Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

| Market Size (2026) | USD 9.40 Billion |

| Market Size (2031) | USD 13.21 Billion |

| Growth Rate (2026 - 2031) | 7.04% CAGR |

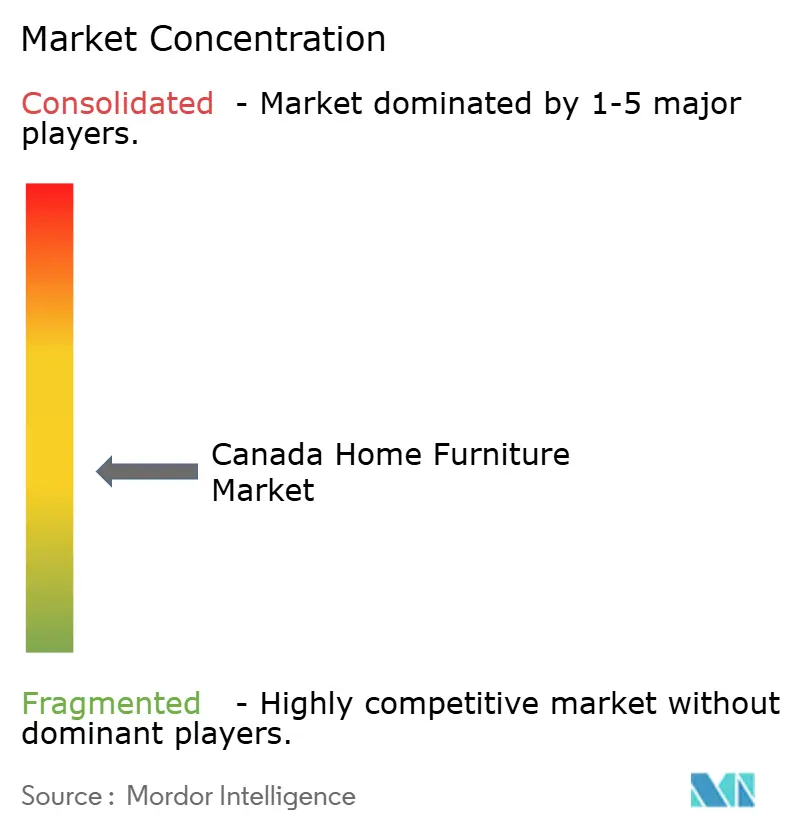

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Home Furniture Market Analysis by Mordor Intelligence

The Canada home furniture market size is estimated at USD 9.40 billion in 2026, and is expected to reach USD 13.21 billion by 2031, at a CAGR of 7.04% during the forecast period (2026-2031). Growth outpaces domestic output trends and reflects durable demand anchored in demographics, housing activity, and household spending. The sector’s performance from 2020 to 2025 showed resilience to rate volatility and supply chain disruption, which left room for recovery as logistics normalized. Easing policy rates and steadier mortgage renewal dynamics are expected to support transactions and renovations that were delayed, lifting categories tied to move-ins and space upgrades. A gradual recovery in housing starts, combined with sustained renovation outlays, underpins baseline volume for the Canada home furniture market through the forecast window.

Key Report Takeaways

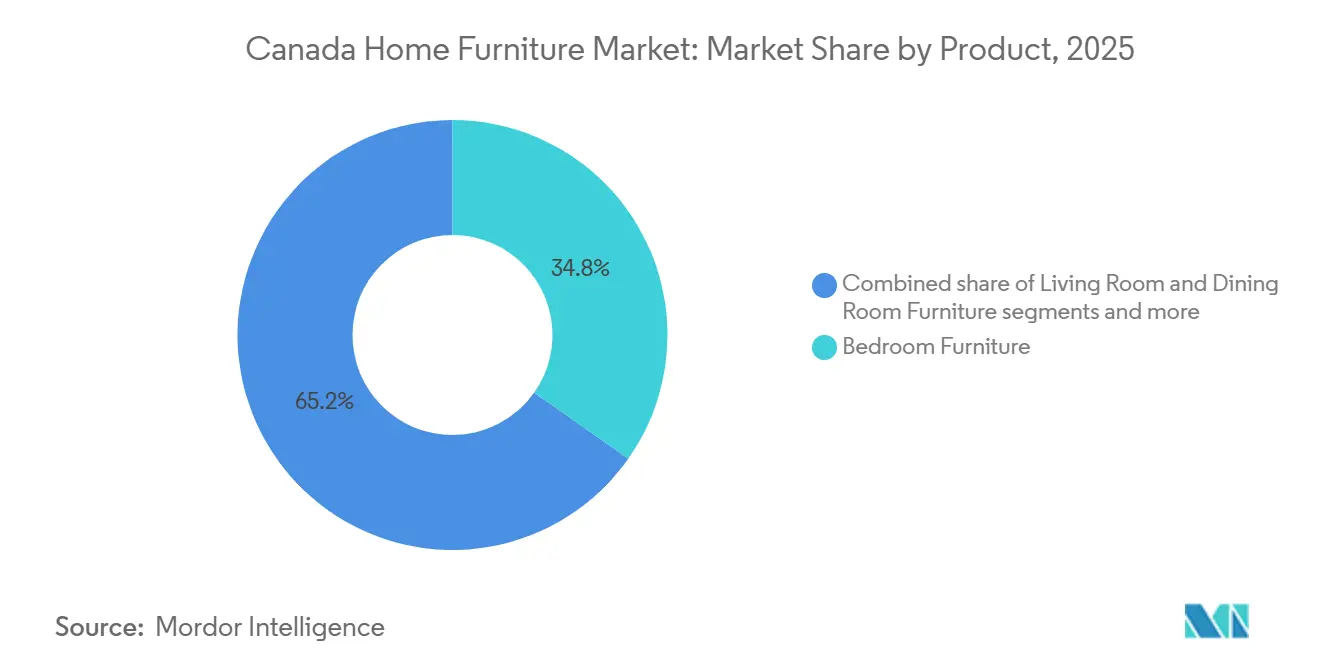

- By product, bedroom furniture led with 34.76% of the Canada home furniture market size in 2025, and home office furniture is forecast to expand at a 9.84% CAGR through 2031.

- By material, wood held 46.37% of the Canada home furniture market share in 2025, and plastic and polymer materials are projected to grow at an 8.48% CAGR to 2031.

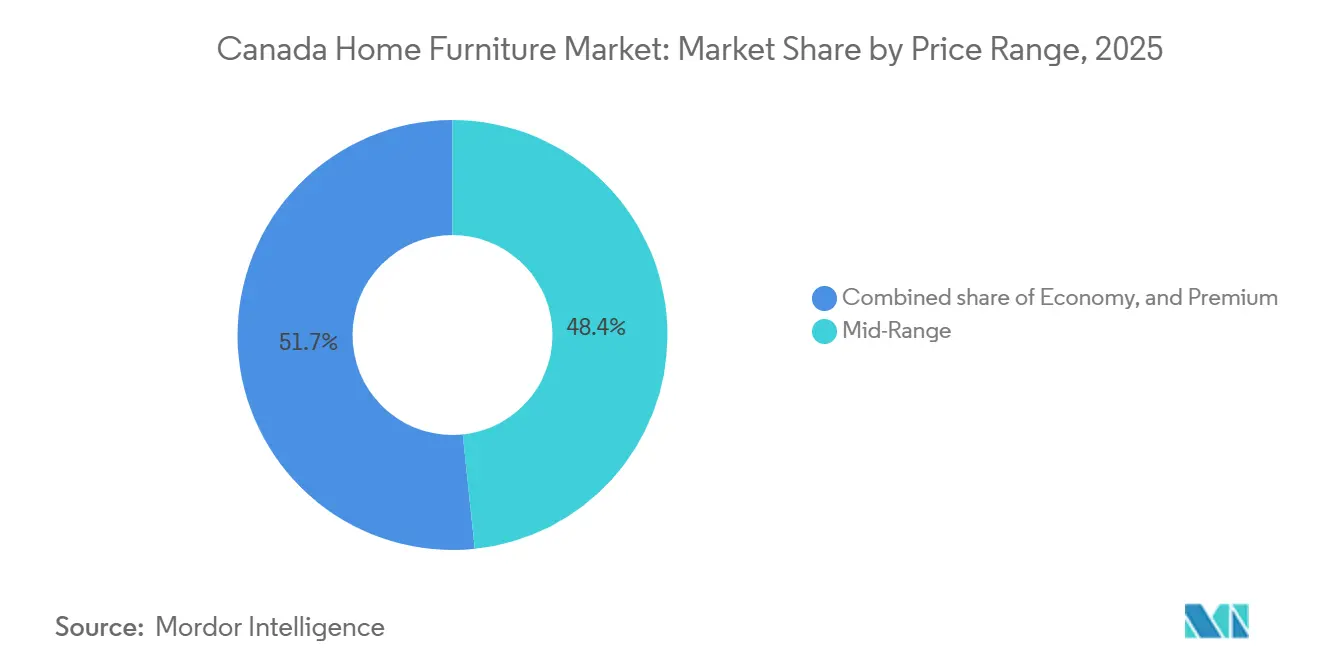

- By price range, mid-range captured 48.35% of the Canada home furniture market share in 2025, while premium is projected to grow at an 11.05% CAGR through 2031.

- By distribution channel, specialty furniture stores accounted for 33.46% of the Canada home furniture market share in 2025, and online is projected to grow at a 12.36% CAGR through 2031.

- By geography, Ontario held 41.37% of the Canada home furniture market share in 2025, while British Columbia is projected to grow at an 11.87% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Canada Home Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Condominium Expansion In Major Urban Centers Driving Modular Furniture Adoption | 1.2% | Toronto, Vancouver, with spillover to Montreal | Medium term (2-4 years) |

| Accelerating Residential Renovation Activity Boosting Furniture Replacement Demand | 0.9% | National, with concentration in Ontario and Quebec | Short term (≤ 2 years) |

| Direct-To-Consumer E-Commerce Platforms Expanding Market Reach With Enhanced Logistics | 0.8% | National, with higher penetration in urban centers | Medium term (2-4 years) |

| New Immigrant Household Establishment Creating Entry-Level Furniture Demand | 0.7% | National, with concentration in major metropolitan areas | Long term (≥ 4 years) |

| Government Sustainability Programs Incentivizing Eco-Certified Wood Product Purchases | 0.6% | British Columbia, Quebec, Ontario | Medium term (2-4 years) |

| Smart Furniture Integration And Connected Home Technology Adoption | 0.5% | National, with early adoption in urban affluent segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Condominium Expansion In Major Urban Centers Driving Modular Furniture Adoption

Purpose-built rental starts surged in 2025, with government-backed CMHC financing underpinning an estimated 88% of new rental construction, according to the Canada Mortgage and Housing Corporation Fall 2025 Housing Supply Report. Calgary and Edmonton remain on track for record-high starts, yet Toronto and Vancouver condominium markets have decelerated sharply due to investor pullback and presale softness. Toronto's housing starts declined 34% year-over-year to 20,999 units in 2024, the lowest level since 2009 on a per-capita basis. Despite this supply contraction, housing completions reached 24,110 units in 2024, a 19% increase, sustaining near-term furniture demand. Vancouver's rental vacancy rate hit a 37-year high as record purpose-built completions and rented condominium apartments flooded the market. Urban density mandates and shrinking unit floor plans, averaging under 700 square feet in new Toronto condos, are steering buyers toward space-efficient sectionals, wall-mounted storage, and convertible sofa beds.

IKEA Canada's FY2025 sales reached USD 1.94 billion (CAD 2.80 billion), with the company investing over CAD 400 million since 2023 to expand fulfilment networks in Greater Vancouver and Greater Toronto, enabling same-day delivery for compact modular furniture. Toronto's demographic exodus, 522,191 residents departed the Greater Toronto Area between 2014 and 2024, has not offset the baseline influx from immigration, ensuring durable replacement demand. Regulatory compliance under Health Canada's Regulations Amending the Furniture and Furnishings (Fire Safety) Regulations (SOR/2023-100) mandates labelling for fire safety and eco-friendly materials, indirectly incentivizing manufacturers to highlight sustainable production and flame-retardant certifications as value-added features.

Accelerating Residential Renovation Activity Boosting Furniture Replacement Demand

Renovation investment commanded 56% of all residential capital expenditure in 2024, totalling USD 71.59 billion (CAD 103 billion) versus USD 59.78 billion (CAD 86 billion) for new housing construction, according to Altus Group's November 2025 market analysis. After three consecutive years of post-pandemic decline, real renovation spending stabilized in mid-2025, with home-improvement retail sales trending upward as homeowners prioritize structural upgrades, energy retrofits, and aging-in-place modifications. The 65+ cohort will expand rapidly through 2030, driving accessibility enhancements and bathroom reconfigurations that necessitate complementary furniture replacements.

The federal Home Energy Loan Program disbursed over USD 3.8 million (CAD 5.5 million) in 2024 for 250-plus net-zero renovation projects, including window and door replacements that often trigger coordinated interior furniture updates. Mortgage-rate resets continue to drain discretionary budgets; however, homeowners locked into existing properties are redirecting capital toward renovations rather than trading up, sustaining demand for replacement bedroom sets, kitchen seating, and living-room configurations. British Columbia construction costs rose 5–8% annually in 2025, with skilled-labour shortages and material tariffs inflating project budgets, yet renovation remains more accessible than new-build entry. The Bank of Canada's October 2024 Monetary Policy Report projected residential investment growth of approximately 6% in 2025 and 2026, buoyed by declining interest rates and rising house prices that support homeowner equity for renovation financing.

New Immigrant Household Establishment Creating Entry-Level Furniture Demand

Canada's population surpassed 41 million in April 2024, with immigration accounting for 98% of 2023 growth, according to Immigration, Refugees and Citizenship Canada's 2025–26 Departmental Plan. The federal government introduced the 2025-2027 Immigration Levels Plan to moderate pressures on housing and infrastructure, setting permanent resident admissions at 395,000 for 2025, declining to 365,000 by 2027, a reduction of approximately 21% from pre-2025 targets, and capping new temporary residents at 673,650 in 2025, down to 543,600 by 2027, with a long-term goal to reduce temporary residents to less than 5% of the population by end-2026.

Despite these reductions, net immigration remains robust: over 40% of 2025 permanent resident admissions transition from students or workers already residing in Canada, ensuring continuity of housing turnover and furniture demand. Calgary and Edmonton experienced population increases of 120.8% and 86.8%, respectively, between 1994 and 2024, according to RE/MAX Canada's October 2025 housing market report, driving rental and owner-occupied housing formations that underpin first-time furniture purchases. CMHC's December 2025 rental-market analysis notes that tenants are more mobile in 2025 owing to increased vacancy rates (national purpose-built vacancy climbed to 3.1%), and landlords compete with incentives such as one to two months of free rent, free appliances, and moving allowances, all of which indirectly stimulate furniture and household-goods spending.

Direct-To-Consumer E-Commerce Platforms Expanding Market Reach With Enhanced Logistics

Direct-to-consumer models that emphasize free returns, modular packaging, and flexible delivery options reduce buyer hesitation on large items while lowering distribution costs. The path to purchase increasingly blends online research with showroom trials, which is strengthened by planning tools and services that simplify configuration and measurement. Companies that integrate visualization features and streamlined reverse logistics convert higher-value orders as customers gain confidence in fit and finish. This evolution improves access to a wider assortment and supports regional coverage beyond legacy store networks in the Canada home furniture market. As large incumbents invest in distributed fulfillment and self-serve planning studios, the competitive bar for service experience continues to rise across both digital and physical channels.

Free-return logistics remove purchase barriers for bulky goods; logistics providers report that holiday shoppers tolerate weeklong delivery waits in only 23% of cases, pressuring retailers to meet fast-shipping standards. Canada Border Services Agency data show commercial releases processed climbed to approximately 29.5 million in FY 2024-2025, up from 25.3 million the prior year, with e-commerce low-value shipments rising exponentially and prompting regulatory amendments effective January 1, 2026, clarifying importer liability for duties and taxes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Elevated Borrowing Costs Constraining Housing Transactions And Furniture Purchases | -0.5% | National, with higher impact in Toronto and Vancouver | Short term (≤ 2 years) |

| Supply Chain Disruptions Extending Product Delivery Timelines | -0.4% | National, with greater impact on coastal regions | Short term (≤ 2 years) |

| Cross-Border Pricing Pressure From U.S. Manufacturers Under Free Trade Agreement | -0.3% | National, with concentration in border regions | Medium term (2-4 years) |

| Rising Consumer Debt Levels Limiting Discretionary Furniture Spending | -0.3% | National, with higher impact in major urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Elevated Borrowing Costs Constraining Housing Transactions And Furniture Purchases

The policy-rate cutting cycle that began in 2024 reduced pressure on some borrowers, but mortgage renewals continue to lift monthly payments for many households, limiting discretionary budgets for big-ticket goods. Toronto and Vancouver experienced declines in new housing starts in the first half of 2025, which tempered order pipelines connected to unit completions and move-ins for the Canada home furniture market [1]CMHC-SCHL.GC.CA https://www.cmhc-schl.gc.ca/media-newsroom/news-releases/2025/slowdown-toronto-vancouver-leave-national-housing-starts-flat-first-half-2025. . The impact has been most visible in categories tied to major room purchases, where some consumers traded down from premium toward mid-range assortments while delaying non-essential upgrades. The effect is uneven across regions and price tiers, and demand has held better in areas with stable employment and more affordable entry pricing. Expectations for gradual stabilization improve forward visibility for retailers as rate-sensitive consumers adjust to new payment levels and renovation activity bridges gaps created by slower new construction.

Supply Chain Disruptions Extending Product Delivery Timelines

In August 2024, shutdowns at the Port of Vancouver and freight stoppages by Canadian National Railway and Canadian Pacific Kansas City Limited caused significant delays in freight and passenger rail networks, as noted in the Canadian Transportation Agency's 2024–2025 Annual Report. Record flooding and extreme cold worsened rail disruptions. Statistics Canada's July 2025 building construction price index highlighted that U.S. tariffs and Canada's countermeasures increased price volatility and material shortages, delaying projects. Skilled labor shortages raised wages, while low building activity and delayed projects intensified competition, pressuring margins.

Ocean Network Express adjusted Asia–North America routes in October 2025, suspending the PS5 service, impacting Canadian importers. U.S. port fees, effective October, could cost Cosco Shipping USD 1.53 billion and OOCL USD 654 million in 2026, with potential cost transfers to shippers, including Canadian furniture importers. The Canada Border Services Agency's October 2025 review raised financial security requirements for release-prior-to-payment (RPP) privileges, with non-compliance by January 15, 2026, leading to prepayment of duties and taxes. Radiant Freight's September 2025 update reported 65% of Ontario carriers as non-compliant with labour laws, risking ground freight disruptions. Holiday shoppers demand fast shipping, but port and carrier delays extended delivery times for bulky imported furniture by two to three weeks, reducing customer satisfaction and conversion rates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Home Office Surges Amid Hybrid-Work Permanence

Bedroom furniture held 34.76% of the Canada home furniture market share in 2025, supported by replacement cycles and the integration of storage into beds and case goods. Home office furniture is the fastest-growing product category, with the Canadian home furniture market size for home offices projected to expand at a 9.84% CAGR through 2031, as hybrid work remains a durable trend. The category includes height-adjustable desks, task seating with ergonomic support, and modular shelving that integrates well with living areas. Spending on furniture, furnishings, and floor coverings was substantial in 2025, reflecting a sustained allocation of household funds to residential upgrades.[2]STATCAN.GC.CAhttps://www150.statcan.gc.ca/t1/tbl1/en/tv.action?pid=3610010701. These dynamics support steady order flow for bedroom sets while creating a growth runway for desks, chairs, and storage designed for blended professional and residential use.

Living room and dining room furniture, the second-largest cluster, benefits from open-concept layouts that favor adaptable tables and modular seating. Kitchen furniture extends these preferences as more floor space is planned for cooking and dining zones in new and renovated homes. Bathroom furniture remains a smaller niche but rises with premium remodels that emphasize storage and materials aligned with indoor air-quality standards. Outdoor segments track seasonal cycles yet gain from the prioritization of livable outdoor space and weather-resilient materials. Other furnishings, including accent seating, entryway storage, and specialty pieces, round out household purchases across move-in and renovation cohorts.

By Material: Wood Dominance Meets Polymer Innovation

Wood accounted for 46.37% of 2025 revenue, supported by perceptions of durability and the wide availability of certified, traceable supply chains. Eco-certifications like FSC continue to expand across supply chains, reinforcing trust in provenance and sustainable practices for the Canada home furniture market. Public-sector green procurement and institutional buyers increasingly reference eco-labels and standards, which translates into stronger visibility for certified wood offerings. Manufacturers also emphasize low VOC finishes and transparent chain-of-custody documentation to meet consumer expectations.

Plastic and polymer alternatives represent the fastest-growing material set, with the Canada home furniture market size for plastic and polymer projected to expand at an 8.48% CAGR through 2031. The segment benefits from design-for-disassembly approaches and recycled-content integration that aligns with circularity objectives. Federal policies on product sustainability and single-use plastics reinforce consumer awareness of material choices, which strengthens interest in recyclable and low-waste designs. Metal furniture maintains a stable share, particularly in frames and utility pieces used in both residential and office settings. Other materials, such as glass, rattan, and hybrid composites, capture niche aesthetics and often sit at higher price points that reward craftsmanship and unique finishes.

By Price Range: Premium Surge Signals Upgrading Appetite

Mid-range offerings captured 48.35% of sales in 2025, balancing quality and price while serving the largest share of households in the Canada home furniture market. Premium outpaced all tiers with an expected 11.05% CAGR through 2031, reflecting willingness to pay for design, materials, and smart features such as integrated charging and app-enabled adjustability. Economy-tier demand remains essential for first-time buyers and rental households, though growth trails as consumers prioritize longevity and features over the lowest upfront prices. Steadier mortgage renewal paths and gradual rate normalization bolster confidence for mid-market purchases as households plan multi-year upgrades. Premium positioning increasingly leverages recognized sustainability and safety marks in specifications, which support procurement in higher-end residential projects.

Value for money remains a strategic battleground as large-format retailers deploy price investments and supply-chain efficiencies to defend volume. IKEA’s price investments across hundreds of products in FY25, combined with expanded planning and pickup points, illustrate tactics to balance accessibility and experience in the Canada home furniture market.[3]https://www.ikea.com/ca/en/files/pdf/10/b9/10b92822/ikea-canada-summary-report-2025-en-digital.pdfIKEA.COM. Population inflows and household formation trends add a supportive base, even as immigration targets evolve and housing supply constraints persist in select regions. Renovation activity continues to absorb demand from incumbent homeowners who prioritize upgrades instead of relocations, further benefiting mid-range and premium products with design and durability features. Certifications around materials, energy, and social responsibility help premium collections stand out in specification-driven purchases for live-work spaces.

By Distribution Channel: Online Advances Amid Omnichannel Integration

Specialty furniture stores accounted for 33.46% of 2025 sales, reflecting the value of in-store consultation and tactile evaluation in considered purchases for the Canada home furniture market. Online is the fastest-growing channel with a projected 12.36% CAGR to 2031, supported by visualization tools, curated assortments, and faster delivery options. Retailers are expanding planning studios and design consultation points to connect digital journeys with in-person services, improving confidence in large-ticket orders. IKEA’s Plan & Order Points provide convenient access to planning support and pickup as part of a seamless model across formats. This blend of in-store and online tools continues to reshape the path to purchase and fulfillment.

Direct-to-consumer brands compress costs by owning design and last-mile logistics, and some are layering showrooms to enable try-before-you-buy experiences. CouchHaus opened a physical showroom in 2024 to complement its e-commerce model, underscoring the value of showrooming for modular seating and configuration advice.[4]COUCHHAUS.COM https://www.couchhaus.com/blogs/featured/canadian-brand-couchhaus-opens-first-retail-store-1. Among scaled incumbents, IKEA reported USD 551.2 million (CAD 793 million) in online transactions in FY25, representing 28.3% of retail sales as the company deepened omnichannel capabilities. Continued investment in planning, pickup, and distribution capacity helps retailers manage delivery times, reduce returns, and maintain margins despite channel mix shifts. Channel strategies now prioritize assortment curation and service layers that align with hybrid living, which keeps online momentum balanced with the role of physical stores.

Geography Analysis

Ontario anchors the Canada home furniture market with 41.37% of 2025 sales, supported by the Greater Toronto and surrounding regions’ depth of demand. Larger-format condo designs and household formation tied to population inflows shape purchasing across bedroom, living, and home-office categories. National housing starts softened in Toronto and Vancouver in the first half of 2025, but steady renovation activity provided a counterweight for furniture demand related to existing homes. Retail investments such as IKEA’s distribution expansion in the Greater Toronto Area underpin service levels and delivery coverage for the province’s dense customer base. The need to close the national housing gap adds structural support for spending on furniture as households prioritize functional upgrades during longer occupancy cycles.

British Columbia is the fastest-growing geography with an expected 11.87% CAGR, balancing affordability adjustments with construction momentum outside of the urban core. Regional consumers show high engagement with certified wood and sustainability claims, which supports premium adoption for materials verified by chain-of-custody programs. Renovation activity and new household formation in cities beyond Metro Vancouver sustain category demand for durable seating, storage, and bedroom ensembles. The province’s supply dynamics favor vendors that can meet indoor air-quality and material-safety standards across price tiers for the Canada home furniture market. Retailers continue to invest in service coverage and logistics agility to ensure lead-time reliability during seasonal peaks.

Quebec and the Atlantic provinces contribute steady growth with mixed demand drivers across rental and ownership segments, while the Prairies benefit from favorable economic conditions and steady migration flows. Renovation-led demand plays a material role where new construction timing is stretched, which supports mid-range and premium segments with storage, workspace, and multi-use features. Quebec’s manufacturing heritage and wood-processing cluster support local supply relationships, including certified inputs that reinforce eco-positioning in the Canada home furniture market. The Atlantic region’s purpose-built rental activity continues to underpin furniture purchases tied to new leases and replacements. Softwood lumber trade developments and related input-cost shifts remain on watch lists for supply planners as vendors manage pricing and sourcing strategies.

Value Chain Analysis

The Canada home furniture value chain starts with inputs (lumber and engineered wood, metal components, plastics and polymers, foams and textiles, adhesives and coatings) from domestic suppliers and imports, then progresses through design, cutting and machining, upholstery, finishing, assembly, packaging, and quality testing. Domestic manufacturing is concentrated in Central Canada, with Ontario reported as having 1,660 furniture manufacturing establishments as of June 2025 and Quebec 1,276, supporting clusters of component suppliers and skilled labor that feed both branded manufacturers and private-label programs.

Downstream, products move through a mix of direct import programs, national retailers, specialty furniture stores, and growing online and direct-to-consumer models. Distribution and last-mile delivery are major cost and service differentiators for bulky goods; for example, Leon's Furniture Limited disclosed a centralized network of 22 delivery warehouse centers and more than 4 million square feet of distribution space (late 2024). The value chain has also been shaped by logistics and compliance friction points, including disruptions tied to ports and rail, as well as the Canada Border Services Agency's tighter requirements for release-prior-to-payment (RPP) financial security, with a compliance deadline of January 15, 2026. These changes can shift working-capital needs for import-heavy assortments and affect how inventory is positioned closer to demand centers.

Competitive Landscape

The Canada home furniture market features a mix of global brands, regional manufacturers, and direct-to-consumer entrants, creating moderate fragmentation and sustained competitive intensity. IKEA, Ashley Furniture, Palliser, EQ3, and Dorel Industries comprise a leading cohort serving broad price points and distribution formats. In FY25, IKEA Canada reported USD 1.94 billion (CAD 2.80 billion) in retail sales and USD 551.2 million (CAD 793 million) in online transactions, equal to 28.3% of retail sales, while continuing price investments across more than 550 products and expanding planning points to support omnichannel growth. Ashley Furniture advanced a category-expansion strategy by acquiring Resident, the parent of Nectar and other sleep brands, positioning the company to integrate direct-to-consumer bedding with its store network. These moves frame a competitive field where scale, digital reach, and supply-chain efficiency are central to share gains.

Dorel Industries undertook a deep restructuring of its home segment through 2025, including facility closures, workforce reductions, SKU rationalization, and financing actions to stabilize operations. The segment’s reported Q3 2025 revenue was USD 78.3 million alongside actions to streamline e-commerce exposure and focus on profitability in 2026. New financing facilities, including senior secured credit and preferred equity, provide runway for repositioning while manufacturing exits reorient the portfolio. These adjustments illustrate how balance sheet strengthening and focused assortment can support recovery efforts amid softer demand and evolving channel mix.

Innovation priorities include modular design, sustainability verification, and service models that reduce friction for large-ticket purchases. La-Z-Boy reported broad-based operational efficiency gains in FY25 through its TranZform initiative and verified that all wood sourced for La-Z-Boy-branded products met sustainable criteria, signaling alignment with consumer expectations for responsibly sourced materials in the Canada home furniture market. Vendors continue to align with specifications such as BIFMA e3 for office-related furnishings as hybrid work sustains demand for professional-grade products in residential settings. RH continued to refresh modern assortments and to adjust its sourcing footprint, highlighting the role of design leadership and supply diversification in premium performance.

Canada Home Furniture Industry Leaders

IKEA

Ashley Furniture Industries Inc.

Palliser Furniture Upholstery Ltd.

EQ3

Dorel Industries Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Technology-enabled product development and shopping journeys are opening room for modular, configurable furniture and faster iteration on new collections. Cozey (Montreal) highlighted this direction in June 2026 by integrating AI tools into design processes, updating tech packs, and using 3D printing to accelerate prototyping, supporting shorter development cycles and more localized assortment tuning. On the customer acquisition and conversion side, retailers and brands are expanding micro-format showrooms and deploying richer visualization tools, including AR in mobile apps, to reduce fit-and-finish uncertainty and returns for online big-ticket purchases.

Circularity and verifiable sustainability claims are also becoming more commercialized opportunity areas across materials and sourcing. Urbanjacks (Vancouver, founded 2023) is scaling operations to divert wood waste from landfills into non-structural products such as cabinets and outdoor furniture, aligning with consumer interest in recycled-content and low-waste designs. Channel mix is also shifting toward partnerships and wholesale distribution that reduce fixed store costs; the May 2026 exit of Yankee Candle from Canadian brick-and-mortar retail, alongside a pivot to wholesale partners such as Canadian Tire and Walmart and continued e-commerce focus, illustrates how brands are adjusting distribution models that furniture players can adapt.

Recent Industry Developments

- May 2026: Palliser Furniture completed its acquisition by China-based MotoMotion (May 29, 2026), following a period of operating pressure tied to trade and input-cost volatility. The transaction excluded EQ3 and its Canadian manufacturing operations, keeping that brand on a separate path while Palliser sought greater stability for supply and operations.

- May 2026: IKEA Canada opened a new Plan and Order Point in Gatineau, Quebec, extending access to planning services and order placement without a full-size store footprint. The move supports omnichannel expansion into additional catchment areas and helps shorten the path from digital browsing to assisted purchase for large-ticket furniture.

- April 2024: CouchHaus opened its first retail showroom on Granville Street in Vancouver to complement its e-commerce-led model. The physical format adds in-person configuration support and visualization for modular seating, reinforcing the shift toward hybrid retail journeys for considered furniture purchases.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Canada home furniture market is defined as the annual value of new indoor and outdoor furniture purchased by households in Canada through retail stores and digital channels, measured at final transaction prices.

Scope exclusions: Used furniture, office or contract furniture, fitted cabinets sold with real estate, and decor accessories are excluded from this market sizing.

Segmentation Overview

- By Product

- Living Room and Dining Room Furniture

- Bedroom Furniture

- Kitchen Furniture

- Home Office Furniture

- Bathroom Furniture

- Outdoor Furniture

- Other Furniture

- By Material

- Wood

- Metal

- Plastic & Polymer

- Others

- By Price Range

- Economy

- Mid-Range

- Premium

- By Distribution Channel

- Home Centers

- Specialty Furniture Stores

- Online

- Other Distribution Channels (includes hypermarkets, supermarkets, teleshopping, warehouse clubs, departmental stores, etc.)

- By Geography

- Atlantic

- Quebec

- Ontario

- British Columbia

- Rest of Canada

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with public data that shows how furniture demand is moving across Canada and across provinces. We reviewed sources such as Statistics Canada retail trade and household spending releases, Canada Border Services Agency and UN Comtrade trade statistics for furniture-related HS codes, and Bank of Canada and Statistics Canada CPI series to understand price movement.

To ground industry structure and product coverage, we also referred to sources such as the Government of Canada tariff schedules, industry association publications, and company annual reports and investor presentations for mix and channel commentary. In parallel, we used paid database subscriptions for company financials and news checks, and for patent lookups where product design trends matter for mix shifts. These sources are illustrative, and many other public datasets, filings, and articles were also used to collect data, validate assumptions, and clarify gaps.

Primary Interviews and Surveys

Primary inputs were gathered through expert interviews and structured surveys with retailers, brands, distributors, and supply chain participants that touch home furniture sales in Canada. Respondent input was used to confirm what is counted as home furniture at checkout prices, and to pressure-test channel splits, price band movement, and regional differences across major provinces and metro areas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 14% | |

| Mid tier: 44% | Functional/Unit leaders: 33% | |

| Smaller Players: 17% | Managers: 53% |

Market-Sizing & Forecasting

Sizing starts from a top-down demand pool build that uses household furniture spend signals and retail receipt trends, then it is shaped into a furniture-only total using category filters that align with how furniture is sold and recorded in Canada. We then corroborate the total with selective bottom-up checks, such as sampled average selling prices multiplied by estimated unit volumes in key categories, and channel checks from major retailers and regional specialists.

A few practical inputs that matter most in this market include household formation and housing turnover, renovation activity, online penetration for bulky goods, import dependence and landed cost pressure, and furniture price inflation versus broader CPI. When a data series is not available at a clean home-furniture level, we bridge gaps using proxy splits from interviews, and we document the adjustment so it can be repeated.

Forecasting is run using scenario analysis supported by regression-style checks on the variables above, since furniture demand tends to move with housing and consumer confidence and not just with population. Assumptions for mix, pricing, and channel shift are finalized only after expert feedback indicates they match what is being seen on the ground.

Data Validation & Update Cycle

Validation is done through multiple passes of cross-checking, where model outputs are compared with independent signals like retail sales direction, trade flow direction, and price movement, followed by checks for unusual jumps by province or channel. When a variance shows up, we revisit the driver, re-check source timing, and re-contact experts if the gap cannot be explained with visible market events.

Before sign-off, the model logic and final totals are reviewed by another analyst so calculation errors and inconsistent assumptions get flagged early. Reports are refreshed annually, with interim updates triggered by material changes such as sharp price swings, policy changes affecting imports, or sudden channel disruptions. Right before delivery, a final review pass is completed so the numbers reflect the latest available data.

Mordor Intelligence's Canada Home Furniture Market Size Compared Against Other Published Estimates

Published market sizes for Canada home furniture often differ because the scope lines are drawn differently and because pricing and channel assumptions are not always handled the same way. Differences show up most when one estimate follows retail transaction value, while another leans on broader industry revenue, wider product baskets, or mixed currencies and years.

The main gap comes from whether adjacent categories are included, where Mordor Intelligence counts only new indoor and outdoor household furniture at final transaction prices and leaves out used items, office or contract furniture, fitted cabinets sold with real estate, and decor accessories, which can shift totals upward in broader definitions.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 9.40 B (2026) | |

| Industry Research Portal A | USD 11.16 B (2025) | Uses a broader furniture and home furnishings basket that includes mattresses and bedding plus decor items, and it is also anchored to a different year, which makes direct comparison to a furniture-only 2026 value difficult. |

| Trade Publication B | USD 14.60 B (2026) | Often presented as total furniture revenue using a CAD-based baseline that can include lighting and other non-furniture categories, and USD conversion timing and channel coverage are not clearly specified. |

Across the three figures, the spread is explained mostly by what gets counted as furniture versus furnishings, and by whether the number is tied to final checkout prices or to a broader revenue pool. Our approach stays traceable because each adjustment is linked to a clear inclusion rule, a visible demand indicator, and a repeatable check against trade and price signals.

Key Questions Answered in the Report

What is the current size and growth outlook for the Canada home furniture market?

The Canada home furniture market size reached USD 9.40 billion in 2026 and is projected to reach USD 13.21 billion by 2031 at a 7.04% CAGR.

Which product categories lead growth within Canada’s home furniture space?

Bedroom furniture led 2025 revenue, while home office furniture is the fastest-growing category, supported by hybrid work and functional storage adoption.

How is channel mix evolving for furniture in Canada?

Specialty stores remain important for consultation, but online is growing fastest, supported by planning tools and improved fulfilment coverage among large retailers.

Which regions are most important to demand in Canada?

Ontario accounted for 41.37% of 2025 sales, and British Columbia is forecast to be the fastest-growing region through 2031, reflecting both household formation and construction dynamics.

Page last updated on: