Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

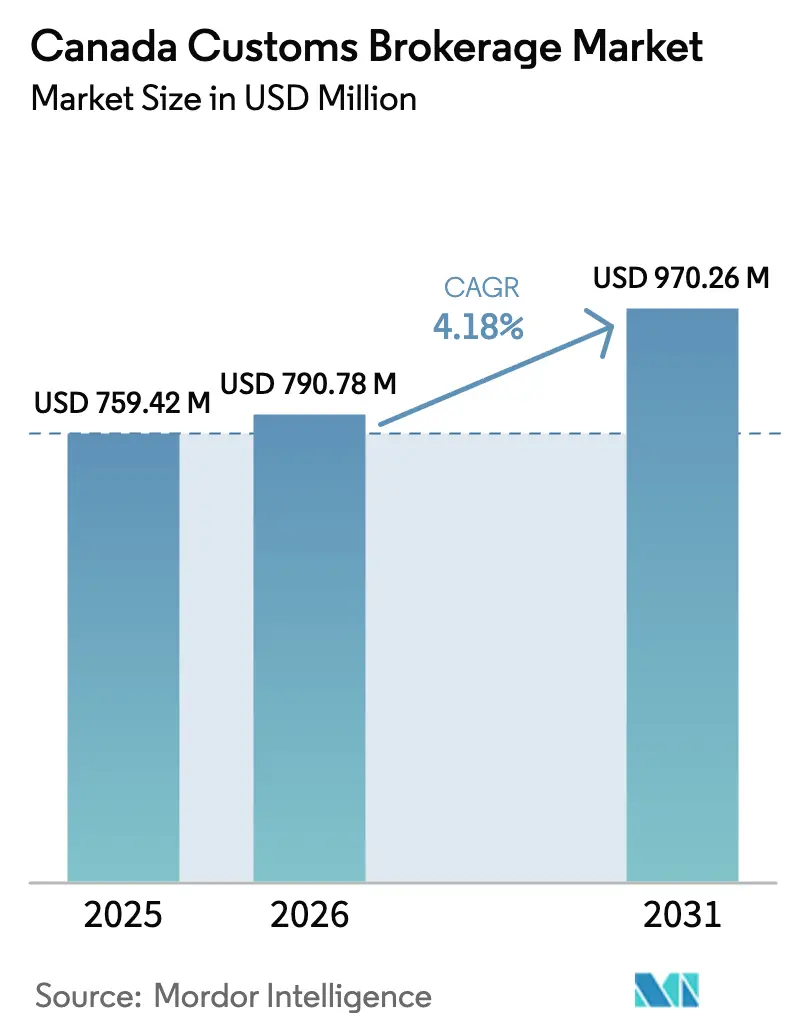

| Base Year Market Size (2025) | USD 759.42 Million |

| Market Size (2026) | USD 790.78 Million |

| Market Size (2031) | USD 970.26 Million |

| Growth Rate (2026 - 2031) | 4.18% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Customs Brokerage Market Analysis by Mordor Intelligence

The Canada Customs Brokerage Market size is estimated at USD 790.78 million in 2026, and is expected to reach USD 970.26 million by 2031, at a CAGR of 4.18% during the forecast period (2026-2031).

Parcel-driven complexity sustained cross-border consumer demand, and CUSMA-linked rules-of-origin verification elevate the competitive stakes across this growing field. Provincial gateway investments, technology-enabled service differentiation, and the steady shift of North American supply chains toward near-shoring collectively expand addressable revenue pools for brokers that can master small-package clearance while still supporting bulk freight. Integrated logistics operators pull incremental volume through bundled offerings, yet specialty providers win premium fees where origin validation, sanctions screening, or sector-specific licensing raise compliance risks. As CARM finalization nears, automation, API connectivity, and cybersecurity readiness further distinguish winners inside the Canada customs brokerage market.

Key Report Takeaways

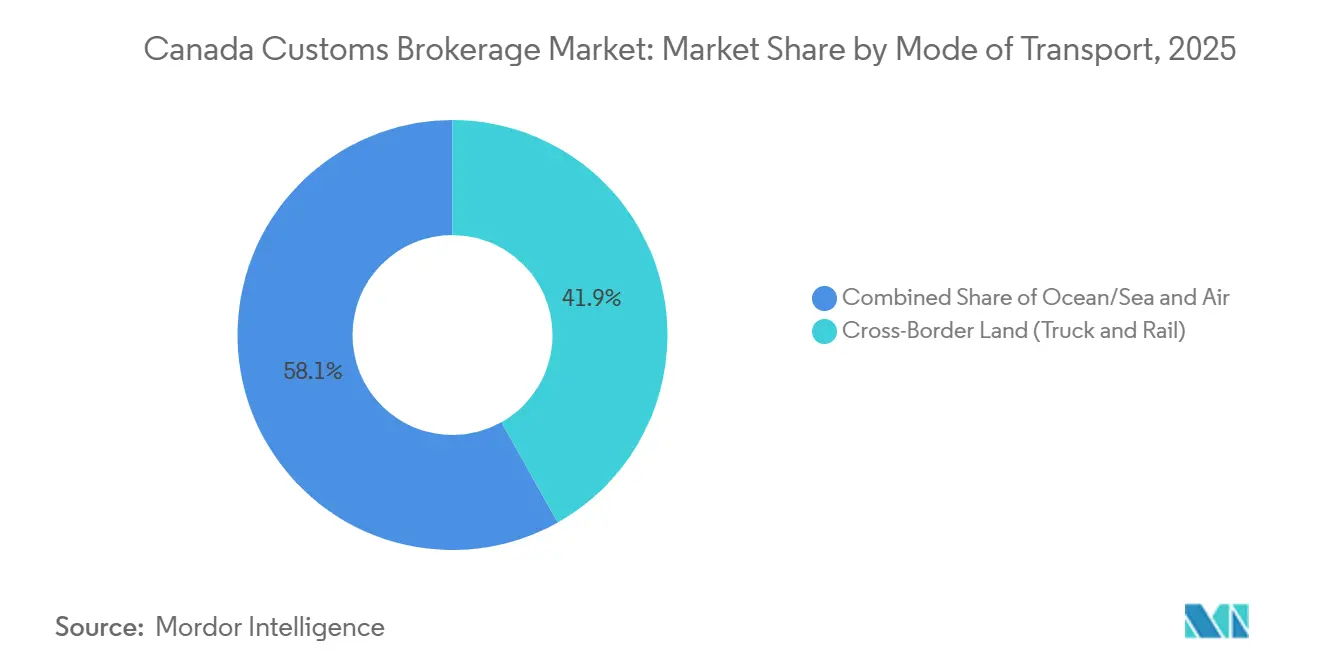

- By mode of transport, cross-border land transport (truck and rail) held 41.86% of the Canada customs brokerage market share in 2025, while air cargo is forecast to register the highest 4.39% CAGR through 2031.

- By broker type, freight-forwarder and 3PL-integrated operators controlled 51.24% of the Canada customs brokerage market size in 2025, whereas pure customs brokers will capture the fastest 4.57% CAGR to 2031.

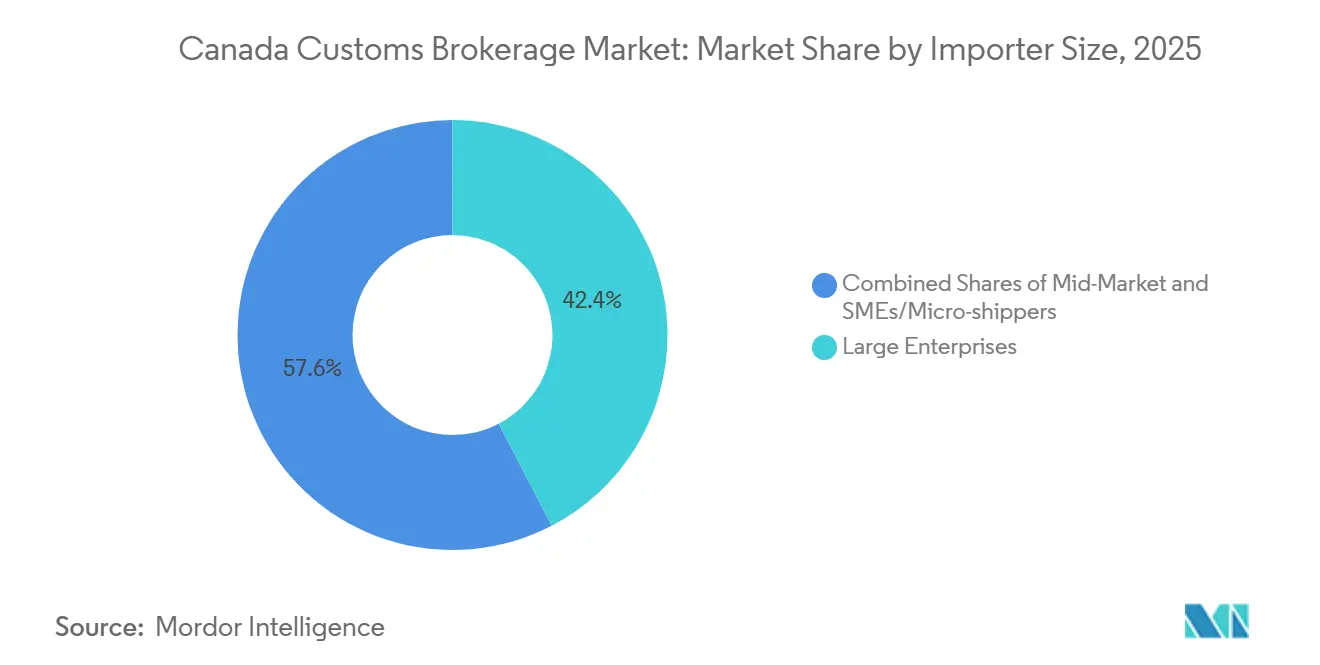

- By importer size, SMEs and micro-shippers advanced at a 4.88% CAGR between 2026-2031; large enterprises retained 42.36% market share in 2025.

- By digital adoption, traditional brokerages accounted for 57.83% of the Canada customs brokerage market size in 2025, yet digital-first providers are expanding at a 4.71% CAGR through 2031.

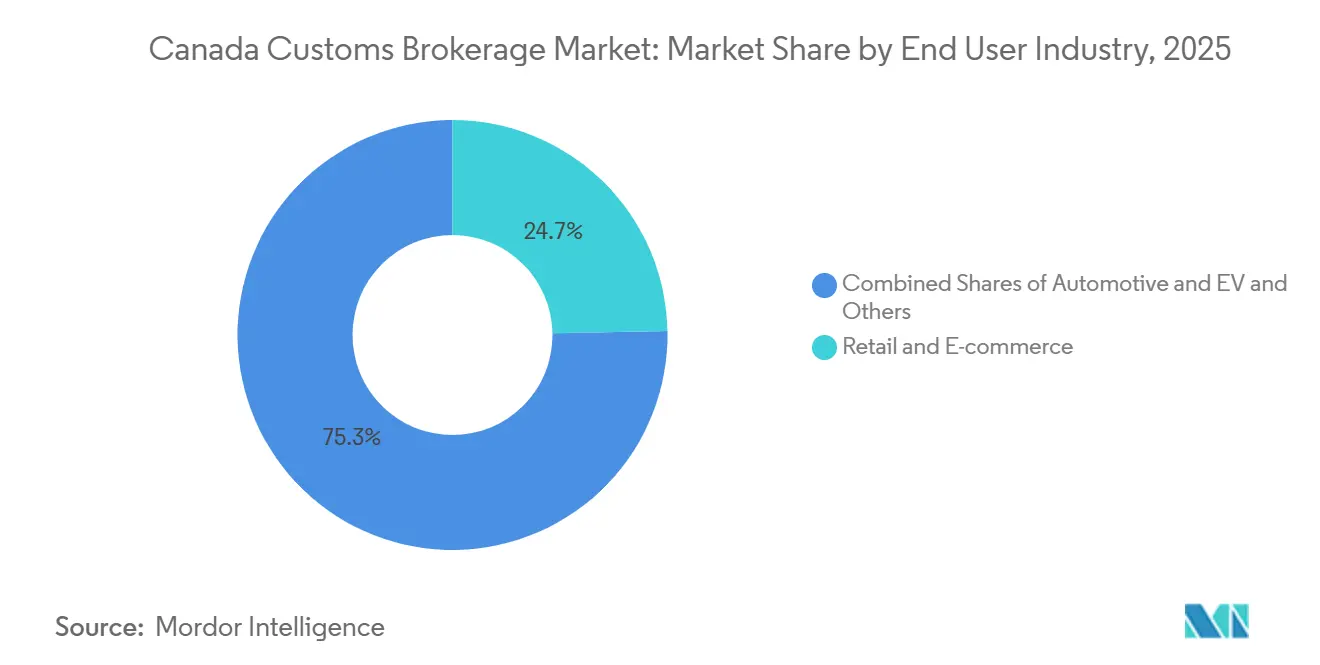

- By end-use industry, retail and e-commerce led with 24.71% share in 2025, while the automotive and EV sector is progressing at a 4.62% CAGR to 2031.

- By province, Ontario commanded 31.24% revenue share in 2025, whereas British Columbia is poised to post a 4.94% CAGR through 2031, the fastest among all provinces.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Canada Customs Brokerage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging cross-border e-commerce parcel volumes | +1.1% | National, most intense in urban fulfillment zones | Short term (≤ 2 years) |

| CUSMA-driven bilateral trade expansion | +0.9% | Ontario, Québec, border-adjacent manufacturing corridors | Medium term (2-4 years) |

| Near-shoring of North American supply chains | +0.7% | Ontario, Québec, core industrial gateways | Long term (≥ 4 years) |

| Proliferation of trade agreements and sanctions | +0.5% | National, high impact on Asia-Pacific corridors | Medium term (2-4 years) |

| AI-enabled HS-code prediction tools | +0.3% | National, technology-forward broker operations | Medium term (2-4 years) |

| Indigenous and Northern supply-chain support | +0.2% | Northern territories, remote Indigenous communities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Cross-Border E-commerce Parcel Volumes

Canada Post processed more than 1 billion parcels during 2025, a record that underscores how direct-to-consumer imports dominate incremental customs declarations[1]Canada Post, “Canada Post Delivers Record Volumes,” canadapost-postescanada.ca. Rapid-fire order cycles and low shipment values force brokers to automate entry generation, harmonized-code allocation, and duty calculation so that parcels clear without jeopardizing promised delivery times. Service portfolios increasingly feature de minimis optimization, allowing retailers to batch shipments below CAD 40 (USD 29) duty thresholds while still meeting regulatory requirements. Distributed gateway routing also gains importance because small packages now arrive simultaneously at Vancouver, Toronto, and Montréal facilities instead of funneling through a single port. Scalability, therefore, turns on cloud-based clearance engines, API connectivity with shopping-cart platforms, and 24/7 remote workforce coverage, all of which become must-have capabilities for contenders inside the Canada customs brokerage market.

CUSMA-Driven Bilateral Trade Growth

Merchandise trade between Canada and the United States totaled USD 745.4 billion in 2025, equal to 75.9% of Canadian exports. CUSMA’s tiered regional-value and labor-value thresholds obligate importers to prove qualifying content across multilayered supplier networks, especially in vehicles, textiles, and agri-foods. Brokers, therefore, pivot from transactional entry filing toward advisory mandates such as supplier document retrieval, costed bill-of-materials tracking, and audit defense preparation. Automotive producers also lean on brokers to certify that 40-45% of vehicle value originates from high-wage facilities, a stipulation that amplifies wage-rate verification complexity. This compliance burden guarantees durable demand, solidifying the Canada customs brokerage market as a strategic partner for manufacturers restructuring under regional sourcing rules.

Boom in Near-Shoring of North American Supply Chains

Manufacturers rebalance production footprints to shorten lead times and hedge geopolitical risk, redirecting component flows from Asia toward Canada and Mexico. Temporary-import permit advice, bonded-warehouse program design, and drawback claim management become lucrative fee generators because near-shored inventories circulate repeatedly across borders. Ontario and Quebec plants now schedule just-in-time deliveries that rely on paper-thin dwell times at ports of entry, necessitating robust broker backstops against classification missteps or system downtime. Brokers that can bundle landed-cost modeling with customs compliance increasingly influence footprint selection decisions, reinforcing their consultancy role within the Canada customs brokerage industry.

Proliferation of Trade Agreements & Sanctions

Canada currently participates in 15 free-trade agreements covering 51 countries, while also enforcing Russia-related sanctions regimes that continue to expand listing scopes[2]Office of the Chief Economist, “Canada’s State of Trade 2024,” international.gc.ca Importers struggle to reconcile divergent origin rules, duty drawback entitlements, and prohibited-party screenings without specialist guidance. Forward-leaning brokers, therefore, license multimarket tariff engines and integrate real-time restricted-party databases to deliver rapid duty-savings insights alongside sanctions compliance assurance. Those dual capabilities differentiate providers and sustain pricing power, particularly for Asia-bound consumer brands and extractive-sector suppliers navigating embargo-sensitive materials.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Freight-forwarder vertical integration | -0.7% | National, mid-market client segment | Medium term (2-4 years) |

| CBSA self-assessment bypassing brokers | -0.5% | National, concentrated among large importers | Short term (≤ 2 years) |

| Licensed-broker talent shortage | -0.4% | National, acute in Montréal, Toronto, Vancouver | Long term (≥ 4 years) |

| Cybersecurity and data-privacy compliance cost | -0.3% | National, all brokers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Freight-Forwarder Vertical Integration

Purolator’s CAD 1.2 billion (USD 869 million) purchase of Livingston in 2024 gave the courier giant instant access to Canada’s largest broker workforce, creating an end-to-end platform that smaller specialists cannot match[3]Statistics Canada, “The Daily — Canadian International Merchandise Trade, December 2024,” statcan.gc.ca. Similar acquisitions by Kuehne + Nagel and Atlas Canada intensify scale-driven pricing pressure because bundled logistics contracts often embed customs clearance at marginal cost. Mid-tier brokers counter by highlighting independence from carrier-related service disruptions and by deepening sector-specific regulatory mastery. Nevertheless, integrated competitors siphon routine parcel entries from the Canada customs brokerage market, shrinking the addressable base for pure brokers.

CBSA Self-Assessment Bypassing Brokers

Programs such as Partners in Protection allow low-risk importers to file entries directly, curtailing broker fee opportunities on predictable SKUs. Multinationals with trade-compliance departments embrace self-assessment to trim transaction costs, yet most small and mid-sized importers still outsource liability to brokers rather than maintain in-house classification expertise. The net impact, therefore, lowers growth velocity in the short term but does not erase the need for professional intermediaries across the Canada customs brokerage market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Transport: E-Commerce Elevates Air Cargo Yet Trucking Still Dominates

The air-cargo slice of the Canada customs brokerage market size is slated to post a 4.39% CAGR to 2031, buoyed by pharmaceutical cold-chain consignments and cross-border parcels that prize speed over freight cost. Brokers clearing airfreight deploy 24-hour desks at Toronto Pearson and Vancouver International to prevent storage penalties and service-level failures. Cross-border land transport (truck and rail) continues to account for 41.86% of 2025 revenue, anchored by automotive and industrial supply chains that rely on same-day border crossings to sustain just-in-time production

Ocean gateways, notably Vancouver and Montréal, cultivate containerized consumer-goods flows where customs specialists mitigate demurrage risk by pre-lodging entries before vessel arrival. Rail-intermodal movements tie West Coast arrivals to Prairie and Central Canadian distribution centers, necessitating close broker-carrier collaboration to match customs release windows with train schedules. Each leg demands differentiated clearance competencies, ensuring that modal diversity remains a defining feature of the Canada customs brokerage market.

By Broker Type: Specialist Expertise Reverses Consolidation Patterns

Freight-forwarder and 3PL-integrated players captured 51.24% market share in 2025, leveraging network density and bundled contracts to secure high-volume parcels and palletized freight. Yet pure players are on track for a 4.57% CAGR, proving that granular HS-code mastery, audit defense, and sector-specific advisory commands premium pricing.

Clients handling batteries, biologics, or aerospace components increasingly separate brokerage from transport to safeguard regulatory oversight, choosing boutique firms that embed compliance officers in client ERP workflows. Meanwhile, integrated giants funnel resources into AI tools and customer portals to narrow the expertise gap, sustaining a two-track competitive landscape inside the Canada customs brokerage market.

By Importer Size: Digital Platforms Democratize Clearance for SMEs

SMEs and micro-shippers will outpace other importer tiers at a 4.88% CAGR through 2031 as self-service booking engines simplify access to cross-border trade. Transparent fee tables, instant landed-cost quotes, and chatbot support allow micro-brands to test foreign sourcing with minimal working capital.

Large enterprises still represent 42.36% of 2025 revenue because their high transaction counts and audit exposure require bespoke compliance dashboards, drawback optimization, and dedicated account teams. Mid-market firms gravitate toward hybrid models, routing low-risk SKUs through online portals while engaging full-service brokers whenever regulatory ambiguity emerges, sustaining diversified demand across the Canada customs brokerage market.

By Digital Adoption: Technology Enhances but Does Not Replace Human Judgment

Traditional firms retained 57.83% of 2025 revenue, underscoring the enduring importance of relationship-based service for classification disputes and valuation negotiations. Nevertheless, API-centric brokerages are advancing at a 4.71% CAGR because instant status updates, rules-based entry generation, and integrated payments resonate with e-commerce-weighted clients.

Incumbents respond by layering robotic process automation onto legacy systems, freeing licensed staff to tackle complex rulings while lowering per-entry costs. The convergence points to a future where human expertise and machine efficiency cohabit rather than compete inside the Canada customs brokerage market.

By End-Use Industry: Automotive Electrification Multiplies Compliance Touchpoints

Retail and e-commerce claimed 24.71% of 2025 revenue thanks to diversified SKU catalogs that drive continuous parcel inflows. In contrast, the automotive and EV value chain is primed for a 4.62% CAGR because battery-content origin tracing and critical-mineral sourcing audits require specialized documentation roadmaps.

Pharmaceutical importers lean on brokers licensed for Health Canada drug establishment activities, while aerospace clients demand controlled-goods program knowledge and ITAR vetting. Electronics traders battle anti-dumping exposure on certain semiconductor categories, turning to brokers for early warning and duty mitigation. This breadth of sector needs to cement multidomain expertise as an engine of differentiation across the Canada customs brokerage market.

By Province: British Columbia Accelerates on Trans-Pacific Momentum

Ontario preserved 31.24% of 2025 turnover on the back of manufacturing density and three high-throughput border bridges. Nonetheless, British Columbia is forecast to register a 4.94% CAGR through 2031, propelled by Vancouver’s 4.1 million-TEU container throughput and expanding Asia-Pacific consumer-goods pipelines.

Quebec combines aerospace exports and EU-linked consumer-goods imports to keep Montréal brokers busy, while Alberta leverages energy-equipment demand around Calgary’s freight village. Collectively, these regional dynamics reinforce the geographic breadth that characterizes the Canada customs brokerage market.

Geography Analysis

Ontario’s leadership rests on dense auto, consumer-goods, and industrial corridors that generate around-the-clock clearance volumes, forcing brokers to synchronize shift schedules with Detroit-Windsor and Buffalo-Fort Erie crossing windows. Toronto Pearson’s belly-freight influx adds further workload, especially for pharmaceutical and electronics SKUs requiring temperature-controlled or high-value custodial protocols. Ontario brokers also pilot early CARM integrations because pilot importers cluster inside the province’s corporate headquarters belt.

British Columbia’s growth trajectory hinges on continuous berth expansions and inland-rail capacity upgrades that ferry Asia-sourced merchandise to Prairie provinces. Brokers in Vancouver fine-tune processes for high-volume containers, leveraging pre-arrival entry filing to minimize dwell fees and integrating AES data exchanges for U.S. in-transit shipments. Provincial e-commerce hubs near Richmond and Surrey magnify small-package traffic, making parcel automation investments imperative.

Quebec occupies a strategic midpoint between Europe and North America, with Montréal focusing on aerospace-component imports and aluminum-sector raw materials. Bilingual document services bolster competitiveness, while tightened EU carbon-border-adjustment mechanisms drive new advisory revenue. Alberta, Saskatchewan, and Atlantic provinces jointly represent emerging arenas for project cargo and energy-equipment clearance, encouraging brokers to widen office footprints beyond the core Golden Horseshoe and Pacific Rim gateway cities[4]Source: Vancouver Fraser Port Authority, “Port of Vancouver Statistics,” portvancouver.com.

Competitive Landscape

The Canada customs brokerage market balances concentration at the top with vibrant long-tail specialization. Purolator-Livingston now blends the nation’s biggest courier network with the largest brokerage payroll, granting a uniquely integrated value proposition that scales from parcel to project cargo. C.H. Robinson, Kuehne + Nagel, and DSV follow similar playbooks, expanding Canadian footprints via acquisitions or facility builds to surround clients with multimodal options.

Specialist independents such as Cole International, Argo Customs, and Jori Logistics protect niches via AI-driven classification dashboards, controlled-goods accreditations, and Northern-logistics credentials. API-native entrants like BorderBuddy lure start-ups by advertising all-in USD rates and five-minute account sign-ups, although complex entries frequently revert to human review. Cybersecurity has become a front-line differentiator, with ISO 27001 certification featuring prominently in RFP responses after multiple ransomware events hit mid-sized brokers in 2025.

Technology investment races escalate: Livingston’s predictive HS-code engine, C.H. Robinson’s consolidation algorithm, and FedEx Trade Networks’ penalty-avoidance analytics all illustrate how software budgets now rival brick-and-mortar expansions. Yet relationship equity still matters; seasoned account managers guide clients through CBSA audit remedies, CARM cutovers, and tariff-reclassification appeals, cementing loyalty even as platforms proliferate. This twin focus on high-touch counsel and digitized execution keeps competitive intensity elevated across the Canada customs brokerage market.

Canada Customs Brokerage Industry Leaders

Livingston International

Kuehne + Nagel

UPS Supply Chain Solutions

FedEx Trade Networks

DHL

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Livingston International launched a real-time CARM duty-management dashboard that aggregates transaction histories and shows live security deposit balances for importer of record numbers.

- November 2025: Purolator opened expanded customs hubs in Toronto and Vancouver, enabling 24/7 CARM-compliant processing for express and freight traffic.

- October 2025: GEODIS doubled Calgary floor space to support energy-sector customs and project-cargo warehousing.

- September 2025: C.H. Robinson unveiled an AI-optimized cross-border consolidation service promising transport-plus-brokerage cost savings up to 40%.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the Canada customs brokerage market as the fee-based services delivered by CBSA-licensed brokerages that classify goods, calculate duties and taxes, submit electronic declarations, and liaise with border officers for all commercial import shipments moving by ocean, air, truck, or rail.

Scope exclusion: courier "section 321" low-value shipments cleared directly by express integrators are outside the sizing.

Segmentation Overview

- By Mode of Transport

- Ocean / Sea

- Air (Express and General Cargo)

- Cross-Border Land (Truck and Rail)

- By Broker Type

- Pure Customs Broker

- Freight Forwarder / 3PL-Integrated Brokers

- By Importer Size

- Large Enterprisess

- Mid-Market

- SMEs / Micro-shippers

- By Digital Adoption

- Traditional Brokerages

- Digital-first / API-based Brokerages

- By End-User Industry

- Retail and E-commerce

- Automotive and EV

- Electronics and Semiconductors

- Pharmaceuticals and Life Sciences

- Aerospace and Defense

- Chemicals and Industrial Goods

- Others

- By Province

- Ontario

- Quebec

- British Columbia

- Alberta

- Others

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed veteran compliance managers at automotive OEMs, trade lawyers in Ontario, and executives at mid-market brokerages across British Columbia and Quebec. The conversations validated fee dispersion, CARM readiness costs, and importer switching trends that desk research could not quantify.

Desk Research

We began by mapping Canada's import transaction universe through open data from the Canada Border Services Agency, Statistics Canada customs trade tables, and Transport Canada modal throughput records. Additional insight was gathered from the Canadian Society of Customs Brokers, WTO tariff files, and parliamentary budget briefs that quantify duty revenues. Company 10-Ks and investor decks supplied average brokerage fee yields, whereas news flows mined via Dow Jones Factiva helped us track merger activity and digital platform launches. This list illustrates our evidence base only; numerous other public and paid references aided data checks.

Secondary sources establish volume and rate corridors, yet they rarely split revenues by broker type or importer cohort, which is why primary outreach is vital.

Market-Sizing & Forecasting

A top-down reconstruction starts with CBSA shipment counts by mode, then multiplies them by verified average clearance fees for large, mid-market, and SME importers. Results are corroborated with selective bottom-up roll-ups of revenues disclosed by listed brokers and private filings shared in confidence. Variables such as cross-border truck clearance growth, e-commerce parcel imports, average duty rates, CARM compliance uptake, and GDP-linked trade elasticity feed an ARIMA forecast, which is stress-tested against three macro scenarios. Gaps in private broker revenues are bridged with fee-per-entry benchmarks and importer surveys before totals are finalized.

Data Validation & Update Cycle

Outputs pass a three-layer analyst review; variance against historical duty collections is flagged, and anomalies trigger call-backs to interviewees. The model refreshes each year, while material events like CARM phase shifts prompt interim revisions, ensuring clients always receive a current baseline.

Why Our Canada Customs Brokerage Baseline Commands Reliability

Published market figures often vary because firms choose divergent scopes, duty-calculation assumptions, and refresh cadences. Key gap drivers here include whether courier low-value entries are counted, how digital-only brokers are classified, and the currency-conversion date applied. Our disciplined scope alignment, variable transparency, and yearly refresh make Mordor's number the dependable starting point for planning.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 759 M (2025) | Mordor Intelligence | - |

| USD 730 M (2024) | Regional Consultancy A | Excludes rail clearances and applies uniform fee rate |

| CAD 2.5 B (2023) | Trade Journal B | Includes courier low-value shipments and uses gross duty value, inflating total |

Differences seen above stem mainly from scope breadth and fee assumptions; by anchoring estimates to verifiable shipment counts and broker-disclosed fees, Mordor Intelligence delivers a balanced, transparent baseline that users can retrace with confidence.

Key Questions Answered in the Report

What CAGR is forecast for the Canada customs brokerage market through 2031?

The field is projected to expand at a steady 4.18% CAGR, climbing from USD 790.78 million in 2026 to USD 970.26 million by 2031.

Which transport mode is growing fastest for cross-border customs entries?

Air cargo leads with a 4.39% CAGR because e-commerce parcels and cold-chain pharmaceuticals prioritize speed in clearance decisions.

Why are pure customs brokers regaining share despite freight-forwarder consolidation?

Importers facing complex origin verification and sanctions rules pay premium fees for deep compliance expertise that integrated logistics firms often lack.

How does CUSMA affect customs brokerage demand in Canada?

Rigorous regional-value content rules across automotive, textile, and agri-food sectors compel manufacturers to seek brokers for continuous documentation management and audit defense.

Which province shows the quickest brokerage-revenue growth?

British Columbia is forecast to advance at a 4.94% CAGR on the back of rising Asia-Pacific container volumes moving through the Port of Vancouver.

What technology investments matter most for brokers during the CARM transition?

API-driven duty-payment interfaces, AI-powered HS-code prediction, and ISO-aligned cybersecurity controls are becoming decisive selection criteria for importers.

Page last updated on: