Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 22.15 Billion |

| Market Size (2026) | USD 22.74 Billion |

| Market Size (2031) | USD 25.93 Billion |

| Growth Rate (2026 - 2031) | 2.66% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Motor Insurance Market Analysis by Mordor Intelligence

The Canada Motor Insurance Market size in terms of premium value is expected to grow from USD 22.15 billion in 2025 to USD 22.74 billion in 2026 and is forecast to reach USD 25.93 billion by 2031 at 2.66% CAGR over 2026-2031.

Catastrophic weather losses, rising advanced-vehicle repair costs, and federal zero-emission targets are reshaping risk pools. However, established pricing models and capital buffers keep the market growing steadily. Record insured weather losses of CAD 8.5 billion in 2024 are accelerating demand for comprehensive coverage, while electric vehicles (EVs) command higher premiums because repair bills average CAD 6,795 versus CAD 5,122 for conventional cars. Provincial regulations guide premium trajectories, with Ontario’s complex tort system supporting the largest premium base and Alberta’s pending no-fault model spurring the fastest growth. Distribution is shifting as the majority of drivers are willing to share driving data for personalized rates, prompting incumbent carriers to scale telematics and digital aggregator partnerships.

Key Report Takeaways

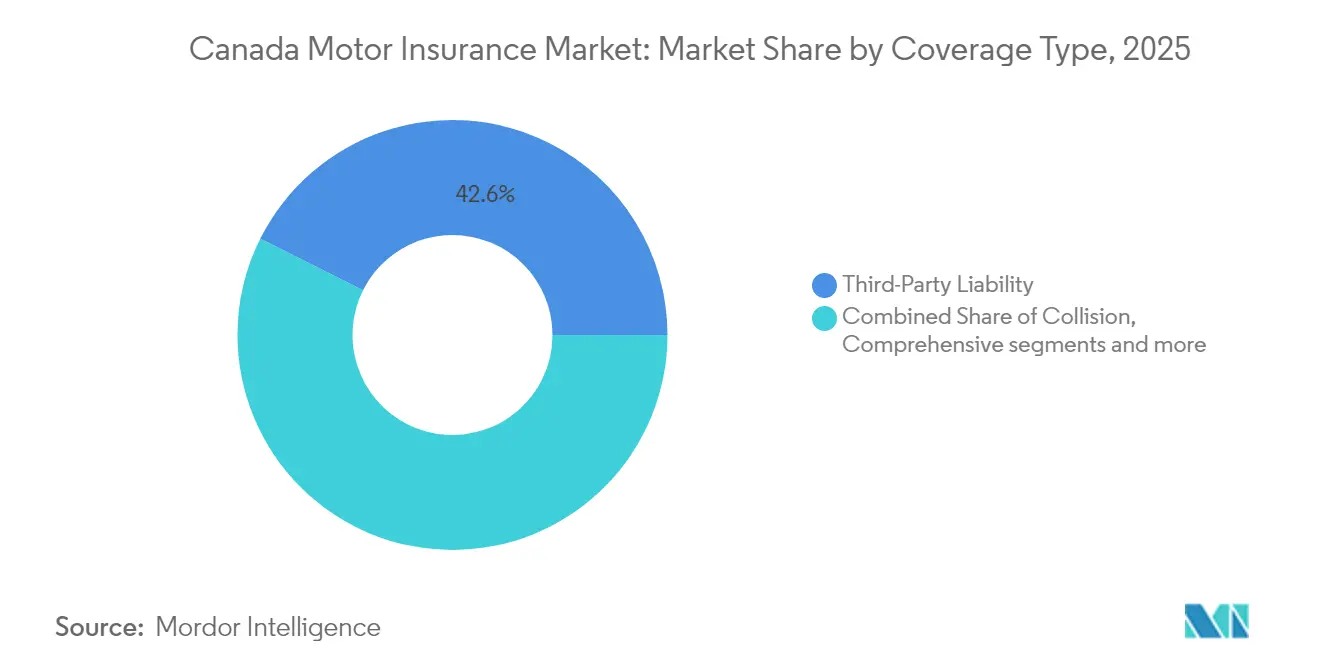

- By coverage type, third-party liability led with 42.62% revenue share in 2025; comprehensive coverage is advancing at a 6.74% CAGR through 2031.

- By vehicle category, passenger cars accounted for 31.58% of the Canada motor insurance market size in 2025, while electric vehicles are forecast to grow at a 14.31% CAGR between 2026-2031.

- By distribution channel, agents and brokers retained a 64.55% share of the Canada motor insurance market size in 2025; digital aggregators are recording an 11.81% CAGR.

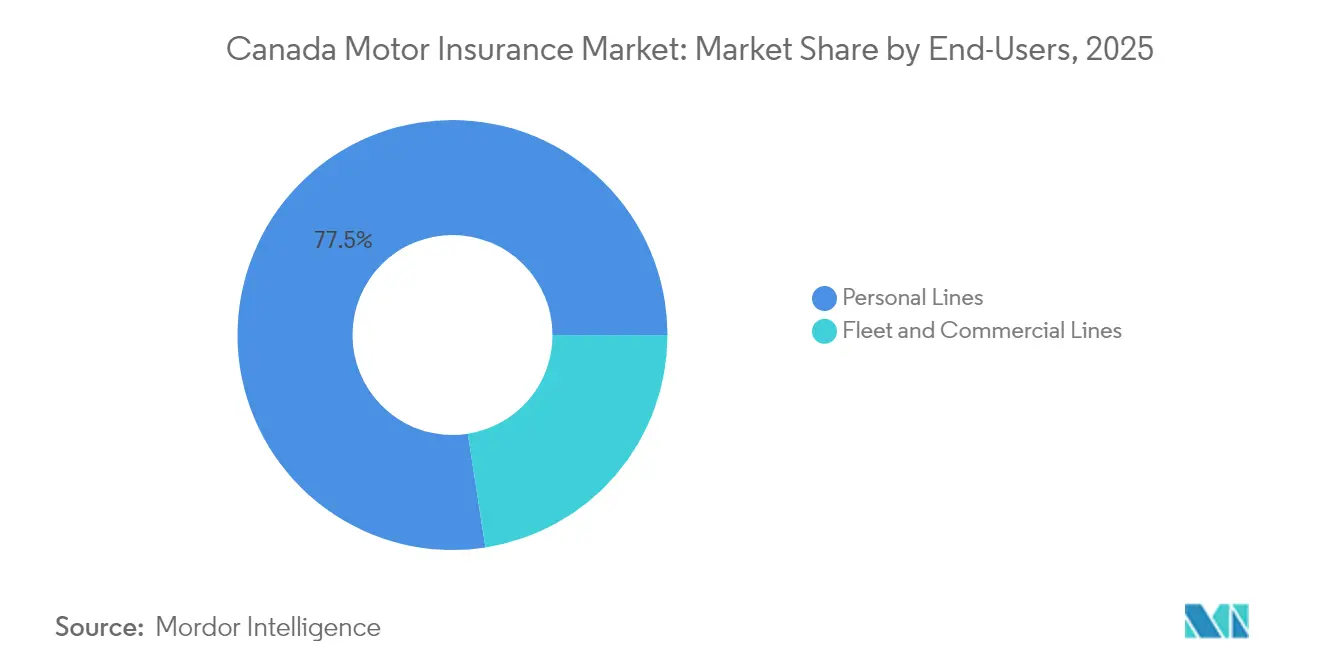

- By end user, personal lines represented 77.45% of the Canada motor insurance market size in 2025, and commercial lines are rising at a 7.12% CAGR.

- By province, Ontario held 38.12% of Canada motor insurance market share in 2025, whereas Alberta is projected to expand at a 5.53% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Motor Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Catastrophic weather events | +0.8% | Alberta, Ontario, Atlantic provinces | Medium term (2-4 years) |

| Rapid EV adoption under federal incentives | +0.6% | Ontario, Quebec, British Columbia | Long term (≥ 4 years) |

| Rising ADAS-related repair costs | +0.4% | Urban centers with newer fleets | Short term (≤ 2 years) |

| Stringent provincial liability limits | +0.3% | Ontario and Alberta | Long term (≥ 4 years) |

| Rising auto theft losses | +0.2% | Ontario and Quebec | Short term (≤ 2 years) |

| Affordability push toward minimum coverage | +0.1% | Price-sensitive markets nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Catastrophic weather events driving comprehensive coverage uptake

Insured storm, wildfire, and flood losses soared to CAD 8.5 billion in 2024, eclipsing prior records and signaling a structural shift in climate risk [1]Insurance Bureau of Canada, “Severe Weather Insurance Losses Reach Record Levels,” ibc.ca. A single Calgary hailstorm produced CAD 3 billion in claims, underscoring how localized events can reshape provincial premium pools. As severe-weather frequency now exceeds the 20-year average by more than 400%, vehicle owners increasingly add comprehensive cover, lifting premium volumes and prompting insurers to refine catastrophe modeling. Carriers are piloting parametric deductibles that trigger faster payouts for weather losses while tightening coastal and wildfire exposure limits. Enhanced satellite forecasting and granular geospatial pricing are becoming core competencies for players that want to sustain underwriting margins amid volatile weather patterns.

Rapid EV adoption under federal iZEV incentives elevating premium pool

The federal iZEV rebate of CAD 5,000 and phased zero-emission sales mandates are accelerating EV penetration, expanding the Canada motor insurance market by drawing higher-premium vehicles into the pool[2]Government of Canada, “Zero-Emission Vehicle Sales Mandate Regulations,” canada.ca. EV premiums climbed 18.9% year-on-year in Q1 2025 because average repair bills and battery replacement costs of CAD 5,000–20,000 often push cars to total loss. The government’s CAD 680 million charging-network program further lowers range anxiety, bolstering adoption. Insurers that build specialist EV repair networks and offer battery degradation add-ons stand to capture premium growth while mitigating loss-ratio volatility.

Rising ADAS-related repair costs are inflating claim severity and premiums

The increasing complexity and cost of repairing advanced driver-assistance systems (ADAS) are significantly impacting the Canadian motor insurance market. By early 2024, the average cost of a repairable claim rose to CAD 5,044, driven in part by the calibration of cameras, sensors, and lidar, adding approximately CAD 1,500 per incident. Concurrently, skilled labor costs escalated to CAD 75 per hour, while extended repair durations have led to longer rental-car usage, further inflating total claim outlays. In response, insurers are proactively investing in certified ADAS-capable repair networks and establishing data-sharing partnerships with OEMs to minimize claims leakage. As Canada moves toward its 2030 goal of universal collision-avoidance technology adoption, these initiatives are critical. Additionally, telematics data, particularly from features like lane-keep assist is being integrated into pricing models, allowing insurers to more accurately balance ADAS safety gains against rising repair costs

Stringent provincial liability limits sustaining premium base

Higher mandatory third-party limits, such as Manitoba’s CAD 500,000 floor, create a consistent premium base even when competition intensifies. Alberta’s incoming no-fault regime promises wider medical and income benefits that extend premium flows, while Ontario’s optional Direct Compensation Property Damage supports price segmentation that attracts value-seeking drivers without compromising coverage adequacy. Consequently, well-capitalized carriers with strong actuarial teams leverage limit increases to balance loss trends, whereas smaller firms struggle to absorb the working-capital hit from larger reserves.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory and taxation challenges | -0.4% | All provinces, different timelines | Long term (≥ 4 years) |

| Public-auto models in BC and Manitoba | -0.3% | British Columbia and Manitoba | Long term (≥ 4 years) |

| Escalating bodily-injury litigation costs | -0.2% | Ontario and Alberta | Medium term (2-4 years) |

| Telematics-enabled UBI margin compression | -0.2% | Ontario and Quebec | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory and taxation challenges

Dual-track filing in Ontario, interim rate caps in Alberta, and evolving AI guidelines increase compliance costs and create approval lags that blunt premium growth[3]Financial Services Regulatory Authority of Ontario, “Guidance on Automobile Insurance Rate Filings,” fsrao.ca. The Global Minimum Tax Act further complicates capital allocation as multinational corporations adjust transfer-pricing structures. While stronger firms absorb the overhead, smaller players risk margin erosion, prompting consolidation. Market participants lobby for streamlined approval windows and consistent AI standards to sustain innovation velocity.

Public-auto models in BC and Manitoba shrink private addressable market

ICBC’s Enhanced Care program has frozen basic rates for six years, using scale and retained earnings to fund injury benefits. Manitoba Public Insurance keeps premiums among the country’s lowest, tightening political pressure on adjacent provinces to mirror public-sector pricing. Private players thus face growth ceilings and must differentiate through add-ons, fleet insurance, and usage-based products rather than core compulsory cover.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Coverage Type: Comprehensive policies accelerate on climate volatility

Third-party liability captured 42.62% of the Canada motor insurance market share in 2025, reflecting mandatory purchase rules. Comprehensive premiums are growing at a 6.74% CAGR as wildfires, floods, and hailstorms raise awareness of physical-damage risks. Collision coverage advances steadily on the back of urban traffic density, while optional glass and roadside add-ons benefit from bundling strategies. Catastrophe modeling and parametric deductibles help carriers price severe-weather volatility and protect the Canada motor insurance market from earnings shocks.

The comprehensive segment’s rising weight improves revenue diversity but increases capital charges, pushing carriers to transfer more risk into reinsurance markets. Provincial initiatives that promote climate-resilient infrastructure may slow claim frequency over time, although insured values will likely remain elevated given higher EV penetration and ADAS equipment costs.

By Vehicle Type: EVs reshape underwriting norms

Passenger cars continued to hold 31.58% of 2025 premium income, yet the electric-vehicle segment is expanding at a 14.31% CAGR thanks to federal zero-emission mandates. Higher battery repair costs and specialized technicians lift EV loss severity and raise the Canada motor insurance market size for this niche. Commercial trucks and light-duty delivery vans post resilient growth amid e-commerce trends, while shared-mobility vehicles remain a small but emerging segment.

As EV repair shops scale, parts costs may normalize, but battery degradation and recycling risks keep underwriting complexity high. Insurers that develop EV-specific coverage—battery warranty extensions, roadside charging—secure an early-mover advantage and deepen presence across the broader Canada motor insurance market.

By Distribution Channel: Hybrid models gain traction

Agents and brokers accounted for 64.55% of written premiums in 2025, leveraging regulatory know-how and claims advocacy. Digital aggregators, however, are growing at 11.81% CAGR as comparison culture spreads. Direct-to-consumer portals from incumbent carriers combine self-serve features with call-center support, forming a hybrid experience that preserves retention while controlling acquisition costs.

Brokers embed robo-advice tools to preserve advisory relevance, whereas pure-play insurtechs use API connectivity to crop underwriting and servicing expenses. These developments expand the overall Canada motor insurance market reach, especially among Gen Z policyholders who expect real-time quotes and policy changes through mobile apps.

By End User: Commercial lines outpace personal

Personal lines contributed 77.45% of premiums in 2025, but fleet and commercial portfolios are forecast to rise 7.12% CAGR through 2031 as logistics and construction rebound. Telematics devices, dashcams, and driver-coaching apps lower accident frequency in commercial fleets, enabling performance-based discounts that grow policies in force and increase the Canada motor insurance market size.

Small-business customers demand tailored deductibles and cargo endorsements, spurring product innovation that boosts fee income. Carriers with specialist underwriting teams and risk-engineering services capitalize on this trend, while personal-line heavyweights face saturated growth and heightened price sensitivity.

By Insurer Ownership: Private carriers leverage agility

Crown corporations in British Columbia, Manitoba, and Saskatchewan constrain private-sector expansion in those provinces. Yet private carriers dominate the rest of the Canada motor insurance market and deploy analytics to refine risk segmentation and claims triage. Intact Financial Corporation’s 92.2% combined ratio in 2024 illustrates scale benefits and disciplined pricing.

Consolidation is reshaping the landscape; Definity’s CAD 3.3 billion purchase of Travelers Canada moves it to fourth place by premium, widening product breadth and IT investment capacity. Private carriers that ally with insurtechs for data enrichment and embedded-insurance pilots will likely widen their lead over regional mutuals that lack modern core systems.

Geography Analysis

Ontario anchors 38.12% of total premiums thanks to dense population, high vehicle penetration, and layered tort benefits that elevate average claim costs. Recent FSRA reforms introduce fast-track filings and greater price transparency, but continued adoption of optional coverages such as Direct Compensation Property Damage keeps pricing flexible. Chronic auto-theft exposures and urban collision frequencies drive sustained demand for comprehensive and collision products.

Alberta is on a 5.53% CAGR trajectory to 2031, buoyed by population inflows and transition to a no-fault model that promises faster benefits and reduced litigation expenses. Interim rate caps temper short-term top-line growth; however, expanded accident-benefits tables are expected to enlarge the Canada motor insurance market size over the forecast horizon. Rising parts costs from potential U.S. import tariffs pose a claims-cost risk but also justify premium recalibration.

Quebec operates a hybrid system where bodily injury is publicly insured, leaving private carriers to compete on property damage and optional add-ons. British Columbia’s public monopoly narrows private opportunity to opt for alternative products but also provides a benchmark for affordability debates nationwide. Atlantic provinces exhibit moderate growth driven by weather-related coverage demand, whereas the Territories remain niche, with high per-vehicle costs tied to sparse repair networks.

Competitive Landscape

The market shows moderate concentration; the five largest private insurers control more than two-thirds of direct premiums. Intact leads with USD 24 billion in operating premiums and continues to invest in AI-driven underwriting and omnichannel service. Economies of scale allow larger carriers to negotiate favorable reinsurance terms and fund R&D in telematics and parametric cover.

Consolidation continues as mid-tier insurers seek diversification. Definity’s pending acquisition of Travelers Canada will create more than USD 6 billion in combined premiums and aims to harvest USD 100 million in cost synergies by unifying claims platforms and broker networks. Smaller mutuals and regional carriers focus on community relationships and niche segments such as classic cars or farm vehicles to avoid direct competition with national giants.

Technology integration is the central strategic lever. 81% of players automate part of the quote workflow, and 88% use algorithmic rating models in underwriting. Investments target cloud-native policy platforms, low-code claims modules, and AI tools that triage photo-based damage estimates in minutes. Players that lag face higher expense ratios and slower product-development cycles, making them likely acquisition targets for larger competitors.

Canada Motor Insurance Industry Leaders

Intact Financial Corporation

Desjardins General Insurance Group

Co-operators General Insurance

Allstate Insurance Company of Canada

Economical Insurance (Definity)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Government of Canada stated auto-theft incidents fell 18.6% in 2024 after investing CAD 28 million in border inspections that intercepted 2,277 stolen vehicles

- January 2025: Insurance Bureau of Canada confirmed CAD 8.5 billion in 2024 severe-weather losses, the highest on record, and urged adoption of climate-resilient building codes.

- May 2025: Definity Financial Corporation agreed to acquire Travelers Canada for CAD 3.3 billion, elevating it to the country’s fourth-largest P&C writer and targeting USD 100 million in synergies

- December 2024: Financial Services Regulatory Authority of Ontario launched a territory-rating pilot in the Greater Toronto Area to move beyond postal code factors and test granular risk variables.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Canadian motor insurance market as all gross written premiums that arise from mandatory and optional cover for road-worthy private and commercial vehicles, including third-party liability, collision, and comprehensive products that are issued by provincially licensed carriers.

Scope exclusion: Reinsurance treaties, extended warranty products, and specialty off-road vehicle policies fall outside this analysis.

Segmentation Overview

- By Coverage Type

- Third-Party Liability

- Collision

- Comprehensive

- Personal Injury Protection

- Optional Add-ons (Roadside, Glass, etc.)

- By Insurer Ownership

- Private

- Public

- By Vehicle Type

- Passenger Cars

- Commercial Vehicles

- Heavy Commercial Vehicles

- Pooled Transport

- Electric Vehicles

- By Distribution Channel

- Agents & Brokers

- Direct Response (Captive / Direct Writers)

- Bancassurance

- Digital Aggregators & Insurtech

- By End User

- Personal Lines

- Fleet & Commercial Lines

- By Region

- Ontario

- Québec

- Alberta

- British Columbia

- Saskatchewan

- Manitoba

- Atlantic Canada (NB, NS, PE, NL)

- Territories (YT, NT, NU)

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed provincial regulators, underwriting heads at multiline carriers, and large brokerage networks across Ontario, Alberta, Québec, and Atlantic Canada to validate premium pools, loss trends, and price elasticity. Follow-up surveys with fleet managers and insurtech founders clarified telematics penetration and average selling prices.

Desk Research

We first mapped statutory and operating metrics that Statistics Canada, the General Insurance Statistical Agency, the Insurance Bureau of Canada, Alberta's Automobile Insurance Rate Board, and the Office of the Superintendent of Financial Institutions publish, and then cross-checked them with open parliamentary committee transcripts on rate reforms. Our team also reviewed aggregate loss-cost trend notes, provincial accident benefit schedules, and vehicle registration data to anchor exposure units. To enrich the picture, D&B Hoovers supplied carrier financial splits, while Dow Jones Factiva flagged material weather-loss events that distorted recent premium growth. Trade association briefings and publicly filed management discussion sections helped us trace emerging usage-based products. These sources are illustrative, not exhaustive.

Market-Sizing & Forecasting

A top-down reconstruction, starting with registered vehicle counts, average written premium per vehicle, and province-level distribution mix, established the 2024 baseline, which was then corroborated through selective bottom-up roll-ups of carrier filings and channel checks. Key fingerprints such as weather-related loss ratios, electric-vehicle parc growth, repair cost inflation, mileage recovery, and regulatory cap adjustments feed a multivariate regression that projects premiums to 2030. Where bottom-up estimates lag in smaller provinces, gap-fill ratios derived from historic premium density were applied before final reconciliation.

Data Validation & Update Cycle

Outputs pass three layers of analyst review, anomaly flags trigger re-contact with primary sources, and published figures refresh each year, with mid-cycle updates when material rate reforms or catastrophic losses emerge. Clients therefore receive the freshest calibrated view.

Why Mordor's Canada Motor Insurance Baseline Commands Confidence

Published estimates often diverge because firms pick different premium definitions, currency bases, and refresh cadences.

Key gap drivers include narrow scopes that drop broker-originated premiums, aggressive scenario multipliers for electric vehicles, or the bundling of non-motor lines under 'property and casualty.' Mordor's disciplined variable selection and annual refresh temper such swings, giving decision-makers a grounded baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 22.15 B (2025) | Mordor Intelligence | - |

| USD 15.18 B (2024) | Regional Consultancy A | Leaves out premiums written through digital aggregators and adjusts to nominal CAD without consistent FX treatment |

| USD 37.5 B (2023) | Trade Journal B | Bundles fleet self-insurance pools and roadside assistance fees into motor premiums, inflating totals |

Taken together, the comparison shows that Mordor Intelligence delivers a balanced, transparent baseline that ties directly to verifiable premium drivers and repeatable steps, helping users steer strategic and regulatory conversations with confidence.

Key Questions Answered in the Report

What is the current size of the Canada motor insurance market?

The market generated USD 22.74 billion in premiums in 2026 and is forecast to reach USD 25.93 billion by 2031.

Which province contributes the most to Canada’s motor insurance premiums?

Ontario leads with a 38.12% share because of its dense population and tort-based benefits structure.

How fast is the electric-vehicle insurance segment growing?

Premiums tied to electric vehicles are projected to rise at a 14.31% CAGR between 2026 and 2031 owing to federal zero-emission mandates and higher repair costs.

Why are comprehensive coverage premiums increasing more quickly than other coverages?

Record weather-related losses and heightened climate-risk awareness are driving a 6.74% CAGR in comprehensive policies.

Page last updated on: