Carcinoembryonic Antigen (CEA) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.31 Billion |

| Market Size (2031) | USD 3.12 Billion |

| Growth Rate (2026 - 2031) | 6.24% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Carcinoembryonic Antigen (CEA) Market Analysis by Mordor Intelligence

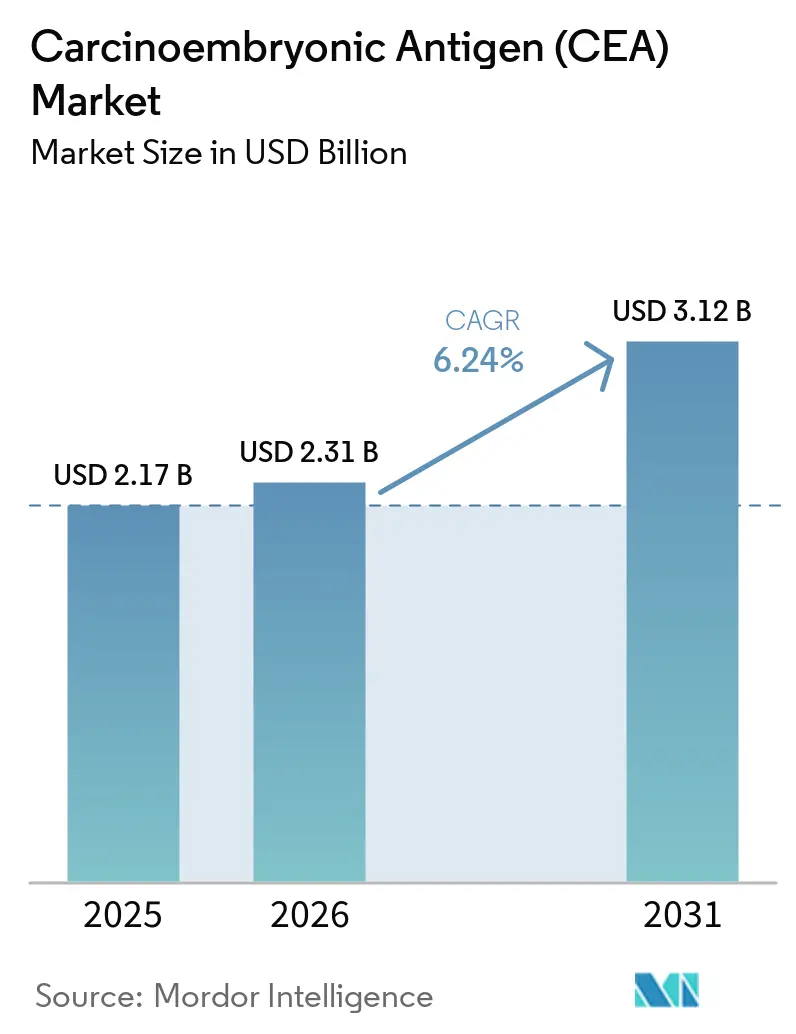

The Carcinoembryonic Antigen (CEA) market size is expected to increase from USD 2.17 billion in 2025 to USD 2.31 billion in 2026 and reach USD 3.12 billion by 2031, growing at a CAGR of 6.24% over 2026-2031. Diagnostic laboratories, hospitals, and research institutes are scaling up biomarker testing volumes as colorectal cancer incidence climbs in both developed and emerging regions. Advances in high-sensitivity multiplex immunoassays, wider regulatory acceptance of liquid biopsy, and national cancer-screening initiatives are broadening clinical adoption of CEA-based monitoring. At the same time, large manufacturers are bundling assay kits with automated analyzers and AI-driven software to streamline workflows, while start-ups focus on ultra-fast point-of-care formats. Strategic partnerships around companion diagnostics signal an increasingly collaborative competitive environment in which assay commoditization places margin pressure on legacy products.

Key Report Takeaways

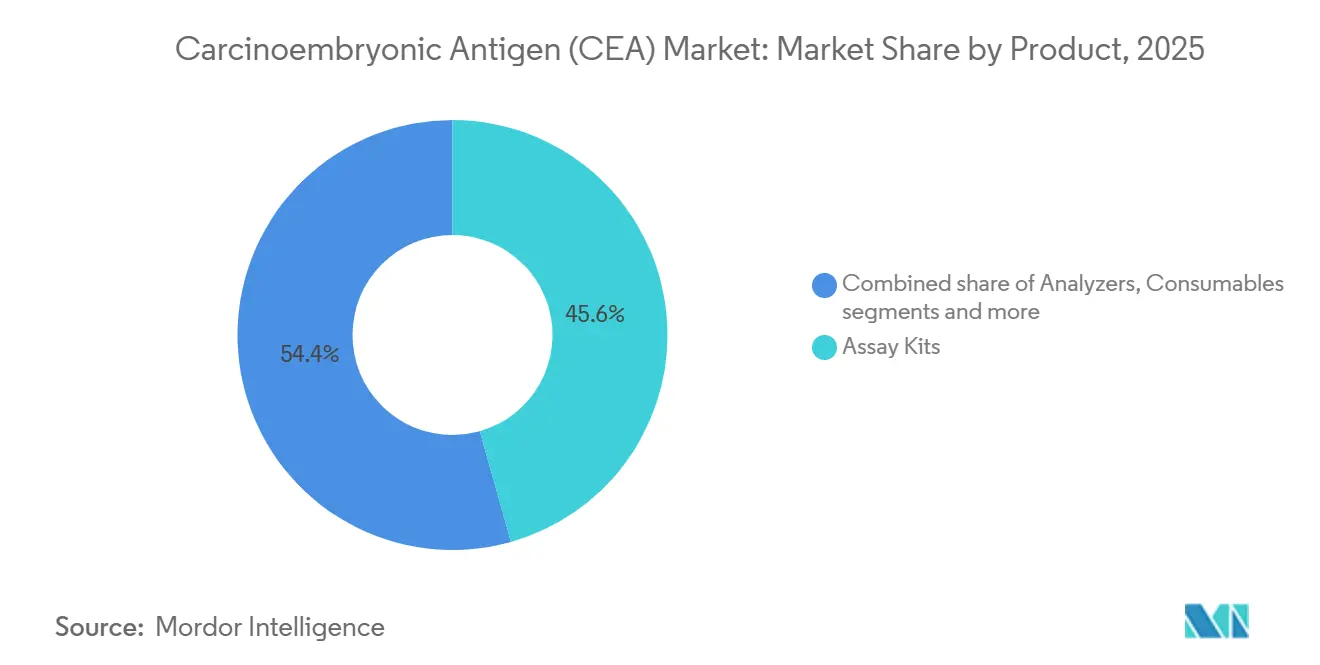

- By product, assay kits captured 45.62% of the Carcinoembryonic Antigen (CEA) market share in 2025; consumables and reagents are projected to post the fastest 7.21% CAGR through 2031.

- By application, colorectal cancer generated 44.05% of the Carcinoembryonic Antigen (CEA) market share in 2025, while liver cancer is advancing at a 7.07% CAGR to 2031.

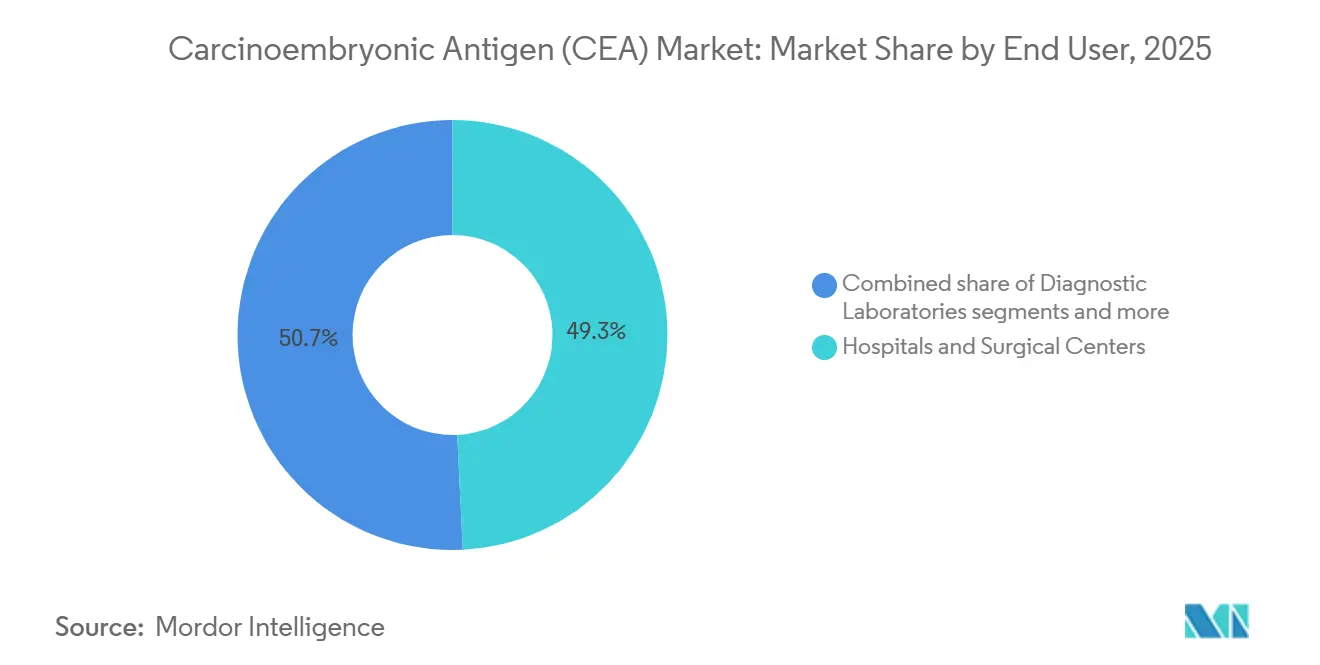

- By end user, hospitals and surgical centers held 49.25% of the Carcinoembryonic Antigen (CEA) market share in 2025; diagnostic laboratories record the highest projected CAGR at 6.95% through 2031.

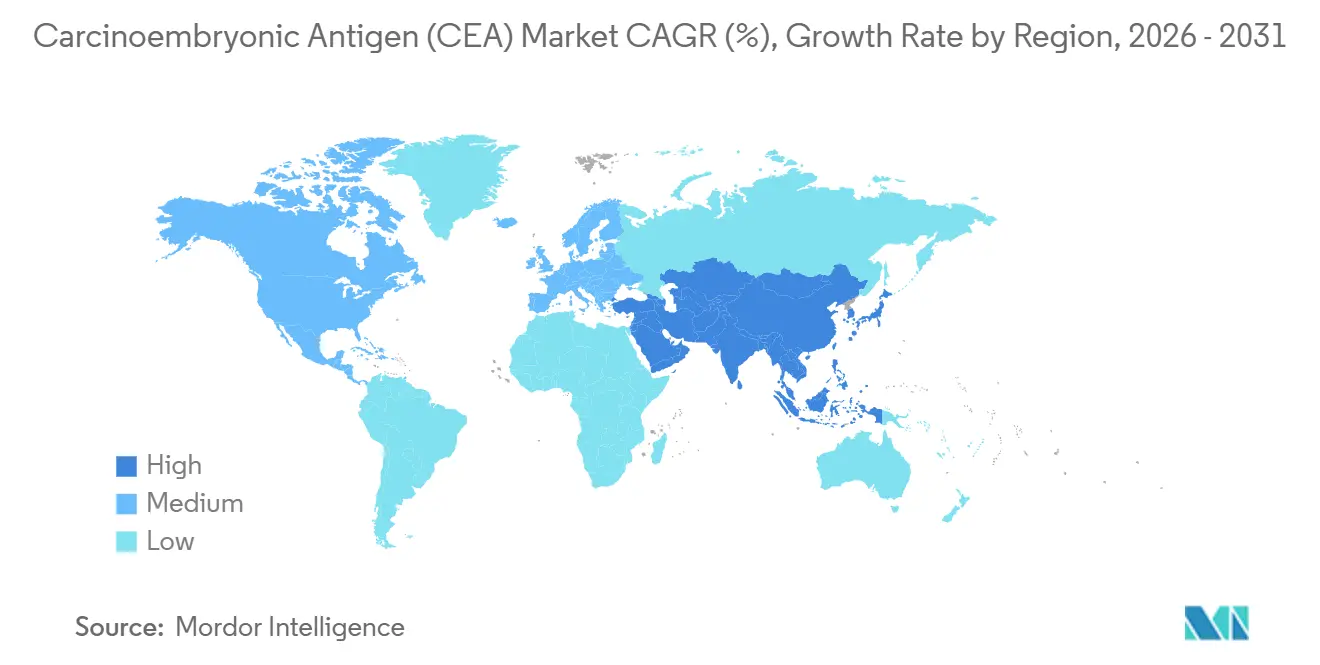

- By geography, North America led with 41.86% of the Carcinoembryonic Antigen (CEA) market share in 2025, whereas Asia-Pacific is set to expand at a 6.82% CAGR over the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Carcinoembryonic Antigen (CEA) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating global colorectal cancer prevalence | +1.8% | Global, with highest impact in Asia-Pacific and North America | Long term (≥ 4 years) |

| Shift toward minimally-invasive biomarker-based monitoring | +1.2% | Global, led by developed markets | Medium term (2-4 years) |

| Technological advances in high-sensitivity multiplex immunoassays | +0.9% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Expanding government-funded cancer screening programs in Asia-Pacific | +0.7% | APAC core, with spillover to emerging markets | Long term (≥ 4 years) |

| Rising demand for companion diagnostics in biologics trials | +0.6% | North America & EU, with APAC adoption | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating Global Colorectal Cancer Prevalence

Rising colorectal cancer incidence is a structural growth catalyst for the CEA market. China alone reported about 4.8 million new cancer cases in 2022, with colorectal malignancies among the top contributors Lifestyle shifts toward Western diets, ageing populations, and improved detection are enlarging the addressable patient pool across Asia-Pacific and North America. Healthcare systems now embed CEA measurement into routine surveillance, as seen in Thailand’s two-step FIT-plus-CEA program that feeds patients into colonoscopy pathways . Clinicians value CEA for its 80% sensitivity in identifying liver metastases, reinforcing its role in longitudinal monitoring . As screening participation rises, test volumes—and thus consumable pull-through—scale proportionally. This dynamic sustains baseline growth even when adoption of competing genomic tools accelerates.

Shift Toward Minimally-Invasive Biomarker-Based Monitoring

Physicians show mounting preference for blood-based assays that lower procedural burden while sustaining diagnostic accuracy. The FDA approval of the Shield test in 2024, which detects colorectal cancer with 83% sensitivity, exemplifies this non-invasive trend [1]Source: Center for Devices and Radiological Health, “Shield – P230009,” fda.gov . Capillary-blood micro-collection devices now match venous-draw accuracy, enabling frequent outpatient testing without phlebotomy queues. Post-operative surveillance protocols increasingly replace imaging with serial CEA measurement, reducing patient exposure to radiation and cost. Patient adherence improves materially when follow-up requires a finger-stick rather than a colonoscopy, and AI algorithms that analyze CEA trajectories are further elevating clinical confidence. These factors collectively widen the clinical window for early intervention and reinforce recurring reagent demand.

Technological Advances in High-Sensitivity Multiplex Immunoassays

Next-generation platforms deliver sub-nanogram detection while measuring several oncology proteins in one run, reshaping value propositions in the CEA market. Nanopore-linked ELISAs have achieved 500 ng/mL limits of detection and multiplex up to four markers simultaneously. Hybrid microfluidic “paper-in-polymer-pond” plates push sensitivity to 0.32 ng/mL with shorter assay times . Laboratories adopt these systems to profile CA19-9, AFP, and NSE alongside CEA, creating richer clinical context without extra sample volume. Surface-enhanced Raman spectroscopy further enhances signal-to-noise, allowing detection in early-stage disease. Vendors that integrate multiplex capability with automated throughput gain strategic advantage as oncologists pivot toward holistic biomarker panels.

Expanding Government-Funded Cancer Screening Programs in Asia-Pacific

Public health agencies across China, Japan, and Thailand are rolling out mass-screening initiatives that budget for biomarker tests, inserting predictable volume into the CEA market. China’s latest prevention blueprint explicitly endorses blood-based tumor markers for early detection. Japan recommends endoscopic checks every two years for adults over 50, with follow-up CEA monitoring for positive findings. Thailand’s FIT-first strategy funnels high-risk individuals into biomarker surveillance backed by cost-effectiveness modeling showing superior quality-adjusted life-years when CEA is included. Government reimbursement reduces out-of-pocket expense, spurring institutional procurement of assay kits and analyzers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited specificity of CEA leading to false positives | -1.4% | Global, with higher impact in screening applications | Medium term (2-4 years) |

| Competition from emerging genomic & proteomic biomarkers | -0.8% | North America & EU, expanding globally | Long term (≥ 4 years) |

| Pricing pressure from assay commoditization | -0.6% | Global, with highest impact in cost-sensitive markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Specificity of CEA Leading to False Positives

Despite ubiquity, CEA suffers non-malignant elevation in smokers, diabetics, and patients with benign polyps, producing false-positive rates as high as 99.5% within the 5.1–10 ng/mL band [KAMJE.ORG]. In routine surveillance, nearly half of colorectal cancer survivors record sporadic CEA spikes unrelated to relapse, driving unnecessary imaging and patient anxiety.

Laboratories therefore adopt reflex testing algorithms that delay clinical action until sequential rises are confirmed, but this lengthens turnaround and raises cost. The specificity shortfall limits CEA utility in population screening, confining its core value to treatment monitoring. Research now orients toward multi-analyte models that blend CEA with ctDNA or proteomic signatures to mitigate erroneous positives.

Competition from Emerging Genomic & Proteomic Biomarkers

Liquid biopsy assays targeting circulating tumor DNA detect minimal residual disease up to two years earlier than imaging, eroding the comparative advantage of CEA. Multi-cancer early-detection blood tests report stage-I sensitivities exceeding 90% with 99% specificity, setting new performance benchmarks. Pharma companies favor genomic companion diagnostics that link directly to actionable mutations, limiting CEA to adjunctive monitoring roles. AI-powered proteomics platforms extract hundreds of protein features at once, offering richer insights than a single-marker readout. As reimbursement frameworks evolve, payers may funnel funds toward higher-value genomic tests, challenging price elasticity for legacy CEA assays.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Standardization Keeps Assay Kits in Front

Assay kits commanded 45.62% market share in 2025, reflecting their central role in standardizing CEA testing across diverse laboratory environments. The dominance of assay kits stems from their comprehensive nature, providing complete testing solutions that ensure reproducibility and regulatory compliance across different healthcare settings. However, the consumables and reagents segment is projected to grow at 7.21% CAGR through 2031, driven by increasing test volumes and the recurring revenue model inherent in consumables. Analyzers and instruments represent the smallest segment but provide the technological foundation for high-throughput CEA testing, with companies like BD launching advanced platforms such as the FACSDiscover A8 Cell Analyzer featuring breakthrough spectral and real-time imaging technologies.

The shift toward automation and high-throughput testing is reshaping product demand patterns, with Siemens Healthineers focusing on human-centered engineering in laboratory automation to enhance diagnostic workflows and reduce manual intervention requirements . Point-of-care testing platforms are emerging as a disruptive force, with bioMérieux's acquisition of SpinChip Diagnostics in January 2025 bringing immunoassay technology that delivers results from whole blood samples in 10 minutes. This technological evolution is creating new product categories that blur traditional boundaries between assay kits, instruments, and consumables, as integrated platforms offer complete testing solutions with minimal user intervention.

By Application: Colorectal Cancer Dominates, Liver Cancer Accelerates

Colorectal cancer commanded 44.05% of demand in 2025, anchoring the CEA market. The biomarker’s 80% sensitivity for hepatic metastatic spread cements its role in peri-operative management, while guideline updates in North America and Europe recommend quarterly monitoring during the first two surveillance years. Liver cancer testing, though smaller, is set for a 7.07% CAGR as clinicians deploy CEA to stratify hepatocellular carcinoma prognosis and track post-ablation response.

Multi-cancer detection paradigms add complexity: research trials embed CEA within multi-protein classifiers to allocate patients to imaging pathways, broadening its indirect utility. Pancreatic and breast cancer segments use CEA combined with CA 15-3 or CA 19-9 to gauge therapy efficacy, though absolute volumes remain modest. Lung adenocarcinoma studies show CEA’s additive prognostic value when paired with CA-125 and CA-199, hinting at new protocol inclusion . Diversified application breadth supports the CEA market share even as genomic assays penetrate frontline diagnostics.

By End User: Hospitals Hold Ground as Central Labs Gain Speed

Hospitals and surgical centers generated 49.25% of revenue in 2025, reflecting embedded CEA ordering in inpatient oncology pathways. Peri-operative workflows routinely schedule pre- and post-resection serum testing, anchoring volumes within hospital laboratories. Outsourced diagnostic laboratories, however, are growing at 6.95% CAGR as payers encourage centralization for cost efficiency. High-throughput reference labs deploy robotic platforms that batch thousands of assays daily, driving reagent economies of scale and tightening procurement contracts.

Academic and research institutes leverage ultra-sensitive CEA panels during clinical trials, often in tandem with ctDNA analysis, influencing next-generation protocol design. Emerging point-of-care sites—oncology day clinics and ambulatory surgery centers—adopt 10-minute microfluidic cartridges that support rapid treatment decisions. As reimbursement frameworks shift toward bundled payments, healthcare providers seek lower-cost yet high-fidelity testing, prompting competitive tendering that reshapes the CEA market size distribution among end users.

Geography Analysis

North America’s 41.86% revenue share in 2025 underscores deep integration of companion diagnostics, generous insurance coverage, and robust oncology infrastructures. The United States benefits from Medicare reimbursement for CEA monitoring in resected colorectal cancer, while the FDA fast-tracks innovative assays, sustaining technology refresh cycles . Consolidation among private payers pressures laboratories on pricing, yet elevated test volumes keep aggregate revenues stable. Canada and Mexico contribute incremental growth through national screening roll-outs and cross-border reference-lab collaborations.

Asia-Pacific delivers the fastest 6.82% CAGR and will add sizeable absolute value to the CEA market by 2031. China funds multi-cancer screening pilots incorporating blood-based biomarkers, with provincial programs purchasing bulk assay lots under centralized tenders. Japan’s biennial endoscopy plus biomarker monitoring regimen drives sustained kit consumption. India’s AI-augmented oncology diagnostics ecosystem blends affordable multiplex assays with cloud analytics, widening rural access and lifting reagent demand.

Europe shows steady single-digit growth via harmonized health-technology assessment pathways that endorse CEA for surveillance rather than screening. National Health Services negotiate volume-based discounts, nudging vendors toward value-based contracting. South America and the Middle East & Africa remain nascent but promising: improving cancer registries and donor-funded screening pilots will gradually pull CEA test orders upward. Collectively, regional heterogeneity balances the global CEA market, with high-growth emerging markets offsetting mature-region price erosion.

Competitive Landscape

The CEA market exhibits moderate concentration with established players leveraging technological innovation and strategic partnerships to maintain competitive advantages. Abbott Laboratories, F. Hoffmann-La Roche, and Thermo Fisher Scientific dominate through comprehensive diagnostic portfolios and global distribution networks, while emerging players focus on specialized applications and next-generation technologies. The competitive intensity is heightening as companies invest in companion diagnostics development, with BD's partnership with Quest Diagnostics exemplifying the collaborative approach required to bring novel diagnostics to market. Strategic acquisitions are reshaping the landscape, with bioMérieux's acquisition of SpinChip Diagnostics in January 2025 bringing 10-minute immunoassay technology that could disrupt traditional testing workflows[2]Source: LabMedica International, “bioMérieux Acquires SpinChip,” labmedica.com .

White-space opportunities exist in point-of-care testing and artificial intelligence integration, where companies can differentiate through rapid results and enhanced diagnostic accuracy. Siemens Healthineers is advancing laboratory automation through its Atellica Portfolio, which enhances efficiency and reduces turnaround times for diagnostic testing including CEA. Emerging disruptors are focusing on multi-cancer early detection platforms that combine CEA with other biomarkers, potentially commoditizing single-analyte testing while creating new value propositions. The regulatory landscape is evolving to support innovation, with the FDA's phased approach to laboratory developed tests creating clearer pathways for diagnostic approval while maintaining safety standards. Technology adoption is becoming a key differentiator, with companies leveraging automation, artificial intelligence, and advanced analytics to improve testing efficiency and clinical utility.

Carcinoembryonic Antigen (CEA) Industry Leaders

F. Hoffmann-La Roche AG

Laboratory Corporation of America Holdings

Merck KGaA

Quest Diagnostics

Creative Diagnostics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2024: ImmunityBio launched the enrollment and initial follow-up for the safety portions of a clinical trial of a tri-valent combination of antigens delivered by a second-generation Adenovirus vector (Tri-Ad5 CEA/MUC1/brachyury).

- February 2024: Aster Labs launched its new blood test to detect CEA (carcinoembryonic antigen) levels in the blood. CEA is a protein formed by gastrointestinal tissue during fetal development. Its production declines as pregnancy advances and stops before the baby's birth.

Global Carcinoembryonic Antigen (CEA) Market Report Scope

As per the scope of the report, the CEA test quantifies a blood glycoprotein, known as carcinoembryonic antigen (CEA), characterized by an abundance of sugars attached to it by both normal and cancerous cells. Often referred to as a tumor marker or antigen, CEA, like other tumor markers, is produced and released by specific cancer cells into bodily fluids.

The Carcinoembryonic Antigen (CEA) market is segmented by test type, application, end user, and geography. The test type segment is further divided into serology tests and molecular tests. The application segment is further divided into cancer diagnosis and treatment monitoring. By end user, the market is segmented into hospitals, diagnostic centers, and others. The geography segment is further divided into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report offers the value (USD) for all the above segments.

| Assay Kits |

| Analyzers / Instruments |

| Consumables & Reagents |

| Colorectal Cancer |

| Pancreatic Cancer |

| Lung Cancer |

| Breast Cancer |

| Liver Cancer |

| Others |

| Hospitals & Surgical Centers |

| Diagnostic Laboratories |

| Academic & Research Institutes |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Product (Value) | Assay Kits | |

| Analyzers / Instruments | ||

| Consumables & Reagents | ||

| By Application (Value) | Colorectal Cancer | |

| Pancreatic Cancer | ||

| Lung Cancer | ||

| Breast Cancer | ||

| Liver Cancer | ||

| Others | ||

| By End User (Value) | Hospitals & Surgical Centers | |

| Diagnostic Laboratories | ||

| Academic & Research Institutes | ||

| Others | ||

| By Geography (Value) | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the Carcinoembryonic Antigen (CEA) Market?

The Carcinoembryonic Antigen (CEA) Market size is expected to reach USD 2.31 billion in 2026 and grow at a CAGR of 6.24% to reach USD 3.12 billion by 2031.

What is the current Carcinoembryonic Antigen (CEA) Market size?

In 2026, the Carcinoembryonic Antigen (CEA) Market size is expected to reach USD 2.31 billion.

Who are the key players in Carcinoembryonic Antigen (CEA) Market?

F. Hoffmann-La Roche AG, Laboratory Corporation of America Holdings, Merck KGaA, Quest Diagnostics and Creative Diagnostics are the major companies operating in the Carcinoembryonic Antigen (CEA) Market.

Which is the fastest growing region in Carcinoembryonic Antigen (CEA) Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Carcinoembryonic Antigen (CEA) Market?

In 2025, the North America accounts for the largest market share in Carcinoembryonic Antigen (CEA) Market.

What years does this Carcinoembryonic Antigen (CEA) Market cover, and what was the market size in 2025?

In 2025, the Carcinoembryonic Antigen (CEA) Market size was estimated at USD 2.17 billion. The report covers the Carcinoembryonic Antigen (CEA) Market historical market size for years: 2019, 2020, 2021, 2022, 2023, 2024 and 2025. The report also forecasts the Carcinoembryonic Antigen (CEA) Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: