end-user revenue in 2025, which kept them as the core buyer group in the percutaneous coronary intervention guidance devices market. Their lead rested on the concentration of cath lab infrastructure, credentialed operators, and reimbursement pathways for complex PCI in tertiary and academic centers. Hospitals also remain the primary setting for left-main, bifurcation, and heavily calcified cases, which are the procedures most likely to use advanced imaging and physiology tools. This gives large health systems continued influence over platform placements, upgrade cycles, and preferred vendor ecosystems. In the near term, hospital demand still anchors most revenue because complex care pathways and capital budgets remain concentrated there.

Ambulatory surgical centers are projected to grow at a 13.67% CAGR through 2031, which makes them the fastest-growing end-user category and the most important new procurement channel. A MedPAC review found that cardiology was the fastest-growing ASC specialty between 2018 and 2023, and CMS added 86 new cardiovascular procedure codes to the ASC Covered Procedures List in 2026. A nationwide study also found that ASC procedural volume is expected to rise by 21% between 2024 and 2034, while the American College of Cardiology launched its Cardiovascular ASC Registry Suite in early 2024. These changes matter for the percutaneous coronary intervention guidance devices market size because vendors will need smaller-footprint systems, simpler workflows, and different pricing models for outpatient economics. Specialty cardiology centers and standalone catheterization laboratories remain smaller in scale, but they add a growing layer of demand in settings that value procedural efficiency and flexible capital deployment.

Geography Analysis

North America held 39.58% of the percutaneous coronary intervention guidance devices market share in 2025, which kept it as the largest regional contributor. The region benefits from mature reimbursement architecture, a dense base of high-volume PCI centers, and the commercial presence of the leading platform vendors. U.S. guideline changes continue to support capital and consumable demand because hospitals increasingly link imaging use with expected standards of care in complex PCI. Payment support also remains stronger here than in most other regions, even if coding details still vary by site of care. Canada and Mexico add to regional volume, though procurement timelines and uneven tertiary access still limit the pace of broader adoption.

Europe remained the second-largest region in 2025, with Germany, France, and the United Kingdom acting as the main centers for advanced intravascular guidance use. The region combines an established interventional cardiology base with growing demand for system refreshes as older platforms approach replacement cycles. Philips strengthened its European position in March 2026 by launching IntraSight Plus with both FDA and CE marks, which supports hospitals seeking a combined IVUS and physiology workflow on one screen. Adoption is still uneven across the region because high-volume centers move faster than community hospitals where capital constraints keep angiography-guided practice more common.

Asia-Pacific is projected to grow at a 14.73% CAGR in the percutaneous coronary intervention guidance devices market size through 2031, making it the fastest-growing region. Japan remains the benchmark market because more than 80% of PCI procedures are already performed under intravascular imaging guidance. That level of use shows how reimbursement alignment and clinical culture can reinforce each other over time. The broader region also benefits from procedural volume growth, expanding cath lab infrastructure, and rising interest in integrated and hybrid platforms. South Korea is important because it has contributed pivotal evidence in AI-assisted PCI workflow validation, including the FLASH Trial. India and Southeast Asia remain longer-conversion markets where private hospital networks are adding capability, but reimbursement support for adjunct imaging is still inconsistent. The Middle East and Africa are growing from a small base, led by tertiary investment in Gulf countries and early adoption in South Africa. South America remains anchored by Brazil, though reimbursement limits and approval friction still constrain wider use across public systems.

Competitive Landscape

The percutaneous coronary intervention guidance devices market remains moderately concentrated around a small group of global platform vendors. Abbott, Philips, and Boston Scientific control most of the installed console base and account for a large share of recurring catheter demand, which gives them meaningful pricing and procurement influence. Their position is reinforced by broad product portfolios that combine consoles, catheters, guidewires, and software in one ecosystem. This structure raises switching costs for hospitals because a platform decision often shapes disposable purchasing and staff workflow for several years. Even so, the category is no longer closed, because hybrid imaging specialists and software-focused entrants are now pushing into specific clinical and workflow gaps.

Strategic activity in 2025 and 2026 showed how quickly the competitive field is evolving. Philips agreed to acquire SpectraWAVE in December 2025, adding DeepOCT-NIRS imaging and X1-FFR angiography-based physiology to its portfolio. Abbott then received FDA clearance and CE mark for Ultreon 3.0 in April 2026, introducing a 1-second pullback and more automated AI-supported insights for coronary imaging. Philips also launched IntraSight Plus in March 2026, which sharpened competition around integrated IVUS, iFR, FFR, and co-registration workflows.

A second layer of competition is emerging around hybrid imaging and software-led guidance. Terumo completed the first U.S. procedure with OPUSWAVE in June 2026, signaling a more direct challenge in dual-sensor imaging for high-volume centers. CathWorks strengthened the case for angiography-derived physiology with the ALL-RISE Trial, which supported broader commercial credibility for wire-free assessment. These moves suggest that future share gains may come from better workflow integration and software usability, not only from image quality alone. The percutaneous coronary intervention guidance devices market therefore remains top-heavy at the installed-base level, but still open enough for targeted innovation to alter procedure mix, replacement cycles, and premium pricing in selected segments.

Percutaneous Coronary Intervention Guidance Devices Industry Leaders

Abbott Laboratories

Boston Scientific Corporation

Esaote S.p.A.

Koninklijke Philips N.V.

Terumo Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Terumo Corporation completes first US procedure with OPUSWAVE dual-sensor imaging system. The OFDI+IVUS DualView catheter procedure, performed at Mount Sinai Fuster Heart Hospital by Dr. Annapoorna Kini, marks Terumo's commercial entry into the US intravascular imaging market, where it aims to leverage its established Japan leadership into high-volume US tertiary centers.

- April 2026: Abbott Laboratories receives FDA clearance and CE mark for Ultreon 3.0 AI-powered OCT imaging platform. The platform introduces 1-second pullback, AI-automated plaque characterization, and enhanced stent sizing workflows, directly targeting complex calcified cases and bifurcation interventions where accurate pre-procedural planning is most consequential.

- March 2026: Koninklijke Philips N.V. launched IntraSight Plus interventional guidance platform. The redesigned platform unifies Class IA IVUS, direct iFR/FFR measurement, co-registration, tri-registration, and real-time device visualization on a single screen, with claims of 47% reduction in system operation time. It is FDA 510(k) cleared and CE marked.

Global Percutaneous Coronary Intervention Guidance Devices Market Report Scope

As per the scope of the report, percutaneous coronary intervention (PCI) guidance devices are specialized tools used during coronary angioplasty to visualize, measure, and guide stent placement or balloon dilation inside coronary arteries. They include intravascular ultrasound (IVUS), optical coherence tomography (OCT), and fractional flow reserve (FFR) systems, which provide real‑time imaging and physiological assessment. These devices improve accuracy, safety, and patient outcomes by enabling precise lesion characterization and optimized intervention planning.

The percutaneous coronary intervention (PCI) guidance devices are segmented by product type, technology, application, end user, and geography. By product type, the market is segmented into intravascular ultrasound (IVUS) systems, optical coherence tomography (OCT) systems, fractional flow reserve (FFR) systems, iFR systems, hybrid IVUS-OCT systems, accessories, and disposables. By technology, the market is segmented into IVUS-based guidance, OCT-based guidance, FFR/iFR physiological guidance, AI-enabled PCI guidance, and others. By application, the market is segmented into lesion assessment, stent selection and optimization, post-PCI expansion assessment, complex PCI guidance, and others. By end user, the market is segmented into hospitals, ambulatory surgical centers, specialty cardiology centers, cardiac catheterization laboratories, and others. The geography segment is further divided into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market size and forecasts in value (USD) for the above segments.

| Intravascular Ultrasound (IVUS) Systems |

| Optical Coherence Tomography (OCT) Systems |

| Fractional Flow Reserve (FFR) Systems |

| iFR Systems |

| Hybrid IVUS-OCT Systems |

| Accessories and Disposables |

| IVUS-Based Guidance |

| OCT-Based Guidance |

| FFR/iFR Physiological Guidance |

| AI-Enabled PCI Guidance |

| Others |

| Lesion Assessment |

| Stent Selection and Optimization |

| Post-PCI Expansion Assessment |

| Complex PCI Guidance |

| Others |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Cardiology Centers |

| Cardiac Catheterization Laboratories |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Intravascular Ultrasound (IVUS) Systems | |

| Optical Coherence Tomography (OCT) Systems | ||

| Fractional Flow Reserve (FFR) Systems | ||

| iFR Systems | ||

| Hybrid IVUS-OCT Systems | ||

| Accessories and Disposables | ||

| By Technology | IVUS-Based Guidance | |

| OCT-Based Guidance | ||

| FFR/iFR Physiological Guidance | ||

| AI-Enabled PCI Guidance | ||

| Others | ||

| By Application | Lesion Assessment | |

| Stent Selection and Optimization | ||

| Post-PCI Expansion Assessment | ||

| Complex PCI Guidance | ||

| Others | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Cardiology Centers | ||

| Cardiac Catheterization Laboratories | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving growth in percutaneous coronary intervention guidance devices through 2031?

Growth is being supported by rising use of imaging-guided and physiology-guided PCI, more complex calcified lesions, and stronger reimbursement support in mature markets. The category is projected to grow from USD 2.14 billion in 2026 to USD 3.33 billion by 2031 at an 9.23% CAGR.

Why is IVUS still leading over other product types?

IVUS held 36.74% of revenue in 2025 because physicians are familiar with it, hospitals already have installed systems, and it remains practical in left-main and calcified disease.

Which technology is expanding the fastest in coronary guidance platforms?

FFR and iFR physiological guidance is projected to grow at a 12.89% CAGR through 2031, helped by simpler workflows and stronger evidence for angiography-derived and wire-free assessment options.

Why are complex PCI cases so important for device demand?

Complex PCI guidance is the fastest-growing application at a 11.72% CAGR because left-main, bifurcation, multi-vessel, and calcified lesions increasingly require better lesion preparation and optimization tools.

How is the shift toward ambulatory surgical centers changing vendor strategy?

ASCs are projected to grow at a 13.67% CAGR, which means vendors will need smaller systems, easier workflows, and pricing models suited to outpatient economics.

Which region offers the strongest long-term expansion opportunity?

Asia-Pacific is forecast to grow at a 14.73% CAGR through 2031, supported by rising procedural volume, expanding cath lab capacity, and strong adoption benchmarks in Japan.

Page last updated on: