Cannabis Lighting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

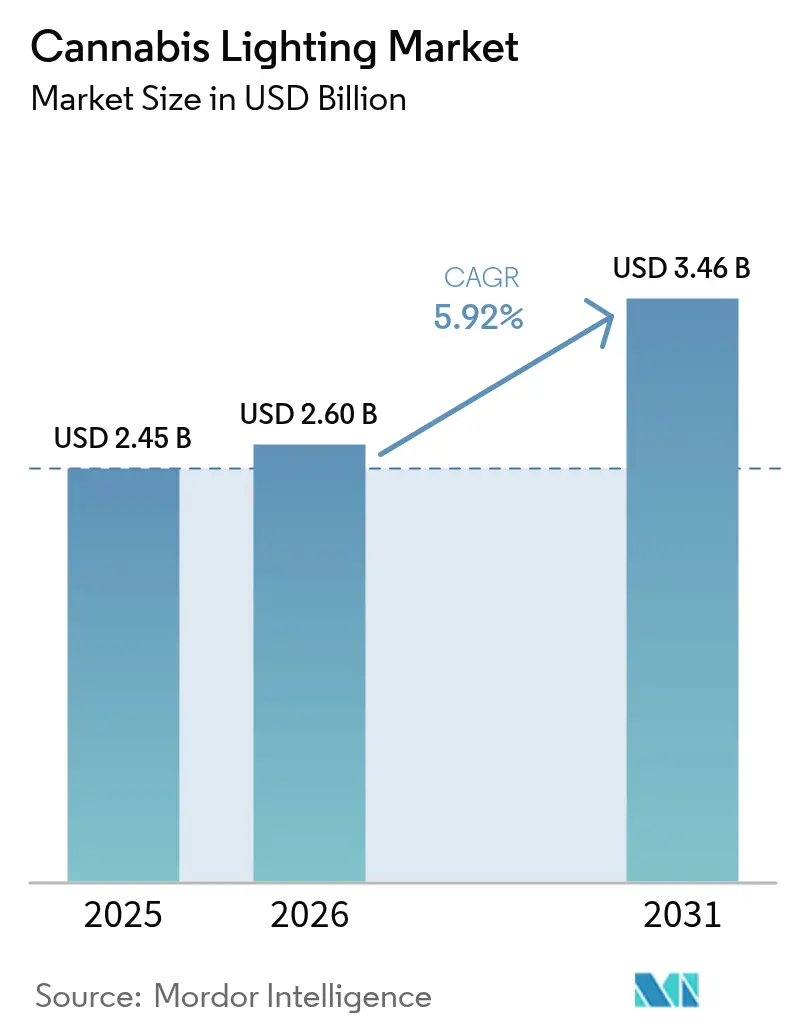

| Market Size (2026) | USD 2.6 Billion |

| Market Size (2031) | USD 3.46 Billion |

| Growth Rate (2026 - 2031) | 5.92% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cannabis Lighting Market Analysis by Mordor Intelligence

The cannabis lighting market size was valued at USD 2.45 billion in 2025 and estimated to grow from USD 2.6 billion in 2026 to reach USD 3.46 billion by 2031, at a CAGR of 5.92% during the forecast period (2026-2031). Robust growth stems from synchronized legalization waves, energy-efficiency regulations that accelerate light-emitting diode (LED) adoption, and rising demand for controllable spectra that drive premium yields across commercial cultivation sites. Germany’s 2024 Cannabis Act illustrates regulatory momentum that fuels equipment demand; patient counts surged from 250,000 to 900,000 within 13 months, lifting facility construction and, in turn, lighting procurement needs. Large multi-state operators (MSOs) standardize lighting specifications across sites to contain costs, while mercury and compact fluorescent phase-out rules in Canada and the European Union compel a rapid shift toward LED arrays. [1]Government of Canada, “Regulations Amending the Products Containing Mercury Regulations,” canadagazette.gc.ca Vertical farming structures register the fastest uptake because their tiered layouts magnify light-use efficiency, and intercanopy strategies that insert fixtures within plant canopies have delivered 20% higher yields and 27% larger buds in commercial trials.

Key Report Takeaways

- By lighting technology, LED commanded 77.12% of the cannabis lighting market share in 2025.

- By application, indoor cultivation facilities represented 63.45% share of the cannabis lighting market size in 2025, while vertical farming structures are predicted to expand at an 7.78% CAGR through 2031.

- By installation type, retrofits held 56.05% of the cannabis lighting market size in 2025; new-build projects record the highest projected CAGR at 6.72% to 2031.

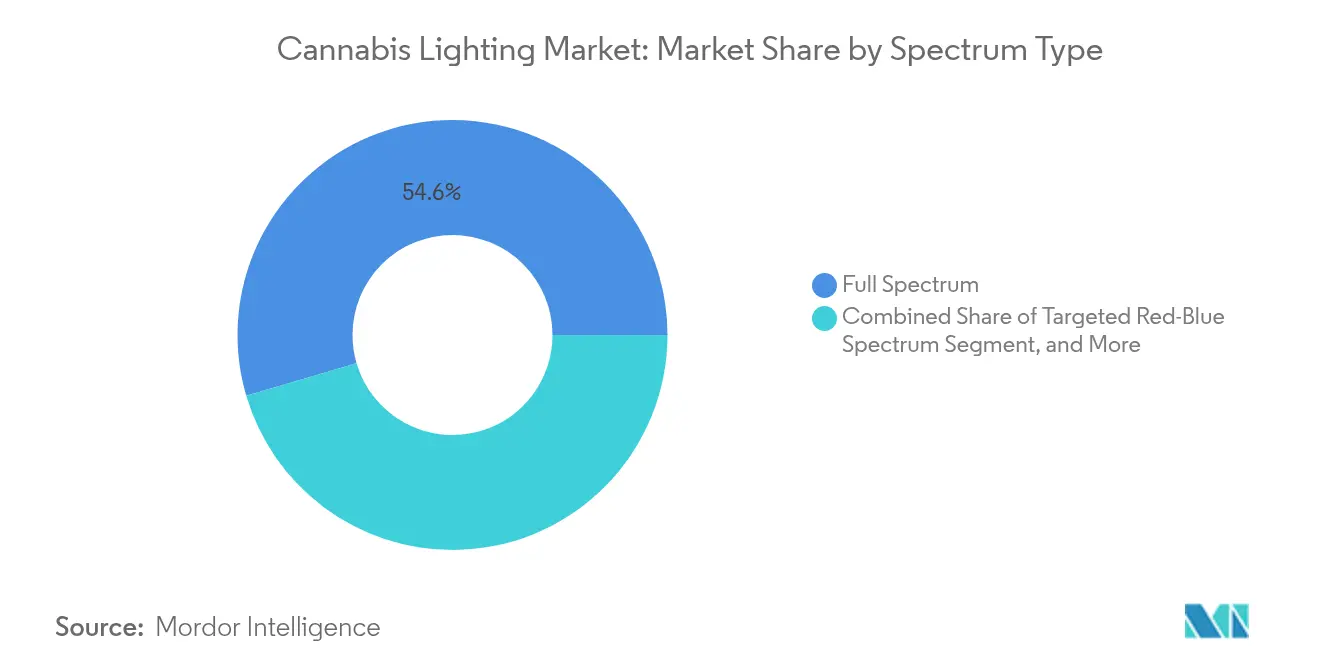

- By spectrum type, full-spectrum luminaires commanded 54.55% share in 2025, whereas UV plus far-red supplemental systems are expected to grow the fastest at 6.95% CAGR to 2031.

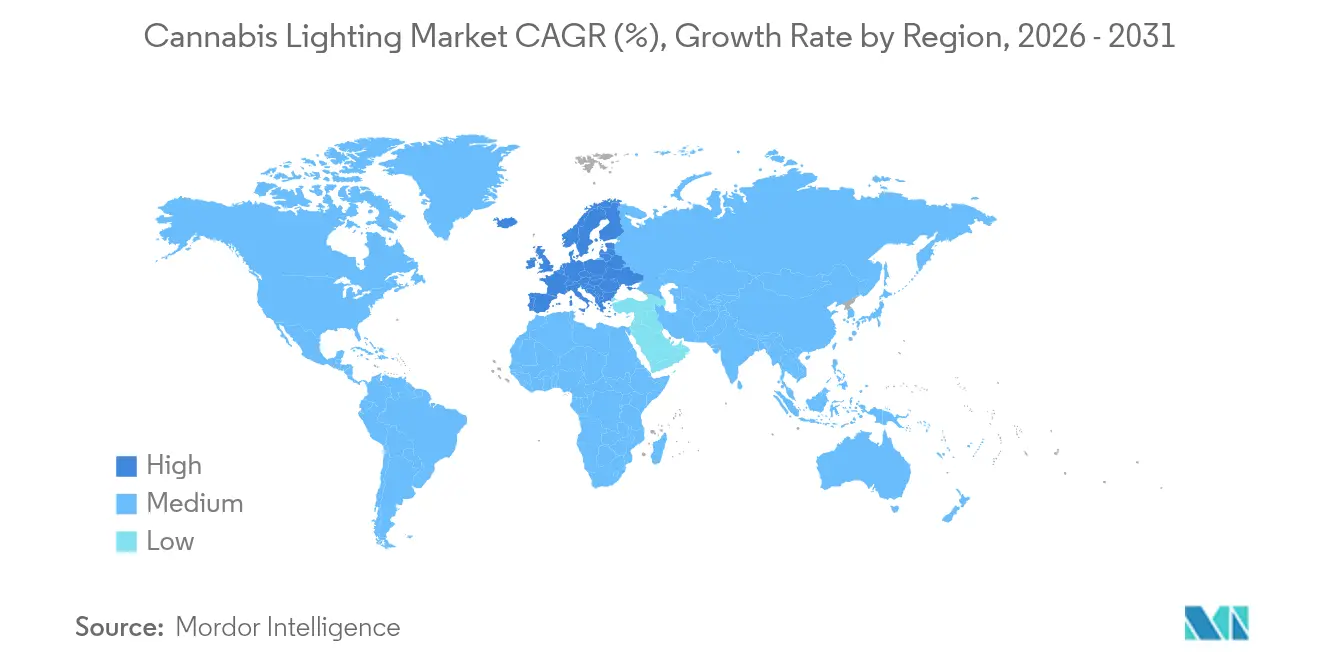

- By geography, North America accounted for 54.45% of the cannabis lighting market share in 2025, whereas Europe is projected to post the fastest 6.55% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cannabis Lighting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid expansion of legalized recreational cannabis markets in North America driving large-scale indoor farms | +1.2% | North America | Medium term (2-4 years) |

| Energy-efficiency mandates in Canada and EU incentivizing LED adoption in cannabis cultivation facilities | +0.9% | North America & EU | Short term (≤ 2 years) |

| Yield-optimization requirements for high-THC premium flower pushing demand for tunable spectrum luminaires | +0.8% | Global | Medium term (2-4 years) |

| Growth of vertically integrated multi-state operators (MSOs) leading to retrofit cycles of legacy HID fixtures | +0.7% | North America | Short term (≤ 2 years) |

| Surge in EU GMP-compliant medical cannabis exports from Portugal and Denmark requiring consistent photoperiod lighting | +0.6% | Europe | Medium term (2-4 years) |

| Advancements in smart, IoT-enabled lighting controls reducing operational costs for cultivators | +0.5% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid expansion of legalized recreational markets driving indoor farm development

Large-scale indoor sites underpin demand in the cannabis lighting market. Recreational frameworks in the United States and Canada incentivize year-round production under tightly managed photoperiods. Germany’s medical expansion added 650,000 patients in just over a year, triggering new construction that requires high-intensity LEDs and intelligent controls to maintain pharmaceutical-grade consistency. MSOs roll out standardized fixture layouts that streamline procurement and assure repeatable yields across state lines. Studies show yield climbs proportionally up to 1,800 µmol m² s-¹, reinforcing high-power LED investments that replace high-pressure sodium (HPS) lamps. [2]Frontiers in Plant Science, “Indoor Grown Cannabis Yield Increased Proportionally with Light Intensity,” frontiersin.org Modern facilities thereby maximize canopy productivity and reduce risk associated with legacy lighting variability.

Energy-efficiency mandates accelerating LED adoption in cannabis cultivation

Regulatory initiatives remain pivotal. Canada’s amended Products Containing Mercury Regulations prohibit most mercury and metal-halide lamps between 2025 and 2028, a move projected to save USD 5.16 billion in energy costs. The European Ecodesign Regulation 2024/1781 sets durability and efficiency thresholds that LED products already meet. [3] European Parliament and Council, “Regulation 2024/1781,” eur-lex.europa.eu Lighting drives 38% of an indoor grow’s energy expenditure, so swapping HPS units for LEDs cuts consumption by more than 40%, lowers cooling demand, and secures utility rebates. As a result, operators see paybacks in two to three years despite higher purchase prices, fueling continual growth in the cannabis lighting market.

Yield-optimization requirements driving demand for tunable-spectrum luminaires

Competitive differentiation increasingly relies on terpene and cannabinoid profiles, thus growers seek advanced fixtures that allow spectral fine-tuning. Full-spectrum models still dominate, yet adoption of ultraviolet (UV) and far-red supplementation grows at 7.3% CAGR as cultivators quantify secondary metabolite gains. Czech trials reported significant rises in flower mass and potency at 1,300 µmol m² s-¹ photon density relative to 900 µmol m² s-¹, outcomes facilitated by tunable LEDs. Intercanopy arrays further even out light distribution, and commercial tests confirm 20% yield uplifts. These performance premiums continue to pull capital into spectrum-adaptive solutions within the cannabis lighting market.

Growth of MSOs creating retrofit opportunities

Retrofit activity remains pronounced. MSOs often acquire older facilities equipped with HPS or ceramic metal halide units. Urban-Gro revealed more than 1,000 controlled-environment projects and a USD 20 million build contract with an MSO, illustrating scale. [4]U.S. Securities and Exchange Commission, “urban-gro Form 10-K,” sec.gov LED life spans exceed 50,000 hours, curbing lamp replacement labor and cutting downtime. Consolidated purchasing supports volume discounts, driving fresh demand across MSO property portfolios and sustaining the retrofit-oriented share of the cannabis lighting market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capital expenditure of full-spectrum LED arrays relative to HPS fixtures, especially for small growers | -0.8% | Global | Short term (≤ 2 years) |

| Regulatory uncertainty and delayed licensing rounds in Germany and United States states stalling facility construction | -0.6% | North America & EU | Medium term (2-4 years) |

| Heat-management challenges in high-density vertical farms limiting use of high-intensity fixtures | -0.4% | Global | Medium term (2-4 years) |

| Illicit market persistence in Asia-Pacific dampening investment in professional-grade cultivation lighting | -0.3% | Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High upfront capital expenditure limiting LED adoption among small-scale growers

Professional-grade LEDs cost two to three times more than HPS setups. A medium farm retrofit can reach USD 200,000, yet banking constraints in federally illegal U.S. markets impede access to equipment loans. Smaller operators hence postpone investments despite long-term savings, tempering near-term volume growth for manufacturers within the cannabis lighting market.

Regulatory uncertainty and licensing delays stalling facility construction

Jurisdictional shifts introduce scheduling risk. Germany’s switch to authorization-based licensing yielded initial confusion, while new U.S. state programs face prolonged review periods, lagging real estate build-outs and equipment orders. Developers hesitate to commit to lighting purchases until permits are secure, slowing conversion of forecast demand into booked revenue across the cannabis lighting market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Lighting Technology: Efficiency rules reinforce LED ascendancy

LED systems captured 77.12% cannabis lighting market share in 2025 and are projected to grow at 6.25% CAGR to 2031. Canada’s mercury ban mandates replacement of fluorescent and metal-halide lamps, triggering compulsory conversions that expand the cannabis lighting market. LEDs cut energy use by 40%, emit less heat, and deliver spectral precision increasingly vital for premium flower. HPS fixtures persist among cost-constrained cultivators, whereas ceramic metal halide lights remain confined to niche phenotyping or specialty strain rooms. Compact fluorescents are scheduled for elimination, accelerating their exit. Overall, technology substitution cycles secure a central position for LEDs in the cannabis lighting industry.

LED upgrades often coincide with broader facility improvements. Operators add wireless sensors, dim-to-watt drivers, and networked controls that modulate intensity by growth stage. These enhancements integrate seamlessly with HVAC systems to maintain stable vapor-pressure deficits, driving holistic efficiency gains. In new builds, architects design electrical distribution and bench layouts around modular LED bars, underscoring how technology choices reshape cultivation footprints while expanding the cannabis lighting market.

By Application: Indoor grows dominate while vertical farms accelerate

Indoor sites accounted for 63.45% of the cannabis lighting market size in 2025. Tight environmental control satisfies good manufacturing practice (GMP) rules and enables year-round harvest schedules. Close-canopy LED installations improve photon-use efficiency by up to 100% when fixture clearance narrows to 15 cm. Vertical farms, although newer, outpace all other applications with an 7.78% CAGR. Urban land-price pressures, zoning limits, and local-sourcing mandates make multi-tiered formats attractive for metropolitan retailers, boosting the cannabis lighting market.

Greenhouses blend sunlight with supplemental LEDs to moderate operating costs. Combined photosynthetic photon flux maintains cannabinoid consistency during winter months, and automatic shading systems prevent photoinhibition in summer. Indoor and greenhouse strategies thus coexist: operators select configurations that align with electricity tariffs, real estate constraints, and product positioning as the cannabis lighting industry matures.

By Spectrum Type: Full spectrum leads; supplemental UV gains momentum

Full-spectrum fixtures held 54.55% share of the cannabis lighting market in 2025, offering turnkey flexibility without the need for spectral tuning. Yet UV-plus-far-red supplementation posts the strongest growth, reflecting evidence that targeted wavelengths influence terpene pathways. Blue-heavy recipes encourage compact vegetative structure, while red-rich spectra accelerate floral biomass. Developers embed on-board diodes that deliver programmable recipes, enabling cultivators to fine-tune cycles and command premium prices. As crop-steering software links sensor feedback with lighting arrays, demand for adaptive spectral platforms continues to grow within the cannabis lighting market.

Simpler red-blue boards remain relevant where capital budgets are tight, particularly for vegetative rooms. However, the advent of dynamically addressable channels diminishes earlier cost gaps. Suppliers now market mid-priced fixtures that automate sunrise-sunset ramps, reinforcing elevated quality norms across regulated markets and widening adoption of spectral agility in the cannabis lighting industry.

By Installation Type: Retrofit predominates; new-build pace quickens

Retrofit projects contributed 56.05% to the cannabis lighting market size in 2025 as growers swapped aging HID fixtures for LEDs. Operators value immediate utility savings and cooling-load reductions. Project teams often integrate lighting refits with electrical panel upgrades, adopting lower-gauge wiring as LEDs reduce amperage draw. New builds are growing faster—6.72% CAGR—because legalization in frontier jurisdictions sparks greenfield complexes engineered for vertical integration. Electrical architecture, ceiling height, and bench spacing are optimized from inception, lowering installation cost per micromole and widening future retrofit windows for advanced modules, which sustains expansion of the cannabis lighting market.

Geography Analysis

North America continued to generate 54.45% of global revenue in the cannabis lighting market during 2025. Mature adult-use programs in Canada and 24 U.S. states underpin large contract volumes. Utility rebates offset 20-30% of LED invoice costs, enabling rapid recoupment of investment. Canadian federal mercury restrictions further compel replacement, ensuring fixture demand even in flat-sales provinces.

Europe delivers the fastest 6.55% CAGR to 2031. Germany’s patient base almost quadrupled post-legalization, spurring cultivation capacity investments that rely on LED arrays to satisfy pharmacopeial purity standards. Portugal and Denmark export EU-GMP flower, and southern markets combine greenhouse structures with supplemental LEDs to mitigate summer heat stress. The EU Ecodesign law, effective mid-2024, cements LED preference and channels funding toward high-efficiency products.

Asia-Pacific, South America, and the Middle East & Africa represent nascent territories for the cannabis lighting market. Illicit trade, limited financing, and evolving statutes restrain near-term volumes. Nonetheless, Brazil and Thailand examine broader medical frameworks, while Japan backs clinical trials that could unlock domestic cultivation. Multinationals position regional hubs to leverage eventual liberalization, anticipating future uplift in the cannabis lighting industry.

Competitive Landscape

Competition remains fragmented; no single vendor holds double-digit revenue share across all regions. Multinational lighting groups acquire niche horticultural brands to deepen domain expertise. Signify’s 2024 purchase of Fluence broadened its agricultural suite and added North America-focused Gavita products. Scotts Miracle-Gro divested Hawthorne Collective in April 2025, signaling portfolio realignment that may shift distribution alliances.

Strategic partnerships dominate differentiation strategies. Hydrofarm joined with Trolmaster to integrate IoT-ready controllers and deliver remote spectrum scheduling. Sollum’s collaboration with Leaficient combines in-plant sensors and adaptive lighting algorithms aimed at real-time photon deployment efficiency. Certification gains importance following new IEC horticultural standards that set safety and reliability thresholds, a development that favors firms with in-house compliance capacity.

Vendors that couple data analytics, cultivation modeling, and service networks improve stickiness within the cannabis lighting market. Integrated offerings reduce downtime, facilitate preventive maintenance, and increase lifetime customer value. As regulatory scopes broaden, companies that master local compliance and utility rebate paperwork will outpace competitors that rely solely on hardware pricing.

Cannabis Lighting Industry Leaders

OSRAM Licht AG

Gavita Holland BV

Illumitex Inc.

Signify Holding

LumiGrow, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Scotts Miracle-Gro transferred Hawthorne Collective to a strategic partner, tightening focus on core lawn and garden lines.

- February 2025: The United States Pharmacopeia and European Pharmacopoeia released harmonized cannabis quality chapters, raising contamination-control expectations for lighting designers.

- December 2024: Hydrofarm and Trolmaster signed a distribution deal to bundle smart environmental controls with LED fixtures.

- June 2024: EU Regulation 2024/1781 established ecodesign benchmarks, cementing LED requirements.

Global Cannabis Lighting Market Report Scope

Cannabis can be seen in several forms, and the health advantages of cannabis are increasing. Lighting is crucial during cannabis cultivation, whether indoor or outdoor. The light cycle for flowering cannabis directly correlates to a crop's quality and overall yield. Cannabis is a photosensitive plant, which means that the amount of light it receives in 24 hours causes it to respond. There are different types of Lighting Technology such as Light Emitting Diodes (LEDs), T5 High Output Fluorescent Light, Ceramic Metal Halide Light, Compact Fluorescent Light, and Magnetic Induction Light that include different Applications such as Greenhouse, Indoor, Vertical Farming, multiple geographies. The impact of Covid-19 on the market and affected segments are also covered under the scope of the study.

| Light Emitting Diodes (LED) |

| High-Pressure Sodium (HPS) Lamps |

| Ceramic Metal Halide (CMH) Lights |

| T5 High Output Fluorescent |

| Compact Fluorescent Lights (CFL) |

| Magnetic Induction Lights |

| Other Technologies |

| Full Spectrum |

| Targeted Red-Blue Spectrum |

| UV and Far-Red Supplemental Spectrum |

| New Build Facilities |

| Retrofit Projects |

| Indoor Cultivation Facilities |

| Greenhouses |

| Vertical Farming Structures |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Nordics | ||

| Rest of Europe | ||

| South America | Brazil | |

| Rest of South America | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Lighting Technology | Light Emitting Diodes (LED) | ||

| High-Pressure Sodium (HPS) Lamps | |||

| Ceramic Metal Halide (CMH) Lights | |||

| T5 High Output Fluorescent | |||

| Compact Fluorescent Lights (CFL) | |||

| Magnetic Induction Lights | |||

| Other Technologies | |||

| By Spectrum Type | Full Spectrum | ||

| Targeted Red-Blue Spectrum | |||

| UV and Far-Red Supplemental Spectrum | |||

| By Installation Type | New Build Facilities | ||

| Retrofit Projects | |||

| By Application | Indoor Cultivation Facilities | ||

| Greenhouses | |||

| Vertical Farming Structures | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Nordics | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Rest of South America | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the cannabis lighting market?

The cannabis lighting market is valued at USD 2.6 billion in 2026.

How fast will the market grow through 2031?

Revenue is projected to rise to USD 3.46 billion by 2031, representing a 5.92% CAGR.

Which lighting technology leads today’s sales?

LED fixtures dominate with 77.12% market share in 2025, driven by energy-efficiency rules and yield-optimization needs.

Why are vertical farming structures expanding quickly?

Vertical farms achieve space efficiency in urban locales and post an 7.78% CAGR because tiered racks maximize photon use and leverage controlled spectra.

Which region offers the highest growth potential?

Europe shows the fastest 6.55% CAGR as Germany, Portugal, and Denmark scale EU-GMP facilities under new legalization frameworks.

What hampers small growers from adopting LEDs?

Full-spectrum LED arrays cost 200-300% more than HPS systems, and limited financing options extend payback periods, slowing uptake among capital-constrained operators.

Page last updated on: