Glyoxal Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

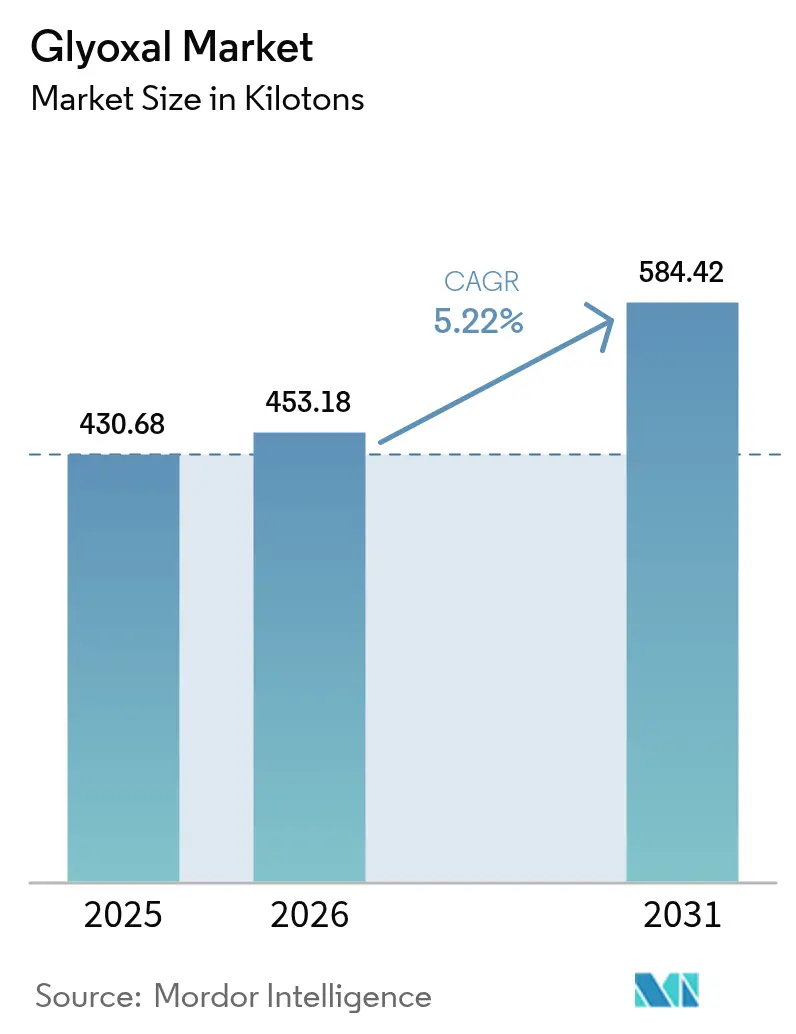

| Market Volume (2026) | 453.18 kilotons |

| Market Volume (2031) | 584.42 kilotons |

| Growth Rate (2026 - 2031) | 5.22% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Glyoxal Market Analysis by Mordor Intelligence

The Glyoxal Market size was valued at 430.68 kilotons in 2025 and estimated to grow from 453.18 kilotons in 2026 to reach 584.42 kilotons by 2031, at a CAGR of 5.22% during the forecast period (2026-2031). Robust demand in textile finishing, water-borne adhesive formulations and nascent battery-electrolyte uses underpins this trajectory, largely because glyoxal’s dual-aldehyde structure delivers stronger, formaldehyde-free cross-linking. Asia-Pacific remains the principal consumption hub, fueled by China’s expanding yarn exports and India’s maturing chemical-intermediates platform. Liquid-solution grades are displacing solid formats in all major applications because automated dosing lines improve batch consistency and reduce processing downtime. Parallel growth in chemical-intermediate synthesis, particularly for pharmaceuticals and specialty materials, broadens the addressable customer base and cushions cyclicality in the textile sector. Rising defense allocations in the United States and BASF’s new Chinese complex underline how supply-chain decentralization and near-shoring strategies are reshaping long-term capacity planning.

Key Report Takeaways

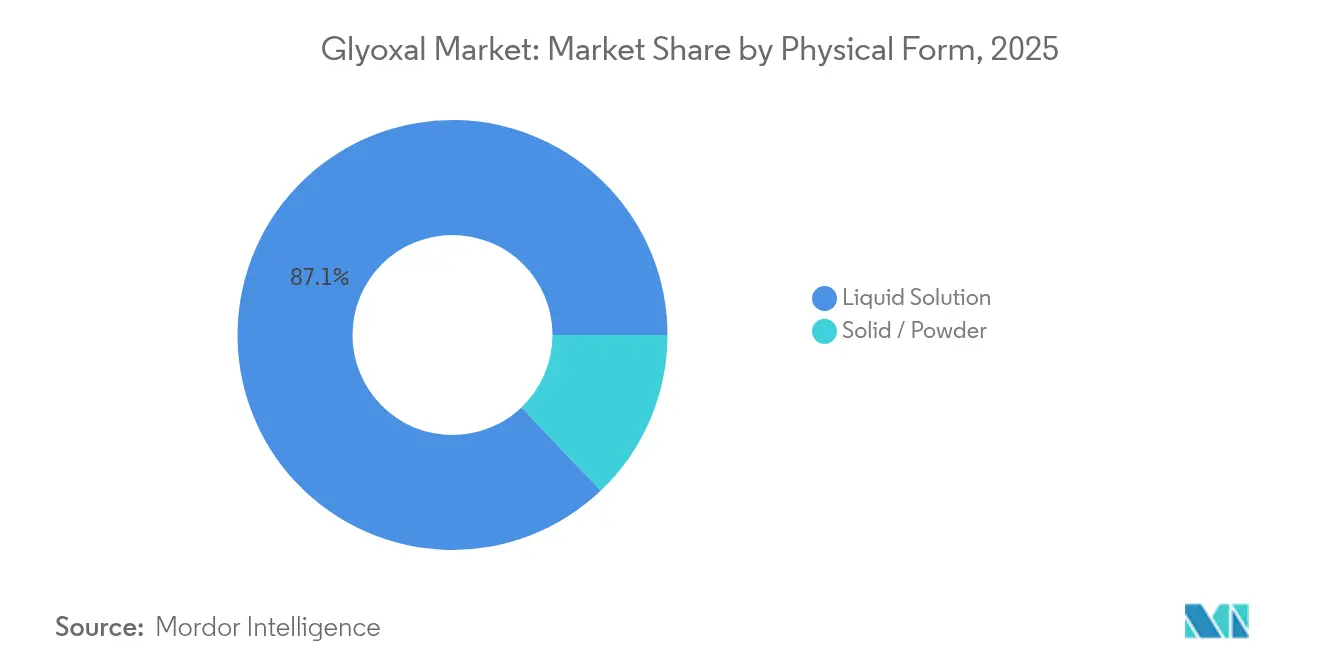

- By physical form, liquid solutions captured 87.12% of glyoxal market share in 2025; solid and powder formats are forecast to post the fastest 6.15% CAGR through 2031.

- By application, cross-linking agents led with a 64.10% revenue share in 2025, while chemical intermediates are projected to advance at a 5.86% CAGR to 2031.

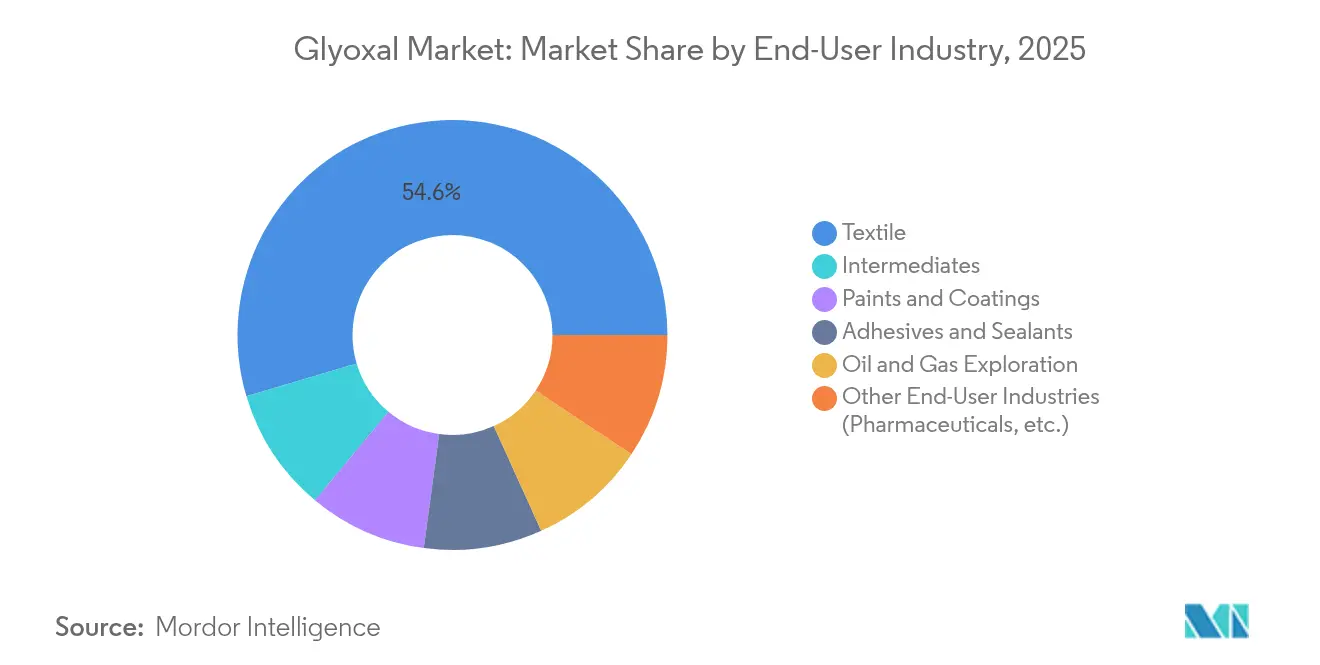

- By end-user industry, textiles accounted for 54.60% of the glyoxal market size in 2025 and intermediates are expanding at a 5.98% CAGR through 2031.

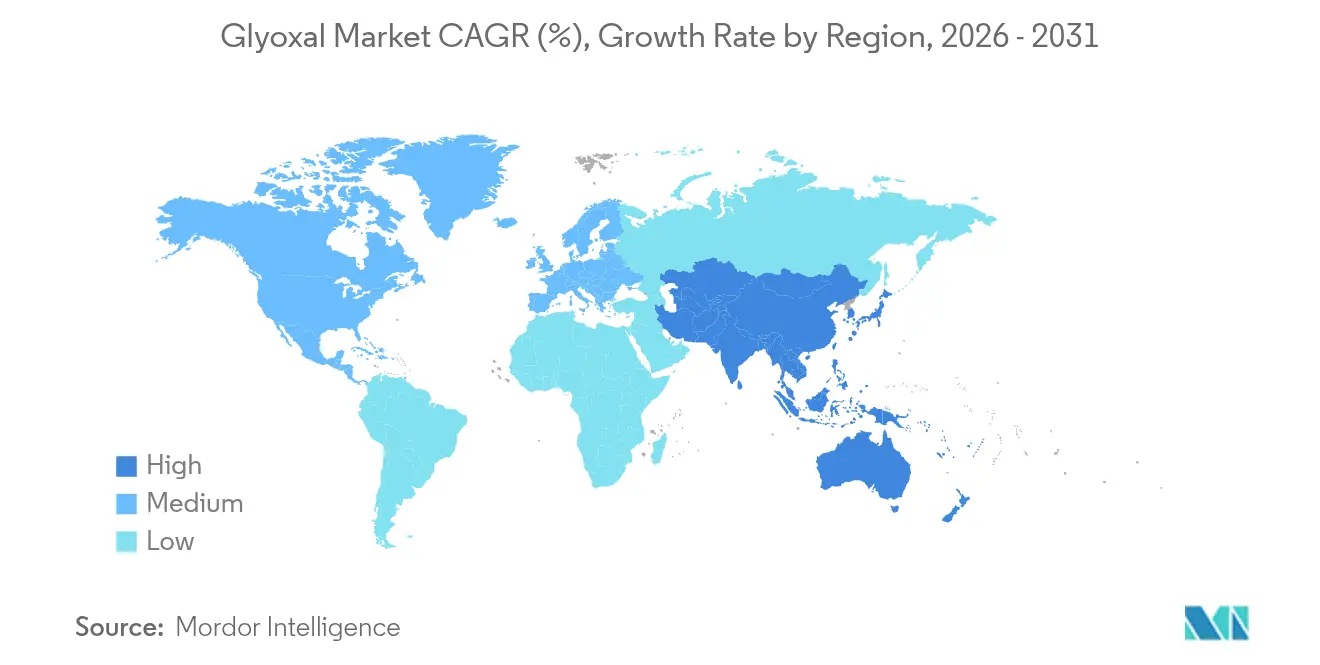

- By geography, Asia-Pacific dominated with 44.55% of the glyoxal market share in 2025; the region is also set to record the highest 6.30% CAGR during the forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Glyoxal Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising textile and apparel production in developing economies | +1.2% | APAC core, spill-over to South America | Medium term (2-4 years) |

| Expanding use as cross-linking agent in water-borne adhesives | +0.8% | Global, with concentration in North America & EU | Short term (≤ 2 years) |

| Growing demand for oil-field chemicals in deep-water drilling | +0.6% | North America, Middle East, offshore regions | Long term (≥ 4 years) |

| Glyoxal adoption as biodegradable biocide in paper and board packaging | +0.5% | EU, North America, with expansion to APAC | Medium term (2-4 years) |

| Emerging role in silicon-anode battery electrolyte formulations | +0.3% | APAC manufacturing hubs, technology centers globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Textile and Apparel Production in Developing Economies

China exported USD 13.7 billion in yarn during 2023, with cotton yarn comprising 70% of shipments, an output scale that necessitates durable-press and antimicrobial finishing aided by glyoxal cross-linking. The compound’s biodegradability meets stricter import regulations in the European Union and North America, making it a preferred alternative to formaldehyde for brands marketing “cleaner” garments. BASF’s Zhanjiang complex, operational from 2025, exemplifies how major suppliers are co-locating capacity in Asia to shorten logistics lanes and capture incremental orders from Vietnam, Bangladesh and India[1]BASF SE, “BASF Starts Up First Plants at Zhanjiang Verbund Site,” basf.com. Medium-term impact is tied to the typical 2-4 year build-out cycle of new spinning and dyeing mills. As these plants scale, glyoxal market demand should parallel fiber throughput because every incremental meter of fabric finished with wrinkle-free or antimicrobial chemistry contains a defined aldehyde loading.

Expanding Use as Cross-Linking Agent in Water-Borne Adhesives

Stringent global emission rules have accelerated the phase-down of solvent-borne wood and paper adhesives, elevating glyoxal’s attractiveness in aqueous systems. Its ability to generate stable hemi-acetal bridges in cellulose substrates allows adhesive formulators to meet low-VOC thresholds without sacrificing bond strength. BASF enacted price increases on diols and derivatives in April 2025, a move that reflects broader raw-material cost inflation and pressures converters to seek more efficient curatives such as glyoxal that enable single-component formulations. The driver exerts short-term impact because adhesive plants retrofit mixers and reactors relatively quickly—typically within a fiscal year—once raw-material approvals are secured. North American building-products makers view glyoxal as a direct pathway to keep ahead of potential formaldehyde re-classification under the EPA’s IRIS program.

Growing Demand for Oil-Field Chemicals in Deep-Water Drilling

Macromolecular gels used in hydraulic fracturing rely on cross-linkers that maintain viscosity at 150 °C and beyond; glyoxal retains reactivity under such extremes, whereas lower-molecular weight aldehydes degrade[2]American Chemical Society, “High-Temperature Fracturing Fluids Using Dialdehydes,” acs.org. Operators in the Gulf of Mexico and the Brazilian pre-salt have begun specifying glyoxal-activated guar and cellulose gels to stabilize fracture networks in ultra-deep wells. Because project sanctioning spans half-decades, the chemical’s requirement profile is locked during early field-development stages, creating predictable offtake volumes over the long term. Middle-Eastern NOCs trialed glyoxal-based diverter fluids in 2024 and initial case studies report 15% higher hydrocarbon flow rates. The slow yet steady pipeline of new offshore projects suggests sustained, albeit niche, volume lift for the glyoxal market through 2030.

Glyoxal Adoption as Biodegradable Biocide in Paper and Board Packaging

European food-contact legislation favors preservatives that decompose rapidly post-use, and glyoxal’s dual action as both cross-linker and antimicrobial aligns with this framework. FDA compliance for resin-coated paper further reassures North American mills that the aldehyde can be incorporated without additional GRAS petitions. Producers of molded fiber trays and cups increasingly deploy glyoxal to reduce spoilage microbes, extending shelf life by 48 hours in fresh-produce trials. Medium-term adoption hinges on packaging converters’ equipment upgrade cycles and on confirming toxicological endpoints in emerging markets. The driver’s 0.5 percentage-point push to global CAGR is therefore anchored in Europe and the United States but will diffuse to APAC printers as multinational consumer-goods companies harmonize packaging specs across regions.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Toxicological concerns and stricter workplace exposure limits | -0.7% | Global, with strictest enforcement in EU & North America | Short term (≤ 2 years) |

| Price volatility of ethylene glycol feedstock | -0.4% | Global supply chains, acute in regions dependent on imports | Short term (≤ 2 years) |

| Competition from dialdehyde starch and other green cross-linkers | -0.3% | EU & North America leading, expanding to APAC markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Toxicological Concerns and Stricter Workplace Exposure Limits

Regulators scrutinize dialdehydes because of potential genotoxicity; WHO’s 2024 review flagged glyoxal for advanced glycation end-product formation, prompting calls to tighten occupational limits. The European Chemicals Agency is reassessing the current 0.1 mg/m³ workplace exposure threshold, and OSHA initiated a parallel data-collection effort that could impose ventilation upgrades costing small mills up to USD 2 million. These compliance costs may drive marginal producers from the market, consolidating supply under better-capitalized companies. Short-term pressure is most acute in Europe and North America, where enforcement staff can audit plants within weeks of new limits taking effect, temporarily dampening production growth.

Price Volatility of Ethylene Glycol Feedstock

Glyoxal output hinges on vapor-phase oxidation of ethylene glycol, itself subject to naphtha and natural-gas price swings. Spot EG prices spiked 23% in Q1 2025 on Middle-East plant turnarounds, compelling glyoxal suppliers to issue USD 70 per-ton surcharges. Producers in Southeast Asia, heavily reliant on imported EG, faced squeezed margins, and several cut operating rates by 10%. Though surcharges typically pass through, converters making price-sensitive textile finishes may substitute lower-performance dialdehyde starch when glyoxal premiums exceed 15%. Short-term volatility thus trims 0.4 percentage points from the forecast CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Physical Form: Liquid Solutions Drive Processing Efficiency

Liquid grades commanded 87.12% of 2025 consumption, reflecting plant-level preferences for pumpable, ready-to-use aldehyde solutions. Automated dosing lowers batch variability and shortens cycle times, factors that have helped the liquid glyoxal market size outpace overall demand at a 5.78% CAGR. Powder forms maintain relevance in remote oil-field operations where weight-based metering and storage stability trump convenience. Growth in containerized textile-chemical “kitchen” installations across Bangladesh and Ethiopia supports continued liquid-grade penetration through 2031. Solid glyoxal derivatives remain important in resin capsules and latency-controlled adhesive kits, but rising freight costs for bulky solids encourage converters to formulate on-site liquids instead.

Processing efficiency explains why liquid solutions remain the preferred specification for fashion, home-textile and technical-fabric producers. Inline pH-controlled injection ensures homogeneous fixation, reducing rework rates by 4% in denim finishing trials. This cost benefit justifies modest price premiums over powders. Moreover, regulations governing shipping of oxidizable solids are tightening; liquids classed as non-combustible enjoy simpler documentation under IMDG rules, a logistics advantage that supports the liquid share’s incremental expansion.

By Application: Chemical Intermediates Accelerate Despite Cross-Linking Dominance

Cross-linking applications still dominated 2025 with a 64.10% share of the glyoxal market, underlining the molecule’s enduring role in durable-press fabrics, paper sizing and water-borne wood glues. Nevertheless, the fastest 5.86% CAGR stems from chemical-intermediate use, reflecting glyoxal’s versatility as a C2 dialdehyde in heterocycle and API synthesis. Pharmaceutical firms exploit it to construct imidazoles and pyrazines, while specialty polymer start-ups condense it into bio-based barrier resins. Pilot plants in India report a threefold rise in glyoxal consumption for pyrimidine intermediates since mid-2024.

Diversification toward intermediates lessens reliance on cyclical textile demand and often yields margins 200 basis points higher than commodity finishing grades. FDA and BfR clearances for food-contact coatings further broaden glyoxal’s utility, allowing film-forming resin producers to address the fast-growing fresh-produce packaging niche. These trends anchor the segment’s acceleration even as cross-linkers remain core volume drivers.

By End-User Industry: Intermediates Segment Outpaces Textile Leadership

Textiles retained 54.60% of 2025 volume because wrinkle-free shirtings, medical apparel and home linens rely on aldehyde fixation to achieve durable hand-feel and antimicrobial persistence. The glyoxal market share of textiles is expected to dilute modestly as the intermediates segment climbs at 5.98% CAGR on the back of broader chemical-synthesis uptake. Adhesives hold steady, aided by construction-grade water-borne polyvinyl-alcohol glues shifting away from formaldehyde. In oil and gas, glyoxal-cross-linked gels feature in high-temperature fracturing fluids where alternative curatives degrade, ensuring a small but lucrative off-take stream.

Pharmaceutical and “other” categories exhibit the sharpest absolute growth, spurred by demand for antibiotic scaffolds and specialty coatings. Their share gains are magnified because end-use pricing can exceed USD 4,000 per ton, more than double textile-grade benchmarks, further buoying overall glyoxal market profitability.

Geography Analysis

Asia-Pacific captured 44.55% of worldwide volume in 2025 and is forecast to expand at a 6.30% CAGR to 2031, more than one percentage point above the global glyoxal market CAGR. China’s yarn export engine exemplifies underlying fabric-finishing demand, while India’s pharmaceutical build-out stimulates intermediate consumption. Japan and South Korea contribute innovation pull through advanced battery programs evaluating glyoxal-based electrolytes. The region’s integrated petrochemical chains mitigate ethylene-glycol feedstock shocks, giving APAC producers a structural cost edge.

North America remains the second-largest regional cluster due to established chemical infrastructures and legislative momentum behind low-emission adhesives. The Department of Defense’s USD 24 million, five-year funding for domestic glyoxal manufacturing underscores the compound’s criticality in specialty coatings. Robust housing starts and remodeling spending sustain adhesive demand, while shale-related deep-water tie-backs extend oil-field chemical requirements. Importantly, the continent’s stringent OSHA oversight drives higher-purity and lower-formaldehyde specifications, favoring premium glyoxal formulations.

Europe displays mature demand tempered by stringent occupational exposure regulation but benefits from high-value specialty chemical niches. BASF’s 60,000-ton Ludwigshafen train secures regional supply, complemented by smaller niche makers in Italy and the Netherlands. Transition toward paper-board food packaging, propelled by the Single-Use Plastics Directive, is forecast to add incremental glyoxal biocide volumes. However, rising energy costs and tightened REACH dossiers may compress margins, motivating European converters to shift certain high-volume formulations to Eastern Europe and Türkiye.

Competitive Landscape

The glyoxal market is moderately concentrated. BASF leverages 60,000 tons of captive capacity in Germany and a new Zhanjiang line to safeguard supply for multinational textile and paper clients. Chinese producers focus on volume, often integrating upstream ethylene-glycol availability to maintain cost leadership, while European players differentiate via REACH dossier depth and application-lab support.

Strategically, sustainability credentials dominate competitive positioning. BASF has obtained ISCC+ certification for over 60 glyoxal-containing products, offering carbon-footprint declarations below 0.9 kg CO₂-eq per kg product. Hubei Hongyuan is piloting bio-ethylene glycol routes to hedge fossil volatility. Forward integration into application-specific blends is also a priority; WeylChem launched a turnkey antibacterial paper-coating concentrate in 2025 that eliminates customer side-blending and cuts batch times by 20%. Meanwhile, U.S. mid-tier entrant Locus Performance Materials is marketing glyoxal-enhanced biosurfactant packages for drilling fluids, signaling how niche technology can disrupt traditional supply chains.

Heightened regulatory scrutiny incentivizes larger companies to invest in closed-loop wastewater treatment and continuous reactor retrofits to curb unreacted aldehyde emissions. Smaller producers lacking capital may exit, gradually raising global market concentration. Nonetheless, regional supply security initiatives—such as the Pentagon’s domestic capacity grant—could seed new entrants, balancing consolidation forces.

Glyoxal Industry Leaders

BASF

Haihang Industry

hubei hongyuan pharmaceutical technology co., ltd

WeylChem International GmbH

Zhonglan Industry Co.,Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2023: INEOS announced a USD 700 million agreement with LyondellBasell to acquire its Ethylene Oxide and Derivatives business, including the Bayport Underwood site in Texas. The deal includes a 420 kt Ethylene Oxide plant, a 375 kt Ethylene Glycols plant, and a 165 kt Glycol Ethers plant, along with associated third-party operations. This acquisition strengthens INEOS's position in the global glyoxal market, as ethylene glycol is a key raw material for glyoxal.

- June 2022: As of June 1, 2022, Univar Solutions became the exclusive distributor for BASF's Chemical Intermediates’ Glyoxal in the US and Canada. This partnership enhances their collaboration to provide sustainable solutions across various applications.

Global Glyoxal Market Report Scope

Glyoxal is an organic crystalline solid, white at lower temperatures, yellow at melting point. The chemical formula for glyoxal is OCHCHO. The Market is Segmented by Application and geography. By application, the market is segmented into adhesives and sealants, intermediates, oil and gas exploration, textile, paints and coatings, and other applications. The report also covers the market size and forecasts for the glyoxal market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (kilo tons).

| Liquid Solution |

| Solid / Powder |

| Cross-linking Agents |

| Chemical Intermediates and Synthesis |

| Other Applications (Biocides and Preservatives, etc.) |

| Adhesives and Sealants |

| Intermediates |

| Oil and Gas Exploration |

| Paints and Coatings |

| Textile |

| Other End-User Industries (Pharmaceuticals, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Physical Form | Liquid Solution | |

| Solid / Powder | ||

| Application | Cross-linking Agents | |

| Chemical Intermediates and Synthesis | ||

| Other Applications (Biocides and Preservatives, etc.) | ||

| By End-User Industry | Adhesives and Sealants | |

| Intermediates | ||

| Oil and Gas Exploration | ||

| Paints and Coatings | ||

| Textile | ||

| Other End-User Industries (Pharmaceuticals, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current Glyoxal Market size?

The glyoxal market reached 453.18 kilo tons in 2026 and is forecast to hit 584.42 kilo tons by 2031, reflecting a 5.22% CAGR.

Which region leads glyoxal consumption?

Asia-Pacific holds 44.55% of global volume and is expected to advance at the quickest 6.30% CAGR through 2031.

Why are liquid glyoxal solutions preferred by manufacturers?

Liquid grades enable automated dosing, reduce batch variability and simplify compliance with transport regulations, explaining their 87.12% share in 2025.

What drives glyoxal demand beyond textile finishing?

Rapid uptake in chemical-intermediate synthesis for pharmaceuticals and specialty materials is the fastest-growing application at a 5.86% CAGR.

Page last updated on: