Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.68 Billion |

| Market Size (2026) | USD 3.83 Billion |

| Market Size (2031) | USD 4.67 Billion |

| Growth Rate (2026 - 2031) | 4.05% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Office Furniture Market Analysis by Mordor Intelligence

The Canada office furniture market size is expected to grow from USD 3.68 billion in 2025 to USD 3.83 billion in 2026 and is forecast to reach USD 4.67 billion by 2031 at 4.05% CAGR over 2026-2031. Growth emerges from three interconnected forces: the mainstreaming of hybrid work, the hardening of government green-procurement rules, and a widespread design shift from fixed cubicles toward multi-purpose zones. Corporations are funneling capital into retrofits that add hot-desking benches, lounge clusters, and technology-rich conference suites, even as permanently remote policies compress downtown footprints in Toronto and Vancouver. Domestic manufacturers rely on in-house dealer networks to bypass retail mark-ups, while private-equity funds pursue roll-up plays that promise scale economies. However, rising hardwood and steel prices, coupled with Extended Producer Responsibility (EPR) mandates, pressure margins and accelerate experimentation with recycled polymers across the Canada office furniture market.

Key Report Takeaways

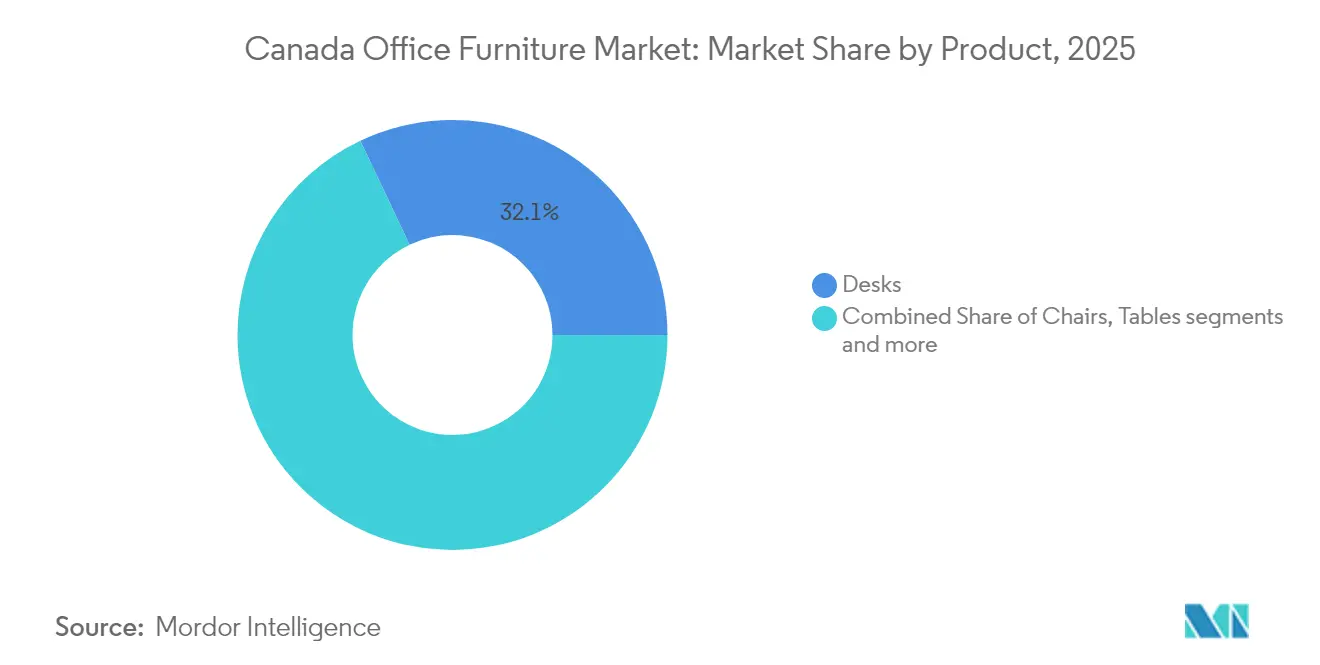

- By product, desks led with 32.05% of the Canada office furniture market share in 2025, whereas sofas and soft seating are advancing at a 4.21% CAGR through 2031.

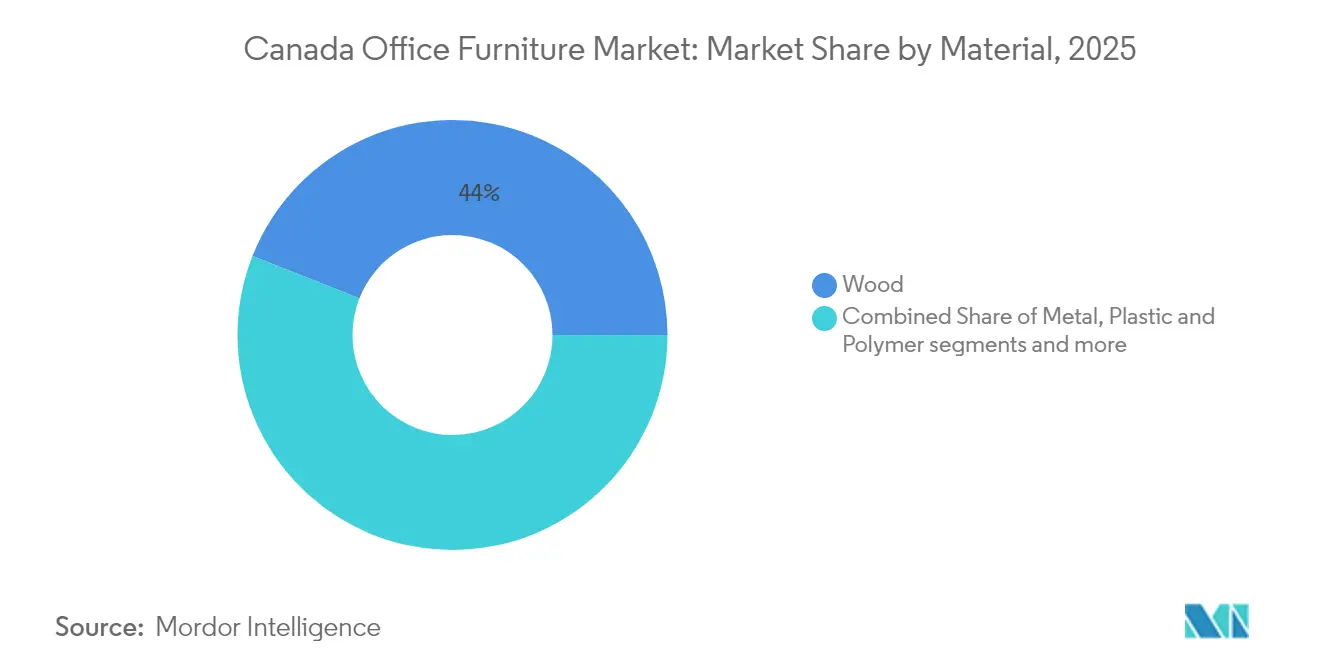

- By material, wood accounted for 44.02% of the Canada office furniture market size in 2025; plastic and polymer solutions are projected to post a 3.88% CAGR to 2031.

- By price range, the mid-range segment captured 50.55% market share in 2025, while premium furniture is slated to expand at a 4.9% CAGR through 2031.

- By end-user, corporate offices held 50.40% of the Canada office furniture market size in 2025; educational institutions show the fastest 4.45% CAGR to 2031.

- By geography, Ontario maintained 36.62% of the Canada office furniture market share in 2025; Alberta is expected to register a 5.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Office Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ergonomic-first workplace designs | +0.8% | Ontario and British Columbia hubs | Medium term (2-4 years) |

| Green-procurement mandates | +0.6% | Nationwide, public-sector-led | Long term (≥ 4 years) |

| Corporate retrofits for collaboration zones | +0.7% | Major urban cores | Short term (≤ 2 years) |

| SME demand uplift from tax credit | +0.4% | Alberta and Saskatchewan | Medium term (2-4 years) |

| Modular acoustic pods in open offices | +0.5% | Tech and finance corridors | Short term (≤ 2 years) |

| Northern community digital-service hubs | +0.2% | Yukon and Northern Territories | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ergonomic-first workplace designs driven by hybrid work policies

Corporate adoption of hybrid schedules has moved ergonomics from an afterthought to a strategic retention lever. Public Services and Procurement Canada now embeds detailed ergonomic standards for rotary seating inside every federal tender, and those criteria have cascaded into private sector bid documents[1]Public Services and Procurement Canada, “Supply Arrangement: Office Seating,” tpsgc-pwgsc.gc.ca. Height-adjustable desks, synchronized-tilt chairs, and flexible footrests dominate specification sheets as facilities teams respond to evidence that discomfort fuels turnover. Gensler survey data show more than half of Canadian employees still visit offices weekly, yet only part-time, so each workstation must flex between focus and collaboration. Post-renovation studies reveal measurable bumps in staff satisfaction when sit-stand and lumbar-support features are standard, reinforcing the driver’s medium-term pull across the Canada office furniture market.

Green-procurement mandates favoring FSC-certified and circular furniture

Government buyers have institutionalized sustainability checklists that require FSC lumber, low-VOC laminates, and vendor take-back guarantees. The Public Prosecution Service attained 100% compliance with green-procurement training, ensuring every furniture tender carries environmental clauses[2]Public Prosecution Service of Canada, “Green Procurement Training,” ppsc-sppc.gc.ca. Provincial EPR laws, such as British Columbia’s 75% recovery target, shift end-of-life costs onto manufacturers and encourage designs that can be disassembled and recycled. Vendors like Envirotech monetize the shift by refurbishing surplus desks and reselling them to value-oriented clients, diverting millions of kilograms of waste. Combined, these rules make circularity a competitive necessity within the Canada office furniture market rather than a marketing add-on.

Corporate retrofits to upgrade collaboration and hot-desking zones

Real-estate leaders are reallocating capital from square-foot expansion to experience upgrades that justify smaller footprints. JLL research finds that more than three-quarters of occupiers are pouring budget into tech-integrated furniture, while four in ten are overhauling conference suites. SnapCab pods illustrate the retrofit ethos: at CAA North & Eastern Ontario, prefabricated rooms arrived finished, slid into place overnight, and delivered acoustic privacy without drywall mess. Capital Cost Allowance rules sweeten payback because traditional desks fall under Class 8 with 20% depreciation, while tech-heavy elements land in Class 50 at 55%[3]T2inc, “Capital Cost Allowance Basics,” t2inc.ca. The result is a rush toward reconfigurable benches, mobile tables, and modular storage that keep pace with agile head-count swings in the Canada office furniture market.

Rapid adoption of modular acoustic pods and phone booths in open offices

The pandemic spotlighted noise and privacy gaps in open-plan layouts once dominated by benching systems. Modern pods from Kubebooth deliver 36 dB insulation, hospital-grade ventilation, and ADA clearance, ticking compliance boxes for federal agencies and universities. Indigenous-owned Elder Eagle markets similar cabins under diversity-procurement streams. Beyond muffling sound, new models embed USB-C ports, PoE lighting, and IoT sensors that feed workspace-use analytics. Fast delivery, minimal installation, and lease-friendly pricing make pods an attractive stopgap as companies reassess long-term real-estate strategies across the Canada office furniture market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile hardwood and steel prices | -0.9% | Quebec and Ontario manufacturing corridors | Short term (≤ 2 years) |

| Global delays for polymer and actuator parts | -0.6% | Import-dependent plants nationwide | Medium term (2-4 years) |

| Shrinking downtown footprints under remote work | -0.7% | Five largest metros | Medium term (2-4 years) |

| Provincial EPR rules elevate compliance costs | -0.3% | All provinces, staggered rollout | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile hardwood and steel input prices are squeezing manufacturer margins

In April 2025, Eastern SPF lumber prices increased to CAD 655 per 1,000 board feet, surpassing the 52-week average of CAD 620[4]Natural Resources Canada, “Lumber and Panel Prices,” ressources-naturelles.canada.ca. Steel prices experienced a nearly 25% surge, as highlighted by Avison Young, while container costs doubled, disrupting several office fit-out projects. Mid-sized manufacturers, without adequate hedging mechanisms, are struggling with significant pricing volatility, which undermines cost predictability. Some manufacturers have pivoted to recycled materials to offset rising costs; however, these measures provide only partial relief. The cost pressures are particularly severe for wood-centric brands in Quebec and steel-intensive seating manufacturers in Ontario. This has led to a narrowing of profit margins across the Canadian office furniture market, further challenging the sector's growth potential.

Shrinking downtown office footprints under permanently remote policies

The federal plan to repurpose half its real-estate portfolio into housing aims for USD 3.9 billion in savings over a decade. Private landlords echo that contraction: Toronto vacancies approach 20%, while Calgary and Ottawa remain elevated. Several departments lack seats for mandated three-day returns, highlighting a mismatch between staff counts and reduced square footage. The surplus fuels a secondary market for gently used desks, cooling demand for new inventory. Together, these forces trim growth expectations for the Canada office furniture market even as niche categories such as pods and lounge seating rise.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Desks Drive Market Leadership

Desks controlled 32.05% of the Canada office furniture market share in 2025, underscoring their role as the workday anchor. Height-adjustable variants attract interest because they satisfy ergonomic policies and support hot-desking scripts. Dedicated federal supply arrangements list technical, environmental, and life-cycle criteria that vendors must meet, reinforcing the segment’s baseline demand. Sofas and soft seating, with a 4.21% CAGR, signal a cultural turn toward informal interaction zones and residential comfort. Booths and dividers fill the privacy void left by open-plan layouts, while storage adapts into personal lockers that accompany mobile work patterns.

In the second tier, chairs benefit from universal ergonomic mandates and advanced mechanism options that extend user comfort across task, guest, and meeting applications. Conference tables regain relevance by embedding power, data, and video infrastructure needed for hybrid sessions. The Canada office furniture market thus tilts toward flexible systems—desks, pods, and movable lounges—that allow employers to re-script floorplates without structural renovation.

By Material: Wood Dominance Faces Sustainability Pressure

In 2025, wood accounted for 44.02% of the Canada office furniture market, driven by its aesthetic appeal and the strength of a well-established domestic supply chain. Groupe Lacasse's investment in laminated-panel automation highlights the integration of provincial mills into finished goods production, showcasing the efficiency of the supply chain. However, fluctuations in lumber prices and stricter Extended Producer Responsibility (EPR) targets are prompting specifiers to explore alternative materials. Recycled polymers, which recorded a 3.88% CAGR, are gaining traction as a viable substitute. Metal frames are also facing cost pressures, with powder-coated steel becoming a more expensive input for seating and table bases, further influencing material selection trends.

Designers are increasingly adopting composites that incorporate recycled PET, bio-resins, and post-consumer aluminum, as these materials align with LEED certification requirements and mitigate the impact of commodity price volatility. In the healthcare and education sectors, plastic shells are emerging as a preferred choice due to their color adaptability and ease of maintenance. This shift reflects a broader trend in the market, where material selection is becoming a strategic decision. Stakeholders must balance the traditional appeal of wood with the cost stability and functional benefits offered by polymers. As the Canada office furniture market evolves, the interplay between heritage materials and innovative alternatives will continue to shape purchasing decisions and product development strategies.

By Price Range: Mid-Range Dominance Reflects Value Optimization

In 2025, mid-range office furniture captured 50.55% of the market share, driven by businesses prioritizing durability and cost management. Companies typically allocate CAD 500-1,250 for desks and CAD 750-1,500 for task chairs, focusing on ergonomic features without incurring luxury-level costs. The adoption of accelerated depreciation under CCA Class 8 further supports this segment by enabling faster asset write-offs, making mid-range products a financially viable choice. This segment's strong performance reflects its ability to meet specification requirements while maintaining affordability, positioning it as the preferred option for a significant portion of the market. The mid-tier category continues to dominate due to its alignment with the financial and operational priorities of businesses, particularly in balancing quality and budget constraints.

The premium segment, growing at a 4.9% CAGR, is defined by features such as executive branding, bespoke veneers, and embedded sensors for utilization tracking. Leasing models have made these high-cost products accessible to mid-sized enterprises that prioritize predictable cash flow management. Conversely, economy furniture lines cater to startups and home offices, leveraging flat-pack shipping and online configurators to deliver cost-effective solutions. The Canadian office furniture market spans a diverse spectrum of offerings, but demand remains concentrated in the mid-tier segment. This concentration highlights the market's focus on products that balance rigorous specifications with financial efficiency, making mid-range furniture the cornerstone of the industry. The segmentation of the market underscores the varied needs of businesses, with mid-range products emerging as the dominant choice due to their practicality and value proposition.

By End-User: Corporate Offices Lead Institutional Diversification

In 2025, corporate offices accounted for 50.40% of the Canada office furniture market, driven by the concentration of headquarters in Toronto and Vancouver. Despite the reduction in overall office footprints due to hybrid work models, investments are shifting toward amenity-rich office layouts that emphasize collaboration, employee wellness, and brand identity. The healthcare segment is emerging as a key driver of specialty furniture demand, with a focus on infection-control fabrics and bariatric seating. Global Furniture Group's expanding hospital portfolio highlights the growth potential in this segment. Educational institutions are projected to record the highest CAGR of 4.45%, supported by campus renovation programs and increasing student enrollments. Suppliers such as CDI Spaces are capitalizing on this trend by providing mobile tables, stackable chairs, and power-enabled study booths for new STEM facilities.

Government offices are navigating a dual challenge of space optimization and compliance with retrofit mandates, resulting in selective procurement processes with detailed specifications. The hospitality sector, retail back offices, and professional services firms are also contributing to the demand for office furniture, creating a diverse market landscape. While hybrid work trends are reshaping corporate office requirements, the focus on wellness and collaboration is expected to sustain investments in innovative furniture solutions. Additionally, the healthcare and education sectors are anticipated to remain key growth drivers, supported by evolving infrastructure needs and demographic trends. The market's dynamics reflect a shift toward functionality and adaptability, with suppliers aligning their offerings to meet sector-specific requirements. This diversification of demand underscores the importance of targeted strategies to capture growth opportunities across various end-user segments in the Canada office furniture market.

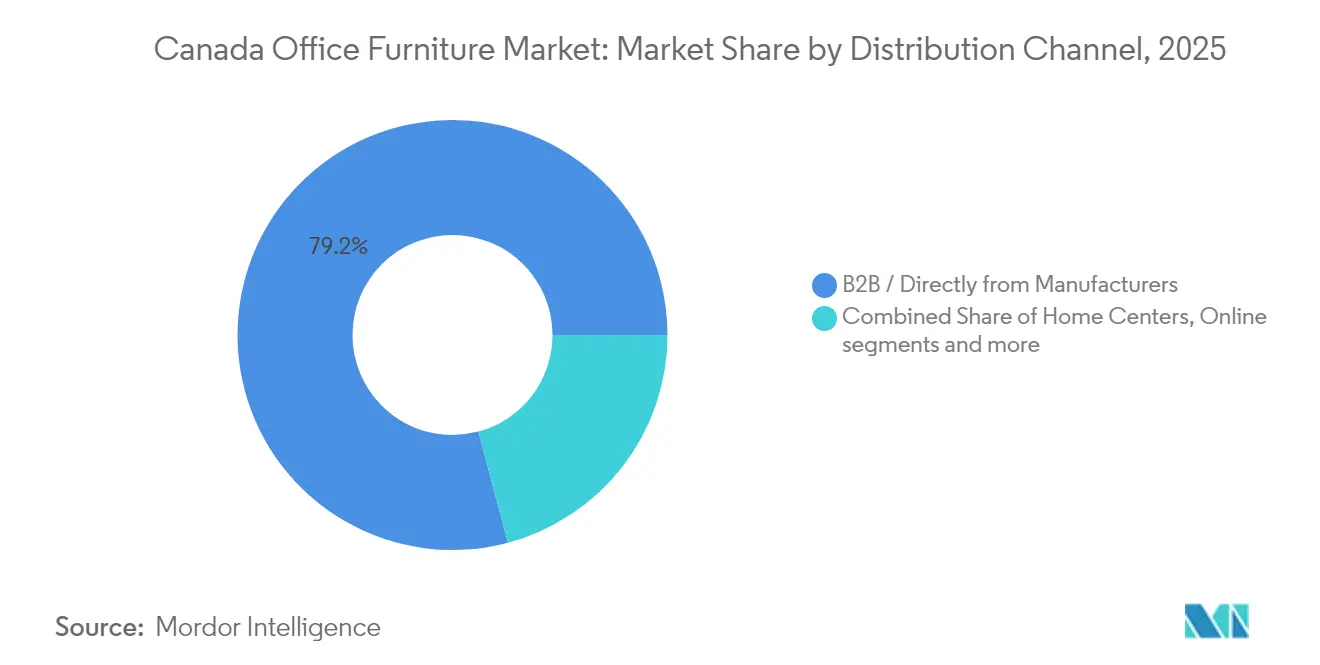

By Distribution Channel: B2B Direct Sales Dominate Market Access

In 2025, B2B direct channels accounted for 79.15% of the market share, driven by the demand for single-source accountability in managing complex projects. These channels streamline processes by integrating design, logistics, and after-sales services under one umbrella. Teknion’s extensive dealer network across Canada exemplifies how manufacturers leverage direct channels to maintain factory pricing while ensuring localized installation services. Early engagement through direct channels enables manufacturers to influence space planning decisions, securing product ecosystems before general contractors enter the bidding process for interior projects. This approach not only enhances operational efficiency but also strengthens long-term client relationships, positioning B2B direct channels as a critical revenue driver.

Conversely, the B2C segment caters to small businesses and home-office users, with players like Source Office Furniture offering showroom pickups and last-mile delivery services. While online sales surged during the pandemic, the segment now faces challenges such as high shipping costs for bulky items like desks. Specialty retailers continue to differentiate themselves by providing tactile experiences, which remain a key advantage over pure e-commerce platforms. The Canadian office furniture market operates on a hybrid channel model, where the coexistence of B2B and B2C channels addresses diverse customer needs. However, direct B2B relationships remain the dominant force, setting the pace for market growth and revenue generation.

Geography Analysis

Ontario anchors the Canada office furniture market through its dense corporate corridor stretching from Toronto’s Financial District to Ottawa’s federal precincts. Provincial procurement volumes combine with resident manufacturing fleets—such as Global Furniture Group’s chair plants—to create a feedback loop of local supply and demand. Yet elevated vacancy in Toronto’s Class-A towers forces landlords to re-imagine suites as flexible plug-and-play spaces, injecting fresh orders for modular lounges and sit-stand benching that help owners attract hybrid tenants.

Quebec pairs a strong manufacturing heritage with a design-forward positioning. Brands like Artopex and Groupe Lacasse leverage proximity to North-eastern U.S. markets, short transport lanes, and a pool of skilled cabinetmakers. Government grants supporting equipment automation strengthen competitiveness, while Montreal’s tech accelerators generate incremental demand for agile breakout furniture. The province also benefits from strict provincial green-building codes that align with its low-carbon electricity grid, nudging buyers toward locally sourced FSC hardwoods and laminated panels.

Western growth centers on Alberta, where the energy sector rebound underpins the fastest CAGR in the Canada office furniture market. Calgary’s shift from pure oil headquarters to diversified tech and logistics tenants sparks office-core refurbishments that favor acoustic booths and collaborative sofas. British Columbia adds tech-startup velocity and province-wide corporate supply arrangements featuring big-name manufacturers, guaranteeing price transparency for public buyers and pulling national brands into Vancouver warehouses. Across the Atlantic provinces and Northern Territories, population density limits volume, yet federal digital-hub rollouts and call-center expansions provide steady albeit smaller streams of orders.

Competitive Landscape

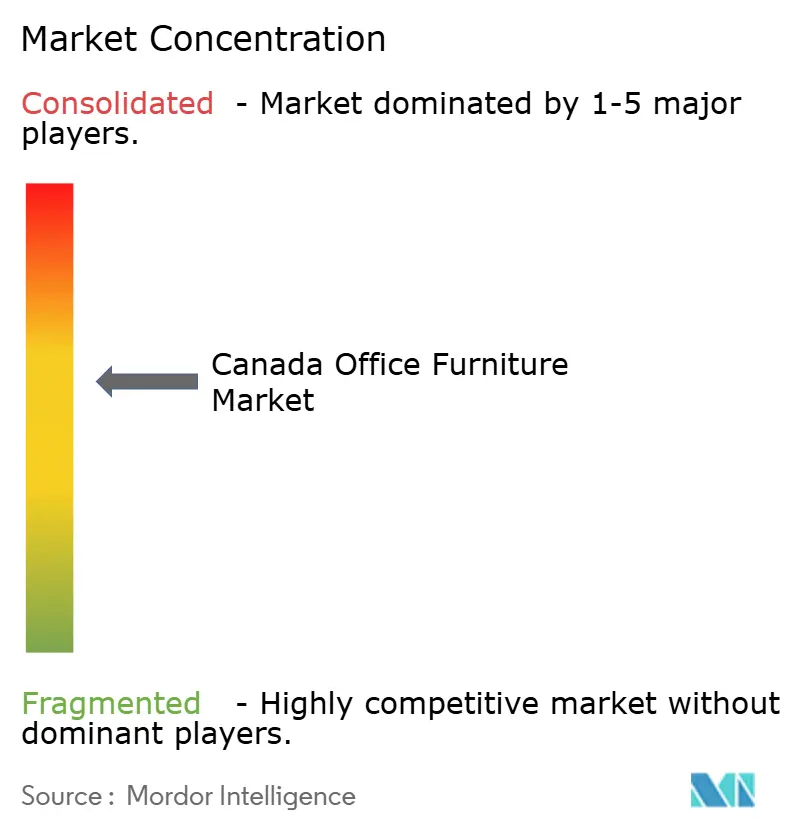

The Canada office furniture market exhibits moderate fragmentation, shaped by a mix of heritage manufacturers, imported premium labels, and nimble specialists. Domestic stalwarts such as Teknion, Global Furniture Group, Artopex, and Groupe Lacasse balance scale production with localized design studios, enabling fast turnaround on custom finishes. International icons—Steelcase, Herman Miller, Haworth, and Knoll—compete mainly in the specification-driven corporate and government tenders where global product certifications matter.

Strategic differentiation increasingly pivots on service scope rather than mere catalog breadth. Full-line vendors deliver workspace consulting, 3-D visualization, and post-occupancy analytics, turning furniture sales into multi-year relationship platforms. Circular-economy propositions—from Humanscale’s refurbishment program to Envirotech’s remanufacturing lines—help bidders score high on ESG evaluation criteria embedded in public tenders.

Private-equity interest signals a coming wave of consolidation designed to stitch regional dealer networks into national footprints. Mycroft Holdings’ investment in Heartwood Manufacturing exemplifies the thesis: combine complementary product sets, optimize freight, and deepen penetration of Western Canada. Niche disruptors such as Kubebooth tap underserved pockets like acoustic privacy, showing that innovation still finds air even as the competitive field coalesces.

Canada Office Furniture Industry Leaders

Global Furniture Group

Teknion

Steelcase Inc.

Haworth Inc.

Herman Miller Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Mycroft Holdings completed a strategic investment in Heartwood Manufacturing and Heartwood Distributors. The deal provides capital and managerial expertise aimed at scaling production capacity in Western Canada while integrating dealer networks under a unified platform.

- April 2025: Humanscale unveiled its Humanscale Living collection at Salone del Mobile 2025. The launch marks a deliberate push beyond corporate workstations into residential and hospitality settings, reflecting the blurred lines between home and office use cases.

- February 2025: Groupe Lacasse refreshed its website under the “2.0” initiative. The digital upgrade accompanies earlier factory automation investments, reinforcing the brand’s message of modern craftsmanship and streamlined customer access.

- January 2025: Artopex opened a two-level showroom in Old Montreal’s former Royal Bank headquarters. The space uses panoramic Quebec landscape imagery to contextualize furniture vignettes and champion local design talent.

Canada Office Furniture Market Report Scope

A complete background analysis of the Canada office furniture market, which includes an assessment of the National accounts, economy, and the emerging market trends by segments, significant changes in the market dynamics, and the market overview is covered in the report.

By Product

| Chairs | Employee Chairs |

| Meeting Chairs | |

| Guest Chairs | |

| Tables | Conference Tables |

| Desks | |

| Other Tables | |

| Storage Units | Filing Cabinets |

| Bookcases & Shelving | |

| Sofas / Soft Seating | |

| Booths & Office Dividers | |

| Other Office Furniture (Stools, Reception, Accessories) |

By Material

| Wood |

| Metal |

| Plastic & Polymer |

| Other Materials |

By Price Range

| Economy |

| Mid-range |

| Premium |

By End-user

| Corporate Offices |

| Healthcare Offices |

| Educational Institutions |

| Government & Public Offices |

| Hospitality & Retail Back-office |

| Others |

By Distribution Channel

| B2C / Retail | Home Centers |

| Specialty Furniture Stores | |

| Online | |

| Other Channels | |

| B2B / Direct from Manufacturers |

By Geography

| Ontario |

| Quebec |

| British Columbia |

| Alberta |

| Saskatchewan & Manitoba |

| Atlantic Canada |

| Northern Territories |

| By Product | Chairs | Employee Chairs |

| Meeting Chairs | ||

| Guest Chairs | ||

| Tables | Conference Tables | |

| Desks | ||

| Other Tables | ||

| Storage Units | Filing Cabinets | |

| Bookcases & Shelving | ||

| Sofas / Soft Seating | ||

| Booths & Office Dividers | ||

| Other Office Furniture (Stools, Reception, Accessories) | ||

| By Material | Wood | |

| Metal | ||

| Plastic & Polymer | ||

| Other Materials | ||

| By Price Range | Economy | |

| Mid-range | ||

| Premium | ||

| By End-user | Corporate Offices | |

| Healthcare Offices | ||

| Educational Institutions | ||

| Government & Public Offices | ||

| Hospitality & Retail Back-office | ||

| Others | ||

| By Distribution Channel | B2C / Retail | Home Centers |

| Specialty Furniture Stores | ||

| Online | ||

| Other Channels | ||

| B2B / Direct from Manufacturers | ||

| By Geography | Ontario | |

| Quebec | ||

| British Columbia | ||

| Alberta | ||

| Saskatchewan & Manitoba | ||

| Atlantic Canada | ||

| Northern Territories | ||

Key Questions Answered in the Report

How large will the Canada office furniture market be by 2031?

Forecasts place the value at USD 4.67 billion.

Which product segment is growing the fastest?

Sofas and soft seating are projected at a 4.21% CAGR due to demand for residential-style comfort zones.

What factors are driving sustainability demand?

Federal and provincial green-procurement rules plus EPR mandates push buyers toward FSC-certified and circular-economy furniture.

Why are acoustic pods gaining traction?

Open-plan offices need quiet rooms for video calls, and modular pods offer fast installation without permanent walls.

Which province shows the strongest growth outlook?

Alberta leads on the back of energy-sector recovery and infrastructure spending.

How are manufacturers countering raw-material volatility?

Many shift to recycled polymers, sign flexible supply contracts, and redesign products to reduce steel and hardwood content.

Page last updated on: