Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

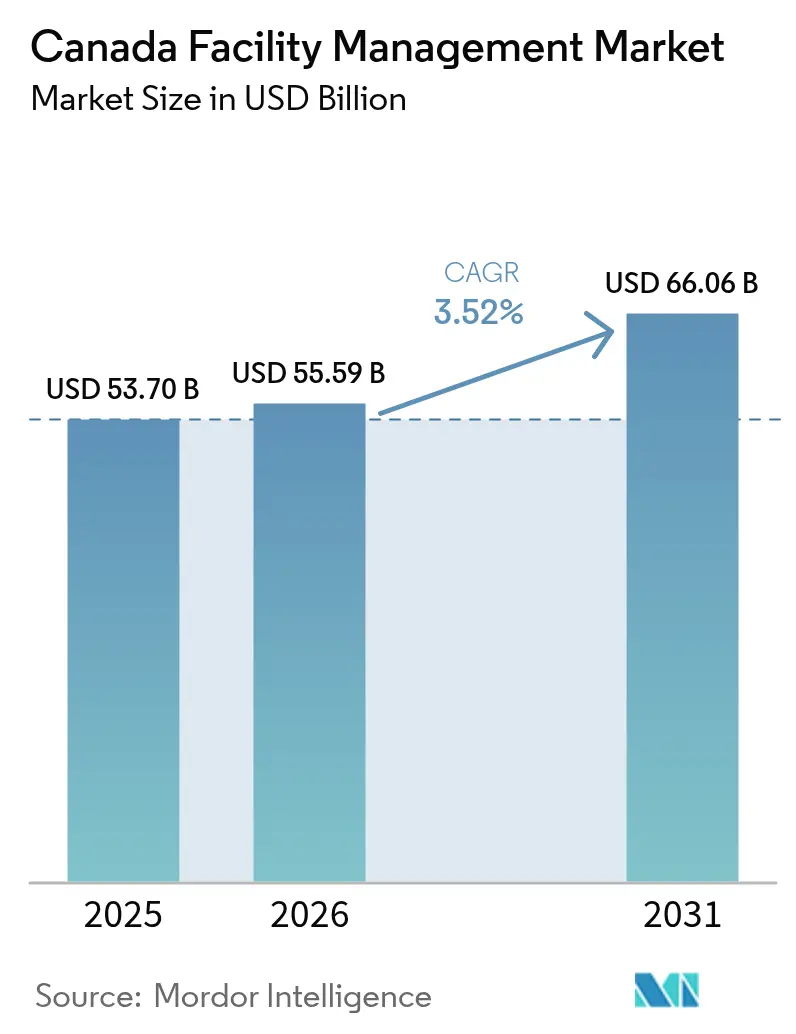

| Base Year Market Size (2025) | USD 53.70 Billion |

| Market Size (2026) | USD 55.59 Billion |

| Market Size (2031) | USD 66.06 Billion |

| Growth Rate (2026 - 2031) | 3.52% CAGR |

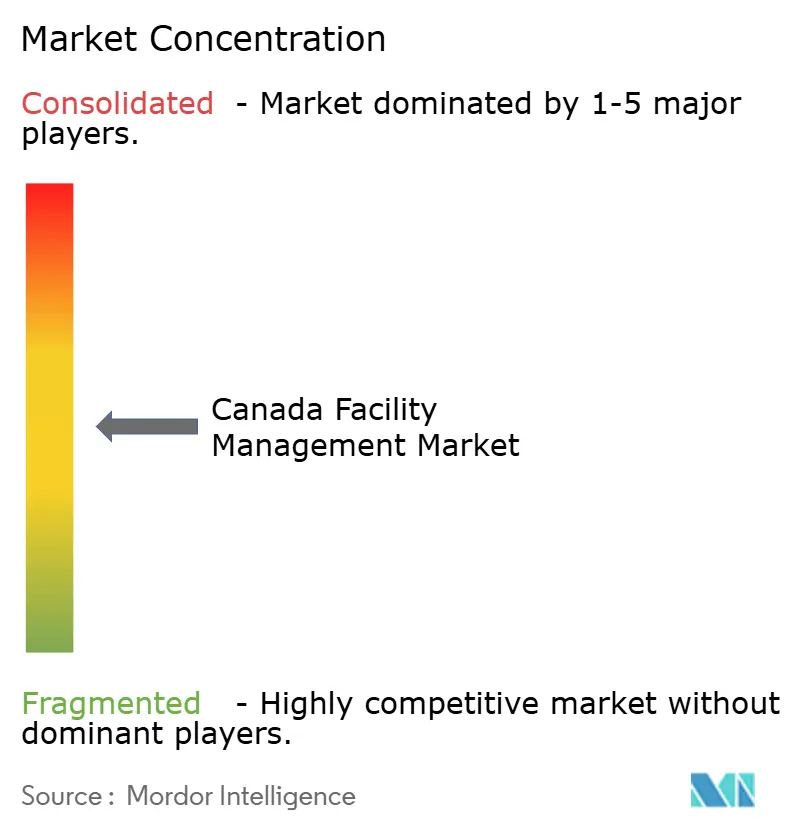

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Facility Management Market Analysis by Mordor Intelligence

The Canada facility management market size in 2026 is estimated at USD 55.59 billion, growing from 2025 value of USD 53.70 billion with 2031 projections showing USD 66.06 billion, growing at 3.52% CAGR over 2026-2031. Rapid digitalization, stricter energy-performance rules, and accelerated ESG reporting demands have changed spending priorities across the public and private sectors. Provincial code harmonization, led by the National Energy Code of Canada for Buildings (NECB) 2020, is forcing owners to retrofit HVAC, lighting, and envelope systems, thereby lifting demand for data-driven hard-service contracts. Providers are embedding IoT sensors, digital twins, and AI-based analytics to limit unplanned downtime and to assure compliance, especially in hospitals, data centers, and multi-tenant offices where business continuity is paramount. Persistent labor shortages and wage inflation have nudged building operators toward automated cleaning robots, sensor-guided security patrols, and remote monitoring centers. At the same time, the push to cut greenhouse-gas emissions has spurred outcome-based contracts that tie vendor fees to verified energy savings and carbon-reduction metrics, reinforcing the premium paid to integrated service partners with deep decarbonization credentials.

Key Report Takeaways

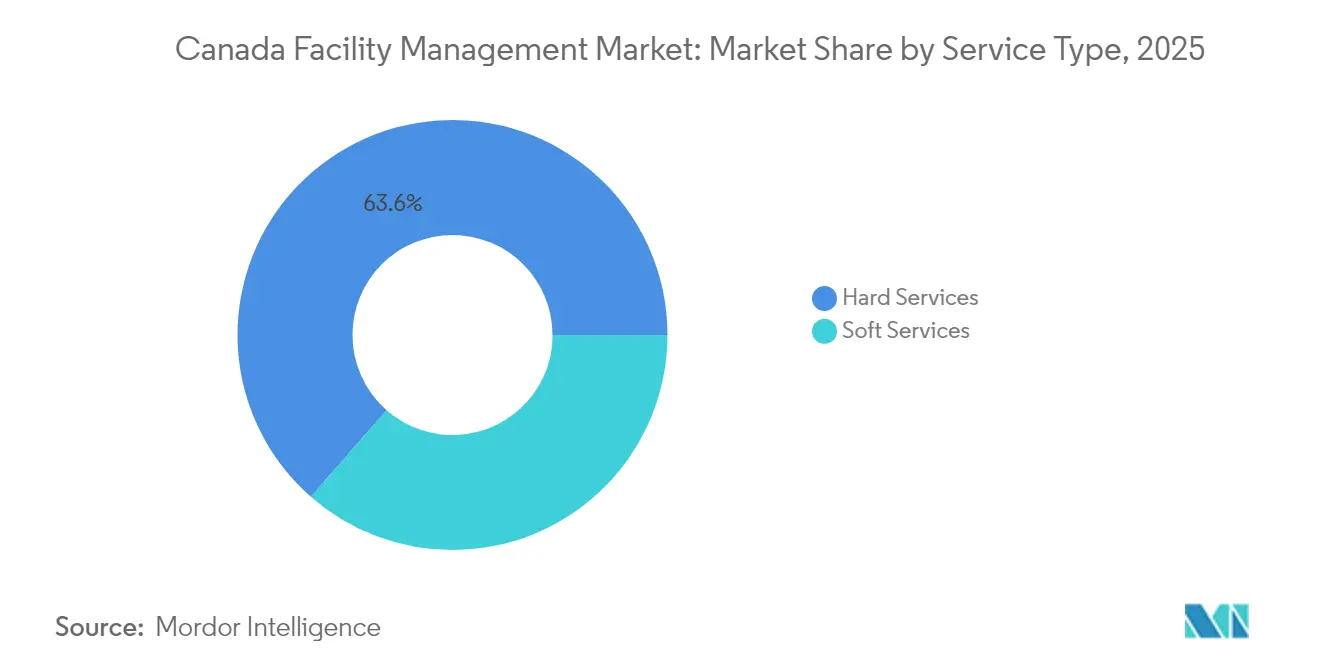

- By service type, Hard Services captured 63.55% of Canada's facility management market share in 2025, whereas Soft Services is forecast to expand at a 4.92% CAGR through 2031.

- By offering type, the In-house model controlled 53.10% of the Canada facility management market in 2025, while the Outsourced segment is projected to register the fastest 5.45% CAGR between 2026 and 2031.

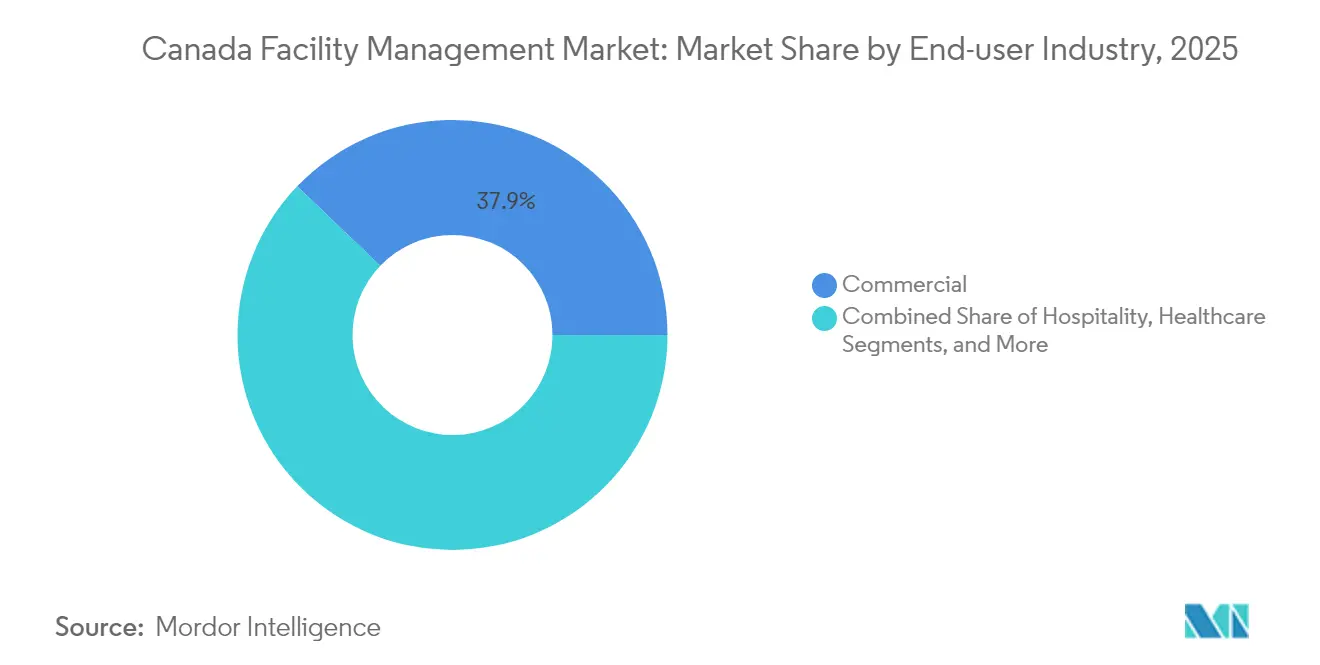

- By end user, the Commercial sector commanded 37.85% revenue in 2025, yet Institutional and Public Infrastructure is expected to deliver the highest 4.72% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Technological Integration Reshaping Service Delivery | +1.2% | National, with early gains in Ontario, Quebec, and British Columbia | Medium term (2-4 years) |

| ESG Compliance Driving Strategic Investments | +0.9% | National, with provincial variations in implementation | Long term (≥ 4 years) |

| Outsourcing Acceleration Reshaping Market Structure | +0.8% | National, concentrated in major metropolitan areas | Short term (≤ 2 years) |

| Rising Energy Costs Intensifying Efficiency Focus | +0.7% | National, with a higher impact in energy-intensive provinces | Medium term (2-4 years) |

| Mandatory Net-Zero Public Building Retrofit Programs | +0.6% | Federal and provincial government buildings nationwide | Long term (≥ 4 years) |

| Public–Private Partnership Lifecycle FM Niches | +0.5% | National, with a concentration in infrastructure-heavy provinces | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Technological Integration Reshaping Service Delivery

Hospitals, universities, and corporate campuses deployed IoT gateways, smart meters, and cloud-native computer-aided facility management software that streamlines work orders and anticipates component failures. The Canadian Agency for Drugs and Technologies in Health found that predictive algorithms shaved close to 50 hours of annual downtime from each CT and MRI scanner, thereby increasing imaging throughput and lowering overtime costs.[1]Canadian Agency for Drugs and Technologies in Health, “Predictive Maintenance for Medical Imaging Equipment,” cadth.ca Building information modeling files linked to live sensor feeds support digital twins that visualize energy flow, occupancy density, and air-quality shifts. Early adopters in Ontario and British Columbia bundled these dashboards into outcome-based agreements where fees hinge on verified uptime and energy intensity targets. Though semantic-data gaps still slow integration across platforms, vendors address the hurdle by adopting open middleware and by training technicians on data governance. Widespread rollouts are expected to continue as asset owners seek hard evidence of efficiency gains while battling wage inflation and shrinking maintenance budgets.

ESG Compliance Driving Strategic Investments

Federal authorities mandated every ministry to chart a path to net-zero operations by 2050 through the Greening Government Strategy, turning low-carbon facility upgrades from optional to essential. Commercial landlords mirrored public-sector action; several real-estate investment trusts plugged ESG data portals into building-management systems and reported 15–20% operating-cost cuts after LED installations and waste audits. NECB 2020 introduced four performance tiers that escalate from modest upgrades to Tier 4, which slices energy use 60% below baseline requirements. These targets accelerated demand for commissioning, air-leakage testing, and envelope insulation expertise. Investors screened facility management proposals for science-based carbon targets before awarding long-term contracts, prompting mid-sized providers to either reskill or risk exclusion. The resulting flight to quality is expected to lift contract values for providers that can measure, verify, and report sustainability metrics inside a single dashboard.

Outsourcing Acceleration Reshaping Market Structure

Boards facing capital constraints increasingly shifted in-house departments to outsourced integrated-FM packs that bundle HVAC, cleaning, landscaping, and security. The Public-Private Partnership (P3) Canada Fund deployed USD 1.3 billion across 25 large assets, illustrating the size of multi-decade lifecycle deals now on offer in transit, defense, and healthcare projects. ENGIE’s USD 1.9 billion concession to modernize Ottawa’s district-energy network until 2055 set a precedent for pay-for-performance clauses that guarantee 40% emissions cuts by 2030. Small and mid-cap property owners also adopted single-provider models to dodge compliance risk and to lock in predictable invoicing amid labor-market volatility. These shifts underpin the outsized 5.7% CAGR forecast for the Outsourced slice of the Canada facility management market.

Rising Energy Costs Intensifying Efficiency Focus

Electricity prices trended higher after 2024, especially in provinces using natural-gas peaker plants, while global fuel volatility increased interest in on-site micro-grids and advanced building controls. British Columbia’s Energy Step Code and Quebec’s mandatory consumption-reporting rules encouraged owners to install sub-metering, envelope-sealing, and smart-ventilation systems that limit wastage. Facility management firms capable of guaranteeing Tier-aligned performance won multi-property portfolios and leveraged resulting data to develop advisory spin-offs. Harmonization between provincial codes lowered duplication costs for national vendors and allowed them to scale standardized retro-commissioning toolkits. These offerings created a reliable revenue stream that counterbalanced cyclicality in basic janitorial and landscaping services.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Labor Shortages Escalate Wage Pressures and Automation Costs | -0.8% | National, with acute impact in Ontario and British Columbia | Short term (≤ 2 years) |

| Regulatory Compliance Complexity Increasing Operational Burden | -0.5% | National, with provincial variations in implementation | Medium term (2-4 years) |

| Aged Building Stock Raises Hazard Mitigation Costs | -0.4% | National, concentrated in older urban centers | Long term (≥ 4 years) |

| CAD–USD Exchange Volatility Elevates Imported Tech Expenses | -0.4% | National, affecting technology-intensive service providers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Labor Shortages Escalate Wage Pressures and Automation Costs

Statistics Canada reported that 28.3% of businesses cited recruiting challenges as their prime obstacle, while average hourly wages climbed 4.9% year-over-year in late 2024.[2]Statistics Canada, “Business Conditions Survey Q4 2024,” statcan.gc.ca New licensing rules in the Ontario condo segment shrank the eligible manager pool and pushed senior compensation as high as USD 220,000. Providers responded by adopting robotics for floor polishing, drone inspections for façades, and machine-vision security patrols, yet steep capital outlays reduced short-term margins. Amendments to the Canada Labour Code, effective June 2025, which bar replacement workers during strikes, further raised contingency costs for firms servicing critical infrastructure.

Regulatory Compliance Complexity Increasing Operational Burden

Each province maintains its own fire-safety, accessibility, and energy codes on top of federal statutes, forcing vendors to track dozens of inspection templates and record-keeping formats. Absence of standardized digital forms extends bid cycles and inflates administrative overhead. Compliance lapses invite heavy penalties, making multi-disciplinary code teams a competitive necessity. National players funnel resources into bilingual regulatory hubs in Montreal and safety-engineering centers in Calgary and Vancouver. Smaller firms either invest heavily in legal counsel and software or cede complex portfolios to larger rivals, reinforcing the gradual consolidation already visible in the Canada facility management market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Essential Hard Services Sustain Dominance While Soft Services Accelerate

Hard Services generated 63.55% of revenue in 2025, underscoring the continued primacy of mechanical, electrical, and plumbing maintenance in the Canada facility management market. NECB 2020 raised minimum efficiency thresholds for boilers, chillers, and building envelopes, compelling owners to prioritize capital for HVAC upgrades and fire-system inspections. Asset managers at hospitals and data centers adopted predictive analytics to trim emergency call-outs, strengthening margins for vendors able to guarantee uptime. Aging public-hospital campuses with equipment older than a decade sought retrofit packages that linked vibration-monitoring sensors to centralized dashboards, widening the addressable market for condition-based maintenance specialists.

Soft Services, while representing a smaller base, posted a 4.92% CAGR and is poised to capture a larger slice of the Canada facility management market as organizations embrace hybrid work. Employers revamped cleaning protocols to emphasize disinfection and indoor-air-quality testing, actions that justify higher service premiums. Security providers deployed AI-enabled cameras and analytics to offset guard shortages, and office-support teams integrated desk-booking software that recalibrates space usage. Catering operators pivoted toward modular kitchens and digital ordering to reduce waste on low-occupancy days. Altogether, Soft Services are expected to pull sustained contract renewals, allowing vendors to cross-sell wellness and sustainability add-ons.

By Offering Type: Outsourcing, Momentum, Challenges, Legacy In-house Models

The In-house model retained 53.10% of 2025 spending, driven by legacy arrangements within government agencies and large financial campuses. Persistent labor shortages and rising benefit costs, however, spurred many owners to test external providers. The Outsourced slice of the Canada facility management market is projected to post a 5.45% CAGR as integrated FM contracts replace piecemeal task orders. Bundled FM deals deliver economies of scale and reduce vendor-management overhead, while lifecycle contracts on P3 infrastructure offer decades-long cash-flow visibility. Single-service outsourcing remains relevant for smaller portfolios seeking proof of concept before committing to integrated models. Technology-rich providers, able to consolidate energy dashboards, work orders, and compliance logs into a single platform, command premium fees and enjoy higher renewal rates.

By End-user Industry: Institutional and Public Infrastructure Leads Growth Curve

Commercial landlords held 37.85% of 2025 revenue, buoyed by dense office and logistics footprints in Toronto and Vancouver. Lease renewals often specify smart-building credentials and wellness ratings, generating incremental demand for air-quality sensors and tenant-experience platforms. Yet, Institutional and Public Infrastructure properties are forecast to deliver the fastest 4.72% CAGR through 2031, supported by federal hospital, courthouse, and public transit investments. Predictive maintenance reduced downtime on surgical suites, while energy-performance contracts funded LED retrofits without upfront expenditure. University campuses overhauled dormitories to meet updated accessibility and energy codes, and transit authorities bundled snow clearing, lift maintenance, and passenger information systems into integrated FM tenders. Industrial plants, especially in Alberta’s petrochemical triangle, pursued carbon-capture retrofits and safety audits, offering cyclical but high-value contracts. Canada Hospitality portfolios rebounded on revived travel volumes, with owners focusing on guest-experience analytics and back-of-house automation to ease labor shortages.

Geography Analysis

Ontario remained the single largest provincial market thanks to its diversified economy and dense outlook of commercial real estate, government bureaus, and healthcare facilities. The Greater Toronto Area and Ottawa corridor accounted for a substantial share of contracts, yet acute technician shortages pushed wages and overtime bills upward. FM providers mitigated delays by clustering mobile hubs near mass-transit lines, introducing app-based dispatch, and collaborating with polytechnics on apprenticeships. Provincial subsidies for electric-heat-pump retrofits and hospital expansion drive sustained capital inflows into compliance testing, commissioning, and predictive maintenance.

Quebec ranked second but presented distinct linguistic and regulatory hurdles. The Environmental Performance Act obliges energy-use disclosures, stimulating uptake of advanced metering and data-aggregation platforms. Hydroelectric abundance afforded lower electricity tariffs, shifting owner attention to water conservation, indoor-air quality, and waste minimization. Bilingual service capacity became a tender prerequisite in Montreal and Quebec City, so homegrown providers with French digital portals established an edge. These local advantages limited outside competition, although partnerships between national chains and regional specialists are emerging to secure province-wide frameworks.

Alberta’s spending trajectory swings with commodity cycles, yet large carbon-capture pilots and petrochemical projects underpin long-run facility-service needs. FM providers certified in process safety and heavy-machinery maintenance won multi-year service agreements for CO₂ compression stations and pipeline hubs. Downtown Calgary’s office towers adopted flexible lease structures, thus demanding space-planning software and dynamic cleaning schedules. British Columbia rounded out the top four provinces; the Energy Step Code and seismic-resilience requirements created a robust pipeline for envelope retrofits, structural monitoring, and emergency-readiness training. National players deployed cloud-native analytics across disparate regional portfolios, providing consistent reporting and centralized account management while respecting province-specific code nuances.

Competitive Landscape

The Canada facility management market remained moderately fragmented in 2025 as incumbent multinationals shared space with agile mid-cap specialists. Consolidation persisted; major players targeted bolt-on acquisitions that add geographic density and deep vertical know-how. GDI Integrated Facility Services divested its high-voltage utility arm to refocus on bundled FM contracts with predictable recurring revenue. BGIS, under private-equity stewardship, emphasized datacenter and defense portfolios, building on a footprint covering 320 million square feet globally.[4]Brookfield Business Partners, “Sale of BGIS to CCMP Capital,” bbu.brookfield.com

Technology differentiation intensified. Leading firms funneled capital into cloud CMMS suites, sensor networks, and machine-learning maintenance engines that anticipate part failure and optimize technician routes. These platforms unify energy, water, and waste streams, thereby easing ESG reporting compliance and bolstering client retention. Strategic alliances with prop-tech startups allowed rapid deployment of retro-commissioning tools and augmented-reality work instructions for field staff, shortening diagnostic times and sharpening competitive bids.

Sector attractiveness for private equity remained strong due to inflation-indexed fees and high renewal rates. ISS and Sodexo tapped bond markets for growth capital, signaling lender confidence in cash-flow resilience. Mid-sized players defended niches in laboratory clean rooms, high-rise window care, and military grounds maintenance, while forming joint bids to contest mega-contracts. The top five providers controlled about 45% of national revenue, suggesting room for further roll-ups and technology-centric integration.

Canada Facility Management Industry Leaders

ION Facility Services Inc.

Black & McDonald

Avison Young (Canada) Inc.

Veolia Services Canada Inc.

Brookfield Global Integrated Solutions Canada LP (BGIS)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Sodexo trimmed its FY 2025 growth outlook to 3–4% amid slower North American expansion, especially in education and healthcare.

- January 2025: Badger Infrastructure Solutions Ltd. posted a 7% revenue gain to USD 172.6 million for Q1 2025 and announced a planned 4–7% hydrovac-fleet expansion.

- December 2024: GDI Integrated Facility Services Inc. sold its Ainsworth Power Construction unit to Tristar Electrical Inc., a subsidiary of Aecon Utilities Group Inc., so that it could concentrate on core integrated-FM offerings.

- September 2024: Public Services and Procurement Canada awarded a USD 2 billion Leopard 2 tank sustainment contract to KNDS Deutschland GmbH and Co. KG, establishing a regional maintenance centre in Alberta and creating 295 positions.

Canada Facility Management Market Report Scope

The study tracks the facility management (FM) industry trends in Canada, and the market estimations are arrived at by analyzing the revenues accrued by the service providers. The core objective is to analyze the scope for in-house and outsourced FM.The market estimates and projections are for both the segments and have been arrived at considering the impact of covid on the current estimate as well the future projections.

The Canada facility management market is segmented by service type (hard services [asset management, MEP and HVAC services, fire systems and safety, and other hard FM services] and soft services [office support and security, cleaning services, catering services, and other soft FM services]), offering type (in-house and outsourced [single FM, bundled FM, and integrated FM]), and by end-user (commercial, hospitality, institutional & public infrastructure, healthcare, industrial & process sector, and others). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

By Offering Type

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

By End-user Industry

| Commercial (IT and Telecom, Retail and Warehouses, etc.) |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) |

| Institutional and Public Infrastructure (Govt, Education, Transportation) |

| Healthcare (Public and Private Facilities) |

| Industrial and Process (Manufacturing, Energy, Mining) |

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

| By Offering Type | In-house | |

| Outsourced | Single FM | |

| Bundled FM | ||

| Integrated FM | ||

| By End-user Industry | Commercial (IT and Telecom, Retail and Warehouses, etc.) | |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) | ||

| Institutional and Public Infrastructure (Govt, Education, Transportation) | ||

| Healthcare (Public and Private Facilities) | ||

| Industrial and Process (Manufacturing, Energy, Mining) | ||

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) | ||

Key Questions Answered in the Report

What is the current value of the Canada facility management market?

The market was valued at USD 55.59 billion in 2026.

How fast will the Canada facility management market grow by 2031?

It is projected to expand at a 3.52% CAGR, reaching USD 66.06 billion.

Which service category dominates spending?

Hard Services led with 63.55% of market revenue in 2025.

Why is outsourcing gaining popularity?

Owners pursue outsourced integrated contracts to access specialized skills, cut compliance risk, and offset labor shortages, supporting a 5.45% CAGR for the segment.

Which end-user group will grow the fastest?

Institutional and Public Infrastructure buildings are forecast to log the highest 4.72% CAGR through 2031, powered by hospital and transit upgrades.

How are ESG regulations influencing vendor selection?

Federal net-zero mandates and NECB 2020 energy tiers require measurable emissions cuts, so clients favor facility managers who provide data-verified sustainability reporting within one platform.

Page last updated on: